Intelligent Electronic Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

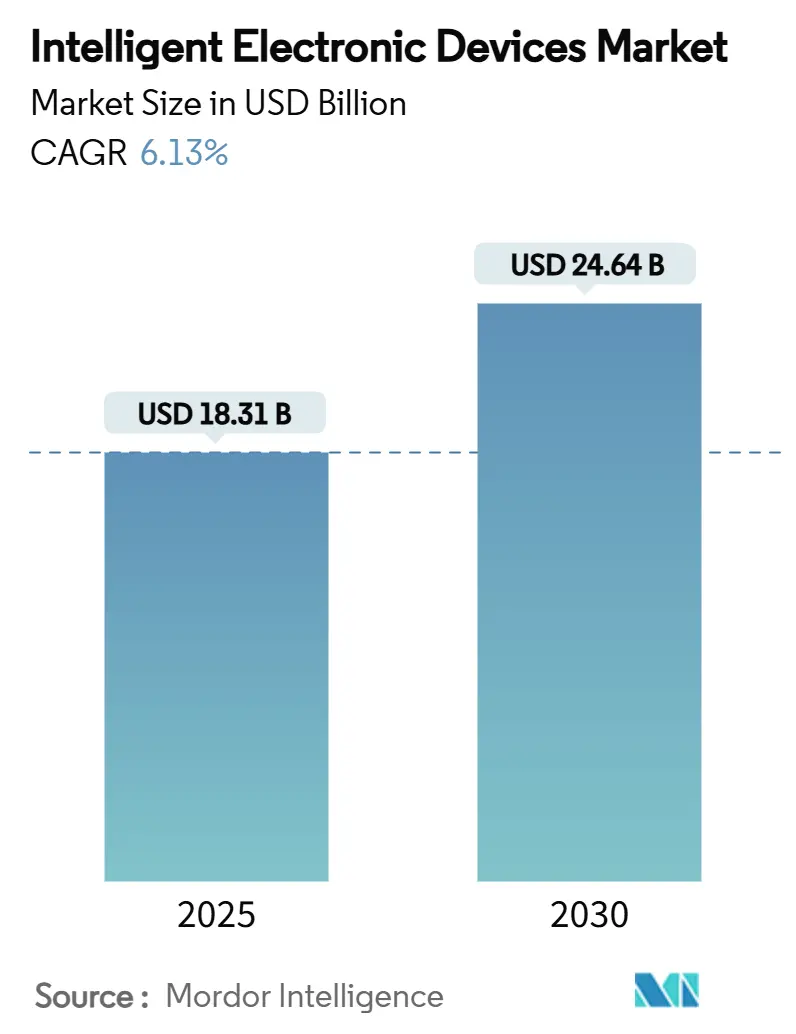

| Market Size (2025) | USD 18.31 Billion |

| Market Size (2030) | USD 24.64 Billion |

| Growth Rate (2025 - 2030) | 6.13% CAGR |

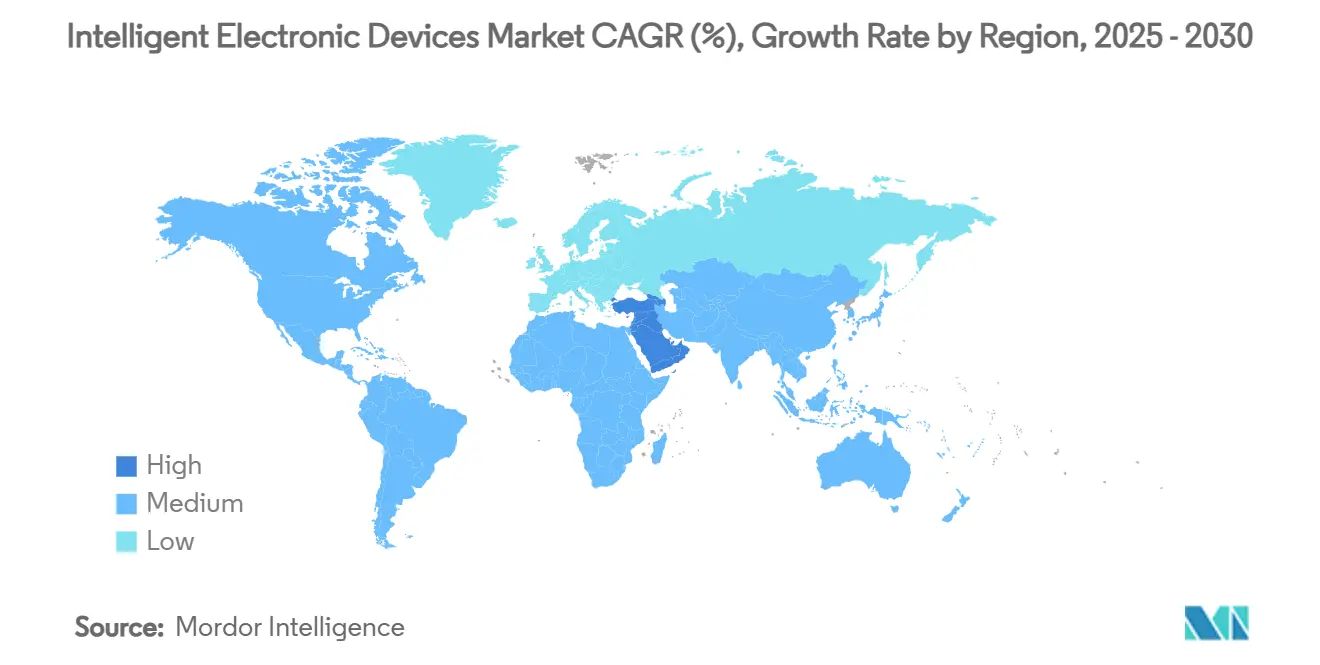

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

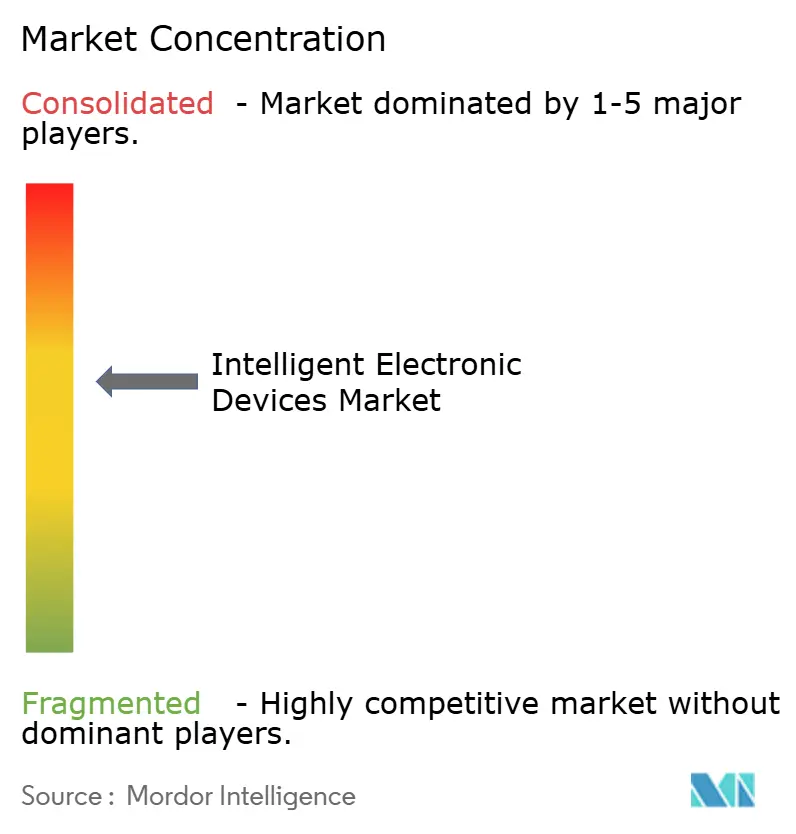

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Electronic Devices Market Analysis by Mordor Intelligence

The intelligent electronic devices market size is valued at USD 18.31 billion in 2025 and is forecast to reach USD 24.64 billion by 2030, reflecting a 6.13% CAGR over the period. Strong demand stems from grid-modernization mandates, rapid distributed energy resource (DER) integration, and heightened cybersecurity requirements that collectively accelerate digital substation rollouts. Asia-Pacific retains leadership owing to large-scale infrastructure investments, while the Middle East records the swiftest uptake as smart-city and renewable Mega-projects scale. Utilities anchor current volumes; however, data-center operators are expanding deployments to assure power resilience for AI and cloud workloads. Competitive rivalry intensifies as established OEMs virtualize hardware functions, pursue software-defined architectures, and integrate end-to-end cyber-resilience to defend share.

Key Report Takeaways

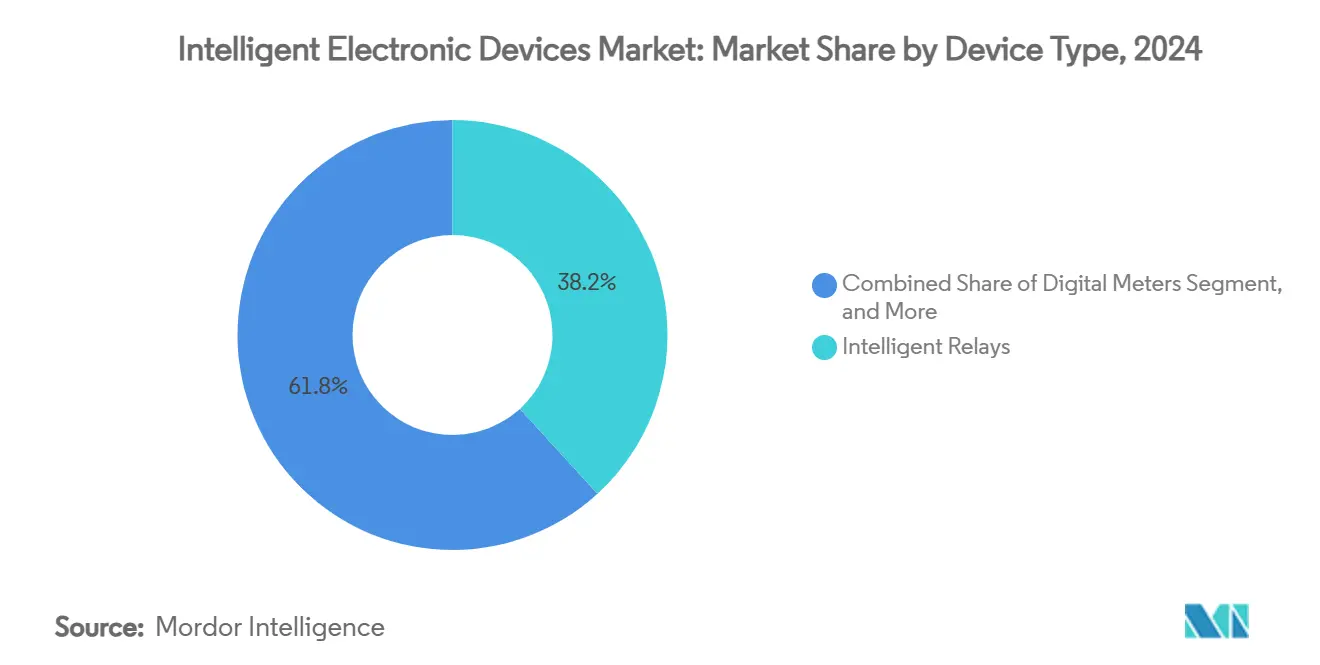

- By device type, intelligent relays accounted for 38.23% of intelligent electronic devices market share in 2024; capacitor bank controllers are projected to grow at an 8.34% CAGR through 2030.

- By application, substation automation commanded 39.45% of the intelligent electronic devices market size in 2024, whereas power quality monitoring and recording is advancing at a 9.26% CAGR to 2030.

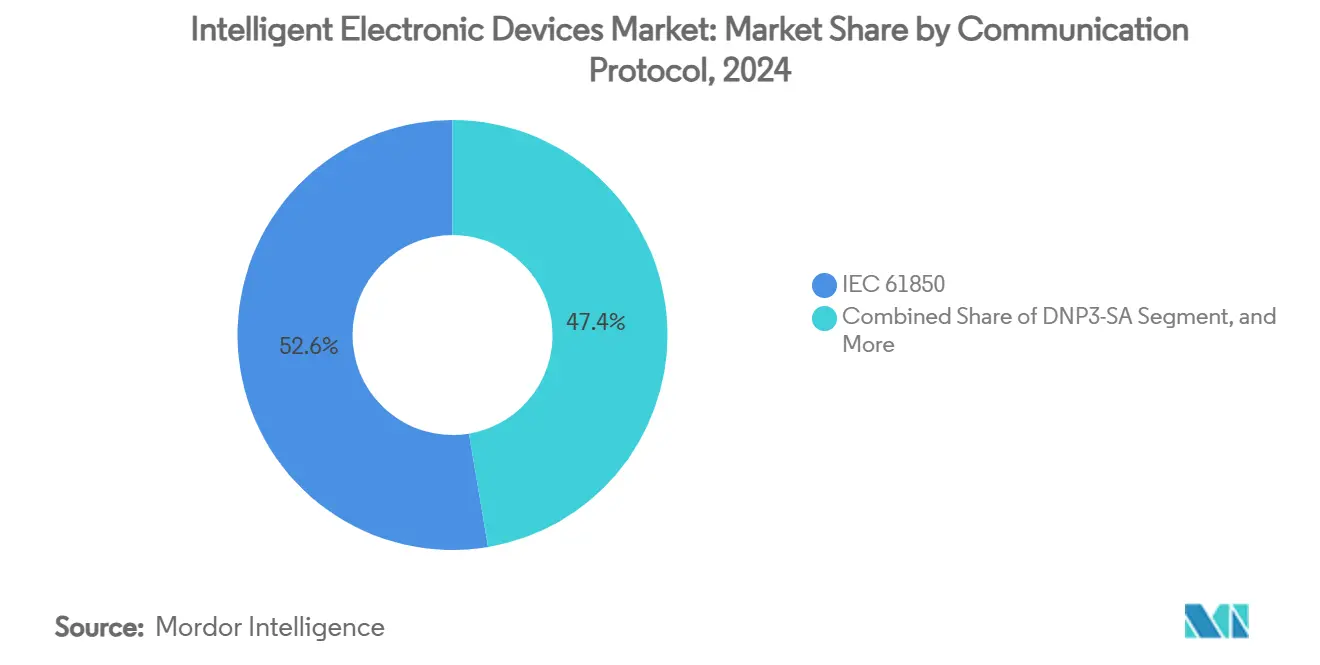

- By communication protocol, IEC 61850 held 52.64% share of the intelligent electronic devices market in 2024, while DNP3-SA is expected to expand at a 12.89% CAGR through 2030.

- By end-user industry, utilities led with 48.23% revenue share in 2024; data centers represent the fastest-growing vertical at an 11.89% CAGR to 2030.

- By geography, Asia-Pacific represented 33.38% of global revenue in 2024, and the Middle East is projected to post an 11.65% CAGR through 2030.

Global Intelligent Electronic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization mandates and stimulus funding | +1.9% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Surge in distributed energy resources (DER) integration | +1.8% | APAC core, spill-over to MEA and Europe | Long term (≥ 4 years) |

| Rising substation automation projects in emerging Asia | +1.2% | APAC, particularly China, India, Southeast Asia | Short term (≤ 2 years) |

| Cyber-resilience requirements for critical infrastructure | +0.9% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Solid-state breaker adoption for high-frequency switching | +0.8% | Global, led by industrial and data center applications | Long term (≥ 4 years) |

| Expansion of IEC 61850-9-2LE process bus architectures | +0.7% | Global, with faster adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Mandates and Stimulus Funding

Government funding surges ensure that utilities prioritize digital protection, control, and monitoring. Dubai Electricity and Water Authority earmarked AED 7 billion (USD 1.9 billion) in 2024 to automate restoration, catalyzing demand for multiprotocol IEDs compatible with IEC 61850 process-bus topologies.[1]Control Engineering Staff, “Automatic Smart Grid Restoration Funding in Dubai,” controleng.com China’s State Grid Corporation invested CNY 600 billion (USD 83.5 billion) in 2024 for ultra-high-voltage corridors, embedding IED deployments across thousands of substations.[2]State Grid Corporation of China, “Smart Grid Digitalization Initiatives,” sgcc.com.cn These fiscal stimuli compress payback periods, accelerate procurement cycles, and encourage platform standardization that favors vendor ecosystems offering integrated hardware, software, and cyber-resilience.

Surge in Distributed Energy Resources Integration

Photo-voltaic roofs, battery storage, and vehicle-to-grid services disrupt traditional protection philosophies by injecting bidirectional flows with low inertia. Advanced IEDs harness machine-learning fault prediction that achieves 100% disturbance-detection precision.[3]IEEE Editorial Board, “Ethernet and IEC 61850 Communications,” ieeexplore.ieee.org Merging units digitize analog signals adjacent to instrument transformers, beam sampled values via fiber, and enable coordinated voltage control that stabilizes rapid PV-induced fluctuations beyond legacy regulator capability. Utilities thus pivot to hierarchical voltage-control schemes that combine DER dispatch with real-time analytics to keep frequency and voltage within strict limits.

Rising Substation Automation Projects in Emerging Asia

Indonesia commissioned its first fully digital substation in 2024, achieving a 30% reduction in copper cabling by adopting process-bus architectures. Thailand’s Energy 4.0 blueprint scales digital substations across industrial corridors, while Nepal’s 39-substation plan underscores the region’s leapfrog modernization. Centralized Protection and Control systems integrate AI-driven asset analytics, delivering predictive maintenance that cuts mean time-to-repair by 20% and reduces outage minutes for fast-growing urban loads. Global OEMs tailor modular skids and containerized solutions to compress construction timelines amid rapid electrification.

Cyber-Resilience Requirements for Critical Infrastructure

Successful attacks on legacy RTUs elevate cyber-risk to board-level priority. DNP3-SA adds AEAD-AES-256-GCM encryption and role-based authorization to mitigate man-in-the-middle exploits. The Thales–SEL laboratory launched in 2024 supplies utilities with scenario-based cyber-range training that integrates real protection relays to model blended IT/OT intrusions. Modern IEDs embed deep-packet inspection, secure boot, and over-the-air patching, enabling utilities to fulfill NERC-CIP or EU NIS2 obligations without extensive truck-rolls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX and ROI uncertainty | -0.7% | Global, particularly affecting smaller utilities | Short term (≤ 2 years) |

| Legacy asset interoperability challenges | -0.4% | Developed markets with extensive existing infrastructure | Medium term (2-4 years) |

| Scarcity of utility-grade time-synchronization skills | -0.3% | Global, with acute shortages in emerging markets | Medium term (2-4 years) |

| EMS-DMS platform cyber-liability risk transfer gaps | -0.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX and ROI Uncertainty

Major substation retrofits incorporating IEC 61850 digital bays, optical CT/VT sensors, and cyber-secure bay controllers can exceed USD 50 million, straining budgets of small co-ops. Recovering costs through tariff filings remains uncertain where regulators scrutinize rate impacts on consumers. Soft benefits—improved SAIDI/SAIFI metrics, deferred asset replacement, and workforce safety—often lack immediate fiscal translation, lengthening approval cycles.

Legacy Asset Interoperability Challenges

Utilities with mixed vintages of electromechanical and digital relays wrestle with protocol gateways that add latency and complicate maintenance. Proprietary point-to-point wiring conflicts with object-oriented IEC 61850 naming, necessitating costly rewiring or dual-operating modes during cutover. Semantic mismatches between SCADA databases and logical nodes further elevate integration complexity, impeding fast adoption in brownfield environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Intelligent Relays Assume Central Protection Role

Intelligent relays captured 38.23% intelligent electronic devices market share in 2024 as utilities replaced aging electromechanical units with multifunction microprocessor platforms capable of distance, differential, and arc-flash protection in a single chassis. The intelligent electronic devices market size for capacitor bank controllers is forecast to expand at 8.34% CAGR through 2030, propelled by solid-state switching that delivers sub-cycle VAR compensation critical for high-PV feeders. Providers now embed machine-learning algorithms that predict capacitor-switch contact wear and schedule maintenance only when statistical failure thresholds near, saving operating expense.

Capacitor bank controller uptake accelerates alongside DER penetration because fast VAR support mitigates flicker and voltage violations. Meanwhile, digital meters advance through AMI rollouts that allow granular power-quality analytics, enabling utilities to monetize premium-quality service tiers. Feeder protection IEDs integrate traveling-wave technology for high-impedance fault detection, curbing wildfire risk in drought-prone territories. Voltage regulator controllers shift toward vacuum interrupters that last 10× longer than oil counterparts, lowering lifecycle cost for rural co-ops.

By Application: Substation Automation Underpins Digital Grid Strategy

Substation automation generated 39.45% of 2024 revenue as utilities specified fully digital secondary systems. The intelligent electronic devices market size allocated to power-quality monitoring and recording is accelerating at 9.26% CAGR through 2030 as sensitive electronic loads proliferate. Modern automation architectures collapse separate protection, control, and metering devices into centralized virtualization nodes, reducing panel footprints by 50% and simplifying version control.

High-resolution disturbance recorders feed synchrophasor algorithms that detect oscillatory instability seconds before blackout thresholds, empowering control rooms to shed noncritical load preemptively. Distribution automation leverages FLISR (fault location, isolation, service restoration) schemes using GOOSE messaging for sectionalizer coordination, cutting outage duration by 40% on feeder faults. Transmission automation emphasizes wide-area adaptive relaying backed by GPS time-sync precise to ±40 ns, enabling differential schemes across 300 km lines without communication channel compensation.

By Communication Protocol: IEC 61850 Remains De Facto, Cyber-Secure DNP3-SA Climbs

IEC 61850 controlled 52.64% of protocol deployments in 2024 because its object-oriented model ensures vendor-agnostic inter-operability. Utilities appreciate engineering efficiency, cutting configuration hours per relay by 40% through standardized SCL files. Expected cyber-threat escalation positions DNP3-SA for a 12.89% CAGR, attracting operators who favor lightweight stacks with deterministic performance and embedded encryption.

Legacy Modbus persists in cost-sensitive industrial skids, while Profibus supports process-plant determinism requirements. Multi-protocol gateways increasingly appear as micro-service containers, dynamically instantiating translation engines on white-box servers close to the substation edge to minimize latency.

By End-User Industry: Utilities Dominate While Hyperscale Data Centers Accelerate**

Utilities retained 48.23% share in 2024, reflecting regulatory mandates for reliable public-service delivery. The intelligent electronic devices market size servicing data centers is growing at 11.89% CAGR as hyperscalers expand AI clusters requiring 100% uptime. Operators deploy redundant IED-controlled static transfer switches that shift loads between dual utility feeds within 4 ms, protecting GPU farms from voltage sags that would crash training runs.

Industrial complexes adopt feeder management relays paired with IEC 61850 process bus to curtail downtime in continuous-process plants. Commercial campuses integrate advanced power meters with building-management systems, enabling curtailment strategies to avoid demand-charges. Transportation hubs pursue regenerative-braking energy recapture schemes that rely on rapid over-voltage protection to safeguard traction converters.

Geography Analysis

Asia-Pacific anchors global volume due to audacious grid-expansion programs, with China executing record-scale ultra-high-voltage AC/DC corridors and India fast-tracking digital substation packages under RDSS reform. Regional governments champion policies that fast-track right-of-way clearances and local-content incentives, compressing project timelines and spurring vendor localization. Utilities embed AI-based asset-health models that forecast breaker anomalies 60 days out, allocating capex toward predictive replacement rather than reactive outages.

The Middle East’s 11.65% CAGR through 2030 stems from sovereign diversification agendas prioritizing smart cities powered by renewables. Dubai’s AED 7 billion restoration system and Saudi Arabia’s 2.5 GW storage project demonstrate commitment to reliability and cybersecurity. HVDC interconnect schemes such as the proposed USD 4.8 billion undersea link between India and the Gulf align with GCC ambitions for continental power exchange, translating into sizeable IED packages rated for multi-terminal topologies.

North America modernizes 1970-era infrastructure, targeting wildfire mitigation in California and cyber-risk abatement nationwide under NERC-CIP-013. Utilities replace copper pilot wires with PRP-enabled fiber rings, integrating line-voltage distributed sensors. Europe focuses on flexibility to reach 65% renewables by 2030, leveraging wide-area adaptive schemes. South America invests in sub-transmission reinforcement for mining expansions in Chile and Peru, while Africa’s electrification corridors adopt standardized prefabricated substation skids pre-fitted with digital secondary systems to leapfrog legacy topologies.

Competitive Landscape

Competitive intensity is moderate, with top five suppliers collectively commanding roughly 45% share, signaling neither dominance nor fragmentation extremes. ABB, Siemens, and Schneider Electric sustain leadership through vertically integrated portfolios spanning sensors to cloud analytics. ABB’s SSC600 SW virtualizes as many as 30 protection functions on a single x86 platform, lowering lifecycle expense by 15% and enabling pay-as-you-grow licensing. Siemens advances software-defined substations using Container-as-a-Service, accelerating feature rollouts without hardware swap-outs.

Equipment makers are recalibrating supply-chains after copper prices peaked at USD 5.20 per lb in May 2024, triggering substitution toward fiber-optic architectures and aluminum bus bars. M&A activity chases cybersecurity competency; ABB’s 2025 purchase of Siemens’ China wiring-accessory arm expands low-voltage reach, while Cisco–Hitachi Energy partnership fuses IT routing heritage with OT domain expertise to craft edge-secure, deterministic substation backbones.

Regional specialists flourish in niche areas such as IEC 61850 test automation and solid-state breaker modules, leveraging agile R&D cycles to out-innovate conglomerates in specific application corridors. Patent filings on traveling-wave differential, SiC-based breaker topologies, and AI-driven disturbance analytics spotlight continued innovation momentum, positioning challengers for share capture when utilities tender feature-rich specifications.

Intelligent Electronic Devices Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

General Electric Company (GE Grid Solutions)

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hitachi Energy announced an additional USD 250 million investment to expand transformer capacity, a strategic hedge against global supply shortages and an opportunity to lock in long-term utility frame agreements amid accelerated grid build-outs.

- March 2025: ABB finalized the acquisition of Siemens’ wiring-accessories business in China, broadening its low-voltage product depth and embedding cross-selling channels for IED-centric digital-building solutions.

- December 2024: ABB committed USD 120 million to new U.S. IED-manufacturing lines, shortening lead times for stimulus-funded projects that carry domestic-content clauses.

- December 2024: Siemens unveiled SIMATIC ET 200SP e-Starter, integrating motor protection with PLC functionality, positioning the firm at the convergence of power and process automation

Global Intelligent Electronic Devices Market Report Scope

| Intelligent Relays |

| Digital Meters |

| Capacitor Bank Controllers |

| Feeder Protection IEDs |

| Voltage Regulators and Tap-changer Controllers |

| Substation Automation |

| Distribution Automation |

| Transmission Automation |

| Power Quality Monitoring and Recording |

| IEC 61850 |

| DNP3-SA |

| Modbus |

| Profibus |

| Other Protocols (GOOSE, MMS, IEC 60870-5-104) |

| Utilities |

| Industrial (Oil and Gas, Mining, Manufacturing) |

| Commercial and Institutional |

| Data Centers |

| Transportation (Rail, Airports, Ports) |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Device Type | Intelligent Relays | ||

| Digital Meters | |||

| Capacitor Bank Controllers | |||

| Feeder Protection IEDs | |||

| Voltage Regulators and Tap-changer Controllers | |||

| By Application | Substation Automation | ||

| Distribution Automation | |||

| Transmission Automation | |||

| Power Quality Monitoring and Recording | |||

| By Communication Protocol | IEC 61850 | ||

| DNP3-SA | |||

| Modbus | |||

| Profibus | |||

| Other Protocols (GOOSE, MMS, IEC 60870-5-104) | |||

| By End-user Industry | Utilities | ||

| Industrial (Oil and Gas, Mining, Manufacturing) | |||

| Commercial and Institutional | |||

| Data Centers | |||

| Transportation (Rail, Airports, Ports) | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the intelligent electronic devices market?

The market is worth USD 18.31 billion in 2025 and is projected to hit USD 24.64 billion by 2030.

Which region commands the largest revenue share?

Asia-Pacific leads with 33.38% share in 2024, driven by large-scale grid-modernization investments.

Which segment shows the fastest growth?

Capacitor bank controllers are forecast to grow at an 8.34% CAGR owing to the need for rapid reactive-power support in high-renewable grids.

Why is DNP3-SA adoption accelerating?

Utilities value DNP3-SA’s built-in encryption and authentication, which mitigate escalating cyber-threats targeting critical infrastructure.

How are data centers influencing the market?

Hyperscale operators deploy redundant, cyber-secure IED schemes to guarantee 100% uptime, driving an 11.89% CAGR in the data-center vertical.

What strategic moves dominate recent corporate activity?

Firms invest in domestic manufacturing to meet localization mandates, acquire software businesses for virtualization expertise, and partner on cyber-secure, fiber-optic networking solutions.

Page last updated on: