Learning Management System (LMS) In Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 10.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

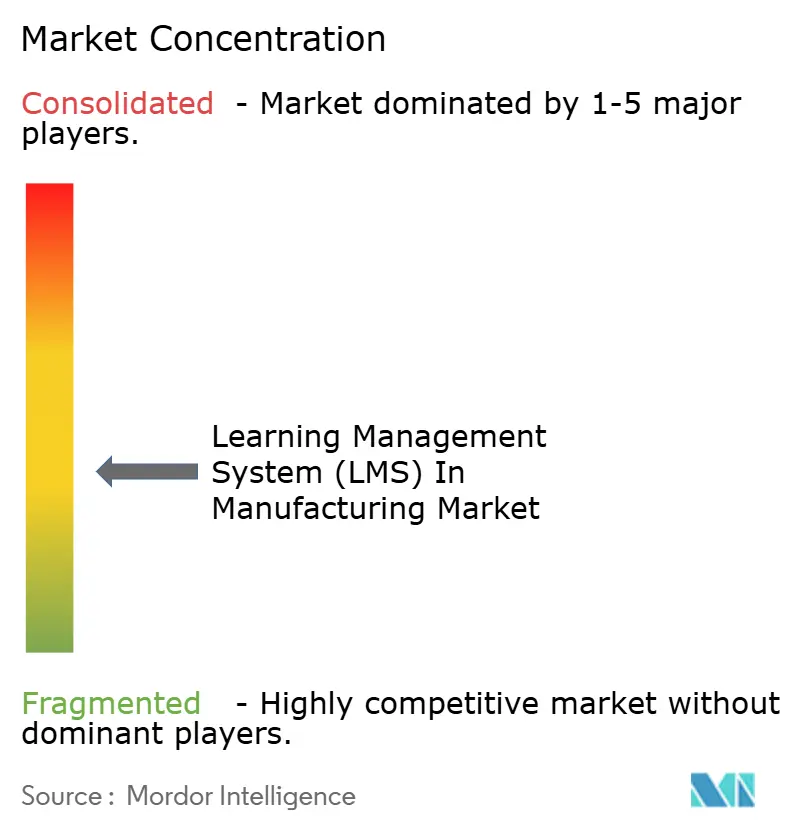

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Learning Management System (LMS) In Manufacturing Market Analysis by Mordor Intelligence

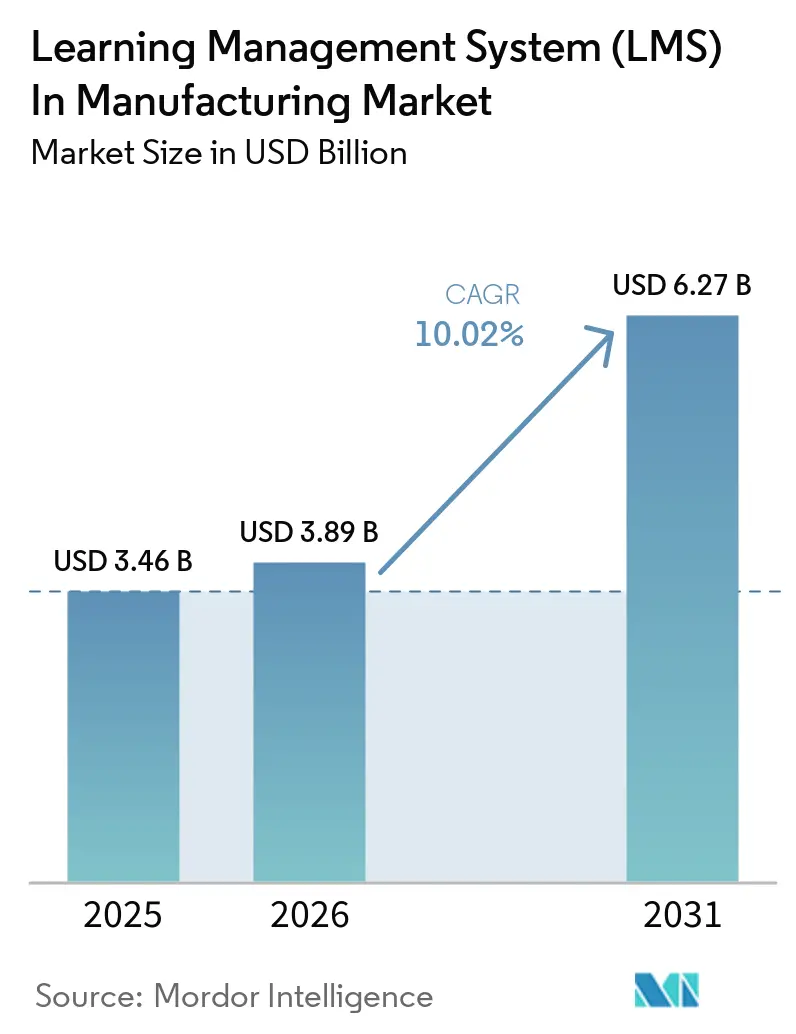

The learning management system (LMS) market in manufacturing was valued at USD 3.46 billion in 2025 and USD 3.89 billion in 2026, and is forecast to reach USD 6.27 billion by 2031, expanding at a CAGR of 10.02% over 2026-2031. Manufacturers spent USD 32 billion on workforce training and upskilling programs in 2026, up from USD 26.2 billion in 2019, and average training hours per employee rose to 47.6 from 42.9 over the same period, indicating that learning spend is now more closely tied to plant performance than to discretionary HR budgets. Robotics deployment, AI-led quality workflows, and tighter compliance obligations are pushing manufacturers to adopt platforms that can document training, speed role readiness, and support repeatable skill development at scale. Demand also remains anchored by large multi-site operators that want consistent training across shifts, plants, and regions without adding local administrative burden. Cloud deployment, software-led delivery, and enterprise-scale buying patterns show that platform adoption is increasingly shaped by rollout speed, audit readiness, and operational standardization rather than by one-time digitalization programs. The result is a market where usage is supported by recurring workforce change, ongoing certification needs, and the constant need to onboard new workers into structured production environments.

Key Report Takeaways

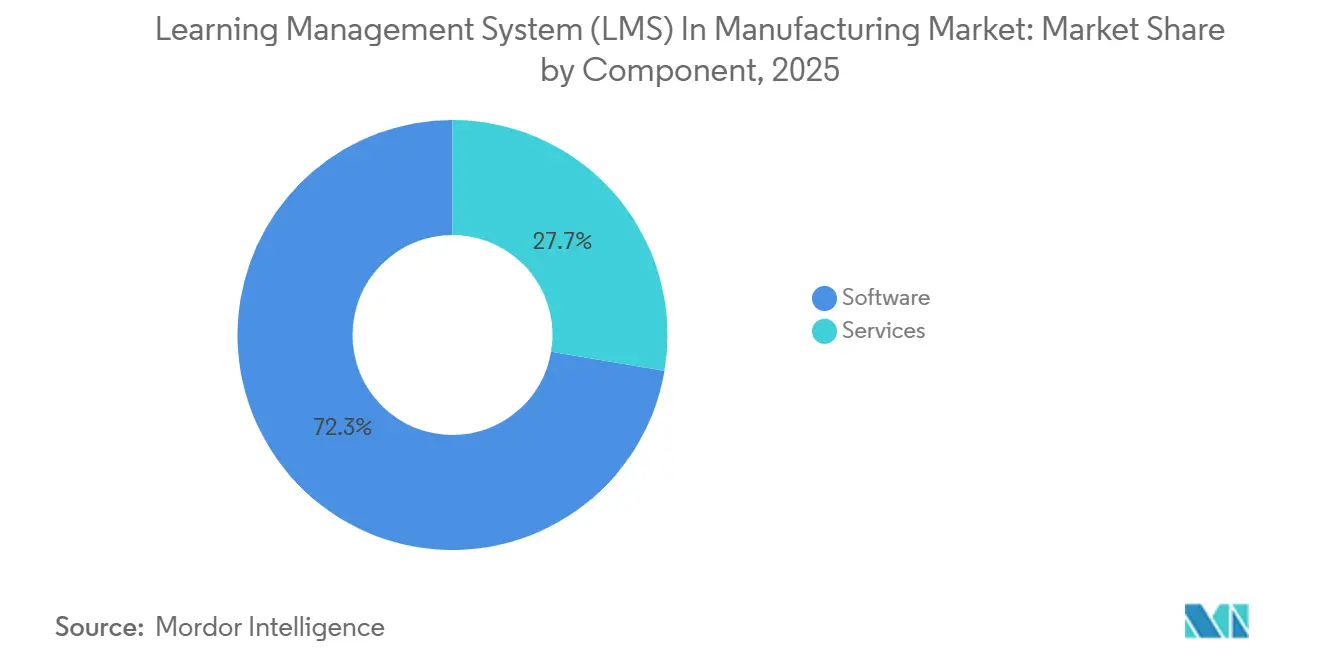

- By component, software accounted for 72.34% of the learning management system (LMS) market in 2025, while services are projected to expand at a 11.23% CAGR through 2031.

- By deployment model, cloud-based deployments accounted for 68.47% of the market in 2025 and recorded the highest projected CAGR of 12.37% through 2031.

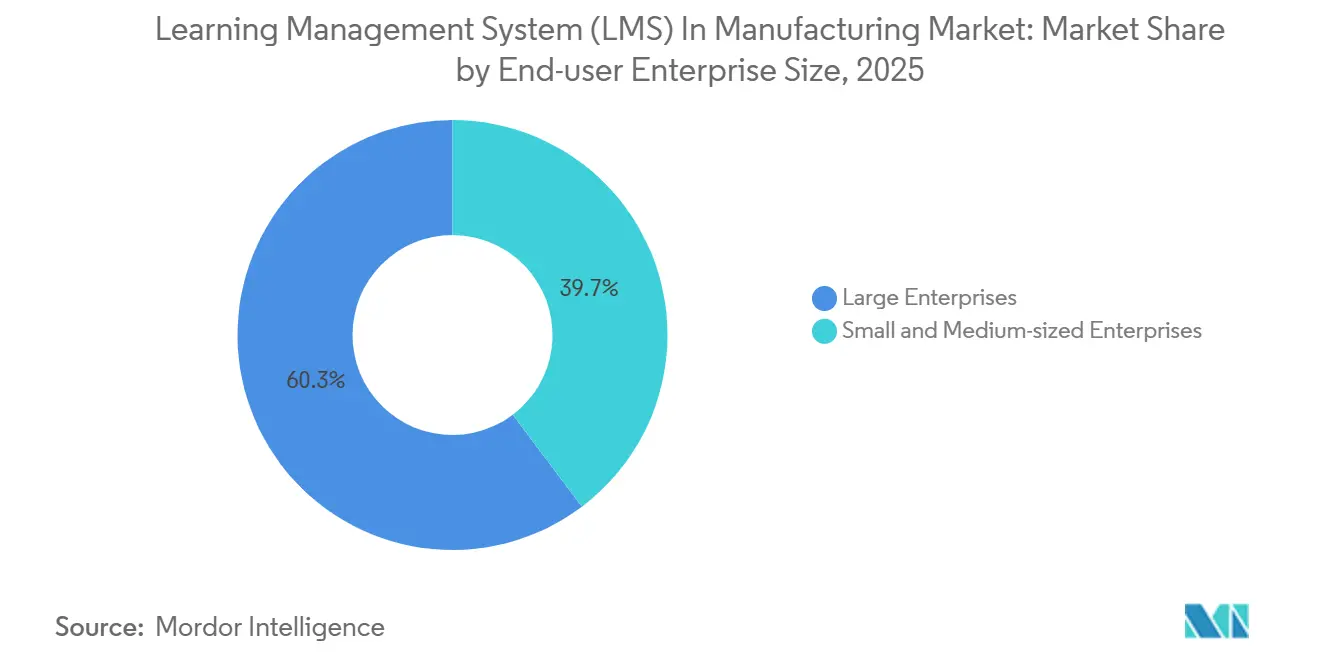

- By enterprise size, large enterprises captured 60.28% of the market in 2025, while SMEs are forecast to grow at an 11.46% CAGR through 2031.

- By training function, technical skills training led with a 34.62% share in 2025, while employee onboarding is projected to advance at an 11.79% CAGR through 2031.

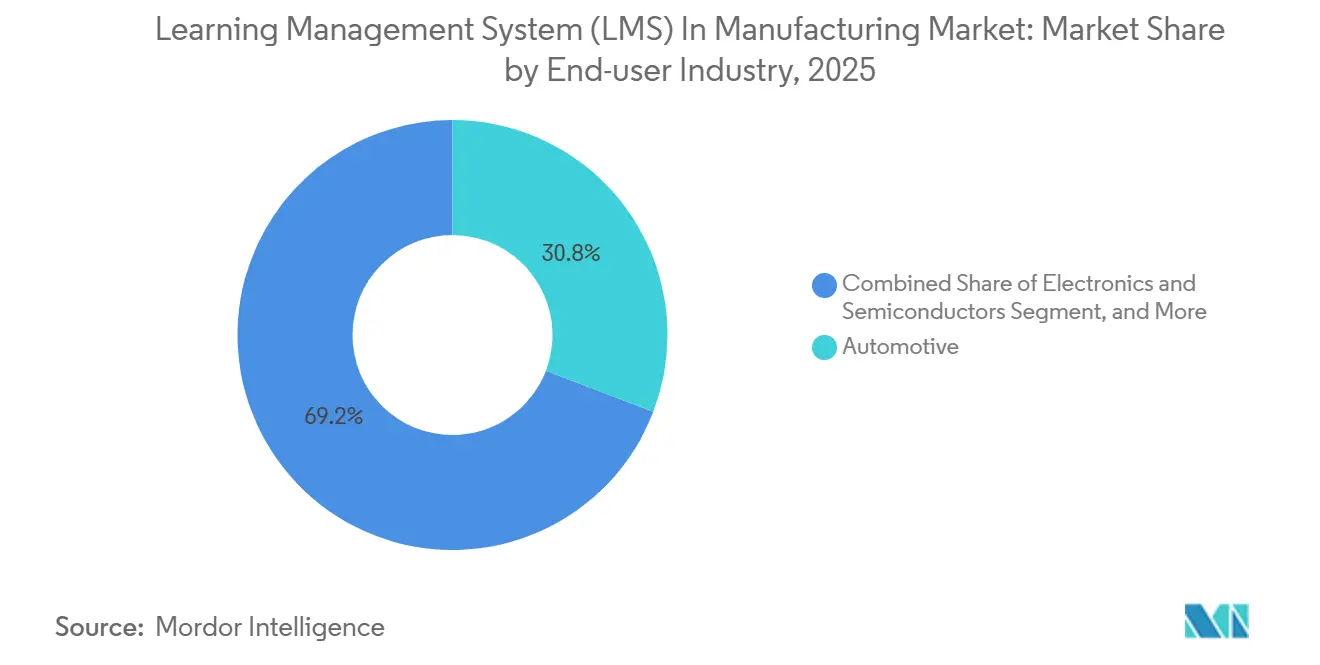

- By end-user industry, automotive held 30.81% of the market in 2025, while electronics and semiconductors are expected to grow at a 13.24% CAGR through 2031.

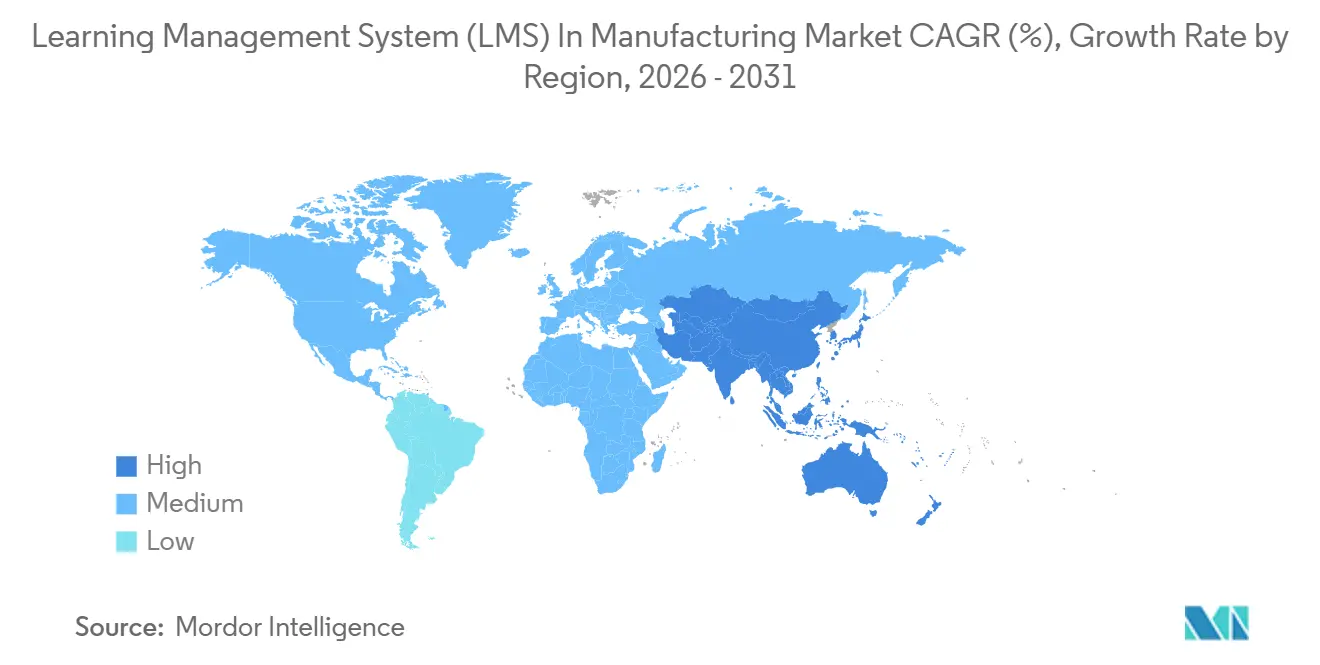

- By geography, North America held 38.69% of the market in 2025, while Asia-Pacific is projected to record the fastest regional CAGR of 14.37% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Learning Management System (LMS) In Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0 Reskilling Across Smart Factories | +2.5% | Global, with concentrated demand in North America, Germany, China, Japan, South Korea | Medium term (2-4 years) |

| Audit-Ready Compliance and Certification Tracking | +1.8% | Global, highest regulatory density in North America, Europe, and APAC pharma and food verticals | Short term (≤ 2 years) |

| Multi-Site Training Standardization Across Plants and Shifts | +1.3% | North America, Europe, Asia-Pacific, multinational automotive and electronics manufacturers | Medium term (2-4 years) |

| Mobile and Offline Learning for Deskless Workers | +1.0% | Global, with highest immediate uptake in South and Southeast Asia, South America | Short term (≤ 2 years) |

| AI Conversion of SOPs Into Microlearning | +0.8% | North America, Europe, expanding to Asia-Pacific as AI tooling matures | Medium term (2-4 years) |

| Contractor and Temporary Labor Credentialing at Plant Gates | +0.6% | North America, Middle East, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Industry 4.0 Reskilling Across Smart Factories

The LMS in the manufacturing market is being shaped by a broader redesign of factory work as digital tools change the skills required on the production floor. The World Economic Forum projected that 39% of existing worker skill sets will be transformed or outdated by 2030, with advanced manufacturing employers ranking AI and big data, robotics, and new materials among their most urgent capability gaps.[1] World Economic Forum, “The Future of Jobs Report 2025,” World Economic Forum, weforum.org That shift means learning systems are now expected to support role-based capability building, not just course delivery or annual compliance refreshers. The World Economic Forum and McKinsey and Company also found that more than 40% of Gen Z employees in manufacturing consider leaving within 3-6 months when career development and skill-building pathways are missing, and the attrition cost reached USD 52,000 per departing frontline employee. In the LMS in the manufacturing market, this raises the value of platforms that can map skills to machine types, work cells, and job families in a way that stays useful after the first deployment. Vendors that provide only course libraries face weaker long-term positioning because manufacturers are increasingly treating structured skills architecture as part of core plant infrastructure rather than a simple training add-on.

Audit-Ready Compliance And Certification Tracking

The LMS in the manufacturing market continues to benefit from the need to maintain documented evidence of workforce readiness across safety, quality, and operating procedures. Manufacturers face a dual documentation burden because regulatory requirements call for explicit training records, while broader management systems require proof of controlled processes, certifications, and recurring refresh cycles. This makes centralized reporting, automated reminders, and version-controlled content much more important than in less regulated office environments. In the LMS manufacturing market, purchasing decisions are often driven by whether the platform can produce inspection-ready records quickly and consistently across sites. That preference strengthens vendors that can tie certifications, training completions, and role permissions into a single auditable workflow, rather than leaving manufacturers to reconcile spreadsheets and disconnected point tools. The result is a pricing environment in which audit-ready reporting and credential traceability support stronger commercial positioning than basic learning-delivery features alone.

Multi-Site Training Standardization Across Plants And Shifts

The LMS in the manufacturing market is also gaining traction due to the need to standardize training across plants operating in different languages, shifts, and production contexts. Procedure drift between facilities creates quality variance, slows workforce mobility, and increases the chance that one site will fall out of step with corporate standards. Costa Farms, after standardizing connected worker and training processes across 9 sites and 3 languages, reduced SOP access time by 65% and shortened documentation approval cycles by 80%.[2]Scott Ginsberg, “The New Playbook for Operational Learning and Development,” Dozuki, dozuki.com The World Economic Forum noted that 55% of mining and metals employers and 46% of automotive and aerospace employers expect significant transformation due to trade restrictions, raising the odds that manufacturers will need to bring new facilities into their operating networks quickly, in the LMS in the manufacturing market, that supports demand for multi-tenant systems, localized governance, and role-based access models that can be extended without rebuilding the platform for each site. Vendors that can handle central control with plant-level flexibility are therefore better placed than those that rely on heavily customized single-instance deployments.

Mobile And Offline Learning For Deskless Workers

The LMS in the manufacturing market is expanding into a workforce that spends most of its time away from desks, shared terminals, and formal classrooms. Research shows that deskless workers make up close to 80% of the global manufacturing workforce, which helps explain why mobile learning access is becoming more central to platform design.[3]JD Dillon, “Unlock Deskless Worker Potential With AI,” ATD Blog, td.org In 2026, 60% of frontline workers wanted mobile access to training, 37% preferred using their own devices, and 63% wanted shorter learning modules. Those signals matter because long digital courses do not solve the time pressure of shift work if workers still have to step away from the line for extended periods. In the manufacturing LMS market, completion rates depend as much on module design and offline usability as on the quality of the content itself. Vendors that restructure learning into short, task-linked sessions for changeovers, breaks, and shift handovers are better aligned with the operational reality of deskless production teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy ERP, MES, and HRIS Integration Complexity | -1.5% | Global, most acute in large enterprises with installed SAP, Oracle, or legacy MES environments | Long term (≥ 4 years) |

| Production-Time Trade-Offs That Limit Learning Hours | -0.9% | Global, highest friction in continuous-process industries such as food and beverage, chemicals, and pharma | Medium term (2-4 years) |

| Multilingual Content Governance Across Plants | -0.6% | Asia-Pacific, Europe, South America, manufacturing clusters with diverse linguistic workforces | Medium term (2-4 years) |

| Data Residency and IP Leakage Concerns | -0.4% | Europe, China, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy ERP, MES, And HRIS Integration Complexity

The LMS in the manufacturing market still faces a major restraint when new learning systems have to connect with deeply embedded enterprise software stacks. In 2026, manufacturing ERP integration projects exceeded initial budgets by an average of 72%, while discrete manufacturers saw overruns as high as 215%.[4]Andy Erk, “Manufacturing ERP Integration, Hidden Costs of Legacy System Mistakes,” MIE Solutions, mie-solutions.com That problem carries over into learning deployments because user provisioning, credential records, job roles, plant hierarchies, and training triggers often sit across ERP, MES, and HRIS systems that were not designed to work together. The burden is especially heavy for mid-market manufacturers that have already invested in core systems but lack internal teams for custom API work and long integration cycles. In the LMS manufacturing market, pre-built connectors now function more as minimum entry requirements than as premium differentiators, because buyers expect them before a platform is even shortlisted. Vendors with weak connector libraries or limited implementation depth, therefore, face slower sales cycles, higher project risk, and lower adoption among buyers that otherwise need digital training systems.

Production-Time Trade-Offs That Limit Learning Hours

The LMS in the manufacturing market also remains constrained by the direct conflict between training time and production time. A survey published in April 2026 found that 69% of manufacturers cited work-hour interruptions as the main barrier to training, 65% cited scheduling conflicts, and 48% cited cost. That means even well-supported training programs can stall if managers believe mandatory learning will disrupt throughput or labor planning. Long digital courses do little to solve the issue because they still remove workers from active operations for extended periods that accumulate across lines and shifts. In the LMS market for manufacturing, platforms that show how learning can fit around break periods, equipment changeovers, and short shift transitions are more likely to win operational support. The commercial advantage is moving toward vendors that can demonstrate preserved production hours and reduced disruption, not just higher completion rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals A Shift Toward Managed Outcomes

Software accounted for 72.34% of the LMS market size in manufacturing in 2025, underscoring how strongly platform licenses already anchor adoption across large manufacturers and regulated plants. The software layer became the center of most deployments because manufacturers first needed systems that could manage learning paths, certification records, and user administration in one place. That installed base grew across 2019-2025 as cloud platforms replaced instructor-led and spreadsheet-led training administration in more facilities. In the LMS in the manufacturing market, software also benefited from the need to run recurring compliance programs with less manual oversight across plants and shifts. This made the component mix look heavily platform-led before deeper service demand emerged.

Services, however, are projected to grow at a 11.23% CAGR through 2031, suggesting a shift in what buyers now expect after the first rollout. As deployments move from basic compliance tracking into skills intelligence, AI-assisted content creation, cross-plant analytics, and workflow integration, manufacturers increasingly need implementation, configuration, and managed support. In the LMS, the manufacturing industry favors providers and partners with manufacturing process knowledge over generic enterprise LMS capacity alone. It also reflects a broader shift in the LMS market for manufacturing toward bundled delivery models where the value lies in outcomes, governance, and adoption support, not just in access to software seats. Vendors that can combine platform depth with plant-level execution are therefore better positioned to capture a growing share of services revenue as training programs become more embedded in operations.

By Deployment Model: Cloud Growth Leads, While Hybrid Holds Its Place In Regulated Settings

Cloud-based deployment held 68.47% of the LMS market share in manufacturing in 2025 and also posted the fastest projected CAGR at 12.37% through 2031. That combination is notable because it shows the largest deployment model is still extending its lead rather than losing ground to niche alternatives. Manufacturers have been drawn to cloud systems because they enable faster rollouts across distributed plants and reduce the infrastructure burden of local server management. In the LMS market for manufacturing, cloud adoption also appeals to buyers who want regular updates, easier administration, and lower upfront investment. These features are especially attractive to mid-sized manufacturers that need enterprise-grade training control but cannot justify the complex on-site infrastructure required at each location.

Even so, on-premises and hybrid models remain relevant where training data, validation rules, or sector-specific controls limit the use of public cloud environments. Pharmaceutical manufacturers continue to prioritize controlled change management, while defense-related operations may face stricter rules for handling training records and supporting data. Hybrid deployment, therefore, remains a practical middle ground because it lets companies keep sensitive records under local control while still using cloud-delivered content and broader administrative tools. In the LMS in the manufacturing industry, that balance matters in Europe and parts of Asia where data residency rules shape architecture decisions as much as cost and speed do. The LMS market in manufacturing is therefore consolidating around cloud for scale, but it still leaves room for hybrid models in regulated verticals that need both flexibility and tighter control.

By End-User Enterprise Size: SMEs Gain Ground As Access Costs Fall

Large enterprises accounted for 60.28% of the LMS market share in manufacturing in 2025, reflecting the early buying power of global automotive, electronics, and pharmaceutical manufacturers. These companies were better placed to sign multi-year agreements, fund integration work, and deploy standardized training at scale across multiple facilities. Their larger compliance burden also made centralized training records and recurring certification workflows easier to justify in budget terms. In the manufacturing LMS market, enterprise demand helped establish the category through large deployments that linked workforce learning to plant governance and quality control. That legacy still gives large organizations the broadest installed base today.

SMEs are projected to expand at a 11.46% CAGR through 2031, underscoring how cloud pricing and simpler deployment models have changed the economics of adoption. Smaller manufacturers now have access to subscription structures that remove much of the upfront cost that once delayed or blocked deployment. Many of these companies still face the same safety and certification obligations as their larger peers, but with thinner compliance teams and less administrative capacity. In the manufacturing LMS market, automated reminders, audit-ready records, and easy user management are especially valuable for 100-1,000 employees. The shift narrows the gap between enterprises and smaller buyers, and it gives vendors room to win share with learner-compliance-first offerings that do not require heavy implementation.

By Training Function: Onboarding Speed Matters More In Tight Labor Conditions

Technical skills training accounted for 34.62% of the LMS market share in manufacturing in 2025, supported by the ongoing need to qualify operators and maintenance staff for more complex equipment and automated systems. This segment remains central because production performance depends on workers' detailed understanding of machine behavior, setup steps, and standard operating procedures. Technical instruction also tends to be repeated as equipment changes, software updates arrive, and experienced staff leave the workforce. In the LMS in the manufacturing market, this keeps technical learning at the center of initial deployments, especially in plants where equipment uptime and output quality depend on precise operator behavior. The segment remains the largest because it connects directly to plant productivity and workforce readiness.

Employee onboarding is forecast to grow at a 11.79% CAGR through 2031, reflecting how labor shortages are increasing the cost of slow time-to-productivity. Manufacturers using immersive digital onboarding increased onboarding speed by more than 50% and reduced onboarding costs by up to 54%. That matters because manufacturers are under pressure to move new hires from induction to safe and productive work with fewer supervisors available for extended shadowing. In the LMS market for manufacturing, onboarding is therefore becoming a more strategic budget line, not just an HR process at the front end of employment. Safety and compliance, equipment training, quality and lean training, operational process modules, and other custom functions remain core adoption triggers, but faster onboarding is becoming one of the strongest reasons to expand platform use after the first implementation.

By End-User Industry: Electronics Momentum Builds, While Automotive Keeps Its Scale

Automotive held 30.81% of the LMS market share in 2025, reflecting the scale of OEM and supplier workforces and the sector’s mature quality and compliance systems. The vertical has long relied on structured qualification, repeatable work instructions, and documented training aligned to tightly managed production environments. That gives automotive manufacturers a natural fit with digital learning platforms that can standardize training across plants, roles, and supplier-facing quality processes. In the manufacturing LMS market, automotive also benefits from its large installed workforce, which creates recurring demand for new-hire onboarding, safety refreshers, and equipment certification. These factors keep the sector ahead even as other industries accelerate their deployments.

Electronics and semiconductors are projected to grow at a 13.24% CAGR through 2031, supported by fab capacity expansion and the need for structured training around cleanroom protocols, process control, and equipment qualification. This vertical places a premium on traceable learning paths because new facilities need workers who can operate in tightly controlled conditions from the start of production ramp-up. Generic learning systems often struggle in this environment when they lack industry-specific certification workflows or content aligned to equipment and process sensitivity. Pharmaceuticals and chemicals continue to support stable demand as validated training remains tied to audit and quality requirements, and Gyrus Systems reported a 40% reduction in audit preparation time in a Swiss-American CDMO case after LMS deployment. Food and beverage, aerospace and defense, and industrial machinery and equipment further broaden the vertical mix, meaning the LMS in the manufacturing market draws strength from several end markets that each face their own compliance, onboarding, and skills pressures.

Geography Analysis

North America held a 38.69% share of the LMS market in manufacturing in 2025, driven by layered compliance requirements and a dense base of multi-site manufacturers that need audit-ready training infrastructure. The United States accounts for the largest share of regional demand because documented learning, recurring certifications, and plant-level reporting remain central to manufacturing compliance and workforce governance. Canada and Mexico add to that demand through cross-border production networks, where manufacturers need synchronized learning workflows and multilingual delivery that can align with U.S.-based standards. The LMS market in manufacturing is therefore deeply established in North America because training systems are used not only for learning delivery but also for proof, traceability, and operational consistency. This gives the region a strong installed base that is difficult for other geographies to match in current share.

Europe remains an important region for the LMS in the manufacturing market because compliance expectations and data governance needs shape platform selection more directly than in many other regions. Demand is concentrated in Germany, the United Kingdom, and France, where buyers must balance training control with close attention to data architecture and residency requirements. A 4,500 m² training center opened in Pfronten, Germany, in February 2026, which underlines the region’s continued commitment to structured workforce development infrastructure even outside formal LMS deployments. European deployment choices are also shaped by the need to balance scalable content delivery with region-specific control over records and user data. That dynamic keeps hybrid and compliance-aware cloud models relevant across advanced manufacturing clusters in the region.

Asia-Pacific is the fastest-growing geography at a 14.37% CAGR through 2031, led by China, India, South Korea, Japan, and the expanding Southeast Asian manufacturing base. In China, a 2025 study on digital production management reported that more than 65% of manufacturing enterprises were piloting AI-powered training recommendation systems, with penetration expected to exceed 85%. Japan’s Ministry of Economy, Trade and Industry noted that manufacturers were still advancing digital transformation unevenly, with many firms remaining focused on Kaizen improvements in individual processes rather than enterprise-wide digital upskilling. India’s manufacturing expansion and Southeast Asia’s nearshoring gains continue to create new cohorts of workers who need rapid onboarding, role certification, and multilingual learning support. South America, the Middle East, and Africa remain smaller in terms of current share, but they are expanding as industrial diversification and formal credential tracking become more important. In 2026, it was reported that 23% of unplanned production stoppages in South American plants originated from the incorrect assignment of unqualified personnel.

Competitive Landscape

The LMS market in manufacturing remains fragmented, with no single vendor holding a dominant position across all geographies, deployment models, and training functions. Competition spans purpose-built manufacturing platforms and broader enterprise LMS providers that are extending their offerings with plant-floor modules, AI features, and deeper workforce analytics. Docebo, Absorb Software, and 360Learning generally compete on integration breadth, broader enterprise workflows, and, increasingly, AI-enabled learning support. Dozuki, Vector Solutions, and Intertek Alchemy differentiate more through manufacturing-specific functionality such as SOP-linked training, connected worker workflows, compliance-centered content, and floor-level operational fit. This leaves buyers choosing between broad platform flexibility and stronger manufacturing process specificity, rather than comparing a uniform set of interchangeable products.

Recent strategic activity shows that leading vendors are moving beyond content delivery into broader workforce intelligence and embedded operational support. Docebo announced in April 2026 that it acquired 365Talents and Zive, using those additions to build Docebo AgentHub and Docebo Skills Intelligence around automated skills campaigns, personalized learning delivery, and knowledge workflows. In November 2025, 360Learning announced a strategic partnership with Workday, integrating its AI-powered authoring tools and Academies with Workday’s talent management capabilities. Valamis also announced a strategic partnership with IFS in May 2026 to bring enterprise learning, workforce compliance, and certification management into the IFS Cloud ecosystem for industrial customers. These moves show that the LMS in the manufacturing market is moving toward tighter integration between learning, skills visibility, HR workflows, and the operating systems used across industrial environments.

A second competitive shift is taking place at the point of work, where connected worker platforms are embedding training into digital work instructions rather than routing users through a separate learning portal. This matters in manufacturing because context switching is costly, and training completion often drops when learning is detached from the task or machine in front of the worker. In February 2026, Dozuki expanded data center presence to Frankfurt, Paris, Singapore, and Tokyo, a move aimed at supporting data sovereignty needs in multiple regions. That kind of infrastructure investment shows that compliance, localization, and deployment architecture are now part of competitive positioning, not back-office details. Vendors with shallow connector portfolios, weaker content depth, or limited manufacturing specialization are therefore under greater pressure as buyers consolidate their vendor lists and demand stronger proof of operational fit.

Learning Management System (LMS) In Manufacturing Industry Leaders

Docebo S.p.A.

Absorb Software Inc.

Litmos US, L.P.

Epignosis LLC

360Learning S.A.S.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Valamis partnered with IFS to integrate enterprise learning, compliance, and certification management into the IFS Cloud ecosystem, linking workforce enablement with operational transformation.

- April 2026: Docebo acquired 365Talents and Zive, launching AgentHub and Skills Intelligence for automated skills campaigns, personalized learning, and gap analysis.

- April 2026: Docebo also rolled out a major update with the Companion browser extension, Model Context Protocol server for AI assistants, and Harmony AI Tutor for guided learning.

- March 2026: Schoox won two Lighthouse Tech Awards for AI-driven learning delivery, recognized for practical AI innovation and frontline-focused solutions.

Global Learning Management System (LMS) In Manufacturing Market Report Scope

In the manufacturing market, a Learning Management System (LMS) is a digital platform and service that enables manufacturing enterprises to deliver, manage, and track workforce training programs across diverse industrial sectors. These solutions cover technical skills, safety and compliance, equipment and machinery handling, lean manufacturing, operational processes, and employee onboarding, and are deployed via cloud, on-premises, or hybrid models. Delivered through flexible formats, LMS platforms help large and small manufacturers enhance workforce productivity, ensure regulatory compliance, improve quality standards, and support continuous upskilling across industries such as automotive, electronics, food and beverage, pharmaceuticals, and aerospace.

The Learning Management System (LMS) in Manufacturing Market is segmented by Component (Software and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), End-user Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Training Function (Technical Skills Training, Safety and Compliance Training, Equipment and Machinery Training, Quality and Lean Manufacturing Training, Operational Process Training, Employee Onboarding, and Other Training Functions), End-user Industry (Automotive, Electronics and Semiconductors, Industrial Machinery and Equipment, Pharmaceuticals and Chemicals, Food and Beverage, Aerospace and Defense, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Technical Skills Training |

| Safety and Compliance Training |

| Equipment and Machinery Training |

| Quality and Lean Manufacturing Training |

| Operational Process Training |

| Employee Onboarding |

| Other Training Functions |

| Automotive |

| Electronics and Semiconductors |

| Industrial Machinery and Equipment |

| Pharmaceuticals and Chemicals |

| Food and Beverage |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Training Function | Technical Skills Training | |

| Safety and Compliance Training | ||

| Equipment and Machinery Training | ||

| Quality and Lean Manufacturing Training | ||

| Operational Process Training | ||

| Employee Onboarding | ||

| Other Training Functions | ||

| By End-user Industry | Automotive | |

| Electronics and Semiconductors | ||

| Industrial Machinery and Equipment | ||

| Pharmaceuticals and Chemicals | ||

| Food and Beverage | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the Learning Management System (LMS) In Manufacturing Market size in 2025 and 2031?

The Learning Management System (LMS) In Manufacturing Market was valued at USD 3.46 billion in 2025 and is forecast to reach USD 6.27 billion by 2031, growing at a 10.02% CAGR over 2026-2031.

Which region leads demand for manufacturing learning platforms?

North America led with a 38.69% share in 2025, supported by compliance-heavy adoption and a high concentration of multi-site manufacturing operations.

Why are manufacturers increasing spending on learning management systems?

Manufacturers spent USD 32 billion on workforce training and upskilling in 2026, and rising automation, AI use, and compliance needs are making structured digital training more important.

Which deployment model is growing the fastest for factory learning systems?

Cloud-based deployment held 68.47% of the market in 2025 and is also the fastest-growing model, with a projected 12.37% CAGR through 2031.

Which training function is expanding most quickly across factories?

Employee onboarding is the fastest-growing training function, projected to expand at an 11.79% CAGR through 2031 as manufacturers try to reduce time-to-productivity for new hires.

Which end-user sector creates the strongest demand today?

Automotive was the largest end-user industry in 2025 with a 30.81% share, while electronics and semiconductors is expected to grow the fastest through 2031.

Page last updated on: