Austria Cartonboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

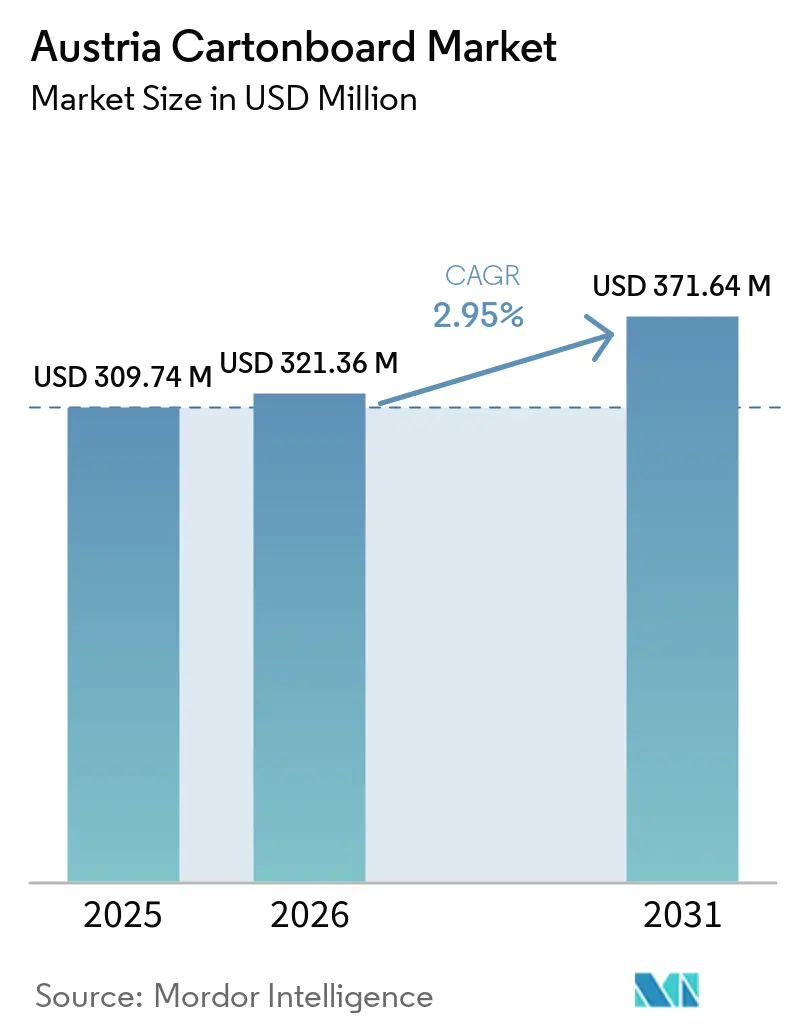

| Base Year Market Size (2025) | USD 309.74 Million |

| Market Size (2026) | USD 321.36 Million |

| Market Size (2031) | USD 371.64 Million |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

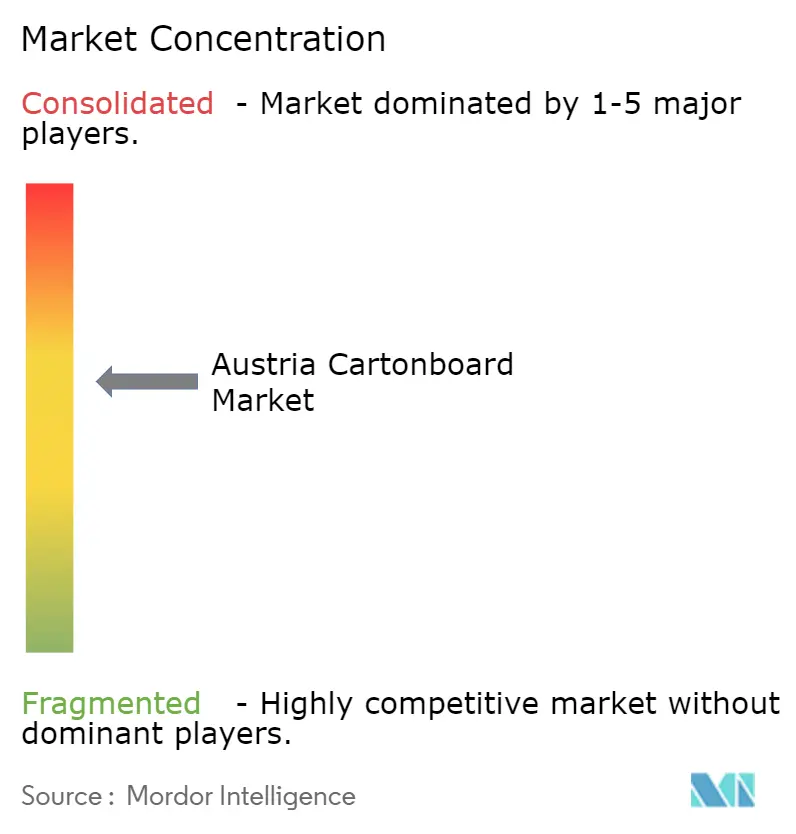

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Cartonboard Market Analysis by Mordor Intelligence

The Austria Cartonboard Market size is projected to be USD 309.74 million in 2025, USD 321.36 million in 2026, and reach USD 371.64 million by 2031, growing at a CAGR of 2.95% from 2026 to 2031.

Growth remains tied to steady packaging demand from food and beverage applications, a well-established pharmaceutical manufacturing base, and Austria’s strong paper and board recycling system. The market also benefits from Austria’s role as both a producer of cartonboard and an importing, converting center within Central Europe, which supports faster sourcing and shorter supply cycles for domestic converters. Premium board grades are gaining importance because pharmaceutical, healthcare, premium food, and cosmetics customers increasingly require better print quality, cleaner surfaces, and stronger compliance performance. At the same time, value-added growth is moving faster than commodity-grade demand as packaging buyers shift toward formats that better align with recycling rules, product differentiation, and retail presentation needs. Cost pressure on pulp and energy remains the main near-term constraint, especially for independent converters that cannot offset input swings through internal fiber supply.

Key Report Takeaways

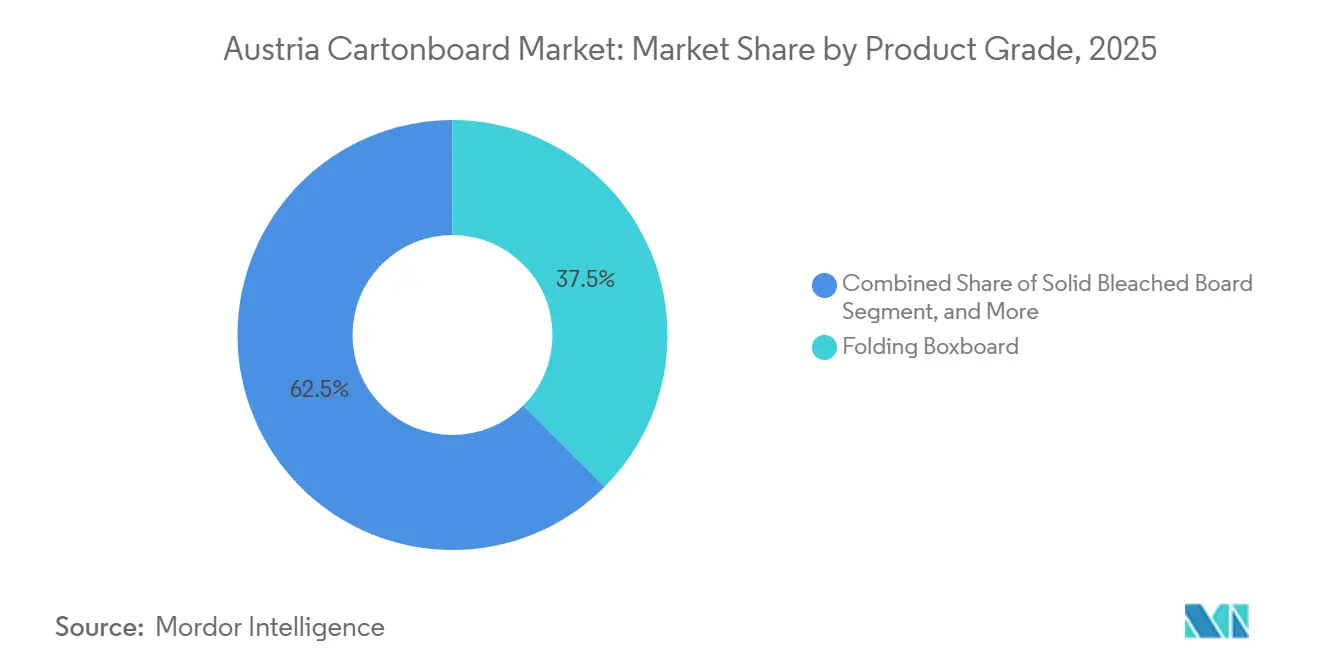

- By product grade, folding boxboard held 46.35% of the Austria cartonboard market in 2025, while solid bleached board is projected to grow at a 5.19% CAGR through 2031.

- By packaging format, folding cartons accounted for 58.34% share in 2025, while liquid packaging is forecast to expand at a 5.42% CAGR through 2031.

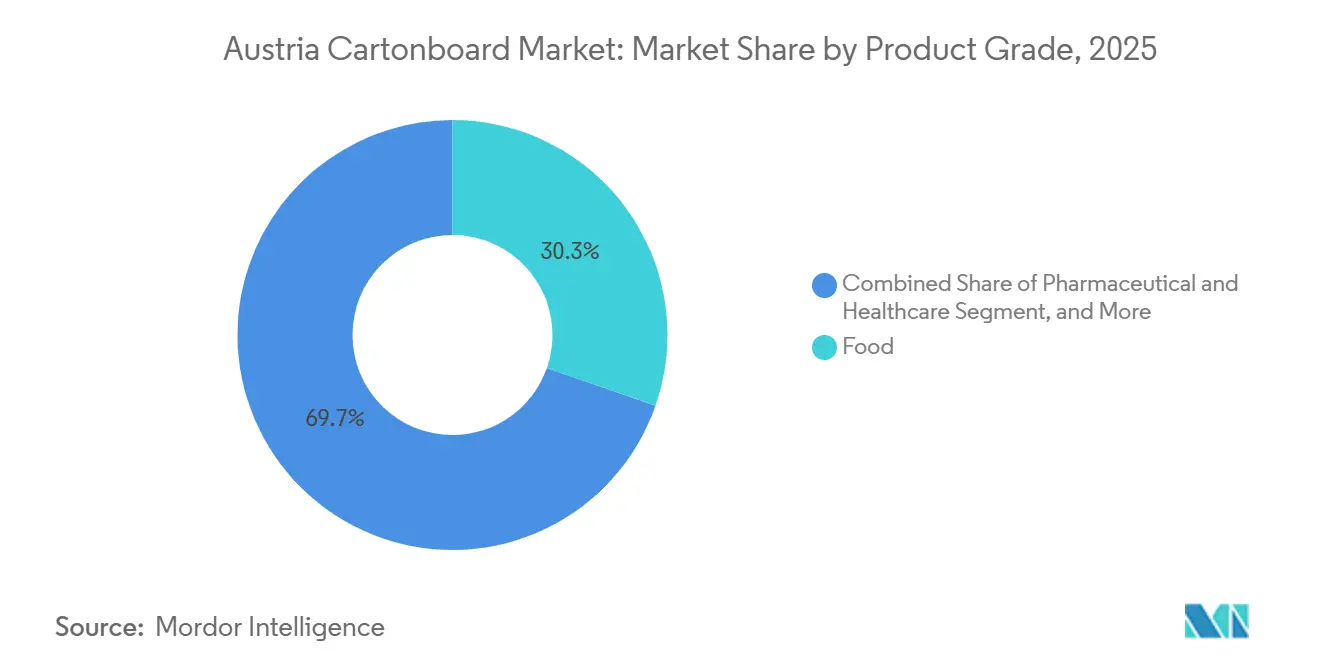

- By end-user industry, food held 31.23% share of demand in 2025, while pharma and healthcare is projected to record the fastest growth at a 5.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Cartonboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Plastic To Fiber-Based Packaging | +0.9% | EU-wide, with Austria and Germany as early-mover markets | Medium term (2-4 years) |

| Strong Food And Beverage Carton Demand | +0.6% | Austria, Central Europe | Short term (≤ 2 years) |

| Premium Pharma And Healthcare Carton Needs | +0.4% | Austria, EU regulatory zone | Medium term (2-4 years) |

| High Recyclability Advantage Of Paper Packaging | +0.3% | EU-wide, Austria leads in collection infrastructure | Long term (≥ 4 years) |

| Aluminum-Free Aseptic Carton Adoption In Austrian Dairy | +0.2% | Austria-specific, with spillover to Germany and Switzerland | Medium term (2-4 years) |

| Organic And Plant-Based Shelf Expansion Raising Premium Carton Needs | +0.2% | Austria and Nordic markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Plastic To Fiber-Based Packaging Drives Structural Demand

Austria’s move from plastic toward fiber-based packaging is already more advanced than in many European markets because paper and board collection systems are stronger and more established. ARA reported plastic recycling at 38% of ARA-licensed volumes in 2025, while paper and board collection performed materially better, which keeps cartonboard in a favorable position for replacement applications.[1]Altstoff Recycling Austria, “Packaging Data And Recycling Performance,” Altstoff Recycling Austria, ara.at The PPWR entered into force on February 11, 2025 and is set to apply from August 12, 2026, which means labeling, recyclability, and recycled-content rules are now shaping packaging decisions well before the full compliance date.[2]European Commission, “Packaging And Packaging Waste Regulation, Regulation (EU) 2025/40,” European Commission Environment, environment.ec.europa.eu A less visible part of this shift is that large Austrian retailers such as BILLA and Spar Austria have been moving own-label packaging toward fiber formats ahead of regulation, which shortens the adoption cycle for cartonboard-based solutions in the Austria cartonboard market. Suppliers with recyclable barrier coatings and heat-sealable grades are therefore in a better position than producers competing only on scale, because conversion readiness has become a practical buying criterion rather than a future requirement.

Strong Food And Beverage Carton Demand Anchors Baseline Volume

Food and beverage demand remains the most stable volume base for the Austria cartonboard market because it draws on a broad mix of bakery, confectionery, chilled meals, frozen food, dairy, and beverage packaging demand. PROPAK reported EUR 515 million, USD 561.4 million, in folding carton and cardboard production value in 2023, which shows the depth of Austria’s packaging conversion base that continued to support demand through 2025. Food alone held 31.23% share in 2025, which kept it as the single largest end-user anchor even while some higher-specification applications expanded faster. Another useful demand layer comes from modified atmosphere packaging trays that combine cartonboard with barrier functionality for chilled convenience foods, because brands want longer shelf life without weakening recyclability claims. Beverage cartons for juices, plant milks, and soups have also expanded as carton formats gained preference in chilled retail settings, which gives the Austria cartonboard market a dependable floor even when premium categories move unevenly.

Premium Pharma And Healthcare Carton Needs Accelerate Upmarket Shift

Pharma and healthcare packaging is reshaping the quality mix in the Austria cartonboard market because board flatness, stiffness, clean print performance, and compliance have become central purchase criteria. EU rules under the Falsified Medicines Directive and Delegated Regulation (EU) 2016/161 made serialization and tamper-evident packaging standard across prescription drug packaging, which narrows the usable board pool for many carton lines. MM Group’s 2025 annual report pointed to growing customer demand for certified tamper-evident grades in healthcare packaging, which supports the segment’s 5.14% CAGR through 2031. Austria also benefits from local production facilities linked to Boehringer Ingelheim, Novartis, and Pfizer, which gives converters access to a concentrated, high-value customer base with strict packaging standards. That geographic closeness improves lead times and scheduling flexibility, so domestic converters serving pharma customers in the Austria cartonboard market can compete on service reliability as well as on board quality.

High Recyclability Advantage Of Paper Packaging Reinforces Market Position

Austria’s paper and board recovery system gives the Austria cartonboard market a structural advantage because post-consumer fiber can return into local or regional mill systems with much less friction than competing substrates. The Austrian Federal Packaging Ordinance set a 75% paper and board recycling target from 2025 and an 85% target from 2030, which gives long-range visibility to recycled-fiber availability and compliance planning. This matters at brand-owner level because certified recyclability has become part of retail negotiations and sustainability disclosures, not only a waste-management issue. The benefit is especially clear in foodservice and retail-ready formats, where single-material trays and sleeves can replace more complex laminate combinations that are harder to collect and sort. Producers that keep developing water-based and dispersion barrier coatings are aligning with a regulatory setting that rewards recoverable packaging, which should preserve cartonboard’s position well beyond the current cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pulp And Energy Cost Volatility | -0.5% | Global, particularly EU integrated mills | Short term (≤ 2 years) |

| Competition From Flexible Packaging And Rigid Plastics | -0.3% | Global | Long term (≥ 4 years) |

| Reuse Mandates Limiting Single-Use Foodservice Board Upside | -0.2% | EU-wide, Austria as early mover | Medium term (2-4 years) |

| PPWR Compliance Burden On Design, Labeling, And Traceability | -0.2% | EU-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pulp And Energy Cost Volatility Compresses Converter Margins

Pulp and electricity costs remain the main near-term restraint on the Austria cartonboard market because both affect board production economics and converter purchasing conditions at the same time. Billerud reported that European cartonboard demand stayed weak through 2025, while input conditions remained difficult, and Metsä Board’s comparable operating result fell to EUR -80.2 million, USD -87.4 million, in FY2025, showing how margin pressure reached even major producers. The pressure is more severe for smaller Austrian converters because they buy board and pulp at market rates and do not have internal recovered-fiber streams to smooth cost swings. Contract price pass-through often takes 3 to 6 months, so margins can tighten before customer pricing adjusts, which leaves non-integrated players at a disadvantage in the Austria cartonboard market. Unless European energy conditions normalize more fully, cost volatility will continue to favor integrated groups with stronger sourcing control and balance-sheet flexibility.

Competition From Flexible Packaging And Rigid Plastics Persists In Niche Applications

Flexible packaging and rigid plastics still hold ground in several applications where barrier needs, moisture resistance, or installed equipment make substrate switching slower. In processed food, frozen items, portion packs, and snack applications, flexible formats remain hard to replace because metallized film and retort pouch lines are already in use and continue to serve specific barrier requirements. In fresh produce and bakery, PET clamshells and polypropylene trays remain present because cartonboard often needs extra coating layers to match moisture performance in those uses. Another brake on switching is the installed-base effect, since thermoforming equipment already operating in Austrian food plants can stay in service for 5 to 8 years after a packaging redesign decision. That means the Austria cartonboard market is likely to gain share progressively rather than evenly, with some of the larger substitution gains arriving later in the 2026-2031 period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Folding Boxboard Leads While Premium Grades Gain Ground

Folding boxboard accounted for 46.35% share of the Austria cartonboard market size in 2025, which kept it as the leading product grade across food, pharmaceutical, and cosmetics carton applications. Its strong stiffness-to-weight performance and dependable printability continue to make it suitable for a wide range of folding carton uses, including lines that now require better coding and serialization quality. Solid bleached board is projected to grow at a 5.19% CAGR through 2031, which makes it the fastest-growing product grade as demand shifts toward cleaner surfaces, high brightness, and stronger hygiene assurance. This split between the largest grade and the fastest-growing grade shows that the Austria cartonboard market is still anchored in mainstream converting demand, while value growth is moving toward higher-specification board.

Solid unbleached board and white-lined chipboard continue to serve cost-sensitive applications where stiffness and functional performance matter more than premium print finish. SUB remains relevant in alcohol outer cartons, while WLC still supports shelf-ready and shipping-oriented applications, although it faces pressure as food brands move toward brighter presentation formats. The Austria cartonboard industry is also seeing food service board and liquid packaging board remain smaller in volume but strategically important in conversion planning, especially as food contact rules and municipal restrictions reshape format selection. MM Group’s continued investment in coated mechanical grades across its Central European converting network supports this direction, because producers are gradually favoring higher-value folding boxboard and solid bleached board over slower-moving commodity grades. The result is a product mix where premium grades are expanding faster than the overall Austria cartonboard market, even though traditional folding boxboard still carries the largest revenue base.

By Packaging Format: Folding Cartons Stay Dominant As Liquid Packaging Accelerates

Folding cartons held 58.34% of the Austria cartonboard market share in 2025, which confirms that the conventional carton remains the basic workhorse format across food and pharmaceutical packaging. The segment continues to benefit from its wide compatibility with established packing lines, its design flexibility, and its fit with both high-volume and mid-volume production runs. At the same time, liquid packaging is set to expand at a 5.42% CAGR through 2031, which makes it the fastest-growing format as dairy and plant-based beverage producers move toward aluminum-free aseptic structures. This balance shows that the Austria cartonboard market is still led by established folding cartons, while the faster format innovation is taking place in beverages and adjacent liquid applications.

The makeup of folding carton demand is also changing within the segment. Short-run digital printing for gifting, seasonal packs, private-label launches, and pharmaceutical starter kits is gaining relevance because customers want lower minimum volumes and better version control. That shift broadens the use case for cartonboard in categories that previously leaned on packaging formats with less design flexibility or higher order thresholds. SIG’s partnership with Berglandmilch, launched in September 2025, brought aluminum-free aseptic cartons into Austrian commercial production and documented a 22% reduction in CO₂ emissions per carton compared with standard aluminum-barrier formats. That move supports the view that liquid packaging is not just expanding in volume, it is also raising the technical and sustainability value of the Austria cartonboard market.

By End-User Industry: Food Holds Scale While Pharma Lifts Specification Demand

Food held 31.23% of the Austria cartonboard market in 2025, which kept it as the largest end-user segment across dry foods, confectionery, frozen products, chilled meals, and produce packaging. That scale gives the market a stable demand base, because food packaging is less exposed to abrupt swings than smaller premium categories. Pharma and healthcare is forecast to grow at a 5.14% CAGR through 2031, which makes it the fastest-expanding end-user group as packaging specifications continue to tighten. In practical terms, this means the Austria cartonboard market is led by food in volume and current value, while healthcare has become the main source of upmarket growth.

Austria’s pharmaceutical base around Vienna and Graz supports this change because manufacturers in those clusters operate under strict EU Good Manufacturing Practice requirements that directly affect substrate choice. Board flatness, surface quality, print precision, and low migration performance exclude lower-specification grades from many healthcare folding carton lines, which supports premium-grade demand. Beverage packaging is also changing internally, since plant-based and ambient dairy alternatives are moving into carton formats faster than carbonated drinks are leaving PET. Cosmetics and toiletries remain smaller by volume but attractive by value because high-gloss finishes, bright surfaces, and premium shelf appearance support coated solid bleached board usage. The Austria cartonboard industry also retains a diversified long tail through tobacco, toys, apparel, household goods, electrical goods, automotive parts, and foodservice, which helps reduce dependence on any single customer group.

Geography Analysis

Austria occupies an unusual place in Europe because it combines domestic converting capability with meaningful dependence on imported primary board from Nordic and Central European mills. PROPAK reported EUR 515 million, USD 561.4 million, in folding carton and cardboard production value in 2023, of which EUR 311 million, USD 339.0 million, was exported, which shows the scale of Austria’s converting strength relative to its size.[3]PROPAK Austria, “PROPAK Jahresbericht 2023/2024 - Folding Carton And Cardboard Production Data,” Advantage Austria, advantageaustria.org This structure gives the Austria cartonboard market a practical advantage because converters can pair nearby end users with short-haul inbound board supply from strong regional mill networks. It also means demand growth through 2031 will not depend only on domestic consumption, since Austria’s role as a conversion platform links local operations to wider Central European packaging demand.

Demand inside Austria is centered around industrial and consumer clusters in Vienna and Lower Austria, where pharmaceutical and consumer goods manufacturing are concentrated, and in Upper Austria and Styria, where food and beverage production support steady carton volumes. That regional footprint is important because it keeps many converters close to the sectors that now require faster lead times, smaller runs, and tighter packaging compliance. Mayr-Melnhof Karton AG’s headquarters and production footprint place a major board producer at the center of this domestic supply geography, which is unusual in Europe and improves coordination across sourcing, conversion, and customer service. The Verpackungsverordnung 2014 also strengthens the domestic position of cartonboard because its 75% paper and board recycling target from 2025 and 85% target from 2030 align with a collection system that is already operational at scale.

Austria’s broader regional role adds another layer to the Austria cartonboard market because converters in the country regularly serve Czechia, Slovakia, Slovenia, and Hungary from single production sites. That cross-border model matters as pharmaceutical packaging demand rises in nearby Central and Eastern European economies with growing generic drug manufacturing bases. Organic and plant-based food brands also add to local premium packaging activity because Austria recorded the highest per-capita organic food expenditure in the EU in 2024, which supports demand for shorter print runs, stronger shelf presentation, and higher-brightness cartons. Austria’s compact geography further helps premium coated grades move quickly from Nordic mills to local converters, which reduces safety-stock needs and supports just-in-time procurement across the Austria cartonboard market.

Competitive Landscape

The Austria cartonboard market is moderately concentrated at the producer level, with Mayr-Melnhof Karton AG holding a structurally strong position through its scale in recovered-fiber processing and regional converting operations. MM Group’s 2025 revenue reached EUR 3,885.3 million, USD 4,235.0 million, and its Fit-for-Future program delivered EUR 70 million, USD 76.3 million, in cost improvements, which shows that the group is actively reshaping margins and portfolio focus rather than only defending volume.[4]Mayr-Melnhof Karton AG, “Annual Report 2025,” MM Group, mm.group At the converting tier, however, competition is much more dispersed, with Cardbox Packaging, Van Genechten Packaging, Schwarzach Packaging, and specialist pharmaceutical packagers competing alongside larger multinational groups. This creates a two-level competitive structure in the Austria cartonboard market, where board production is more consolidated but conversion remains fragmented and service-driven. That split matters because integrated producers can absorb fiber and energy shocks more effectively than smaller independent converters operating on tighter spreads.

Strategic repositioning has become a clear feature of competition. MM Group completed the sale of its TANN packaging business in June 2025, which sharpened its focus on core cartonboard activities and higher-specification board segments. Metsä Board announced a collaboration with HEIDELBERG in May 2026 to connect cartonboard surface data with digital press controls, which aims to reduce print waste and improve quality consistency for converters serving premium food and pharmaceutical customers. Metsä Board also completed the acquisition of a folding carton converting business in Winschoten in April 2026, which extends its integrated supply-and-convert model in Europe. These moves show that the Austria cartonboard market is increasingly shaped by players that combine substrate capability, conversion reach, and process-data value.

Product and format innovation is another active front. SIG’s Austrian dairy partnerships with Berglandmilch and SalzburgMilch moved aluminum-free aseptic carton formats closer to retail scale, which strengthens differentiation in liquid packaging and raises the competitive bar for beverage-related board supply. Smaller suppliers such as WEIG Group and Pankaboard Oy compete through specialist niches, including grease-resistant food service board and ultra-clean solid bleached grades, rather than by matching the scale of larger integrated groups. Sappi’s proposed closure of the Alfeld mill in Germany would remove around 90,000 tonnes per year of coated specialty paper and board capacity from the European system, which could tighten availability in some coated grades and support pricing for nearby competing mills. The PPWR application date in August 2026 is also becoming a competitive filter, because converters and board suppliers that secured compliant substrate approvals earlier are in a stronger position to win multi-year contracts in the Austria cartonboard market.

Austria Cartonboard Industry Leaders

Mayr-Melnhof Karton AG

Metsä Board Corporation

SIG Group AG

Graphic Packaging International LLC

RDM Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Metsä Board Corporation and Heidelberger Druckmaschinen AG (HEIDELBERG) announced a technical collaboration on May 7, 2026, integrating cartonboard surface quality data into digital press control workflows, enabling real-time compensation for board micro-variations during print runs. The initiative targets measurable waste reduction and improved quality consistency for pharmaceutical and premium food carton converters, and positions Metsä Board's coated grades as process-data-compatible from the start of the print run.

- April 2026: Metsä Board reported the completion of its acquisition of a folding carton converting business in Winschoten, the Netherlands, as part of its Q1 2026 results released on April 29, 2026. The acquisition extended the company's downstream presence in European cartonboard converting and created an integrated supply-and-convert model that reduces procurement complexity for customers sourcing directly from the producer.

- March 2026: MM Group published its full-year 2025 Annual Report on April 8, 2026, confirming EUR 3,885.3 million (USD 4,235.0 million) in consolidated revenue and Fit-For-Future structural savings of EUR 70 million (USD 76.3 million). The group signaled further portfolio optimization toward healthcare and premium food cartonboard grades, with a target of EUR 250 million (USD 272.5 million) in cumulative Fit-For-Future contribution by 2027.

Austria Cartonboard Market Report Scope

The Austria Cartonboard Market encompasses the production, distribution, and application of cartonboard materials for packaging. Key product grades in the market include Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board. These grades are used across various packaging formats, including folding cartons, liquid packaging, sleeves, trays, cups, and foodservice containers. Due to their recyclability, printability, and sustainable packaging attributes, these cartonboard solutions are widely used across sectors such as food, beverage, pharmaceuticals, tobacco, cosmetics, and more.

The Austria Cartonboard Market is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, Other Packaging Formats), End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, Other End-User Industries). The Market Forecasts are in Value (USD).

| Solid Bleached Board |

| Solid Unbleached Board |

| Folding Boxboard |

| White-Lined Chipboard |

| Liquid Packaging Board |

| Food Service Board |

| Folding Cartons |

| Liquid Packaging |

| Sleeve and Tray |

| Other Packaging Formats (Cups, Foodservice Containers) |

| Food |

| Beverage |

| Pharmaceutical and Healthcare |

| Tobacco |

| Cosmetics and Toiletries |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

| By Product Grade | Solid Bleached Board |

| Solid Unbleached Board | |

| Folding Boxboard | |

| White-Lined Chipboard | |

| Liquid Packaging Board | |

| Food Service Board | |

| By Packaging Format | Folding Cartons |

| Liquid Packaging | |

| Sleeve and Tray | |

| Other Packaging Formats (Cups, Foodservice Containers) | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Healthcare | |

| Tobacco | |

| Cosmetics and Toiletries | |

| Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice) |

Key Questions Answered in the Report

What is the current and forecast value of the Austria cartonboard space?

The Austria cartonboard market stood at USD 321.36 million in 2026 and is projected to reach USD 371.64 million by 2031, growing at a 2.95% CAGR over 2026-2031.

Which product grade leads demand in Austria?

Folding boxboard led in 2025 with 46.35% share by value, supported by its wide use across food, pharmaceutical, and cosmetics carton applications.

Which packaging format is expanding the fastest in Austria?

Liquid packaging is the fastest-growing format, with a projected 5.42% CAGR through 2031, driven by dairy and plant-based beverage shifts toward aluminum-free aseptic cartons.

Why is pharmaceutical packaging becoming more important for cartonboard suppliers in Austria?

Pharma and healthcare is forecast to grow at 5.14% CAGR through 2031 because serialization, tamper evidence, print precision, and compliance standards favor higher-specification board grades.

What is supporting cartonboard adoption over plastics in Austria?

Strong paper and board recovery systems, PPWR-related compliance pressure, and retailer moves toward recyclable fiber packaging are improving cartonboard’s competitive position.

What is the main near-term risk for suppliers and converters?

Pulp and energy cost volatility remains the main risk, especially for independent converters that face delayed cost pass-through and do not have integrated fiber sourcing.

Page last updated on: