Embedded Controllers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

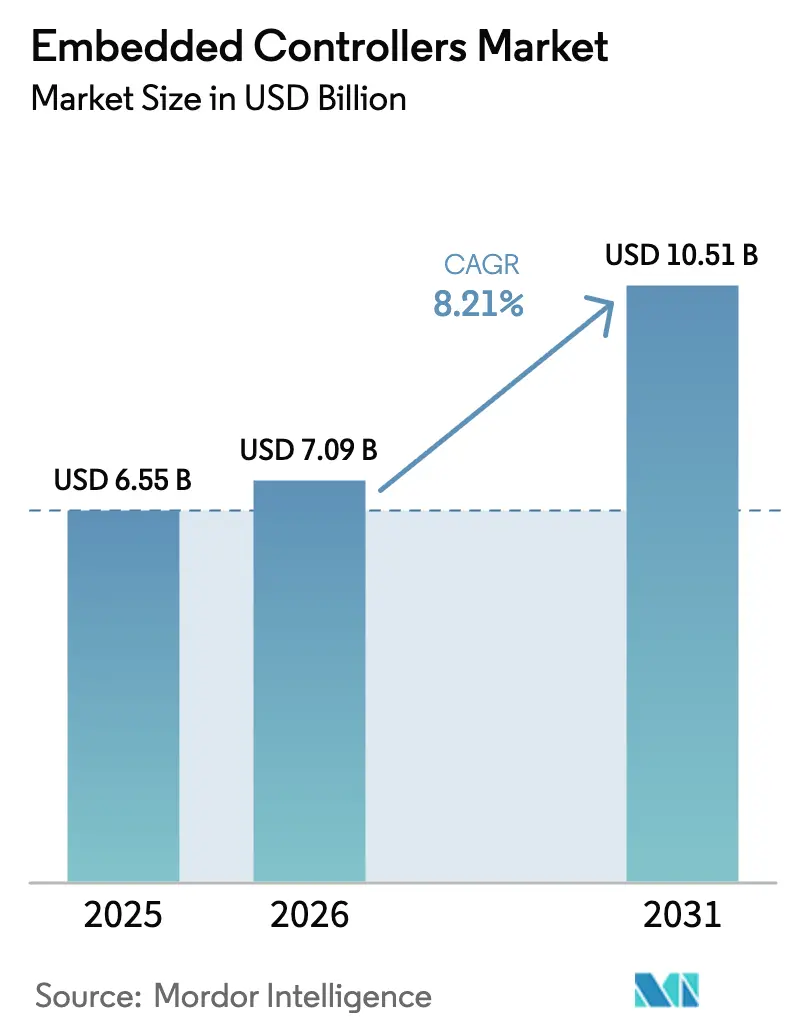

| Market Size (2026) | USD 7.09 Billion |

| Market Size (2031) | USD 10.51 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

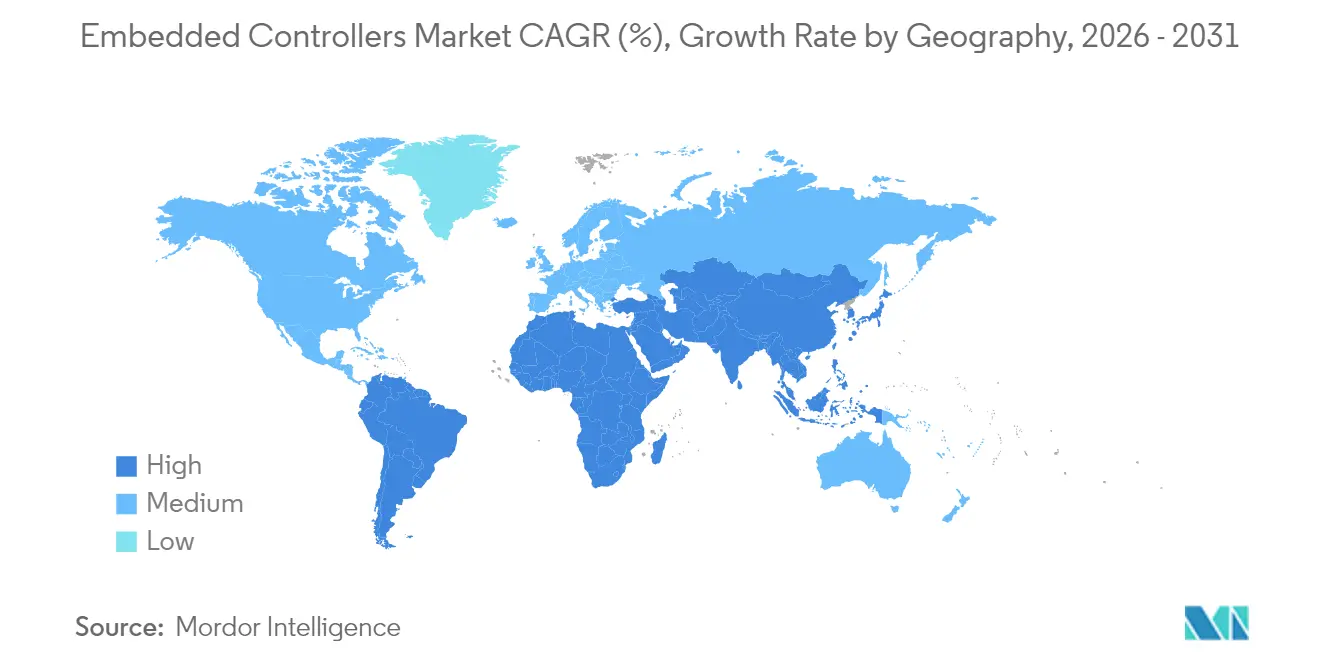

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

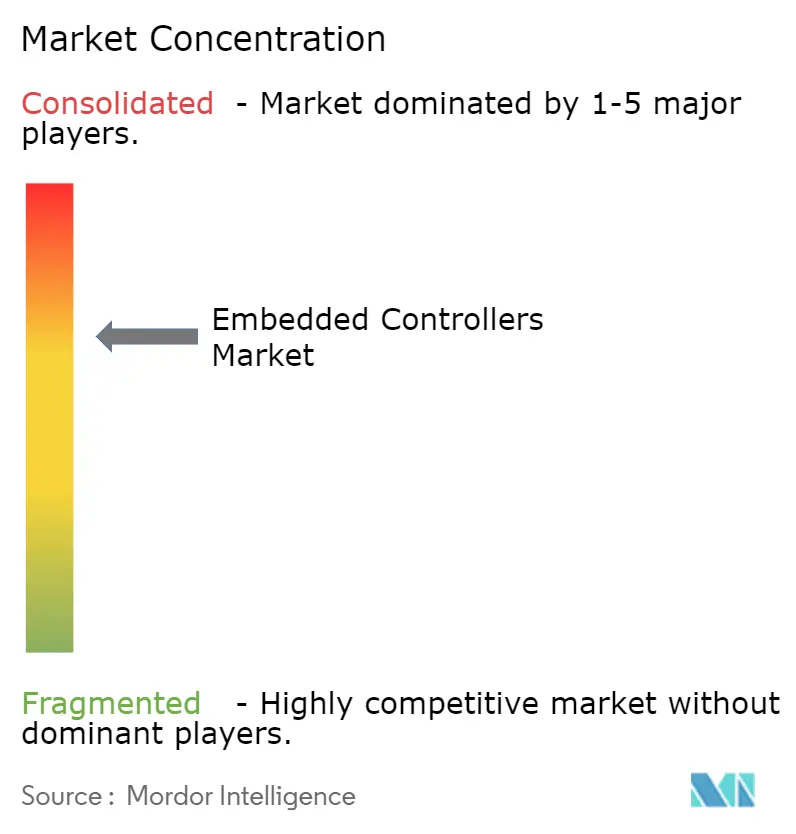

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded Controllers Market Analysis by Mordor Intelligence

The embedded controllers market size was valued at USD 6.55 billion in 2025 and estimated to grow from USD 7.09 billion in 2026 to reach USD 10.51 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031). Intensifying demand for intelligent subsystems in vehicles, factories, medical devices, and smart buildings anchors this upward curve. Supply chains are re-architecting around higher-flash, pin-compatible parts so OEMs can hedge against 28 nm capacity gaps while extending product life through secure over-the-air updates. Asia Pacific retains the lead with 45% revenue share because its contract electronics clusters, incentive packages, and policy-backed smart-factory rollouts keep local design win pipelines full. Meanwhile, regulatory initiatives such as Euro-7, U.S. OBD-II upgrades, and India’s Smart Meter National Programme are lifting average controller counts per system and boosting ASPs. Competitive focus is shifting away from raw clock speed races toward ecosystem depth, functional-safety credentials, cyber-resilience, and multi-decade supply guarantees that reassure risk-averse industrial and automotive customers.

Key Report Takeaways

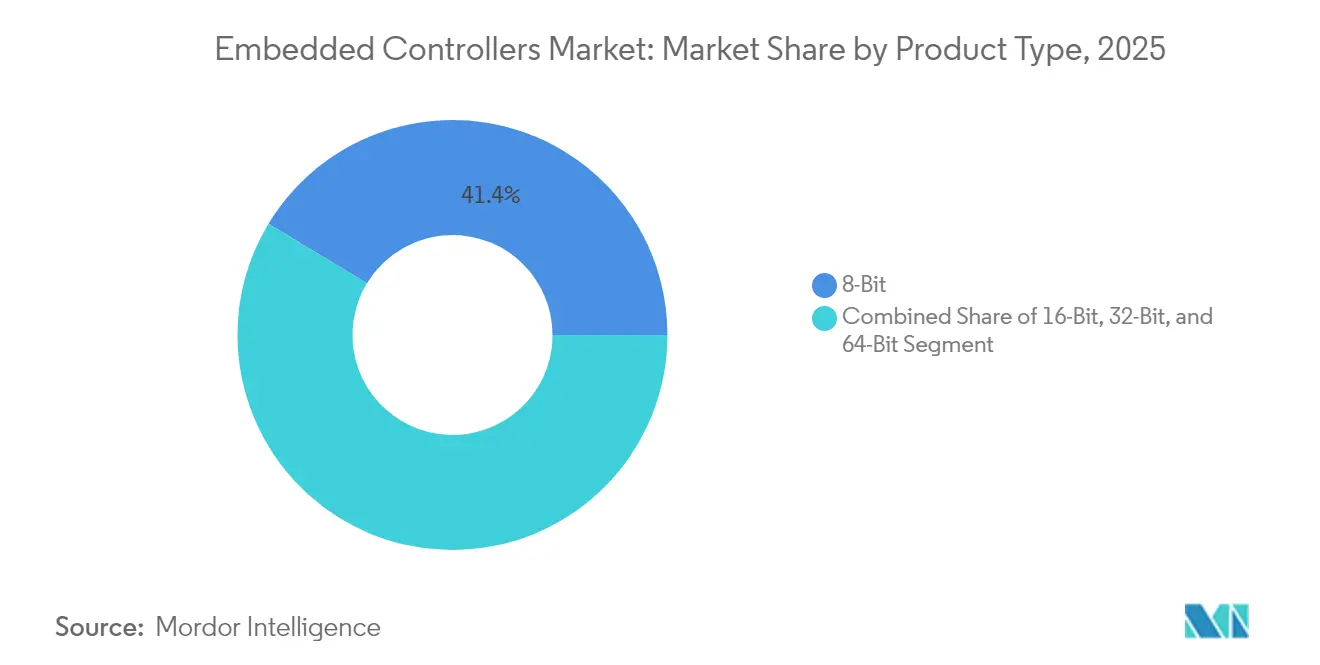

- By product type, 8-bit devices held 41.35% of the embedded controllers market share in 2025, while 32-bit microcontrollers are projected to advance at a 10.28% CAGR through 2031.

- By device architecture, Simple Programmable Logic Devices led with a 59.42% revenue share in 2025; Complex Programmable Logic Devices are expected to post the fastest growth across the forecast horizon.

- By application, automotive accounted for 29.60% of the embedded controllers market size in 2025, whereas healthcare applications are on track to grow at an 10.74% CAGR between 2026-2031.

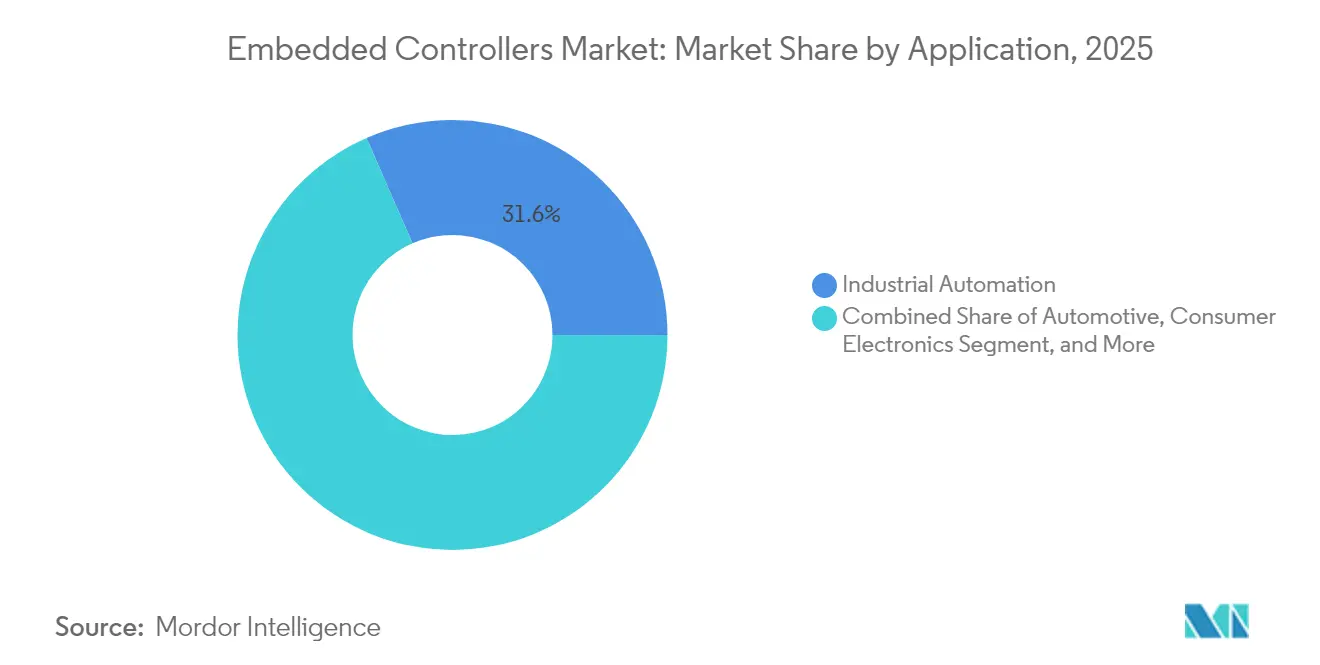

- By end-user industry, industrial automation captured 31.55% revenue in 2025, while smart home and building automation is poised to expand at a 11.52% CAGR through 2031.

- By geography, Asia Pacific commanded 44.20% of 2025 sales; the Middle East & Africa region is forecast to chart the quickest expansion through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Embedded Controllers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from 8-bit to 32-bit MCUs for ADAS & EV powertrains | +2.1% | Europe, North America | Medium term (2-4 years) |

| Edge-AI enabled industrial IoT nodes in smart factories | +1.8% | Asia Pacific | Medium term (2-4 years) |

| U.S. OBD-II / Euro-7 mandates elevating controller counts | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Secure ultra-low-power controllers in connected medical devices | +1.7% | North America | Medium term (2-4 years) |

| India’s Smart Meter National Programme | +0.9% | Asia Pacific (India) | Medium term (2-4 years) |

| OTA firmware services driving high-flash controllers | +0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift from 8-bit to 32-bit MCUs for ADAS & EV Powertrains

Automotive developers are migrating rapidly from 8-bit to 32-bit devices so they can close sensor-fusion loops, motor-control routines, and functional-safety diagnostics within tight real-time windows. A single RH850/U2B 32-bit controller now consolidates eight discrete blocks inside an E-Axle, cutting wiring mass, PCB area, and software integration overhead while still meeting ASIL-D targets.[1]Renesas Electronics Corporation, “Renesas Jointly Developed World-Class ‘8-in-1’ Proof of Concept for E-Axle Systems for Electric Vehicles,” renesas.com Euro-7’s real-time emissions monitoring accelerates this migration because higher code density and deterministic interrupt handling are mandatory. As platform engineers reuse that silicon across multiple vehicle lines, the embedded controllers market benefits through rising ASPs, deeper software toolchain stickiness, and multi-year supply agreements that smooth demand cycles.

Edge-AI Enabled Industrial IoT Nodes in Smart Factories

In Asia Pacific assembly plants, line operators rely on edge-deployed controllers that perform vision inference, vibration profiling, or anomaly scoring locally, bypassing unpredictable WAN links and trimming cloud traffic bills. OEMs preload quantized neural networks into on-chip flash, then push incremental model updates during planned maintenance windows. Predictive-maintenance programs that adopt these AI-enabled controllers report double-digit reductions in unplanned downtime and energy costs, creating a flywheel that funds further controller upgrades. Tool vendors now bundle no-code model translators with real-time operating systems, helping machine builders shorten commissioning cycles and strengthen ties to their controller suppliers.

U.S. OBD-II / Euro-7 Mandates Elevating Controller Counts Per Vehicle

Regulators want real-time emissions, knock, and particulate monitoring plus advanced diagnostics inside every new powertrain. Achieving that diagnostic granularity pushes ECU counts past 100 units in mainstream passenger cars, each hosting at least one microcontroller that speaks automotive Ethernet and CAN-FD.[2]Semiconductor Engineering, “Transforming Industrial IoT With Edge AI And AR,” semiengineering.com Tier 1 suppliers position domain controllers as gateway hubs that coordinate dozens of sensor nodes, raising silicon content and the embedded controllers market size captured per vehicle. Because homologation deadlines are firm, automakers lock multi-year wafer capacity at trusted fabs and pay premiums for parts pre-qualified to AEC-Q100 Grade 0.

Secure Ultra-Low-Power Controllers in Connected Medical Devices

U.S. and Canadian med-tech firms are standardizing on controllers that combine sub-10 µA deep-sleep current, hardware AES-128, true random number generators, and secure boot to safeguard patient data in wearables. Continuous-glucose monitors and ambulatory ECG patches transmit encrypted telemetry via Bluetooth LE to clinician dashboards, meeting HIPAA requirements while maximizing battery life.[3]Winbond Electronics, “W77Q Secure Flash Memory - TrustME,” winbond.com Hospital procurement teams now evaluate proof-of-penetration tests alongside IEC 60601 safety clearances, tilting awards toward suppliers with dedicated cyber-resiliency roadmaps. These dynamics amplify North American revenue for the embedded controllers market because hospitals buy certified silicon in concert with cloud analytics subscriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 28 nm MCU wafer shortages at Taiwanese foundries | −1.5% | Global, highest in Asia Pacific | Short term (≤ 2 years) |

| IEC-62443 cyber-certification costs for industrial OEMs | −0.7% | Europe | Medium term (2-4 years) |

| RISC-V vs ARM ecosystem bifurcation | −0.8% | Global | Medium term (2-4 years) |

| Thermal limits for 64-bit controllers in compact wearables | −0.3% | Global | Long term |

| Source: Mordor Intelligence | |||

28 nm MCU Wafer Shortages at Taiwanese Foundries

Persistent 28 nm bottlenecks have pushed average automotive-grade lead times past 40 weeks, forcing OEMs to redesign boards around thicker-geometry, pin-compatible devices or dual-source from higher-cost captive fabs. Geopolitical tensions magnify the risk because Taiwan produces 38.9% of worldwide semiconductors, making any disruption a global crisis. Component brokers report price spikes of 25% on high-rel i-grade MCUs, squeezing margins in cost-sensitive appliances. Until new capacity in Japan and the U.S. ramps, allocation policies will favor high-value medical and industrial lines, dampening short-run consumer demand within the embedded controllers market.

IEC-62443 Cyber-Certification Costs for Industrial OEMs

European machine builders now budget six-figure sums for audits, penetration tests, and lifecycle documentation to achieve IEC-62443-4-2 Security Level 2 certification.[4]Schneider Electric, “First in Industry to Obtain Higher Level Cybersecurity Certification for EcoStruxure IT DCIM Solutions,” se.com Compliance improves supply-chain trust but diverts engineering resources from feature innovation and stretches launch timelines. Smaller firms often license reference designs from larger vendors or exit high-security tenders entirely, limiting controller penetration in low-volume niches. Long term, wider availability of pre-certified software stacks should reduce per-unit integration costs, yet near-term adoption curves for advanced controllers in Europe remain muted.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 32-Bit MCUs Redefine Performance Boundaries

32-bit devices deliver the fastest expansion at a 10.28% CAGR, enabling embedded neural-network inference, secure communications, and deterministic motor control on a single die. Automotive domain controllers, factory robots, and medical infusion pumps increasingly specify dual-bank flash so engineers can stage fail-safe OTA updates without stopping mission-critical code. At the same time, 8-bit units preserve dominance in quantity because they power door-open sensors, appliance touch panels, and entry-level lighting nodes, keeping their 41.35% 2025 embedded controllers market share intact.

The 16-bit tier provides an intermediate upgrade path for legacy boards that lack the power budget or PCB real estate needed for 32-bit packages. Early 64-bit rollouts target premium wearables and augmented-reality devices, but designers throttle clock frequencies aggressively to contain heat per square millimeter. Suppliers counter these constraints with advanced power gating, DVFS frameworks, and ultra-thin package substrates that spread thermal load. As flash density rises and process geometries shrink below 28 nm, average controller ASPs trend higher, lifting the embedded controllers market size for performance-class products.

By Type: CPLD Flexibility Drives Industrial Innovation

Simple PLDs held a 59.42% revenue share in 2025 because they solve glue-logic tasks at pennies per I/O and guarantee nanosecond-level deterministic response. However, power tool manufacturers, telecom baseband designers, and avionics integrators now pivot toward CPLDs to embed multi-voltage translators, cryptographic MAC engines, and remote-field-upgrade logic within a single chip. Texas Instruments notes that one high-density CPLD can replace 94% of discrete gates on a legacy board, slashing PCB real estate by 90% and improving BOM reliability.

The embedded controllers market therefore sees rising demand for CPLDs that ship with hardened I/O banks and differential-pair support, allowing designers to bridge LVDS sensors to low-cost MCUs without timing skews. Meanwhile, high-end FPGAs stay parked in data-plane acceleration roles where full Linux or RT-Linux stacks drive complex protocols. Hybrid SoC roadmaps now position low-leakage CPLD blocks alongside Cortex-M cores, letting companies future-proof designs even when interface standards evolve late in the program.

By Application: Healthcare Innovations Accelerate Adoption

Healthcare secured the fastest growth trajectory, clocking an 10.74% CAGR, as remote patient monitoring, handheld ultrasound, and AI-driven diagnostics proliferate. Hardware security modules embedded inside MCUs enforce data integrity, bolstering HIPAA compliance while maintaining <10 µA deep-sleep currents for multi-day battery autonomy. The embedded controllers market size allocated to medical electronics therefore outstrips headline averages, supported by reimbursement shifts toward telehealth.

Automotive retains the largest revenue slice at 29.60% because the silicon content per vehicle climbs every model year: zone architectures, Ethernet backbones, and battery-management systems all demand deterministic control loops. Industrial automation sits between the two extremes, piloting real-time Ethernet, condition-monitoring gateways, and collaborative robot arms that pack multi-axis controllers. Consumer electronics sustains vast unit volumes for smart-home sensors and wearables, though price sensitivity tempers ASPs; yet OTA updatability is now mandatory, driving universal migration to high-flash die.

By End-User Industry: Smart Buildings Reshape Automation Landscape

Industrial automation kept its 31.55% share in 2025, leveraging predictive-maintenance algorithms, vision-guided pick-and-place, and closed-loop process controllers to convert sensor torrents into actionable insights. These deployments often blend safety-certified firmware with deterministic Ethernet, ensuring sub-millisecond jitter across PLC networks and cementing embedded controllers market leadership.

Smart home and building automation, however, steps into the growth spotlight with a 11.52% CAGR through 2031. AI-infused controllers dynamically orchestrate HVAC, lighting, and access control, shaving utility bills while responding to occupancy patterns in real time. Open-standard Thread and Matter stacks drive vendor interoperability, persuading builders to pre-install controller-rich hubs that integrate voice, video, and environmental sensing. Security remains paramount, so manufacturers embed on-chip key provisioning and secure-boot flows that survive 15-year building lifecycles. Automotive and healthcare sectors continue to chase electrification and remote-patient-care tailwinds, yet energy-efficient buildings extend the embedded controllers market addressable space into every apartment complex and commercial tower, promising high-margin retrofit cycles as sustainability regulations tighten.

Geography Analysis

Asia Pacific generated 44.20% of 2025 revenue because China’s EMS corridors, Japan’s precision-mechatronics prowess, and South Korea’s memory ecosystem collectively anchor vast economies of scale. Local governments subsidize 300 mm fab expansions and award tax breaks on advanced packaging lines, buffering domestic OEMs against global supply shocks. India’s plan to deploy 250 million smart meters layers a structurally durable demand stream for 16- and 32-bit RF-mesh controllers that withstand harsh outdoor environments.

North America remains a crucible for software-defined vehicles, digital-health breakthroughs, and Department of Defense modernization, all of which prioritize trustworthy silicon supply. Federal incentives have catalyzed greenfield fabs in Arizona and Texas that promise to shorten future logistics chains and temper geopolitical exposure. Healthcare OEMs cluster around Boston and Minneapolis, co-locating firmware teams and ASIC prototyping labs so they can integrate custom security enclaves into controllers for FDA-regulated devices.

Europe’s share leans heavily on automotive platforms, industrial automation, and stringent cyber-resilience statutes. IEC-62443 certification, Euro-7 emissions mandates, and the push toward carbon-neutral factories ensure that embedded controller deployments remain mission-critical. The Middle East & Africa and Latin America together deliver a smaller slice today, yet Gulf sovereign funds bankroll smart-city pilots and Brazilian auto assemblers localize electronics content, nudging controller design wins upward. Across every region, the embedded controllers market’s next inflection hinges on edge-AI toolchains that cut cloud dependence, accelerate response times, and comply with data-sovereignty laws

Competitive Landscape

The embedded controllers market is moderately concentrated: NXP Semiconductors, Microchip Technology, Renesas Electronics, STMicroelectronics, and Infineon Technologies together control just over 80% of worldwide sales. Infineon’s USD 2.5 billion acquisition of Marvell’s automotive-Ethernet unit adds protocol stacks vital for software-defined vehicles, deepening its footprint in zonal architecture design-wins. NXP expanded its edge-AI credentials by absorbing Kinara for USD 307 million, gaining neural processing cores that slot into industrial vision and driver-monitoring subsystems.

Renesas leverages its ownership of both MCUs and power devices to ship system-in-package E-Axe solutions that bundle inverter control, functional-safety accelerators, and cybersecurity firewall blocks. STMicroelectronics builds zonal-controller reference boards combining gigabit-switch fabrics and virtualization-ready firmware stacks, enabling OEMs to collapse ECU sprawl without risking functional-safety compliance. Microchip differentiates through certified long-term supply programs that guarantee availability for two decades, a decisive factor for aerospace and medical contracts.

White-space niches entice smaller players: ultra-low-leakage RISC-V cores target energy-harvesting sensors, while secure co-processors with quantum-safe cryptography address critical infrastructure upgrades. Distributors notice rising design-in activity around open-source toolchains that promise royalty-free instruction sets, yet entrenched ARM ecosystems still command superior silicon-support depth. As customers diversify sourcing strategies, strategic partnerships and multi-year wafer agreements replace spot-market buys, locking controller suppliers and OEMs into aligned product-roadmap cadences.

Embedded Controllers Industry Leaders

OMRON Corporation

ABB Ltd.

Honeywell International Inc.

Robert Bosch GmbH

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon Technologies acquired Marvell Technology’s automotive-Ethernet business for USD 2.5 billion, fortifying its software-defined vehicle portfolio.

- April 2025: Global Payments agreed to acquire Worldpay, scaling embedded-payment technologies that process USD 3.7 trillion annually.

- April 2025: Qorvo introduced ultra-wideband location, Matter connectivity, and battery-management solutions targeting industrial and automotive systems

- March 2025: Infineon rolled out AURIX™, TRAVEO™ T2G, and PSoC™ Automotive families with cost-effective dev-kits to expedite automotive and industrial designs.

- March 2025: NXP Semiconductors bought edge-AI pioneer Kinara for USD 307 million to embed NPUs across its controller range

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the embedded controllers market as all standalone microcontroller-class integrated circuits sold to original-equipment manufacturers for dedicated control tasks in electronic systems, spanning 8-bit, 16-bit, and 32-bit devices used in automotive ECUs, smart appliances, industrial IoT nodes, and similar edge hardware.

Scope Exclusion: board-level single-board computers, discrete general-purpose processors, and controllers bundled solely inside system-on-chip packages are not counted.

Segmentation Overview

- By Product Type

- 8-Bit

- 16-Bit

- 32-Bit

- 64-Bit

- By Type

- Simple Programmable Logic Devices (SPLD)

- Complex Programmable Logic Devices (CPLD)

- By Application

- Industrial Automation

- Automotive

- Consumer Electronics

- IT and Telecom

- Healthcare

- Smart Home and Building Automation

- Aerospace and Defense

- Others

- By End-User Industry

- OEMs

- Contract Manufacturers (EMS)

- System Integrators

- Semiconductor Foundries (Fabless/Fab-lite)

- By Geography

- North America

- Europe

- Asia-Pacific

- South America

- Middle East

- Africa

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed semiconductor marketing managers, Tier-1 auto-electronics architects across Asia and Europe, and contract manufacturers in Shenzhen and Guadalajara to validate unit shipment mixes, automotive fitment rates, and emerging RISC-V adoption. Structured surveys with smart-home appliance OEMs and industrial-automation integrators helped refine lifecycle ASP erosion curves and regional growth assumptions.

Desk Research

Our analysts first mapped shipment and value trends from tier-1 public sources such as UN Comtrade customs codes for microcontrollers, World Semiconductor Trade Statistics monthly billings, Germany's VDMA automation dashboards, and the US Energy Information Administration's smart-meter roll-out logs. Company 10-Ks, investor decks, and patent filings enriched understanding of pricing shifts and architecture roadmaps, while paid tools like D&B Hoovers and Dow Jones Factiva supplied firm-level revenue splits and news on fab capacity expansions. These sources illustrate demand pools and average selling prices that anchor the base year. The list above is illustrative, and many additional databases and trade journals were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down reconstruction begins with global microcontroller revenue reported by WSTS, which is then filtered by functional share attributable to embedded-controller workloads before geography and vertical splits are applied. Bottom-up spot checks, supplier roll-ups for key 32-bit families and sampled ASP × volume audits, bridge gaps and fine-tune totals. Model drivers include light-vehicle production, global IoT installed base, average controller content per appliance, fabrication node transitions influencing die cost, and regulatory safety mandates (e.g. Euro 7). Forecasts employ multivariate regression blended with scenario analysis to capture cyclical auto build rates and semiconductor inventory swings, producing a 2025-2030 CAGR aligned with consensus from our expert panel.

Data Validation & Update Cycle

Outputs pass variance checks against import data, fab utilization reports, and quarterly vendor disclosures. Senior reviewers challenge anomalies, and we refresh every twelve months, issuing interim amendments if supply shocks or regulation shifts materially alter the outlook.

Why Our Embedded Controllers Baseline Commands Reliability

Published figures often diverge because firms pick different product scopes, apply flat ASP curves, or stretch forecast horizons.

Key gap drivers include: Some studies fold SoC-embedded cores into totals, inflating value. Others assume linear ASP decline, ignoring 28 nm supply tightness that Mordor factors in. Refresh cadence varies; our annual update captures the latest EV platform ramps, whereas others still cite pre-chip-shortage data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.55 B (2025) | Mordor Intelligence | - |

| USD 8.03 B (2025) | Regional Consultancy A | Includes non-standalone SoC controllers and applies uniform 10 % ASP erosion |

| USD 6.00 B (2023) | Trade Journal B | Uses older base year and omits emerging RISC-V volumes |

| USD 7.12 B (2023) | Global Consultancy C | Relies on production capacity announcements without shipment verification |

These contrasts show how Mordor's measured scope, dual-path validation, and timely refreshes give decision-makers a balanced, transparent baseline they can track and replicate.

Key Questions Answered in the Report

What is the embedded controllers market size in 2026 and its growth outlook?

The market stands at USD 7.09 billion in 2026 and is projected to reach USD 10.51 billion by 2031, reflecting an 8.21% CAGR.

Which geographic region leads the embedded controllers market?

Asia Pacific accounts for 44.20% of global revenue, underpinned by its dense manufacturing base and accelerating smart-factory investments.

Why are 32-bit microcontrollers outpacing 8-bit adoption?

They supply the processing headroom needed for ADAS, electric-powertrain control, and edge-AI workloads, driving a 10.28% CAGR through 2031.

How do Euro-7 and OBD-II regulations influence controller demand?

Stricter real-time diagnostics and emissions-monitoring rules raise the number of controllers per vehicle, lifting semiconductor content and market revenue.

Which end-user segment is expanding fastest?

Smart home and building automation is growing at a 11.52% CAGR as AI-enabled controllers manage HVAC, lighting, and security for energy efficiency.

What are the main restraints facing the industry?

28 nm wafer shortages, rising IEC-62443 certification costs, and ecosystem uncertainty between ARM and RISC-V architectures are the key headwinds.

Page last updated on: