Singapore Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

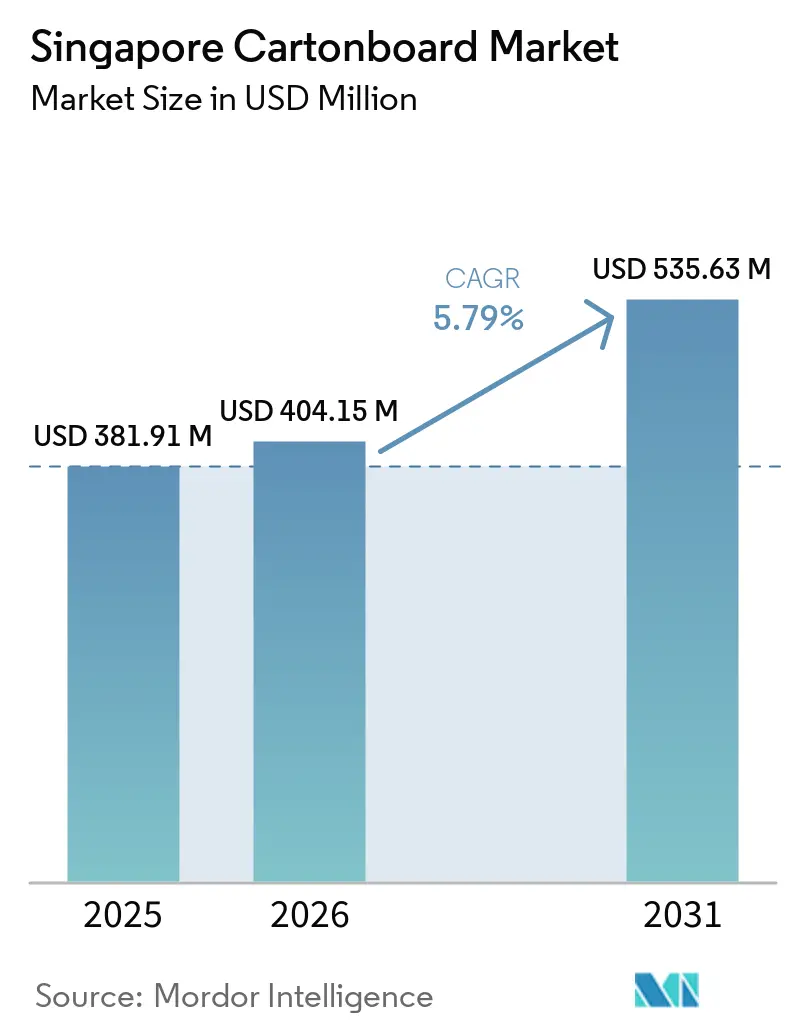

| Base Year Market Size (2025) | USD 381.91 Million |

| Market Size (2026) | USD 404.15 Million |

| Market Size (2031) | USD 535.63 Million |

| Growth Rate (2026 - 2031) | 5.79% CAGR |

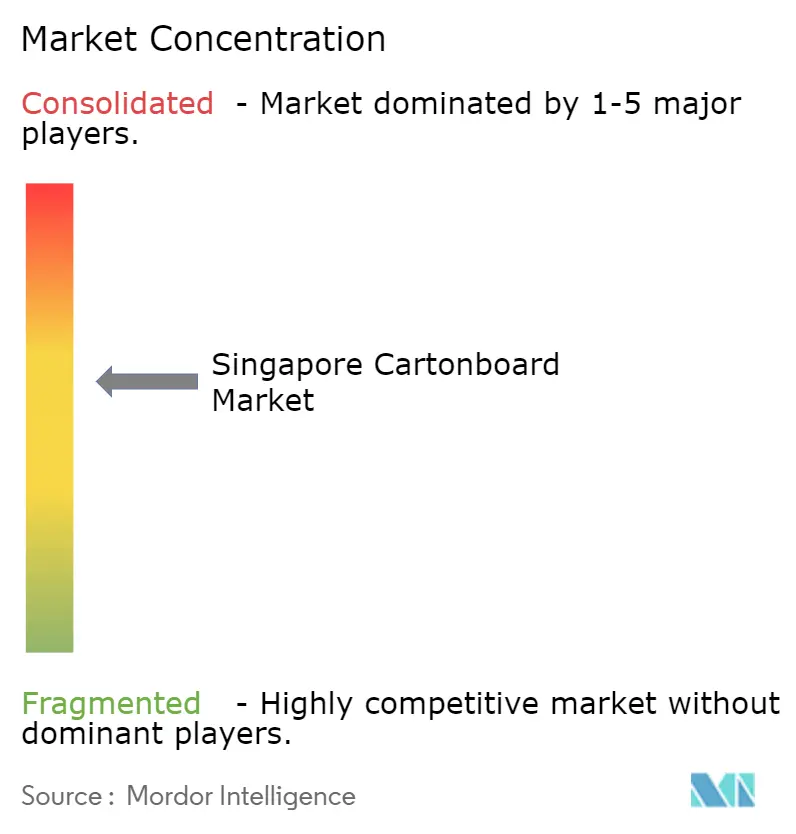

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Cartonboard Market Analysis by Mordor Intelligence

The Singapore cartonboard market size was valued at USD 381.91 million in 2025 and estimated to grow from USD 404.15 million in 2026 to reach USD 535.63 million by 2031, at a CAGR of 5.79% during the forecast period (2026-2031). The market is being shaped by a steady shift toward fiber-based packaging as packaging compliance requirements become more stringent and plastic recovery remains weak. The Singapore cartonboard market is also benefiting from stricter pharmaceutical labeling and traceability rules, which are raising the specification level for outer cartons used in regulated product categories. Foodservice demand is adding another layer of support as delivery-led consumption and modern retail formats keep packaging requirements broad and more quality sensitive. At the same time, the Singapore cartonboard market remains exposed to margin pressure because the country imports all its board requirements, and local converters lack a domestic mill base to offset freight or raw material swings. This leaves growth intact while also keeping the competitive focus on premium grades, compliance-ready conversion, and faster response to specification changes.

Key Report Takeaways

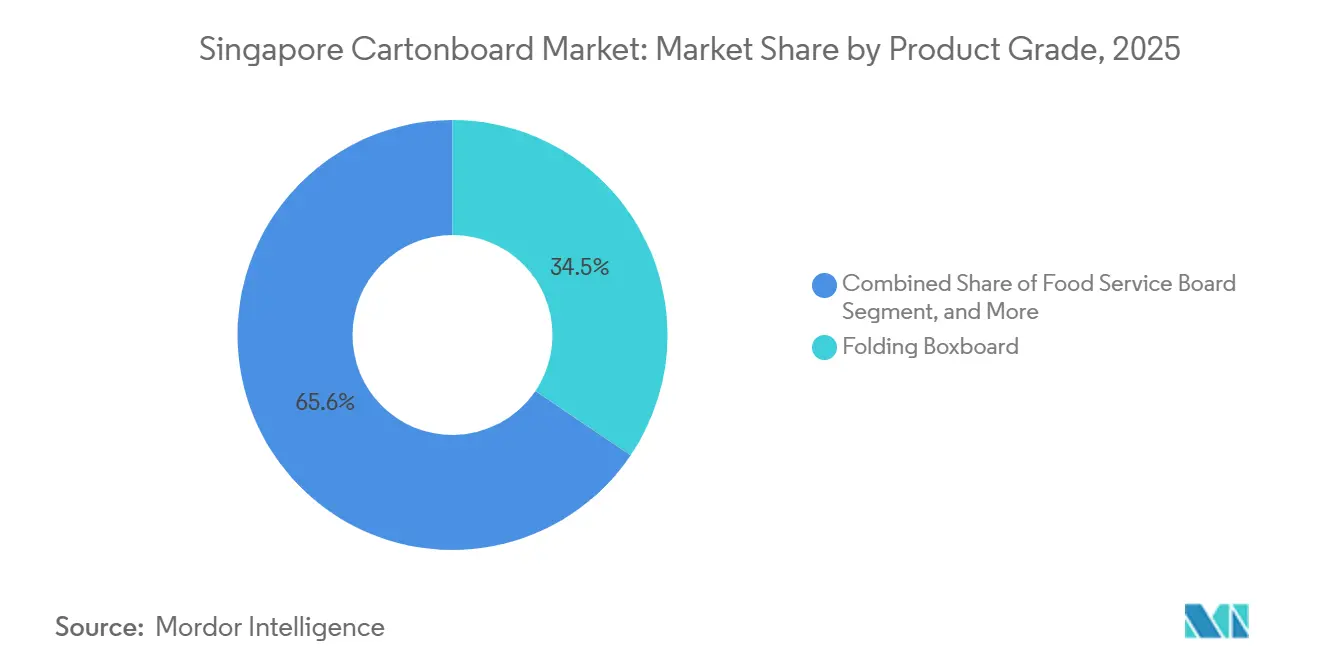

- By product grade, folding boxboard captured 34.45% of the Singapore cartonboard market share in 2025.

- By packaging format, the Singapore cartonboard market size for the liquid packaging segment is forecast to advance at a 6.43% CAGR through 2031.

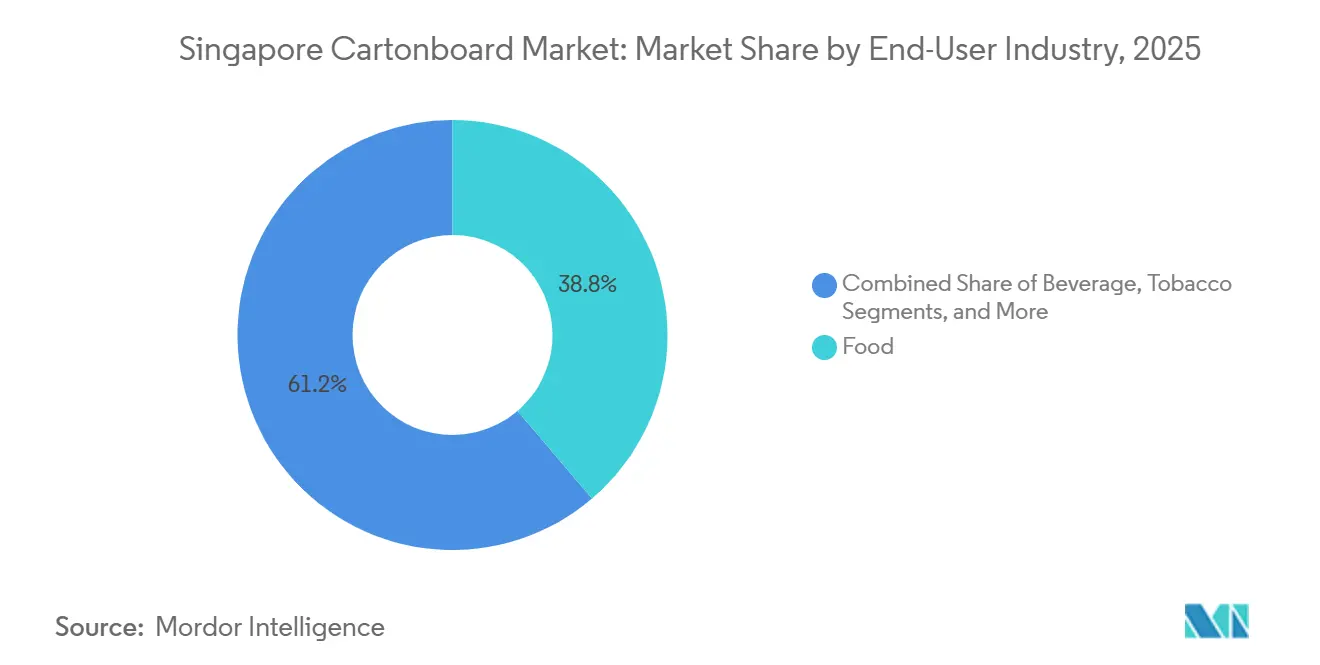

- By end-user industry, food captured 38.76% of the Singapore cartonboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Plastic to Fiber-Based Packaging | +1.3% | Global, with direct policy enforcement in Singapore | Short term (≤ 2 years) |

| Growth in Packaged Food and Beverage Demand | +1.2% | Singapore domestic market, with export-oriented food processors | Medium term (2-4 years) |

| Pharmaceutical and Healthcare Compliance Needs | +0.8% | Singapore as APAC pharmaceutical hub and distribution center | Medium term (2-4 years) |

| Premiumization in Cosmetics and Toiletries Packaging | +0.6% | Singapore domestic retail and regional export channels | Medium term (2-4 years) |

| Tightening Food-Contact Traceability and Import-Compliance Requirements | +0.5% | Singapore, with spill-over to ASEAN sourcing networks | Long term (≥ 4 years) |

| Short-Run SKU Proliferation and Digital Conversion Demand | +0.4% | Singapore domestic converters, particularly in FMCG and food and beverage | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Plastic to Fiber-Based Packaging

The Singapore cartonboard market is receiving direct support from packaging rules that make material reporting and reduction plans more visible and more operational for regulated companies. Singapore’s Mandatory Packaging Reporting scheme requires covered businesses to submit packaging data and annual 3R plans, and the 2025 amendment regulations took effect on July 1, 2025.[1]National Environment Agency, “Mandatory Packaging Reporting,” National Environment Agency, nea.gov.sg The 2025 data submission window ran from January to March 2026, meaning packaging decisions must already align with a tighter reporting structure in the current cycle. Singapore also activated its Beverage Container Return Scheme in April 2026, with a SGD 0.10 (USD 0.07) deposit on plastic and metal beverage containers, keeping paper-based beverage formats outside that levy structure and supporting fiber-based options in adjacent applications.[2]Ministry of Sustainability and the Environment, “Response to Adjournment Motion on Towards a Safer, Plastic-Lite Singapore - Dr Janil Puthucheary,” Ministry of Sustainability and the Environment, mse.gov.sg Only 5% of the plastics generated in Singapore were recycled in 2024, while plastics accounted for nearly 14% of total waste generated, drawing attention to alternatives that create fewer end-of-life concerns in public policy and corporate reporting. In this setting, the Singapore cartonboard market is benefiting not only from substitution away from plastics, but also from the shorter decision window that brand owners now face when they need packaging formats with clearer compliance and food-contact credentials

Growth in Packaged Food and Beverage Demand

The Singapore cartonboard market is also supported by a food and beverage base that needs a broad mix of printed, shelf-ready, transport, and food-contact packaging. Food remained the largest end-user in 2025, accounting for 38.76% of total demand, underscoring the strong link between board consumption and daily packaged food distribution across retail, convenience, and foodservice channels. Folding cartons remained central to this structure because they serve secondary packaging in dry foods, confectionery, ready-to-eat products, and multipack applications that move through organized retail and delivery channels. The Beverage Container Return Scheme, which started in April 2026, also adds another policy signal in favor of fiber-based secondary and complementary packaging formats for beverage sales. Within the Singapore cartonboard market, this demand is not only volume-led, as the product mix is also moving toward formats that require better print finish, greater stiffness, and more reliable food-contact performance. That mix shift helps converters defend value even when tonnage growth is more measured than the expansion in packaged food offerings.

Pharmaceutical and Healthcare Compliance Needs

Pharmaceutical packaging requirements carry unusual weight in the Singapore cartonboard market because Singapore serves both as a domestic healthcare market and as a regulated distribution point for products moving across Asia-Pacific. The Health Sciences Authority updated its therapeutic product registration requirements, effective July 30, 2025, introducing machine-readable code requirements for outer cartons and labels, including QR codes and barcodes. The same update also tightened information requirements for excipients, container systems, and route-of-administration clarity, thereby increasing the specification burden on carton converters serving pharmaceutical customers. Singapore’s Food Safety and Security Act 2025 also established a formal legal basis for regulating food-contact articles, thereby strengthening the broader compliance case for qualified food-grade and healthcare-grade cartonboard.[3]Singapore Statutes Online, “Resource Sustainability (Packaging Reporting) (Amendment) Regulations 2025,” Singapore Statutes Online, sso.agc.gov.sg Once a packaging design has cleared a regulatory review cycle, switching away from a qualified board grade becomes difficult and costly, providing the Singapore cartonboard market with a stable demand anchor in regulated categories.[4]Health Sciences Authority, “Regulatory Updates for Therapeutic Product Registration (Effective 30 July 2025),” Health Sciences Authority, hsa.gov.sg This is why pharmaceutical demand is growing faster than the broader market, even though it does not represent the largest end-user base by volume.

Premiumization in Cosmetics and Toiletries Packaging

The Singapore cartonboard market is also gaining from premium positioning in cosmetics and toiletries, where outer packaging often carries a strong role in product presentation and perceived quality. Singapore’s beauty retail environment is heavily shaped by premium and imported brands, which tend to favor rigid, well-finished carton formats over lightweight commodity packaging. That preference supports demand for folding boxboard and solid bleached board, as both grades can handle higher print quality and more complex finishing in cartons used for skincare, fragrance, and personal care ranges. Premium packaging also tends to require greater color consistency, better stiffness, and specialty effects such as embossing or foil work, which can lift value per tonne for converters with the right equipment. In the Singapore cartonboard market, that dynamic matters because it creates a segment that is less exposed to price-only competition than standard folding carton work. It also fits Singapore’s role as a launch point for regional consumer brands seeking packaging formats aligned with premium shelf display and a more controlled brand presentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Board and Freight Cost Volatility | -1.1% | Singapore, complete import dependency and no domestic mills | Short term (≤ 2 years) |

| Competition From Lower-Cost Regional Converters | -0.8% | Singapore versus Thailand, Indonesia, Malaysia, and Vietnam | Medium term (2-4 years) |

| Limited Domestic Recovered Fiber Availability | -0.5% | Singapore, no pulping infrastructure and a declining recycling rate | Long term (≥ 4 years) |

| Migration-Testing and Food-Contact Qualification Costs | -0.3% | Singapore, with spill-over to ASEAN export customers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Imported Board and Freight Cost Volatility

The biggest structural limit on the Singapore cartonboard market is the lack of a domestic pulping or papermaking base for cartonboard grades. Local converters have to import folding boxboard, solid bleached board, liquid packaging board, and other grades, which means freight costs and supplier pricing move directly into procurement economics. That dependency matters most when supply routes tighten, because Singapore cannot shift part of its requirements to local mills as larger regional markets can. The same dependence also keeps converters exposed to premium European grades, which are important in pharmaceutical, premium food, and cosmetic applications, where alternative sourcing is limited. In the Singapore cartonboard market, this leaves margins vulnerable even when end-user demand is healthy, because converters can win orders but still struggle to protect profitability when landed board costs stay high. The effect is more severe in standard jobs where customers closely compare prices and have the option to source converted cartons from neighboring countries.

Competition From Lower-Cost Regional Converters

Regional competition is the second major restraint on the Singapore cartonboard market, as domestic converters face structurally higher land, labor, and utility costs than their peers in Thailand, Indonesia, Malaysia, and Vietnam. SCG Packaging reported THB 124,374 million (USD 3,712 million) in revenue from sales in 2025 and announced a 2026 capital expenditure budget of THB 10,000 million (USD 299 million), signaling continued regional capacity investment in consumer packaging and integrated production. Large regional producers also benefit from closer access to pulp, paperboard, or recovered fiber systems, which lowers their cost base in standard folding carton work. This is especially relevant in food and beverage packaging, where brand owners can move high-volume, technically simpler carton orders across ASEAN with limited operational disruption. The Singapore cartonboard market still holds an advantage in short-run, highly specified, or compliance-sensitive work, but that strength does not fully offset the gradual loss of more commoditized jobs. As a result, local converters are being pushed toward premium finishing, digital short runs, and regulated packaging rather than broad volume competition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Anchors the Market While Food Service Board Accelerates

Folding boxboard held 34.45% of the Singapore cartonboard market share in 2025, the largest among product grades, and that position reflects its wide use across food, cosmetics, pharmaceutical, and tobacco packaging. The grade remains central because converters rely on it for strong printability, stiffness, and consistent caliper in applications where shelf appearance and carton performance both matter. Within the Singapore cartonboard industry, folding boxboard also aligns well with the local demand profile, as the market has a premium retail mix and a high share of packaged imported consumer goods that require well-finished secondary packaging. Solid bleached board, solid unbleached board, and white-lined chipboard each continue to serve distinct price and performance niches, with solid bleached board particularly important in pharmaceutical and premium cosmetic uses where cleaner surfaces and strict certification standards carry more weight.

The food service board segment is projected to grow at a 6.27% CAGR through 2031, making it the fastest-growing grade in the Singapore cartonboard market. That growth is tied to rising use of cups, trays, bakery packs, and service containers in delivery-led food consumption and quick-service channels. Stora Enso launched Performa Natura Aqua in April 2026 as a dispersion-coated folding boxboard for foodservice and bakery packaging, with grammages ranging from 195 to 320 g/m², demonstrating how suppliers are tailoring grades to meet grease resistance and improved paper recovery needs. Pharmaceutical demand is also influencing the product mix, as the Health Sciences Authority’s 2025 labeling update highlighted the need for cartons with better printability and machine-readable code integration, which supports the use of higher-caliper premium board in regulated applications.

By Packaging Format: Folding Cartons Lead as Liquid Packaging Claims the Growth Frontier

Folding cartons accounted for 55.38% of the Singapore cartonboard market in 2025, making them the dominant packaging format by a wide margin. Their lead is broad-based because they serve food, pharmaceuticals, cosmetics, and general consumer goods, giving them resilience across multiple end-user cycles. Sleeve and tray formats remain relevant for retail-ready and display-oriented applications, particularly when printed outer presentation supports merchandising in organized retail. This wide application range keeps folding cartons at the center of the Singapore cartonboard market, even as new format innovation is concentrated in more specialized segments.

Liquid packaging is forecast to expand at a 6.43% CAGR through 2031, making it the fastest-growing format in the Singapore cartonboard market. Tetra Pak expanded its paper-based barrier technology to high-speed A3/Speed filling lines in Asia in February 2026, and the resulting Tetra Brik Aseptic 200 Slim carton reached 87% renewable content with a 26% lower carbon footprint per package. SIG Group also reported 7.8% constant-currency and constant-resin revenue growth in Asia-Pacific in Q1 2026, which supports the case for continued regional demand for liquid carton systems. These developments matter because barrier innovation is raising the specification level for boards used in beverage and dairy cartons, which increases value per tonne and makes access to technology more important for suppliers serving Singapore.

By End-User Industry: Food Drives Volume While Pharmaceutical and Healthcare Advances Fastest

Food accounted for 38.76% of demand in 2025, giving it the largest end-user share in the Singapore cartonboard market. That base reflects the city-state’s mature packaged food retail system, its dependence on imported food products, and the resulting need for both primary support packaging and secondary printed cartons across distribution channels. Beverage demand adds to this mix through carton multipacks and liquid packaging formats that align with a broader shift toward recyclable fiber-based packaging for food and drink. In the Singapore cartonboard industry, food remains the volume anchor because it is diversified across dry goods, frozen foods, confectionery, and convenience-oriented formats rather than depending on a single category.

The pharmaceutical and healthcare sector is projected to grow at a 6.61% CAGR through 2031, giving it the fastest expansion rate among end users in the Singapore cartonboard market. The segment is being supported by Singapore’s role as a regulated pharmaceutical logistics and distribution hub and by the Health Sciences Authority’s stricter rules on secondary packaging documentation, machine-readable codes, and product information display. The Food Safety and Security Act 2025 also strengthens the regulatory basis for oversight of food contact articles, supporting higher, more standardized qualification requirements in adjacent packaging categories. Because pharmaceutical filings tend to lock in packaging specifications for longer cycles, converters already qualified for this segment can retain work more consistently than in standard commodity carton applications.

Geography Analysis

Singapore’s cartonboard demand is shaped by geography in a way different from that of larger ASEAN markets, as the country has no domestic pulp or paperboard production base and relies entirely on imports. The Singapore cartonboard market is therefore defined by trade flows, landed costs, and converter access to overseas mills rather than by local mill integration. Premium grades have typically come from Scandinavian suppliers such as Stora Enso, Metsä Board, and Billerud, while more cost-competitive board and converted packaging also come from Indonesia, Thailand, and India, which gives the supply base some diversity but does not remove import dependence. This structure means the Port of Singapore remains central to the movement of both finished cartons and board sheets destined for local conversion, linking the market closely to regional logistics conditions and freight volatility. The country’s lack of local substitution options keeps the Singapore cartonboard market more exposed to shipping disruptions than neighboring markets with domestic paperboard assets.

Within ASEAN, Singapore is small in absolute cartonboard volume, but it is weighted toward higher-specification demand because pharmaceuticals, premium foods, cosmetics, and compliance-sensitive packaging carry a larger role in the local end-user mix. That positioning makes the Singapore cartonboard market different from those in Indonesia, Thailand, and Vietnam, where population scale and local manufacturing drive higher tonnage in standard FMCG packaging. Singapore instead competes on quality, regulatory alignment, and conversion precision, which is why premium board grades and qualified converter relationships matter more than pure volume economics. The Food Safety and Security Act 2025 further strengthens that position by providing a firmer legal framework for regulating food contact articles entering the local market.

Recycling conditions add another geographic constraint because Singapore’s paper recycling rate fell to 32% in 2024 from 52% in 2018, while the domestic recycling rate reached 11% in 2024. Tay Paper Recycling exited in 2024, and the Waste Management and Recycling Association of Singapore reported in 2025 that paper recyclers were scaling down due to low waste material prices and higher operating costs, which weakened economics. Since Singapore has no local pulping facilities, recovered paper must be exported after collection, which removes a potential domestic source of secondary fiber for cartonboard production. For the Singapore cartonboard market, that means converters needing recycled-content credentials must source certified recycled board from overseas mills, often at a premium that competitors in fiber-richer geographies do not face to the same extent.

Competitive Landscape

The Singapore cartonboard market has a moderate competitive structure, with supply anchored by multinational board producers and a more distributed converter base serving the pharmaceutical, food, cosmetics, and general consumer goods sectors. Stora Enso, Metsä Board, and Billerud remain important in premium folding boxboard and liquid packaging board, while PT APP Purinusa Ekapersada and SCG Packaging add pressure in more price-sensitive grades and regional supply options. Local players such as OVOL Singapore Pte. Ltd. and Singapore Cartons (Pte) Ltd. remain relevant because they hold working relationships across FMCG and pharmaceutical packaging chains, where service quality and responsiveness matter as much as substrate access. In the Singapore cartonboard market, competition is no longer centered solely on printed carton output, as the value pool is shifting toward serialization, short-run digital work, premium finishing, and faster turnaround for regulated jobs. That shift is raising the importance of technical capability over simple conversion capacity.

Several strategic moves in 2026 show where supplier priorities are moving. Metsä Board announced its 2026-2030 "Lead the Pack" strategy on March 19, 2026, and identified healthcare, food, and foodservice packaging as the main growth engines, which align closely with the parts of the Singapore cartonboard market expanding fastest. In May 2026, Metsä Board and HEIDELBERG entered a strategic collaboration that combined premium paperboard materials with printing and packaging machinery expertise, giving converters a clearer path to substrate and press optimization in one relationship. Graphic Packaging International also disclosed USD 450 million in capital spending for 2026 in its Q1 filing, including continued investment in international paperboard packaging operations, indicating that global capacity development remains active across the supply chains feeding Asia-Pacific. These moves support the idea that premium board supply and conversion capability are tightening around the same customer groups that matter most in Singapore.

The main white-space areas remain digital short-run pharmaceutical cartons, foodservice conversion for delivery-heavy channels, and sustainable premium packaging for cosmetics and personal care. SCG Packaging’s 2026 investment plan and continued integration efforts underscore how aggressively regional rivals are building scale and automation in consumer packaging, which will keep pricing pressure high in standard jobs. That makes compliance credentials such as ISO 9001 and Health Sciences Authority-aligned manufacturing discipline more important as practical defenses for Singapore-based converters that cannot win on cost alone. The Singapore cartonboard market is therefore likely to remain moderately concentrated on the supply side, but competition in converted packaging will remain active, as buyers can still balance premium local service with lower-cost ASEAN sourcing for less-sensitive work.

Singapore Cartonboard Industry Leaders

PT APP Purinusa Ekapersada

Stora Enso Oyj

Metsä Board Corporation

Mayr-Melnhof Karton AG

Oji Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Metsä Board and HEIDELBERG SE entered a strategic collaboration combining Metsä Board's premium paperboard materials with Heidelberg's printing and packaging machinery expertise. The partnership is designed to help brand-owner customers optimize substrate-and-press configurations for consumer and healthcare packaging, with commercial implications for the Singapore market through Metsä Board's APAC distribution channels.

- April 2026: Stora Enso launched Performa Natura Aqua, a GC2-grade dispersion-coated folding boxboard for foodservice and bakery packaging, available in grammages from 195 to 320 g/m². The board uses a dispersion barrier instead of conventional poly coatings, enabling faster repulping and improved paper recovery, attributes that align with Singapore's NEA packaging reporting obligations and cartonboard-user 3R commitments.

- March 2026: Metsä Board's board of directors approved the company's "Lead the Pack" strategy and financial targets for 2026-2030. The strategy targets annual consumer packaging revenue CAGR exceeding 4% from a 2025 baseline, supported by a EUR 200 million (USD 216 million) EBITDA improvement program launched July 31, 2025. Healthcare, food, and foodservice packaging are identified as the primary growth segments, with a new packaging design studio opened in Milan.

- January 2026: Tetra Pak expanded its paper-based barrier technology to its high-speed A3/Speed filling lines in Asia, with Maeil Dairies of South Korea implementing the technology for its soy milk product. The resulting Tetra Brik Aseptic 200 Slim carton achieved 87% renewable content and a 26% reduction in carbon footprint, establishing a new sustainability benchmark for liquid packaging board specifications in the APAC region, including Singapore.

Singapore Cartonboard Market Report Scope

The Singapore Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include solid bleached board, solid unbleached board, folding boxboard, white-lined chipboard, liquid packaging board, and food service board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Singapore Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and Other Packaging Formats), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics and Toiletries, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of cartonboard demand in Singapore?

The Singapore cartonboard market size stood at USD 381.91 million in 2025, reached USD 404.15 million in 2026, and is forecast to reach USD 535.63 million by 2031 at a 5.79% CAGR.

Which packaging format leads cartonboard use in Singapore?

Folding cartons led demand with a 55.38% share in 2025 because they are used across food, pharmaceuticals, cosmetics, and general consumer goods.

Which product grade is growing the fastest in Singapore?

Food service board is the fastest-growing grade and is projected to expand at a 6.27% CAGR through 2031, supported by delivery-led food consumption and foodservice packaging needs.

Which end-user segment is expanding the fastest?

Pharmaceutical and healthcare is projected to grow at a 6.61% CAGR through 2031 as labeling, traceability, and secondary packaging compliance requirements become stricter.

Why does import dependence matter so much for cartonboard converters in Singapore?

Singapore has no domestic pulping or papermaking base for cartonboard, so converters remain exposed to freight swings, imported board costs, and tighter margins than regional peers with local mill access.

What is the main competitive advantage for local converters in Singapore?

Local converters are strongest in premium, short-run, and compliance-sensitive work, especially pharmaceutical cartons, premium cosmetic packs, and higher-specification printing and finishing jobs.

Page last updated on: