Consumer IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

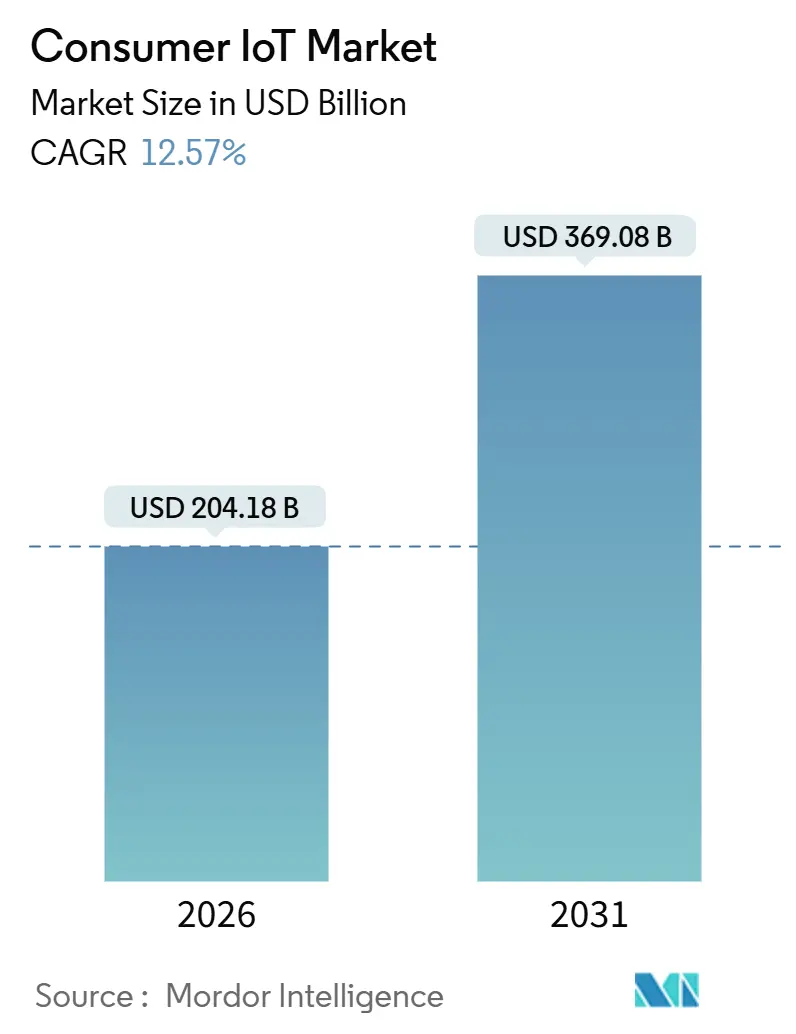

| Market Size (2026) | USD 204.18 Billion |

| Market Size (2031) | USD 369.08 Billion |

| Growth Rate (2026 - 2031) | 12.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Consumer IoT Market Analysis by Mordor Intelligence

The Consumer IoT market stood at USD 204.18 billion in 2026 and is projected to reach USD 369.08 billion by 2031, reflecting a 12.57% CAGR across the period and confirming a strong upward trajectory in both current market size and future value. Growth is fueled by satellite-connectivity integrations that push device coverage beyond terrestrial networks, regulatory pressure for energy efficiency that embeds smart devices into building codes, and the arrival of Matter 1.5 which at last introduces cross-brand camera interoperability. Competitive positioning has shifted toward platform control, with Amazon, Google, Apple and Samsung embedding on-device large-language-model inference that locks users into branded ecosystems. Hardware commoditization, falling sensor prices below USD 0.50, and ISO-based reference architectures have tilted value capture toward software and services, while chip-foundry expansions in Arizona and Texas improve supply resilience. Insurance-linked discounts, 5G and LPWAN rollouts, and energy-price volatility are additional catalysts that expand adoption in homes, wearables, and connected vehicles.

Key Report Takeaways

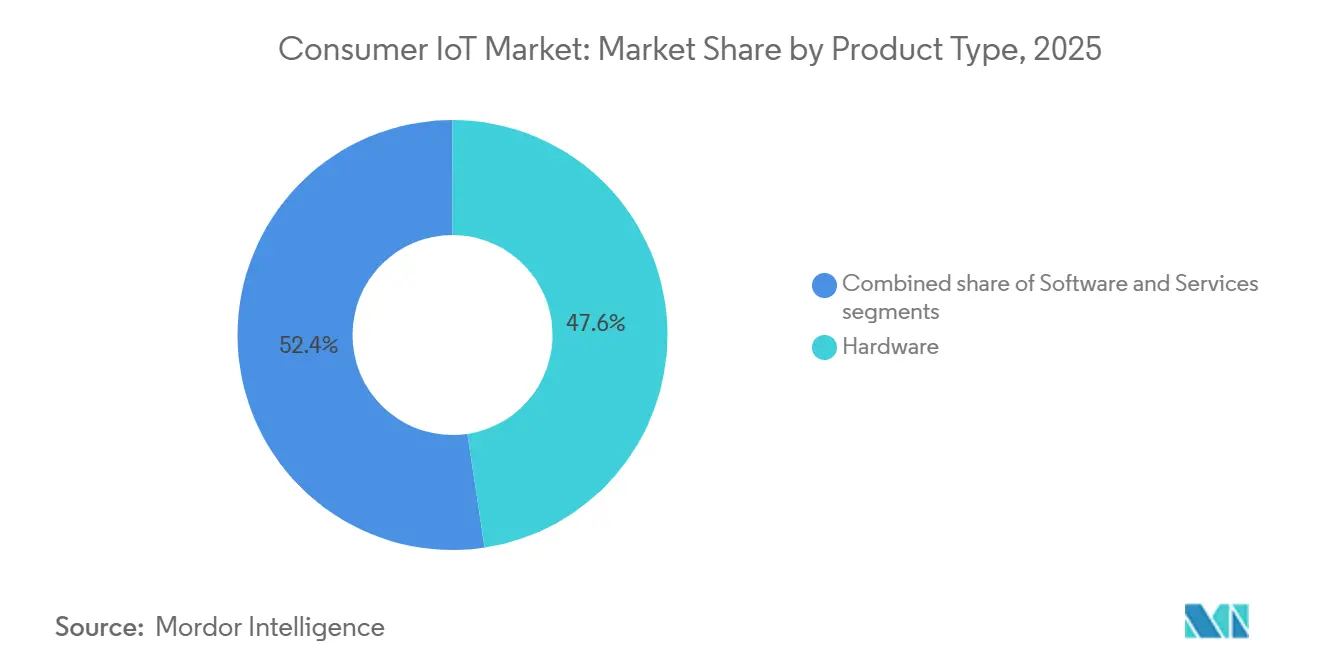

- By product type, Hardware led with 47.62% revenue share in 2025, while Services are advancing at a 13.21% CAGR through 2031.

- By connectivity technology, Wi-Fi commanded 43.44% of deployments in 2025, whereas Ultra-Wideband is forecast to register a 13.62% CAGR through 2031.

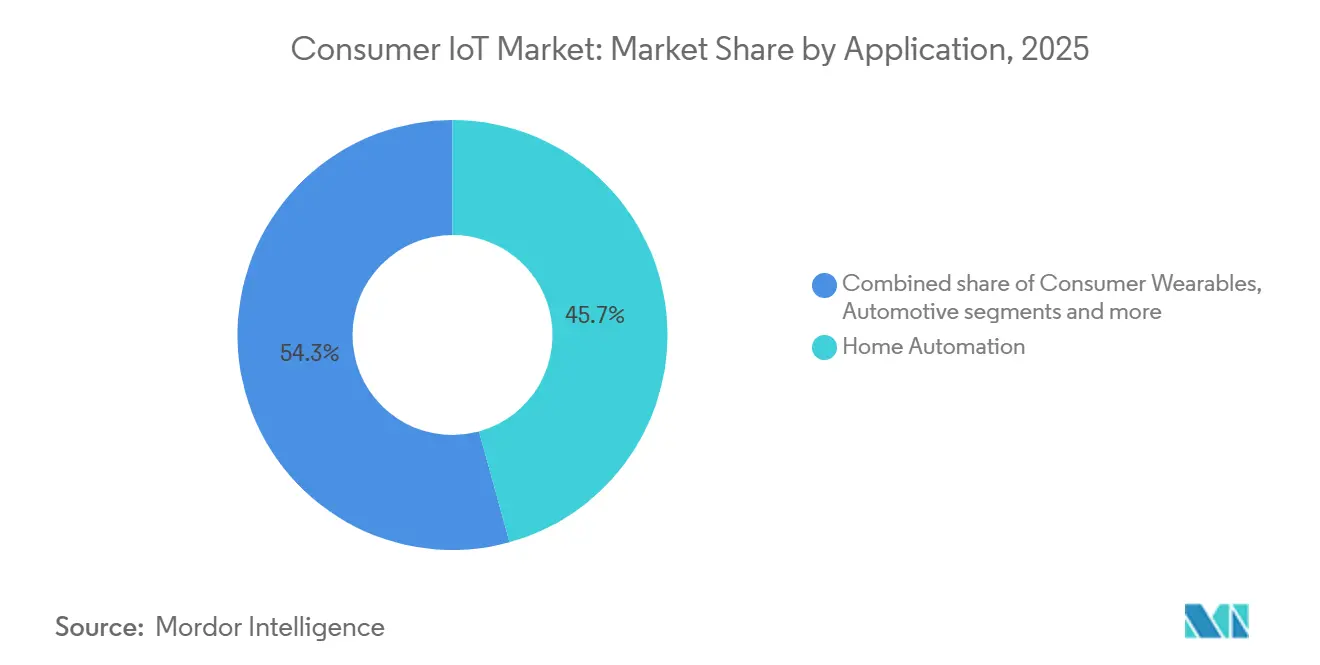

- By application, Home Automation accounted for 45.73% of revenue in 2025, while Healthcare Devices are projected to rise at a 13.93% CAGR through 2031.

- By distribution channel, Online sales captured 56.91% share in 2025 and are poised to increase at a 13.08% CAGR through 2031.

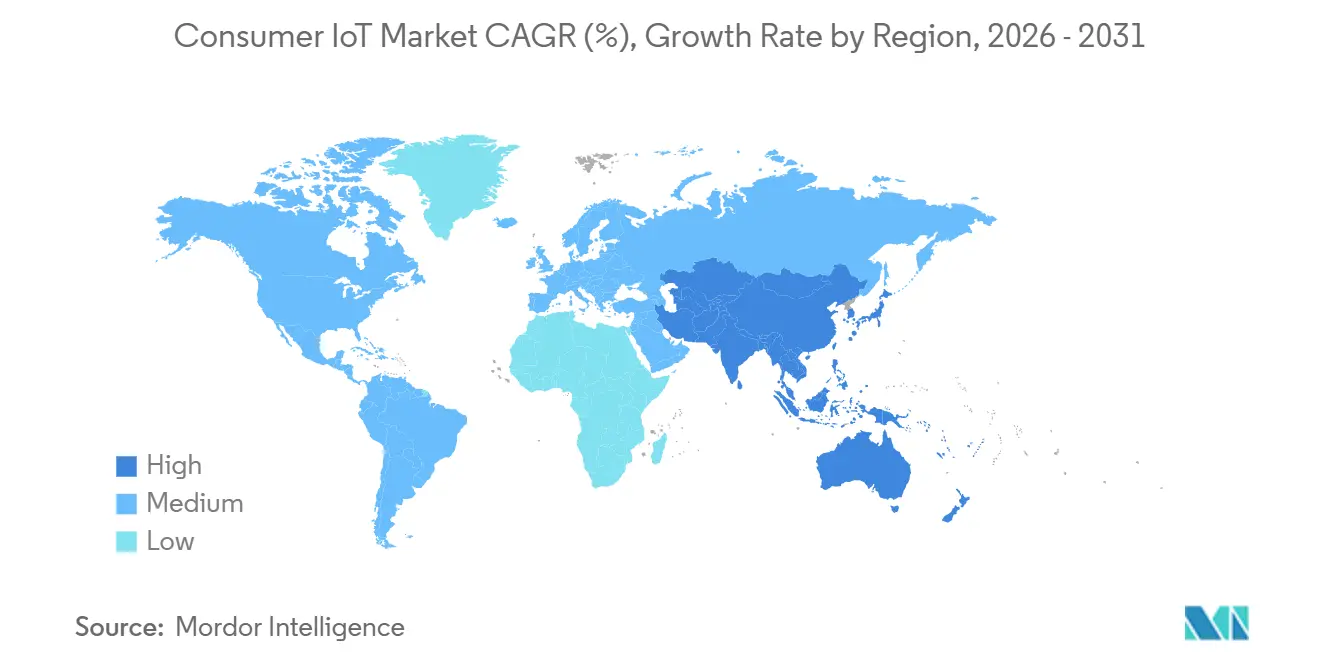

- By geography, North America held 37.89% of global revenue in 2025, while Asia-Pacific is set to expand at a 14.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Connected Consumer Devices and Falling Sensor Prices | +2.1% | Global, with APAC core manufacturing hubs | Medium term (2-4 years) |

| Roll-out of 5G and LPWAN Connectivity | +2.4% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Rapid Smart-Home Ecosystem Adoption | +2.3% | North America and EU lead, APAC catching up | Medium term (2-4 years) |

| AI-Driven Voice-Assistant Integration | +1.8% | Global, concentrated in English and Mandarin markets | Short term (≤ 2 years) |

| Insurance-Linked Incentives for Risk-Mitigating IoT Devices | +1.2% | North America, emerging in EU | Long term (≥ 4 years) |

| Energy-Price-Driven Demand for Smart Home Energy Management | +1.9% | EU regulatory push, North America incentive-driven | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Connected Device Proliferation and Falling Sensor Prices

The number of Thread-certified products exceeded 1,100 by late 2025, pushing unit costs for motion, temperature, and humidity sensors below USD 0.50, which supports sub-USD 20 retail prices for basic smart plugs and door sensors. Foundry ramps by TSMC, Intel and Samsung in Arizona and Texas collectively added more than 1 million wafer starts per year, stabilizing microcontroller lead times and widening supply access. Bosch Sensortec’s BHI360 and BHI380 sensor hubs integrate on-chip machine learning that reduces external processor load and lengthens battery life in wearables and nodes. These cost efficiencies, coupled with ISO/IEC 30141 reference architectures, reduce engineering overhead and reposition differentiation toward software-based services.

Roll-out of 5G and LPWAN Connectivity

GSMA counted 1.6 billion 5G connections globally by early 2024, while Ericsson projected 60% population coverage by the end of 2025, delivering sub-10 millisecond latency necessary for real-time health monitoring and immersive applications.[1]GSMA, "5G Connection and Statistics," gsma.comSkylo partnerships with Qualcomm, Samsung, Google, and Garmin embed satellite messaging into premium smartphones and wearables, closing terrestrial gaps and supporting emergency communication. Orange Europe added satellite SMS services in November 2025 for maritime and alpine regions.[2]Orange, “Satellite SMS Services Launch,” orange.com Semtech’s HL78 LoRa Edge module combines LPWAN with GNSS positioning to extend battery life beyond five years in asset trackers.[3]Semtech, “HL78 LoRa Edge Module Release,” semtech.com Thread 1.4 introduced sleepy end devices that cut energy draw by up to 40% compared with always-on Wi-Fi, benefiting rural and low-power deployments.

Rapid Smart-Home Ecosystem Adoption

Eurostat data showed that 71% of European internet users operated connected devices in 2024, and 63% used at least one smart-home product, surpassing 59% a decade earlier. Samsung became the first to support Matter 1.5 cameras in December 2025, enabling encrypted video across Apple, Google and Amazon ecosystems. Despite this, a Japanese survey revealed ownership rates of only 4.7% for robot vacuums and 1.2% for smart locks, with 41% of respondents citing no perceived need, underscoring cultural and regulatory factors that shape adoption. Berg Insight estimated 4.5 million home-energy-management systems in place by end-2024 and forecast a 22.3% CAGR to 12.3 million by 2029, driven by the EU Energy Performance of Buildings Directive. GDPR and local data-residency rules continue to influence vendor roadmaps and consumer confidence.

AI-Driven Voice-Assistant Integration

Amazon unveiled Alexa+ in September 2025, integrating generative-AI responses and proactive suggestions, while Google introduced Gemini for Home in October 2025, embedding large-language-model inference directly into Nest devices. Samsung partnered with Google to equip the Ballie companion robot with similar AI capabilities, eliminating wake-word friction and driving natural-language control. A Verizon survey found that 68% of U.S. smart-home owners issued voice commands daily in October 2025, eclipsing mobile-app usage for primary control. The forthcoming EU AI Act classifies certain voice-assistant functions as high-risk, compelling transparency and compliance that favor large incumbents with established legal resources.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cyber-Security Concerns | -1.6% | EU enforcement lead, global spillover | Short term (≤ 2 years) |

| Inter-operability Fragmentation Despite Matter Roll-out | -1.3% | Global, acute in APAC and emerging markets | Medium term (2-4 years) |

| Chip-Supply Volatility and Pricing Pressure | -0.9% | Global, with APAC manufacturing dependencies | Short term (≤ 2 years) |

| E-Waste, Right-to-Repair and Eco-Design Regulation Impact | -0.7% | EU regulatory core, spreading to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

The European Data Protection Board has imposed EUR 4.5 billion (USD 5.1 billion) in GDPR fines since 2018, including Meta’s EUR 1.2 billion (USD 1.36 billion) penalty in May 2023, prompting IoT vendors to localize data storage and refine permission frameworks. Eurostat recorded 7% of EU citizens citing security fears as a barrier to adoption in 2024, rising to 12% in lower-income households. The FDA’s TEMPO pilot, launched December 2025, obligates medical-device applicants to submit cybersecurity threat models and software bills of materials. Smaller vendors face disproportionate compliance costs, accelerating consolidation around platform operators that can absorb legal overhead.

Interoperability Fragmentation Despite Matter Roll-out

Although the Connectivity Standards Alliance had certified more than 1,100 Matter products by late 2025, Samsung’s claim of first-to-market support for Matter 1.5 cameras exposed multi-year gaps in the standard. Proprietary UWB implementations by Apple and Samsung remain partially siloed, limiting cross-brand digital-key use. Legacy Zigbee and Z-Wave installations demand costly bridge devices, adding latency and failure points. Fragmentation deters cost-sensitive buyers in Asia-Pacific and emerging markets, where local brands such as Xiaomi and Huawei maintain their own ecosystems. Policy incentives that subsidize installers or certify device interoperability are still nascent, prolonging consumer hesitation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Monetize the Installed Hardware Base

Services are expanding at a 13.21% CAGR from 2026 to 2031 as vendors pivot from one-time hardware sales to subscription bundles that include firmware updates, predictive maintenance, and usage analytics. The Consumer IoT market size for Services is rising faster than hardware even though Hardware maintained 47.62% Consumer IoT market share in 2025, indicating that recurring revenue is eclipsing upfront margin compression. Amazon’s premium Alexa+ tier and Google’s Gemini-based cloud storage for Nest cameras illustrate how platforms convert hardware owners into long-lived subscribers. EU energy-efficiency mandates drive dashboard software that aggregates consumption data and triggers automated load shedding, as seen in Schneider Electric’s Wiser Energy platform.

Hardware shipment volumes remain critical because device proliferation anchors any attach rate for services. Cost reductions from Bosch Sensortec’s integrated sensor hubs and wafer-capacity additions by U.S. foundries have kept entry-level prices low, yet commoditization squeezes margins. ISO/IEC 30141 accelerates reference-architecture alignment, lowering integration costs and channeling profit pools toward analytics, cloud hosting, and AI features that software and service providers supply.

By Connectivity Technology: Ultra-Wideband Challenges Wi-Fi Dominance

Wi-Fi accounted for 43.44% of deployments in 2025 due to legacy router bases and multi-gigabit upgrades to Wi-Fi 7. However, Ultra-Wideband is projected to post a 13.62% CAGR to 2031, scaling upward from automotive key fobs to smartphones that offer centimeter-level positioning. The Consumer IoT market size for UWB-enabled devices is accelerating particularly in digital-key, asset-tracking, and spatial-audio scenarios, and gains are eroding the once unassailable presence of Wi-Fi in indoor navigation. FCC Part 15 and ETSI compliance requirements set emission limits that vendors must address early in product design, but global members of the FiRa Consortium are pooling reference designs that lower certification hurdles.

Bluetooth and BLE sustain huge unit volumes in wearables and headphones, though always-on power draw constrains battery-sensitive endpoints. Low-power mesh standards such as Thread benefit sensors and door contacts, especially since Thread 1.4 introduced sleepy end devices that extend battery life markedly. Cellular NB-IoT and LTE-M serve mobility use cases, while Skylo’s satellite overlay pushes messaging beyond terrestrial coverage, expanding adoption in remote security devices and adventure wearables.

By Application: Healthcare Devices Outpace Consumer Electronics

Home Automation held 45.73% revenue in 2025, underlining thermostats, lighting, and security cameras as mature categories. Healthcare Devices are forecast to achieve a 13.93% CAGR through 2031, and this growth elevates their contribution to the overall Consumer IoT market size as FDA clearances pour in. Continuous glucose monitors from Dexcom, cuffless blood-pressure sensors from Aktiia, and ECG features from Whoop demonstrate an evolving pipeline in regulated wearables. The Consumer IoT market share for Healthcare Devices therefore widens as payers reimburse clinically validated gadgets, reinforcing adoption beyond fitness enthusiasts.

Consumer Wearables join the healthcare arc by adding satellite messaging for wilderness safety, while Consumer Electronics evolves through generative-AI embedded appliances such as Samsung’s Bespoke AI line. Automotive connectivity also rises, with Mercedes-Benz, BMW and Stellantis developing in-house operating systems that support over-the-air updates and third-party apps. Niche categories like pet trackers adopt UWB for precise geofencing, showing that even small segments follow the broader shift toward high-accuracy positioning.

By Distribution Channel: Direct-to-Consumer Models Dominate Online

Online channels captured 56.91% of revenue in 2025 and are tracking a 13.08% CAGR through 2031 as consumers value direct-to-consumer bundles that include firmware provisioning and subscription add-ons. E-commerce penetration, measured at 16.4% of U.S. retail sales in Q3 2025, underpins this shift as electronics and appliances top growth leaderboards. Detailed product reviews, installation videos, and one-click ecosystem bundling lower the perceived complexity of the Consumer IoT market, facilitating broader reach.

Brick-and-mortar stores still serve demonstrations and immediate fulfillment, yet margin compression pushes retailers to blend online ordering with in-store pickup. Samsung’s dual strategy for Bespoke AI appliances exemplifies omnichannel balancing. Regulatory obligations such as the EU Digital Services Act heighten compliance costs for smaller online marketplaces, consolidating volume with platforms that can maintain transparent return policies and data-privacy disclosures.

Geography Analysis

North America contributed 37.89% of global revenue in 2025, supported by insurance discounts that reach 15% for smart-home installations and by federal tax credits for smart thermostats under the U.S. Inflation Reduction Act. State mandates such as California’s Title 24 require load-management controls in new homes, further embedding intelligent devices. Canadian utilities mirror these incentives through rebates and time-of-use tariffs, while Mexico’s nearshoring boom and cross-border e-commerce invite mid-income households into the Consumer IoT market.

Asia-Pacific is projected to expand at a 14.11% CAGR to 2031, the fastest regional pace. Xiaomi shipped more than 100 million smart-home devices in 2024, using aggressive pricing to lower entry barriers in China. India’s Digital India program subsidizes broadband and nurtures local assembly lines, delivering wider access to connected devices. South Korea’s 5G coverage surpasses 95%, fostering rapid uptake of AI-enhanced appliances from domestic champions Samsung and LG. Japan exhibits high awareness but low ownership, with interoperability and perceived value hindering rollouts despite the spread of Matter certification.

Europe’s trajectory ties directly to the Energy Efficiency Directive 2023/1791, which mandates an 11.7% consumption reduction by 2030 and effectively requires smart meters in all new buildings. Right-to-Repair legislation adopted in 2024 extends device lifespans, encouraging software-update revenue more than replacement hardware sales. Nordic countries benefit from near-universal broadband and eco-conscious consumers, whereas Italy and Spain accelerate meter deployment through national energy plans. GDPR and forthcoming AI regulation sustain compliance demands that favor incumbents.

South America remains nascent but benefits from expanding urban middle classes in Brazil and Argentina. Middle East and Africa rely on sovereign smart-city megaprojects; the UAE allocated AED 11 billion (USD 3 billion) for 1,000 technology installations by 2031, including 600,000 smart meters already active in Abu Dhabi and Dubai. Saudi Arabia’s Vision 2030 and South Africa’s grid-modernization initiatives also spur localized demand. World Bank data shows Gulf Cooperation Council members enjoy more than 90% 5G coverage and mobile broadband speeds above 100 Mbps, underpinning future adoption.

Regulatory Landscape

Consumer IoT regulation is tightening around cybersecurity, privacy, and product safety, with the EU and key Anglosphere markets setting the compliance pace. The EU Cyber Resilience Act (Regulation (EU) 2024/2847) entered into force on December 10, 2024, introducing mandatory security-by-design obligations for products with digital elements, with Member States required to designate notifying authorities for conformity assessment bodies by June 11, 2026. Reporting obligations for actively exploited vulnerabilities and severe incidents apply from September 11, 2026, creating near-term requirements for vulnerability intake, triage, and disclosure processes ahead of the CRA's full application date of December 11, 2027.

In the United States, the FCC adopted a voluntary cybersecurity labeling program (Cyber Trust Mark) for wireless consumer IoT products, while NIST's consumer IoT cybersecurity work informs baseline expectations around device capabilities and disclosure. In April 2026, the FCC named the ioXt Alliance as Lead Administrator for the Cyber Trust Mark program on April 13, 2026, which puts more emphasis on vendor certification readiness and evidence packages across device security and software update practices. In parallel, regimes such as the UK PSTI (effective April 2024) and related privacy requirements increase documentation and assurance needs for connectable products sold into multiple jurisdictions.

Value Chain Analysis

The consumer IoT value chain starts with silicon and sensor suppliers (microcontrollers, connectivity chipsets, MEMS sensors and modules), then moves through device OEMs and ODMs, and appliance makers that integrate firmware, reference architectures (for example, ISO/IEC 30141-aligned designs), and connectivity stacks (Wi-Fi, Bluetooth/BLE, Thread, cellular and satellite overlays). As hardware prices compress, platform and ecosystem layers (voice assistants, smart-home hubs, device-management services, cloud storage, and identity and account systems) increasingly capture value, with ecosystem owners such as Amazon, Google, Apple and Samsung monetizing installed bases through assistants and subscriptions.

Downstream, distribution has shifted toward online direct-to-consumer and marketplace channels, while installers and utility or insurance-linked programs influence adoption in energy management and home security. Compliance and assurance now sit across the chain, not just at the endpoint: the UK Information Commissioner's Office published final guidance in June 2026 for consumer IoT products and services, clarifying how UK GDPR and PECR apply across device, app, and associated online services. In Europe, multi-layered requirements (including CRA cybersecurity obligations and broader safety and liability frameworks) raise coordination burden among hardware vendors, firmware contractors, app developers, and cloud providers, making end-to-end integration ownership and supply-chain documentation a larger determinant of time-to-market.

Competitive Landscape

Market power clusters around ecosystem owners Apple, Amazon, Google, Samsung and Microsoft, whose proprietary assistants, app stores, and cloud services generate high switching costs. Amazon’s Alexa+ and Google’s Gemini for Home embed generative-AI features that harvest usage data while driving subscription revenue. Samsung’s Ballie robot links hardware with cloud intelligence to sustain user engagement. Matter certification surpassed 1,100 products by late 2025, but gaps surrounding cameras and energy devices allow first movers to extract interoperability premiums.

Satellite connectivity is an emerging white space. Skylo’s partnerships with Qualcomm, Samsung, Google and Garmin bring non-terrestrial messaging to mainstream devices, expanding the Consumer IoT market into remote, maritime and disaster-preparedness zones. Healthcare wearables carry regulatory hurdles yet promise high margins; FDA clearances in 2025 validate paths for smaller entrants. Xiaomi and Huawei pursue vertical integration in Asia, bundling routers, smartphones and appliances within closed ecosystems that circumvent Western cloud dependencies.

Technology differentiation is shifting to on-device AI and energy efficiency. Bosch Sensortec’s sensor hubs offload computation from higher-power processors, while Schneider Electric’s Wiser platform optimizes solar self-consumption at the circuit level. The upcoming EU AI Act will boost compliance budgets and likely consolidate share among incumbents. Patent filings in Ultra-Wideband positioning and satellite protocols underscore long-term bets on secure digital keys and ultra-precise indoor navigation.

Consumer IoT Industry Leaders

-

Apple Inc.

-

Amazon.com Inc.

-

Samsung Electronics Co. Ltd.

-

Alphabet Inc. (Google)

-

Huawei Technologies Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Interoperability upgrades create a clear whitespace in multi-ecosystem smart homes, where consumers want shared device access across platforms without replacing existing hardware. The Connectivity Standards Alliance released Matter 1.6 in June 2026, adding Joint Fabric for multi-ecosystem sharing and NFC-based commissioning, which targets setup friction and cross-platform household management across Apple, Amazon, Google and Samsung environments. This supports opportunities for device makers and service providers to package cross-ecosystem onboarding, household sharing, and managed-support bundles, especially for cameras, thermostats, and energy devices where interoperability gaps have been most visible.

Security and compliance services are becoming an addressable layer as regulations and labeling programs mature and move from principles to operational requirements. The EU Cyber Resilience Act makes manufacturer vulnerability reporting obligations active from September 11, 2026, while the FCC's Cyber Trust Mark program advanced its administration by naming the ioXt Alliance as Lead Administrator in April 2026, and the CSA introduced Product Security 1.1 in June 2026 to broaden evaluation from devices to complete IoT systems (including apps, gateways, and remote processes). These developments support opportunities for vendors that can provide system-level security evidence (SBOMs, update policies, vulnerability handling) and for platforms that can standardize compliance workflows across consumer devices, companion apps, and cloud services.

Recent Industry Developments

- July 2026: Google opened pre-orders for a new Google Home Speaker positioned as its first audio device designed for Gemini for Home, with availability starting June 25, 2026. The pre-order push ties generative AI interactions to dedicated in-home hardware, strengthening the assistant-led control layer that drives ongoing services and device attach in smart homes.

- December 2025: Samsung SmartThings added support for Matter 1.5 cameras, enabling encrypted cross-brand video interoperability across major ecosystems. Camera interoperability reduced one of the most visible fragmentation points in smart-home setups, raising the value of standards-compliant devices while increasing competitive pressure on proprietary camera platforms.

- May 2024: The European Data Protection Board continued tightening enforcement under GDPR, with cumulative fines reaching EUR 4.5 billion since 2018 and a major penalty issued to Meta in May 2023 serving as a prominent precedent. This enforcement backdrop pushed IoT vendors to prioritize privacy-by-design, data minimization, and regional data-handling choices that influence device features and cloud-service architectures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the consumer IoT market is defined as the annual revenue generated from consumer-owned connected devices and the related consumer-facing services that enable monitoring, control, automation, or convenience in everyday use.

Scope exclusions: We exclude industrial and enterprise IoT platforms, purely B2B M2M modules, and stand-alone data monetization revenues that are not tied to consumer device or service spending.

Segmentation Overview

-

By Product Type

- Hardware

- Software

- Services

-

By Connectivity Technology

- Wi-Fi

- Bluetooth / BLE

- Zigbee / Z-Wave / Thread

- Cellular

- Ultra-Wideband (UWB)

-

By Application

- Home Automation

- Consumer Wearables

- Consumer Electronics

- Healthcare Devices

- Automotive

- Other Applications

-

By Distribution Channel

- Online

- Offline

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what qualifies as consumer IoT spending, and to collect common reference points on adoption, connectivity, and device shipment patterns. We used public and official sources such as ITU connectivity indicators, OECD digital economy statistics, World Bank macro series, US FCC materials on broadband availability, and Eurostat ICT usage datasets, along with relevant peer reviewed journals on connected-device adoption behavior.

To keep the inputs practical, we also reviewed company filings, investor decks, and association publications that describe category growth, average pricing moves, and service attach rates for consumer devices. Where extra structure was required, paid subscriptions were used only for company financials and intelligence, news and financials tracking, and patent databases to cross-check product cycles. The desk sources listed here are illustrative, and we used additional public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what actually gets paid for, since connected-device markets can be overstated when revenues are defined differently. We spoke with a mix of device ecosystem participants, channel stakeholders, and industry specialists across APAC, EMEA, and the Americas to confirm category boundaries, realistic ASP ranges, service attachment, and the timing of major refresh cycles. We then used these checks to finalize assumptions that were not clear in public sources.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | APAC: 41% |

| Mid tier: 50% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 21% | Managers: 42% | Americas: 22% |

Market-Sizing & Forecasting

The core model uses a top-down approach, where consumer connected-device demand is reconstructed from household and individual adoption signals, device shipment trends, and connectivity readiness. Those demand pools are converted into revenue using category-level pricing and service attachment assumptions. We also cross-check results with selective bottom-up approximations, including sampled ASP times unit volumes for major device groups, plus channel checks on subscription penetration, which helps correct totals when a single input series appears noisy.

Key model inputs include smart home and wearable device shipment direction, broadband and smartphone penetration as a readiness filter, average selling price progression by device type, consumer service attach rates (security monitoring, cloud features, and extended support), and replacement cycle timing that shifts with new standards and product releases. For forecasting, scenario analysis is used to reflect how adoption and pricing can move under different macro conditions and connectivity rollouts, then narrowed using the consensus ranges heard in primary conversations. When bottom-up data is incomplete, gaps are handled by using proxy categories with similar pricing and adoption curves, scaled back to align with validated demand indicators.

Data Validation & Update Cycle

Outputs are checked against independent signals, so the estimate is not driven by a single data stream. We compare mismatches across device volumes, pricing, and implied household penetration. When a variance is found, the underlying assumption is reviewed, then a second pass by another analyst checks that the correction is consistent across regions and years.

The work is refreshed annually, with interim adjustments when a material event changes device pricing, connectivity economics, or consumer purchasing behavior. If an anomaly persists after desk checks, respondents are re-contacted to re-validate the specific variable causing the swing. Before delivery, a final update pass is completed so clients receive the latest view that fits the report scope and time cutoffs.

Mordor Intelligence's Consumer IOT Market Sizing Compared With Other Published Estimates

Published market sizes for consumer IoT often differ because the timing and mechanics behind the numbers are not the same across publishers. Differences usually come from what each definition counts as consumer spending, how device prices are trended over time, and whether the estimate reflects recent product cycles and currency movements.

The spread also shows up when some studies use factory-gate value logic while others use end-user spending, and when service revenues are added using broad attachment ratios without on-the-ground checks. In our work, the refresh cadence and the currency timing used to convert regional revenues are treated as active inputs. ASP logic is then re-tested against channel signals, which is why the 2026 figure is positioned the way it is in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 204.18 B (2026) | |

| Global Report Publisher A | USD 249.82 B (2026) | Uses a broader value construct that can lean toward factory-gate valuation plus a wider service revenue stack, which can lift totals when consumer spend boundaries are not separated from upstream revenues. |

| Industry Research Publisher B | USD 301.24 B (2025) | Uses a different base year and tends to apply faster ASP and adoption progression into the base period, and the scope can be looser on what counts as consumer IoT across adjacent connected electronics. |

Taken together, the comparison points to three practical reasons for variation, which are base-year selection, the revenue point in the value chain, and how prices and service attach are updated as the market shifts. Our approach stays traceable because each total can be walked back to adoption, volume, and pricing assumptions that are reviewed again when new signals appear.

Key Questions Answered in the Report

What is the projected value of the Consumer IoT market in 2031?

It is expected to reach USD 369.08 billion, representing a 12.57% CAGR during 2026-2031.

Which region is forecast to grow the fastest through 2031?

Asia-Pacific, supported by China’s Xiaomi ecosystem and India’s Digital India program, is projected to expand at a 14.11% CAGR.

Which connectivity technology is gaining ground on Wi-Fi?

Ultra-Wideband is set for a 13.62% CAGR, fueled by smartphone integrations that enable centimeter-level positioning.

Why are Services becoming more important than Hardware?

Falling sensor costs commoditize devices, so vendors shift to subscription models that monetize firmware updates and analytics, driving Services at a 13.21% CAGR.

How do data-privacy regulations impact Consumer IoT growth?

GDPR and similar frameworks add compliance costs that slow smaller vendors and concentrate market share among large platforms with robust legal resources.

Page last updated on: