Japan Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

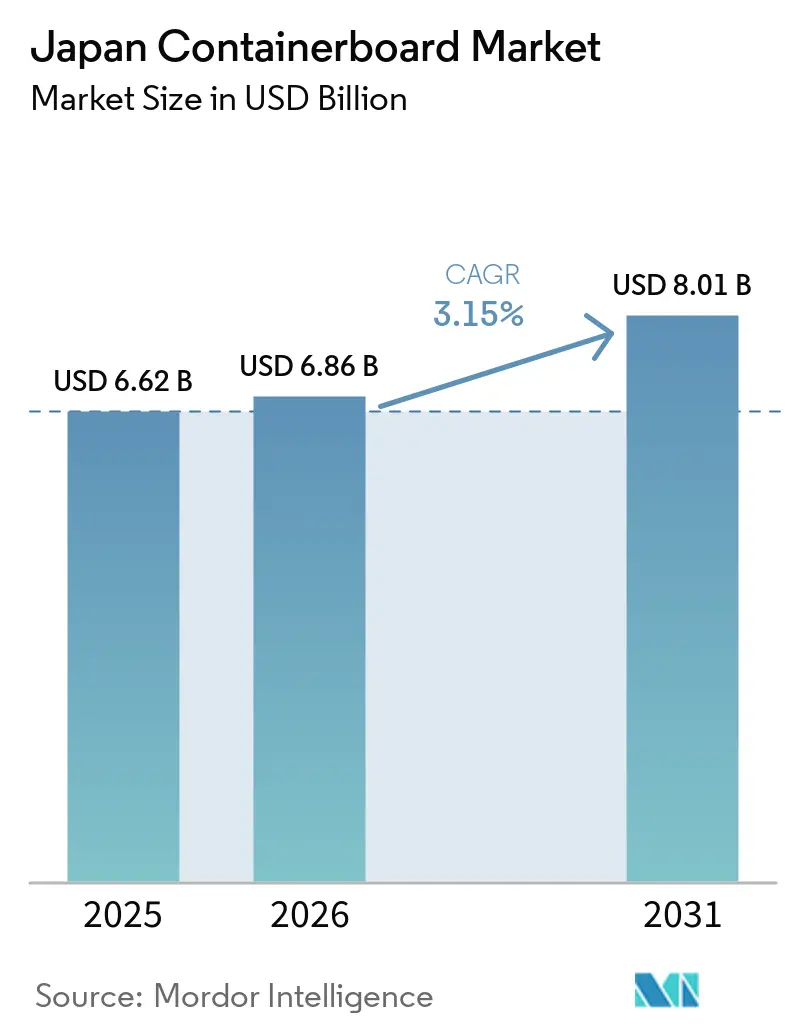

| Base Year Market Size (2025) | USD 6.62 Billion |

| Market Size (2026) | USD 6.86 Billion |

| Market Size (2031) | USD 8.01 Billion |

| Growth Rate (2026 - 2031) | 3.15% CAGR |

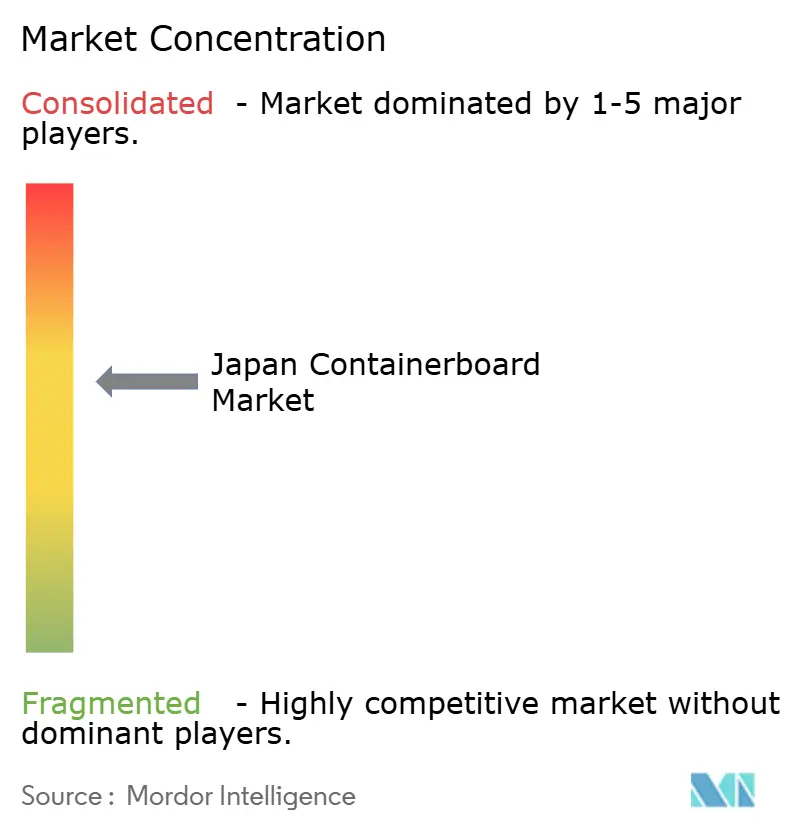

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Containerboard Market Analysis by Mordor Intelligence

The Japan containerboard market size is expected to increase from USD 6.62 billion in 2025 to USD 6.86 billion in 2026 and reach USD 8.01 billion by 2031, growing at a CAGR of 3.15% over 2026-2031. Growth in the Japan containerboard market is being supported by the shift away from fossil-based plastics and by stable parcel volumes from domestic e-commerce. These two forces are expanding the role of paper-based shipping formats across retail, food distribution, and everyday consumer deliveries. At the same time, export packaging for electronics and semiconductors is lifting demand for stronger kraft-based grades that can protect higher-value goods and meet stricter handling needs. Competition remains concentrated at the mill level, but a wide converter base keeps service quality, customization, and regional delivery performance important in the Japan containerboard market. Cost volatility in recovered paper, fuel, and transport still limits upside, so future gains in the Japan containerboard market are likely to depend as much on product mix and pricing discipline as on pure volume recovery.

Key Report Takeaways

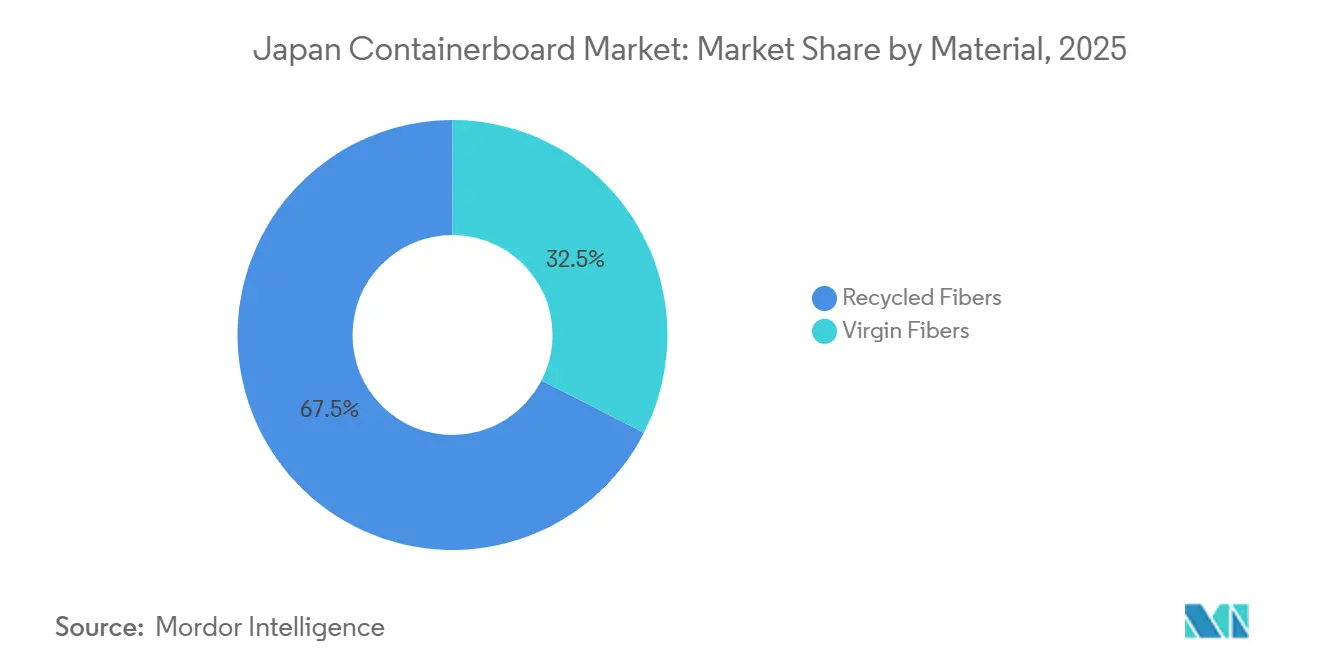

- By material, recycled fibers captured 67.48% of the Japan containerboard market share in 2025.

- By product type, the Japan containerboard market size for the kraftliners segment is forecast to advance at a 4.41% CAGR through 2031.

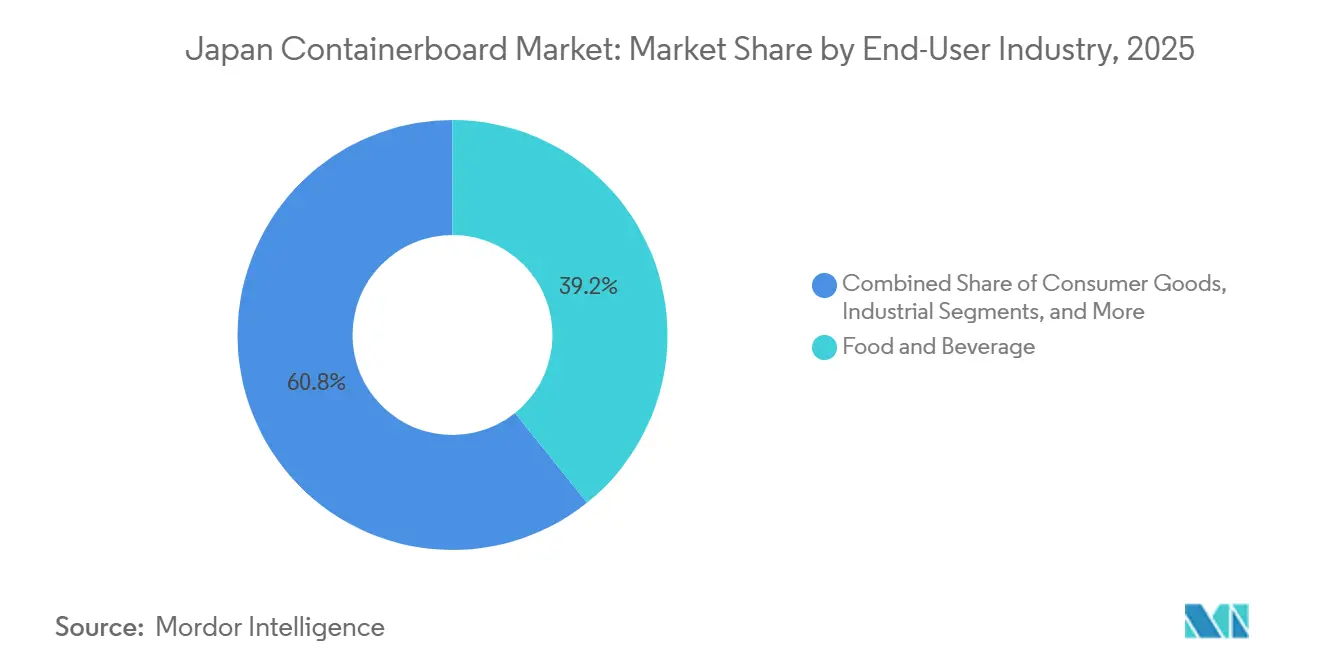

- By end-user industry, food and beverage captured 39.24% of the Japan containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plastic Substitution And Recyclability Preferences | +0.9% | National, with highest impact in Tokyo, Osaka, and major urban retail corridors | Short term (≤ 2 years) |

| E-Commerce And Parcel Delivery Demand | +0.8% | Kanto (Tokyo metro), Kansai (Osaka-Kyoto-Kobe), Chubu (Nagoya) | Short term (≤ 2 years) |

| Stable Food And Beverage Corrugated Consumption | +0.5% | National, concentrated in Hokkaido, Tohoku (seafood and dairy), and Kyushu (agricultural exports) | Medium term (2-4 years) |

| Electronics, Semiconductor, And Industrial Export Packaging Demand | +0.4% | Kyushu (semiconductor cluster), Tohoku (EV battery plants), Kanto | Medium term (2-4 years) |

| Cardboard Cushioning Replacing EPS In Protective Packaging | +0.3% | National, with key activity in Kanto and Kinki distribution centers | Medium term (2-4 years) |

| Lightweight And Automation-Ready Board Demand From Logistics Reform | +0.2% | National, accelerated in Kanto and Kansai mega distribution centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plastic Substitution And Recyclability Preferences

Japan's mandated move away from fossil-derived plastics is widening the addressable demand base for the Japan containerboard market.[1]Keitaro Tsuji, “Japan's Policy Related to Plastic Resource Circulation,” Ministry of the Environment, Japan, iges.or.jp The positive-list system for synthetic food-contact packaging became fully effective on June 1, 2025, raising compliance requirements for non-paper formats in food-related applications.[2]“Japan - Changes to Rules for Synthetic Food Containers and Packaging,” New Zealand Ministry of Foreign Affairs and Trade, mfat.govt.nz Recycling obligations under the Container and Packaging Recycling Law also improve the relative cost position of mono-material corrugated formats when compared with more complex plastic structures. This means packaging users can move toward paper even when end buyers are not actively selecting sustainable formats, because the economics and compliance burden are shifting upstream. Oji has already quantified that direction by targeting a reduction of 5,000 tonnes of plastic annually through sustainable packaging substitution by FY2030, up from 3,000 tonnes achieved in FY2024. This gives the Japan containerboard market a policy-backed demand channel that does not rely on short-term consumer sentiment and is likely to remain relevant across food, retail, and transport packaging decisions.

E-Commerce And Parcel Delivery Demand

Japan's digital retail economy is changing both how much board is used and what box specifications are needed in the Japanese containerboard market.[3]“Analysis of Growth Outlook for Japan's Overall E-Commerce Market,” Japan E-Commerce Association, en.jasec.or.jp Japan's B2C e-commerce market reached JPY 26.1 trillion (USD 186.4 billion) in FY2024, up 5.1% year on year, and cross-border purchases of Japanese products totaled JPY 5.78 trillion (USD 41.3 billion). Food and beverage e-commerce reached JPY 3.12 trillion (USD 20.6 billion), driving demand for insulated, moisture-resistant corrugated shippers used in cold and fresh delivery formats. The 2024 overtime cap for truck drivers is also pushing fulfillment operators toward thinner and more exact-fit boxes that reduce dimensional-weight charges and improve loading efficiency. Rengo's J-RexS automatic packaging machine, launched in January 2025, shows how equipment innovation is helping distribution centers produce right-sized corrugated cases at scale. Together, these shifts show that the Japan containerboard market is benefiting not only from more parcels but also from a redesign of packaging around speed, cube efficiency, and automated fulfillment.

Stable Food And Beverage Corrugated Consumption

Food and beverage remains the most stable demand base in the Japan containerboard market because essential distribution volumes do not depend on discretionary online spending or short-lived retail cycles. Processed food, grocery delivery, and fresh-produce shipments are increasing the use of moisture-resistant corrugated shippers in cold-chain routes across both store replenishment and home delivery channels. Retailers and packaging users are also replacing EPS coolers and some plastic clamshells with wax-free or paper-based alternatives in selected food logistics applications. This keeps paper-based transport packaging relevant in both domestic distribution and export-oriented food supply chains, even when overall box demand is not particularly fast. The segment also offers producers a more dependable base load, as everyday food flows continue even when industrial shipments soften temporarily. That stability matters in the Japan containerboard market because it supports mill utilization and converter throughput while other end uses move through more cyclical phases.

Electronics, Semiconductor, And Industrial Export Packaging Demand

Japan's semiconductor and industrial policy is opening a higher-margin demand pocket inside the Japan containerboard market.[4]“Semiconductor and Digital Industry Strategy (Revised),” Ministry of Economy, Trade and Industry, meti.go.jp Subsidized foundry investment, including activity around Kumamoto and EV-related manufacturing in Tohoku, is increasing demand for triple-wall and anti-static corrugated packaging. These applications need stronger burst and ring-crush performance, which supports the rising use of premium kraft-based grades in the Japanese containerboard market. Clean-room and electrostatic-discharge requirements are also pushing converters toward tighter quality control than is required for standard domestic shipping boxes. Producers that place technical-grade capacity closer to Kyushu and Tohoku can achieve better pricing than commodity liner suppliers typically do. This matters because it lets the Japan containerboard market generate value growth from specialized grades even when base domestic shipment growth remains measured.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OCC, Energy, And Fuel Cost Volatility | -0.5% | National, with strongest exposure in inland mills and long-haul delivery zones | Short term (≤ 2 years) |

| Competition From Reusable Plastic Crates And Alternative Packaging Formats | -0.3% | Kanto (retail and logistics hubs), Kansai (FMCG distribution) | Medium term (2-4 years) |

| Logistics 2024 Rule Changes Raising Delivered-Cost Pressure | -0.2% | National, particularly remote regions (Hokkaido, Okinawa) and small-lot multi-stop routes | Short term (≤ 2 years) |

| Recovered-Paper Quality Ceiling And Contamination Limits | -0.1% | National, concentrated in high-throughput recycling hubs near Tokyo and Osaka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OCC, Energy, And Fuel Cost Volatility

Input cost swings remain the most direct earnings pressure for producers in the Japan containerboard market. Japanese OCC export prices to Southeast Asia moved from USD 195-205 per tonne in August 2024 to USD 145-150 per tonne in January 2026, which shows how quickly regional recovered-paper values can shift. Domestic recovered-paper inventories also rose 61% year on year by the end of December 2025, which temporarily eased feedstock pressure but also signaled unstable supply-demand conditions. Energy adds a second layer of risk because mills are heavy fuel users, and Rengo completed its coal-to-LNG conversion at Kanazu Mill in FY2025 as part of a broader cost and emissions transition. Even when long-term efficiency improves, these swings in raw materials and fuel prices can compress margins before selling prices fully catch up. This makes procurement discipline and price pass-through a persistent issue across the Japan containerboard market, especially for producers exposed to inland transport and volatile export-linked recovered-paper flows.

Competition From Reusable Plastic Crates And Alternative Packaging Formats

Reusable plastic crates and other returnable formats continue to pose a structural challenge in selected parts of the Japan containerboard market. They are most competitive in closed-loop food-service and automotive routes where high-frequency returns make reuse economically attractive and disposal costs are limited. Recycling-cost obligations for single-use packaging also raise the cost burden on corrugated formats in institutional settings, where reuse economics are easy to measure. That risk is highest in urban processed-food distribution, where box volumes are large, and route density is high. The pressure is partly offset by Japan's logistics reform, as tighter driver availability increases the handling burden for reverse logistics pickup runs that reusable crates depend on. Even so, this remains a real substitution threat for the Japan containerboard market, particularly on specific closed-loop routes where corrugated does not enjoy a clear convenience or cost advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominates, But Virgin-Fiber Growth Signals A Specification Upgrade

Recycled fibers held 67.48% of the Japan containerboard market share in 2025, making them the clear base material across the market. That lead reflects Japan's long-established preference for recovered paper in standard shipping, retail transit, and everyday distribution formats where availability and cost control matter most. Domestic mills rely heavily on recycled inputs for testliners and recycled fluting because these grades fit the needs of broad domestic box demand without requiring premium fiber costs. Established collection habits and disciplined sorting also help keep recycled inputs usable at scale, which supports stable output for mass-market packaging applications. As a result, recycled fibers remain the default choice where price stability, local availability, and predictable performance matter more than the absolute highest strength profile.

Virgin fibers are projected to expand at a 4.32% CAGR from 2026 to 2031, indicating that a portion of the Japan containerboard market is shifting toward higher-performance packaging. This growth is tied to export-grade industrial packaging and electronics shipments that require better ring-crush strength and burst resistance than recycled liners can consistently deliver in demanding applications. Daio started operations at its commercial cellulose nanofiber plant in Mishima in July 2025, with an annual capacity of 2,000 tonnes, 20 times its earlier scale. That investment suggests the material gap may narrow over time as producers develop thinner but stronger board structures for logistics and packaging uses. The direction of travel is clear in the Japan containerboard market; recycled fibers still anchor broad volume demand, while virgin-fiber growth is being pulled by applications where technical performance justifies a higher input profile.

By Product Type: Testliners Anchor Volume, While Kraftliners Capture The Margin Premium

Testliners accounted for 43.66% of the Japan containerboard market in 2025, keeping them at the center of volume demand. Their leadership reflects the strength of recycled-fiber-based supply in domestic consumer, food, and general merchandise logistics, where standard corrugated formats dominate shipment flows. Testliners fit a wide range of everyday box specifications, which makes them the practical workhorse for national distribution and routine warehouse replenishment. Flutings remained important as the middle layer in corrugated board, where producers compete mainly on scale, availability, and proximity to converters serving standard packaging needs. This mix favors mills with reliable access to recovered fiber, large-scale output, and regional delivery networks that can support a stable converter supply.

Kraftliners are forecast to grow at a 4.41% CAGR from 2026 to 2031, reflecting a shift toward stronger, more specialized packaging applications. Export packaging for semiconductor equipment, industrial goods, and food products is increasing demand for higher burst strength, moisture resistance, and certification-ready paper grades. Rengo's second biomass boiler at Yashio Mill, backed by JPY 9 billion (USD 60.1 million) of investment and scheduled for commissioning in FY2026, is expected to cut CO2 emissions by 25,000 tonnes annually and strengthen the cost base for higher-grade liner production. Recycling obligations across the packaging value chain also encourage lighter board designs that can reduce material use without sacrificing performance. This is why the Japanese containerboard market is seeing volume anchored by testliners, while value and margins are increasingly tied to kraftliner demand in higher-specification end uses.

By End-User Industry: Food And Beverage Holds The Base, While Consumer Goods Sets The Growth Pace

Food and beverage accounted for 39.24% of Japan's containerboard market share in 2025, making it the largest end-use segment. The segment remains resilient because food distribution moves daily and is less exposed to discretionary spending swings than many other packaging categories. Processed food, grocery delivery, and fresh-produce fulfillment are driving the use of insulated, moisture-resistant corrugated shippers across domestic logistics. Paper-based formats are also replacing EPS coolers and some plastic clamshells in selected food logistics applications where recyclability and material simplicity matter more. This keeps base demand steady even when broader corrugated shipment growth is modest, which is why food and beverage continues to underpin the Japan containerboard market.

Consumer goods are projected to grow at a 4.48% CAGR from 2026 to 2031, making them the fastest-moving end-user pocket in the Japan containerboard market. Direct-to-consumer subscriptions, beauty e-commerce, premium household goods, and short-run branded shipping formats are supporting that pace. These categories often require precise sizing, cleaner print presentation, and lighter box formats that still protect goods during transit through parcel networks. Industrial demand remains important as automotive, precision manufacturing, and semiconductor shipments continue to require heavy-duty recyclable transport packaging. Oji demonstrated a closed-loop application at Expo 2025 Osaka in May 2025, where aseptic carton packages were recycled into corrugated boxes with Tetra Pak Japan and Gold Pak. This balance between essential food shipments, faster-growing consumer parcels, and durable industrial demand gives the Japan containerboard market a broader end-use base than a simple retail packaging story would suggest.

Geography Analysis

The Kanto area remains the dominant consumption hub within the Japan containerboard market because it combines the country's largest population base with the densest concentration of warehouses and retail flows. The Tokyo-Osaka corridor carries the broadest mix of food processing, distribution center activity, and e-commerce fulfillment in Japan. This concentration makes plant location more important as freight costs rise across the Japan containerboard market. Japan's April 2024 overtime cap for truck drivers, set at 960 hours annually, increased delivered-cost pressure on long-haul routes and reduced flexibility in transport planning. Rengo's 35-plant corrugated network across Japan gives it a structural advantage in this environment because shorter average delivery distances support service reliability and cost control.

Kyushu is emerging as the strongest product-mix upgrade zone in the Japan containerboard market, as semiconductor investment is boosting demand for higher-specification boxes. Subsidized projects in Kumamoto and other industrial areas are increasing demand for triple-wall, anti-static corrugated packaging for semiconductor equipment and components. The region also sits close to key Asian sea lanes, which support the dispatch of kraftliner-heavy packaging for industrial and food-related shipments. Hokkaido and Tohoku remain important for seafood, dairy, and agricultural shipments that need wax-free or barrier-coated corrugated transport packaging. These northern regions also matter because temperature-sensitive goods tend to require sturdier outer packaging and more consistent handling performance than basic dry-goods distribution.

Kinki, centered on Osaka, Kyoto, and Kobe, forms the third strategic demand node in the Japan containerboard market with strong pull from food and beverage processors, healthcare distributors, and e-commerce operators. Oji's Expo 2025 Osaka recycling project also showed how the region can function as a commercial test bed for new circular containerboard applications. Japan's 93% paper and paperboard self-sufficiency rate gives the Japan containerboard market size a domestic supply buffer against import cost swings and currency pressure. Demand growth is likely to stay measured, so future gains in the Japan containerboard market will depend more on mix improvement and premium grades than on a sharp rise in basic box volumes.

Competitive Landscape

The Japan containerboard market combines high concentration at the mill level with fragmentation at the converting level. The top four producers control approximately 65% of domestic board capacity, while more than 400 independent converters still serve regional and specialty customers. This structure gives large mills the advantage in fiber procurement, energy investment, and national supply contracts. It also leaves room for smaller converters that can win business through customization, fast turnaround, and local delivery service. Oji held 25.8% of domestic paperboard production volume in 2024 and is shifting its portfolio toward sustainable packaging and forest-biomass businesses.

Oji's Medium-Term Management Plan 2027 set out JPY 270 billion (USD 1.8 billion) of growth investment and targeted sustainable packaging revenue of JPY 128 billion (USD 0.9 billion) by FY2027, up from JPY 70 billion (USD 0.5 billion) in FY2024. Its April 2024 acquisition of Walki Holding Oy added paper-based laminate and barrier capability that can help corrugated formats replace more plastic-intensive packaging structures in moisture-sensitive uses. Rengo completed coal-to-LNG conversion at Kanazu Mill in FY2025, cutting CO2 emissions by 130,000 tonnes as it improved the operating base for future production. Rengo also expanded its international footprint through the JPY 25.4 billion (USD 169.7 million) investment in TRICOR Packaging and Logistics AG in Goch, Germany, where production began in July 2025. These moves show that leading companies in the Japan containerboard market are competing through technology, decarbonization, and network strength rather than only through commodity output.

Daio strengthened its technical position in July 2025 by commencing commercial operations at its 2,000-tonne cellulose nanofiber plant in Mishima, which supports the production of thinner, stronger packaging materials. That focus on fiber science matters because automation-ready, lightweight boards and anti-static, high-burst corrugated remain open spaces in the Japan containerboard market. Japan's recycling and plastic-circulation rules are also making documented sustainability performance more important in packaging procurement decisions. Suppliers that can pair technical strength, stable fiber sourcing, and verified sustainability are likely to retain pricing power as the Japan containerboard market shifts toward higher-specification grades.

Japan Containerboard Industry Leaders

Oji Holdings Corporation

Rengo Co., Ltd.

Marusan Paper Mfg. Co., Ltd.

Taiko Paper Mfg., Ltd.

Nippon Paper Industries Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tokushu Tokai Paper Co., Ltd. formulated its 7th Medium-Term Management Plan under "Vision 2035," effective from May 2026, with a focus on resource re-utilization, environmental measures, and new business development, alongside a revised, more generous dividend payout policy.

- March 2026: Daio Paper Corporation completed the acquisition of a 16.24% equity stake in Hokuetsu Corporation from Daio Kaiun Co., Ltd. and Misuga Kaiun Co., Ltd. for JPY 26.3 billion (USD 175.8 million), following a basic strategic alliance announced in May 2024. The transaction rebalances the cross-shareholding relationship and deepens a production-technology and logistics-sharing partnership targeting JPY 20 billion (USD 133.7 million) in combined operating profit improvement by FY2026.

- January 2026: Hokuetsu Corporation established a new International Paper Export Sales Division, effective April 1, 2026, as part of a broader organizational restructuring. Rating and Investment Information upgraded Hokuetsu's issuer credit rating from A- (Positive) to A (Stable) in November 2024, citing portfolio diversification and strengthened cash-flow generation following the strategic divestment of approximately 90% of its Chinese white-paperboard operations.

- January 2026: Tokushu Tokai Paper Co., Ltd. signed a paper-insulation license agreement with Tomoegawa Co., Ltd. following its acquisition of Tomoegawa's functional paper business assets, announced in July 2025. The move extends Tokushu Tokai's specialty materials portfolio into insulation-grade papers, widening its addressable market beyond standard containerboard-adjacent applications.

Japan Containerboard Market Report Scope

The Japan Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Japan Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Japan containerboard market in 2026 and what is the outlook for 2031?

The Japan containerboard market stands at USD 6.86 billion in 2026 and is forecast to reach USD 8.01 billion by 2031, growing at a 3.15% CAGR over 2026-2031.

Which material segment leads demand in Japan?

Recycled fibers led with 67.48% share in 2025, while virgin fibers are the faster-growing material type with a 4.32% CAGR through 2031.

Which product type is strongest in current demand and which one is growing fastest?

Testliners led with 43.66% share in 2025, while kraftliners are projected to grow fastest at a 4.41% CAGR through 2031.

Which end-user group creates the largest pull for corrugated board in Japan?

Food and beverage remained the largest end-user with 39.24% share in 2025, supported by steady daily distribution and rising demand for moisture-resistant shipping formats.

Why is higher-specification board becoming more important in Japan?

Semiconductor, electronics, and export packaging need stronger, cleaner, and more specialized corrugated formats, which is lifting demand for kraftliners, triple-wall boxes, and anti-static solutions.

How is competition structured among suppliers and converters in Japan?

The top 4 producers control around 65% of domestic board capacity, but more than 400 independent converters still compete on service, customization, and regional delivery reach.

Page last updated on: