Federated Learning In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

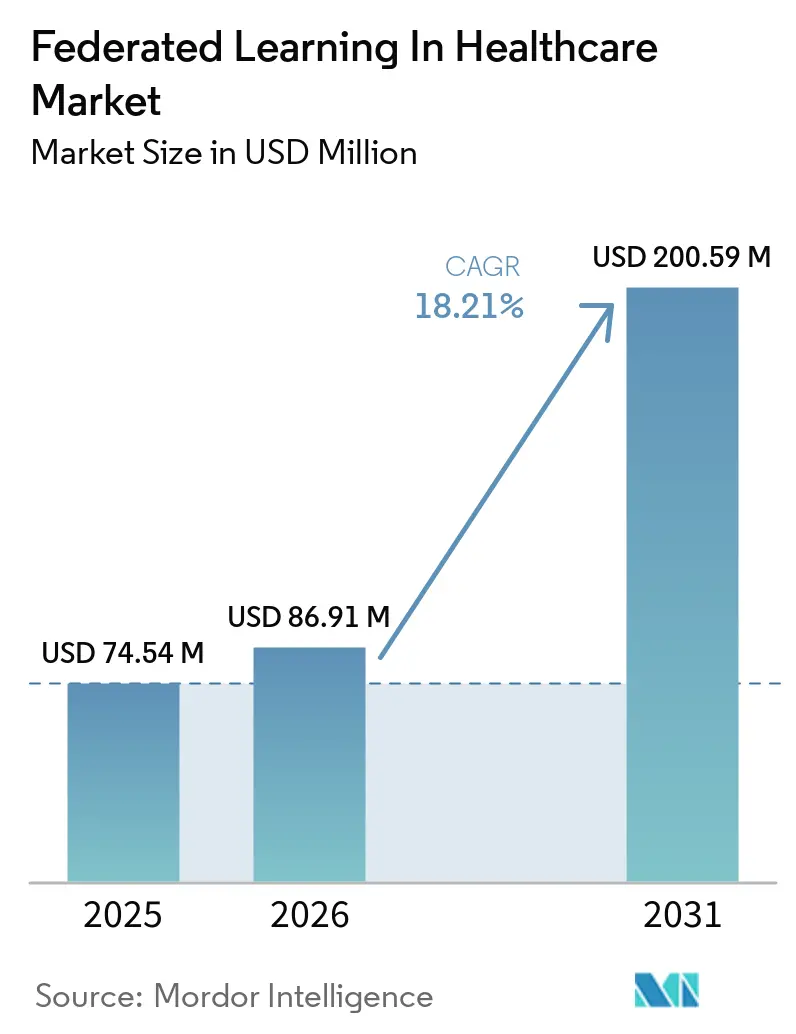

| Market Size (2026) | USD 86.91 Million |

| Market Size (2031) | USD 200.59 Million |

| Growth Rate (2026 - 2031) | 18.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Federated Learning In Healthcare Market Analysis by Mordor Intelligence

The Federated Learning In Healthcare Market size is projected to be USD 74.54 million in 2025, USD 86.91 million in 2026, and reach USD 200.59 million by 2031, growing at a CAGR of 18.21% from 2026 to 2031.

The federated learning in healthcare market is moving from pilot work to production infrastructure as hospitals, research centers, and drug developers look for ways to build AI models without moving sensitive patient data outside local control. Privacy rules under HIPAA, GDPR, and the European Health Data Space are making centralized data pooling harder to sustain, so distributed learning is becoming part of compliance design rather than only a technical option. The Federated learning in healthcare market is also benefiting from confidential computing tools that protect data while it is being processed, which is reducing a major barrier to cloud adoption for regulated workloads. Competition is tightening as leading vendors combine compute, orchestration, privacy controls, and managed services in one stack, which raises the pressure on stand-alone analytics providers to match enterprise performance and governance expectations. The forecast still depends on how well the Federated learning in healthcare market can manage non-IID clinical data, model drift, and legacy hospital system integration in real deployment environments.

Key Report Takeaways

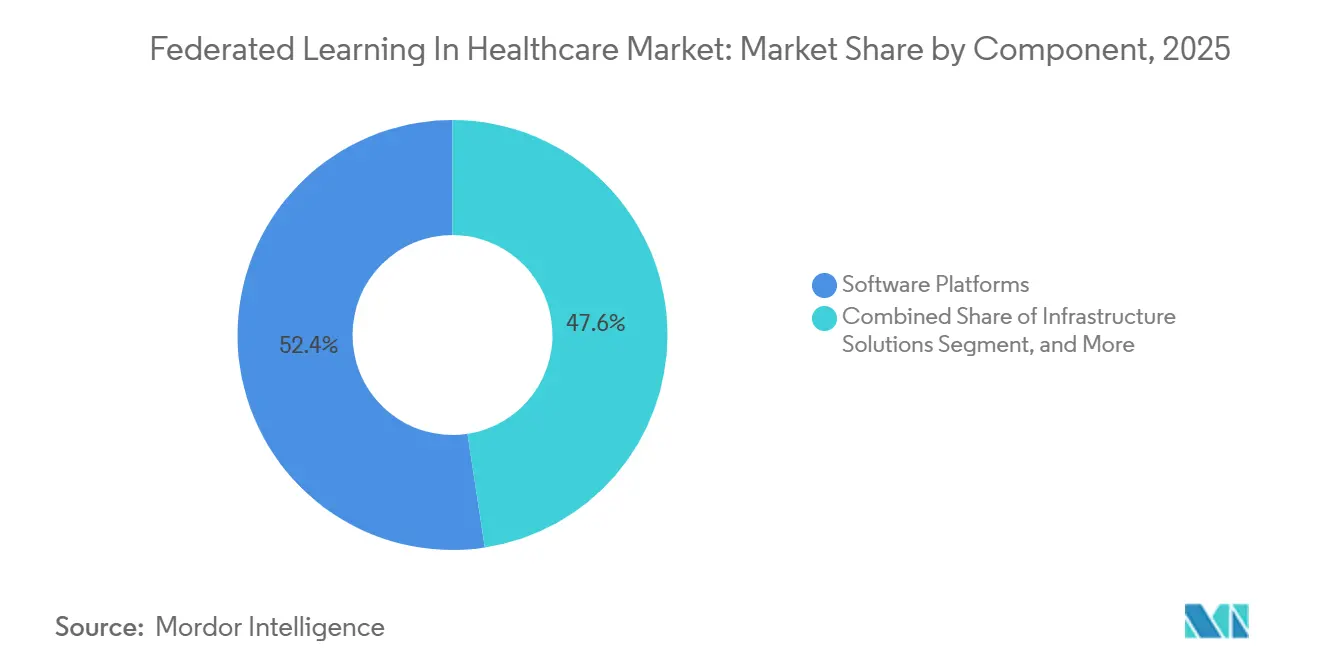

- By component, software platforms led with 52.38% revenue share in 2025, while services recorded the highest projected CAGR at 19.16% through 2031.

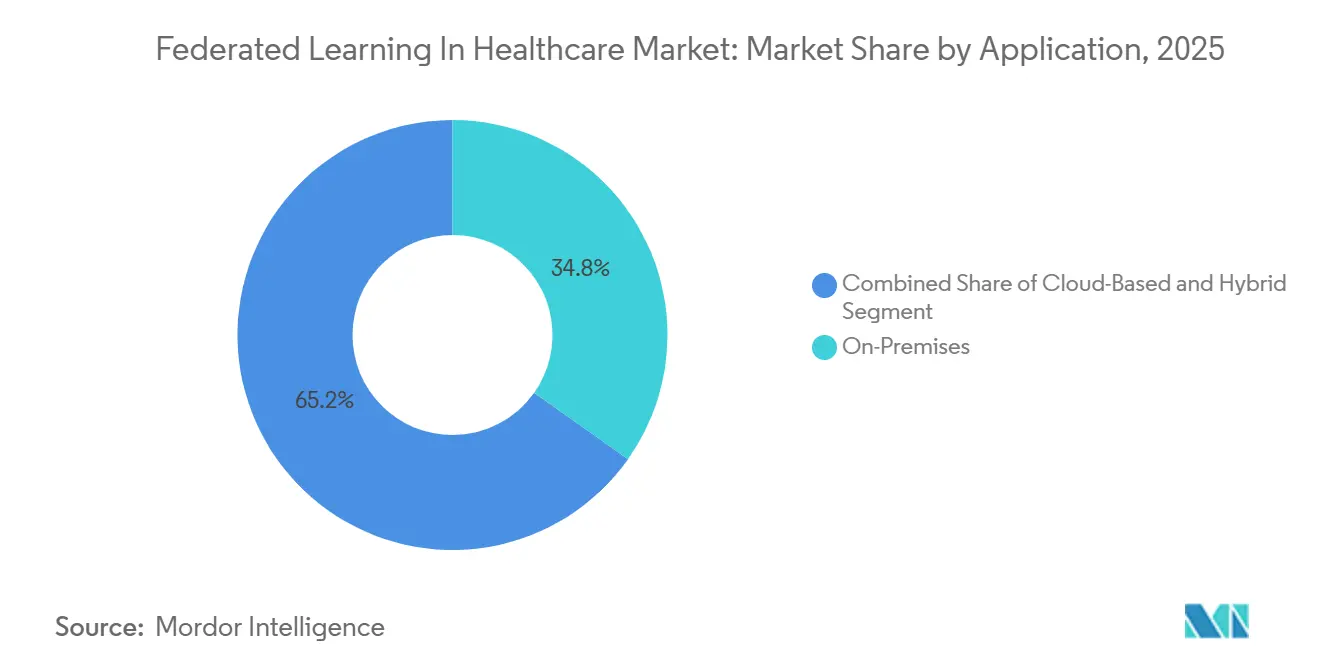

- By deployment mode, on-premises held 57.61% share in 2025, while cloud-based deployment is forecast to expand at an 18.83% CAGR through 2031.

- By application, medical imaging and diagnostics accounted for 34.83% share in 2025, while drug discovery and development is advancing at a 19.85% CAGR through 2031.

- By end user, hospitals and health systems represented 38.92% share in 2025, while pharmaceutical and biotechnology companies posted the highest projected CAGR at 19.15% through 2031.

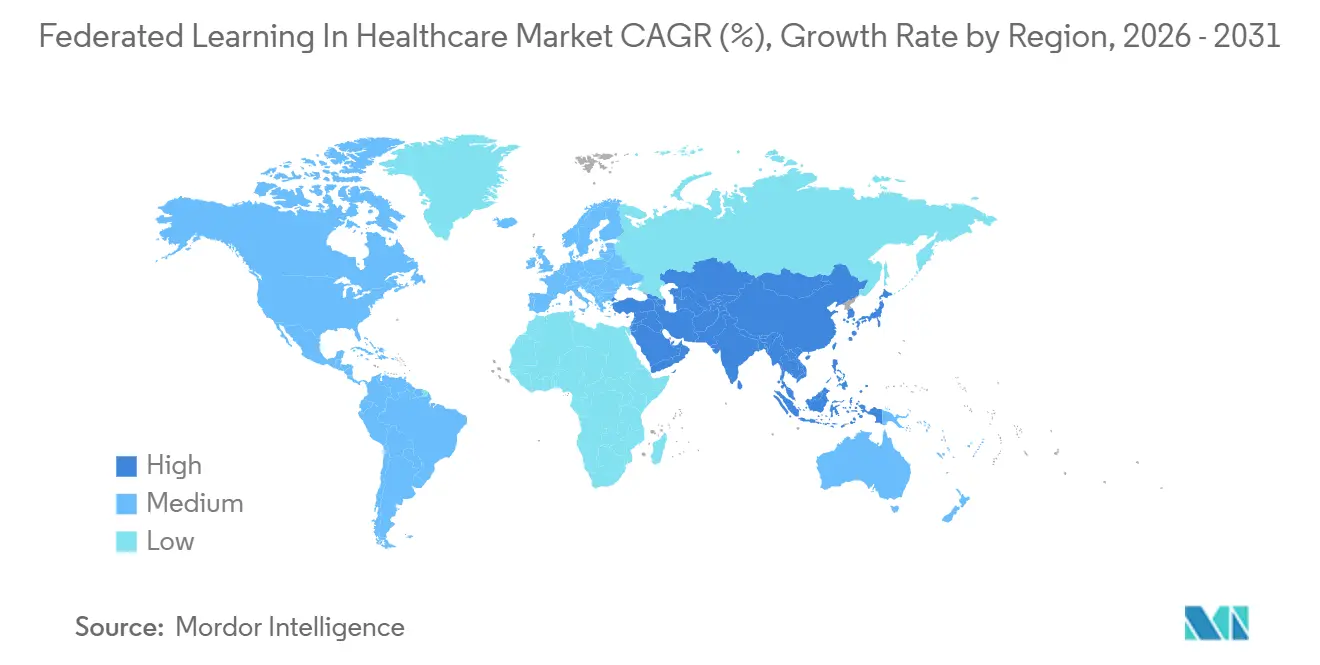

- By geography, North America held 41.42% share in 2025, while Asia-Pacific is forecast to grow at an 18.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Federated Learning In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Regulation-Driven Decentralized AI Adoption | +3.5% | Global, with strong relevance in the US and Europe | Short term (≤ 2 years) |

| Multi-Institution Imaging Model Scaling Without Data Pooling | +2.8% | North America and Europe | Short term (≤ 2 years) |

| Biopharma Demand for Privacy-Safe Collaborative Drug Discovery | +2.5% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Cloud and Confidential Computing Stack Maturity | +2.0% | Global, led by North America | Medium term (2-4 years) |

| EHDS-Enabled Cross-Border Secondary-Use Pathways | +1.8% | Europe, with spillover to nearby markets | Medium term (2-4 years) |

| Federated AI Registries and Algorithmic Vigilance Networks | +1.2% | Global, with early activity in the US, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy Regulation-Driven Decentralized AI Adoption

Data protection rules have moved from background compliance work into core architecture decisions across the Federated learning in healthcare market. Hospitals and health networks in the United States and Europe are under rising pressure to avoid raw patient-data transfers across institutional and national boundaries, which makes centralized AI training harder to justify in clinical settings.[1]European Commission Directorate-General for Health and Food Safety, “Regulation (EU) 2025/327 on the European Health Data Space,” European Commission, health.ec.europa.eu A 2026 study in Scientific Reports showed that a federated framework using differential privacy and homomorphic encryption reduced membership-inference risk from 20% to 5% against non-private federated baselines, which supports the case for privacy-safe model development without a major utility tradeoff. European policy is pushing this shift further because the EHDS creates a formal structure for secondary use and cross-border access that aligns more naturally with distributed analytics than with raw data pooling. This is creating multi-year software buying cycles as providers look for platforms that already contain auditability, traceability, and governance controls. For smaller hospitals and regional systems, the Federated learning in healthcare market is especially attractive when vendors can absorb legal, technical, and workflow complexity through managed deployment models.

Multi-Institution Imaging Model Scaling Without Data Pooling

Imaging has become one of the clearest early demand centers in the Federated learning in healthcare market because radiology and pathology data are both valuable and difficult to share. Traditional multi-site imaging collaborations often slow down at contracting, liability review, and local governance approval, which can delay or stop pooled-data model training. A February 2026 study in npj Digital Medicine found that combining federated learning with a traveling-model approach across multiple sites reduced misclassification disparities from 34% to 26% while also improving balanced accuracy, which shows that distributed training can improve both robustness and fairness.[2]R. Souza et al., “Combining Federated Learning and Travelling Model Boosts Performance and Opens Opportunities for Digital Health Equity,” npj Digital Medicine, nature.com GE HealthCare’s work with Mass General Brigham and the University of Wisconsin-Madison on a 3D MR foundation model trained on more than 200,000 multi-site images shows that health systems are starting to treat imaging archives as shared training infrastructure rather than isolated local assets. That raises the bar for vendors that still depend on single-site datasets, especially in radiology and pathology, where performance gaps can become visible quickly. As a result, the Federated learning in healthcare market is seeing imaging-led adoption not only because privacy matters, but also because model quality now improves when more institutions can participate without surrendering raw scans.

Biopharma Demand for Privacy-Safe Collaborative Drug Discovery

Drug discovery is opening a second major demand lane for federated learning in healthcare market because no large pharmaceutical company wants to hand over raw compound data to direct peers. Federated training changes that equation by letting partners collaborate at the model layer while retaining control over proprietary structures, labels, and downstream intellectual property. In July 2025, Elix and LINC commercialized an AI drug discovery platform that used federated-learning models trained across 16 pharmaceutical companies with the kMoL library developed with Kyoto University, which showed that industrial-scale federated collaboration had moved beyond research pilots. The FLuID framework reported in Nature Chemical Engineering in April 2025 also showed that knowledge-distillation-based federated approaches improved ADMET and binding-affinity prediction across institutions without exchanging molecular structures.[3]C. Li, “Breaking Data Silos in Drug Discovery with Federated Learning,” Nature Chemical Engineering, nature.com Eli Lilly has already pushed this model into production through TuneLab on NVIDIA FLARE, giving biotech partners access to strong models while keeping partner data local and protected. This is why the Federated learning in healthcare market is drawing capital from biopharma even when data sharing remains commercially sensitive, because collaboration can now improve models without exposing the underlying assets that create competitive advantage.

Cloud and Confidential Computing Stack Maturity

The federated learning in healthcare market is also gaining traction because cloud providers and chip vendors have improved the security model for data-in-use protection. Trusted execution environments such as Intel TDX, AMD SEV-SNP, and confidential computing GPUs create isolated compute environments where participants can verify that training runs inside protected hardware boundaries. A March 2026 paper in Scientific Reports showed that confidential-computing-enabled federated frameworks outperformed standard federated baselines on cross-institutional biomedical benchmarks while also reducing gradient leakage attack surfaces. This matters for hospitals because earlier objections to cloud deployment were often tied to who could inspect memory during active processing rather than to data-at-rest controls. The commercial stack is also broadening as confidential AI vendors extend protection across training, fine-tuning, inference, and agent workflows, which supports longer-term enterprise adoption. For the Federated learning in healthcare market, that means cloud growth is no longer only a cost argument, because the security posture is moving closer to what hospital governance teams require for regulated clinical workloads.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Non-IID Clinical Data Heterogeneity and Model Drift | -2.5% | Global | Short term (≤ 2 years) |

| Legacy EHR and PACS Integration Burden | -2.0% | North America and Europe | Medium term (2-4 years) |

| Site-Level GPU, MLOps, and Networking Cost Burden | -1.5% | Emerging Asia-Pacific markets and smaller facilities globally | Medium term (2-4 years) |

| Model IP, Liability, and Contributor-Value Allocation Disputes | -1.0% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Non-IID Clinical Data Heterogeneity and Model Drift

The most persistent technical restraint in the federated learning in healthcare market is the mismatch between clinical datasets collected at different sites. Hospitals vary in imaging protocols, device vendors, coding behavior, patient mix, and label quality, so standard aggregation methods do not always deliver a model that generalizes evenly across all participants. Research from the Federated Tumor Segmentation challenge, published in Nature Communications in April 2025, found that adaptive aggregation algorithms could perform well on average across a federation while still showing meaningful performance drops at specific institutions. That means average federation performance can mask local risk, which is a serious issue when clinical teams need dependable results at each hospital rather than only a strong pooled benchmark. Early 2026 work on drift-aware fine-tuning points in a better direction, but it also shows that site-level tuning sensitivity remains a live issue in medical settings. As a result, the federated learning in healthcare market still favors well-resourced academic centers and large health systems that can maintain per-site monitoring, recalibration, and validation workflows over time.

Legacy EHR And PACS Integration Burden

Legacy integration remains a major brake on deployment because the federated learning in healthcare market depends on strong local data pipelines at every participating site. Many hospitals still run on older HL7 interfaces, siloed PACS environments, and EHR architectures that were not built to expose consistent structured data to external model orchestration layers. A 2025 paper in the International Journal of Computer Assisted Radiology and Surgery showed that federated frameworks for multimodal health data must bridge major architectural differences between tabular EHR records and high-dimensional DICOM imaging, and there is still no universally deployed system that handles both smoothly in one model workflow. Another 2025 study in BMC Medical Informatics and Decision Making showed that interoperability-aware metadata pipelines remain necessary to enable federated analyses across fragmented health IT environments. This means providers often need FHIR R4 preprocessing, OMOP harmonization, and structured DICOM reporting before a single training round can run reliably. In the Federated learning in healthcare market, the engineering burden lengthens timelines, raises deployment cost, and gives an advantage to vendors that already understand hospital workflow complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Anchor Deployment, Services Accelerate Adoption

Software platforms held 52.38% of component revenue in 2025, which gave this layer the largest position in the Federated learning in healthcare market. The leading demand driver was the need for orchestration, model aggregation, privacy tooling, and governance functions that hospitals could procure as a supported product instead of assembling internally. Procurement behavior also favored software because many providers wanted a turnkey environment that could fit existing compliance processes without requiring a deep in-house federated engineering team. Open-source frameworks such as NVIDIA FLARE, Flower, and PySyft have widened technical access, but they have also increased pressure on commercial vendors to differentiate through workflow integration, monitoring, auditability, and implementation support.

Services is the fastest-growing component segment, with the federated learning in healthcare market size for services projected to expand at 19.16% CAGR between 2026 and 2031. That pace reflects the fact that many institutions can buy software, but still need outside help for configuration, validation, governance mapping, training operations, and ongoing MLOps support. Managed delivery is becoming more important because healthcare buyers want accountable deployment outcomes rather than only access to a software license. This is also why service scope is moving past implementation into runtime operations, as vendors increasingly support inference routing, monitoring, and federation management across distributed environments. Over time, the Federated learning in healthcare market is likely to see services narrow the distance with software revenue as providers treat federated AI as managed infrastructure rather than as a tool set they operate entirely on their own.

By Deployment Mode: On-Premises Leads, Cloud Closes the Trust Gap

On-premises deployment held 57.61% share in 2025, which made it the leading mode in the federated learning in healthcare market. That result reflected long-standing hospital preferences for keeping protected health information inside institutional boundaries and extending existing PACS, storage, and local GPU investments into new AI workflows. For many academic medical centers, on-premises deployment was a natural continuation of earlier imaging analytics and research infrastructure rather than a completely new capital decision. Risk officers also tended to prefer local control because it simplified internal approval and reduced concern over third-party access during model development.

Cloud-based deployment is the fastest-growing mode, with the federated learning in healthcare market size for cloud-based deployment projected to expand at 18.83% CAGR through 2031. Growth is being supported by confidential computing tools that let hospitals protect data during active processing and verify workload integrity in shared infrastructure. Europe is also creating a regulatory pathway for cloud-resident secure processing environments as health data access frameworks mature, which lowers policy uncertainty for providers evaluating hybrid and remote orchestration models. Hybrid deployment is therefore gaining ground across multi-site networks that want cloud-level coordination while still keeping local computation and raw data on site. In the Federated learning in healthcare industry, deployment choices are becoming less about cloud versus local ideology and more about which model best matches governance, scale, and integration readiness.

By Application: Imaging Leads, Drug Discovery Drives the Next Growth Cycle

Medical imaging and diagnostics commanded 34.83% of application revenue in 2025. Imaging reached that position because radiology data is highly sensitive, clinically rich, and already tied to mature benchmark tasks that adapt well to distributed model development. The 2025 Federated Tumor Segmentation work in Nature Communications and the federated ultrasound foundation model work in npj Digital Medicine both showed that imaging-focused federated research had advanced beyond basic proof of concept into stronger validation across multiple institutions and modalities. That combination of privacy needs and technical maturity keeps imaging at the front of current commercialization.

Drug discovery and development is the fastest-growing application, with the Federated learning in healthcare market size for this segment projected to expand at 19.85% CAGR through 2031. Growth reflects a strong pharmaceutical need to train on broader molecular and biological diversity without exposing raw compound structures to collaborators or competitors. The Elix and LINC commercialization across 16 pharmaceutical companies showed that multi-party federated drug discovery had become commercially credible, not only academically interesting. EHR and clinical data analytics, clinical trial optimization, and remote patient monitoring are also advancing as organizations search for privacy-safe ways to generate clinical evidence across distributed records. Across the federated learning in healthcare market, applications that combine strong privacy pressure with high-value multi-site data are moving fastest from testing into repeatable deployment.

By End User: Hospitals Dominate, Pharma and Biotech Grow Fastest

Hospitals and health systems represented 38.92% of end-user spending in 2025 and held the largest share of the Federated learning in healthcare market. Their lead reflects a practical need to train clinically useful AI models on local patient cohorts without taking on the legal and governance burden of exporting raw records across institutional boundaries. Large academic medical centers remain the most active buyers because they combine research mandates, high imaging volume, specialist clinical teams, and stronger internal data governance resources. Smaller hospitals are participating more often through consortia and partner networks rather than through independent platform ownership, which keeps procurement concentrated among better-resourced systems.

Pharmaceutical and biotechnology companies are the fastest-growing end-user group, with the Federated learning in healthcare market size for this segment projected to rise at 19.15% CAGR from 2026 to 2031. Drug discovery, clinical trial design, and regulatory science are all pulling demand upward because these workflows benefit from broader data exposure without requiring full data exchange. A 2025 pilot involving the FDA, Swissmedic, and the Danish Medicines Agency showed that regulators themselves are evaluating federated pipelines for pharmacovigilance, which strengthens the compliance case for decentralized data collaboration across the drug development chain. Research and academic institutions remain important participants, especially in rare disease and multicenter clinical research, where no single site has enough volume to train strong models alone. Diagnostic laboratories, imaging networks, and contract research organizations are also using federated learning in the healthcare market to join multi-site collaborations while preserving control over their own data assets.

Geography Analysis

North America held 41.42% of the federated learning in healthcare market share in 2025, which made it the largest regional contributor. The region benefits from a dense concentration of academic medical centers, established HIPAA-driven governance processes, and early commercial deployment of federated platforms in healthcare and life sciences. The US remains the core revenue center because it combines strong AI infrastructure, active enterprise software adoption, and visible production examples such as NVIDIA FLARE in biomedical and pharmaceutical settings. Canada is also contributing through research-led collaboration models, while Mexico remains earlier in adoption because hospital digitization and advanced analytics infrastructure are less mature across many provider environments.

Europe is gaining structural weight in the federated learning in healthcare market because policy design is directly shaping infrastructure demand. Regulation (EU) 2025/327 established the European Health Data Space, set up Health Data Access Bodies in each member state, and formalized HealthData@EU for cross-border secondary use, which makes federated infrastructure central to future data access workflows. Germany has moved faster than most peers in national preparation, building on the Gesundheitsdatennutzungsgesetz and related work around research data infrastructure and interoperability roles. This gives Europe a different market profile from North America because adoption is not only enterprise-led, it is also being shaped by public regulatory architecture. That dynamic should support procurement of governance-rich platforms, secure processing environments, and cross-border federation tools over the forecast period.

Asia-Pacific is the fastest-growing region, and the federated learning in healthcare market size for Asia-Pacific is projected to expand at 18.61% CAGR through 2031. South Korea’s March 2026 plan for a national medical data space shows how public policy is starting to mirror the federated model by keeping raw data inside each hospital while enabling secure multi-institutional AI development. Taiwan is also notable because its national healthcare federated learning initiative uses NVIDIA FLARE, which shows that state-backed adoption can accelerate once a common orchestration layer is selected. China offers large potential, but local data rules favor architectures that preserve domestic control and often support on-premises federation rather than broader cross-border pooling. India and Australia remain earlier-stage markets centered on academic medical centers and cancer research networks, while the Middle East and Africa demand is being shaped by GCC digital health spending, and South America is led by Brazil under privacy conditions that resemble European-style data protection expectations.

Competitive Landscape

The federated learning in healthcare market remains moderately fragmented, with large technology groups and specialist federated vendors competing from different starting points. NVIDIA, Google, Microsoft, IBM, and Intel bring compute, cloud, and foundational software layers, while Owkin, Rhino Federated Computing, Flower Labs, Duality Technologies, FedML, and Secure AI Labs compete more directly on federation workflows, privacy tooling, and governance features. This creates a bifurcated structure where scale players own infrastructure depth, and specialists try to win on implementation speed, compliance alignment, and healthcare-specific usability. The Federated learning in healthcare market is therefore not dominated by one platform, but it is increasingly shaped by vendors that can cover more of the stack. NVIDIA FLARE has become especially influential because it appears in both pharmaceutical and public-health implementations, which strengthens its role as an orchestration reference point across the ecosystem.

Competitive positioning is shifting toward vertically integrated offerings. Eli Lilly’s February 2026 launch of LillyPod connected NVIDIA FLARE with DGX SuperPOD compute and TuneLab drug discovery workflows, which showed how hardware, software, and secure collaboration can now be packaged into one enterprise environment. Owkin is pursuing a different route by building durable access to federated patient-data networks through long-term health system relationships, including its July 2025 partnership with Newcastle upon Tyne Hospitals NHS Foundation Trust and its May 2026 licensing agreement with AstraZeneca. GE HealthCare is using its imaging footprint and PACS familiarity to extend into federated imaging workflows, which is a credible move because workflow integration remains one of the hardest barriers for buyers to solve internally. These moves show that the federated learning in healthcare market is rewarding vendors that can combine technical performance with deployment trust and workflow fit.

White space remains open in several parts of the federated learning in healthcare market. Smaller hospitals still need federated learning as a service because many do not have dedicated MLOps teams or the budget for site-level engineering staff. There is also room for federation-level model monitoring, drift surveillance, and contributor-value attribution tools because these functions remain underdeveloped relative to training orchestration. European regulation will increase the value of platforms that already support secure data access, governance documentation, and cross-entity coordination, which should strengthen vendors with mature compliance features. Overall, the federated learning in healthcare market is competitive enough to remain dynamic, but concentrated enough that ecosystem control is beginning to matter more than isolated software features.

Federated Learning In Healthcare Industry Leaders

GE HealthCare Technologies Inc.

IBM Corporation

NVIDIA Corporation

Owkin

Secure AI Labs Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Owkin signed a three-year licensing agreement with AstraZeneca for its K Pro AI Scientist platform, committing to build specialised biopharma AI agents integrated within AstraZeneca's internal IT and decision workflows, expanding a prior collaboration on AI-based gBRCA mutation prescreening in breast cancer.

- May 2026: Opaque Systems acquired post-quantum cryptographic AI technologies from Abu Dhabi's Technology Innovation Institute, following its USD 24 million Series B at a USD 300 million valuation, extending confidential AI capabilities across training, fine-tuning, inference, and agentic workloads with quantum-safe encryption.

- March 2026: South Korea's government announced plans to build a national medical data space for secure multi-institutional medical AI development, with data remaining within each hospital under CSAP-certified cloud environments and only pseudonymised outputs extractable.

- February 2026: Eli Lilly launched LillyPod, the world's first NVIDIA DGX SuperPOD with DGX B300 systems, 1,000+ Blackwell Ultra GPUs, and 9,000+ petaflops, deploying NVIDIA FLARE for TuneLab, a federated drug discovery platform giving biotech partners access to models trained on over USD 1 billion of Lilly data.

Global Federated Learning In Healthcare Market Report Scope

The federated learning in healthcare market encompasses the software, platforms, and services that enable multiple healthcare organizations, such as hospitals, clinics, and research institutes to collaboratively train artificial intelligence and machine learning models without transferring or exposing sensitive, raw patient data

The federated learning in healthcare market is comprehensively segmented across multiple dimensions, reflecting the diverse ecosystem of technologies and stakeholders driving its growth. By component, the market includes software platforms, infrastructure solutions, and services that enable federated learning adoption. In terms of deployment mode, organizations are implementing solutions through on‑premises, cloud‑based, and hybrid models depending on their operational needs. The applications of federated learning span drug discovery and development, medical imaging and diagnostics, electronic health records (EHR) and clinical data analytics, remote patient monitoring, and clinical trial optimization. The end‑user base is equally broad, encompassing hospitals and health systems, pharmaceutical and biotechnology companies, research and academic institutions, diagnostic laboratories and imaging networks, as well as contract research organizations. Finally, the market is analyzed across geographies, including North America, Europe, Asia‑Pacific, the Middle East & Africa, and South America. Forecasts for all these segments are provided in terms of value (USD), offering a clear view of the financial outlook and growth potential of federated learning in healthcare.

| Software Platforms |

| Infrastructure Solutions |

| Services |

| On-Premises |

| Cloud-Based |

| Hybrid |

| Drug Discovery & Development |

| Medical Imaging & Diagnostics |

| Electronic Health Record & Clinical Data Analytics |

| Remote Patient Monitoring |

| Clinical Trial Optimization |

| Hospitals & Health Systems |

| Pharmaceutical & Biotechnology Companies |

| Research & Academic Institutions |

| Diagnostic Laboratories & Imaging Networks |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platforms | |

| Infrastructure Solutions | ||

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud-Based | ||

| Hybrid | ||

| By Application | Drug Discovery & Development | |

| Medical Imaging & Diagnostics | ||

| Electronic Health Record & Clinical Data Analytics | ||

| Remote Patient Monitoring | ||

| Clinical Trial Optimization | ||

| By End User | Hospitals & Health Systems | |

| Pharmaceutical & Biotechnology Companies | ||

| Research & Academic Institutions | ||

| Diagnostic Laboratories & Imaging Networks | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of federated learning in healthcare?

Adoption is being driven by stricter privacy regulation, demand for cross-site AI training without raw data transfer, and better confidential computing support for regulated workloads.

How large is federated learning in healthcare expected to become by 2031?

The sector is forecast to reach USD 200.59 million by 2031, up from USD 86.91 million in 2026, at an 18.21% CAGR over 2026-2031.

Which application area leads current demand?

Medical imaging and diagnostics leads current demand with a 34.83% revenue share in 2025 because imaging data is both sensitive and well suited to multi-site model training.

Which end users are spending the most on these platforms?

Hospitals and health systems led spending with 38.92% share in 2025 because they need clinically strong AI without exporting patient records across organizational boundaries.

Why is cloud deployment rising if hospitals still prefer on-premises setups?

Cloud deployment is growing because confidential computing now protects data during active processing, reducing a major trust barrier for regulated healthcare workloads.

Page last updated on: