EMEA IoT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

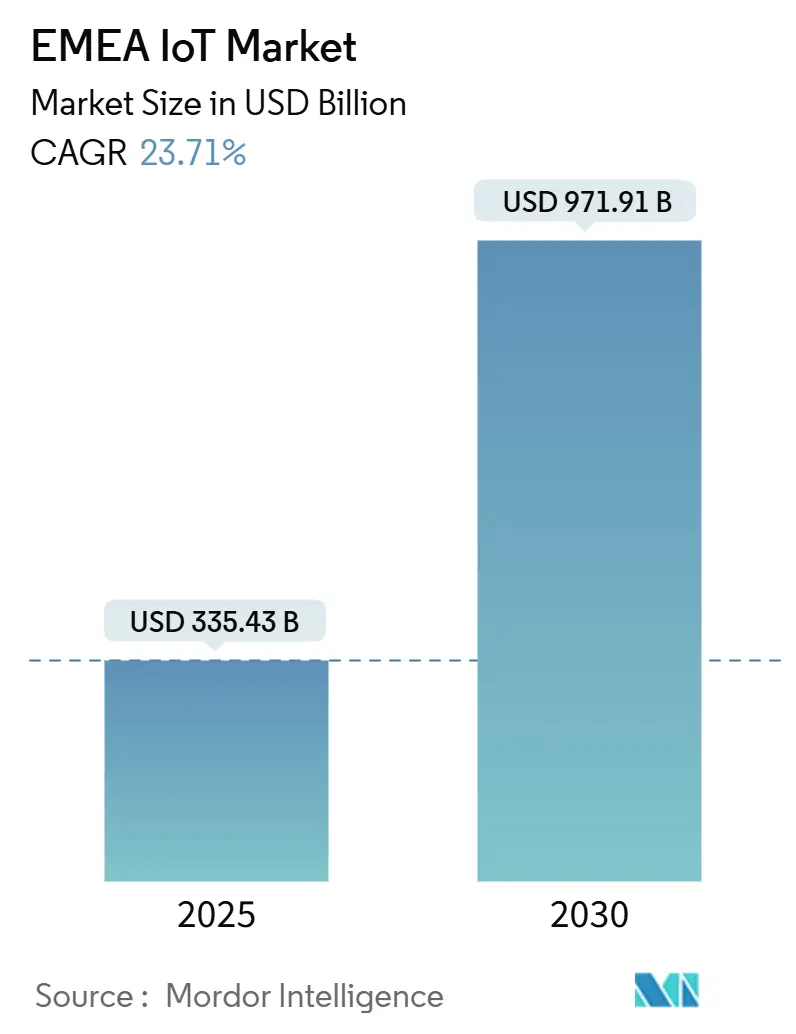

| Market Size (2025) | USD 335.43 Billion |

| Market Size (2030) | USD 971.91 Billion |

| Growth Rate (2025 - 2030) | 23.71% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EMEA IoT Market Analysis by Mordor Intelligence

The EMEA IoT market size stands at USD 335.43 billion in 2025 and is projected to reach USD 971.91 billion by 2030, posting a robust 23.71% CAGR through the forecast period. Growing 5G standalone coverage, EU Digital Decade grants, and factory-floor automation are propelling the EMEA IoT market, while managed platforms and edge-cloud orchestration create recurring revenue streams. Hardware remains a scale anchor, yet platform-centric services outpace device sales as enterprises shift toward outcome-based models. Cellular connectivity leads today, but LPWAN and hybrid satellite links lower operating costs for utilities and logistics. Europe provides the largest installed base, whereas Gulf smart-city programs and African mobile-first projects add momentum, broadening the addressable opportunity for vendors.

Key Report Takeaways

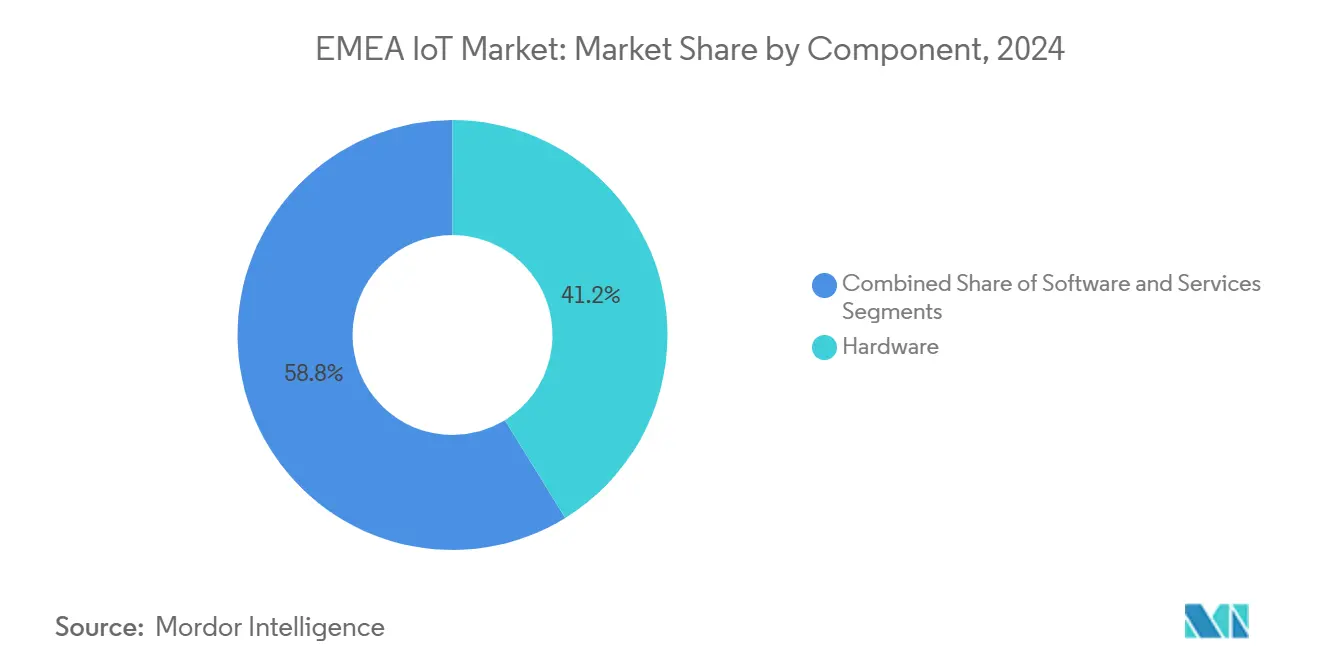

- By component, hardware captured 41.22% of the EMEA IoT market share in 2024; services are forecast to advance at a 24.78% CAGR through 2030.

- By connectivity technology, cellular led with 45.89% revenue share in 2024, while LPWAN is projected to expand at a 23.82% CAGR to 2030.

- By application, manufacturing and Industrial 4.0 held 27.64% of the EMEA IoT market size in 2024; smart cities are set to grow at a 23.78% CAGR.

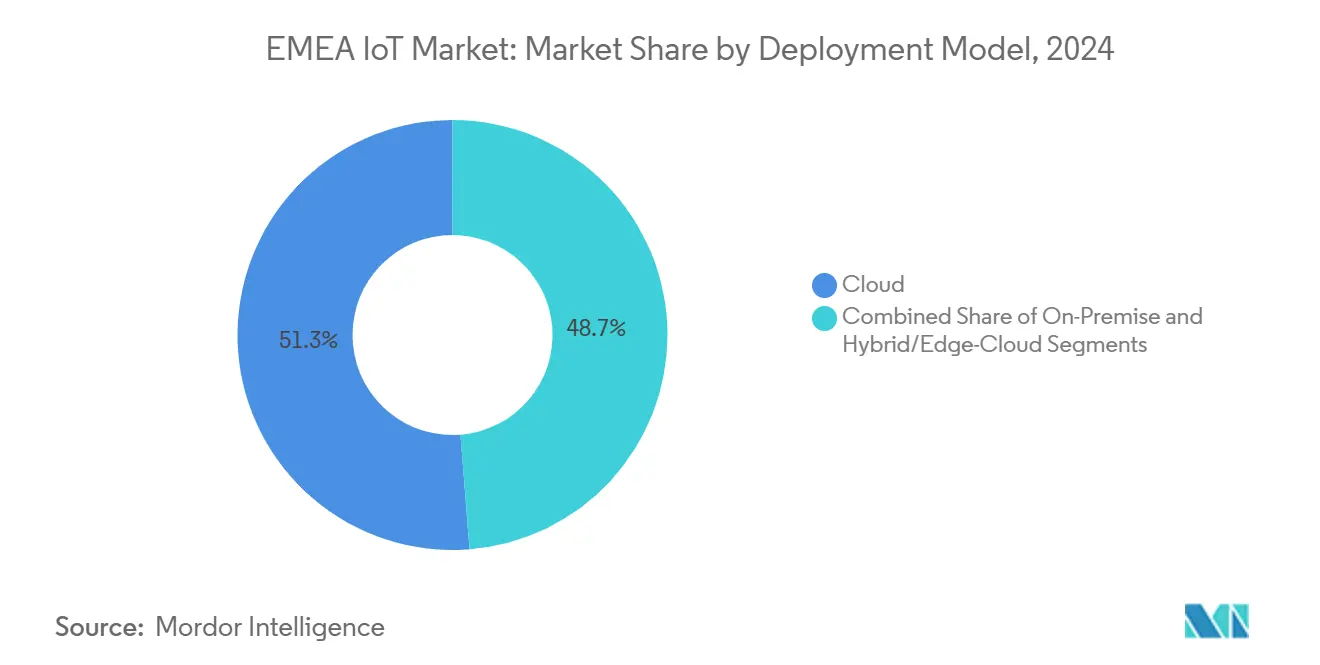

- By deployment model, cloud deployments accounted for 51.26% of the EMEA IoT market size in 2024, and hybrid edge-cloud architectures are advancing at a 24.64% CAGR.

- By enterprise size, large enterprises controlled 61.89% of the EMEA IoT market share in 2024, whereas SMEs exhibited the highest 24.93% CAGR.

- By geography, Europe led with 56.77% of 2024 revenue; the Middle East records the fastest 24.14% CAGR through 2030.

EMEA IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G SA roll-outs slash latency and boost industrial IoT adoption | +4.2% | Europe, Middle East core markets | Medium term (2-4 years) |

| EU Digital Decade funds for smart-grid modernization | +3.8% | Europe, spillover to North Africa | Long term (≥ 4 years) |

| Post-COVID manufacturing automation surge | +3.1% | Global EMEA manufacturing hubs | Short term (≤ 2 years) |

| E-SIM and iSIM simplify cross-border device provisioning | +2.9% | Global EMEA, cross-border applications | Medium term (2-4 years) |

| Energy-harvesting sensor nodes cut maintenance OPEX | +2.4% | Europe, Middle East utilities | Long term (≥ 4 years) |

| Green-tax incentives for carbon-tracking sensors | +1.8% | Europe, select Middle East markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Standalone Architecture transforms industrial IoT economics

Ultra-low-latency 5G SA networks unlock sub-10 ms control loops that legacy LTE could not support, shifting automation ROI calculations in heavy manufacturing lines. Network slicing lets factories reserve premium bandwidth for safety-critical robots while keeping non-critical sensors on cost-efficient slices, encouraging plant-wide adoption. Vodafone’s cross-border partnership with Mobily showcases this sub-second consistency across Saudi production sites. [1]Vodafone Group, “Vodafone Business IoT and Mobily Expand 5G SA Connectivity in Saudi Arabia,” vodafone.com The simplified core removes 4G anchors, enabling private networks that industrial operators can self-manage, cutting integration timelines. As a result, EMEA manufacturers view 5G SA less as faster broadband and more as the digital backbone of converged OT-IT environments, lifting spending trajectories.

EU Digital Decade funding reshapes smart-grid investment patterns.

EU-backed capital allocates billions for grid digitization, steering utility tenders toward IoT-ready hardware and data platforms. Water, gas, and power firms accelerate roll-outs because real-time telemetry slashes truck rolls and shrinks non-technical losses. Netmore’s award to replace 1.3 million LoRaWAN meters at Yorkshire Water shows how public grants catalyze one of Europe’s largest utility IoT deployments. [2]Netmore Group, “Yorkshire Water to Deploy 1.3 Million LoRaWAN Meters,” netmoregroup.com Cross-border projects hedge component shortages by pooling inventories, while standardized data schemas born from EU directives ripple into neighboring North African utilities seeking interoperability. Vendors able to pre-certify to these frameworks shorten sales cycles and command premium service margins.

Manufacturing automation surge drives edge computing adoption.

Factory owners hasten robotics programs to counter rising wages and supply-chain shocks, lifting unit demand for rugged gateways and on-premise analytics nodes. Q1 2025 shipments of cellular IoT modules rose 23%, reflecting the scramble for multi-vendor redundancy amid geopolitical friction. Process engineers increasingly insist on edge inference for quality inspection, trimming cloud round-trip and bandwidth fees. Providers combining hardware, containerized apps, and managed security differentiate in a segment where downtime penalties remain high. Data-sovereign architectures, especially in Germany and France, tip procurement specs toward solutions that execute AI locally yet integrate with corporate cloud dashboards.

E-SIM and iSIM technologies eliminate cross-border barriers

Remote-provisioned SIMs let logistics trackers and consumer wearables roam across dozens of EMEA networks without physical swaps, collapsing SKU counts and time-to-market. Pelion’s consumer eSIM rollout exemplifies how providers extend beyond industrial M2M into smartwatch and health-monitor segments. [3]Pelion, “Consumer eSIM Launch Extends Seamless Connectivity to Wearables,” pelion.com OEMs cut plastics and slot mechanics, meeting eco-design rules while lowering the bill of materials. Regulators from the GCC to the EU now embrace eSIM standards, shrinking certification cycles. As carrier lock-in fades, platform vendors that bundle connectivity, SIM lifecycle tools, and security keys position themselves as one-stop shops for cost-conscious SMEs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented spectrum regulation across MENA | -2.8% | Middle East, North Africa | Medium term (2-4 years) |

| Cyber-skills shortage inflates secure-by-design costs | -2.1% | Global EMEA, acute in Europe | Long term (≥ 4 years) |

| Scarcity of RoHS-compliant chip packaging in Africa | -1.6% | Sub-Saharan Africa primarily | Short term (≤ 2 years) |

| EU Data Act may throttle raw-data monetization | -1.4% | Europe, spillover effects globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented spectrum regulation constrains MENA scaling.

Operators in neighboring Gulf and North African nations license different frequency blocks and power limits, forcing device makers to craft market-specific SKUs. Compliance labs report multi-band certification fees as high as 15% of total device cost for pan-MENA logistics trackers, eroding ROI. Harmonization efforts remain nascent, so vendors pre-load firmware tables for each regulator, adding update complexity. The result is slower regional adoption despite strong sovereign funding commitments.

Cybersecurity skills shortage inflates secure-by-design costs.

Across EMEA, unfilled cyber positions push consulting rates beyond USD 200 per hour, straining SME deployment budgets. Industrial firms divert scarce developers to patching device firmware rather than building new features, lengthening pilot phases. Dependence on external auditors raises vendor lock-in risks, while insurers raise premiums for projects lacking certified in-house experts. Until vocational programs catch up, cost overruns and delayed go-lives act as a drag on overall EMEA IoT market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services capture growth momentum

Hardware still underpins deployments, holding 41.22% of 2024 revenue; however, managed platforms and analytics services compound at 24.78% CAGR, eclipsing unit sales growth. The EMEA IoT market size for services reflects enterprises’ desire to outsource lifecycle management rather than expand IT headcount. Subscription-priced device management, firmware-over-the-air, and remote SIM provisioning shift capital expense to operating expense, smoothing budgets. Hardware makers such as Advantech now bundle monitoring dashboards to upsell post-install support.

Ongoing green-tax compliance, predictive maintenance, and SaaS-based AI models further raise service penetration. The pivot rewards providers offering industry-specific blueprints for water utilities, smart buildings, and fleet telematics. Enterprises that initially procured hardware-only now revisit total cost of ownership and migrate to platform contracts that guarantee service-level agreements, reinforcing the recurring-revenue flywheel and reshaping vendor valuation multiples.

By Connectivity Technology: LPWAN accelerates, cellular adapts

Cellular accounts for 45.89% of 2024 connectivity spend, leveraging ubiquitous macro-grid coverage and carrier billing relationships. Still, LPWAN volume grows fastest at 23.82% CAGR as energy-harvesting sensors stretch battery life to 10 years and subscription fees drop below USD 1 per device annually. The EMEA IoT market share of LPWAN endpoints rises in rural utilities, street-lighting, and smart-agriculture because single-base-station networks cover tens of square miles. LoRa Gen 4’s improved link budget pushes that radius even farther.

Carriers respond by bundling NB-IoT and Cat-M in 5G core slices, preserving relevance for mobile-originated use cases. Satellite back-haul increasingly augments both cellular and LPWAN footprints; Iridium’s NTN Direct integration with Deutsche Telekom illustrates hybrid orchestration that enterprises can manage via a single portal. Vendors capable of auto-switching between terrestrial and non-terrestrial networks mitigate coverage gaps, appealing to logistics and mining operators with multi-country asset pools.

By Application: Smart-city spend outpaces factory budgets.

Manufacturing maintains the single-largest 27.64% slice thanks to entrenched Industry 4.0 roadmaps, yet city administrators are signing multi-year ICT tenders that push smart-city CAGRs to 23.78%. Public-private partnerships fund traffic-light optimization, waste-bin fill sensors, and AI-enabled surveillance. Abu Dhabi’s USD 2.5 billion cognitive-city program anchors Gulf momentum and signals sovereign intent to leapfrog legacy infrastructure.

Meanwhile, factory capex remains steady but increasingly targets advanced analytics, robot orchestration, and vision inspection rather than basic sensor retrofits. Energy and utilities use cases progress as regulators mandate real-time grid balancing, leveraging the same edge nodes deployed for manufacturing. Healthcare pilots for remote patient monitoring gain traction following pandemic tele-health success, while retail footfall analytics rebounds as malls reboot omnichannel strategies.

By Deployment Model: Hybrid edge-cloud finds its footing

With 51.26% of 2024 revenue, public cloud still underpins many dashboards, yet data-residency statutes and latency needs propel a 24.64% CAGR for hybrid edge-cloud rollouts. The EMEA IoT market size attached to on-premise gateways grows as firms deploy micro-data-centers that filter noise locally, forwarding only tagged insights to the cloud. Akenza’s 300-site U.K. smart-building win highlights how centralized policy enforcement coexists with branch autonomy.

Regulators cite GDPR and emerging EU Data Act clauses when urging enterprises to process customer identifiers within regional boundaries. Hardware suppliers embed Kubernetes distributions to harmonize container orchestration between factory PCs and hyperscaler regions. This duality boosts demand for observability tools that reconcile data lineage across tiers and for zero-trust frameworks that secure east-west traffic inside the plant.

By Enterprise Size: SME adoption surges on turnkey offers

Large enterprises dominated 61.89% of 2024 spending, but streamlined no-code dashboards and pay-as-you-grow pricing lifted SME growth to 24.93% CAGR. Start-ups curb time-to-value by integrating sensors, cellular data, and analytics behind a single invoice, minimizing in-house DevOps. For instance, Swiss module-maker u-blox posted 41% H1 2025 EMEA revenue growth by packaging GPS-assisted cloud services that simplify asset tracking for smaller fleets.

SMEs often enter through compliance triggers-cold-chain monitoring or ESG reporting-then extend deployments once ROI is visible. As E-SIM makes roaming costs predictable, cross-border exporters warm to fleet telematics that previously required bespoke SIM swaps. Large enterprises, meanwhile, pilot AI-driven prescriptive maintenance and carbon-footprint dashboards, demanding enterprise-grade audit trails and open APIs that smaller vendors must rush to deliver.

Geography Analysis

Europe retains 56.77% of the 2024 EMEA IoT market revenue, buoyed by mature industrial clusters, Digital Decade subsidies, and strict data-sovereignty mandates that favor local providers. German automotive lines, U.K. smart-grid retrofits, and French environmental monitoring collectively sustain a broad supplier ecosystem. The region now channels budgets toward AI co-processors at the edge, backed by public investment such as the U.K.’s partnership with NVIDIA to build national AI supercomputing capacity.

Middle-East spending grows at 24.14% CAGR as sovereign wealth funds bankroll giga-projects like Saudi Arabia’s NEOM, embedding IoT infrastructure from day zero. Dubai’s port authority integrates IoT cranes with blockchain cargo manifests to cut berth dwell times, illustrating holistic adoption. Edge computing racks manufactured locally in the UAE benefit from zero-tariff import of semiconductors, further catalyzing domestic value chains.

Africa presents a mobile-first patchwork where prepaid cellular dominates, yet smart-agriculture pilots in Kenya and IoT-enabled mine ventilation in South Africa display leapfrog potential. Component shortages and RoHS-compliant packaging shortfalls inflate BOM costs by up to 20%, encouraging regional assembly ventures that court government incentives. Cross-border harmonization of spectrum and customs regimes remains pivotal for unlocking continental scale.

Competitive Landscape

The vendor field shows moderate fragmentation; the top five hardware and connectivity suppliers hold roughly 45% combined share, leaving ample white space for niche entrants. Advantech, Kontron, and Eurotech extend industrial PCs with AI accelerators, pitching end-to-end bundles instead of boards alone. Telit Cinterion and Quectel enhance modules with direct-to-cell and NTN firmware to safeguard relevance as satellite options proliferate.

Platform specialists such as LORIOT champion protocol-agnostic device managers that orchestrate LoRaWAN, cellular, and satellite links under one SLA. Blues’ September 2025 launch of Starnote positions it to serve asset trackers needing global coverage without carrier negotiations, challenging terrestrial incumbents. Private-equity moves, including Advent’s USD 1.19 billion buyout of u-blox, signal rising valuations for component makers with software attach potential.

Partnership networks multiply: Netmore’s acquisition of Arson Metering extends its vertical reach into smart water, while Forterro’s purchase of Inology broadens industrial ERP hooks for IoT data ingestion. Success factors increasingly hinge on cybersecurity credentials, multi-modal connectivity orchestration, and compliance automation. Vendors unable to meet secure-by-design checklists risk exclusion from EU-funded tenders, prompting M&A as a shortcut to certification portfolios.

EMEA IoT Industry Leaders

Advantech Co., Ltd.

Sierra Wireless (now Semtech Corp. IoT Division)

u-blox Holding AG

Telit Cinterion Ltd.

Quectel Wireless Solutions Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Blues expanded global satellite IoT coverage with Starnote for Iridium, offering hybrid connectivity for remote asset tracking.

- September 2035: Netmore acquired Arson Metering to strengthen utility smart-meter solutions.

- September 2025: Forterro bought Inology, bolstering industrial IoT software breadth.

- September 2025: Iridium began integrating NTN Direct with Deutsche Telekom for hybrid satellite-terrestrial services.

EMEA IoT Market Report Scope

| Hardware |

| Software |

| Services |

| Cellular (2G/3G/4G/5G) |

| LPWAN (LoRaWAN, Sigfox, NB-IoT, LTE-M) |

| Short-Range (Wi-Fi, Bluetooth, Zigbee/Thread) |

| Satellite IoT |

| RFID/NFC |

| Manufacturing and Industrial 4.0 |

| Smart Cities |

| Energy and Utilities |

| Healthcare |

| Retail |

| Transportation and Logistics |

| Agriculture |

| Cloud |

| On-Premise |

| Hybrid/Edge-Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Connectivity Technology | Cellular (2G/3G/4G/5G) | |

| LPWAN (LoRaWAN, Sigfox, NB-IoT, LTE-M) | ||

| Short-Range (Wi-Fi, Bluetooth, Zigbee/Thread) | ||

| Satellite IoT | ||

| RFID/NFC | ||

| By Application | Manufacturing and Industrial 4.0 | |

| Smart Cities | ||

| Energy and Utilities | ||

| Healthcare | ||

| Retail | ||

| Transportation and Logistics | ||

| Agriculture | ||

| By Deployment Model | Cloud | |

| On-Premise | ||

| Hybrid/Edge-Cloud | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Geography | Europe | United Kingdom |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the EMEA IoT market in 2025?

The EMEA IoT market size is USD 335.43 billion in 2025, with a projected 23.71% CAGR to 2030.

Which segment is growing fastest within EMEA IoT deployments?

Services, covering managed platforms and analytics, are expanding at a 24.78% CAGR through 2030.

What connectivity option is challenging cellular dominance?

LPWAN networks, aided by energy-harvesting sensors, are growing at a 23.82% CAGR and gaining share in utilities and agriculture.

Why are hybrid edge-cloud architectures gaining traction?

Data-sovereignty rules and latency-sensitive industrial apps require local processing, driving a 24.64% CAGR for hybrid deployments.

Which geography shows the highest growth momentum?

The Middle East leads with a 24.14% CAGR, propelled by sovereign smart-city mega-projects and AI infrastructure spending.

How are SMEs adopting IoT despite limited resources?

Turnkey platforms with eSIM-enabled connectivity and subscription pricing let SMEs deploy quickly, fueling a 24.93% CAGR in this segment.

Page last updated on: