Germany Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.01 Billion |

| Market Size (2026) | USD 2.10 Billion |

| Market Size (2031) | USD 2.63 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

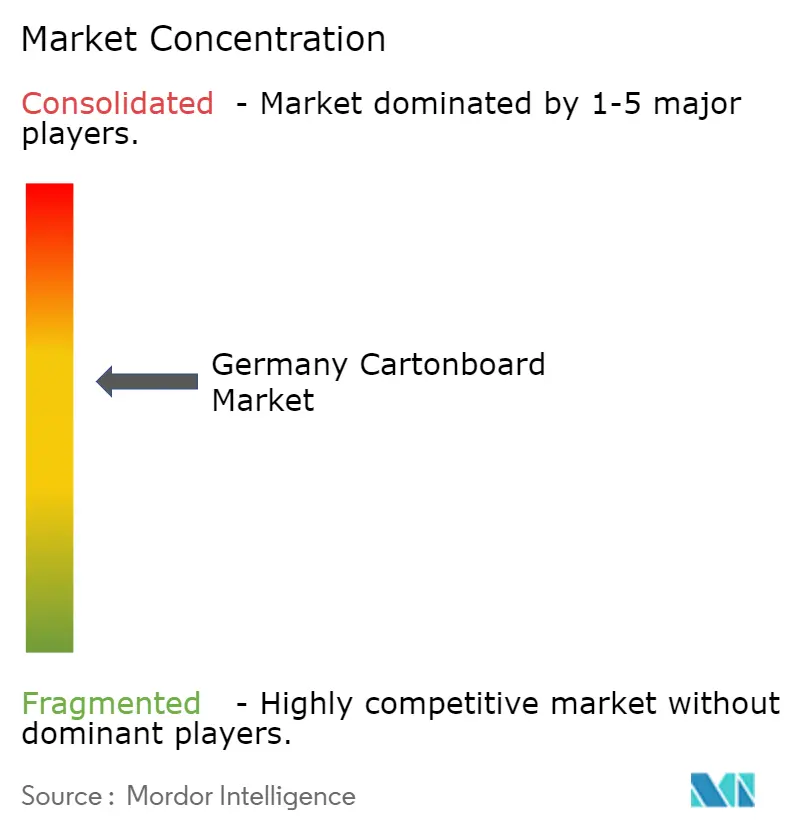

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cartonboard Market Analysis by Mordor Intelligence

The Germany Cartonboard Market size was valued at USD 2.01 billion in 2025 and is estimated to grow from USD 2.10 billion in 2026 to reach USD 2.63 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

Demand in 2026 is being supported by structural packaging changes rather than by a short-lived rebound, which gives the current growth profile a firmer base across regulated and everyday-use categories. The Packaging and Packaging Waste Regulation is widening the addressable use of fiber-based packs because recyclability-by-design rules are pushing brand owners away from plastic-heavy and composite packaging formats. Germany also enters this regulatory phase with a stronger operating base than many neighboring markets because its sorting and recovery system allows compliance spending to translate into higher-specification board demand. Pharmaceuticals continue to provide a stable demand floor, while food and beverage conversion activity and premium packaging demand in cosmetics are moving the product mix toward higher-value grades. Pricing conditions remain tight because new European board capacity and higher energy-linked cost pressure are limiting margin expansion, even as the overall Germany cartonboard market keeps growing through the forecast period.

Key Report Takeaways

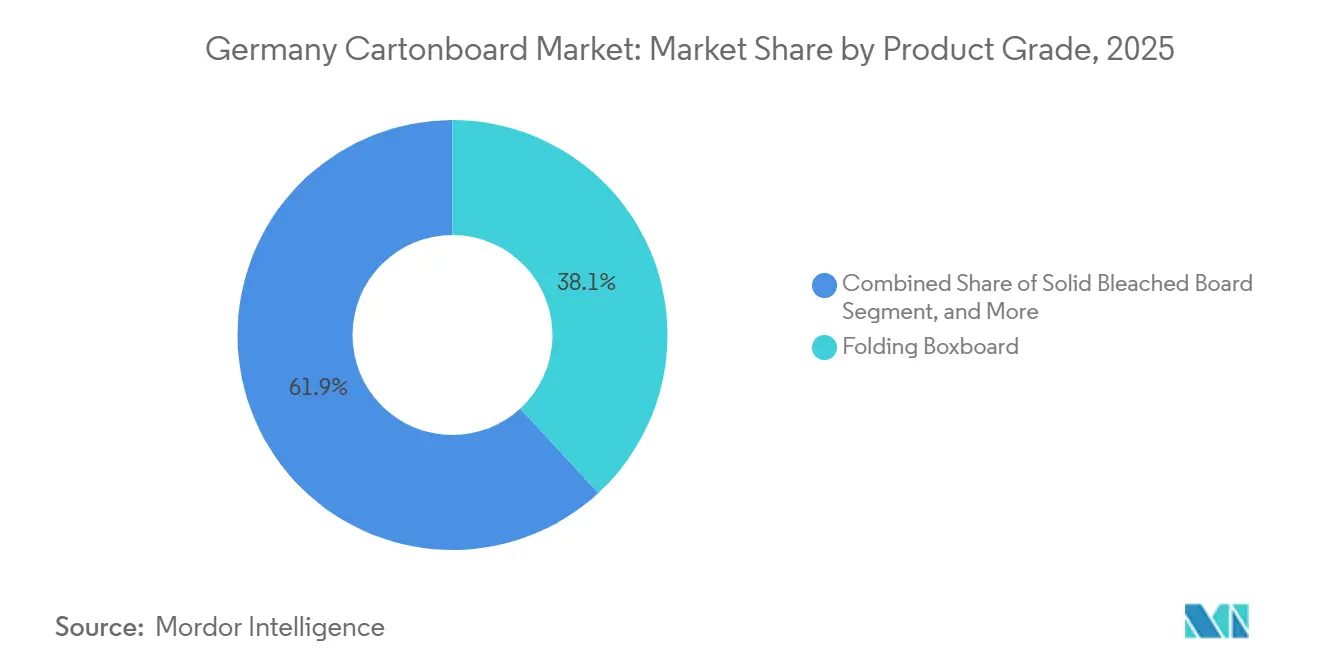

- By product grade, folding boxboard led with 38.13% revenue share in 2025, while solid bleached board is forecast to expand at a 7.53% CAGR through 2031 in the Germany cartonboard market.

- By packaging format, folding cartons held 48.41% of revenue in 2025, while liquid packaging is projected to grow at a 5.45% CAGR through 2031.

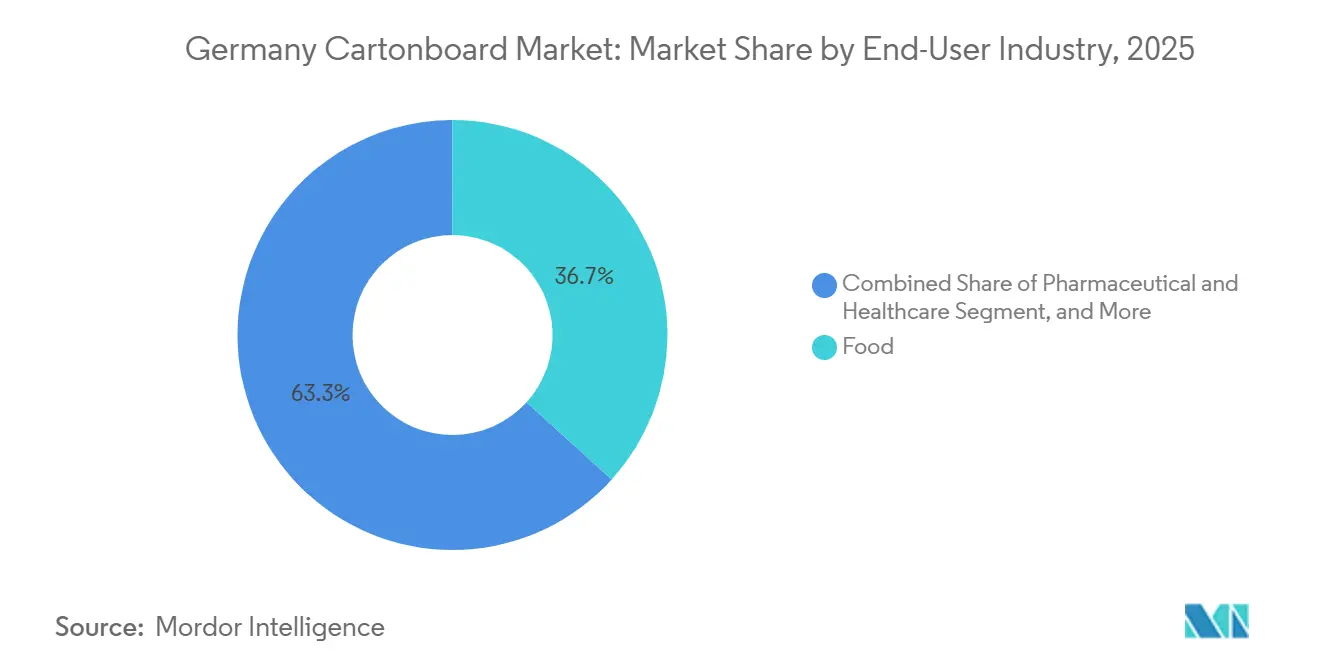

- By end-user industry, food accounted for 46.21% of 2025 revenues, while cosmetics and toiletries is forecast to expand at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PPWR-Led Recyclability-By-Design Adoption | +1.5% | National, with early gains in major FMCG manufacturing clusters in Bavaria, Baden-Württemberg, and Rhine-Ruhr | Long term (≥ 4 years) |

| Plastic-To-Fiber Shift In Food And Beverage Packs | +1.2% | National, spillover to Austria and Benelux via German brand owners | Medium term (2-4 years) |

| Pharma And OTC Carton Demand Resilience | +0.8% | National pharmaceutical manufacturing hubs in Baden-Württemberg, Bavaria, and North Rhine-Westphalia | Long term (≥ 4 years) |

| Folding Carton Preference For Shelf Impact And Compliance | +0.6% | National, concentrated in premium food, cosmetics, and OTC retail clusters | Medium term (2-4 years) |

| ZSVR Fee Incentives Favoring Pure-Fiber Designs | +0.4% | National, aligned with VerpackG and EU PPWR eco-modulation rules | Short term (≤ 2 years) |

| Barrier-Coated Board Replacing Plastic Windows And Fluorinated Formats | +0.3% | National, with early adoption in food contact and confectionery applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PPWR-Led Recyclability-By-Design Adoption

The PPWR entered into force in February 2025 and moves into its core operational phase in August 2026, which means packaging placed on the EU market must align more clearly with harmonized recyclability classifications and conformity requirements.[1]European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council on Packaging and Packaging Waste,” Official Journal of the European Union, eur-lex.europa.eu In Germany, that requirement lands on top of an established compliance system, because the Zentrale Stelle Verpackungsregister and the VerpackG framework already give producers, converters, and brand owners a clear route for registration, data reporting, and recyclability assessment.[2]Zentrale Stelle Verpackungsregister, “Basic Information About the ZSVR’s Catalogue,” Verpackungsregister, verpackungsregister.org Procurement behavior is already shifting ahead of the August 2026 milestone, with brand owners tightening tender specifications around recyclability, mono-material structures, and documentation that can withstand closer regulatory review. That change improves the position of cartonboard against paper-plastic-foil structures because fiber packs can meet both design and recyclability expectations with fewer material conflicts. It also improves the standing of mills that can offer certified recyclable portfolios and clearer traceability across grades, coatings, and converting steps. As those declarations become part of routine packaging governance, the Germany cartonboard market is moving toward higher-specification demand instead of simple volume replacement.

Plastic-To-Fiber Shift In Food And Beverage Packs

Plastic substitution in German food and beverage packaging is moving with more force because retailer mandates, consumer expectations, and EU-aligned packaging rules are all pointing toward recyclable fiber formats. Large own-label programs in food retail are giving that shift scale, because a single redesign decision can move substantial packaging volumes from plastic-heavy formats toward folding boxboard, foodservice board, and barrier-coated cartonboard. The commercial effect is not limited to tonnage, since food-contact conversion requires coatings and structures that can preserve product safety while still supporting recyclability claims, which raises the technology threshold for suppliers. That is why the Germany cartonboard market is gaining a larger premium layer inside food packaging, rather than only adding lower-value replacement volumes. Henkel and MM Board and Paper illustrated this direction in 2025 when they replaced a blister pack with a 100% cartonboard solution using TOPCOLOR® BARRIER AROMA, and that pack won the German Packaging Award 2025. Because food represented 46.21% of 2025 revenues, continued redesign activity in this end-use gives the Germany cartonboard market a large and durable platform for further coating and product development.

Pharma And OTC Carton Demand Resilience

Germany’s pharmaceutical base gives the Germany cartonboard market a steady source of demand because medicine packaging volumes are tied more closely to regulation, patient need, and product availability than to short-term consumer sentiment. Carton use in this area remains structurally supported by serialization, tamper-evidence, labeling discipline, and the high documentation standards expected in regulated healthcare packaging. The more active growth layer is the OTC category, where self-care demand, broader product ranges, and shorter production runs are lifting the need for printed cartons that can handle frequent changes in artwork and information density. This favors substrates with surface consistency, cleanliness, and dependable converting performance, which is why Solid Bleached Board is gaining traction in several healthcare-related applications. Entry barriers also remain meaningful because converters in this space need validated operating processes, strong quality systems, and customer trust built around compliance execution rather than simple price competition. That mix of regulation-led stability and specification upgrades keeps pharmaceuticals and OTC as one of the more dependable demand anchors in the Germany cartonboard market.

Folding Carton Preference For Shelf Impact And Compliance

Folding cartons remain central because they meet 2 needs at once, they satisfy compliance and communication requirements while also giving brands a visible and workable packaging surface across dense retail categories. In food, cosmetics, and OTC products, this matters because brand owners need packs that can carry more information, adapt quickly to new launches, and still present a premium appearance on shelf or in direct-to-consumer delivery. Coated cartonboard supports those needs through better print definition, cleaner color response, and compatibility with finishing techniques that help products stand out without moving into less recyclable material combinations. MM Group’s beauty packaging work showed how tactile printing and finishing are being used more actively to support premium presentation and faster commercial cycles. At the same time, Germany’s Mindeststandard 2025 strengthens the design pressure on converters by discouraging non-recyclable windows and problematic decorative elements in packaging structures. As e-commerce shipments add new requirements around stiffness, durability, and presentation, the Germany cartonboard market keeps seeing a pull toward higher-caliper and better-performing carton formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Recovered-Fiber Cost Volatility | -1.2% | National, with higher exposure in gas-dependent recycled-fiber mill clusters in Rhine-Ruhr and Hamburg | Short term (≤ 2 years) |

| European Cartonboard Overcapacity And Import Pressure | -1.0% | National and Western Europe, particularly in fresh-fiber grades with new Scandinavian capacity | Medium term (2-4 years) |

| Reusable Foodservice Rules Limiting One-Way Pack Growth | -0.5% | National, urban centers under enforcement pressure from EU Single-Use Plastics Directive | Short term (≤ 2 years) |

| Barrier Reformulation And Requalification Costs | -0.3% | National, concentrated in food contact and pharma converting operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy And Recovered-Fiber Cost Volatility

Energy volatility remains the most immediate cost risk for the Germany cartonboard market in 2026, because mills are still operating in an environment where fuel, transport, and input costs can move quickly and unevenly. Mayr-Melnhof stated in its April 2026 trading update that significantly higher energy, transport, and chemical costs were the main driver of margin compression, and management said these pressures had become noticeable since March 2026. Recycled-fiber grades are especially exposed because their economics are more sensitive to energy-intensive processing and to changes in recovered paper pricing. Germany’s strong collection and recovery system helps keep supply chains active, but that same concentration can make cost movements in recovered fiber pass through mills faster than producers would prefer. Operators with co-generation assets, biomass systems, or power purchase agreements are better placed to absorb sudden cost shifts, yet those investments also require capital at a time when selling prices are under pressure. The result is a sharper split between suppliers that can defend margins and those that face weaker flexibility as the Germany cartonboard market moves through the current cost cycle.

European Cartonboard Overcapacity And Import Pressure

European supply conditions remain difficult because the Germany cartonboard market sits inside a broader regional system where fresh-fiber capacity additions and aggressive offers can quickly flow into domestic pricing. Germany’s position as both a major consumption market and a trade hub means that any imbalance in European board supply shows up quickly in local negotiations, especially in more standardized grades. Mayr-Melnhof described 2025 cartonboard conditions as persistently weak and marked by structural overcapacity, with fresh-fiber grades under downward price pressure from new supply, subdued demand, and offers from Asian producers. That environment puts the greatest strain on mills and converters whose cost positions are not protected by vertical integration, technical differentiation, or a stronger mix of specialty business. Pressure is also visible further down the chain, because Smurfit Westrock said it had initiated consultations in 2025 on the permanent closure of 2 German converting sites as part of asset optimization. Until regional supply and demand come back into a better balance, the Germany cartonboard market is likely to stay disciplined on price even where end-use demand remains sound.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors The Market As Solid Bleached Board Accelerates

Folding Boxboard held 38.13% of the Germany cartonboard market share in 2025, which kept it as the largest product grade across the country’s cartonboard mix. Its lead comes from a broad fit across food retail, pharmaceutical secondary packaging, and premium consumer goods, where stiffness, printability, and recyclability all need to work together in a practical format. That operating balance matters in Germany because many converters run high-speed lines and need a substrate that supports efficient throughput without compromising pack quality or presentation. White-Lined Chipboard also remains important in outer food packs and lower-premium consumer goods, but its 2026 economics are under greater strain because recycled-fiber grades are more exposed to energy-linked cost volatility.

Solid Bleached Board is the fastest-growing grade, with a forecast CAGR of 7.53% from 2026 to 2031, and this part of Germany cartonboard market size is being lifted by cosmetics and OTC healthcare applications that require cleaner visual performance and stronger hygiene positioning. Brand owners moving toward brighter surfaces, more even print results, and tighter product protection are steadily shifting selected packs toward SBB and other premium fresh-fiber grades when recycled alternatives cannot deliver a consistent finish. Liquid Packaging Board and Food Service Board remain narrower in scale, but both gain when beverage and food-contact packs move further into fiber-based designs that still need barrier performance. Solid Unbleached Board serves a smaller niche centered on food-safe uses and kraft-style premium positioning, which keeps its role stable even if its share is more limited than Folding Boxboard or SBB. Across the grade landscape, the Germany cartonboard market is putting more weight on documented recyclability and barrier credibility, which improves the standing of suppliers with verified recyclable portfolios and clearer technical documentation.

By Packaging Format: Folding Cartons Dominate While Liquid Packaging Drives Incremental Growth

Folding Cartons accounted for 48.41% of revenue in 2025, which made them the largest packaging format in the Germany cartonboard market and confirmed their central role across major end-use categories. Their lead is rooted in everyday operating needs rather than in a temporary cycle, because pharmaceuticals, food retail, and cosmetics all depend on carton structures that can combine speed, communication space, and compliance-ready design. In medicines, carton use stays firm because packs must accommodate dense information and secure presentation, while in food retail the move away from plastic continues to pull more outer packaging demand toward fiber-based cartons. Germany’s Mindeststandard 2025 supports this trajectory by pushing packaging design away from non-recyclable windows and other features that make recyclability harder to demonstrate under evolving rules.

Liquid Packaging is the fastest-growing format, with a projected CAGR of 5.45% from 2026 to 2031, and this slice of Germany cartonboard market size is supported by beverage diversification beyond traditional dairy and juice applications. Growth in plant-based drinks and functional beverages is helping liquid cartons extend into more shelves, which gives converters a wider case for aseptic and chilled pack development. Germany also benefits from an established recycling base for liquid cartons, and Elopak noted that around 180,000 tonnes of liquid cartons are produced for the German market annually, which reinforces the format’s operational credibility. Sleeve and Tray formats remain relevant in retail-ready packaging and selected food-service uses, while cups and related one-way foodservice structures face a tighter near-term ceiling where reuse provisions begin to shape format economics more directly under the PPWR. This leaves the Germany cartonboard industry with a stable format base in folding cartons and a smaller but steadily strengthening expansion path in liquid packaging.

By End-User Industry: Food Holds Half The Market As Cosmetics Outpaces All Other Segments

Food accounted for 46.21% of 2025 revenues, which made it the largest end-user category in the Germany cartonboard market and confirmed its role as the structural foundation of demand. The segment’s scale reflects Germany’s large food manufacturing base, dense retail structure, and steady need for paperboard outer packaging across ambient, frozen, and refrigerated products. Beverage, pharmaceutical and healthcare, and tobacco follow very different demand patterns, because beverage rises with liquid packaging adoption, pharmaceuticals stay supported by regulation and OTC expansion, and tobacco continues to contract in volume even though packaging rules still preserve some carton use. Food matters beyond its share because it is the main arena where packaging reformulation can shift demand from laminates and rigid plastics into mono-material fiber structures, which then feeds back into board mix and coating needs.

Cosmetics and toiletries is the fastest-growing end-user segment, with a forecast CAGR of 6.67% from 2026 to 2031, and this part of Germany cartonboard market size is expanding faster because cartons are being used as a premium communication surface as much as a protective pack. Brands in this category are moving toward Solid Bleached Board and premium coated Folding Boxboard that can support high-gloss print, embossing, tactile effects, and visible recyclability claims in a single paper-based format. MM Group’s beauty packaging work highlighted how tactile printing and finishing are becoming commercially important for premium products that need fast lead times and stronger shelf visibility. The Other End-User Industries cluster, which includes toys, apparel, automotive aftermarket, household goods, electrical products, and foodservice, gives the Germany cartonboard industry a broader base and reduces reliance on only 1 discretionary demand stream. This wider spread of applications helps the Germany cartonboard industry absorb weakness in contracting categories while still moving its mix toward higher-value packaging programs.

Geography Analysis

Germany holds a central place in the European fiber packaging system, and the Germany cartonboard market reflects that role through its combination of large domestic demand, advanced converting capacity, and stronger regulatory readiness than many neighboring countries. Demand is shaped heavily by pharmaceuticals, food, and cosmetics, which together create dense and specification-driven packaging needs across the main board grades. Germany’s VerpackG system and the LUCID Packaging Register give market participants an established path for registration, reporting, and compliance management, which lowers the operational friction around recyclable packaging adoption. With the PPWR entering its core operational phase in August 2026, Germany’s existing systems are well placed to act as a practical foundation for wider EU-aligned packaging enforcement. That combination of industrial depth and institutional readiness gives the Germany cartonboard market a stronger ability to convert regulatory change into commercially relevant board demand.

Regional differences inside the country still matter because end-use concentration and production patterns are not spread evenly across Germany. Baden-Württemberg and Bavaria stand out for pharmaceutical and cosmetics manufacturing, which supports stronger demand for higher-value SBB and premium Folding Boxboard grades. Rhine-Ruhr remains important for food retail packaging conversion and for large-volume operations that need efficient supply into Germany’s biggest retail and FMCG distribution channels. This leaves the Germany cartonboard market with a regional split where premium fresh-fiber demand is more visible in healthcare and beauty clusters, while recycled-fiber grades remain more embedded in high-volume mainstream programs. It also means that packaging redesigns initiated by major brand owners in 1 region can move quickly through national converting networks and reshape buying patterns at a broader level.

Trade flows add another dimension because the Germany cartonboard market is highly exposed to moves in wider European board supply and pricing. Fresh-fiber imports from Nordic producers raise competitive intensity in categories such as Folding Boxboard and liquid packaging board, which keeps domestic pricing under discipline when regional capacity is high. Germany’s converting base also exports higher-value carton structures into nearby Western European markets, which supports suppliers that compete through technical performance, print quality, and compliance execution rather than on price alone. Its optical sorting and recovery capabilities reinforce the recyclability case for fiber packaging, which matters even more as declarations of conformity become a more visible part of packaging governance across the EU.

Competitive Landscape

The Germany cartonboard market is moderately concentrated at the board supply level, because a relatively small set of European producers serves much of the country’s mill-grade demand while the converting layer remains more fragmented. Mayr-Melnhof Karton, Metsä Board, Stora Enso, Billerud, Holmen, and RDM Group shape much of the supply environment across Folding Boxboard, Solid Bleached Board, and other grades sold into Germany. Competition is increasingly defined by certified recyclability, barrier functionality, print surface performance, and the ability to support customers through documentation and compliance requirements rather than by basic capacity alone. Producers with integrated mill systems have an advantage when customers want proof that material performance and recyclability claims can stand together inside a single packaging structure. That keeps the Germany cartonboard market competitive even when headline demand growth is steady and broad-based.

Leading suppliers are responding through targeted strategy moves that are aimed more at quality, cost discipline, and premium positioning than at undifferentiated volume growth. Mayr-Melnhof said its Fit-For-Future program is pushing fixed-cost reduction, efficiency gains, and cost-structure harmonization across its European network, which fits a period where margin control is as important as sales expansion. Metsä Board presented its Lead the Pack strategy for 2026-2030 with a target of improving EBITDA by EUR 200 million by the end of 2028, and the second phase centers on brand-enhancing consumer packaging solutions that align well with premium demand in Germany.[3]Metsä Board Corporation, “Metsä Board’s Transformation Progressing, Comparable EBITDA at EUR 17 Million in January-March 2026,” Metsä Group, metsagroup.com Billerud also continued its Evolution program investments directed at solid bleached board capacity, which shows that premium fresh-fiber grades still sit high on supplier investment agendas.[4]Billerud AB, “Sequential Volume Uplift With Challenged Margins: Interim Report January-March 2026,” Billerud, billerud.com These examples show that the Germany cartonboard market is rewarding companies that can defend a higher-value position rather than rely on commodity exposure alone.

At the converting level, specialist players in pharmaceuticals and premium FMCG packaging have more room to protect margins because automation, serialization capability, embellishment know-how, and certification narrow the field of credible suppliers. That is especially relevant where customers need tamper-evident formats, short-run flexibility, or premium visual effects delivered without weakening recyclability claims.

Germany Cartonboard Industry Leaders

Mayr-Melnhof Karton Aktiengesellschaft

Metsä Board Corporation

Stora Enso Oyj

RDM Group S.p.A.

Holmen AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mayr-Melnhof Karton reported Q1 2026 adjusted EBITDA of EUR 104.1 million (USD 117.6 million), a decline of 12.7% versus Q1 2025, attributing the shortfall primarily to significantly higher energy, transport, and chemical costs driven by Middle East geopolitical tensions since March 2026, the Fit-For-Future program simultaneously delivered stronger-than-planned fixed cost and efficiency progress.

- March 2026: Metsä Board Corporation presented its "Lead the Pack" strategy for 2026-2030, targeting a EUR 200 million (USD 226 million) improvement in EBITDA by end-2028 through a cost savings and profitability program, the strategy's second phase focuses on growth in brand-enhancing consumer packaging solutions, reinforcing Metsä Board's positioning in premium FBB for the German market.

- September 2025: Koehler Paper launched NexPlus® Seal Coat, a paper packaging material with high-gloss surfaces and flex-crack resistance, at Fachpack 2025 in Nuremberg, the product enables brands to specify paper packaging with comparable aesthetics to plastic while meeting recyclability requirements under the PPWR.

Germany Cartonboard Market Report Scope

The Germany Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Germany Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the size outlook for Germany cartonboard demand through 2031?

The Germany cartonboard market was valued at USD 2.01 billion in 2025, reached USD 2.1 billion in 2026, and is forecast to reach USD 2.63 billion by 2031 at a 4.60% CAGR.

Which product grade leads demand in Germany?

Folding Boxboard led product-grade demand with a 38.13% revenue share in 2025 because it fits food, pharmaceutical, and premium consumer goods packaging needs.

Which cartonboard grade is growing the fastest in Germany?

Solid Bleached Board is projected to grow at a 7.53% CAGR from 2026 to 2031, supported by cosmetics and OTC healthcare applications that need print quality and hygiene performance.

Why are folding cartons still the main packaging format in Germany?

Folding Cartons held 48.41% of 2025 revenue because they remain the main format across food, pharma, and cosmetics, where compliance, print area, and conversion efficiency all matter.

Which end-user segment is expanding the fastest?

Cosmetics and toiletries is the fastest-growing end-user segment, with a 6.67% CAGR through 2031, driven by premiumization and recyclable mono-material packaging upgrades.

What are the main risks affecting supplier margins in 2026?

The main risks are energy and recovered-fiber cost volatility, along with regional overcapacity and import pressure, which are keeping pricing conditions tight even as demand grows.

Page last updated on: