Integrated Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

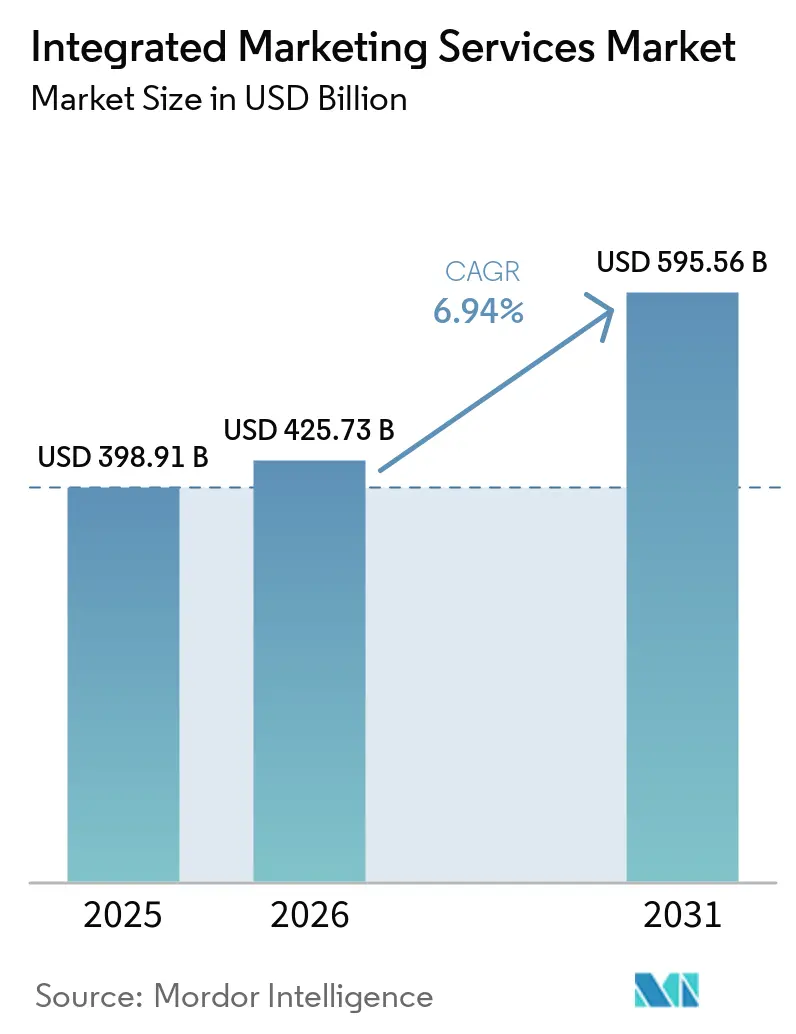

| Market Size (2026) | USD 425.73 Billion |

| Market Size (2031) | USD 595.56 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Integrated Marketing Services Market Analysis by Mordor Intelligence

The integrated marketing services market size is expected to increase from USD 398.91 billion in 2025 to USD 425.73 billion in 2026 and reach USD 595.56 billion by 2031, growing at a CAGR of 6.94% over 2026-2031. This expansion reflects a deeper reset in how brands organize spending across channels, partners, data, and measurement systems. Demand is moving toward service bundles that connect media, creative, digital execution, customer engagement, and analytics in one operating structure, because clients now want fewer handoffs and clearer accountability. Artificial intelligence is widening the scope of billable work instead of simply lowering labor needs, since brands still need agencies to manage personalization, workflow integration, and measurement across channels. Large holding companies are also pushing scale as a competitive tool, and the Omnicom and Interpublic combination has raised pressure on mid-sized firms to specialize, partner on technology, or deepen sector expertise. At the same time, privacy rules, AI governance requirements, and outcome-linked pricing are increasing execution complexity, which is creating room for providers that can combine creative capability with data infrastructure and compliance discipline in the integrated marketing services market.

Key Report Takeaways

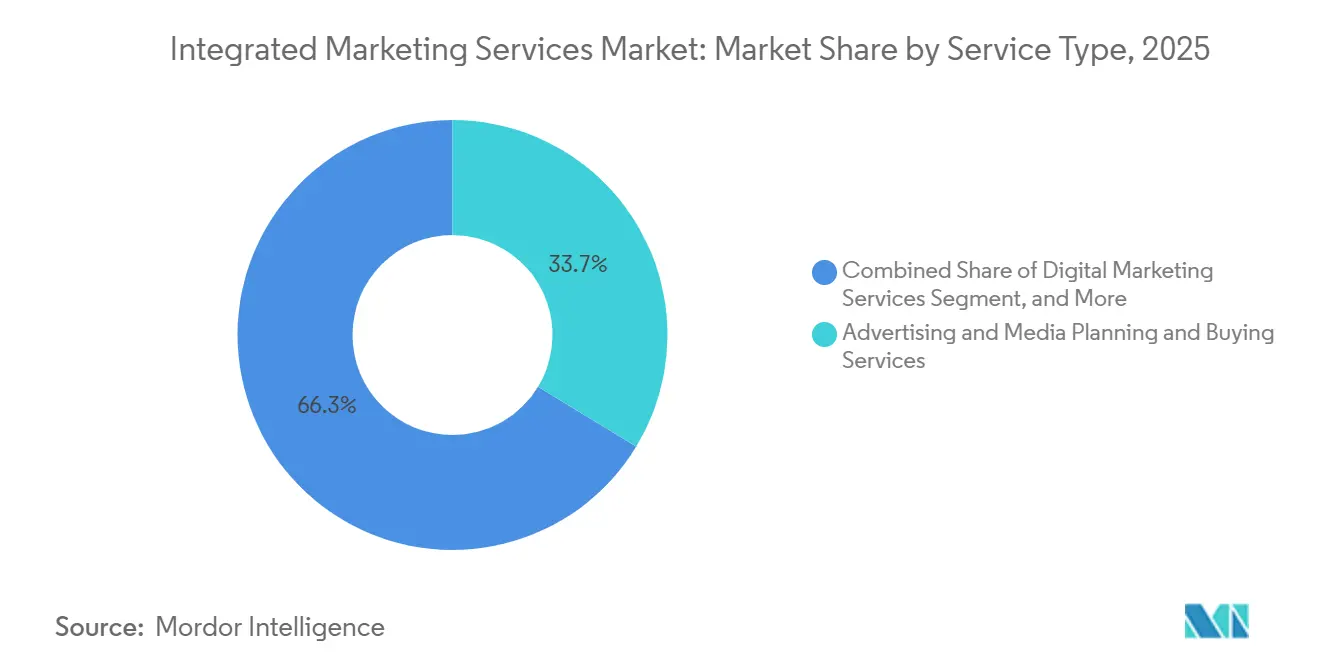

- By service type, Advertising and Media Planning and Buying Services held 33.68% share of the integrated marketing services market in 2025, while Digital Marketing Services is projected to expand at a 7.21% CAGR through 2031.

- By delivery model, Retainer-Based Engagement held 41.48% share in 2025, while Performance-Based Engagement is projected to expand at a 8.02% CAGR through 2031.

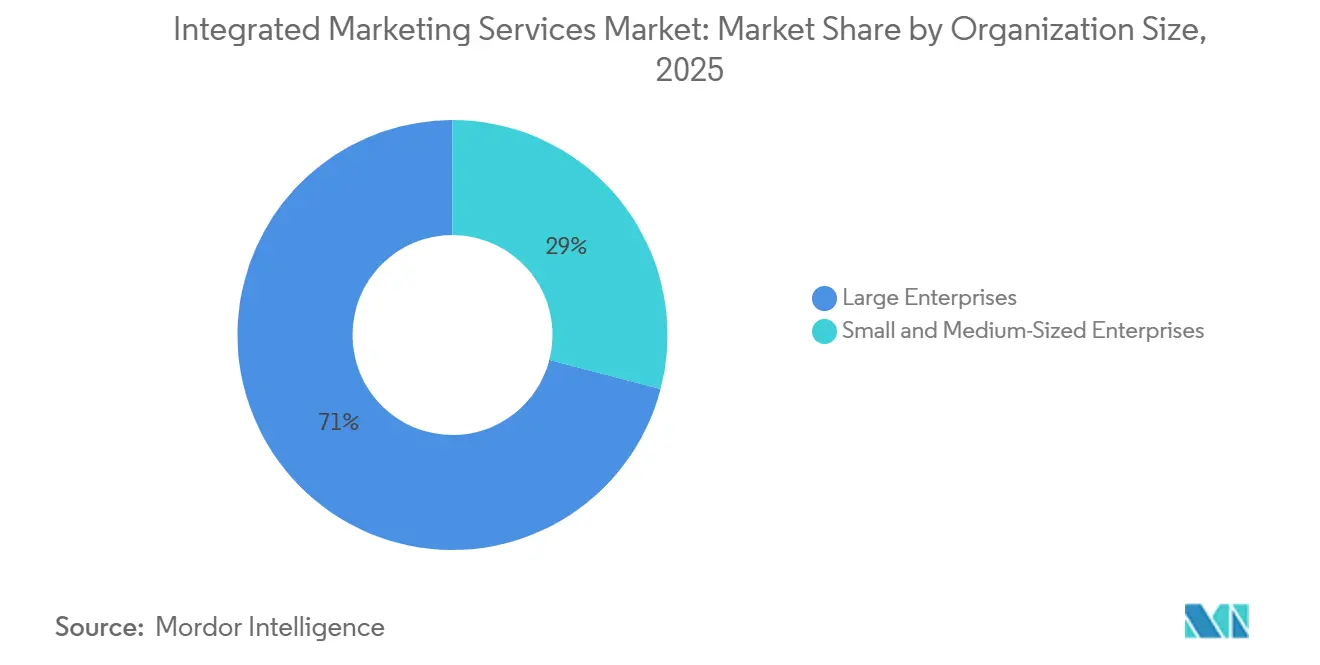

- By organization size, Large Enterprises held 70.96% of the integrated marketing services market share in 2025, while Small and Medium-Sized Enterprises are projected to expand at a 8.26% CAGR through 2031.

- By end-user industry, Retail and E-commerce held 22.74% share in 2025, while Healthcare and Life Sciences are projected to expand at an 7.96% CAGR through 2031.

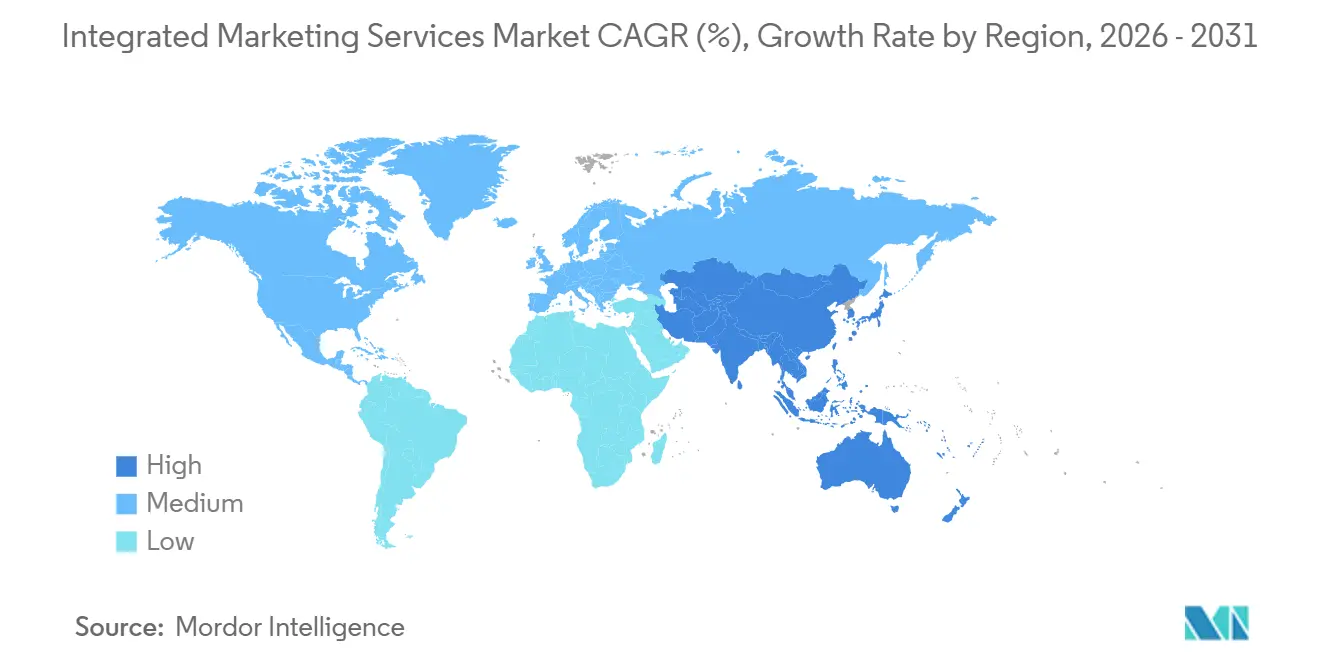

- By geography, North America held 34.46% share of the integrated marketing services market size in 2025, while Asia-Pacific is projected to expand at an 8.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Integrated Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Omnichannel Brand Consistency Mandates | +0.7% | Global, with early intensity in North America and Europe | Medium term (2-4 years) |

| Performance-Based Budget Allocation | +0.8% | North America and Western Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Artificial Intelligence-Enabled Personalization and Content Production | +1.3% | Global, enterprise-led in North America, scaling in Asia-Pacific | Medium term (2-4 years) |

| Retail Media and Creator Commerce Expansion | +1.0% | Global, strongest in North America and Asia-Pacific e-commerce markets | Medium term (2-4 years) |

| First-Party Data Collaboration and Clean-Room Adoption | +0.6% | North America and Europe, with early-stage adoption in core Asia-Pacific markets | Long term (≥ 4 years) |

| Fragmented SMB Martech Stacks Increasing Agency Outsourcing | +0.5% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Artificial Intelligence-Enabled Personalization Reshapes Agency Value Proposition

Artificial intelligence is reducing the time between audience analysis and live campaign delivery, and that shift is changing the commercial model of the integrated marketing services market. In 2026, CMOs allocated 15.3% of total marketing budgets to AI initiatives, yet only 30% of marketing organizations reported mature readiness, which left a clear execution gap for agency partners to fill. That gap matters because clients are not only looking for automation, they are also looking for agencies that can connect personalization, media, and measurement into one service structure. Publicis showed the commercial effect in 2025, when AI-powered products and services contributed 300 basis points to its 5.6% organic growth, which indicates that AI-native execution is already supporting share gains for scaled providers.[1]Publicis Groupe S.A., “Full Year 2025 Results,” Publicis Groupe Investor Relations, publicisgroupe.com The same spending shift is expanding work in adjacent areas such as CTV attribution and real-time loyalty orchestration, so retainers are becoming broader rather than smaller. For the integrated marketing services market, AI is therefore raising the value of agencies that can combine tools, talent, governance, and cross-channel execution in one operating model.

Retail Media and Creator Commerce Drive Demand for Full-Funnel Integration

Retail media is no longer treated as a narrow lower-funnel tactic, and that shift is increasing the amount of coordination brands expect from agency partners across the integrated marketing services market. Dentsu projected global retail media growth of 12.3% in 2026, which placed it among the fastest-growing digital channels and reinforced its role in shopper marketing, audience strategy, and brand building.[2]Dentsu Group Inc., “Ad Spend Growth Is Projected to Slow to 5.0% in 2026, Still Outpacing Economic Growth,” Dentsu News Releases, dentsu.comThe implication is that agencies now need to connect retailer data, content, media planning, and upper-funnel brand positioning instead of handling each area separately. Publicis reinforced that direction in 2025 by investing EUR 1 billion (USD 1.08 billion) in bolt-on acquisitions that included captiv8 and HEPMIL, which expanded its position in creator intelligence, influencer commerce, and regional digital activation.[3]Publicis Groupe S.A., “Full Year 2025 Results,” Publicis Groupe Investor Relations, publicisgroupe.com This matters because creator commerce is becoming more valuable when agencies can link audience insight to retailer activation and close the path from content to purchase. In practice, that is pushing the integrated marketing services market toward broader account scopes, larger retainers, and stronger category specialization in verticals such as health and beauty.

First-Party Data and Clean-Room Adoption Create Long-Cycle Agency Dependency

The decline of third-party data signals is pushing the integrated marketing services market toward longer-duration relationships built around first-party data collaboration and measurement design. In 2025, 66% of organizations said they were using data clean rooms in some capacity, which showed how quickly this model had moved from experimental use to mainstream planning in retail media environments. That change is important because brands are no longer commissioning isolated campaign support, they are funding multi-year programs that require identity management, governance, activation, and reporting to work together. WPP moved directly into this space through its InfoSum acquisition, while Publicis continued to position Epsilon as a clean-room-enabled identity layer that reaches 91% of U.S. adults. These moves show that large groups are competing to own the infrastructure that sits underneath media activation, not just the campaign itself. Industry standards from the IAB Tech Lab and related compliance frameworks are also shaping adoption, because brands increasingly want agency partners that can handle privacy expectations and data collaboration inside one integrated mandate.

Performance-Based Contracts Redefine Integrated Agency Pricing Architecture

Outcome-linked pricing is changing how agencies win, price, and expand business across the integrated marketing services market. Omnicom reported that Precision Marketing grew 8.6% in constant currency in 2025, which outpaced its broader agency disciplines and showed that performance-oriented work is carrying stronger momentum inside large holding companies. The 2025 CMO Survey also found that nearly three-quarters of companies rated digital marketing’s contribution to performance as strong, which supports the push toward contracts tied more directly to measured outcomes. This pricing shift matters because many clients now want proof of impact within shorter review windows, especially when internal budgets remain under pressure. Once agencies establish measurement credibility, these mandates often broaden into more stable retainer relationships that include media, content, analytics, and customer engagement. That means performance pricing is acting as both an acquisition path and a scaling tool inside the integrated marketing services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy Regulation and Signal Loss | -1% | Europe and North America, with spillover to global multi-market advertisers | Medium term (2-4 years) |

| Cross-Channel Measurement Fragmentation | -0.7% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Generative Artificial Intelligence Rights and Indemnity Exposure | -0.6% | Europe, North America, and the United Kingdom | Medium term (2-4 years) |

| Answer-Engine Search and Platform Volatility | -0.5% | Global, especially among advertisers dependent on Google and Meta policy shifts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy Regulation and Signal Loss Compress Addressable Reach

Privacy enforcement is now affecting campaign design and attribution inside the integrated marketing services market, not just legal review. As of January 2026, rules across 12 or more U.S. states required businesses to detect and honor browser-based universal opt-out signals, which reduced the practical room for default tracking assumptions in performance marketing. California also moved browser-level opt-out requirements further forward through Assembly Bill 566, which signaled a more automated and persistent consent environment. Google’s June 2026 Consent Mode change added another layer of operational pressure by making ad_storage the main control over what ad data passes from GA4 into Google Ads for EEA advertisers. The result is a smaller addressable pool for some campaigns and higher infrastructure costs for agencies that now need stronger consent management and first-party data workflows. Even so, agencies that absorb those compliance tasks into broader service bundles can turn a market restraint into a client retention advantage within the integrated marketing services market.

Generative Artificial Intelligence Rights and Indemnity Exposure Elevate Agency Liability

Generative AI is also adding a new layer of legal and insurance exposure to the integrated marketing services market. The EU AI Act’s Article 50(4) took effect on 2 August 2026 and introduced disclosure obligations for AI-generated public-facing content, with penalties that can reach EUR 15 million (USD 16.2 million) or 3% of global annual turnover. At the same time, professional indemnity insurers started adding AI-specific exclusions to coverage, which raised the risk that agencies could carry uncovered liability for copyright disputes tied to training data or output ownership. The Association of National Advertisers acknowledged the uncertainty in 2025 through its generative AI contractual rider, which recognized that enforceability and copyright protection depend heavily on the degree of human authorship. Insurance pricing has also moved higher for enterprise AI use cases, which means many fee structures still do not fully reflect the cost of compliant AI-enabled production. This is slowing aggressive adoption in some accounts, even as clients continue to expect AI-assisted speed and personalization from agency partners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Media Scale Still Leads, but Digital Expansion Is Stronger

Advertising and Media Planning and Buying Services held 33.68% share in 2025, which made it the largest revenue block in the integrated marketing services market. That position reflects the continuing central role of programmatic media, walled-garden buying, and cross-channel planning in large agency operating models. Omnicom’s Media and Advertising discipline generated USD 10 billion in 2025, or 58% of total company revenue, which showed how much scale still sits inside paid media and related execution services. Public Relations and Communications Services remained relevant because experiential work expanded 19% in constant currency for Omnicom in 2025, which pointed to a stronger overlap between earned media, content, events, and brand experience.

Brand Strategy and Creative Services faced more pressure, and Omnicom’s Branding and Retail Commerce discipline declined 15.8% in constant currency in full-year 2025, which suggested that many clients were folding creative budgets into wider media-led mandates. Digital Marketing Services is projected to advance at a 7.21% CAGR from 2026 to 2031, which makes it the fastest-growing service area in the integrated marketing services industry. Its growth reflects stronger demand for search, social commerce, connected TV, and generative engine optimization, all of which require faster testing, more data feedback, and tighter links between content and media. Content and Campaign Management Services, along with Customer Engagement, CRM and Loyalty Services, are also moving upward because brands want agency support that connects owned data, campaign activation, and retention programs inside one service structure. Compliance markers such as ISO 27001 and GDPR or CCPA readiness are becoming procurement filters as well, which means service differentiation now depends on operational assurance as much as creative or media capability in the integrated marketing services market.

By Delivery Model: Retainer Scale Holds Firm, but Performance Contracts Gain Ground

Retainer-Based Engagement accounted for 41.48% of total revenue in 2025, which made it the leading delivery model in the integrated marketing services market. This structure remains dominant because enterprise marketers still value continuity, institutional knowledge, and coordination across multiple markets and functions. Large accounts often rely on long-duration relationships when media, data, CRM, and creative activity need to move through one shared operating rhythm. Heineken’s 2025 roster decision illustrated that pattern, because the company reappointed Dentsu for global media and distributed creative work across Publicis, Stagwell, and WPP, which showed that even when clients diversify partners, they still preserve stable long-term relationships for core integrated work.

Project-Based Engagement and Hybrid Embedded Team Engagement are expanding because more mid-market clients want flexibility without signing broad multi-year agreements at the start. Hybrid structures are especially relevant when brands are building internal AI capabilities and still need agency help for execution, integration, and talent support. Publicis has leaned into that model through Marcel and related embedded talent infrastructure, which supports co-working arrangements between internal client teams and agency specialists. Performance-Based Engagement is projected to grow at a 8.02% CAGR through 2031, which shows how strongly buyers now favor outcome-linked pricing once attribution improves. For the integrated marketing services industry, that creates both upside and risk, because agencies can deepen client relationships after early performance wins, but they also take on more exposure when measurement becomes the basis for compensation.

By Organization Size: Enterprise Spending Dominates, but SME Demand Is Rising Faster

Large Enterprises held 70.96% share in 2025, which gave them the clearest weight in the integrated marketing services market size. Their position comes from larger media budgets, broader geographic footprints, more complex customer data environments, and heavier use of CRM and loyalty programs. Large advertisers also face layered compliance demands and internal system fragmentation, which makes external integration support a standing need rather than a discretionary purchase. The Omnicom and Interpublic merger directly targeted this part of the market by building a broader platform across media, data, creative, health, and customer engagement for large multinational clients.

Small and Medium-Sized Enterprises are projected to expand at a 8.26% CAGR from 2026 to 2031, which makes them the fastest-moving organization group in the integrated marketing services market. The user-supplied draft showed that 52% of U.S. SMBs outsourced marketing in 2025 and spent up to USD 3,000 per month with agency partners, which underscored the commercial importance of outsourced execution for smaller firms. This demand is rising because martech stacks have become more fragmented, data integration remains difficult, and smaller internal teams cannot manage multiple tools without outside help. The same draft also indicated that 56% of SMBs had an hour or less per day for marketing work, which reinforced the outsourcing case for packaged, easy-to-activate service models. Agencies that serve this segment well are usually the ones that simplify onboarding, show ROI quickly, and turn a scattered tool environment into a manageable service bundle inside the integrated marketing services market.

By End-User Industry: Retail Holds the Largest Base, While Healthcare Advances Fastest

Retail and E-commerce held 22.74% share in 2025, which gave the segment the largest role in the integrated marketing services market size. That leadership comes from the close connection between performance media, retail media, customer loyalty, and first-party purchase data in commerce-led businesses. Retail marketers often have stronger audience signals than many other sectors, which makes them earlier adopters of closed-loop measurement and clean-room collaboration. This also means they are large buyers of integrated services that combine campaign management, analytics, shopper marketing, CRM, and content operations in one mandate.

Healthcare and Life Sciences is projected to expand at an 7.96% CAGR through 2031, which makes it the fastest-growing end-user group in the integrated marketing services market. In 2025, global healthcare and pharma digital ad spending reached USD 24.77 billion, up 13.3% year over year, and digital video and display were expected to record a 70% budget increase in 2026. The same report showed a continued shift away from linear TV, which had accounted for 30% of healthcare ad budgets in 2021 and is projected to fall to 12% by 2027. That shift is giving an advantage to agencies that can navigate HIPAA-sensitive workflows, FDA promotional expectations, and data-backed patient engagement programs. Havas Health’s exclusive alliance with BrightInsight in February 2026 showed how providers are moving deeper into adherence, persistence, and digital health support, which makes healthcare one of the more defensible verticals in the integrated marketing services market.

Geography Analysis

North America held 34.46% of the integrated marketing services market share in 2025, and it remained the largest regional base in 2026. The region benefits from the deepest concentration of enterprise advertising budgets, the most mature programmatic infrastructure, and the headquarters presence of the largest global holding companies. Omnicom generated USD 9.1 billion from U.S. operations in 2025, or 52.7% of total company revenue, which illustrated the scale of demand concentrated in this market. Publicis also reported 5.4% organic growth in North America in 2025, with the United States contributing 57% of the group's net revenue, which confirmed the region’s structural weight in global agency performance. At the same time, the U.S. market is dealing with tighter privacy enforcement, which is pushing spend toward first-party-data-connected channels and raising the value of integrated service models that can manage compliance and activation together.

Europe remained the second-largest regional block in the integrated marketing services market, supported by digital-first media investment and mature cross-border brand activity. Publicis reported 4.2% organic growth in Europe in 2025, with Germany at 8.9% and the United Kingdom at 7.2%, which showed that demand remained healthy despite a stricter regulatory setting. GDPR, the Digital Services Act, and the AI Act are increasing compliance costs, and that is giving larger networks an advantage because they can spread governance costs across wider client portfolios. South America remained smaller in absolute size, but growth was strong in 2025 as Omnicom’s regional revenue rose 29.3% in constant currency and Publicis reported 18.7% organic growth, with Brazil and Argentina leading the improvement.

Asia-Pacific is projected to grow at an 8.20% CAGR through 2031, which makes it the fastest-growing geography in the integrated marketing services market size. The region is benefiting from stronger digital ad infrastructure, rapid retail media expansion, and platform ecosystems that support commerce, payments, and content inside connected user journeys. The supplied draft also pointed to 9.6% digital ad spending growth in India in 2026 and stronger retail media expansion across Australia, China, Japan, and India, which supports the region’s faster momentum. Southeast Asia’s commerce-media model is also becoming more important because super-app and marketplace environments are shortening the path between exposure, transaction, and measurement. Outside Asia-Pacific, the Middle East posted the strongest concentrated organic growth inside Publicis’s portfolio at 10.8% in 2025, which reflected continued brand investment in Saudi Arabia and the UAE. Africa remained the smallest geography by revenue, but mobile-first adoption in South Africa, Nigeria, and Egypt is supporting early demand for fuller agency capabilities as local brands scale and multinationals expand coverage.

Competitive Landscape

The integrated marketing services market is moderately concentrated at the top, but it is still broad and fragmented in practice. Omnicom, after the Interpublic acquisition, Publicis, WPP, and Dentsu hold a disproportionate share of global enterprise mandates, yet thousands of boutiques, regional groups, and technology-led service firms remain active across local and specialist categories. Omnicom’s merger with Interpublic closed in November 2025 and created a combined operation with trailing revenue of around USD 23.1 billion, which materially raised the scale threshold for clients looking for one partner across media, data, creative, CRM, health, and experiential services. That move increased pressure on middle-tier firms to differentiate through vertical specialization, proprietary technology, or deeper execution partnerships. It also strengthened the case for multi-capability contracts in the integrated marketing services market, because the largest buyers increasingly want fewer coordination points and stronger reporting consistency across service lines.

Publicis continued to defend its position through a technology-linked operating model rather than through scale alone. The company reported an 18.2% operating margin in 2025, which was the highest in the peer group, and it continued to build its proposition around the Marcel AI platform, the Epsilon identity layer, and the Bodhi agentic AI framework. Its 2025 acquisition activity, including captiv8 and HEPMIL, also showed how large groups are buying into creator commerce, identity, and sector-specific digital capability rather than relying only on legacy agency formats. WPP faced a tougher environment in 2025, but it responded by building out WPP Open and by maintaining a stronger focus on data collaboration and workflow modernization.

Technology differentiation is the main battlefield in 2026 across the integrated marketing services market. Stagwell expanded its partnership with The Trade Desk around agentic AI for media planning and buying, and it also partnered with Adobe to build Creative Intelligence Systems that feed audience data more directly into creative production workflows. Industry bodies are shaping the rules of competition as well, because data transparency standards and generative AI contract templates are starting to influence how agencies structure partnerships, approvals, and accountability. White space remains strongest in the mid-market, where many clients still cannot find one provider that combines AI-enabled execution, clean-room measurement, and outcome-linked pricing at a practical scale. Consulting-linked firms such as Accenture Song and Deloitte Digital are relevant at the technology and transformation layer, while Cognizant, Infosys, TCS, and Capgemini remain important in marketing operations and experience platforms. By contrast, IBM and Tech Mahindra appear less representative of full-spectrum integrated marketing competition, because their positioning is more closely tied to enterprise technology services than to end-to-end agency-led brand execution.

Integrated Marketing Services Industry Leaders

Omnicom Group Inc.

Publicis Groupe S.A.

WPP plc

Dentsu Group Inc.

Havas N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Stagwell built a unified AI-powered TV advertising infrastructure by partnering with FreeWheel, integrating FreeWheel's Curation Hub and Buyer Cloud into Stagwell's media acquisition layer through Stagwell Curate, a centralized deal marketplace for premium video and CTV inventory. The integration gives advertisers direct access to streaming advertising infrastructure with greater transparency and faster activation, positioning Stagwell as a scaled alternative to holding company media operations in the CTV market.

- March 2026: Stagwell's Code and Theory formalized a strategic partnership with Adobe to deploy Creative Intelligence Systems across financial services, B2B, sports, and media and entertainment verticals, combining Adobe Experience Platform and GenStudio for Performance Marketing with Code and Theory's creative and technology expertise.

- February 2026: Havas Health announced an exclusive global agency partnership with BrightInsight, the leading biopharma digital persistence and adherence platform, creating the first integrated solution combining healthcare marketing strategy with compliant, scalable digital health tools for patient post-prescription retention. The deal expands Havas Health's addressable market into health technology services, positioning it to compete against consulting-led healthcare marketing offerings.

- February 2026: Omnicom detailed its IPG post-merger integration strategy, doubling its cost-synergy target to USD 1.5 billion over three years from an original USD 750 million, with USD 900 million targeted in 2026. The revised target includes USD 1 billion from labor-cost savings and the remainder from real estate and operational consolidation, alongside accelerated deployment of the Omni intelligence platform integrating Acxiom Real iD and Flywheel Commerce Cloud.

Global Integrated Marketing Services Market Report Scope

The Integrated Marketing Services Market refers to agencies and service providers that combine brand strategy, creative, media, digital, PR, analytics, and customer engagement into one coordinated offering. It focuses on delivering a consistent message and customer experience across multiple channels and touchpoints.

The Integrated Marketing Services Market Report is Segmented by Service Type (Brand Strategy and Creative Services, Advertising and Media Planning and Buying Services, Digital Marketing Services, Public Relations and Communications Services, Content and Campaign Management Services, and Customer Engagement, Customer Relationship Management and Loyalty Services), Delivery Model (Project-Based Engagement, Retainer-Based Engagement, Performance-Based Engagement, and Hybrid and Embedded Team Engagement), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises, and More), End-User Industry (Retail and E-commerce, Consumer Goods and Beauty, Media and Entertainment, IT and Telecom, BFSI, and Healthcare and Life Sciences), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Brand Strategy and Creative Services |

| Advertising and Media Planning and Buying Services |

| Digital Marketing Services |

| Public Relations and Communications Services |

| Content and Campaign Management Services |

| Customer Engagement, Customer Relationship Management and Loyalty Services |

| Other Service Types |

| Project-Based Engagement |

| Retainer-Based Engagement |

| Performance-Based Engagement |

| Hybrid and Embedded Team Engagement |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Retail and E-commerce |

| Consumer Goods and Beauty |

| Media and Entertainment |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Brand Strategy and Creative Services | |

| Advertising and Media Planning and Buying Services | ||

| Digital Marketing Services | ||

| Public Relations and Communications Services | ||

| Content and Campaign Management Services | ||

| Customer Engagement, Customer Relationship Management and Loyalty Services | ||

| Other Service Types | ||

| By Delivery Model | Project-Based Engagement | |

| Retainer-Based Engagement | ||

| Performance-Based Engagement | ||

| Hybrid and Embedded Team Engagement | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Retail and E-commerce | |

| Consumer Goods and Beauty | ||

| Media and Entertainment | ||

| IT and Telecom | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the integrated marketing services market size in 2026 and what will it reach by 2031?

The integrated marketing services market stood at USD 424.73 billion in 2026 and is projected to reach USD 595.56 billion by 2031, growing at a 6.94% CAGR.

Which service segment is growing the fastest through 2031?

Digital Marketing Services is the fastest-growing service segment, with a projected 7.21% CAGR from 2026 to 2031.

Which delivery model is seeing the strongest momentum?

Performance-Based Engagement is advancing the fastest, with a projected 8.02% CAGR, as clients increasingly prefer outcome-linked contracts.

Which customer group is expanding fastest for agency partners?

Small and Medium-Sized Enterprises are the fastest-growing organization segment, with a 8.26% CAGR through 2031, driven by limited internal capacity and fragmented marketing tools.

Which end-user vertical is creating the strongest growth opportunity?

Healthcare and Life Sciences is the fastest-growing end-user segment at an 7.96% CAGR, supported by higher digital ad spending and specialized compliance needs.

Which region offers the strongest growth outlook over the forecast period?

Asia-Pacific is the fastest-growing geography, with an 8.20% CAGR through 2031, supported by stronger digital infrastructure, retail media expansion, and commerce-led platform ecosystems.

Page last updated on: