Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 11.55 Billion |

| Market Size (2031) | USD 24.17 Billion |

| Growth Rate (2026 - 2031) | 15.94% CAGR |

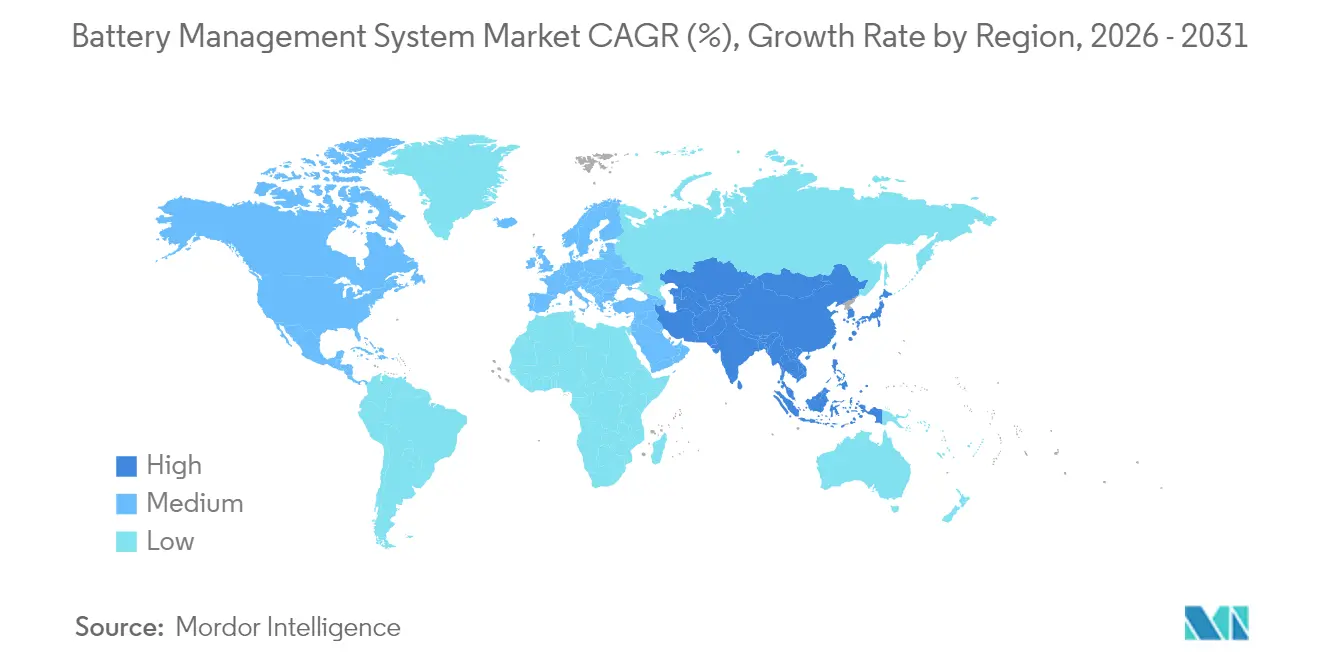

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

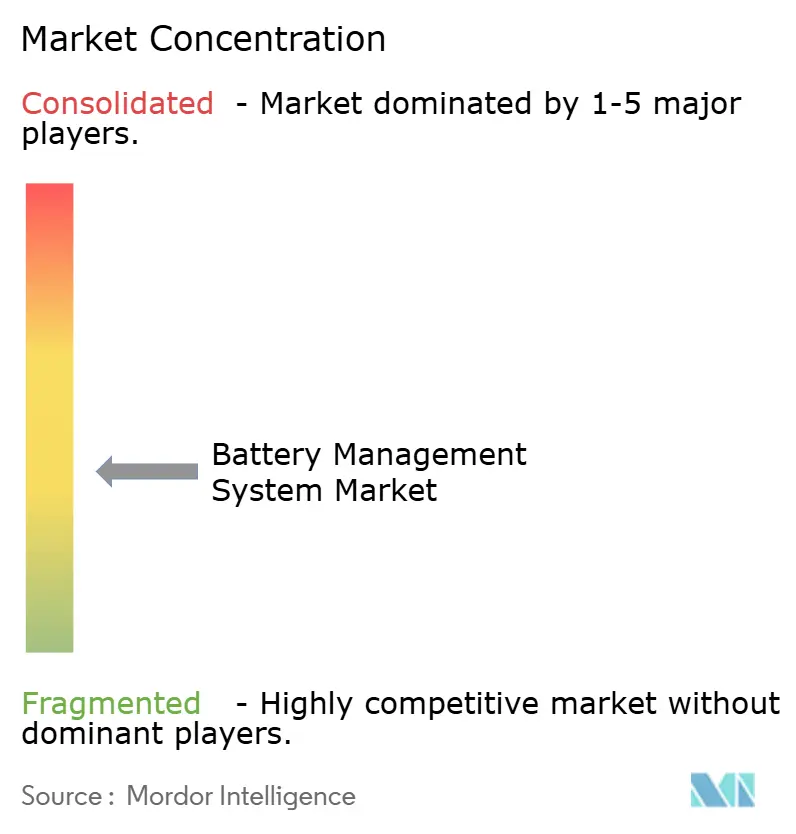

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Battery Management System Market Analysis by Mordor Intelligence

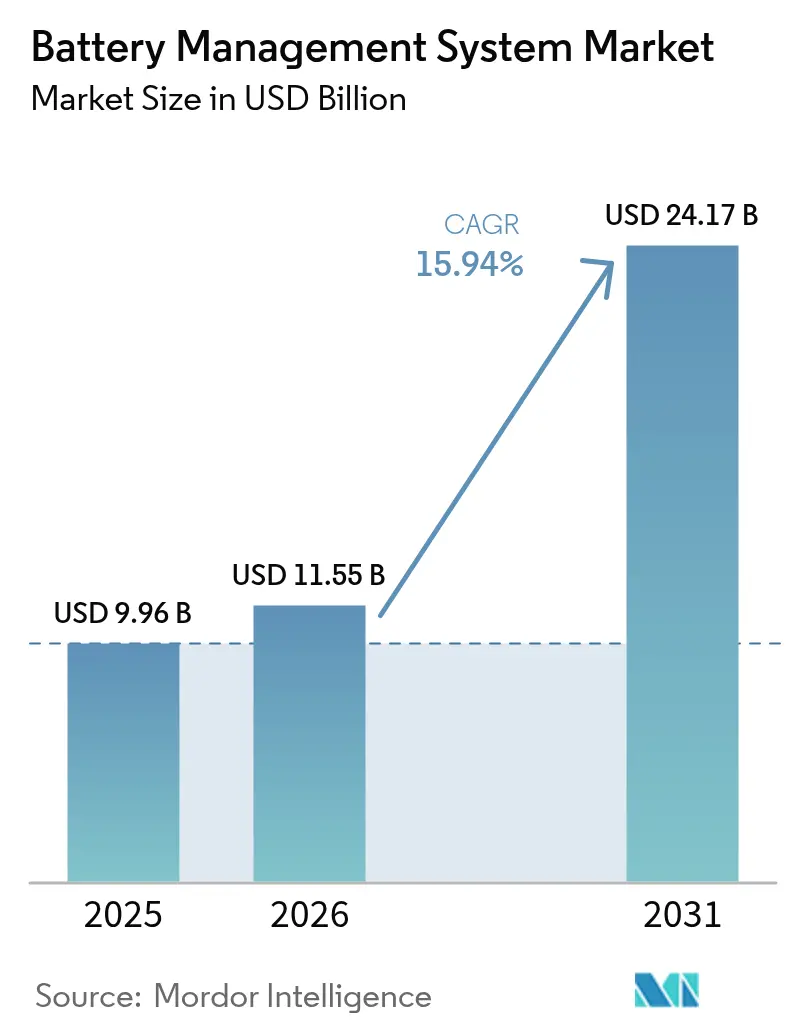

Battery Management System Market size in 2026 is estimated at USD 11.55 billion, growing from 2025 value of USD 9.96 billion with 2031 projections showing USD 24.17 billion, growing at 15.94% CAGR over 2026-2031.

Surging demand for electric vehicles, a boom in grid-scale batteries, and steady advances in analog front-end semiconductors anchor this expansion. Within vehicles, a Battery Management System market solution now acts as a data nerve center, balancing cells, guarding against thermal events, and feeding real-time health analytics into propulsion controls. Grid operators are installing multi-megawatt systems that stretch service life expectations to 20 years, further widening the addressable pool. The Asia-Pacific region dominates installations, thanks to China’s vertically integrated battery value chain, while North America and Europe scale up domestic capacity under generous industrial policies. Vendors are sharpening their differentiation around wireless communication, edge AI diagnostics, and cloud dashboards that promise lower total cost of ownership. Strategic acquisitions, most recently, have seen large chipmakers acquire Ethernet and cybersecurity assets, continuing to reshape competitive boundaries.

Key Report Takeaways

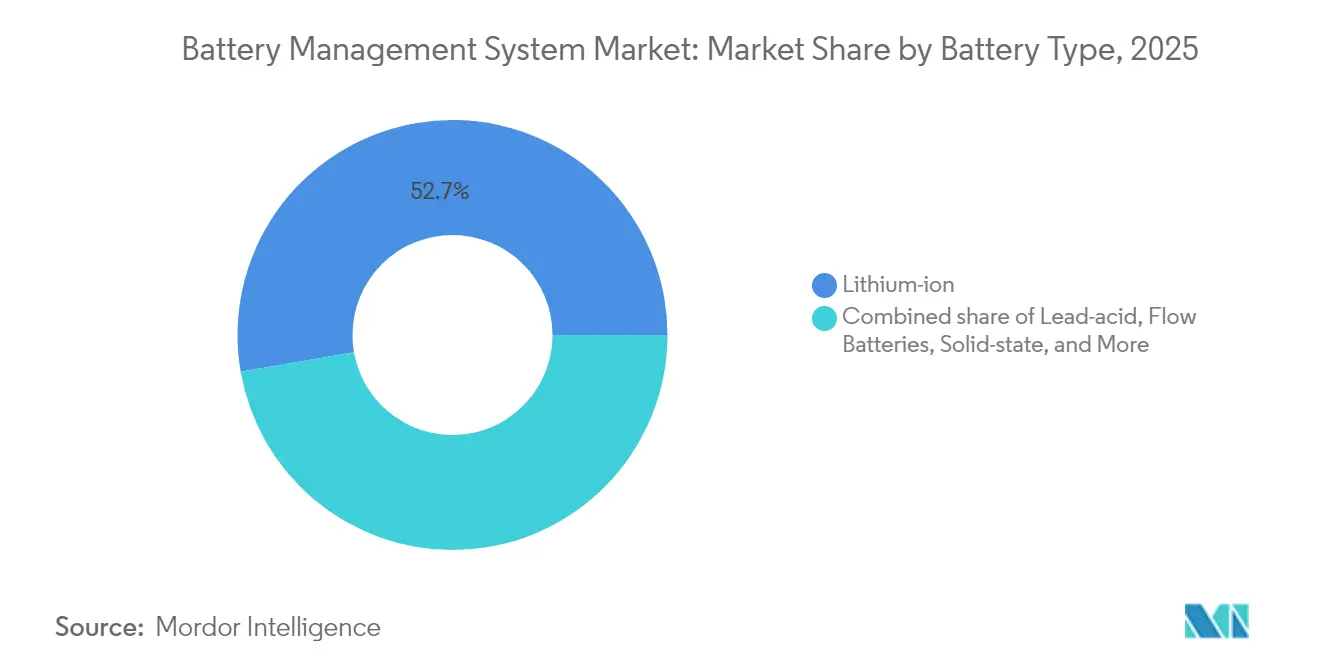

- By battery type, lithium-ion packs captured 52.74% of the Battery Management System market size in 2025, while solid-state variants are expected to accelerate at a 41.38% CAGR to 2031.

- By topology, distributed designs accounted for 42.45% of the revenue in 2025; hybrid wireless approaches are expected to expand at a 22.96% CAGR.

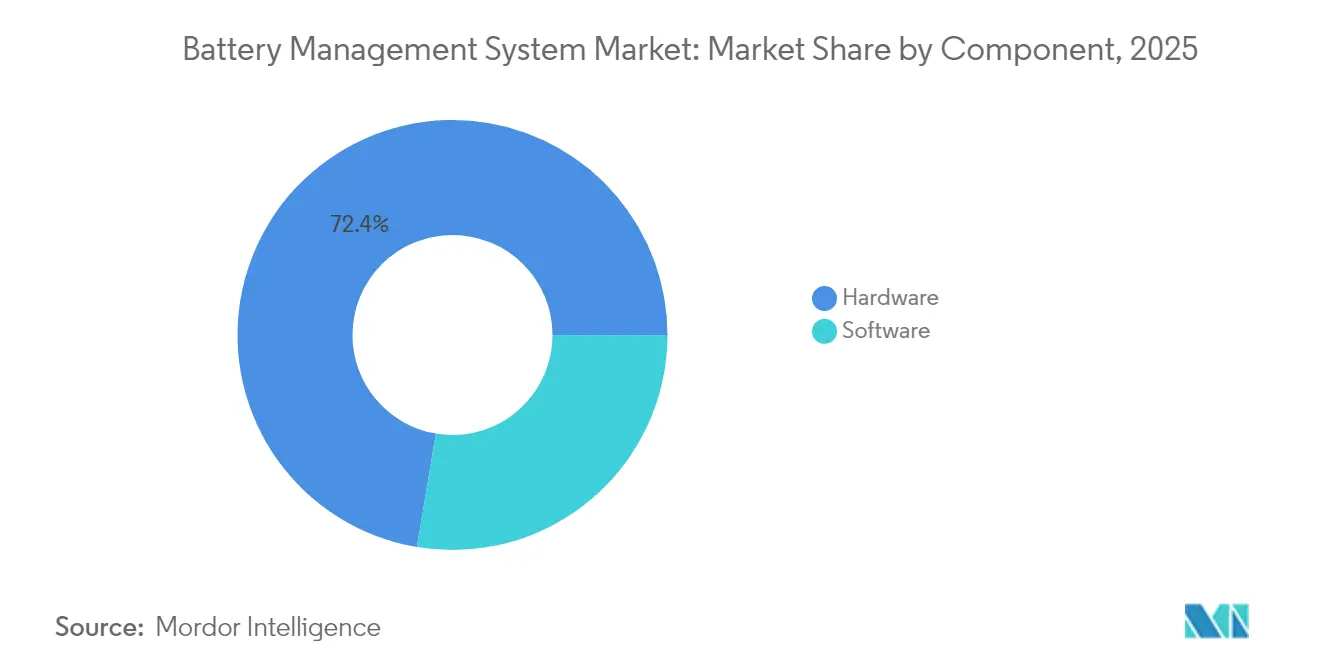

- By component, hardware contributed 72.35% of 2025 revenue, whereas software climbed at a 24.47% CAGR.

- By voltage, high-voltage packs with a voltage of more than 60 V held a 65.88% share of the Battery Management System market size in 2025 and advanced at an 17.62% CAGR.

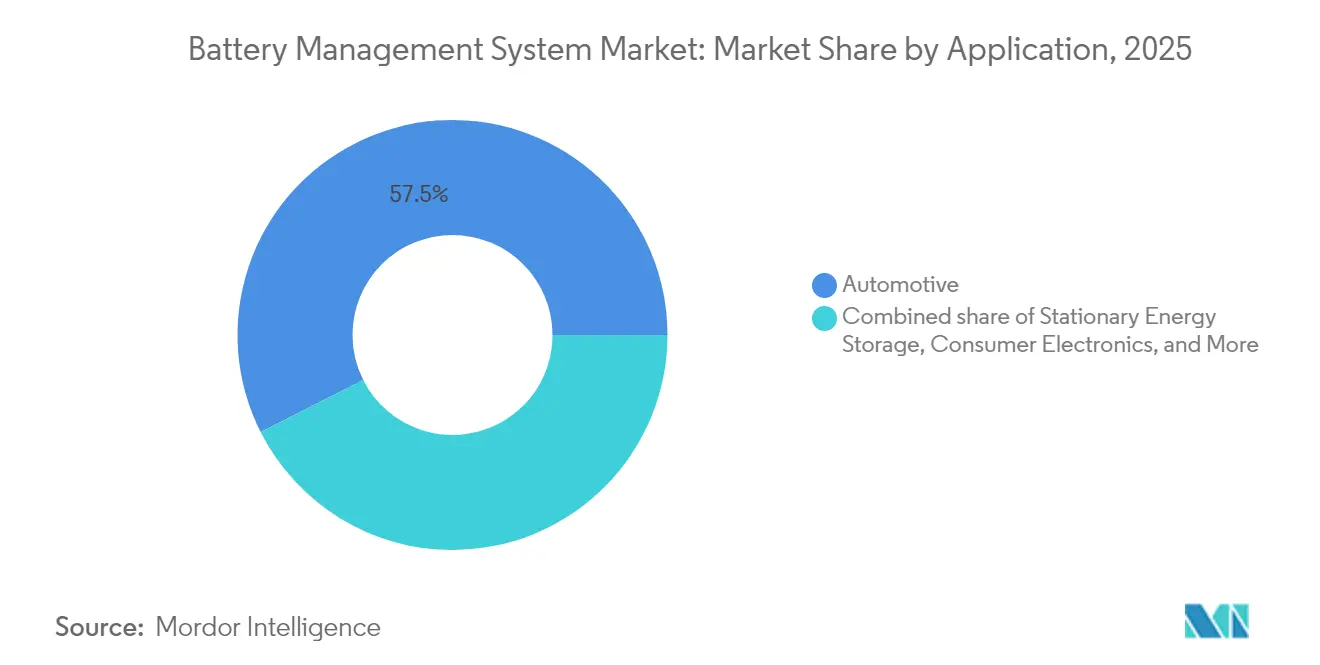

- By application, the automotive sector retained 57.45% of the Battery Management System market share in 2025, while stationary storage is projected to post the highest 30.85% CAGR through 2031.

- By geography, the Asia-Pacific region led with a 60.92% share in 2025 and is expected to remain the fastest-growing region at a 19.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Battery Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV production boom fuels demand for high-voltage BMS | +5.7% | Global, with early gains in China, Europe, North America | Medium term (2-4 years) |

| Government safety & carbon mandates accelerate adoption | +3.2% | Global, spill-over to emerging markets | Long term (≥ 4 years) |

| Falling lithium-ion pack prices expand addressable markets | +2.4% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Grid-scale storage build-out requires utility-grade BMS | +1.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| 800-V power-train shift creates need for next-gen HV BMS | +1.6% | Europe & North America, early adoption in premium segments | Short term (≤ 2 years) |

| Wireless BMS architectures enable flexible pack design | +1.3% | Global, with technology leaders in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV production boom fuels demand for high-voltage BMS

Global battery-electric vehicle sales surpassed 13.9 million units in 2024 and are projected to exceed 30 million by 2027, prompting Battery Management System market vendors to engineer ASIL D-compliant solutions that monitor up to 360 cells in commercial vehicle packs. Automakers such as General Motors deploy wireless BMS designs that remove 90% of harness wiring, thus reducing mass and assembly time. High-voltage 800 V platforms demand advanced thermal algorithms and real-time diagnostics, repositioning the BMS as an active enabler of fast charging rather than a passive safeguard. Supply-chain partnerships around proprietary communication ICs now decide platform wins in premium EV segments.

Falling lithium-ion pack prices expand addressable markets

Lithium-ion costs dipped below USD 100 per kWh in select configurations in 2024, unlocking new industrial and residential projects that previously relied on lead-acid packs. The affordable chemistry trend fosters Battery Management System market penetration into forklifts, telecom UPS, and emerging-market micro-mobility fleets. Vendors respond with simplified boards that retain essential safety while trimming the bill of materials cost. Modular BMS kits scale from 1 kWh solar-home systems to multi-MWh storage farms, supporting quick deployment and reduced servicing downtime.[1]LG Energy Solution, “Utility-Scale Storage Projects Exceed 10 GWh,” lgensol.com

Government safety & carbon mandates accelerate adoption

China enforces two-hour no-fire rules after a thermal runaway incident in July 2026, compelling every domestic EV to integrate high-accuracy cell-temperature sensors and redundant isolation checks. The European Union’s battery regulation adds digital-passport traceability, further elevating BMS firmware requirements for secure data logging. India’s Electric Mobility Promotion Scheme 2024 allocates USD 60 million to subsidize EV purchases, indirectly boosting local BMS assembly.[2]Ministry of Heavy Industries, “Electric Mobility Promotion Scheme 2024,” heavyindustries.gov.in These policies provide long-term visibility, convincing semiconductor foundries to commit capacity for automotive-grade analog nodes.

Grid-scale storage build-out requires utility-grade BMS

Utility batteries exceeding 10 GWh of orders in 2024 rely on cloud-connected BMS for 20-year lifespans and remote analytics. Vendors like Nuvation Energy ship configurable controller racks that supervise thousands of cells while meeting anti-islanding grid codes. Artificial-intelligence algorithms enhance state-of-health forecasting and schedule preventive service visits, reducing lifetime operating costs for independent power producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor shortages constrain BMS shipments | -1.9% | Global, acute impact in automotive supply chains | Short term (≤ 2 years) |

| High integration & certification cost for advanced BMS | -1.3% | Global, particularly affecting smaller OEMs | Medium term (2-4 years) |

| Growing cyber-attack surface of connected BMS platforms | -0.6% | North America & EU, expanding globally | Medium term (2-4 years) |

| Patchy global rules for 2nd-life batteries slow reuse | -0.5% | Global, with regulatory gaps in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor shortages constrain BMS shipments

Automotive-grade analog and power chips remain in short supply through 2026 as foundries prioritize higher-margin smartphone nodes. Battery Management System market suppliers redesign boards around available pin-outs, negotiate multi-year supply contracts, and even bankroll new 200 mm lines to protect allocations. Lead times exceeding 52 weeks compel vehicle manufacturers to hold excess inventory, tying up working capital and delaying the introduction of new models.

High integration & certification cost for advanced BMS

Gaining ASIL D certification can exceed USD 10 million and 18 months of validation, a hurdle that sidelines start-ups and narrows the supplier base.[3]STMicroelectronics, “ASIL-D Certification Costs for BMS Platforms,” st.com Automakers increasingly select platform partners with proven functional-safety stacks to reduce homologation risk. Modular reference designs and standardized CAN-FD or Ethernet gateways are gradually lowering barriers; however, economies of scale still favor tier-one semiconductor companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Solid-State Revolution Accelerates

Lithium-ion retained 52.74% revenue in 2025, yet solid-state boards sprint ahead at 41.38% CAGR as commercial launches near 2028. Toyota targets 20% range gains and 10-minute charges, demanding brand-new impedance-detection logic inside every BMS. The Battery Management System market share for lithium-ion remains sizable thanks to ever-cheaper LFP and high-nickel NMC, while lead-acid lingers in starter batteries. Flow and nickel chemistries address niche industrial operations requiring hour-long discharge or extreme temperature resilience.

By Topology: Distributed Architecture Dominates Innovation

Distributed boards controlled 42.45% revenue in 2025 and led innovation with a 22.96% CAGR. Processing power is spread across modules, trimming harness length, and elevating fault tolerance. NXP’s ultra-wideband chipset eliminates up to 90% of wiring, allowing designers to craft skateboard packs of any shape. Centralized designs prevail in budget scooters and power tools, while modular racks excel in utility storage. Hybrid layouts combine a master ECU with wireless cell nodes to strike a balance between cost and performance.

By Component: Software Monetization Accelerates

Hardware still supplied 72.35% of 2025 revenue, but software rose 24.47% per year as cloud dashboards unlocked predictive maintenance fees. Electrochemical impedance routines running at the edge capture nuanced degradation signs, extending pack life and supporting second-life leasing. KULR and its partners claim that AI-based load balancing can increase usable capacity by 34%, underscoring the value beyond silicon. The Battery Management System industry now revolves around full-stack offerings marrying ±2 mV accuracy with machine-learning forecasts.

By Voltage Range: High-Voltage Systems Drive Efficiency

Systems above 60 V generated 65.88% of the revenue in 2025 and achieved an 17.62% CAGR as automakers transition to 800 V architectures that charge from 5% to 80% in under 23 minutes. Medium-voltage packs power buses and off-highway gear, while <36 V arrays dominate handhelds. Infineon’s 1,200 V SiC MOSFETs selected by FORVIA HELLA underscore how semiconductor progress supports even higher voltages in future lines. Some truck OEMs trial 1,000 V systems, pushing BMS isolation and arc-fault detection to new limits.

By Application: Stationary Storage Emerges as Growth Leader

Stationary energy storage races ahead with a 30.85% CAGR, transforming from pilot projects into mainstream grid assets. The Battery Management System market size for stationary installations is expected to reach half of the automotive volumes by 2030, following LG Energy Solution's securing of over 10 GWh of utility orders in 2024. Operators demand controllers that juggle thousands of cells, assure 20-year duty cycles, and integrate seamlessly with SCADA.

The automotive industry still supplies a significant volume, benefiting from BMW's 800 V Neue Klasse packs that require next-generation thermal safeguards. Consumer electronics remain steady, while industrial and telecom UPSs rebound due to data-center builds, and medical devices command premium pricing for a 30% longer service life. Aerospace and marine markets, although small, reward ruggedized BMS that can withstand extreme vibration and salt fog.

Geography Analysis

The Asia-Pacific region accounted for 60.92% of the revenue in 2025 and is projected to grow at a 19.08% annual rate through 2031. China’s scale drives raw-material refining, cell manufacturing, and final vehicle assembly in the same industrial clusters, thereby lowering the landed cost of domestic BMS boards. CATL alone shipped 36.7% of global EV battery capacity in the first three quarters of 2024 and invests in embedded cell-to-pack diagnostics that demand next-generation controllers. India allocates USD 60 million to boost local EV uptake, giving regional suppliers a path to volume contracts. Japan and South Korea contribute precision ICs and automotive software expertise, rounding out the ecosystem.

North America ranks second as the Inflation Reduction Act ties tax credits to locally sourced batteries. General Motors budgets USD 35 billion for EV programs that rely on in-house Ultium wireless BMS to streamline pack variants. Tesla, Rivian, and legacy automakers are breaking ground on giga-factories across the Midwest, anchoring demand for high-voltage board assemblies. California and Texas lead grid storage installations, each topping 2 GWh added in 2024, driving utility-grade BMS volume.

Europe combines stringent carbon rules with innovation in second-life batteries. Automakers are pursuing 800V drivetrains, seeking faster charging and lighter cables. The EU Battery Regulation mandates material traceability and recycling, prompting manufacturers to embed a secure on-pack data logger to ensure compliance. South America and the Middle East & Africa remain early-stage yet promising. Chile’s lithium wealth and South Africa’s renewable goals encourage pilot energy-storage farms that test cost-optimized BMS boards, laying the groundwork for future growth.

Regulatory Landscape

Battery management systems are increasingly shaped by safety, traceability, and durability requirements that vary by region and application. In the European Union, Regulation (EU) 2023/1542 (EU Battery Regulation) elevates data and compliance expectations across EV, LMT, and stationary batteries, including requirements tied to state-of-health and lifetime-related parameters that place new emphasis on secure BMS data logging and firmware governance. Regulation (EU) 2025/1561 amended the EU Battery Regulation by extending the due diligence obligation deadline for economic operators to 26 July 2026, giving supply chains additional time to align verification and reporting processes while maintaining compliance momentum.

In the United States, 40 CFR 86.1815-27 was updated via a Federal Register amendment published on 18 February 2026 to incorporate GTR No. 22 requirements for battery electric and plug-in hybrid vehicles, with mandatory application starting in model year 2027. This reinforces BMS validation and documentation needs tied to vehicle certification. In China, MIIT released SJ/T 11978-2025 (implemented 31 July 2025) covering lithium-ion BMS technical specifications for consumer, energy storage, and power applications (excluding EVs), pushing regional standardization in non-EV segments and encouraging vendors to maintain separate compliance configurations across automotive and stationary product lines.

Competitive Landscape

The Battery Management System market is moderately fragmented. Analog power specialists such as Texas Instruments, NXP, and Infineon supply high-precision monitoring ICs while acquiring complementary Ethernet or wireless assets to offer turnkey platforms. Infineon’s USD 2.5 billion purchase of Marvell’s automotive Ethernet unit in April 2025 strengthens zone-controller portfolios that merge the domains of propulsion, charging, and battery. EnerSys spent USD 208 million on Bren-Tronics to access rugged, military-grade lithium packs, thereby broadening its defense revenue streams.

Competitive pressure is shifting toward software differentiation. Vendors bundle cloud portals, over-the-air firmware, and AI-driven health scoring to secure recurring revenue from licenses. Wireless intellectual property is a hotly contested area; NXP has introduced an ultra-wideband BMS chipset slated for 2025 production, while Analog Devices partners with LG Energy Solution on impedance spectroscopy analytics. Patent filings around cell-to-pack topologies and solid-state monitoring climbed 18% YoY in 2024, signalling a technology arms race.

Cybersecurity is emerging as a key purchase criterion. Leading players embed hardware root-of-trust and secure boot in monitoring ASICs, anticipating UNECE R155 compliance on vehicle cyber resilience. Mid-tier suppliers without deep silicon resources seek alliances to integrate certified secure-element cores. Overall, intensified M&A and platform strategies are channelling market share toward firms that can deliver combined hardware-software stacks, moving the structure from fragmented boards to consolidated ecosystems.

Battery Management System Industry Leaders

Sensata Technologies, Inc.

Texas Instruments Incorporated

Renesas Electronics

NXP Semiconductors

CATL

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity sits at the intersection of compliance-grade battery data and software-defined diagnostics, especially for stationary storage and EV packs that need to retain usable state-of-health and lifetime-related parameters. The EU Battery Regulation (Regulation (EU) 2023/1542) increases the value of BMS designs that combine secure data storage, audit-ready traceability, and over-the-air controllability, while also creating room for cloud dashboards and firmware toolchains that simplify reporting across multi-site fleets. In stationary storage, interoperability-focused engineering is becoming more explicit: IEEE 2686-2024 (published February 2025) establishes recommended practices for the design, configuration, and interoperability of BMS in stationary energy storage systems, supporting packaged, standards-aligned controller platforms for integrators and utilities.

Technology-led whitespace is also expanding in embedded health analytics and higher-voltage stationary architectures. In June 2026, Texas Instruments introduced the BQ79826Z-Q1 battery monitor with an integrated Electrochemical Impedance Spectroscopy (EIS) engine, bringing lab-grade diagnostics closer to real-time operation inside the BMS hardware stack and enabling differentiated offerings around degradation detection, warranty analytics, and second-life qualification. Grid-forming and higher-voltage stationary systems are lifting expectations for BMS capabilities as well: in June 2026, Huawei Digital Power launched the LUTERRA smart string grid-forming energy storage platform supporting 1000 V AC and 12.5 MW/50 MWh array capacity, which reinforces demand for utility-grade BMS that can coordinate large cell counts, fault handling, and long-duration performance under SCADA-connected operating models. Across both automotive and stationary applications, wireless BMS and cybersecurity-aligned designs (for connected platforms) remain active areas where vendors can monetize integration simplicity and lifecycle services as pack architectures move toward 800 V-class systems and software-defined vehicle networks.

Recent Industry Developments

- June 2026: Texas Instruments introduced the BQ79826Z-Q1, a high-cell-count battery monitor that integrates an Electrochemical Impedance Spectroscopy (EIS) engine. This embeds advanced health diagnostics into the BMS sensing layer, enabling tighter state-of-health estimation and new software-enabled service models for both EV and stationary storage packs.

- March 2026: Sensata Technologies launched the FaultBreak contactor aimed at improving EV safety and reliability by enabling protection and isolation functions in high-voltage architectures. The move supports higher-voltage pack designs where coordinated protection components and the BMS jointly manage fault response and thermal-event risk.

- November 2024: NXP Semiconductors unveiled an ultra-wideband (UWB) wireless battery management system solution. Wireless architectures reduce harness complexity and can shorten assembly time, shifting competitive differentiation toward robust wireless links, diagnostics, and system-level safety validation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned from battery management systems that monitor and control rechargeable battery packs, including sensing, balancing, protection, and the related control electronics and software used across common end-use deployments.

Scope exclusions: This sizing does not count the battery cells themselves, standalone chargers, or broader power electronics that are sold without a defined BMS function.

Segmentation Overview

- By Battery Type

- Lithium-ion

- Lead-acid

- Nickel-based

- Flow Batteries

- Solid-state

- By Topology

- Centralized

- Distributed

- Modular

- Hybrid

- By Component

- Hardware

- Software

- By Voltage Range

- Low (Up to 36 V)

- Medium (36 to 60 V)

- High (Above 60 V)

- By Application

- Automotive

- Stationary Energy Storage

- Consumer Electronics

- Industrial and Telecom UPS

- Medical Devices

- Aerospace and Marine

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to anchor assumptions that can be checked against public signals. We relied on sources such as US DOE publications, IEA data on EV and storage adoption, UNECE and US NHTSA safety and vehicle regulation references, and UN Comtrade trade statistics for relevant electronics and battery related flows. Technical direction was also cross-checked using peer-reviewed journals and patent databases, which helped us separate core BMS functions from adjacent battery monitoring electronics.

On the company side, annual reports, investor presentations, and product documentation were reviewed to understand how suppliers describe BMS hardware, firmware, and sensing content, and how pricing is discussed across voltage and application needs. Paid subscription sources for company financials and news and financials were used selectively to confirm corporate structure, revenue visibility, and event timing. The sources listed above are illustrative, and many other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were completed with a mix of battery pack designers, electronics suppliers, integrators, and downstream buyers in transportation, stationary storage, and portable end uses, so our assumptions could be tested against real operating settings. Interviews covered pricing drivers, typical feature sets, adoption timing, and how BMS content changes by voltage ranges and pack configuration. Outputs were then reconciled across APAC, EMEA, and the Americas to reduce regional bias.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 49% |

| Mid tier: 45% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 16% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

The market was first reconstructed using a top-down approach where EV and energy storage demand indicators were converted into an addressable battery pack pool, and then translated into BMS value using penetration and content assumptions by application. Because BMS value varies by pack voltage and the protections required, pricing and content were adjusted using interview feedback on typical sensing counts, balancing approach, and software intensity for different use cases.

To keep the totals realistic, we corroborated the outputs with selective bottom-up approximations such as sampled ASP times estimated unit volumes for key application buckets, along with channel checks on how BMS is bundled or sold separately in packs. Inputs used in the model included EV production and sales trends, stationary storage deployments, average battery pack sizes, typical voltage range mix, and observed shifts in lithium-ion chemistries that influence balancing and protection needs. Forecasts were developed using scenario analysis, where macro adoption paths and cost-down expectations were translated into volume and ASP trajectories, and then reviewed with expert consensus to avoid overly aggressive curves. When supplier disclosure was limited, gaps were handled through ranges that were narrowed using multiple interview points and publicly visible adoption metrics.

Data Validation & Update Cycle

Outputs were checked through multiple passes so the final number stays consistent with the demand pool and with what buyers and suppliers describe in the field. Analysts compared the model against independent signals such as EV build plans, storage installation trends, and electronics content shifts, and then investigated large variances before sign-off.

If an input moved materially, such as a step-change in battery chemistry mix, a regulation-driven safety requirement, or a pricing reset, follow-up calls were triggered to re-test the assumption. Reports are refreshed annually, with interim updates when major events change volumes, pricing, or supply availability, and a final pre-delivery review is done so clients receive the latest updated view.

Mordor Intelligence's Battery Management System Market Size Compared With Other Published Estimates

Published market sizes for battery management systems can look far apart even when they appear to describe the same topic, since each publisher draws the line around what counts as a BMS and which applications are emphasized. The year picked as the base, the way pricing is trended, and how regional currency conversion is handled are also common reasons the numbers do not match.

The main gap comes from whether adjacent battery electronics are bundled into the value, since some estimates fold in battery pack control units or broader power electronics when they are sold together. By keeping the scope to defined BMS functions and tying the value build to application level demand indicators and voltage driven content, Mordor Intelligence ends up with a different 2026 starting point than sources that lean more heavily on component bundling or earlier base years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.55 B (2026) | |

| Global Consultancy A | USD 8.49 B (2024) | Uses an earlier base year and leans strongly toward EV-mounted rechargeable batteries, which can understate near-term value when stationary storage and non-EV applications are counted more explicitly, and it also shifts the comparison year away from 2026. |

| Industry Research Group B | USD 9.10 B (2024) | Anchors the market in 2024 and applies a 2024 to 2029 growth window, which can produce a different current size when price-down timing, application mix, and voltage range weighting are treated with simpler averages. |

The spread in the table is mostly explained by scope edges and base-year choice, rather than a disagreement that demand is growing. When the model is tied back to clear demand pools, voltage and application mix, and interview-tested ASP logic, the resulting total stays traceable and easier to update as new EV and storage data is released.

Key Questions Answered in the Report

What is the current size of the Battery Management System market?

The market reached USD 11.55 billion in 2026 and is projected to climb to USD 24.17 billion by 2031 at a 15.94% CAGR.

Which application segment leads revenue generation?

Automotive applications accounted for 57.45% of revenue in 2025, while Stationary Energy Storage applications are projected to grow fastest at a 30.85% CAGR through 2031.

Why are distributed topologies gaining traction?

Distributed architectures improve modularity, reduce single points of failure, and support wireless communication, helping them achieve 42.45% share in 2025 and the highest 22.96% growth rate.

How important is software in modern BMS solutions?

Software revenue grows at 24.47% CAGR because predictive analytics, over-the-air updates, and cloud dashboards add value beyond the hardware baseline.

Which region dominates demand?

Asia-Pacific holds 60.92% market share thanks to China’s leadership in battery production and EV manufacturing, coupled with rapid growth in India, Japan, and South Korea.

What are key challenges facing suppliers?

Persistent analog-chip shortages, high functional-safety certification costs, and cybersecurity threats on connected platforms continue to pressure margins and timelines.

Page last updated on: