IoT Microcontroller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

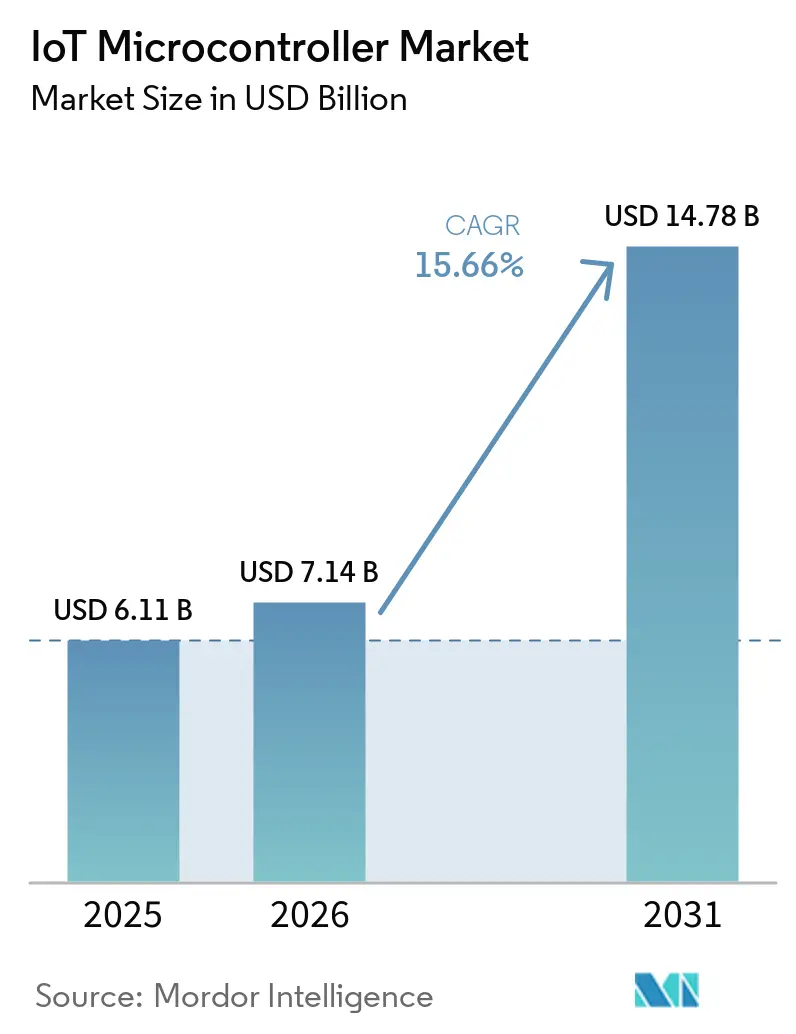

| Market Size (2026) | USD 7.14 Billion |

| Market Size (2031) | USD 14.78 Billion |

| Growth Rate (2026 - 2031) | 15.66% CAGR |

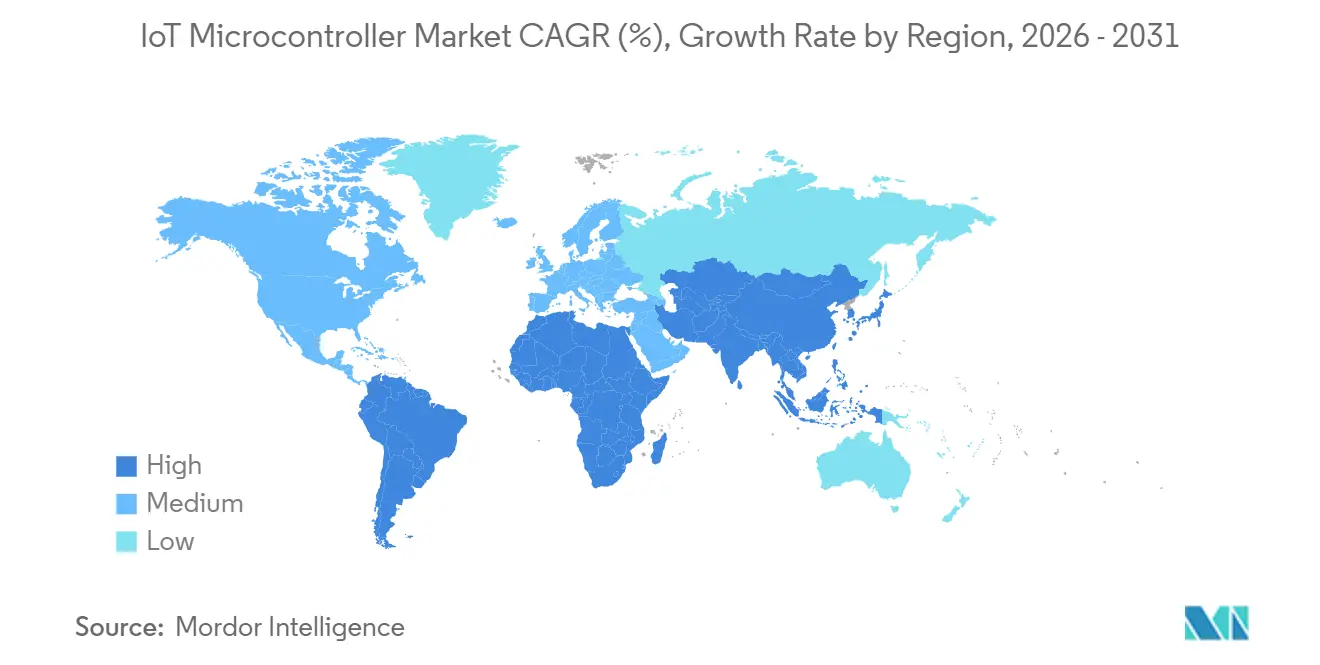

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Microcontroller Market Analysis by Mordor Intelligence

The IoT microcontroller market size is expected to increase from USD 6.11 billion in 2025 to USD 7.14 billion in 2026 and reach USD 14.78 billion by 2031, growing at a CAGR of 15.66% over 2026-2031. Edge-optimized silicon is moving from proof of concept into high-volume production because manufacturers want analytics close to the signal path, regulators insist on strong device security, and sovereign semiconductor policies redirect wafer capacity to new regions. Adoption of on-device AI accelerators is reducing latency for anomaly detection and vision tasks, while factory automation budgets are unlocking new demand for rugged parts that pair real-time control with machine-learning inference. Governments are sustaining momentum, with India and the United States funding localized fabs that guarantee long-term supply commitments. At the same time, multi-protocol radio integration and the rise of the Matter standard are reshaping design roadmaps, steering purchasing decisions toward controllers that can manage multiple wireless stacks without exceeding battery budgets.

Key Report Takeaways

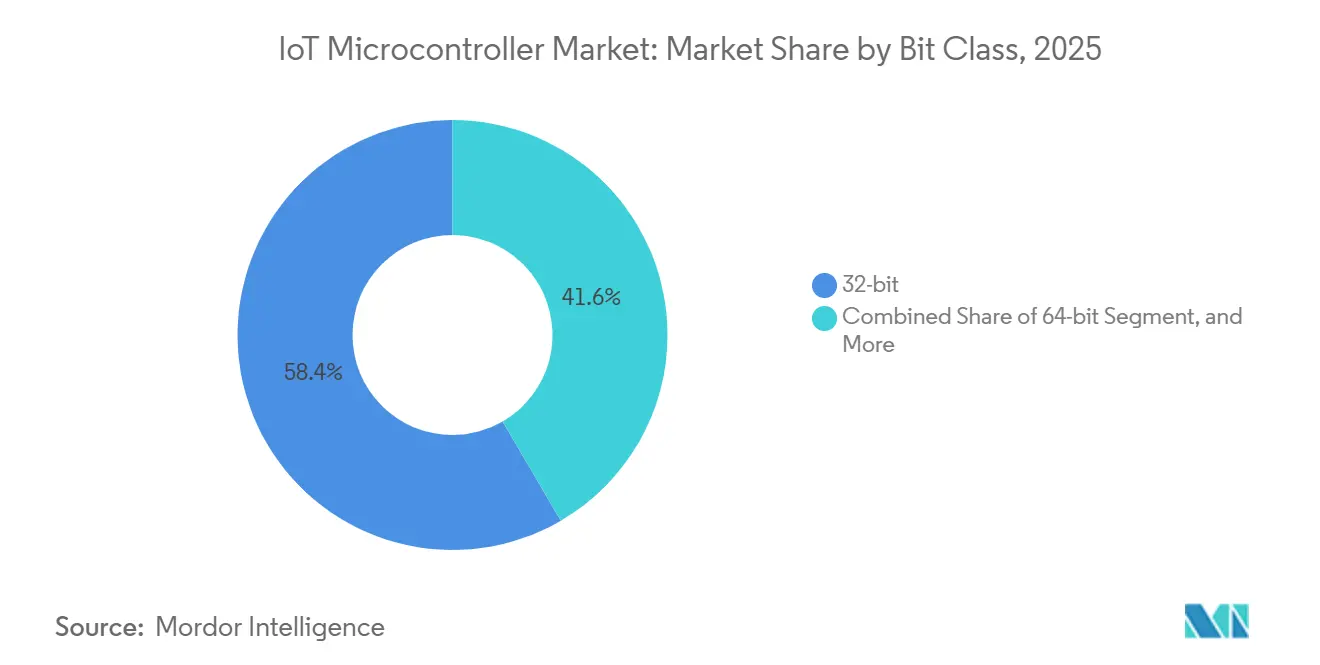

- By bit class, 32-bit devices led with 58.39% of the IoT microcontroller market share in 2025, and 64-bit devices are projected to expand at a 16.46% CAGR through 2031.

- By connectivity type, Wi-Fi modules captured 37.73% revenue share in 2025, and cellular NB-IoT and LTE-M solutions are forecast to grow at a 16.86% CAGR to 2031.

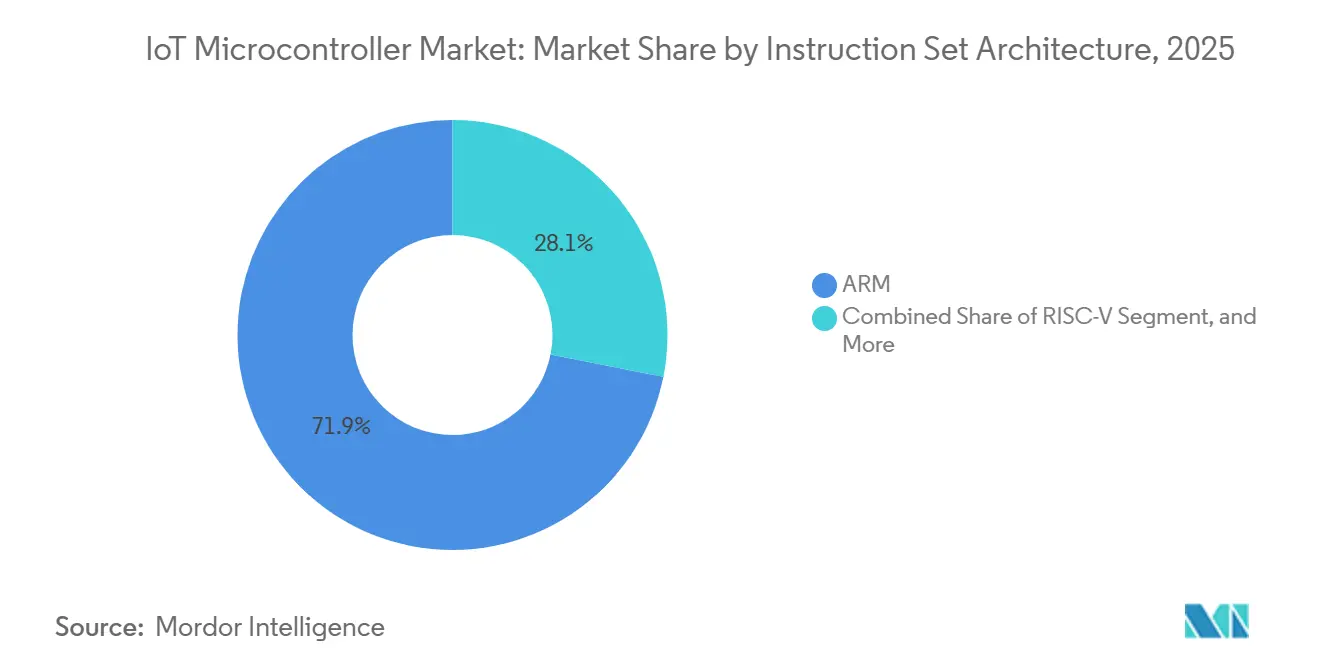

- By instruction set architecture, ARM-based MCUs accounted for 71.89% of total shipments in 2025, while RISC-V devices are poised to grow at a 16.41% CAGR through 2031.

- By application, industrial automation and IIoT accounted for 24.62% of segment revenue in 2025; however, smart-city infrastructure is anticipated to post a 16.66% CAGR during 2026-2031.

- By geography, the Asia-Pacific region generated 38.14% of global revenue in 2025, and the Middle East is expected to register a 16.53% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IoT Microcontroller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Connected Industrial Systems | +3.8% | Global focus, especially Asia-Pacific factories and North America automotive corridors | Medium term (2-4 years) |

| Growing Demand for Secure-by-Design MCUs in Edge AI Devices | +3.2% | North America and European Union, with spillover into Asia-Pacific | Short term (≤ 2 years) |

| Proliferation of Multi-Protocol Wireless MCUs for Smart-Home Ecosystems | +2.9% | North America and EU consumer markets, emerging Middle East demand | Medium term (2-4 years) |

| Government-Led Semiconductor Localization Incentives | +2.5% | India, Vietnam, and secondary effects in North America | Long term (≥ 4 years) |

| Open-Source RISC-V Adoption Reducing Licensing Costs | +1.8% | China-led Asia-Pacific initiatives with global cost-sensitive spillover | Long term (≥ 4 years) |

| Increasing Integration of AI Accelerators Inside 32-Bit MCUs | +1.6% | Worldwide traction in industrial and automotive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Connected Industrial Systems

Factory digitization budgets now prioritize distributed control and analytics as plant managers seek to cut unplanned downtime. Every robot cell, conveyor module, and smart tool embeds at least one controller that must combine sensor fusion with deterministic networking. Predictive-maintenance use cases demand on-chip analog front ends plus enough headroom to run vibration and thermal inference without cloud latency. Infineon's PSOC Edge E8x family, launched in 2025, exemplifies this trend by embedding an ARM Cortex-M33 core alongside an Ethos-U55 neural processing unit, enabling on-chip anomaly detection without cloud latency.[1]Infineon Technologies, “PSOC Edge E8x Product Brief,” infineon.com New product families embed hardware root-of-trust components to meet IEC 62443 mandates, meaning security now rides alongside signal integrity in the bill of materials.

Growing Demand for Secure-by-Design MCUs in Edge AI Devices

Latency-intolerant systems, such as service robots and autonomous drones, are moving inference workloads from the cloud to the board. This change increases the requirements for hardware isolation, secure boot, and tamper detection to prevent the extraction of model weights. Certification frameworks like PSA Certified Level 2 map design choices to clearly defined threat models, but they also extend development schedules by several months. Brands accept the timeline penalty because the EU Cyber Resilience Act and similar U.S. directives impose strict liability for insecure connected products.

Proliferation of Multi-Protocol Wireless MCUs for Smart-Home Ecosystems

Matter adoption is forcing designers to combine Wi-Fi, Thread, Bluetooth Low Energy, and Zigbee stacks on a single die. The integrated-radio path reduces printed-circuit complexity and simplifies regulatory testing, though it increases firmware size and increases the risk of stack interactions. Smart locks and thermostats now seek five-year coin-cell life, so radio suppliers differentiate on deep-sleep leakage and adaptive frequency agility. Vendors that can pre-certify all four stacks and offer over-the-air update infrastructure win sockets ahead of cheaper discrete alternatives.

Government-Led Semiconductor Localization Incentives

India, Vietnam, and the United States are channeling public money into front-end fabs and advanced assembly lines. Grants come with local-content thresholds and workforce-training clauses that require both design and production to be relocated to emerging hubs. The policy mix aims to dilute geographic concentration, yet it can also fragment technical standards because regional authorities write unique compliance playbooks. Over the long term, localized capacity promises shorter logistics chains and preferential supply for domestic original-equipment manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Software Ecosystem Fragmentation for New ISAs | -1.4% | Worldwide, with stronger pressure in China-centric RISC-V rollouts | Medium term (2-4 years) |

| Persistent Semiconductor Supply-Chain Volatility | -1.2% | Global exposure, most acute in automotive and industrial verticals | Short term (≤ 2 years) |

| Rising Cyber-Security Compliance Costs for IoT OEMs | -0.9% | North America and EU regulations, affecting export-oriented Asia-Pacific producers | Short term (≤ 2 years) |

| Performance-Power Trade-offs Limiting Battery Life Gains | -0.7% | Global impact on battery-powered consumer and commercial devices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Software Ecosystem Fragmentation for New ISAs

RISC-V’s open license lowers royalty outlays, but unrestricted custom extensions have created a patchwork of toolchains that lack binary compatibility. Developers often maintain separate code bases for each silicon variant, which inflates non-recurring engineering budgets. Consolidation efforts such as the RVA profiles are underway, yet adherence is optional, and uptake remains uneven. The resulting uncertainty deters automotive and medical designers who must guarantee 15-year software support.

Persistent Semiconductor Supply-Chain Volatility

An additional 300 mm lines funded by incentive programs will not produce meaningful volume until late 2027. In the meantime, geopolitical export controls and continued automotive demand spikes keep lead times for industrial-temperature MCUs above historical norms. Smaller original-equipment manufacturers lack the purchasing leverage to secure long-term capacity agreements, so they over-stock safety inventory, which ties up working capital and delays product launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit Class: Performance Migration Reshapes Design Choices

The 32-bit class delivered 58.39% of revenue in 2025, underscoring its balance between compute ceiling and cost. High-volume controllers in this tier dominate smart gateways and factory drives because they run real-time operating systems alongside compact machine-learning libraries. The IoT microcontroller market continues to pivot toward variants with vector math units and on-chip security blocks, enabling deterministic control without compromising encryption throughput. Raspberry Pi's RP2350, launched in 2024, offers a dual-core configuration that can run either ARM Cortex-M33 or RISC-V Hazard3 instructions, providing developers with architectural flexibility and a migration path from 32-bit to 64-bit workloads.[2]Raspberry Pi Foundation, “RP2350 Microcontroller Announcement,” raspberrypi.com

Demand for 64-bit controllers is climbing at a 16.46% CAGR as high-definition imaging and multi-sensor fusion need wider address spaces. Robotics modules and advanced driver-assistance boards already exceed 4 GB of memory, compelling engineers to adopt wider data paths despite higher active current. As compiler support matures, the jump to 64-bit instruction sets will spread beyond premium designs into mainstream edge analytics.

By Connectivity Type: Ubiquitous Radios Become a Platform Differentiator

Wi-Fi maintained a 37.73% shipment share in 2025 because most gateways are located inside buildings with existing access-point coverage. Smart-home hubs, retail handhelds, and small industrial terminals benefit from the bandwidth headroom and ubiquity of Wi-Fi infrastructure. Modules now support power-saving modes that lower average draw to below 25 µA, extending battery life and nudging Wi-Fi into portable devices once locked to Bluetooth.

Cellular NB-IoT and LTE-M modules are expanding at a 16.86% CAGR as meter companies, logistics providers, and agricultural platforms pursue wide-area reach without owning a private backhaul. The rise of eSIM and global roaming profiles means a single part number can address many regulatory domains, simplifying inventory. Over the forecast horizon, the IoT microcontroller market will reward suppliers that preload certified modem firmware and data-plan management hooks, shortening deployment cycles for fleet operators.

By Instruction Set Architecture: Incumbency Versus Openness

ARM cores accounted for 71.89% of shipments in 2025, thanks to decades of middleware investment and extensive debugger support. The IoT microcontroller market rewards predictable development flows, and ARM’s Cortex-M toolkit remains the benchmark for first-time-right silicon. Even so, boards targeting lower bill-of-material costs are testing RISC-V controllers to avoid per-unit royalties, especially in China, where architectural sovereignty is a policy priority.

RISC-V shipments are rising at a 16.41% pace. Starter kits now bundle toolchains from Segger and IAR, narrowing the usability gap with ARM platforms. Yet, fragmentation risk remains until ecosystem players agree on mandatory vector and security extensions. Consequently, many medical and safety-critical appliances still lock in ARM-based controllers for certification confidence.

By Application: Industrial Core, Smart-City Upside

Industrial automation and IIoT accounted for 24.62% of application revenue in 2025, underscoring factories’ willingness to pay for longevity and real-time determinism. Controllers in this spaceship feature functional safety credentials and galvanic isolation, designed to survive harsh plant-floor environments. Predictive-maintenance algorithms resonate with operations leaders because they turn vibration and thermal data into direct cost savings.

Smart-city infrastructure is the fastest-growing sector, with a 16.66% CAGR. Urban planners deploy connected lighting, waste bins, and air-quality monitors that sleep for months yet wake instantly for critical alerts. Controllers must provide sub-µA standby current and hardware root-of-trust functions so that a single compromised sensor does not jeopardize municipal networks. As national stimulus packages underwrite megaprojects across the Gulf region, opportunity widens for multi-protocol, temperature-hardened MCUs.

Geography Analysis

Asia-Pacific captured 38.14% of global revenue in 2025, anchored by China’s contract-manufacturing depth, Japan’s precision robotics base, and India’s fiscal incentives that reduce import reliance. Domestic cloud providers in China increasingly recommend RISC-V parts for edge nodes, reinforcing local supply chains and lowering royalty exit risk. India’s disbursement of INR 15,554 crore (approximately USD 1,648 million) under its production incentive plan has already attracted several bump-and-test houses that shorten the time from wafer to finished module.[3]Press Information Bureau, “Union Budget 2025-26: India Semiconductor Mission 2.0,” pib.gov.in

North America benefits from strong automotive electronics demand and continuing upgrades to industrial automation infrastructure. The CHIPS and Science Act funnels multi-billion-dollar grants to mature nodes serving the IoT microcontroller market, but new fabs will not reach steady state until the back half of the decade. In the interim, original-equipment manufacturers rely on multi-sourcing strategies and approved alternates to manage allocation shocks. Europe faces higher energy prices that raise wafer fabrication overhead, yet the region remains essential for safety-critical controller design. German and French tier-ones drive stringent ISO 26262 documentation that eventually becomes global best practice, giving European suppliers influence that exceeds their shipment share.

The Middle East, though smaller today, is scaling faster than any peer region at 16.53% CAGR because flagship smart-city programs require sensor networks that survive desert heat and sand ingress. South America and Africa remain emerging opportunities. Pilot programs in precision irrigation and solar-microgrid monitoring highlight long-range cellular controllers that bridge infrastructure gaps. As data plans and satellite-backhaul tariffs decline, these regions will shift from proof of concept to scaled deployments, lifting long-tail unit volumes for value-optimized 32-bit parts.

Competitive Landscape

Roughly half of 2025 revenue is moderately fragmented among STMicroelectronics, NXP, Texas Instruments, Microchip, and Renesas, reflecting decades of channel depth and field-application support. Each incumbent builds value ladders around software libraries, evaluation boards, and cloud gateways that lock customers through high switching costs. Average design cycles in industrial and automotive sectors stretch five to seven years, which shields incumbents even as selling prices compress in consumer categories.

Chinese entrants such as Espressif Systems and GigaDevice attack the lower end of the IoT microcontroller market with aggressively priced Wi-Fi and Bluetooth SoCs that bundle extensive development kits. Their ability to spin silicon in twelve-month cadences forces Western vendors to accelerate refresh schedules that once stretched to three years. Qorvo's 2024 patent for sub-1 µA sleep-mode circuitry in multi-protocol SoCs and Silicon Labs' 2025 filing for adaptive frequency hopping in congested 2.4 GHz environments underscore the race to differentiate on power efficiency and coexistence performance.[4]Qorvo, “Sub-1 µA Sleep Current SoC Datasheet,” qorvo.com To protect margin, established suppliers package security certificates, probabilistic fault detection, and over-the-air provisioning tools that raise barriers beyond pure hardware cost.

Strategic white space centers on secure multi-protocol controllers with integrated neural engines. Building these parts requires RF coexistence expertise, low-leakage digital libraries, and long-tail compiler maintenance. Patent filings show a race to drive sleep current below one microamp while sustaining multi-stack radio support. Vendors that master both hardware and software will convert sockets into multiyear service annuities as firmware updates and cloud dashboards become bundled revenue.

IoT Microcontroller Industry Leaders

NXP Semiconductors N.V.

Renesas Electronics Corporation

STMicroelectronics N.V.

Microchip Technology Inc.

Texas Instruments Inorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: STMicroelectronics launches the STM32H9 series, pairing a Cortex-M85 core with Helium vector extensions and TrustZone security, bringing 64-bit performance envelopes to predictive-maintenance gateways and industrial drives.

- March 2026: Infineon Technologies begins high-volume production of its PSOC Edge E85 family on a 28 nm line in Kulim, Malaysia. The devices combine a Cortex-M33 core, an Ethos-U55 neural engine, and integrated Wi-Fi 6 for factory-floor analytics.

- February 2026: Nordic Semiconductor introduces the nRF91x3 multi-mode cellular SiP, adding 5G RedCap to its LTE-M and NB-IoT modem for asset-tracking and smart-meter deployments that need multi-year battery autonomy.

- January 2026: Texas Instruments commences pilot wafer runs at its expanded 300 mm Lehi, Utah facility, producing automotive-grade and industrial-temperature MCUs to alleviate ongoing lead-time pressures for Tier-1 suppliers.

Global IoT Microcontroller Market Report Scope

The IoT Microcontroller Market refers to the global industry focused on the development, production, and commercialization of microcontroller units (MCUs) specifically designed for Internet of Things (IoT) applications. These MCUs integrate processing cores, memory, communication interfaces, and peripheral functionalities into compact semiconductor devices that enable sensing, connectivity, real-time control, data processing, and low-power operation across connected environments. IoT microcontrollers are widely utilized in smart consumer devices, industrial systems, automotive electronics, healthcare equipment, and smart infrastructure to support intelligent automation and machine-to-machine communication.

The IoT Microcontroller Market Report is Segmented by Bit Class (8-bit, 16-bit, 32-bit, and 64-bit), Connectivity Type (No Integrated Connectivity, Wi-Fi, Bluetooth/BLE, Zigbee/Thread, Cellular NB-IoT/LTE-M, and Multi-protocol SoC), Instruction Set Architecture (ARM, RISC-V, x86, and Proprietary/Others), Application (Smart Home and Wearables, Industrial Automation and IIoT, Automotive and Transportation, Healthcare and Medical Devices, and Smart City Infrastructure), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 8-bit |

| 16-bit |

| 32-bit |

| 64-bit |

| No Integrated Connectivity |

| Wi-Fi |

| Bluetooth / BLE |

| Zigbee / Thread |

| Cellular NB-IoT / LTE-M |

| Multi-protocol SoC |

| ARM |

| RISC-V |

| x86 |

| Proprietary / Other Instruction Set Architectures |

| Smart Home and Wearables |

| Industrial Automation and IIoT |

| Automotive and Transportation |

| Healthcare and Medical Devices |

| Smart City Infrastructure |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Bit Class | 8-bit | ||

| 16-bit | |||

| 32-bit | |||

| 64-bit | |||

| By Connectivity Type | No Integrated Connectivity | ||

| Wi-Fi | |||

| Bluetooth / BLE | |||

| Zigbee / Thread | |||

| Cellular NB-IoT / LTE-M | |||

| Multi-protocol SoC | |||

| By Instruction Set Architecture | ARM | ||

| RISC-V | |||

| x86 | |||

| Proprietary / Other Instruction Set Architectures | |||

| By Application | Smart Home and Wearables | ||

| Industrial Automation and IIoT | |||

| Automotive and Transportation | |||

| Healthcare and Medical Devices | |||

| Smart City Infrastructure | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the IoT microcontroller market size in 2026?

The IoT microcontroller market size is projected at USD 7.14 billion in 2026, according to Mordor Intelligence.

Which bit class holds the largest revenue share?

32-bit devices led with 58.39% share in 2025, reflecting their balance of performance and cost.

Which region is forecast to grow the fastest?

The Middle East is expected to record a 16.53% CAGR through 2031 owing to large smart-city rollouts.

How quickly will RISC-V MCUs grow compared with ARM parts?

RISC-V shipments are forecast to rise at 16.41% CAGR, outpacing overall market growth while ARM retains the largest base.

What segment drives premium pricing?

Industrial automation and IIoT favor rugged, long-lifecycle MCUs with functional-safety certification, supporting higher average selling prices.

Page last updated on: