Market Overview

| Study Period | 2020 - 2031 |

|---|---|

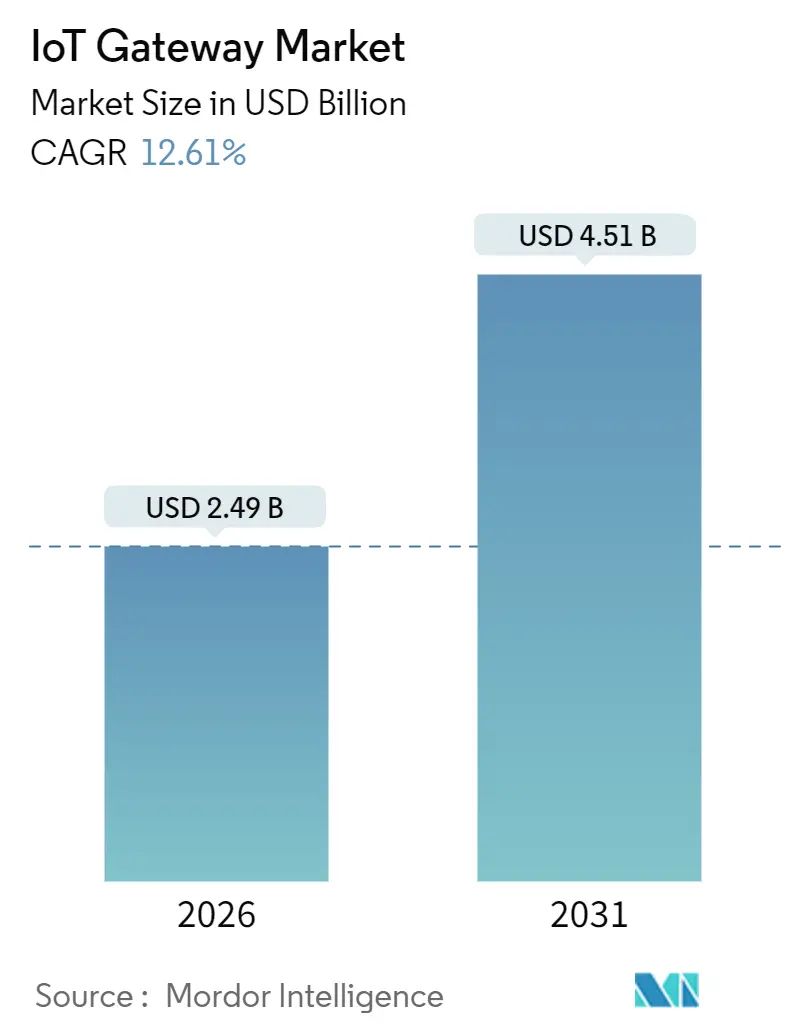

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 12.61% CAGR |

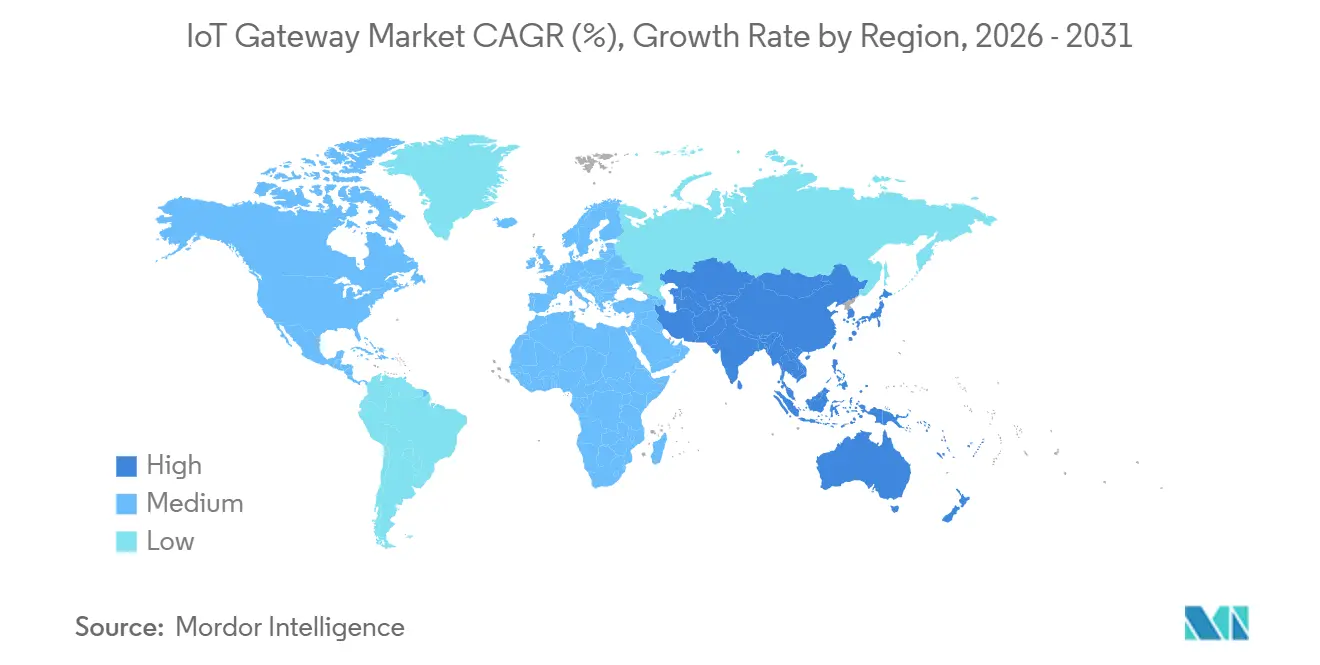

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

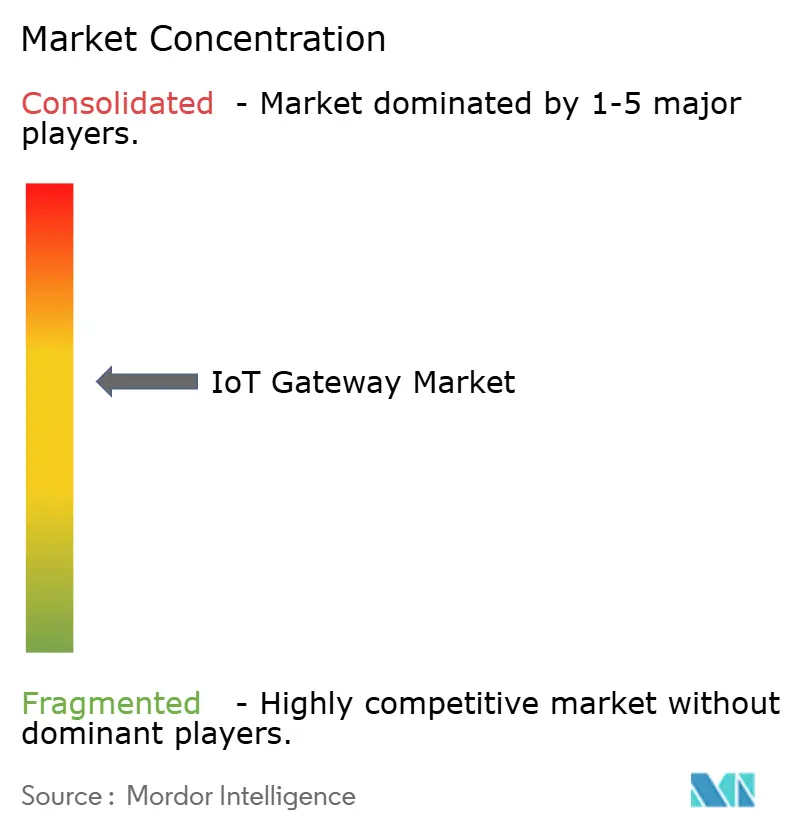

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Gateway Market Analysis by Mordor Intelligence

The IoT gateway market size reached USD 2.49 billion in 2026 and is projected to climb to USD 4.51 billion by 2031, advancing at a 12.61% CAGR during the forecast span. The expansion reflects a structural redesign in distributed computing, where gateways run containerized AI workloads at the network edge, trimming round-trip latency below 10 milliseconds for industrial automation and clinical monitoring. Early 5G standalone roll-outs, the arrival of Wi-Fi 7 backhaul, and the inclusion of neural processing units inside gateway SoCs are compressing deployment costs and broadening performance headroom. At the same time, private-network slicing helps enterprises segregate operational traffic from public routes, raising adoption among manufacturers that need deterministic throughput. Cyber-secure lifecycle management, led by eSIM activation and hardware root-of-trust, is becoming a non-negotiable purchase criterion as threat actors intensify attacks on operational technology assets.

Key Report Takeaways

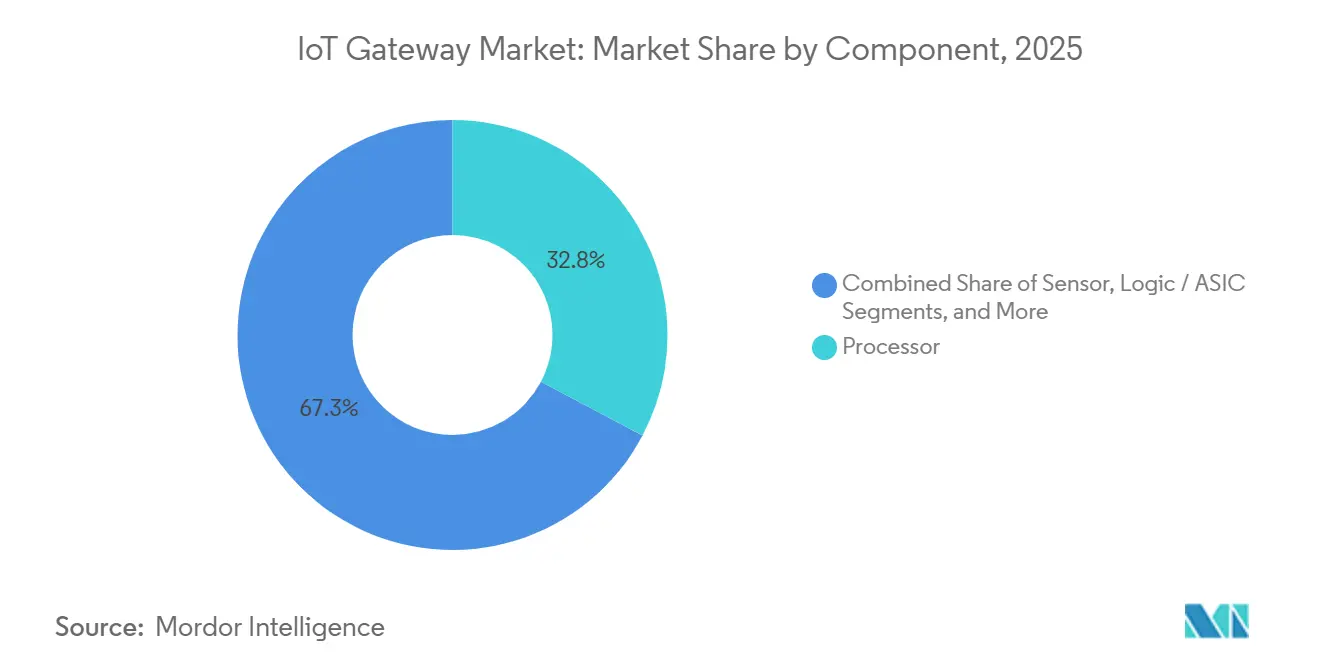

- By component, processors held 32.75% of IoT gateway market share in 2025, while connectivity ICs are on track to expand at a 13.11% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 29.84% of the IoT gateway market size in 2025 and healthcare is progressing at a 12.98% CAGR during 2026-2031.

- By deployment environment, DIN-rail gateways commanded 34.74% share in 2025, whereas rugged outdoor units are projected to advance at a 13.33% CAGR.

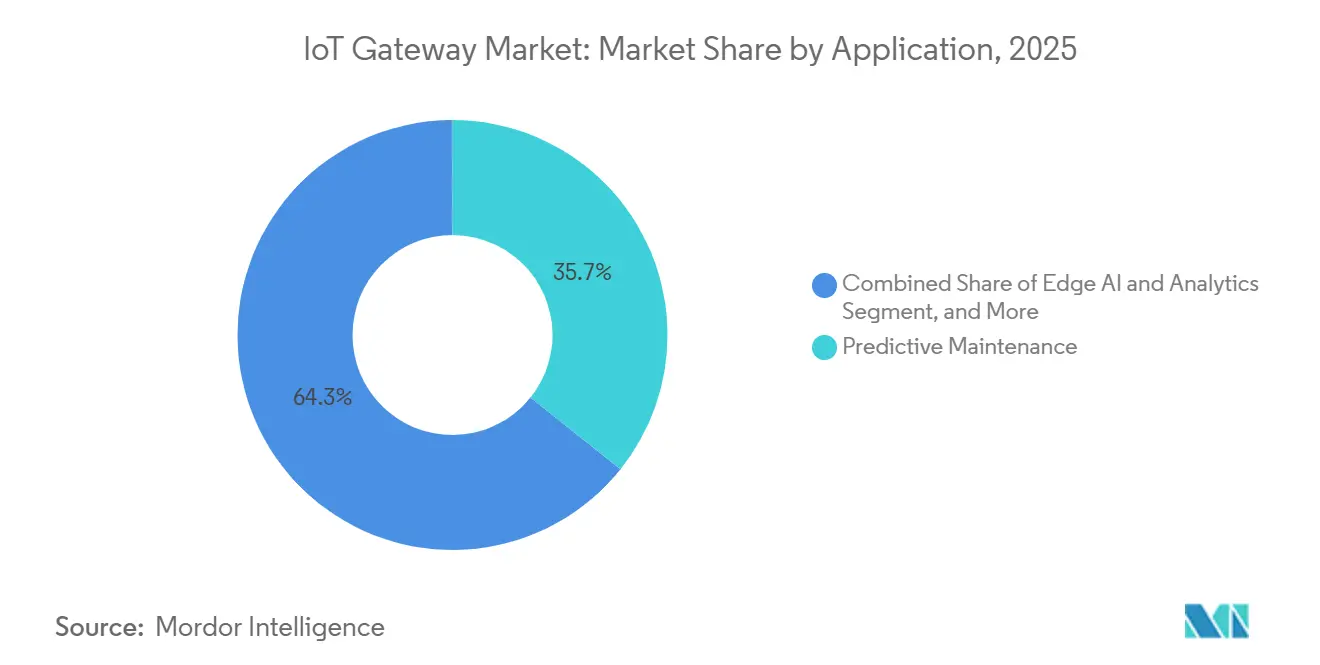

- By application, predictive maintenance led with 35.73% share of the IoT gateway market size in 2025 and edge AI is set to grow at a 13.55% CAGR.

- By geography, North America captured 38.74% share in 2025; Asia-Pacific is poised for a 13.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IoT Gateway Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G-enabled low-latency edge connectivity roll-outs | +2.8% | Global, with early density in South Korea, UAE, and US metro clusters | Short term (≤ 2 years) |

| Industry 4.0 adoption and factory edge analytics | +2.4% | Europe and Asia-Pacific manufacturing corridors, spillover to Mexico and Vietnam | Medium term (2-4 years) |

| Rapid smart-city LPWAN gateway deployments | +1.9% | Asia-Pacific urban centers, selective EU smart-city initiatives | Medium term (2-4 years) |

| AI/ML inference moving from cloud to gateway silicon | +2.6% | North America and Asia-Pacific, limited adoption in cost-sensitive MEA markets | Long term (≥ 4 years) |

| Telco private-network slicing for secure IoT backhaul | +1.7% | Enterprise campuses in North America, Europe, and Australia | Medium term (2-4 years) |

| Growing OEM demand for eSIM-based secure lifecycle management | +1.3% | Global, with regulatory tailwinds in EU (eIDAS 2.0) and US (CMMC 2.0) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G-Enabled Low-Latency Edge Connectivity Roll-Outs

Enterprises are adopting 5G standalone cores that guarantee sub-20 millisecond latency, enabling gateways to control collaborative robots and augmented-reality service tools in real time. Qualcomm’s QCS8550 processor combines a 5G RedCap modem with a 12 TOPS AI engine, letting factory operators keep high-throughput vision inference on-premises while sending model retraining jobs to the cloud.[1]Qualcomm, “Qualcomm QCS8550 IoT Processor,” qualcomm.com Private 5G sites increased by 140% year over year, with gateway shipments into automotive plants accounting for 38% of that volume.[2]Ericsson, “Ericsson Mobility Report 2025,” ericsson.com RedCap became commercially available in mid-2025, however, most battery-powered sensors still rely on LTE-M, resulting in a two-tier architecture with high-bandwidth and low-power links. Early adopters report that deterministic latency cuts unplanned production stoppages by enabling microsecond-level machine coordination.

Industry 4.0 Adoption and Factory Edge Analytics

Manufacturers embed IoT gateways in CNC machines and conveyors to run predictive maintenance models that flag bearing failures 72 hours in advance, cutting downtime by nearly one-third. Siemens delivered more than 50,000 Industrial Edge gateways in 2024, each shipping with a marketplace for containerized analytics apps.[3]Siemens, “Industrial Edge,” siemens.com ABB’s Ability Edgenius platform, launched in March 2025, enables maintenance teams to deploy TensorFlow Lite models via a drag-and-drop interface, eliminating the need for data science staff.[4]ABB, “ABB Ability Edgenius,” abb.com While the return on investment is proven, air-gapped operational networks hinder over-the-air patching; many facilities still use USB keys for firmware updates, thereby extending the mean time to remediation for critical patches.

Rapid Smart-City LPWAN Gateway Deployments

Urban authorities in China, India, and the Gulf states are installing LoRaWAN and NB-IoT gateways on street furniture to monitor air quality, parking, and waste collection. China Mobile surpassed 300 million NB-IoT endpoints by December 2024, anchoring volume economics for ultra-narrowband silicon. Municipal managers report sensor battery life of over five years, resulting in reduced truck rolls for maintenance. European cities such as Lyon are layering Wi-Fi 7 backhaul onto LPWAN clusters to aggregate traffic into edge nodes that can execute basic analytics before forwarding summaries to the cloud. Government funding tied to sustainability goals accelerates deployment, yet procurement cycles remain long because each new gateway must comply with evolving cybersecurity rules.

AI/ML Inference Moving From Cloud to Gateway Silicon

Chipmakers now integrate neural processing units directly into gateway SoCs, delivering 1-8 TOPS of INT8 inference at sub-10-watt power budgets. Intel’s Atom x6000E line ships with a 1.5 TOPS accelerator and Time-Coordinated Computing for deterministic scheduling. NXP’s Ara-1 device reaches 8 TOPS while meeting ISO 26262 ASIL-B requirements, unlocking functional-safety use cases in automotive V2X gateways. Local inference avoids recurring cloud fees that can reach seven-figure sums in camera-rich factories, however, device fleets now require orchestrated model rollouts to sustain accuracy as operating conditions change. Bootloaders with A-B partitions and encrypted payloads are gaining favor to ensure rollback should an update malfunction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented protocol standards and legacy integration cost | -1.8% | Global, acute in brownfield industrial sites with 20+ year-old equipment | Short term (≤ 2 years) |

| Escalating cyber-attack surface at distributed gateways | -2.1% | North America and Europe, where ransomware targeting OT networks intensified post-2023 | Short term (≤ 2 years) |

| Short refresh cycles driving CAPEX and e-waste concerns | -1.4% | Europe and North America, with regulatory pressure from EU WEEE Directive and circular economy mandates | Medium term (2-4 years) |

| Uneven global 5G coverage limiting advanced use-cases | -1.6% | Emerging markets in Africa, South America, and rural Asia-Pacific where 5G penetration remains below 15% | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Protocol Standards and Legacy Integration Cost

Gateways juggle Modbus RTU, OPC UA, MQTT, CoAP, and vendor-specific fieldbus, forcing separate software stacks that bloat firmware images and complicate quality assurance. IEEE research shows conversion bugs trigger nearly half of gateway downtime, with data-type mismatches between Modbus and MQTT topping the list. While the Matter protocol gained momentum in smart homes, only a minority of industrial gateways shipped in 2025 support it, leaving factories to maintain parallel stacks indefinitely. Retrofitting a decade-old PLC with Ethernet/IP can cost more than replacing the controller, stalling upgrade projects in cash-constrained plants. OEMs respond by shipping modular gateway mezzanine cards, but these add BOM cost and lengthen certification cycles.

Escalating Cyber-Attack Surface at Distributed Gateways

Each deployed gateway exposes web services, message brokers, or SSH consoles that adversaries probe for privilege escalation. A 2024 CISA advisory listed 14 critical vulnerabilities across major gateway brands, including Remote Code Execution flaws in default management dashboards. Digi International’s annual security audit disclosed that 22% of its installed base ran firmware more than 18 months old, highlighting slow patch uptake. IEC 62443 certification enforces secure boot and signed updates, yet it stops short of mandating continuous runtime monitoring, leaving space for intrusion that hijacks sensor payloads. The Ponemon Institute pegs the average cost of an IoT-related breach at USD 4.2 million, with gateways the initial point of compromise in almost one-third of incidents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Connectivity ICs Outpace Processors in Mixed-Radio Designs

Connectivity IC revenue is forecast to expand at 13.11% CAGR during 2026-2031 as multi-radio boards demand discrete RF front-ends for Wi-Fi 7, Bluetooth LE, and 5G RedCap. Qualcomm’s tri-band Wi-Fi 7 chipset generates 5.8 Gbps peak throughput, meeting vision inspection workloads that stream 4K video from production lines. Processors remain the largest line item because they anchor compute and security; yet, their growth lags as OEMs extend life cycles to recoup R&D investments. The IoT gateway market size for connectivity ICs is expected to surpass USD 1 billion by 2031, if unit forecasts hold.

Edge AI inflection reshapes processor criteria. Intel and NXP bundle 1-8 TOPS accelerators plus deterministic clocks, commanding a 23% price premium that OEMs gladly pay to differentiate on inference latency. Memory and storage commoditize, though NOR flash with Execute-in-Place (XiP) retains margin because secure boot demands it. Power-management ICs are designed to accommodate wider input voltage ranges, aligning with global certification standards.

By End-User Industry: Healthcare Surges, Manufacturing Holds Ground

Industrial manufacturing claimed 29.84% of IoT gateway market size in 2025, supported by predictive maintenance and collaborative robots that need real-time failsafe signals. Siemens, ABB, and Schneider Electric integrate gateways into PLC cabinets to simplify procurement. Healthcare grows at 12.98% CAGR as reimbursement frameworks cover remote patient monitoring devices that aggregate vital signs, infusion pump data, and ventilator metrics. A JAMA study reported hospital gateways cut sepsis detection times by six hours, saving critical care beds.

Automotive and transportation sectors leverage V2X gateways for fleet telemetry; however, spectrum allocation delays in the EU are pushing large-scale deployment to 2026. Energy and utilities adopt IP67 gateways in substations for grid balancing, while retail chains install camera-enabled gateways to track footfall, although only one-third realize payback within two years.

By Application: Edge AI Leads New Value Creation

Predictive maintenance held 35.73% share of IoT gateway market size in 2025, leveraging vibration and thermal inputs to cut unscheduled stoppages. Edge AI and analytics is the fastest riser at 13.55% CAGR because running TensorFlow Lite or ONNX locally avoids cloud inference fees that can exceed hardware cost multiples. Intel’s OpenVINO toolkit lets engineers port vision models to gateways with minimal code changes, shortening pilot to production by weeks.

Secure connectivity management gains momentum as enterprises migrate from static VPNs to software-defined zero-trust overlays. Protocol translation gateways grow slowly in greenfield projects that adopt MQTT natively, but they remain relevant in brownfield plants where Modbus devices continue to be in service for decades.

By Deployment Environment: Rugged Outdoor Units Extend Edge to Harsh Sites

DIN-rail gateways retained 34.74% share in 2025, benefiting from mechanical compatibility with factory panels. Rugged outdoor models, sealed to IP67, will outpace the overall IoT gateway market at a 13.33% CAGR as utilities shift their monitoring to remote substations. Portable gateways address construction and event sites where short-term connectivity takes priority over capital expenditure, yet their unit price keeps the adoption niche.

Thermal constraints shape enclosure design; outdoor housings cap processor TDP at 25 watts, limiting AI throughput unless vendors adopt advanced heat-pipe assemblies. Solar charging and five-day battery buffers are becoming mandatory in regions with unreliable grids, particularly in parts of Africa and South America.

Geography Analysis

North America captured 38.74% IoT gateway market share in 2025, bolstered by early 5G standalone deployments and logistics hubs that rely on private LTE for asset tracking. Cisco shipped 180,000 industrial gateways in fiscal 2025, bundling Splunk analytics to differentiate. Canada concentrates on mining and forestry with rugged units that endure sub-zero winters, while Mexico’s nearshoring wave installs greenfield IIoT lines for automotive suppliers.

Asia-Pacific grows at 13.66% CAGR, the swiftest worldwide. China deploys NB-IoT gateways for smart meters at massive scale, and India rolls out LoRaWAN hubs in agricultural logistics corridors. Japan and South Korea are pioneers in 5G private networks for autonomous mobile robots, whereas Australia utilizes LPWAN for crop and cattle oversight across vast ranches. Regulatory fragmentation, such as India’s pending device security certification, can postpone launches by up to a year.

Europe held 22% share in 2025. Germany invests heavily under the Industry 4.0 program, France pushes smart-city pilots, and the UK channels post-Brexit policy toward 5G campus networks. The NIS2 Directive mandates IEC 62443 compliance, adding 15-20% to the cost of gateway bills while enhancing baseline security. Southern European adoption trails due to lower automation intensity, and Eastern Europe grows as auto suppliers modernize.

The Middle East and Africa hold a combined 7% share. The UAE and Saudi Arabia fund mega-projects where thousands of gateways support autonomous mobility and energy management. South America adopts LoRaWAN for irrigation and smart metering, though economic headwinds impede broad rollouts.

Competitive Landscape

The IoT gateway market is moderately fragmented as the top 10 suppliers command most of combined revenue. Cisco, Advantech, and Dell Technologies leverage existing networking portfolios to upsell edge hardware, while Intel, Qualcomm, and NXP integrate vertically by offering reference designs that shorten OEM time-to-market. Industrial automation incumbents such as Siemens and ABB build gateway logic into PLCs, framing IoT as a feature rather than a separate SKU. Huawei, Nokia, and Ericsson tie gateways to 5G infrastructure deals, bundling radio, core, and edge in a single contract.

Healthcare requires FDA-cleared data paths, prompting Digi International to launch a HIPAA-compliant gateway that targets the USD 400 million remote patient monitoring niche. Oil and gas demand ATEX-certified enclosures, limiting competition to rugged specialists. Start-ups such as Samsara decouple middleware from hardware, letting customers load containerized workloads over the air. IEC 62443 mandates now filter suppliers that lack secure boot or runtime integrity checks, raising barriers for new entrants.

IoT Gateway Industry Leaders

Cisco Systems, Inc.

Advantech Co., Ltd.

Microchip Technology Inc.

Huawei Technologies Co., Ltd.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Itron acquired Urbint for USD 325 million to embed AI-based risk prediction in smart grid gateways.

- October 2025: Qualcomm unveiled the QCS8550 gateway SoC with integrated 5G RedCap modem and 12 TOPS AI accelerator.

- September 2025: Siemens partnered with AWS to preload Industrial Edge gateways with Greengrass for easy Lambda deployment.

- July 2025: Cisco reported shipping 180,000 industrial gateways, a 34% annual rise, fueled by 5G private network demand.

Global IoT Gateway Market Report Scope

The IoT Gateway Market Report is Segmented by Component (Processor, Sensor, Memory and Storage Device, Connectivity IC, Logic/ASIC, Power Management and Others), End-User Industry (Industrial/Manufacturing, Automotive and Transportation, Healthcare and Life Sciences, Consumer Electronics and Smart Home, Energy and Utilities, BFSI, Oil and Gas, Retail and Hospitality, Aerospace and Defense, Agriculture and Smart Farming), Deployment Environment (DIN-rail/Guide-rail, Wall-mounted/Cabinet, Embedded/Board-level, Rugged Outdoor, Portable/Mobile), Application (Edge AI and Analytics, Remote Monitoring and Telemetry, Predictive Maintenance, Secure Connectivity Management, Protocol Translation Gateway), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Processor |

| Sensor |

| Memory and Storage Device |

| Connectivity IC |

| Logic / ASIC |

| Power Management and Other Components |

By End-User Industry

| Industrial / Manufacturing |

| Automotive and Transportation |

| Healthcare and Life Sciences |

| Consumer Electronics and Smart Home |

| Energy and Utilities |

| BFSI |

| Oil and Gas |

| Retail and Hospitality |

| Aerospace and Defense |

| Agriculture and Smart Farming |

By Application

| Edge AI and Analytics |

| Remote Monitoring and Telemetry |

| Predictive Maintenance |

| Secure Connectivity Management |

| Protocol Translation Gateway |

By Deployment Environment (Form Factor)

| DIN-rail / Guide-rail |

| Wall-mounted / Cabinet |

| Embedded / Board-level |

| Rugged Outdoor |

| Portable / Mobile |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Processor | ||

| Sensor | |||

| Memory and Storage Device | |||

| Connectivity IC | |||

| Logic / ASIC | |||

| Power Management and Other Components | |||

| By End-User Industry | Industrial / Manufacturing | ||

| Automotive and Transportation | |||

| Healthcare and Life Sciences | |||

| Consumer Electronics and Smart Home | |||

| Energy and Utilities | |||

| BFSI | |||

| Oil and Gas | |||

| Retail and Hospitality | |||

| Aerospace and Defense | |||

| Agriculture and Smart Farming | |||

| By Application | Edge AI and Analytics | ||

| Remote Monitoring and Telemetry | |||

| Predictive Maintenance | |||

| Secure Connectivity Management | |||

| Protocol Translation Gateway | |||

| By Deployment Environment (Form Factor) | DIN-rail / Guide-rail | ||

| Wall-mounted / Cabinet | |||

| Embedded / Board-level | |||

| Rugged Outdoor | |||

| Portable / Mobile | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the IoT gateway market in 2031?

The IoT gateway market is expected to reach USD 4.51 billion by 2031, reflecting a 12.61% CAGR during 2026-2031.

Which region is forecast to grow the fastest for IoT gateways to 2031?

Asia-Pacific leads with a projected 13.66% CAGR, driven by large-scale NB-IoT smart-meter programs and rapid 5G private-network adoption.

Which industry vertical shows the highest growth momentum for IoT gateways?

Healthcare is advancing at a 12.98% CAGR as reimbursable remote patient monitoring scales in hospitals and home-care settings.

How does 5G RedCap influence gateway adoption?

5G RedCap delivers 150 Mbps throughput at lower power draw than full 5G, making cellular backhaul economical for mid-bandwidth gateways in logistics and manufacturing.

Why are rugged outdoor gateways gaining traction?

Utilities, oil and gas, and transportation agencies need IP67-rated enclosures that withstand −40 °C to +75 °C, which drives a 13.33% CAGR for rugged models.

Page last updated on: