Marketing Technology Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 90.41 Billion |

| Market Size (2031) | USD 155.59 Billion |

| Growth Rate (2026 - 2031) | 11.47% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marketing Technology Services Market Analysis by Mordor Intelligence

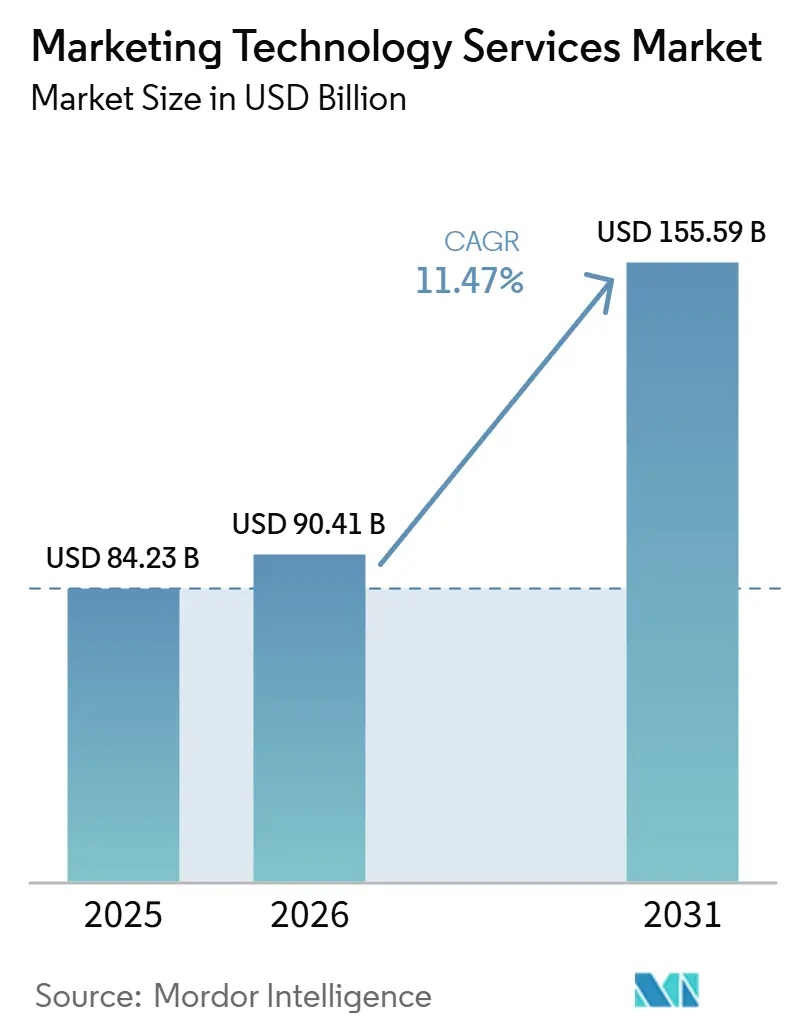

The Marketing Technology Services Market size is projected to expand from USD 84.23 billion in 2025 and USD 90.41 billion in 2026 to USD 155.59 billion by 2031, registering a CAGR of 11.47% between 2026 and 2031. Growth is being shaped by wider use of AI-led orchestration, tighter control over first-party data, and a clear move toward managed service contracts that link delivery to business outcomes. Buyers are also trying to simplify procurement, but the growing number of connected platforms, data rules, and workflow changes is making implementation harder, not easier. That combination is driving demand for service providers that can manage integration, data governance, enablement, and ongoing optimization within a single delivery model. Privacy-led operating changes are also pushing brands to rebuild activation processes, keeping service demand active beyond the initial platform rollout. As a result, the Marketing Technology Services Market is moving toward longer engagements that blend consulting, operations, compliance support, and AI tuning across multiple platforms.

Key Report Takeaways

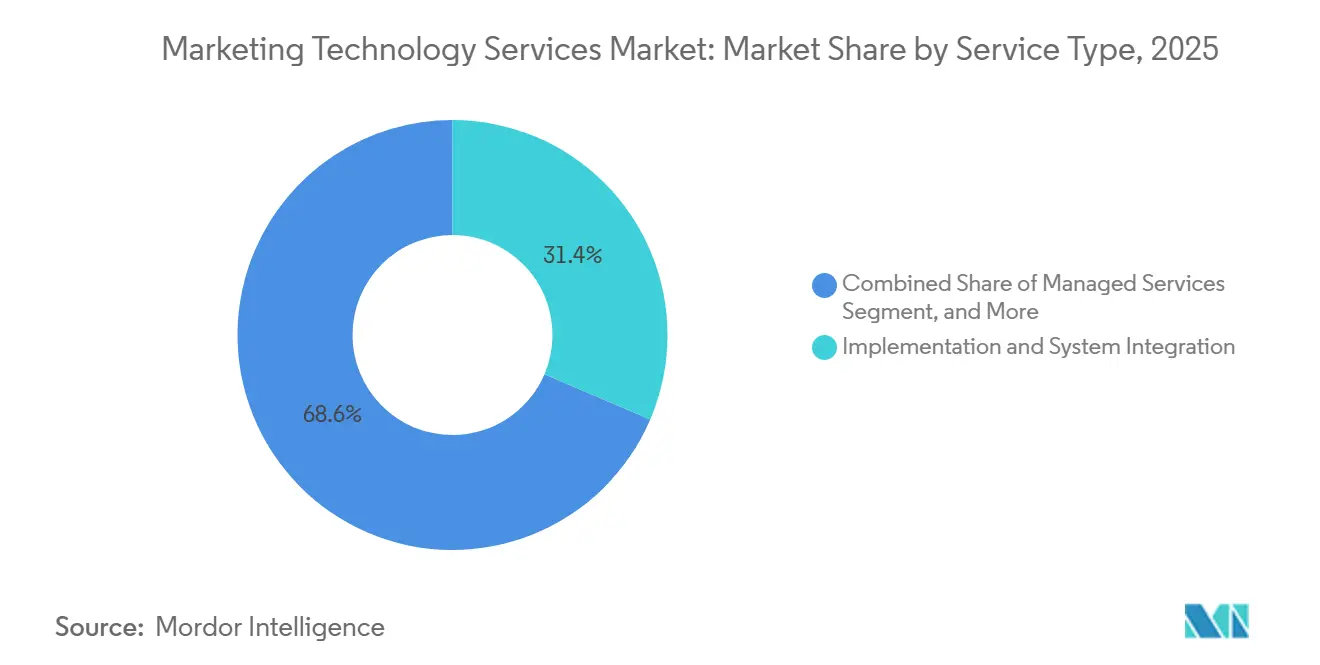

- By service type, implementation and system integration held 31.42% share in the Marketing Technology Services Market 2025, while managed services are projected to expand at a 14.83% CAGR through 2031.

- By deployment, cloud-based delivery held 68.24% share in 2025, while hybrid deployment is projected to grow at a 13.69% CAGR through 2031.

- By technology, marketing automation platforms accounted for 26.71% of the market share in 2025, while customer data platforms are projected to grow at a 15.42% CAGR through 2031.

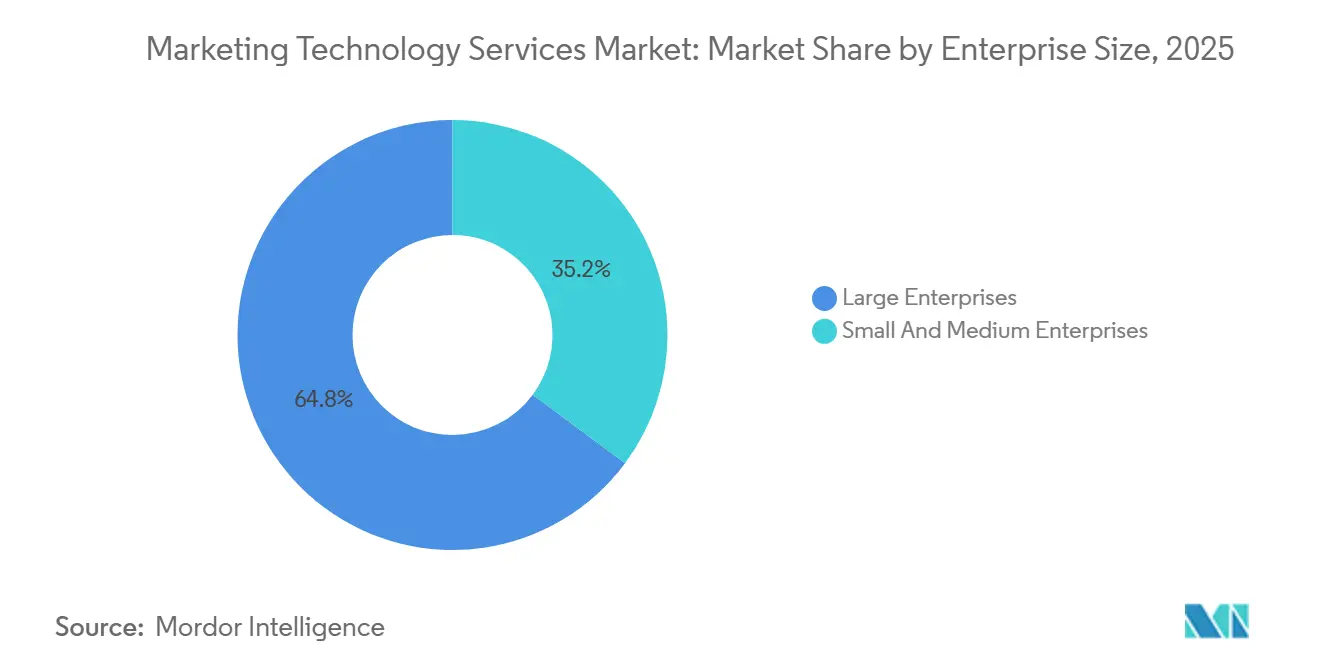

- By enterprise size, large enterprises held 64.83% share in 2025, while small and medium enterprises are projected to grow at a 13.27% CAGR through 2031.

- By end-user industry, retail and e-commerce accounted for 24.19% of the market share in 2025, while healthcare and life sciences are projected to expand at a 14.81% CAGR through 2031.

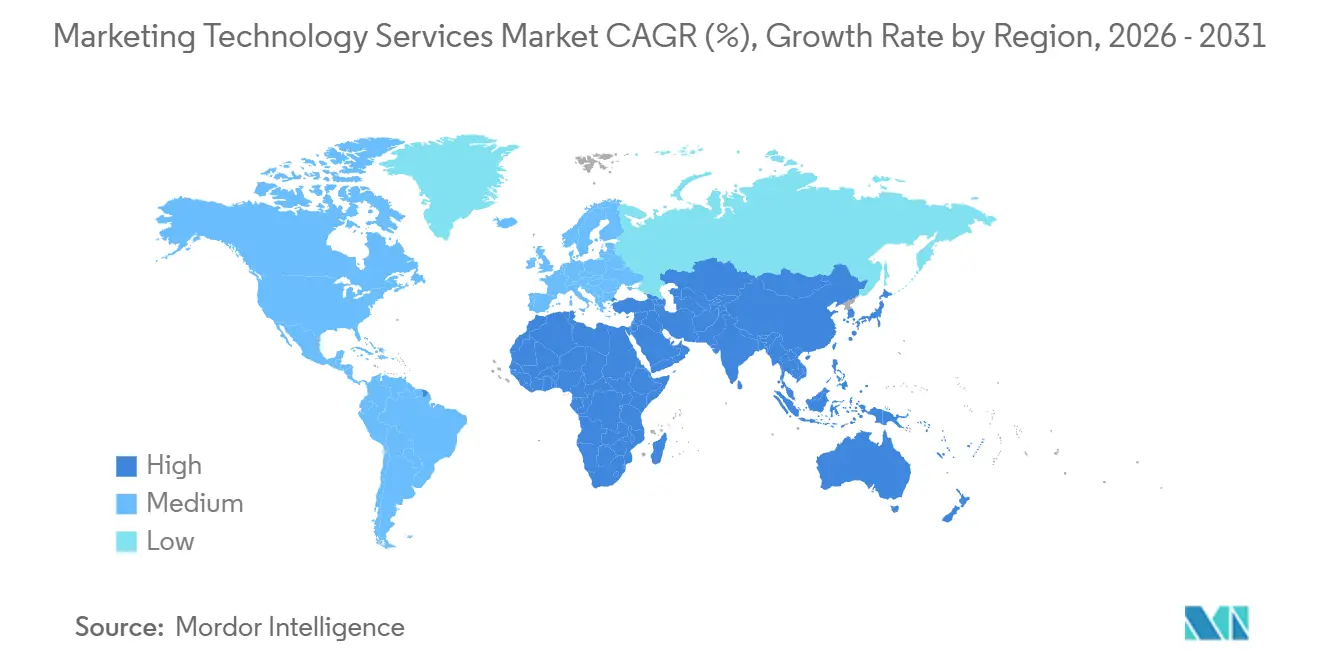

- By geography, North America held 34.62% of the Marketing Technology Services Market share in 2025, while Asia-Pacific is projected to grow at a 13.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marketing Technology Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI-Led Campaign Orchestration | +3.2% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising Demand for Unified Customer Data Activation | +2.5% | Global, accelerated in North America, Europe, and East Asia | Short term (≤ 2 years) |

| Expansion of First-Party Data and Consent-Driven Personalization | +1.7% | Global, with EU and Asia-Pacific compliance mandates most acute | Medium term (2-4 years) |

| Omnichannel Measurement and Attribution Migration | +1.4% | North America and Europe core, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Growth of Embedded Martech Services in Enterprise Transformation Programs | +1.1% | North America, Europe, and Asia-Pacific enterprise hubs | Long term (≥ 4 years) |

| Verticalized Compliance-Ready Marketing Operations | +0.8% | North America in healthcare and BFSI, and Europe in regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI-Led Campaign Orchestration

AI-led orchestration is changing marketing services from project-based campaign setup to continuous operations that require closer platform oversight, stronger workflow controls, and more frequent model tuning. Firstsource Solutions partnered with Typeface in April 2026 to launch Agentic Marketing Services, a full-stack service for transforming and operating AI-native marketing systems in regulated environments.[1]Firstsource Solutions, “Firstsource Partners with Typeface to Launch Agentic Marketing Services,” Newswire, newswire.ca Salesforce also expanded this shift when Agentforce Marketing exposed campaign management functions as model context protocol tools, which lets teams execute journeys from connected interfaces instead of relying only on periodic manual setup. The IAB stated that two-thirds of ad buyers in 2026 are focused on deploying AI agents for campaign execution, which shows that demand is moving quickly from experimentation to scaled deployment. That pattern gives service providers a larger role because enterprises now need partners who can train, govern, and improve AI agents in line with brand rules, customer data structures, and channel-level execution standards. In turn, the Marketing Technology Services Market is drawing more value from always-on optimization work than from one-time deployment alone.[2]Salesforce, “Salesforce Puts an AI Marketing Team in Every Marketer's Hands,” Salesforce News, salesforce.com

Rising Demand for Unified Customer Data Activation

The move toward unified customer data activation is raising the technical depth of service engagements because brands now need stronger links between customer profiles, analytics environments, and campaign execution layers. The CDP Institute reported that composable and warehouse-native CDP vendors grew headcount by 7.8% in the second half of 2025, compared with an industry average of 1.3%, and more than one-quarter of platforms now support warehouse-centric architecture.[3]CDP Institute, “CDP Beyond Marketing, Unifying Data Across the Organization,” CDP Institute, cdpinstitute.org That split creates two service tracks: one focused on faster deployment of packaged platforms, and another on custom identity logic, reverse ETL, activation connectors, and long-term data engineering support. Enterprises that choose composable architectures often need broader integration planning because profile resolution, segmentation logic, and downstream activation rules cannot be standardized across every deployment. Service providers that can connect data unification with execution design are therefore moving higher in the buying cycle, especially when clients want fewer vendors managing a larger share of the operating stack. This keeps the Marketing Technology Services Market closely tied to data architecture decisions rather than solely to software deployment.

Expansion of First-Party Data And Consent-Driven Personalization

First-party data programs are becoming more central to marketing operations because privacy limits have reduced the room for broad third-party targeting and raised the value of direct, permission-based customer records. Bitkom found in 2026 that 84% of companies see AI as the most influential trend through 2027, while 76% expect marketing automation to gain importance, and 34% cite inadequate AI integration as an internal challenge.[4]Bitkom, “Marketing Im Digitalen Wandel, Zwischen Effizienz, Automatisierung Und Wettbewerb,” Bitkom, bitkom.org Those gaps grow larger when consent records, purpose restrictions, and customer permissions do not transfer cleanly across platforms, breaking personalization logic and weakening campaign execution. As a result, service providers are being asked to design data capture, consent governance, audience activation, and customer request workflows as one connected operating model rather than as separate tasks. This change expands the value of implementation work because delivery now extends beyond platform setup into long-running governance and process management. The Marketing Technology Services Market is therefore benefiting from a deeper link between compliance architecture and day-to-day personalization work.

Omnichannel Measurement and Attribution Migration

Measurement models are shifting because privacy changes, signal loss, and weaker cookie-based tracking have reduced confidence in older attribution methods across major digital channels. Accenture Song launched Marketing Investment Navigator in 2026 as an AI-native, unified measurement platform, and early deployments showed business-outcome improvements of 17% or more at twice the speed of conventional approaches. The IAB also reported that only 2% of marketers currently use media mix modeling, incrementality testing, and attribution together, indicating how much operational change remains ahead for most organizations. This gap creates steady demand for specialists who can redesign data flows, update tagging structures, build new testing frameworks, and retrain internal teams on different measurement logic. Projects in this area tend to run longer because they involve reporting systems, budget decisions, performance governance, and channel planning simultaneously. That gives the Marketing Technology Services Market a sustained growth path in analytics integration and measurement operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Tool Stacks Increase Integration and Governance Costs | -2.1% | Global, most acute in large enterprise-heavy markets such as North America and Europe | Short term (≤ 2 years) |

| Data Privacy and Cross-Border Consent Constraints Limit Activation Depth | -1.7% | Europe, North America at the state level, and Asia-Pacific including India and Australia | Medium term (2-4 years) |

| Underinvestment in Attribution and Experimentation Talent Slows ROI Realization | -1.0% | Global, with added pressure in emerging Asia-Pacific markets | Medium term (2-4 years) |

| Vendor Overlap and License Sprawl Delay Suite Consolidation Decisions | -0.7% | North America and Europe enterprise segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Tool Stacks Increase Integration and Governance Costs

Tool fragmentation remains a real restraint because every extra platform adds another layer of data movement, governance review, implementation effort, and operating overhead. Fivetran reported in 2026 that enterprises allocate 14% of total data budgets, or USD 4.2 million, to data integration, while organizations run an average of 328 data pipelines maintained by up to 60 full-time engineers, and only 27% said their data investments exceeded return expectations. In marketing environments, this pressure becomes harder to control when campaign tools, data warehouses, analytics products, and consent systems all need to exchange usable information in near real time. Buyers often respond by delaying new implementation mandates until they can review total operating cost, vendor overlap, and the effort needed to unwind older connections. Service providers can still benefit from rationalization projects, but these projects usually require more discovery work and broader governance review before execution begins. That slows decision speed and creates a practical limit on how quickly the Marketing Technology Services Market can convert demand into booked revenue.

Data Privacy And Cross-Border Consent Constraints Limit Activation Depth

Cross-border consent limits are reducing the depth of audience activation that providers can offer, especially when campaigns depend on customer records moving across multiple legal jurisdictions. California Management Review noted in 2025 that tightening global data privacy rules are forcing businesses to rethink their data strategy at a fundamental level, especially as AI systems need clean, clearly permitted customer data to work well. This means implementation planning now starts with questions about legal basis, permission scope, local storage, and customer rights rather than with campaign design alone. Providers must also build more time into discovery, as cross-border reviews often change segmentation logic, targeting depth, measurement design, and allowed activation paths. Those changes do not remove demand for services, but they do narrow some premium use cases and add friction to multinational rollouts. For the Marketing Technology Services Market, privacy-led complexity is therefore both a source of demand and a limit on execution speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Services Gain Ground As Operating Complexity Rises

Implementation and system integration accounted for 31.42% of the Marketing Technology Services Market size in 2025, reflecting the significant effort still required to connect CRM systems, data platforms, automation tools, analytics layers, and content workflows into a single usable operating stack. This segment remained large because most enterprises still need partner support when replacing older tools, adding AI capabilities, or expanding into more connected activation models. Consulting services also stayed relevant because buyers often need external help to decide vendor architecture, process design, governance ownership, and rollout sequencing before technical work begins. Migration and modernization services added another layer of demand as companies moved from older point solutions toward more unified environments with stronger data controls. Support and maintenance continued to matter because stable operation across multiple tools depends on ongoing issue resolution, workflow refinement, and user adoption after the initial implementation phase.

Managed services are projected to grow at a 14.83% CAGR through 2031, indicating that buyers increasingly want external partners to handle daily operations, platform administration, audience management, and AI tuning rather than building those skills in-house. This shift is especially visible where marketing teams need continuous optimization across many campaigns, channels, and customer data sources rather than periodic technical support. Providers are responding by bundling operations, performance monitoring, compliance checks, and strategic reviews into broader contracts that last longer than older implementation-heavy engagements. Training and enablement remain important because vendor product cycles are releasing new AI functions quickly, and internal teams need structured support to use those features well. In the Marketing Technology Services Market, service type growth is therefore moving from one-off project delivery toward recurring operating partnerships with deeper accountability for outcomes.

By Deployment: Hybrid Models Expand As Data Control And Flexibility Must Coexist

Cloud-based deployment held a 68.24% share in 2025, supported by ease of user onboarding, faster updates, modular pricing, and a long-standing enterprise comfort with software-as-a-service delivery. This model remained the default option for many brands because it lowers infrastructure burden and shortens setup time when teams want to launch campaigns across email, commerce, social, search, and analytics systems. It also fits well with the broader shift toward managed services, since remote administration and continuous optimization are easier to standardize in cloud environments. On-premises deployment still holds importance in regulated use cases, where internal controls, data residency, and tighter review processes remain more important than speed. These conditions kept deployment choices varied even as cloud usage stayed clearly dominant across the broader Marketing Technology Services Market.

Hybrid deployment is projected to grow at a 13.69% CAGR through 2031, which reflects the fact that many global organizations now need both local data control and access to cloud-native AI capabilities. This is no longer a temporary compromise, because large organizations often run customer records in tightly controlled environments while using cloud services for orchestration, content generation, measurement, or collaboration. That structure increases service demand because providers must manage connectors, workflow rules, access controls, and performance standards across multiple environments simultaneously. It also increases the value of delivery partners who understand legal review, system interoperability, and phased rollout planning across multiple jurisdictions. The Marketing Technology Services Market is therefore seeing hybrid architecture emerge as a durable service opportunity rather than a transitional deployment stage.

By Technology: Customer Data Platforms Deepen Service Scope Beyond Activation

Marketing automation platforms held a 26.71% share in 2025, reflecting their central role in campaign execution, journey management, segmentation, lead nurturing, and recurring customer communication. These platforms remained the main operating layer for many enterprises because they connect planning decisions with real campaign delivery across owned and paid channels. Social media management platforms, analytics tools, content management systems, and SEO and SEM platforms also continued to drive service demand, but automation platforms remained closer to daily execution and therefore accounted for the largest revenue share. This leadership also reflects the fact that implementation often begins where campaigns are launched, measured, and adjusted most frequently. Across the Marketing Technology Services Market, technology spending most directly converts into services when tools sit close to campaign workflows and customer engagement activity.

Customer data platforms are projected to grow at a 15.42% CAGR through 2031, giving them the strongest expansion rate across the technology categories covered in the input. The CDP Institute found that composable and warehouse-native providers expanded faster than the broader field in late 2025, supporting the view that architecture is moving toward more flexible, technically demanding deployment models. That change increases service scope because providers must build identity logic, activation pathways, governance rules, and maintenance processes that are often specific to each client environment. Customer data platforms also sit at the center of first-party data strategies, which means providers are expected to integrate data quality, permission controls, and downstream campaign use within a single operating framework. In practical terms, this makes the Marketing Technology Services Market more dependent on deep data engineering and governance capabilities than on simple product configuration alone.

By Enterprise Size: Smaller Firms Accelerate Through Lower-Cost Entry Paths

Large enterprises held a 64.83% share in 2025, supported by larger technology estates, greater integration needs, longer procurement cycles, and multi-year service contracts that deliver greater revenue per client. These organizations often use a broader set of CRM, analytics, commerce, automation, and content systems, keeping service requirements active well after the initial rollout. Their scale also makes governance more important because regional teams, external agencies, customer data rules, and brand controls must all operate within a common framework. As AI functions become more embedded across marketing workflows, large organizations are more likely to fund external specialists to manage complex deployment and oversight requirements. For these reasons, enterprise-scale demand continues to anchor the revenue base of the Marketing Technology Services Market.

Small and medium enterprises are projected to grow at a 13.27% CAGR through 2031, helped by cloud subscriptions, modular buying, and simpler onboarding paths from vendors such as HubSpot and Klaviyo. These firms are entering the category with clearer intent because lower entry costs now make advanced automation and customer engagement tools more accessible than in earlier years. The SBE Council found in March 2026 that 81% of small business AI tool users consider AI important to competitiveness and growth, while 90% said they are confident in their ability to adopt new digital tools. That combination supports demand for lighter implementation work, packaged enablement, and managed support models designed around smaller internal teams with limited technical capacity. In the Marketing Technology Services Market, SME growth is therefore broadening the client base, even though average contract values remain lower than those in large enterprises.

By End-User Industry: Healthcare Builds Momentum As Compliance Work Becomes More Specialized

Retail and e-commerce held 24.19% share in 2025, which made it the largest end-user segment within the Marketing Technology Services Market size because this vertical depends heavily on customer acquisition, retention, conversion optimization, and fast campaign response. Retail brands also tend to move quickly on personalization, customer data activation, and multichannel orchestration because these tools directly affect revenue performance and customer lifetime value. BFSI remained an important segment because financial marketers face tighter standards for customer communications, approval workflows, and data handling across acquisition and retention programs. The Reserve Bank of India issued responsible business conduct directions in 2025 that included detailed requirements on advertising, marketing, and sales practices for all-India financial institutions, which support continued demand for compliance-ready operating models in regulated environments. IT and telecom, media and entertainment, industrial manufacturing, and government and public administration also contributed meaningfully, although service mix varied according to regulatory intensity, customer engagement complexity, and internal digital maturity.

Healthcare and life sciences are projected to grow at a 14.81% CAGR through 2031, making it the fastest-expanding end-user segment in the input market, as compliance and patient data controls become more central to marketing execution. Providers in this area are being asked to support first-party data design, compliant communication workflows, and careful governance around campaign content, analytics, and personalization activity. Elpida launched an AI-powered marketing compliance platform for healthcare in March 2026, designed to monitor risks related to FDA, FTC, CMS, HIPAA, and CCPA rules across marketing assets in real time. That move shows how compliance support is becoming a productized growth layer within service delivery rather than a separate advisory step. As a result, the Marketing Technology Services Market is experiencing stronger expansion in healthcare, where regulatory review and digital engagement must now operate in tandem.

Geography Analysis

North America held 34.62% of the Marketing Technology Services Market share in 2025, maintaining its leading position due to dense enterprise martech adoption, mature partner networks, and generally higher implementation speed than in most other regions. The United States remained the main demand center because large brands continue to outsource integration, campaign operations, and optimization work to shorten launch cycles and improve execution consistency across channels. State-level privacy expansion also keeps governance work active, which supports longer service engagements tied to data controls and permitted activation. Canada added to regional demand through financial services and public-sector programs that require structured digital engagement and tighter operational oversight. South America remained smaller in absolute terms, but digital commerce growth and wider adoption of performance marketing tools continued to open more room for implementation and managed support across the Marketing Technology Services Market.

Asia-Pacific is projected to grow at a 13.94% CAGR through 2031, making it the fastest-growing region in the Marketing Technology Services Market and the clearest source of new expansion outside North America. India plays a dual role as both a major technology services delivery hub and a domestic growth market, where brands are increasing investment in consent-aware customer engagement. Southeast Asia is also supporting demand as platform-led commerce grows and merchants need stronger analytics, measurement, and customer data capabilities to manage performance across large online marketplaces. Japan, China, and South Korea add another layer of demand, as brands in those markets are increasing cloud-native deployments and AI-driven marketing execution while balancing local operating requirements. The result is a region where service growth is driven by both local adoption and offshore delivery strength, giving the Marketing Technology Services Market a broader base for expansion.

Europe remained important because privacy rules, data interoperability requirements, and underused martech capabilities continue to create demand for implementation refinement, training, and managed upgrades. Bitkom reported in 2026 that 76% of surveyed companies expect marketing automation to grow in importance, and 34% see inadequate AI integration as an internal challenge, underscoring the continued need for external support in execution and enablement. The Middle East is gaining relevance as Saudi Arabia and the UAE continue broader digital transformation efforts that encourage enterprise platform deployment and local implementation support. Africa remains earlier stage, but mobile-first commerce growth and rising digital engagement are steadily widening the long-term opportunity for the Marketing Technology Services Market.

Competitive Landscape

The Marketing Technology Services Market remains moderately consolidated at the platform level, where large software ecosystems influence buying patterns, but the services layer is still highly fragmented across system integrators, specialist consultancies, agency networks, and managed service firms. This structure means no single provider controls service delivery, even when a few platform brands shape much of the underlying technology environment. Adobe expanded its partner ecosystem in April 2026 through standardization agreements with dentsu, Havas, Omnicom, Publicis, Stagwell, and WPP for CX Enterprise, demonstrating how leading platforms are channeling more enterprise work through accredited delivery partners. Salesforce also deepened its position through AI-focused expansion, including the completed acquisition of Qualified in April 2026 and the signed agreement to acquire Fin in June 2026. These moves make the competitive environment more demanding, as service partners now need stronger certifications, deeper product knowledge, and clearer execution value to stay relevant in large enterprise deals.

Mid-tier competitors are responding through specialization, faster product cycles, and built-in AI features that can reduce the amount of low-value manual work handled by service providers. Braze launched BrazeAI Operator, BrazeAI Agent Console, and Braze Creative Studio in April 2026, signaling a stronger push to automate campaign creation, content generation, and workflow adjustments. Klaviyo opened its Composer AI marketing agent to public beta in July 2026 and connected it with Customer Agent around the same real-time customer profile, which reinforced the push toward more autonomous execution in the mid-market. HubSpot also introduced HubSpot AEO and expanded Prospecting Agent capabilities in April 2026, showing that growth-stage platforms are using AI to widen their operating reach across planning, visibility, and sales-connected marketing workflows. As these functions become more automated inside the platforms themselves, service providers are being pushed toward higher-value work in orchestration design, governance, data architecture, and cross-platform operating support.

Specialist vendors and boutique service firms still have room to compete because many buyers need focused expertise in measurement, content operations, analytics, regulated workflows, or customer journey design that bundled platforms do not fully solve. Competitive positioning is also improving for providers that can prove privacy-aware delivery, secure architecture, and dependable execution in regulated sectors. That keeps the Marketing Technology Services Market open to a large field of challengers, even as platform ecosystems become more structured. The overall result is a market where large software vendors set the direction, but thousands of service-led firms still compete for execution share, keeping concentration moderate rather than tight.

Marketing Technology Services Industry Leaders

Adobe Inc.

Salesforce, Inc.

Oracle Corporation

HubSpot, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Klaviyo opened its Composer AI marketing agent to public beta alongside major enhancements to Customer Agent. Composer generates, optimizes, and recommends full marketing campaigns and flows from a single prompt, with both agents operating from the same real-time customer profile. The platform serves more than 193,000 paying customers as of the launch date.

- June 2026: Salesforce signed a definitive agreement to acquire Fin, a customer agent platform, to accelerate autonomous agent delivery across enterprise operations. The deal is expected to close in Salesforce's fiscal Q4 2027 and will expand Agentforce's reach into AI-first customer service and marketing workflows.

- April 2026: Adobe completed the acquisition of Semrush Holdings, a leading brand visibility platform. The move strengthens CX Enterprise's discoverability and conversion capabilities as AI interfaces become a primary channel for brand discovery and customer engagement.

- April 2026: Braze launched BrazeAI Operator, BrazeAI Agent Console, and Braze Creative Studio, a suite of agentic AI capabilities designed to automate campaign creation, content generation, and workflow adaptation. Early deployments showed a 90% increase in booking conversion rate and an 81% reduction in unsubscribes among pilot clients.

Global Marketing Technology Services Market Report Scope

The marketing technology services market encompasses the range of professional and managed services required to successfully deploy, integrate, operate, and optimize marketing technology (MarTech) stacks. This market excludes the actual software licenses or platform subscriptions, focusing instead on the human expertise and outsourced operations needed to support technologies such as marketing automation platforms, customer data platforms (CDPs), analytics and attribution tools, social media management platforms, content management systems (CMS), and SEO/SEM platforms.

The Marketing Technology Services Market Report is Segmented by Service Type (Consulting Services, Implementation and System Integration, Managed Services, Support and Maintenance, Training and Enablement, and Migration and Modernization Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Technology (Marketing Automation Platforms, Customer Data Platforms (CDPs), Analytics and Attribution Platforms, Social Media Management Platforms, Content Management Systems (CMS), and SEO and SEM Platforms), Enterprise Size (Large Enterprises, and Small And Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Consulting Services |

| Implementation and System Integration |

| Managed Services |

| Support and Maintenance |

| Training and Enablement |

| Migration and Modernization Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Marketing Automation Platforms |

| Customer Data Platforms (CDPs) |

| Analytics and Attribution Platforms |

| Social Media Management Platforms |

| Content Management Systems (CMS) |

| SEO and SEM Platforms |

| Large Enterprises |

| Small And Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Consulting Services | ||

| Implementation and System Integration | |||

| Managed Services | |||

| Support and Maintenance | |||

| Training and Enablement | |||

| Migration and Modernization Services | |||

| By Deployment | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Technology | Marketing Automation Platforms | ||

| Customer Data Platforms (CDPs) | |||

| Analytics and Attribution Platforms | |||

| Social Media Management Platforms | |||

| Content Management Systems (CMS) | |||

| SEO and SEM Platforms | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By End-User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Media and Entertainment | |||

| Industrial Manufacturing | |||

| Government and Public Administration | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the Marketing Technology Services Market?

The Marketing Technology Services Market was valued at USD 84.23 billion in 2025, is projected at USD 90.41 billion in 2026, and is forecast to reach USD 155.59 billion by 2031 at an 11.47% CAGR.

What is driving demand for marketing technology services in 2026?

Demand is being driven by AI-led campaign orchestration, first-party data activation, consent-led personalization, and the need to rebuild measurement models as older attribution methods lose effectiveness.

Which service type leads revenue and which one is growing the fastest?

Implementation and system integration led with 31.42% share in 2025, while managed services is projected to record the fastest growth at a 14.83% CAGR through 2031.

Which technology area is expanding the fastest?

Customer data platforms are projected to grow at a 15.42% CAGR through 2031 because brands need stronger identity resolution, activation logic, and first-party data governance.

Which region is growing the fastest in the Marketing Technology Services Market?

Asia-Pacific is projected to grow the fastest at a 13.94% CAGR through 2031, supported by rising local adoption, regulatory change, and strong regional delivery capabilities.

Which end-user segment offers the strongest growth opportunity?

Healthcare and life sciences is projected to expand at a 14.81% CAGR through 2031 as compliant patient engagement, first-party data programs, and marketing governance become more specialized.

Page last updated on: