Asia-Pacific Learning Management Systems (LMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

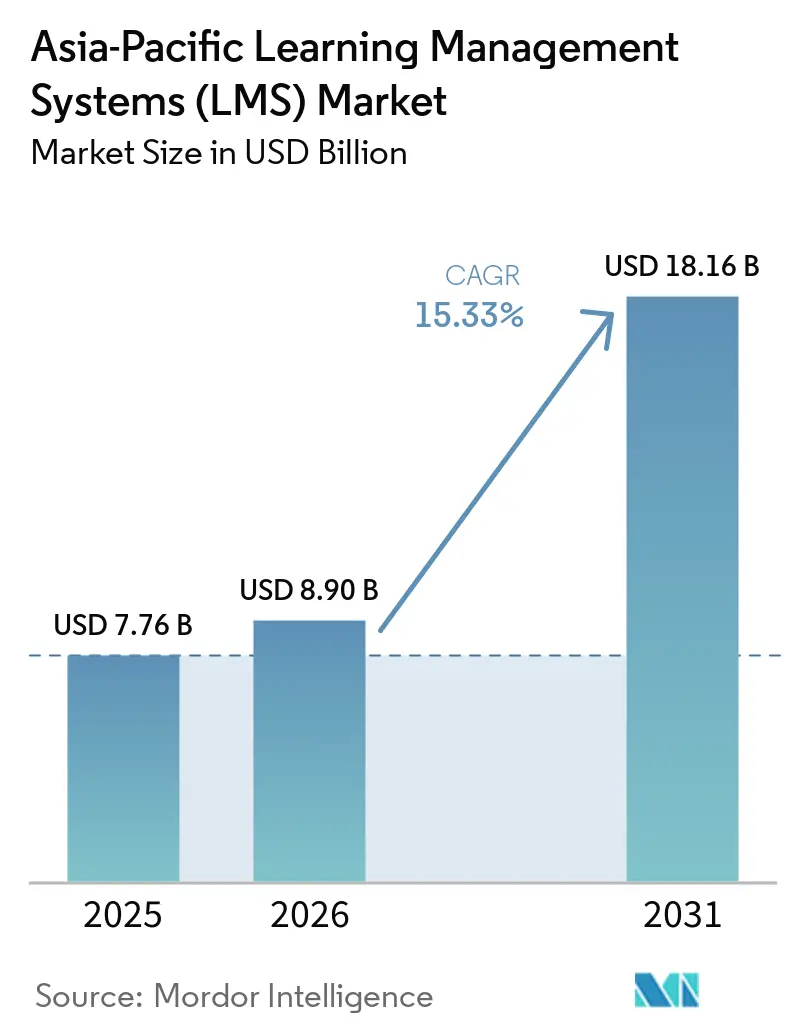

| Base Year Market Size (2025) | USD 7.76 Billion |

| Market Size (2026) | USD 8.90 Billion |

| Market Size (2031) | USD 18.16 Billion |

| Growth Rate (2026 - 2031) | 15.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Learning Management Systems (LMS) Market Analysis by Mordor Intelligence

The Asia-Pacific learning management systems (LMS) market size is expected to increase from USD 7.76 billion in 2025 to USD 8.90 billion in 2026 and reach USD 18.16 billion by 2031, at a CAGR of 15.33% over 2026-2031. The Asia Pacific learning management systems market is expanding on the back of enterprise reskilling needs, rising cloud infrastructure spending, and workforce modernization programs backed by public policy across both developed and emerging economies. Demand is also being reinforced by the move away from ad hoc instructor-led training toward structured learning paths that can be tracked, measured, and linked to compliance or job performance. Competitive activity remains intense because global platforms are broadening their partner networks to meet local-language and pedagogical needs, while domestic vendors in China and India continue to benefit from data-residency rules and public-sector relationships. The opportunity set is widening beyond office workers, as factory-floor training, academic microcredentials, and managed services are creating new revenue pools for vendors that can combine software delivery with implementation and support depth. At the same time, uneven connectivity in parts of Southeast Asia, subscription sensitivity among SMEs, and stricter data localization rules continue to slow adoption in some sub-geographies and lengthen procurement cycles for multinational buyers.

Key Report Takeaways

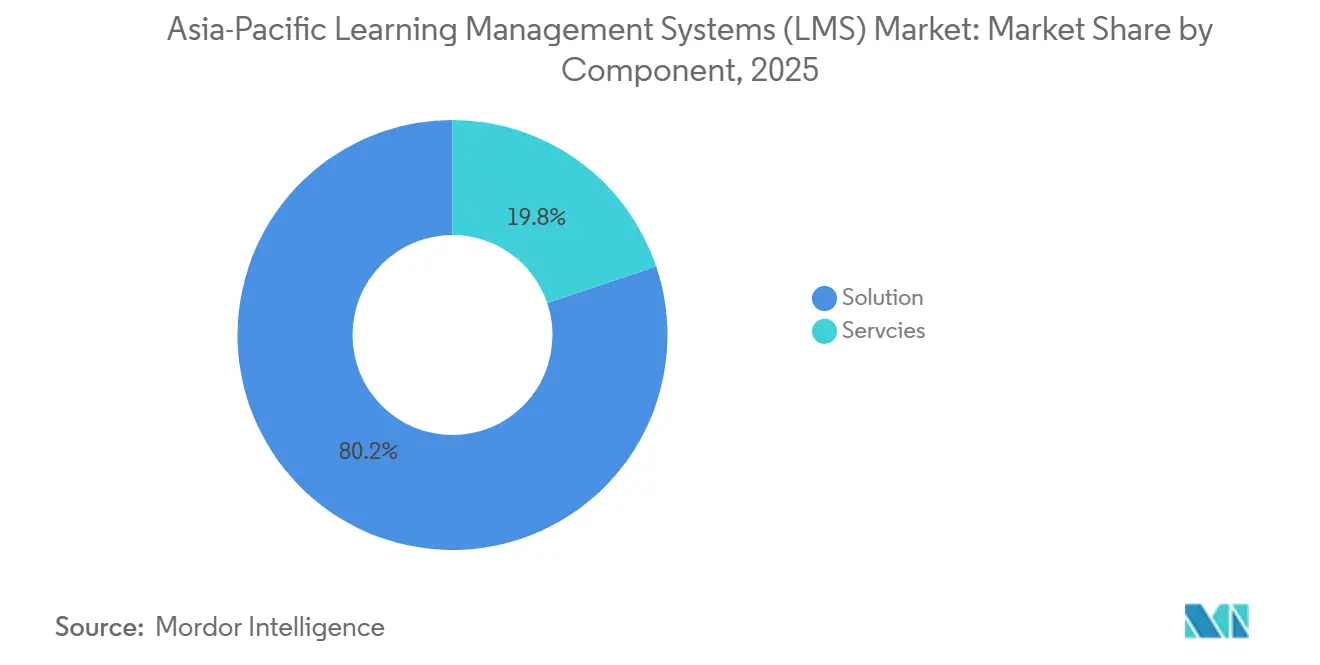

- By component, solutions led the Asia-Pacific learning management systems (LMS) market with 80.19% share in 2025, while services recorded the fastest projected CAGR at 16.24% through 2031.

- By deployment, cloud held a 68.62% share in 2025 and posted the fastest projected CAGR of 17.42% through 2031.

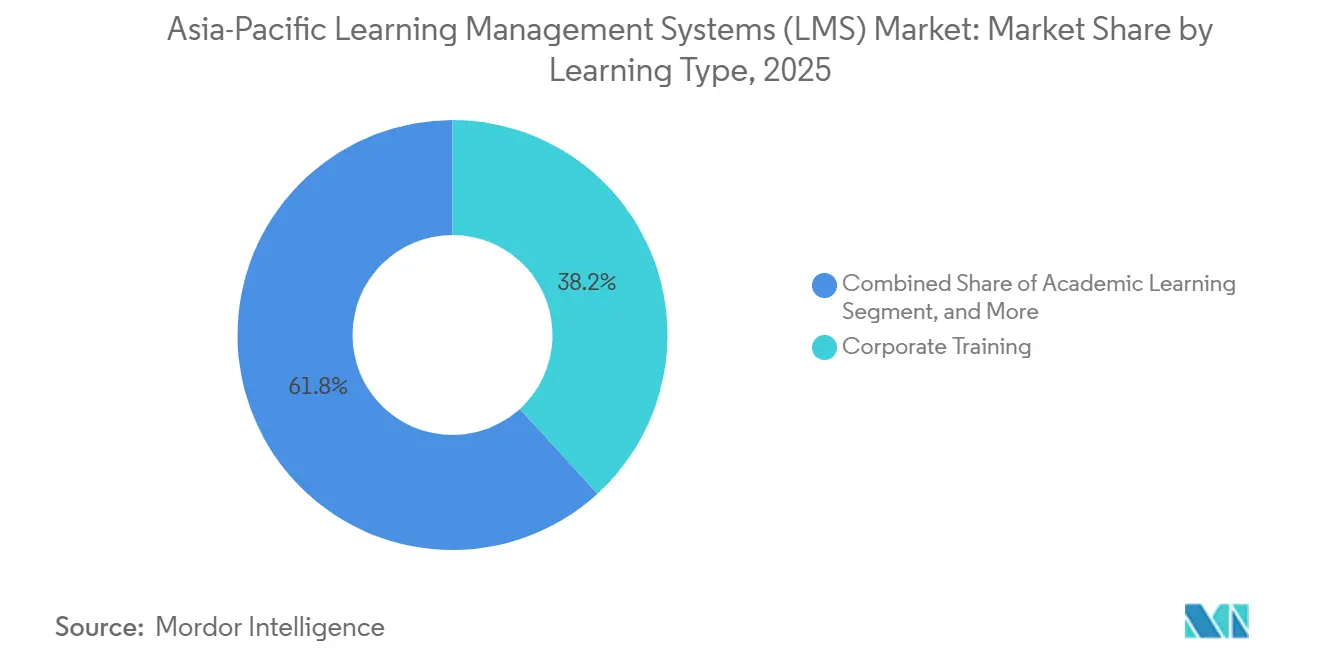

- By learning type, corporate training accounted for 38.23% of the market in 2025, while academic learning is forecast to expand at a 15.61% CAGR through 2031.

- By end-user vertical, BFSI held 34.13% share in 2025, while manufacturing and industrial operations are projected to grow at a 16.84% CAGR through 2031.

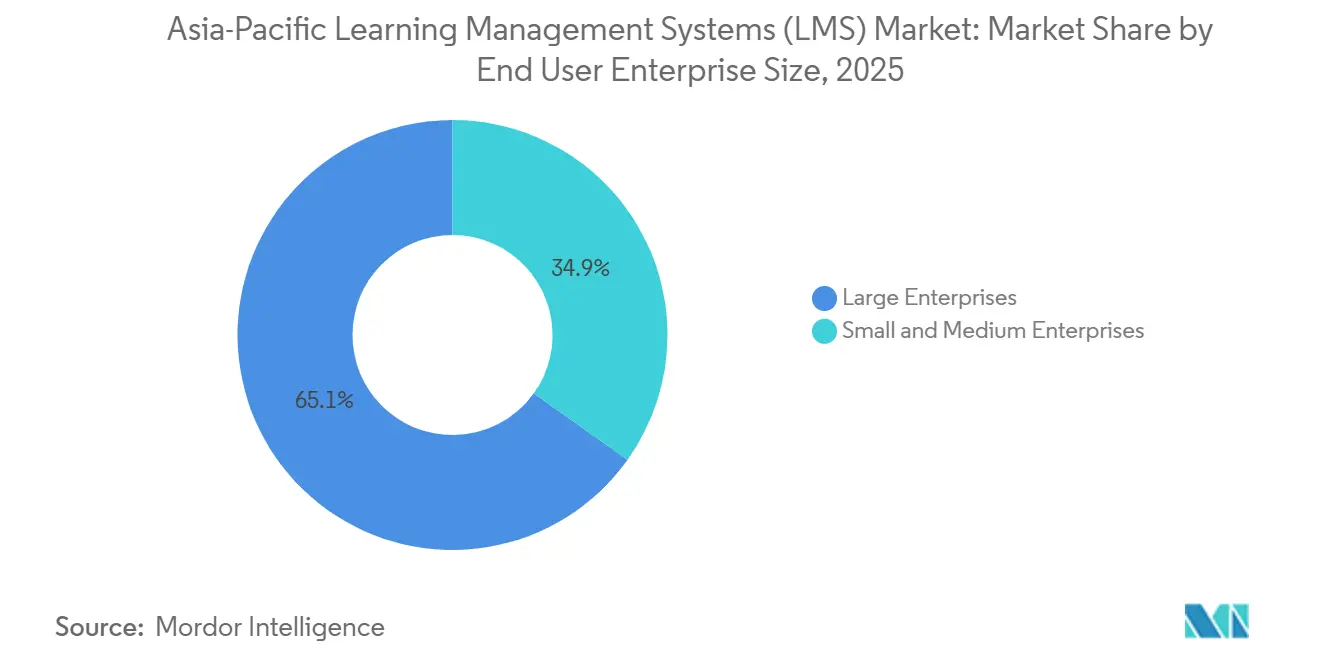

- By enterprise size, large enterprises captured 65.12% of the market in 2025, while SMEs registered the highest projected CAGR of 17.11% through 2031.

- By geography, China represented 32.81% of regional revenue in 2025, while India is projected to record the fastest growth at a 15.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Learning Management Systems (LMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Shift Toward Skills-Based and Objective-Driven Training | +4.2% | Global, with concentration in Australia, Singapore, and Japan | Medium term (2-4 years) |

| Rising Corporate Reskilling and Compliance Training Demand | +3.6% | Global, primary concentration in BFSI-heavy markets including Singapore, Hong Kong, and India | Short term (= 2 years) |

| Accelerating Cloud and Mobile-First Learning Adoption | +2.9% | APAC core, with spill-over to emerging Southeast Asian markets | Medium term (2-4 years) |

| Expansion of Hybrid and Distance Learning Across Higher Education | +2.4% | China, India, Australia, South Korea | Medium term (2-4 years) |

| National Micro-Credential Frameworks and Digital Badge Infrastructure | +1.8% | Australia, Singapore, South Korea | Long term (= 4 years) |

| Skills-Based Internal Mobility Programs Requiring Credential-Mapped Learning Paths | +1.4% | Global, with early gains in Japan, Singapore, and Australia | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Shift Toward Skills-Based and Objective-Driven Training

Enterprises across the region are reorganizing learning budgets around skills and competency needs rather than fixed, role-based course libraries, and that shift is changing how buyers evaluate the Asia Pacific learning management systems market. Procurement is moving toward platforms that can connect content, skills graphs, and measurable capability outcomes within one system. The World Economic Forum identified skills-based talent deployment as a top-three workforce priority in its 2025 workforce outlook, underscoring the growing demand for platforms with competency-mapping and skills-intelligence features. OCBC demonstrated the commercial impact of this approach when 900 wealth advisors were trained in generative AI tools through structured LMS pathways, resulting in a 50% revenue uplift within 3 months and a doubling of weekly client appointments for trained staff compared with untrained peers. This is making vendors with native skills and ontology capabilities more attractive than providers that rely mainly on content depth. Cornerstone OnDemand’s acquisition of SkyHive reinforced that direction by adding skills intelligence to its broader learning and talent stack.[1]World Economic Forum, “The Future of Jobs Report 2025,” World Economic Forum, weforum.org

Rising Corporate Reskilling and Compliance Training Demand

The Asia Pacific learning management systems market is also benefiting from the growing weight of compliance and workforce reskilling obligations, especially in regulated sectors. Compliance training is no longer treated as a routine administrative task, as firms need audit trails, renewal records, and standardized learning-completion data across dispersed operations. The Hong Kong Institute of Bankers updated its Enhanced Competency Framework for Anti-Money Laundering and Counter-Terrorist Financing in August 2025, requiring practitioners to complete 10-12 continuing professional development hours each year. Hong Kong’s Protection of Critical Infrastructures Ordinance took effect on January 1, 2026, and expanded mandatory cybersecurity training requirements across BFSI, energy, and transport, strengthening the case for enterprise LMS deployment. Manufacturing groups with multi-country factory networks are also using unified platforms to manage safety training and certification at scale, which helps explain why BFSI accounted for 34.13% of 2025 regional revenue, while demand is expanding into other regulated verticals.[2]Hong Kong Institute of Bankers, “Enhanced Competency Framework on Anti-Money Laundering and Counter-Terrorist Financing,” Hong Kong Institute of Bankers, hkib.org

Accelerating Cloud and Mobile-First Learning Adoption

Cloud deployment is becoming the default architecture across the Asia Pacific learning management systems market because it lowers upfront spending and shortens implementation timelines for buyers who cannot support large internal IT projects. Cloud already accounted for 68.62% of revenue in 2025, and its 17.42% forecast CAGR reflects how well the model fits both large institutions and cost-sensitive smaller organizations. In several Southeast Asian markets, mobile devices remain the primary means of internet access for large sections of the workforce, so mobile-responsive learning design is a basic requirement rather than a premium feature. PwC Australia’s firmwide AI foundations training rollout in March 2026 demonstrated how cloud-based delivery can support rapid, standardized capability building across a large professional services workforce. The appeal is especially strong in short budget-cycle environments because SaaS pricing reduces capital outlay and supports staged adoption. This opens the door for vendors that can deliver cloud performance alongside mobile-first design for distributed workers, field staff, and factory teams.[3]Australian Government Department of Education, “Microcredentials Pilot Round 2 Announcement,” Australian Government Department of Education, education.gov.au

Expansion of Hybrid and Distance Learning Across Higher Education

Higher education remains an important demand base for the Asia Pacific learning management systems market because hybrid and distance learning models are no longer temporary operating responses. Institutions across the region now depend on LMS platforms to support routine course delivery, learner engagement, assessment tracking, and shorter non-degree offerings. Japan’s Central Council for Education approved digital textbooks in September 2025, which further embedded digital learning practices in the education system. Earlier infrastructure progress also mattered, as Japan’s GIGA School Program improved the student-device ratio from 6.1:1 in 2019 to 1.1:1 by 2023, creating the conditions for platform scale in schools and colleges. Australia’s government committed AUD 18.5 million (USD 13 million) to the Microcredentials Pilot, with 25 providers and 48 courses supported in Round 2 as of August 2024, tying public funding directly to LMS-enabled credential delivery. The University of Canberra is rolling out microcredentials across both semesters of 2026, indicating that LMS-supported alternative credentials are becoming part of normal institutional operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchy Digital Infrastructure Across Emerging Asia-Pacific Markets | -2.1% | Southeast Asia, including Myanmar, Cambodia, Vietnam, and rural Indonesia | Short term (≤ 2 years) |

| Data Localization and Cross-Border Transfer Rules Complicating Cloud Deployments | -1.8% | China, India, Vietnam, Malaysia | Medium term (2-4 years) |

| Difficulty Proving Training ROI Across Disparate HR and Learning Systems | -1.2% | Global, with concentration in large enterprises across all geographies | Medium term (2-4 years) |

| Multilingual and Pedagogical Localization Burdens Across High-Diversity Markets | -0.9% | India, Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patchy Digital Infrastructure Across Emerging Asia-Pacific Markets

Patchy connectivity remains a practical constraint for the Asia Pacific learning management systems market in several lower-income and frontier locations. Rural Indonesia, Cambodia, Myanmar, and parts of Vietnam continue to face broadband and mobile-network instability, which disrupts asynchronous learning completion and weakens measurable outcomes for enterprise buyers. When learning completion and performance data become unreliable, renewal decisions also become harder for clients who need proof of effectiveness. This creates a 2-speed regional structure in which pricing and delivery models that work in Singapore or Australia do not transfer cleanly to lower-connectivity environments. The result is a commercial advantage for vendors that support offline-first or low-bandwidth use cases, because purely cloud-native designs do not perform as well in these settings. The Asia Foundation’s Go Digital ASEAN program has trained more than 400,000 individuals since 2020, and 90% of participants reported higher confidence in digital tools, indicating that learner demand persists even where infrastructure still limits full LMS deployment.

Data Localization and Cross-Border Transfer Rules Complicating Cloud Deployments

Data localization is another important brake on the Asia Pacific learning management systems market, as it increases implementation complexity for organizations operating across multiple countries. Vendors that once treated APAC as a more unified cloud opportunity now have to deal with local hosting, transfer assessments, and country-specific compliance reviews. Vietnam’s Law on Personal Data Protection took effect on January 1, 2026, and introduced penalties of up to 5% of in-country revenue for non-compliant cross-border transfers. Malaysia’s Cross-Border Privacy Data Transfer Guidelines took effect on April 29, 2025, and require a Transfer Impact Assessment that remains valid for 3 years before data can be transferred out of the country. China’s data security audit measures, effective May 1, 2025, require biennial audits for operators handling data from more than 10 million individuals, which raises the burden on large enterprise deployments. India’s Digital Personal Data Protection framework adds similar friction in regulated sectors, so multinational buyers often end up with multi-vendor or split-architecture models that increase total ownership costs and stretch procurement timelines.[4]Cyberspace Administration of China, “Regulations on Network Data Security Audit Measures,” Cyberspace Administration of China, cac.gov.cn

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate While Services Gain Strategic Weight

Solutions accounted for 80.19% of the Asia-Pacific learning management systems (LMS) market in 2025, underscoring the region's continued preference for platform-led procurement over service-led implementations. Buyers across enterprises and institutions are still prioritizing core software that supports content management, learner tracking, analytics, and administrative workflows in a single environment. This pattern also reflects the maturity of the regional vendor base, because plug-and-play cloud platforms have reduced the heavy upfront customization that once made service-intensive deployments more common. In practical terms, many organizations now expect a working platform much earlier in the buying cycle, which keeps the software layer at the center of the contract. The Asia Pacific learning management systems market continues to reward vendors that can offer clear platform functionality without requiring buyers to depend on lengthy, expensive implementation projects.

At the same time, services are becoming increasingly important as the operating environment around these platforms becomes more complex. Services are projected to expand at a 16.24% CAGR through 2031, reflecting rising demand for configuration, integration, content localization, and ongoing administration. Many buyers in regulated sectors need more than a software subscription, as they also require compliance content updates, workflow tuning, and support for internal reporting. Multi-language delivery across diverse workforces also pushes clients toward external support, especially when internal learning teams are small. The longer-term shift is from project work toward recurring managed services that sit inside broader multi-year platform contracts. That model raises switching costs for buyers and creates steadier recurring revenue for vendors. Cornerstone OnDemand’s May 2024 acquisition of SkyHive showed how leading providers are expanding from software delivery into skills intelligence and broader workforce analytics. The Asia Pacific learning management systems industry is therefore seeing services evolve from a supporting layer into a strategic revenue stream that strengthens retention. This shift matters because clients increasingly want a single provider that can support design, deployment, analytics, and compliance management.

By Deployment: Cloud Becomes The Default Operating Model

Cloud accounted for 68.62% of the Asia-Pacific learning management systems (LMS) market in 2025 and is projected to grow at the fastest pace, with a 17.42% CAGR through 2031. That combination shows that cloud is not only the current standard, but also the format attracting the widest set of new buyers. The appeal comes from predictable subscription costs, faster upgrades, and lower internal infrastructure needs. These benefits matter most to SMEs, mid-sized institutions, and government agencies that need enterprise-grade functionality without a capital-intensive implementation. The Asia Pacific learning management systems market is therefore moving toward cloud as the default architecture for most new deployments, especially where organizations want quick rollout and easier scaling across locations.

Instructure’s April 2026 move to simplify Canvas into Core, Plus, and Next illustrated how vendors are reducing pricing and packaging friction to speed adoption across a broader customer base. On-premises platforms remain relevant in China and Japan, especially in government and regulated finance, where data sovereignty rules continue to support local hosting. Hybrid deployment is also becoming a practical bridge for large organizations that want cloud content delivery but need on-premises control for sensitive employee records. That middle path is useful for enterprises with uneven legacy systems and country-specific compliance rules. It also creates a narrow but meaningful opportunity for vendors that can support split architecture without forcing customers into separate licenses or fragmented administration. In this part of the Asia Pacific learning management systems industry, competitive advantage is now tied less to basic hosting choice and more to how well vendors handle compliance, pricing clarity, and system flexibility. Smaller vendors often struggle here because hybrid architecture requires deeper technical capability and stronger support capacity. As a result, cloud-native vendors are winning new SME and mid-market accounts, while incumbents with on-premises history continue to defend large public-sector and financial contracts.

By Learning Type: Corporate Training Leads While Academic Learning Expands Fast

Corporate training accounted for 38.23% of regional revenue in 2025, making it the largest learning segment in the Asia Pacific learning management systems market. The size of this segment reflects the need for structured training records, audit readiness, and measurable employee development across large organizations. Enterprises are moving away from informal learning methods because those approaches do not produce the data needed for compliance, skills-gap reporting, or internal mobility planning. Formal LMS use also supports standardized delivery across offices, factories, and branch networks, which is especially important for multinational employers operating across several APAC jurisdictions. This keeps corporate training at the center of contract value even as the customer base broadens into other use cases.

Academic learning is projected to grow at 15.61% through 2031, making it the fastest-growing learning type as universities and colleges expand hybrid instruction and shorter credential formats. The University of Canberra’s 2026 microcredential rollout showed that institutions are moving beyond pilot programs and embedding these offerings into regular academic operations. Australia’s AUD 18.5 million (USD 13 million) Microcredentials Pilot also confirmed direct public support for LMS-enabled credential delivery. Government and public training sits on a separate demand track, supported by digital government and civil-service upskilling efforts such as India’s iGOT Karmayogi and Singapore’s public workforce training frameworks. Skills development and certification programs add a further layer of growth, particularly where public funding is linked to credentialed reskilling for workers in transition. In South Korea, K-Digital Training supports this pattern by channeling funding into digital training pathways delivered through platform environments. The Asia Pacific learning management systems market is therefore no longer centered solely on enterprise training, as academic and public-sector use cases are steadily expanding the demand base. The result is a more diversified demand structure where corporate learning remains the anchor, but education and certification use cases are contributing more to future growth. That broader mix also favors vendors that can serve both institutional and workforce training needs without changing core platform logic.

By End User Vertical: BFSI Anchors Revenue While Manufacturing Accelerates

BFSI accounted for 34.13% of the Asia-Pacific learning management systems (LMS) market share in 2025, making it the largest vertical in the region. This lead position is tied to the density of compliance requirements in banking, insurance, and financial services, where firms must document training completion, policy awareness, and periodic certification. In heavily regulated environments, learning platforms are part of operational control rather than optional employee development infrastructure. That is why demand in BFSI tends to remain stable even when broader enterprise technology spending becomes more selective. The Asia Pacific learning management systems market continues to depend on this vertical because compliance obligations create recurring usage and strong contract renewal logic.

Manufacturing and industrial operations are forecast to expand by 16.84% through 2031, making it the fastest-growing vertical and a major shift in the market’s growth profile. This reflects the build-up of training debt around safety, equipment operation, and quality standards on factory floors, especially among distributed workforces that were not historically well served by traditional enterprise learning tools. Mobile-first and bite-sized delivery models are helping manufacturers close that gap, particularly where workers are not desk-based. The Hong Kong Institute of Bankers’ 2025 AML training update illustrated how compliance rules keep BFSI spending consistent, but the same logic of mandatory certification is now spreading into manufacturing, healthcare, and other operational settings. Information technology and telecommunications remain the second-largest contributor due to high employee turnover and the constant need to update technical skills. Healthcare and life sciences adoption is widening beyond baseline compliance toward continuing clinical education, where digital delivery is increasingly accepted. Retail and e-commerce are also adding demand, as frontline workers need structured learning on omnichannel operations and product systems. The education vertical remains important for vendors such as Moodle and Instructure, as institutional contracts can run for several years and support varied teaching models. This mix shows that the Asia Pacific learning management systems market is becoming less dependent on purely office-based learning and more tied to sector-specific operational training needs.

By End User Enterprise Size: Large Enterprises Provide Scale While SMEs Drive Growth

Large enterprises accounted for 65.12% of the Asia-Pacific learning management systems (LMS) market in 2025, reflecting their purchasing power and organizational maturity. These buyers typically have formal learning and development teams, cross-country operations, and stronger internal requirements for compliance tracking and workforce reporting. Many multinationals have standardized platforms across regional offices and production sites, which support large multi-year agreements and predictable recurring revenue for vendors. Large accounts also serve as testing grounds for new platform features such as skills mapping, personalization, and deeper analytics. This makes them strategically important beyond their revenue share because feature development often starts with the needs of these more complex customers.

SMEs are projected to expand at a 17.11% CAGR through 2031, making them the fastest-growing enterprise-size segment in the Asia Pacific learning management systems market. Lower SaaS entry points and easier no-code configurations are helping smaller firms adopt platforms without extensive IT support. LinkedIn’s Economic Graph analysis from August 2025 showed that AI literacy penetration in Asia Pacific SMBs ranged from 0.6% to 2.4%, compared with 4.0% to 12.5% in large enterprises, highlighting the upskilling gap that is now pushing smaller organizations toward more formal digital learning tools. APEC also noted that micro, small, and medium enterprises account for more than 97% of businesses in the region, contribute 40% to 60% of GDP, and employ more than 50% of the workforce. Those structural fundamentals make SMEs essential for long-run regional scale, even if their contracts are smaller and more price-sensitive. At the same time, this segment carries more volatility because subscription spending can be cut more quickly during periods of economic stress. Vendors that serve SMEs well, therefore, need simple onboarding, clear returns on investment, and pricing models that do not create lock-in concerns. The Asia Pacific learning management systems industry is likely to see margin expansion from this segment, as vendors can keep customer acquisition and support costs tightly controlled. That balance between broad SME demand and higher churn risk will remain an important competitive filter across the forecast period.

Geography Analysis

China held 32.81% of the Asia-Pacific learning management systems market share in 2025, making it the largest country market in the region. That position reflects not only its scale, but also the maturity of its domestic e-learning ecosystem and the protection that local data-residency rules provide to homegrown vendors. Platforms such as Qixuebao and Yunxuetang have established strong positions in personalized learning, AI-supported delivery, and mobile-first formats that meet local enterprise needs. China’s data security audit measures, effective May 1, 2025, require biennial compliance reviews for operators handling personal data from more than 10 million individuals, reinforcing the case for local deployment and strengthening the regulatory moat around domestic providers. State-supported vocational and enterprise training programs tied to labor and workforce policy also help sustain demand even when private-sector conditions soften.

India is projected to expand at a 15.95% CAGR through 2031, which makes it the fastest-growing geography in the Asia-Pacific learning management systems market. Growth is supported by the National Education Policy 2020 and broader moves toward outcome-based learning and competency mapping in higher education. The regulatory pull is evident in accreditation-linked practices, such as CO-PO mapping and academic quality review requirements, that are pushing institutions away from legacy systems. Japan remains anchored in enterprise training, and its Financial Services Agency issued cybersecurity supervisory guidelines in October 2024 that required security training across regulated financial institutions. South Korea is also moving forward through public reskilling support and channel expansion, with Canvas entering the country through a Linus Technology partnership in June 2025. Australia and Singapore continue to provide among the clearest public demand signals among developed markets. Australia backed microcredentials with AUD 18.5 million (USD 13 million) in pilot funding. Singapore committed SGD 400 million (USD 299 million) in Financial Sector Development Fund grants for training and skills development.

Malaysia and Thailand are consolidating on cloud-first deployment models, though compliance rules are shaping vendor selection and hosting decisions. Malaysia’s cross-border privacy transfer guidelines, which took effect on April 29, 2025, have pushed more buyers toward locally compliant or regionally hosted platforms. Moodle’s September 2025 decision to elevate ModernLMS to Premium Partner status in Malaysia underscores the growing importance of channel depth in this part of the region. The rest of Asia Pacific, including Indonesia, Vietnam, the Philippines, and frontier markets, offers the highest long-term upside but also the highest infrastructure risk, which is why programs such as Go Digital ASEAN continue to matter for expanding the effective learner base in less mature procurement environments.

Competitive Landscape

The Asia-Pacific learning management systems market is moderately concentrated among well-known global platforms, but it remains fragmented when domestic and regional vendors are included. Cornerstone OnDemand, Instructure, Moodle, Docebo, and D2L compete mainly on integration depth, personalization features, and the breadth of reporting needed by large enterprise and institutional buyers. At the same time, local vendors in China and India retain structural strengths because they are better aligned with national data-residency rules and public procurement channels. This creates a competitive structure in which scale matters, but local compliance fit can matter just as much. The Asia Pacific learning management systems market, therefore, does not reward scale alone, as vendors must also align with language needs, pedagogical preferences, and country-specific hosting expectations.

Competition is also shifting away from simple feature comparison and toward ecosystem control. Cornerstone’s expanded partnership with Cognota in March 2026 added learning design automation to its platform, which supports faster course development for enterprise learning teams. Its May 2026 partnership with Questionmark extended that strategy into regulated-industry assessment and stronger compliance validation. Instructure took a different but equally strategic route when it broadly released Canvas Career in January 2026, linking academic learning outcomes with career pathways and graduate employability tracking. These moves show that leading vendors are trying to own more of the workflow for learning, assessment, skills mapping, and employment outcomes, rather than competing only on course delivery.

Geographic reach versus local depth forms a second line of competition across the Asia Pacific learning management systems market. Instructure’s Asia regional hub in the Philippines and its earlier South Korea channel entry showed how global vendors are investing in local coverage, even as domestic providers have traditionally held the advantage. There is still open space in mobile-first manufacturing training, public workforce programs across Southeast Asia, and microcredential delivery for higher education institutions. Smaller providers such as iSpring Solutions and eloomi are finding room in cost-sensitive mid-market accounts, while firms such as OpenLearning and Coursemos are more representative of regional realities than companies like Meridian Knowledge Solutions and Kallidus, which have limited documented presence in this geography. The vendors most likely to sustain advantage will be those that can combine compliance, mobile delivery, and skills intelligence within a commercially simple platform across multiple jurisdictions.

Asia-Pacific Learning Management Systems (LMS) Industry Leaders

Blackboard LLC

Cornerstone OnDemand

Instructure Holdings, Inc

D2L Inc.

Moodle Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cornerstone OnDemand partnered with Questionmark to integrate LMS workflows and assessment tools for compliance-heavy sectors like BFSI and healthcare.

- April 2026: Instructure simplified Canvas into Core, Plus, and Next tiers, easing adoption for SMEs and mid-market institutions.

- March 2026: Moodle and Accipio expanded managed services and content development to New Zealand, targeting corporate LMS demand.

- March 2026: Cornerstone OnDemand deepened its partnership with Cognota, adding learning design automation to accelerate course development and focus on compliance and skills content.

Asia-Pacific Learning Management Systems (LMS) Market Report Scope

The Asia-Pacific Learning Management Systems (LMS) market refers to technology platforms that enable enterprises, institutions, and public organizations to deliver, track, and manage digital learning, compliance training, and skills development. It integrates content, analytics, and workforce capability mapping, supporting cloud, hybrid, and mobile-first deployments across diverse regional sectors.

The Asia-Pacific Learning Management Systems (LMS) Market is segmented by Component (Solutions and Services), Deployment (Cloud, On-Premises, and Hybrid), Learning Type (Academic Learning, Corporate Training, Government/Public Training, and Skill Development/Certification), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Industry Vertical (Information Technology and Telecommunications, Banking Financial Services and Insurance, Healthcare and Life Sciences, Manufacturing and Industrial Operations, Retail and E-commerce, Education, Government and Public Sector, Energy and Utilities, and Media and Entertainment), and Geography (China, India, Japan, South Korea, Singapore, Malaysia, Thailand, Australia, and Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Academic Learning |

| Corporate Training |

| Government / Public Training |

| Skill Development / Certification |

| Information Technology (IT) and Telecommunications |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing and Industrial Operations |

| Retail and E-commerce |

| Education |

| Government and Public Sector |

| Energy and Utilities |

| Media and Entertainment |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| China |

| India |

| Japan |

| South Korea |

| Singapore |

| Malaysia |

| Thailand |

| Australia |

| Rest of Asia-Pacific |

| By Component | Solutions |

| Services | |

| By Deployment | Cloud |

| On-premises | |

| Hybrid | |

| By Learning Type | Academic Learning |

| Corporate Training | |

| Government / Public Training | |

| Skill Development / Certification | |

| By End User Vertical | Information Technology (IT) and Telecommunications |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Manufacturing and Industrial Operations | |

| Retail and E-commerce | |

| Education | |

| Government and Public Sector | |

| Energy and Utilities | |

| Media and Entertainment | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Singapore | |

| Malaysia | |

| Thailand | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the size of the Asia-Pacific learning management systems market in 2026 and 2031?

The Asia-Pacific learning management systems market stands at USD 8.90 billion in 2026 and is forecast to reach USD 18.16 billion by 2031, growing at a CAGR of 15.33%.

Which deployment model leads adoption across the region?

Cloud leads deployment with a 68.62% share in 2025 and is also the fastest-growing model, with a projected CAGR of 17.42% through 2031.

Which customer group is driving the strongest future demand?

SMEs are expected to expand at a 17.11% CAGR through 2031, while large enterprises still account for the biggest revenue base with a 65.12% share in 2025.

Which vertical contributes the most revenue today?

BFSI is the leading vertical with a 34.13% share in 2025 because compliance and certification needs create steady and recurring LMS demand.

Which country leads the region and which one is growing fastest?

China holds the largest regional share at 32.81% in 2025, while India is the fastest-growing country market with a projected CAGR of 15.95% through 2031.

Why are services becoming more important for vendors?

Services are projected to grow at a 16.24% CAGR through 2031 as buyers increasingly need integration, localization, administration, and compliance support alongside software licenses.

Page last updated on: