South Korea Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

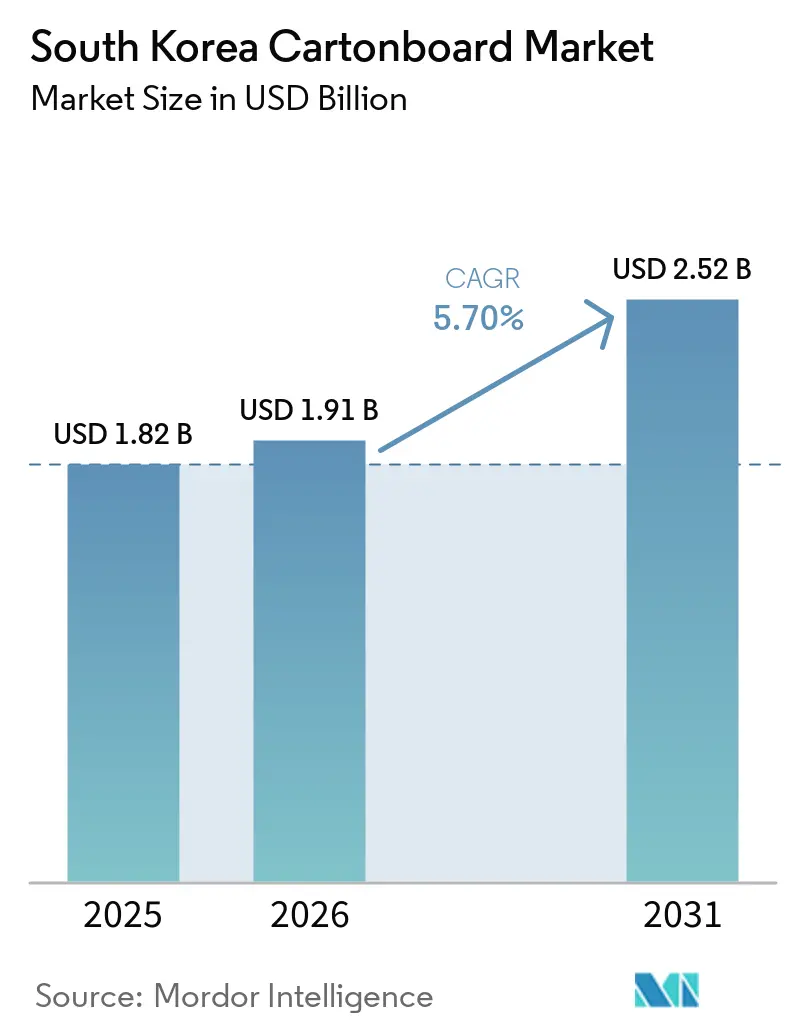

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

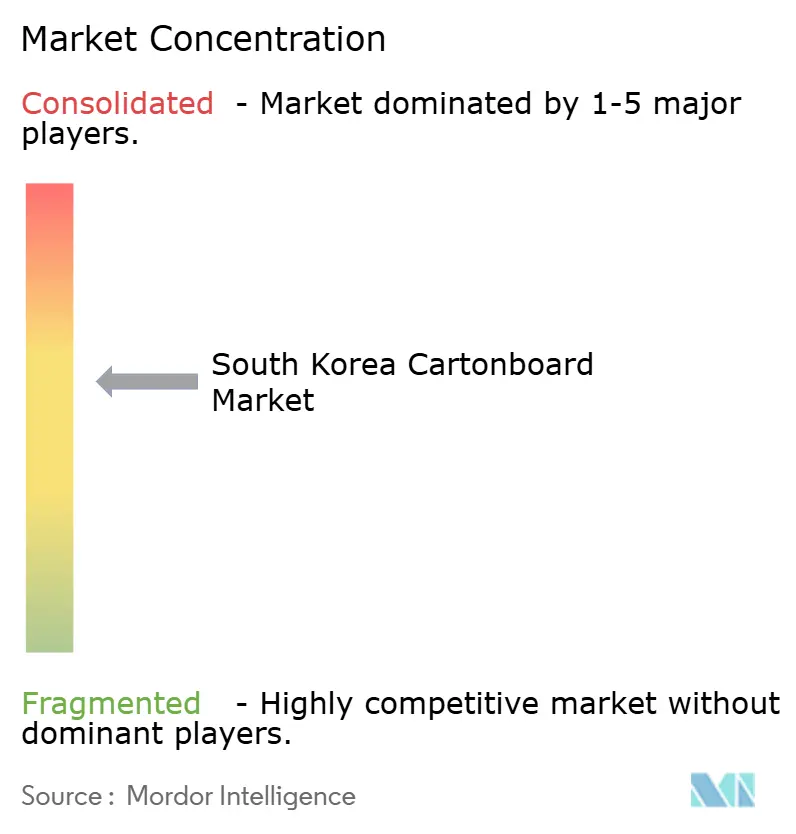

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Cartonboard Market Analysis by Mordor Intelligence

The South Korea cartonboard market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 1.91 billion in 2026 to reach USD 2.52 billion by 2031, at a CAGR of 5.70% during the forecast period 2026-2031. Growth in the South Korea cartonboard market reflects a clear shift in packaging demand toward premium, high-barrier, and recyclable paper-based substrates rather than a simple increase in consumption volume. Recyclability grading, greater producer responsibility pressure, and tighter packaging rules are raising the cost of plastic-heavy formats and improving the commercial position of paper-based alternatives. The South Korean cartonboard market is also benefiting from the country's early adoption of aluminum-free aseptic cartons, which are elevating specification requirements for dairy and beverage packaging. Export-oriented cosmetics, quick-commerce grocery delivery, health functional foods, and premium food gifting are all reinforcing demand for better print quality, stronger barrier performance, and higher-value converting. Competition remains active, but recent regulatory action on paper producers is likely to improve pricing transparency and strengthen competition around specialty grades, sustainability claims, and converter responsiveness.

Key Report Takeaways

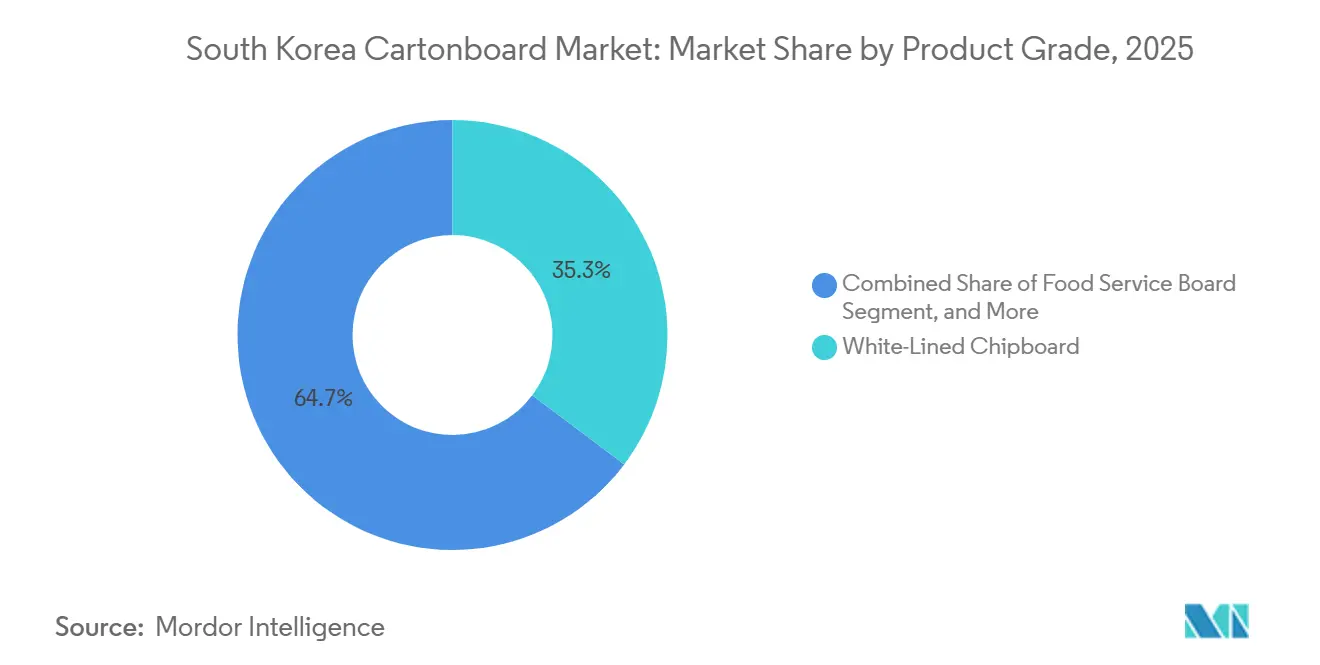

- By product grade, white-lined chipboard captured 35.28% of the South Korea cartonboard market share in 2025.

- By packaging format, the South Korea cartonboard market size for the liquid packaging segment is forecast to advance at a 6.43% CAGR through 2031.

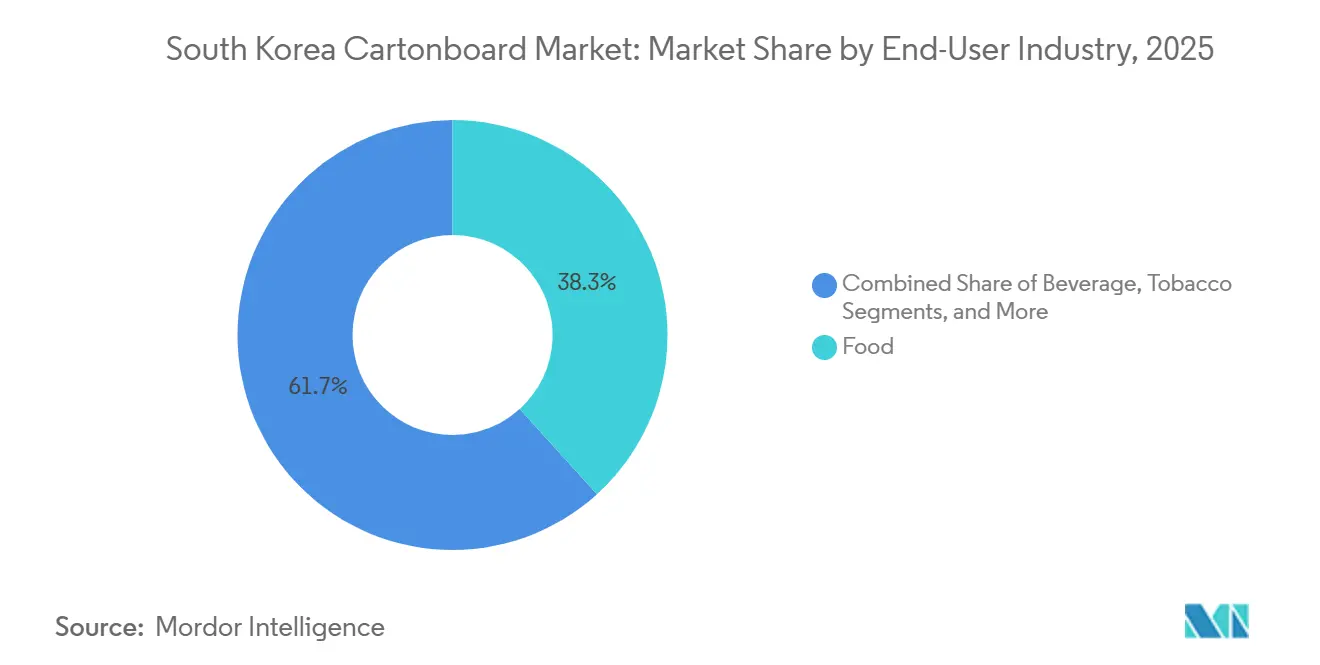

- By end-user industry, food captured 38.28% of the South Korea cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable Packaging Substitution Across Food, Beverage, And Personal Care | +1.4% | National, intensified in Seoul, Gyeonggi, and Incheon industrial packaging zones | Short term (≤ 2 years) |

| Expansion Of Online Grocery And Food Delivery Packaging | +1.1% | National, early demand gains in Seoul, Seongnam, and Busan quick-commerce corridors | Short term (≤ 2 years) |

| K-Beauty Export Momentum Raising Premium Folding Carton Demand | +0.8% | Export-facing, concentrated in Seoul and Gyeonggi cosmetics manufacturing zones | Medium term (2-4 years) |

| Paper-Based Barrier Innovation In Liquid Cartons | +0.7% | National, driven by dairy and beverage hubs in Chungnam and Gyeonggi provinces | Medium term (2-4 years) |

| Health Functional Food And OTC Carton Premiumization | +0.5% | National, growing across urban and suburban pharmacy and specialty retail channels | Medium term (2-4 years) |

| Convenience-Store Private Label And Seasonal Gift Pack Refresh Cycles | +0.3% | National, concentrated in metropolitan convenience-store networks including GS25, CU, and 7-Eleven | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainable Packaging Substitution Across Food, Beverage, And Personal Care

South Korea's tighter packaging rules are acting as a direct demand lever for cartonboard rather than as a minor compliance adjustment. The amended Resource Recycling Promotion Act took effect on April 30, 2026, and it restricts the packaging space ratio for consumer parcels to 50% or below, with penalties of up to KRW 3 million (USD 2,170) per violation. Paper-based cushioning is treated more favorably because parcels using it can operate within a 70% space ratio.[1]Seoul Economic Daily, “Coupang Shifts to Paper Bags for Dawn Delivery in Plastic,” Seoul Economic Daily, en.sedaily.com Coupang moved its door-delivery service to paper bags in April 2026, and that early shift sent a clear signal to other large platforms to review their packaging formats. Recyclability grading and eco-modulated packaging costs are also improving the commercial position of paperboard in procurement decisions across foodservice and consumer goods. This is pushing the South Korean cartonboard market further into secondary cartons, paper cushioning, and recyclable outer formats across convenience retail, parcel delivery, and branded consumer packaging.

Expansion Of Online Grocery And Food Delivery Packaging

Online grocery and food delivery continue to increase packaging intensity as order frequency rises and delivery windows shorten. South Korea's grocery quick-commerce segment is projected to grow 34.8% from USD 3.19 billion in 2025 to USD 4.3 billion by 2030, showing how quickly platform-led fulfillment is scaling in urban areas. Daiso expanded its Today Delivery service to all 25 Seoul districts in May 2026 by using around 1,600 physical stores as urban micro-fulfillment hubs. This kind of operating model supports higher demand for short-cycle folding cartons and food-grade paper formats in Seoul, Incheon, and Gyeonggi. The April 2026 parcel space-ratio rules also favor more structured paper-based delivery packs over soft-plastic mailers in several grocery and meal-delivery use cases. As a result, the South Korean cartonboard market benefits from more frequent printing runs, higher use of protective packaging, and stronger demand for food-safe board in dense metropolitan delivery networks.

K-Beauty Export Momentum Raising Premium Folding Carton Demand

Cosmetics exports are giving premium cartonboard demand a strong external growth engine. South Korean cosmetics exports reached USD 11.43 billion in 2025, up 12.3% year on year, and the country moved into second place as the world's largest cosmetics exporter.[2]Yonhap News Agency, “Gov't to Foster Cosmetics as New Export Growth Engine: Finance Minister,” Yonhap News Agency, en.yna.co.kr In Q1 2026, cosmetics exports rose 19.4% year on year to USD 3.1 billion, and the government formally positioned cosmetics as a strategic export industry. This export momentum is driving demand for solid bleached board and folding boxboard, as brands seek high-white, emboss-compatible, and recyclable outer cartons that support premium presentation and overseas compliance. Hansol Paper highlighted that opportunity at Cosmobeauty Seoul 2026, where it showcased premium cosmetic paper substrates and paper-based flexible packaging alternatives for beauty applications.[3]Herald Business, “Hansol Paper Targets USD 11.4 Billion Cosmetics Export Market,” Herald Business, biz.heraldcorp.com The South Korean cartonboard market benefits from this shift, as premium beauty packaging now serves as both a visual brand asset and a practical tool for export-readiness.

Paper-Based Barrier Innovation In Liquid Cartons

Paper-based barrier innovation is changing the growth profile of liquid packaging board in South Korea. Maeil Dairies became the first producer globally to deploy Tetra Pak's paper-based barrier technology on high-speed Tetra Pak A3/Speed lines in February 2026, producing Tetra Brik Aseptic 200 Slim cartons with 87% renewable content and a 26% lower package carbon footprint verified by the Carbon Trust.[4]Tetra Pak, “Tetra Pak Extends Paper-Based Barrier Packaging to High-Speed Lines,” Tetra Pak, tetrapak.com Seoul Dairy Cooperative launched organic white milk in SIG Terra Alu-free + Full Barrier cartons in October 2025, making it the first aseptic carton in South Korea to receive an official recyclable grade under the country's recyclability grading system. Removing the aluminum layer improves compatibility with South Korea's chilled-carton recycling infrastructure and removes a major technical objection to higher paperboard content in aseptic structures. These commercial launches show dairy, juice, and plant-based beverage fillers that high-barrier performance can be maintained without aluminum. That leaves the South Korean cartonboard market well positioned to benefit from both rising demand for liquid packaging board and higher-value product specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Virgin Fiber And Pulp Cost Volatility | -1.2% | National, affects all South Korean cartonboard mills dependent on imported pulp | Short term (≤ 2 years) |

| Competition From Lightweight Flexible Plastics And Pouches | -0.8% | National, strongest in e-commerce, snack, and personal care packaging channels | Long term (≥ 4 years) |

| Policy Uncertainty Around Disposable Serviceware Rules | -0.4% | National, concentrated in Seoul and Gyeonggi restaurant and delivery sectors | Medium term (2-4 years) |

| Aging Mill And Converting Workforce Outside Core Industrial Clusters | -0.2% | Regional, most visible in Jinju, Ulsan, and Cheongju industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Virgin Fiber And Pulp Cost Volatility

Imported fiber exposure remains one of the clearest structural constraints on domestic cartonboard profitability. South Korea's paper supply chain still relies heavily on imported pulp, leaving mills vulnerable to changes in global fiber prices, freight costs, and supply disruptions. The Bank of Korea's import price index for pulp and paper products stood at 150.98 in March 2026, up from 147.18 in February, confirming continued input-cost pressure at the mill gate. That pressure is especially difficult for virgin fiber-intensive grades such as solid bleached board and folding boxboard, which are also the grades seeing stronger demand from cosmetics, health-related packs, and premium consumer applications. Buyers in those end markets do not always accept price increases at the same speed as mills face cost inflation. This keeps the South Korean cartonboard market under a recurring margin ceiling even when demand conditions are otherwise favorable.

Competition From Lightweight Flexible Plastics And Pouches

Flexible packaging remains a durable substitute in several high-volume applications. Stand-up pouches, retort pouches, refill packs, sachets, and multilayer films still hold strong positions in snacks, sauces, coffee servings, and personal care because they offer weight, speed, and line-efficiency advantages. Plastic packaging suppliers have also moved faster in resealable, shaped, and high-barrier designs, which raises switching costs for brand owners considering cartonboard alternatives. A naphtha supply disruption in Q2 2026 narrowed the cost gap between paper and plastic packaging, giving cartonboard converters a temporary opening to promote paper substitutes. Even so, the same March 2026 import price data show that paper-based materials were also under cost pressure, limiting how aggressively cartonboard suppliers can discount to win volume. This means the South Korea cartonboard market is likely to gain ground first in regulated, premium, or recyclable applications rather than across every flexible-pack category.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Recycled Board Anchors Volume, Service-Oriented Grades Set The Growth Pace

White-lined chipboard commanded 35.28% of the South Korea cartonboard market share by product grade in 2025, supported by the country's established recycled-fiber base and its fit with mass-market food, beverage, retail, and e-commerce secondary packaging. The grade remains well-suited to large-volume uses where converters need dependable performance and competitive cost. Within the South Korea cartonboard industry, that makes WLC is the main volume anchor for everyday cartons rather than the main source of premium value. It also benefits from brand-owner demand for recyclable, familiar substrates, at a time when input-cost volatility is still affecting virgin fiber grades.

The food service board is projected to expand at a 6.16% CAGR from 2026 to 2031, reflecting stronger demand from ghost kitchens, dark stores, meal-kit programs, and quick-service restaurants that require oil-resistant, food-contact-safe paperboard. Solid bleached board and folding boxboard remain the preferred premium grades for beauty, healthcare, and gift-oriented packaging, and that positioning strengthened as South Korean cosmetics exports reached USD 11.43 billion in 2025. Liquid packaging board is also undergoing an upgrade cycle, as Maeil Dairies and Seoul Dairy Cooperative validated aluminum-free aseptic solutions with Tetra Pak and SIG. The South Korea cartonboard market is therefore balancing recycled-board scale with faster growth in foodservice and premium-specification grades.

By Packaging Format: Folding Cartons Hold The Base, Liquid Packaging Drives The Format Upgrade

Folding cartons accounted for 54.19% of the South Korean cartonboard market in 2025, reflecting their central role across food, pharmaceuticals, cosmetics, and seasonal gifting. The convenience-store channel reinforced that leadership because seasonal refreshes require frequent redesigns, short lead times, and large volumes of printed die-cut outers. GS25 alone offered more than 820 gift set SKUs for the 2025 Lunar New Year, underscoring the packaging intensity driven by recurring promotional cycles. That pattern helps the South Korean cartonboard market maintain a strong baseline for local converting and short-run printing.

Liquid packaging is projected to expand at a 6.43% CAGR through 2031, making it the fastest-growing format in the South Korea cartonboard market. That growth reflects both stable demand in dairy and beverages and a material shift from aluminum-layer structures toward new two-material or paper-based barrier designs. Maeil Dairies and Seoul Dairy Cooperative created the format's most visible commercial proof points by adopting Tetra Pak and SIG technologies for recyclable or lower-carbon cartons. Sleeve, tray, and foodservice formats are also expanding with chilled meals, fresh food retail, and platform-led delivery, but liquid packaging is the segment driving the clearest changes in barrier specifications and value capture.

By End-User Industry: Food Provides The Volume Base, Healthcare And Cosmetics Lift Value

Food accounted for 38.28% of the South Korean cartonboard market in 2025, making it the largest end-user segment across packaged convenience foods, chilled meal kits, and seasonal gift assortments. The South Korean cartonboard market benefits from this segment because food applications require frequent ordering, broad retail coverage, and frequent packaging refreshes. Quick-commerce expansion is reinforcing that base as operators add denser delivery coverage and higher packaging intensity in major metro areas. Food demand also spans several grades and formats, from WLC and folding cartons to liquid packaging board and food-contact service board.

The pharmaceutical and healthcare sector is projected to expand at a 6.75% CAGR through 2031, making it the fastest-growing end-user segment in the South Korea cartonboard market. South Korea's health functional food sector reached KRW 5.07 trillion (USD 3.7 billion) in 2024, and exports rose 18.1% year on year in January to April 2026, with the United States market up 64.9%. That trend supports higher demand for export-compliant, high-white outer cartons across OTC products, supplements, and health-focused consumer packs. Cosmetics and toiletries add another margin premium because K-beauty exporters continue to favor emboss-compatible and high-finish folding boxboard for branded outer packaging.

Geography Analysis

The South Korea cartonboard market remained centered on the Seoul-Incheon-Gyeonggi corridor in 2026, where the country's largest concentration of food, cosmetics, e-commerce, and pharmaceutical demand is located. Seoul stands out as the leading consumption node because quick-commerce, convenience retail, and export-facing brand owners are densely clustered there. Daiso expanded its Today Delivery service to all 25 Seoul districts in May 2026, using around 1,600 stores as urban fulfillment hubs, thereby reinforcing demand for short-cycle delivery packaging in the capital region. Coupang's April 2026 shift from plastic bags to paper bags in dawn delivery also showed that regulation-led packaging change can move fastest in the capital area's high-volume parcel channels.

The South Korea cartonboard market size in the capital area is supported by nearby converting assets in Incheon and by supply links to Hansol Paper's Daejeon operations, which help serve metropolitan buyers with shorter lead times. South Korea's main paper and board production clusters are Daejeon, Ulsan, Jinju, Cheongju, and Incheon, and they shape the domestic supply map for both board and converted cartons. The Ulsan-Jinju cluster has a clear structural role because Moorim P&P is the country's only integrated domestic pulp producer, providing it with partial insulation from imported fiber volatility. ANDRITZ completed the startup of an upgraded evaporation plant at Moorim P&P's Ulsan mill in April 2025, improving evaporation capacity and enabling internal condensate reuse. That investment strengthened long-term efficiency in a region where cost control remains important for the broader South Korea cartonboard market.

Export-driven demand is becoming more visible in Seoul's cosmetics base and in the food-processing corridors of Chungcheong province, where packaging standards increasingly reflect destination-market rules. Cosmetics exports reached USD 3.1 billion in Q1 2026, up 19.4% year on year, while health functional food exports rose 18.1% in January to April 2026. The South Korean cartonboard market share of premium and certified grades is therefore likely to rise fastest in export-facing clusters rather than in purely domestic-volume applications. That leaves the South Korea cartonboard market shaped not only by local regulation, but also by the packaging standards of overseas markets that Korean brands increasingly serve.

Competitive Landscape

The South Korea cartonboard market has a moderately concentrated upstream structure, with Hansol Paper and the Moorim group holding the strongest positions in domestic board supply. Downstream converting is far more fragmented, with regional folding-carton players including Barun Box, K and S, Sangjin Enterprise, Sang Jin Pack, and Daewoong Package competing on proximity, print quality, and order flexibility. The Korea Fair Trade Commission imposed KRW 338.3 billion (USD 245 million) in fines on six paper producers in April 2026 for coordinated price fixing, and the ruling added a three-year semi-annual price-reporting obligation that should improve cost transparency for buyers. This makes the competitive position in the South Korean cartonboard market increasingly dependent on specialty capabilities, converter service, and procurement credibility rather than on price moves alone.

Hansol Paper has been moving further into specialty and functional substrates, which shows a deliberate shift away from pure commodity exposure. In April 2026, the company launched Protego HS, a heat-sealable paper-based secondary packaging material designed to replace conventional PP and PE flexible packaging without capital modifications on customer lines. In May 2026, Hansol Paper also used Cosmobeauty Seoul 2026 to target export-oriented cosmetics packaging with premium paper substrates and its Protego eco-flexible packaging range. These moves tie Hansol more directly to beauty, food, and sustainable secondary packaging demand across the South Korea cartonboard market. They also position the company against plastic-film substitutes in categories where recyclability and visual quality carry more weight in buying decisions.

Moorim P&P has taken a different route by using its domestic pulp base to build more defensible positions in food-contact and molded fiber applications. In April 2026, Moorim P&P's food-grade pulp mold product secured TUV AUSTRIA biodegradability certification and food safety approvals from the US FDA and Germany's BfR, and the product was already being supplied to Lotte Mart, Nonghyup Hanaro Mart, and convenience-store ready-to-eat channels. Tetra Pak and SIG also play strategically important roles in liquid packaging board, as their Korean deployments with Maeil Dairies and Seoul Dairy Cooperative set the benchmark for recyclable or lower-carbon aseptic cartons. The South Korea cartonboard market still has open space in mid-range sustainable folding cartons for health functional food, OTC, and K-beauty exporters, where demand is rising faster than certified domestic converting capacity.

South Korea Cartonboard Industry Leaders

Hansol Paper Co., Ltd.

Tetra Pak International S.A.

SIG Group AG

Graphic Packaging International, LLC

Autajon Packaging Pacific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hansol Paper participated in Cosmobeauty Seoul 2026, May 27-29, 2026, Coex, Seoul, South Korea's largest cosmetics trade exhibition, targeting the USD 11.43 billion K-beauty export market with premium cosmetic paper packaging substrates across three display zones covering clean-texture, emboss-compatible, and recycled-material formats. The company also showcased its Protego eco-flexible packaging, designed to replace aluminum and plastic films in cosmetic pouches, positioning paper-based carton solutions as both aesthetically premium and EU PPWR-compliant for export-facing brands.

- May 2026: Hansol Paper reported Q1 2026 operating profit of KRW 11.2 billion (USD 8.1 million), down 44.7% year on year, as simultaneous revenue declines across printing paper, industrial paper, and specialty paper weighed on group profitability. Q1 revenue fell 2.7% to KRW 559.8 billion (USD 405 million), with specialty paper recording the steepest category decline at -8.4%.

- May 2026: The Korea Fair Trade Commission finalized KRW 338.3 billion (USD 245 million) in fines against six paper manufacturers, Hansol Paper, Moorim P&P, Moorim Paper, Moorim SP, Hankuk Paper, and Hongwon Paper, for coordinated printing paper price-fixing conducted across at least 60 meetings between February 2021 and December 2024. All six companies chose not to file administrative lawsuits and became subject to a three-year semi-annual price-reporting order, the first such order in South Korea in 20 years and the largest cartel penalty ever imposed on the domestic paper industry.

- April 2026: Moorim P&P's food-grade pulp mold product secured the highest-grade biodegradability certification from TUV AUSTRIA and food safety approvals from both the US FDA and Germany's Federal Institute for Risk Assessment, BfR. With production capacity of 10 million round plates monthly, the product was commercially supplied to Lotte Mart seafood packaging, Nonghyup Hanaro Mart meat and produce trays, and convenience-store ready-to-eat sections as a certified plastic-alternative food service board solution.

South Korea Cartonboard Market Report Scope

The South Korea Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The South Korea Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of South Korea cartonboard demand?

The South Korea cartonboard market was valued at USD 1.82 billion in 2025, is estimated at USD 1.91 billion in 2026, and is forecast to reach USD 2.52 billion by 2031 at a 5.70% CAGR.

Which packaging format leads demand in South Korea?

Folding cartons lead the format mix with a 54.19% share in 2025, supported by food, cosmetics, pharmaceuticals, and seasonal gift packaging.

Which end-user segment is growing fastest?

Pharmaceutical and healthcare is the fastest-growing end-user segment, with a projected CAGR of 6.75% from 2026 to 2031.

Why are aluminum-free aseptic cartons important in South Korea?

They improve recyclability and reduce carbon footprint while supporting higher paperboard content in dairy and beverage packaging, which helps liquid packaging grow at a 6.43% CAGR.

How are K-beauty exports affecting cartonboard demand?

Cosmetics exports reached USD 11.43 billion in 2025 and USD 3.1 billion in Q1 2026, which is raising demand for high-white, emboss-compatible, and export-ready paperboard cartons.

What is the main cost challenge for local producers?

Imported pulp and paper input inflation remains a key constraint, as shown by the Bank of Korea import price index for pulp and paper products rising to 150.98 in March 2026 from 147.18 in February.

Page last updated on: