Ultra-Low-Power Microcontroller Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

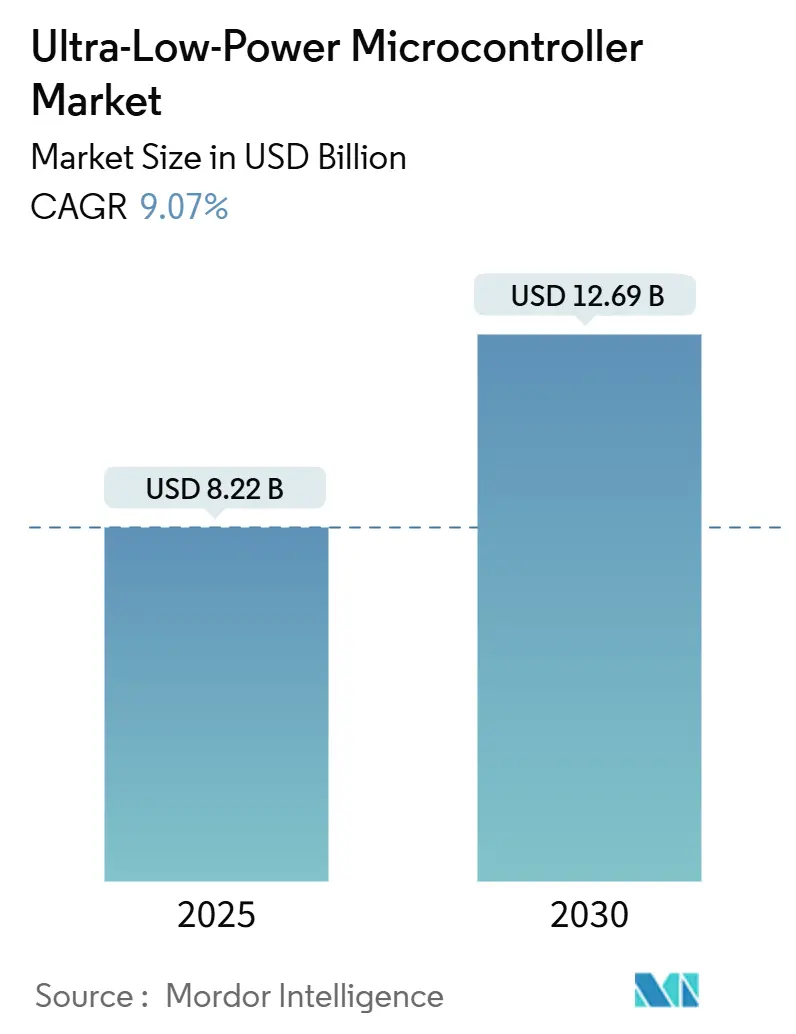

| Market Size (2025) | USD 8.22 Billion |

| Market Size (2030) | USD 12.69 Billion |

| Growth Rate (2025 - 2030) | 9.07% CAGR |

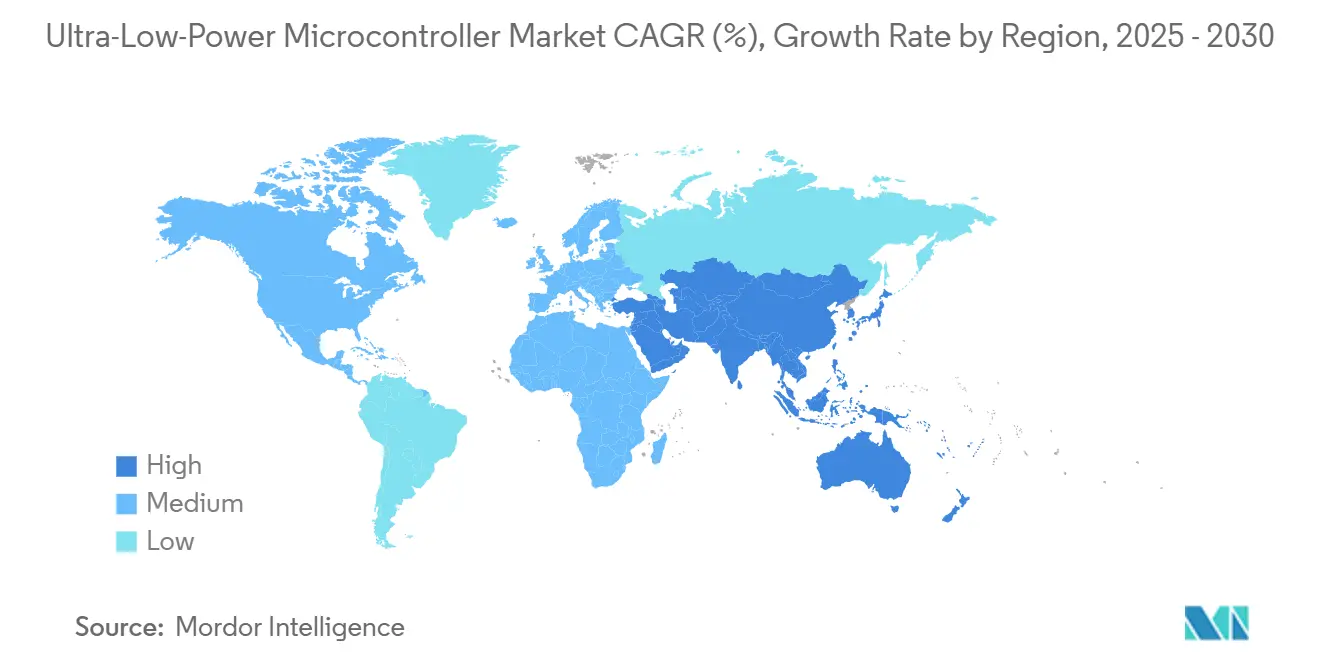

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra-Low-Power Microcontroller Market Analysis by Mordor Intelligence

The Ultra-Low-Power Microcontroller Market size is estimated at USD 8.22 billion in 2025, and is expected to reach USD 12.69 billion by 2030, at a CAGR of 9.07% during the forecast period (2025-2030).

Rising deployment of battery-powered IoT nodes, energy-harvesting architectures, and tightening power-efficiency mandates continue to lift demand for devices capable of sub-10 µA/MHz active power. North America sustains early-mover advantages through smart-grid rollouts and mature regulatory frameworks, while Asia-Pacific’s manufacturing scale accelerates adoption across consumer, industrial, and medical domains. OEM focus has shifted from mere sleep-current reductions to holistic energy budgets covering end-to-end sensing, processing, and connectivity, sparking a design race toward sub-threshold silicon, integrated AI engines, and dynamic power-gating schemes. Competitive positioning now hinges on demonstrating decade-long battery life without sacrificing the compute headroom required for on-device learning and secure communications.

Key Report Takeaways

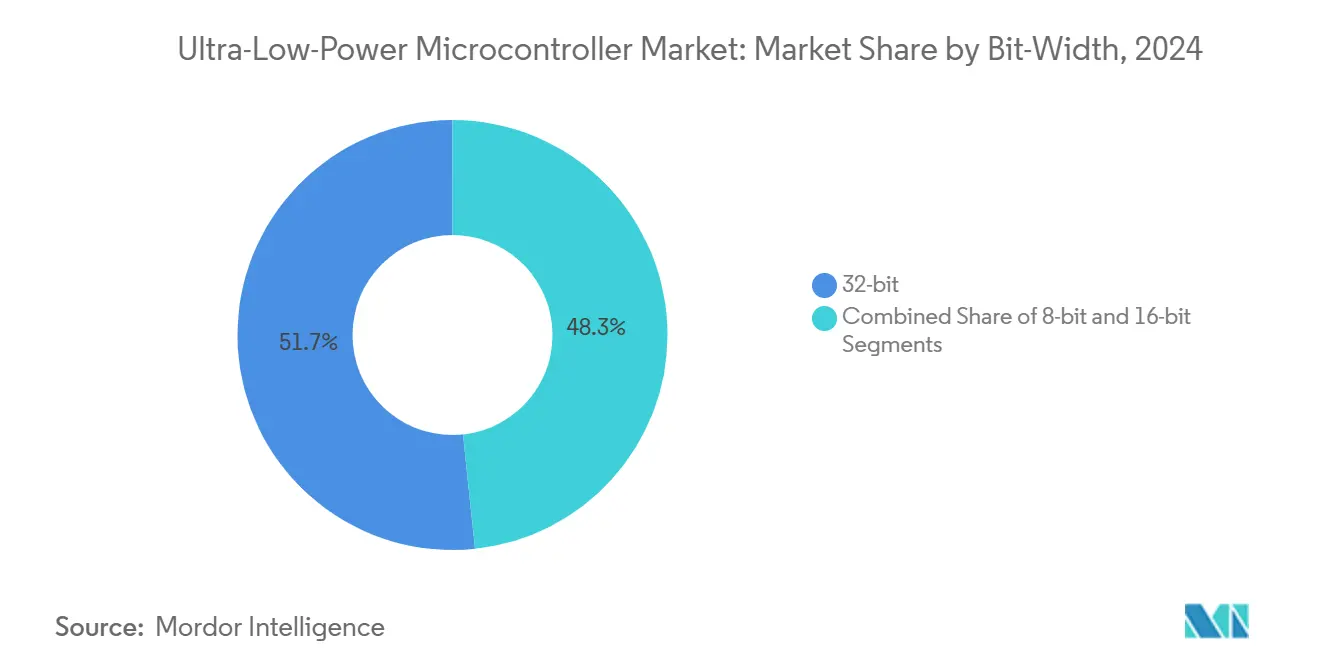

- By bit-width, 32-bit architectures captured 51.67% revenue share in 2024 and are projected to grow at a 9.71% CAGR through 2030.

- By peripheral device type, analog-centric MCUs accounted for 59.78% of 2024 sales, while digital-centric variants are forecast to log a 10.67% CAGR to 2030.

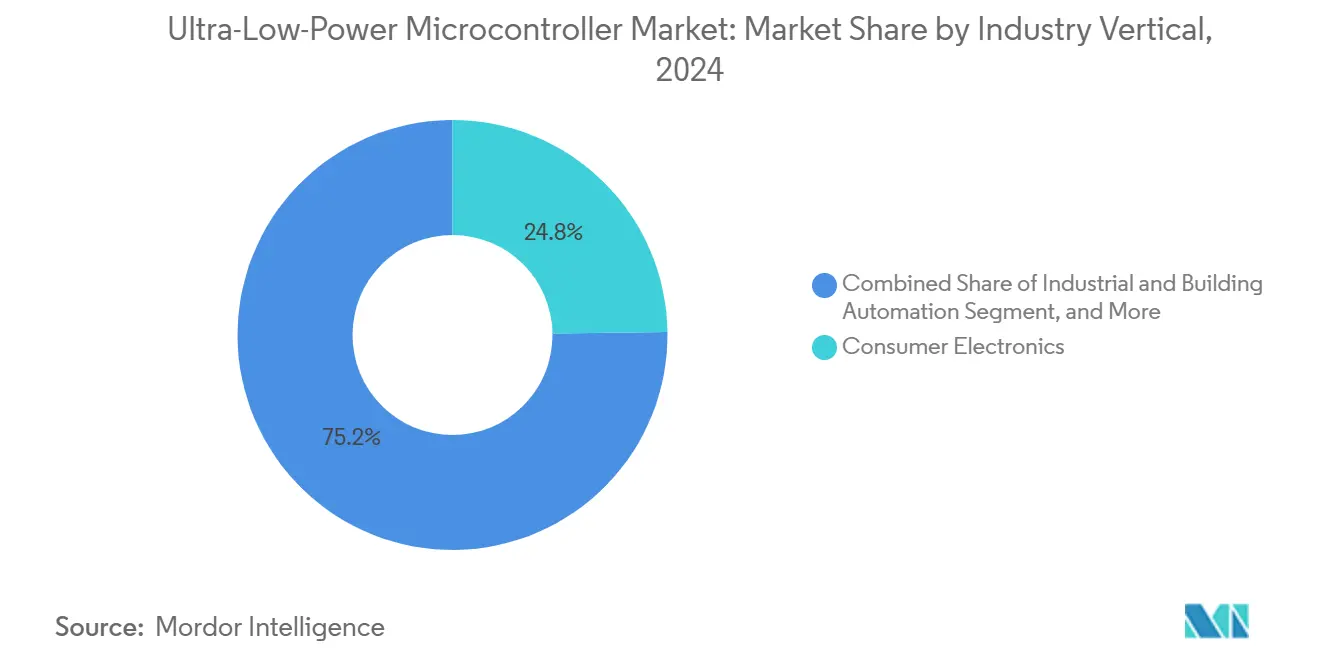

- By industry vertical, consumer electronics dominated with a 24.78% share in 2024; healthcare and medical devices are expected to register the quickest 9.29% CAGR over the forecast period.

- By application, smart-home controllers held 23.86% of the 2024 total, whereas portable and implantable medical devices are poised for a 9.33% CAGR to 2030.

- By geography, North America led with 33.76% market share in 2024, while Asia-Pacific is set to advance at a 10.24% CAGR through 2030.

Global Ultra-Low-Power Microcontroller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of battery-powered IoT endpoints and wearables | +2.8% | Global, with Asia-Pacific leading adoption | Short term (≤ 2 years) |

| Smart meters and smart home expansion | +2.1% | North America and EU primary, Asia-Pacific emerging | Medium term (2-4 years) |

| Industrial IoT sensors demanding energy-harvesting ULP MCUs | +1.9% | Global industrial hubs, concentrated in Germany, China, US | Medium term (2-4 years) |

| Energy-efficiency regulations for electronic devices | +1.4% | EU RED Directive, US Energy Star, China RoHS | Long term (≥ 4 years) |

| On-chip AI/ML accelerators enabling dynamic power-gating | +1.2% | Global, with early adoption in North America, Asia-Pacific | Short term (≤ 2 years) |

| Sub-threshold RISC-V cores for implantables and medical patches | +0.8% | North America, EU regulatory approval markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Battery-Powered IoT Endpoints and Wearables

Wearables and sensor nodes now ship in volumes measured in billions, each expected to run multiple sensing and wireless workloads for more than a week on button cells. Ambiq’s Apollo SOC registers 6 µA/MHz active current, letting smartwatches stream biometric data for weeks instead of days. [1]Ambiq Micro, “Apollo Ultra-Low-Power MCUs,” ambiq.com As deployments scale, device makers combine photovoltaic, thermoelectric, and kinetic harvesters under supervisory PMUs that draw mere nanoamperes, turning maintenance-free service lives into a purchasing baseline. OEMs in Asia-Pacific lead cost discipline, while North American brands push spec sheets toward always-on voice and vision features. The resulting appetite for compute-efficient instructions intensifies the use of custom DSP blocks and fine-grained clock domains to trim every microwatt.

Smart Meters and Smart-Home Expansion

Utilities in Europe and North America stipulate 15-year lifespans with sleep currents below 1 µA, driving LoRaWAN-enabled meters that can survive harsh outdoor climates while remaining firmware-upgradeable. [2]Silicon Labs, “LoRaWAN Wireless Solutions,” silabs.com Residential demand pivots toward voice-first hubs and gesture-aware controllers that require idle power below 30 µW yet burst into multi-hundred-MHz inference modes. Vendors differentiate through deep-sleep state variety, integrated security IP, and modular RF front-ends that shave weeks off design cycles. Cost-down roadmaps depend on moving to 55 nm FD-SOI, though foundry capacity remains tight.

Industrial IoT Sensors Demanding Energy Harvesting

Factories retrofit rotating-equipment nodes sampling at ≥ 10 kHz; algorithms must execute locally to avoid latency and bandwidth costs. Ultra-low-power microcontrollers with 128-bit DSPs and adaptive sampling firmware cut mean current draw to sub-20 µA, enabling vibration sensors to power entirely from piezo harvesters. [3]Zhang L. et al., “Energy Harvesting for Industrial IoT Sensors,” IEEE Sensors Journal, ieeexplore.ieee.org German and Chinese facilities favor turnkey modules that bundle PMIC, MCU, and MEMS transducer, reducing BOM while meeting IEC-Ex safety standards. As predictive-maintenance gains prove ROI, suppliers command premium ASPs despite chip price erosion elsewhere.

Energy-Efficiency Regulations for Electronic Devices

The EU’s Radio Equipment Directive and parallel U.S. Energy Star profiles now set active-power ceilings, obliging brands to evidence savings at audit time. Compliance extends beyond standby to compute efficiency, so OEMs adopt dynamic voltage/frequency scaling tied to real-time workload monitors. Certification cost and lead time encourage selecting silicon pre-qualified under SESIP Level 3 or higher. Longer term, Asian regulators plan harmonized eco-design laws, widening the addressable market for next-generation ultra-low-power cores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Design complexity and higher NRE costs | -1.8% | Global, particularly impacting smaller OEMs | Short term (≤ 2 years) |

| Price erosion amid intense vendor competition | -1.5% | Global, with Asia-Pacific markets most price-sensitive | Medium term (2-4 years) |

| Limited compute/memory restricts high-end applications | -1.2% | Global, affecting AI/ML edge applications | Medium term (2-4 years) |

| Fragile supply of low-leakage FD-SOI and other specialty nodes | -0.9% | Global, concentrated in advanced foundry markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Design Complexity and Higher NRE Costs

Achieving sub-threshold operation below 0.5 V demands rigorous PVT characterization, expanded ESD structures, and sophisticated power-domain isolation, inflating mask sets and verification hours. Small OEMs lacking analog talent face multi-million-dollar barriers before first silicon, pushing them toward off-the-shelf modules despite higher unit pricing. Firmware must orchestrate sleep-wake latencies under 3 µs, adding RTOS tuning cycles that stretch project timelines. Tool vendors now bundle energy-profiling instrumentation, yet steep learning curves persist.

Price Erosion Amid Intense Vendor Competition

Chinese entrants deliver comparable 32-bit devices at 20–30% lower ASPs, compelling established leaders to bundle BLE or sensor hubs for differentiation. TSMC’s announced 10–20% wafer hikes on 28 nm and specialty nodes compress margins further. Vendors counter with long-term supply agreements and ecosystem lock-ins, but customers in appliance and lighting markets remain price-driven, tempering volume-weighted revenue growth despite unit expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit-Width: 32-Bit Architectures Drive Edge Intelligence

The 32-bit class registered 51.67% of the ultra-low-power microcontroller market share in 2024, and the ultra-low-power microcontroller market size for this group is projected to expand at a 9.71% CAGR between 2025-2030. Demand stems from AI inference, floating-point math, and secure boot requirements that 8-bit and 16-bit cores cannot meet. ARM Cortex-M0+, Cortex-M23, and widening RISC-V IP catalogs compress active power below 80 µA/MHz while maintaining tool-chain parity with higher-performance MCUs. Software reuse across cloud and edge cuts engineering cost, reinforcing 32-bit momentum. Meanwhile, 8-bit devices remain indispensable in cost-critical, single-function sensors where code size rarely exceeds 4 KB. New one-time-programmable flash options shrink die area, letting 8-bit stay relevant for smart-lighting, toys, and simple meters even as 16-bit volumes erode.

The architecture race now orbits integrated AI accelerators delivering 0.5–1 TOPS/W, placing 32-bit firmly at the front of the ultra-low-power microcontroller market. Hybrid compute pipelines offload MAC-heavy layers, letting core clocks drop to sub-10 MHz during inference, thereby extending battery life. Vendors also leverage bit-width-agnostic design flows to port mature peripheral IP from legacy nodes, lowering risk when migrating to FD-SOI. Customer roadmaps increasingly specify flashless 32-bit MCUs that stream code from external FRAM, trading marginal standby current for BOM savings and over-air field upgradability.

By Peripheral Device Type: Analog-Centric Solutions Maintain Dominance

Analog-rich MCUs contributed 59.78% of 2024 revenue, reflecting the premium paid for integrated ADCs, PGAs, and sensor-bias generators critical to low-noise data capture. These parts collapse the BOM count by replacing external amplifiers, improve signal integrity, and cut total quiescent currents to microampere levels. Precision biosignal acquisition for ECG, SpO₂, and EEG monitoring relies on offset voltages below 1 µV and input bias in the picoampere range, benefits hard to replicate through discrete front-ends under tight power budgets.

Digital-centric devices, though smaller in today’s mix, grow fastest at 10.67% CAGR as edge-AI, protocol-heavy, and secure-element applications scale. Here, MCU value resides in integrated accelerators: crypto engines, voice DSPs, and neural cores drive packetized workloads, favoring high-density logic over analog precision. Roadmaps point toward converged architectures where designers can configure on-die analog in the mask-option phase, tailoring a single base die to multiple SKUs for consumer, industrial, and medical SKUs. Such versatility underpins vendor strategies aimed at balancing inventory risk against exploding application diversity in the ultra-low-power microcontroller market.

By Industry Vertical: Healthcare Surges Ahead of Consumer Staples

Consumer electronics accounted for 24.78% of 2024 revenue thanks to wearables, hearables, and smart-home hubs demanding always-on sensing. Yet the healthcare and medical-device segment is forecast to clock the quickest 9.29% CAGR as regulators approve long-duration implanted monitors and patch-format biosensors that require <10 µA average current for multi-year life. Continuous glucose monitors, cardiac rhythm management, and closed-loop drug-delivery pumps tip procurement toward MCUs certified under IEC 60601.

Industrial and building automation hold steady CAGRs around mid-single digits as predictive-maintenance and occupancy-aware climate control achieve enterprise ROI visibility. Automotive adoption accelerates with ADAS standby modules, TPMS, and keyless-entry fobs that must endure −40 °C to +125 °C temperature extremes, pushing suppliers to qualify FD-SOI devices to AEC-Q100 Grade 0. Smart-city and utility deployments, though smaller on revenue today, catalyze volume orders due to 15–20-year battery mandates and LoRa/ NB-IoT backhaul requirements, sustaining mid-term growth for the ultra-low-power microcontroller market.

By Application: Medical Devices Lead Future Upside

Smart-home controllers retained a 23.86% share in 2024, underpinned by voice-assisted lighting, HVAC, and security nodes that ping cloud services around the clock. However, portable and implantable medical devices are set to outpace all segments at a 9.33% CAGR, reflecting demographic shifts and reimbursement models that favor continuous patient data. Ultra-low-power microcontroller market size for these medical applications is poised to cross USD 3 billion by 2030, powered by sub-threshold RISC-V cores capable of always-on ECG classification at <20 µW average draw.

Wearables migrate from fitness to medical-grade metrics such as blood pressure and sleep apnea detection, raising the bar on sensor fusion and edge-based ML inference. Wireless sensor nodes form the backbone of Industry 4.0, batching vibration and temperature data into encrypted packets for gateway-side pre-processing. Smart-metering units adopt ultra-low-power microcontrollers with single-cycle multiply and AES-128 engines, enabling secure billing for water, gas, and electric grids across the globe. Industrial edge controllers integrate new TSN-ready Ethernet MACs to satisfy sub-millisecond deterministic control loops while meeting 1 mA/MHz targets that cap enclosure heat dissipation.

Geography Analysis

North America held 33.76% of global revenue in 2024 on the back of mature smart-grid infrastructure, FDA-cleared medical wearables, and an established design-service ecosystem. U.S. utilities lock in multi-year contracts specifying 15-year battery life, reinforcing demand for integrated PMUs and authenticated wireless stacks. Canada’s residential net-zero housing codes and Mexico’s automotive manufacturing expansion add incremental volume for regional suppliers.

Asia-Pacific is projected to post the fastest 10.24% CAGR, spurred by China’s industrial IoT investments expected to hit USD 150 billion by 2030. Government incentives accelerate domestic MCU design houses, yet global players still dominate premium sub-threshold silicon. Japan and South Korea lead in consumer electronics miniaturization, adopting flip-chip WLCSP packages as small as 1.8 × 1.8 mm for earbuds and smart rings. India’s Smart Cities Mission deploys LoRaWAN-based environmental monitors city-wide, banking on low-cost ultra-low-power microcontroller market solutions to curb maintenance. Australia’s mining automation requires rugged- −40 °C-capable parts with high ESD immunity, offering niche but profitable opportunities.

Europe emphasizes sustainability through the RED Directive and circular-economy measures, prompting OEMs to benchmark energy consumption meticulously. Germany’s Industry 4.0 lighthouse factories specify energy-harvesting sensor kits with a five-year return on investment. The U.K. smart-meter rollout continues to generate volume orders for 32-bit MCUs supporting cellular NB-IoT fallback. France and the Netherlands drive integrated building-automation adoption, valuing SESIP Level 3 cybersecurity to comply with GDPR. Eastern European EMS providers attract relocation projects, securing fresh design wins for low-leakage FD-SOI devices.

Competitive Landscape

The ultra-low-power microcontroller market remains moderately fragmented; the top five vendors collectively accounted for roughly 55% of 2024 revenue, leaving ample room for niche innovators. Texas Instruments, STMicroelectronics, and Microchip Technology leverage deep analog catalogs and broad development-tool ecosystems, bundling BLE, Sub-1 GHz, and LP-Wi-Fi connectivity into single-package offerings that simplify board design. Ambiq Micro and Nordic Semiconductor differentiate through extreme active-power efficiency and protocol-optimized radio stacks, respectively, commanding premium ASPs in wearables and asset-tracking.

Strategic activity centers on vertical software integration: Nordic ships turnkey reference apps from fitness-tracking to medical-patch firmware, reducing customer engineering overheads. STMicroelectronics expanded patent holdings around sub-threshold voltage control, insulating its FD-SOI roadmap against commoditization threats. Vendors also form foundry alliances to secure FD-SOI and 22ULL wafer allocation, mitigating supply risk flagged by 2024’s tight capacity.

M&A momentum targets complementary IP blocks-Microchip’s rumored interest in Atmosic could pair energy-harvesting PMICs with its PIC portfolio. Meanwhile, Chinese suppliers undercut pricing in commodity 8-bit segments, accelerating ASP declines but broadening entry-level adoption. Ecosystem lock-in via cloud-linked IDEs and OTA service platforms becomes a defensive moat as hardware margins tighten across the ultra-low-power microcontroller market.

Ultra-Low-Power Microcontroller Industry Leaders

Texas Instruments Incorporated

Silicon Laboratories Inc.

STMicroelectronics N.V.

Microchip Technology Inc.

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nordic Semiconductor unveiled the nPM2100 PMIC, extending primary-cell life to 15+ years through 100 nA quiescent current and multi-source energy-harvesting support.

- December 2024: STMicroelectronics released the STM32WBA5 series with BLE 5.4 and SESIP Level 3 certification for ultra-low-power smart-home nodes.

- November 2024: Ambiq Micro partnered with smart-ring and OTC-hearing-aid brands, embedding Apollo MCUs for week-long biometric monitoring.

- October 2024: Silicon Labs introduced BG29 MCUs featuring 24-bit Σ-Δ ADCs and 2.6 × 2.8 mm WLCSPs aimed at sub-10 µA medical sensors.

Global Ultra-Low-Power Microcontroller Market Report Scope

| 8-bit |

| 16-bit |

| 32-bit |

| Analog-centric |

| Digital-centric |

| Consumer Electronics |

| Industrial and Building Automation |

| Automotive and Transportation |

| Healthcare and Medical Devices |

| Smart Cities and Utilities |

| Aerospace and Defense |

| Wearables and Hearables |

| Wireless Sensor Nodes |

| Smart Metering |

| Portable and Implantable Medical Devices |

| Smart Home Controllers |

| Industrial Edge Controllers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Bit-Width | 8-bit | ||

| 16-bit | |||

| 32-bit | |||

| By Peripheral Device Type | Analog-centric | ||

| Digital-centric | |||

| By Industry Vertical | Consumer Electronics | ||

| Industrial and Building Automation | |||

| Automotive and Transportation | |||

| Healthcare and Medical Devices | |||

| Smart Cities and Utilities | |||

| Aerospace and Defense | |||

| By Application | Wearables and Hearables | ||

| Wireless Sensor Nodes | |||

| Smart Metering | |||

| Portable and Implantable Medical Devices | |||

| Smart Home Controllers | |||

| Industrial Edge Controllers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the ultra-low-power microcontroller market in 2025?

It stands at USD 8.22 billion and is projected to reach USD 12.69 billion by 2030, registering a 9.07% CAGR.

Which region grows fastest for ultra-low-power MCUs?

Asia-Pacific leads with a forecast 10.24% CAGR, driven by China’s expanding industrial IoT and consumer-electronics production.

What bit-width architecture dominates shipments?

32-bit cores hold 51.67% market share and drive the highest 9.71% CAGR due to edge-AI and security requirements.

Why are medical devices important for future demand?

Portable and implantable medical devices require multi-year battery life, pushing adoption of sub-threshold MCUs and fuelling a 9.29% vertical CAGR.

What technological trend shapes next-gen ultra-low-power MCUs?

Integration of AI/ML accelerators alongside energy-harvesting PMUs enables inference at <1 mW, maximizing battery longevity.

How does pricing pressure influence vendors?

Rising Chinese competition and wafer-cost hikes compress ASPs, compelling established players to bundle connectivity, security, and software ecosystems for differentiation.

Page last updated on: