RAN Intelligent Controller Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

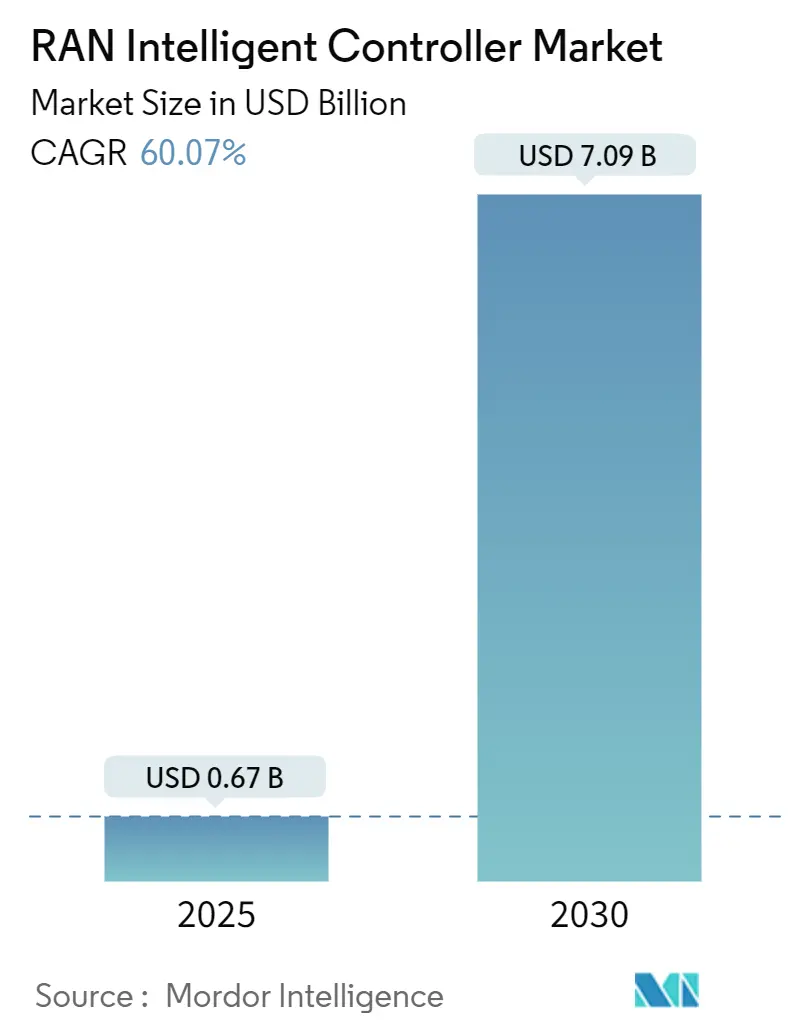

| Market Size (2025) | USD 0.67 Billion |

| Market Size (2030) | USD 7.09 Billion |

| Growth Rate (2025 - 2030) | 60.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

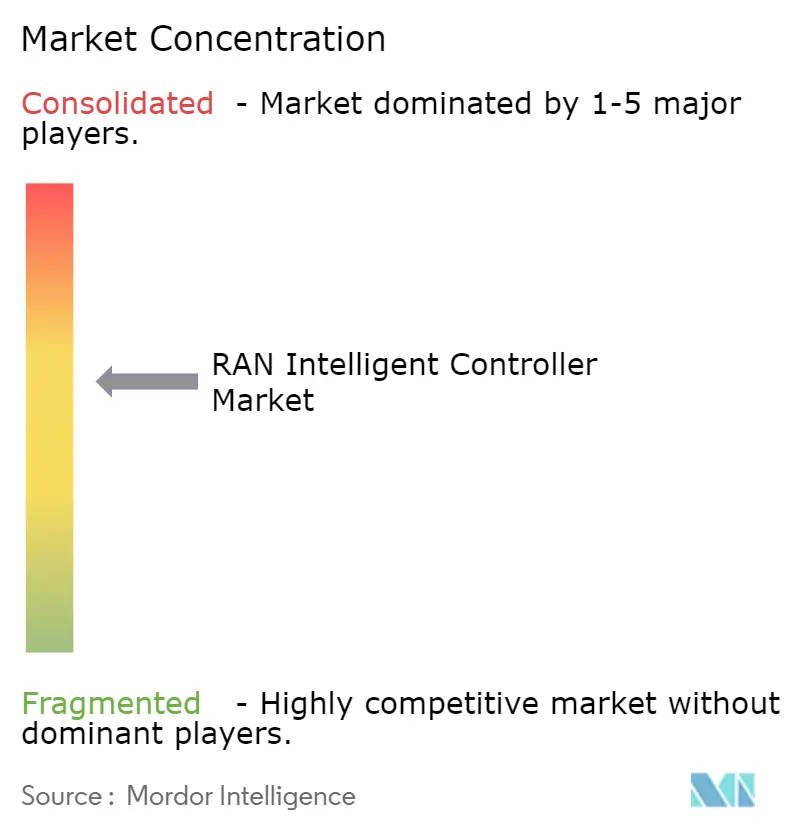

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RAN Intelligent Controller Market Analysis by Mordor Intelligence

The ran intelligent controller market size reached USD 0.67 billion in 2025 and is projected to climb to USD 7.09 billion by 2030, translating into a 60.07% CAGR over the forecast period. Surging 5G standalone roll-outs, formal O-RAN specifications, and generous public-sector incentives are fuelling unprecedented investment momentum. Platforms currently dominate spending as operators rush to establish cloud-native control foundations, while integration services race ahead as the fastest-growing revenue stream. Asia-Pacific’s early 5G leadership anchors the region at the top of the revenue table, yet Middle-East programs backed by sovereign digital-economy plans are expanding at the quickest clip. Traditional RAN suppliers are repositioning around software toolchains and AI engines, and hyperscale cloud providers are leveraging open interfaces to enter the radio domain. Despite sharp gains, the ecosystem faces integration complexity, multicloud orchestration hurdles, and heightened cyber-exposure that demand robust security frameworks.

Key Report Takeaways

- By component, platforms held 68.34% of ran intelligent controller market share in 2024, whereas services are advancing at a 63.17% CAGR to 2030.

- By function, the non-real-time RIC captured 64.53% revenue share in 2024, while the near-real-time RIC is forecast to grow at 64.22% CAGR.

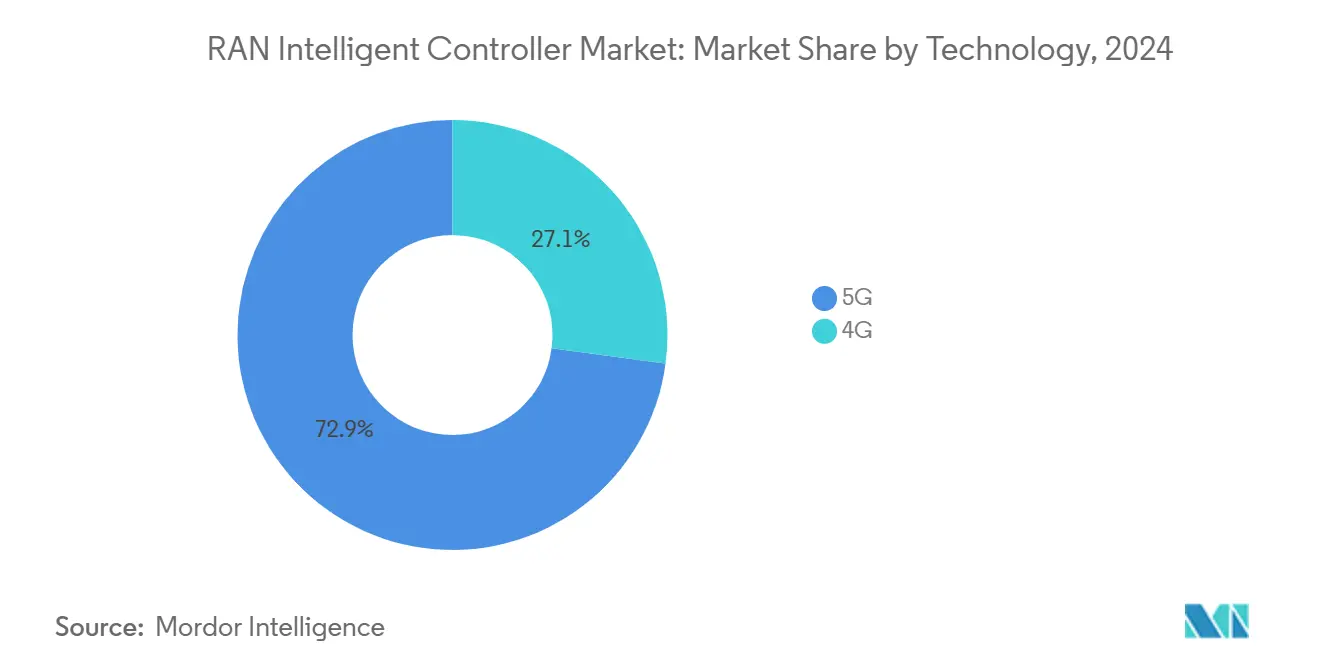

- By technology, 5G commanded 72.89% share of the ran intelligent controller market size in 2024 and also exhibits the highest 63.47% CAGR through 2030.

- By application, rApps accounted for 70.12% of 2024 revenue, whereas xApps are expanding at a 64.97% CAGR.

- By geography, Asia-Pacific led with 38.89% share in 2024; the Middle East is set to record a 61.57% CAGR through 2030.

Global RAN Intelligent Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| O-RAN standardization accelerates multivendor RIC adoption | +8.5% | Global, early gains in US, EU, Japan | Medium term (2-4 years) |

| Telco CAPEX shift toward software-centric RAN automation | +12.2% | North America and EU, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| 5G network slicing monetization demands AI-driven control | +15.8% | Asia-Pacific core, expanding to MEA and Americas | Medium term (2-4 years) |

| Government open-network mandates in US, EU and India | +9.3% | US, EU, India | Short term (≤ 2 years) |

| Renewable-energy KPIs pushing energy-savings rApps | +6.7% | Global, strong in EU | Long term (≥ 4 years) |

| Emergence of dApps enabling sub-10 ms URLLC in 6G testbeds | +7.5% | US, EU, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

O-RAN Standardization Accelerates Multivendor RIC Adoption

Since July 2024 the O-RAN Alliance has issued 74 additional technical documents that codify non-real-time and near-real-time controller interfaces, unlocking practical interoperability across vendors. AT&T validated the concept by running a third-party rApp on Ericsson’s platform in its live network, proving that standardized APIs shorten onboarding cycles. Deutsche Telekom’s collaboration with Google Cloud illustrates how open specifications let hyperscalers inject agentic AI into the RAN.[1]Deutsche Telekom, “Partnership With Google Cloud Boosts Agentic AI in RAN,” telecomtalk.infoNEC and NTT DOCOMO advanced base-station automation with policy engines that trim energy use and raise spectral efficiency. Each successful deployment draws more vendors into the ecosystem, reinforcing the specification cycle that underpins ran intelligent controller market expansion.

Telco CAPEX Shift Toward Software-Centric RAN Automation

Operator balance sheets now prioritize software and AI licenses over proprietary hardware, redirecting billions of dollars toward programmable control layers. Ericsson’s Q2 2025 report showed a 13.2% adjusted EBITA margin on the back of intelligent automation sales. Digital Nasional Berhad hit 99.8% uptime after embracing intent-driven operations that rely on non-real-time RIC insights. AT&T earmarked up to USD 12.5 billion under a multi-year open RAN contract, exemplifying how software line-items are becoming central to budget cycles. Telefónica Germany’s cloud-native core migration highlights the agility gains that motivate similar shifts across Europe. Re-weighted CAPEX thus fuels the ran intelligent controller market because controller platforms anchor every software-defined network roadmap.

5G Network Slicing Monetization Demands AI-Driven Control

Enterprises are paying premiums for deterministic slices, forcing operators to automate radio resources in near real time. SoftBank’s AI-RAN proof boosted uplink channel estimation accuracy by 20%, demonstrating the performance headroom unlocked by learning-based schedulers. China already runs more than 5,325 private 5G networks that depend on slice orchestration, giving local carriers double-digit enterprise revenue growth. stc Group processed over 10,000 optimization actions during the Hajj peak, lifting throughput 10% despite traffic surges thanks to Nokia’s automation suite. As slice revenues scale, reinvestment in smarter controllers accelerates, intensifying demand across the ran intelligent controller market.

Government Open-Network Mandates Drive Strategic Vendor Selection

Public funding and procurement clauses are tilting tender outcomes toward open interfaces. The United States earmarked USD 1.5 billion for interoperable radio projects through the Public Wireless Supply Chain Innovation Fund. [2] Five allied governments released voluntary certification principles that lower the barrier for multivendor RIC roll-outs. Saudi Arabia went live with its first open RAN site, backed by an Intel-supported development center that seeds a local ecosystem. The U.S. Department of Defense plans open RAN deployments across roughly 800 bases, offering suppliers a large, security-sensitive reference customer. Regulation therefore delivers both capital and credibility, helping the ran intelligent controller market secure long-term growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited E2-interface support from legacy RAN vendors | -4.8% | Global, acute in mature markets | Short term (≤ 2 years) |

| CSP hesitation over RIC security and DoS attack surface | -6.2% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Scarcity of commercially deployable xApps ecosystem | -3.9% | Global | Medium term (2-4 years) |

| Integration complexity across multicloud O-Cloud footprints | -7.1% | Enterprise-focused deployments worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CSP Hesitation Over RIC Security and DoS Attack Surface

Academic analyses reveal that distributed denial-of-service strikes can overload RIC control planes, exhausting compute cycles and degrading throughput. [3]Ettiane Raja, “Mitigating Denial of Service Signaling Threats in 5G Mobile Networks,” thesai.orgState-transition exploits on the 5G radio resource control layer pose similar threats, prompting operators to test hardened kernels and anomaly detectors. Benchmarking shows that CPU utilization on RYU controllers spikes sharply when under volumetric attack, cutting available headroom for policy execution. Resulting risk perceptions slow near-term procurement, especially in markets with strict service-level penalties. Vendors now embed zero-trust APIs, isolation sandboxes, and closed-loop monitoring, yet many carriers remain cautious, tempering ran intelligent controller market adoption.

Integration Complexity Across Multicloud O-Cloud Footprints

Orange Labs openly requested industry help after discovering that stitching together disaggregated RAN functions across three cloud providers exceeded internal tooling limits. Controller roll-outs must mesh Kubernetes clusters, real-time hypervisors, and proprietary accelerators without breaking latency budgets. Red Hat and Aarna Networks responded with declarative orchestration blueprints that abstract heterogeneous resources. Research on multicloud MLOps underscores the need for secure artifact pipelines that complicate deployment roadmaps. Added systems-integration fees eat into the total-cost-of-ownership savings promised by open RAN, restraining uptake among operators lacking deep cloud skill sets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Underpin Early Revenue Concentration

Platforms generated 68.34% of 2024 revenue, reflecting the urgent requirement for foundational orchestration layers that unify policy engines, model repositories, and life-cycle management. This dominance translates into a USD 0.46 billion slice of the ran intelligent controller market size in 2024, supported by mature roadmaps from Ericsson, Nokia, and VMware. Services contribute a smaller base today yet sprint ahead at a 63.17% CAGR as carriers outsource integration, validation, and continuous-integration pipelines. Leading operators now request consultative packages that bundle DevOps coaching, security hardening, and performance tuning, pushing services revenue into double-digit growth zones.

Ecosystem differentiation centers on AI toolchains and developer experience. Ericsson’s Intelligent Automation Platform ships with software development kits that cut rApp onboarding time to days, directly feeding the ran intelligent controller market. Nokia’s anyRAN platform offers a cloud substrate that lets carriers rent GPU cycles for model training, converting capital expense into usage-based fees. Intel’s FlexRAN reference designs inject silicon-level optimizations, delivering 15% scheduling efficiency gains that strengthen platform value propositions. As multi-vendor deployments increase, service specialists orchestrate cross-domain testbeds, adding a sticky revenue layer that sustains long-term services expansion.

By Function: Non-RT RIC Provides the Policy Backbone

The non-real-time controller held 64.53% share in 2024 given its role in policy training, slice intent translation, and week-ahead optimization. Carriers depend on its extensive telemetry to craft energy-savings strategies and proactive maintenance routines, ensuring a stable ran intelligent controller market share for the module. The near-real-time RIC delivers sub-second loop closures and now records a 64.22% CAGR as edge-cloud economics improve. Trials confirm that latency below 100 ms can triple cell-edge throughput in high-traffic districts, encouraging wider adoption.

Deployment progression starts with non-real-time pilots that establish data lakes and analytic workflows before moving to near-real-time controls that act on micro-bursts. SoftBank’s 20% gain in channel estimation accuracy validates the performance uplift possible with near-instant decisions. Research on federated neuro-evolution shows that training agents locally and sharing only gradients protects radio privacy while maintaining model convergence, a method well suited to near-real-time loops. Integration of both control tiers under a unified platform gives operators a single governance framework, simplifying security audits and policy rollbacks.

By Technology: 5G Aligns Perfectly With Controller Economics

5G accounted for 72.89% of 2024 revenue, equating to roughly USD 0.49 billion, as the protocol’s service-based architecture intrinsically relies on software hooks for dynamic orchestration. The same 5G substrate posts the fastest 63.47% CAGR thanks to aggressive standalone deployments that elevate controller demand. The ran intelligent controller market size for 5G deployments is projected to surpass USD 5 billion by 2030, reinforcing the technology’s centrality. Hybrid 4G overlays remain viable, yet investment gravitates toward 5G where private-network and slicing opportunities deliver premium margins.

Operators exploit 5G core exposure mechanisms to feed real-time KPIs into controller inference engines, enabling per-flow quality adjustments. Telstra’s cloud RAN implementation shows that virtualized units paired with near-real-time RICs can double cell capacity without hardware swaps. NEC’s vRAN deal with NTT DOCOMO illustrates how software optimization can drop total cost of ownership 30% while halving power draw, accelerating ROI and supporting environmental targets. Continuous 5G performance gains reinforce controller budgets and motivate vendors to align roadmaps around 3GPP Release 18 and beyond.

By Application: rApps Dominate Early while xApps Accelerate

Non-real-time rApps generated 70.12% of 2024 spending because they tackle immediate pain points such as energy trimming, anomaly detection, and traffic forecasting. Rakuten Mobile’s 25% power saving after deploying an energy-efficiency rApp exemplifies the direct OPEX benefits that convince finance teams. xApps show the strongest 64.97% CAGR as developers refine radio-level optimizers capable of beamforming and congestion management in near real time. The ran intelligent controller market size associated with xApps is expected to multiply eightfold by 2030 as marketplaces mature.

Marketplace fragmentation dampens xApp scale today. Nokia supplies the majority of production-grade xApps, while several rivals express doubts about addressable revenue. Academic prototypes demonstrate concept validity yet lack carrier-grade packaging. Standardized SDKs and revenue-sharing portals are emerging to resolve discoverability and compliance issues. Once critical mass is reached, xApp diversity promises autonomous cell orchestration, predictive beam steering, and URLLC packet prioritization that will make xApps the principal growth vector within applications.

Geography Analysis

Asia-Pacific commanded 38.89% of 2024 revenue, largely on the back of Chinese and Japanese operator scale. Massive 5G private-network deployments across manufacturing, mining, and port logistics continue to funnel capital toward controllers that ensure deterministic performance. Japan’s early-adopter culture encourages multi-vendor pilots, sustaining healthy demand for both non-real-time and near-real-time variants. South Korea showcases bare-metal 5G cores that tightly integrate with RICs, reinforcing regional technical leadership and anchoring supplier roadmaps.

The Middle East posts a 61.57% CAGR through 2030 as Gulf Cooperation Council states place network autonomy at the heart of digital-economy visions. Saudi Arabia’s USD 427 million 5G spend, paired with Intel-backed development centers, lowers market-entry barriers for software firms. The United Arab Emirates demonstrated the region’s first 5G cloud RAN in Abu Dhabi, proving that desert temperatures do not preclude edge-cloud deployments. Government tenders often bundle sustainability and localization metrics, prompting vendors to establish local labs and training programs.

North America benefits from federal funding pools and military trials that validate security frameworks, easing commercial procurement risk. Europe balances innovation with stringent data-sovereignty rules, steering demand toward on-premise or sovereign-cloud deployments. Latin America and Africa remain nascent yet represent long-tail upside as device penetration rises and spectrum auctions finalize. Collectively, diversified geographic drivers ensure that the ran intelligent controller market enjoys a resilient global opportunity pipeline.

Competitive Landscape

High entry costs and specialized AI competencies keep the competitive field moderately concentrated. Huawei, Ericsson, and Nokia together hold roughly 74.5% of aggregate RAN equipment revenue, but software-first challengers erode legacy dominance in the controller layer. Ericsson advanced to 25.7% share of controller revenues after clinching multi-year open-RAN contracts with AT&T and Telstra, pairing those wins with record 13.2% EBITA margins.

Nokia leverages a partnership lattice spanning KDDI, SoftBank, T-Mobile, and NVIDIA to deliver platform-as-a-service models that monetize GPUs during AI training cycles. Red Hat, Wind River, and Amdocs supply container stacks, real-time kernels, and service-management layers, crowding the value chain and pressuring incumbent licensing margins. Intel, NVIDIA, and Qualcomm inject chip-level differentiation, embedding AI accelerators that cut inference latency, thus capturing a rising share of platform value.

Strategic moves include the AI-RAN Innovation Center in Washington state, uniting T-Mobile, NVIDIA, Ericsson, and Nokia to co-develop cloud-native inference workflows. Ericsson’s collaboration with AWS adds agentic AI constructs that self-adapt to policy objectives, pushing cognitive networking closer to mainstream rollout. These alliances blur traditional telecom boundaries, and the resulting co-innovation keeps competitive dynamics fluid yet centered on AI-driven value creation.

RAN Intelligent Controller Industry Leaders

Telefonaktiebolaget LM Ericsson

Nokia Corporation

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

ZTE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: AT&T deployed the first third-party rApp on a production network using Ericsson’s Intelligent Automation Platform, proving multi-vendor programmability at scale.

- March 2025: T-Mobile, NVIDIA, Ericsson, and Nokia opened the AI-RAN Innovation Center in Bellevue to merge AI workflows with 5G radios.

- March 2025: NTT Corp., NTT DOCOMO, and NEC demonstrated distributed MIMO for high-frequency 6G links in vehicles and trains.

- February 2025: Ericsson and Telstra agreed to deliver Asia-Pacific’s first fully programmable 5G network with open-RAN-ready radios and AI automation.

Global RAN Intelligent Controller Market Report Scope

| Platforms |

| Services |

| Non-RT RIC (Non-Real-Time) |

| Near-RT RIC (Near-Real-Time) |

| 4G |

| 5G |

| rApps |

| xApps |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Platforms | ||

| Services | |||

| By Function | Non-RT RIC (Non-Real-Time) | ||

| Near-RT RIC (Near-Real-Time) | |||

| By Technology | 4G | ||

| 5G | |||

| By Application | rApps | ||

| xApps | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the ran intelligent controller market?

It stands at USD 0.67 billion in 2025 with a forecast to reach USD 7.09 billion by 2030.

Which region leads revenue generation for ran intelligent controllers?

Asia-Pacific contributes the largest 38.89% share owing to large-scale 5G deployments and supportive regulation.

Which component segment is growing fastest?

Integration and support services post the quickest 63.17% CAGR as operators seek expert help with multivendor roll-outs.

Why are near-real-time RICs gaining traction?

They enable sub-second resource optimization that boosts throughput and latency performance needed for enterprise network slices.

What is the biggest barrier to wider RIC adoption?

Multicloud integration complexity coupled with heightened security risks slows some commercial decisions despite compelling ROI cases.

Page last updated on: