Video Content Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

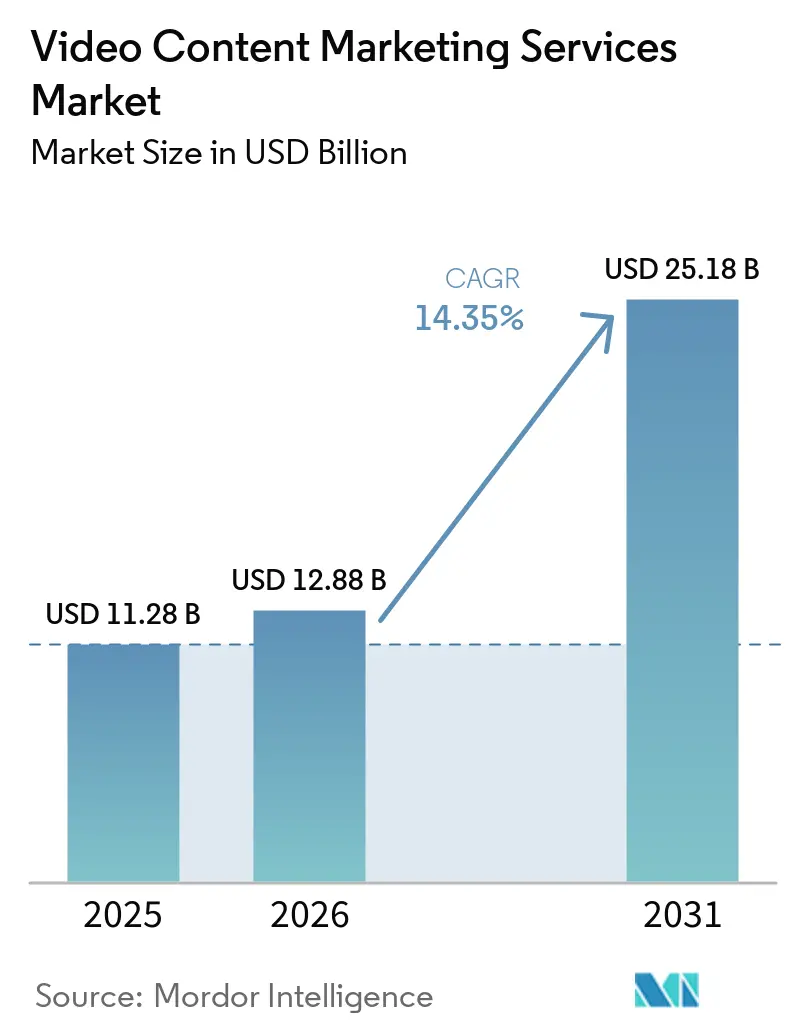

| Market Size (2026) | USD 12.88 Billion |

| Market Size (2031) | USD 25.18 Billion |

| Growth Rate (2026 - 2031) | 14.35% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

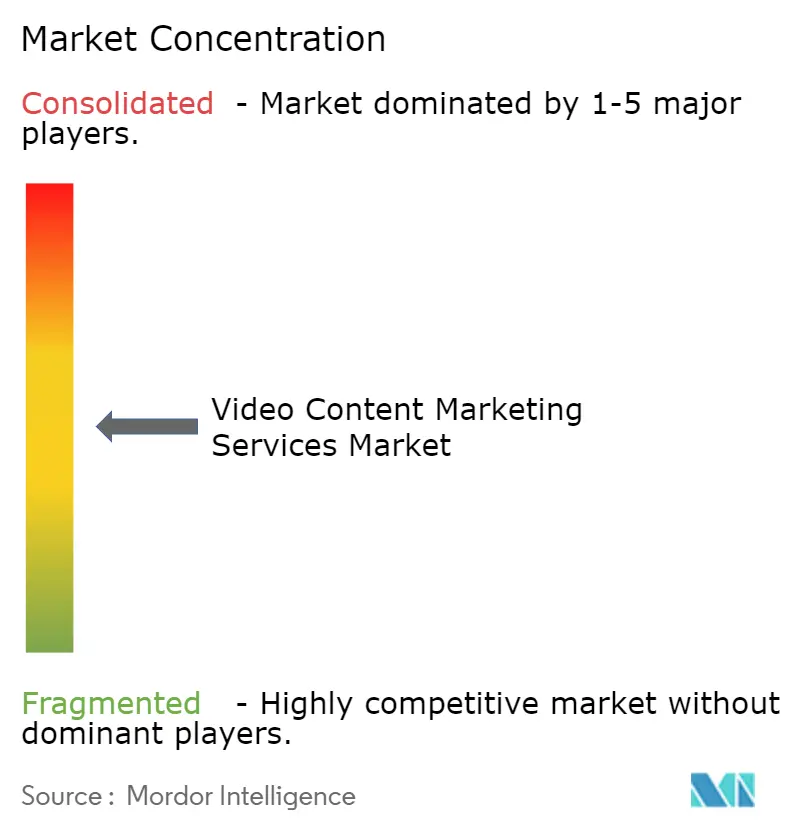

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Content Marketing Services Market Analysis by Mordor Intelligence

The Video Content Marketing Services Market size was valued at USD 11.28 billion in 2025 and estimated to grow from USD 12.88 billion in 2026 to reach USD 25.18 billion by 2031, at a CAGR of 14.35% during the forecast period (2026-2031). Budget allocation is shifting toward video-first programs, which is moving spend away from legacy formats and toward managed production, editing, optimization, and distribution services. Enterprise adoption of AI-assisted workflows is increasing output capacity, but it is also raising the value of providers that can maintain brand control, review discipline, and delivery quality. Short-form, mobile-native formats continue to shape demand because they fit social discovery, retail media placement, and rapid campaign refresh needs. Competition is tightening as global holding companies, consultancy-led firms, and platform-native specialists overlap across service lines, while smaller studios still influence pricing and execution depth. Opportunity remains strongest for providers that can combine scale in production with analytics, localization, and governance support as buyers try to connect rising content volume with clearer commercial outcomes.

Key Report Takeaways

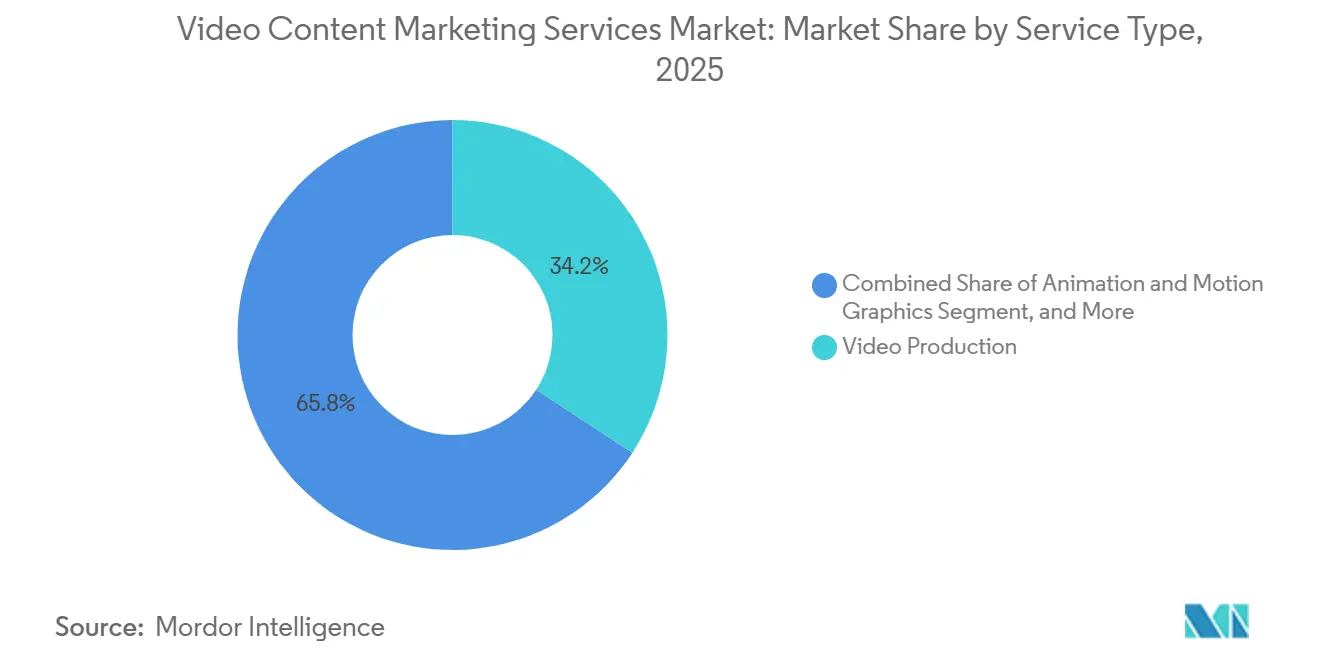

- By service type, video production held 34.22% of the video content marketing services market share in 2025, while animation and motion graphics is projected to expand at 16.12% CAGR through 2031.

- By video type, branded storytelling and promotional videos accounted for 29.56% share in 2025, while explainer videos are projected to grow at 15.89% CAGR through 2031.

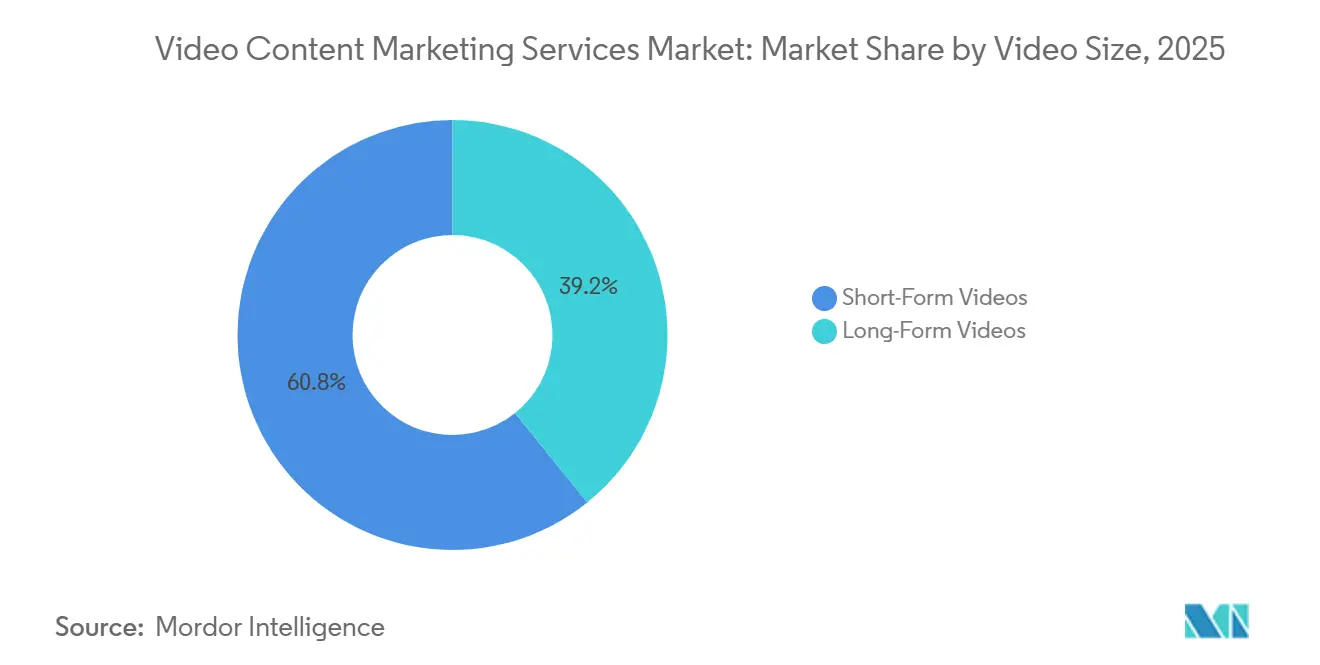

- By video size, short-form videos commanded 60.77% share of the video content marketing services market size in 2025 and are projected to expand at 16.56% CAGR through 2031.

- By end-user industry, retail and e-commerce represented 24.38% share in 2025, while IT and telecom is projected to advance at 16.68% CAGR through 2031.

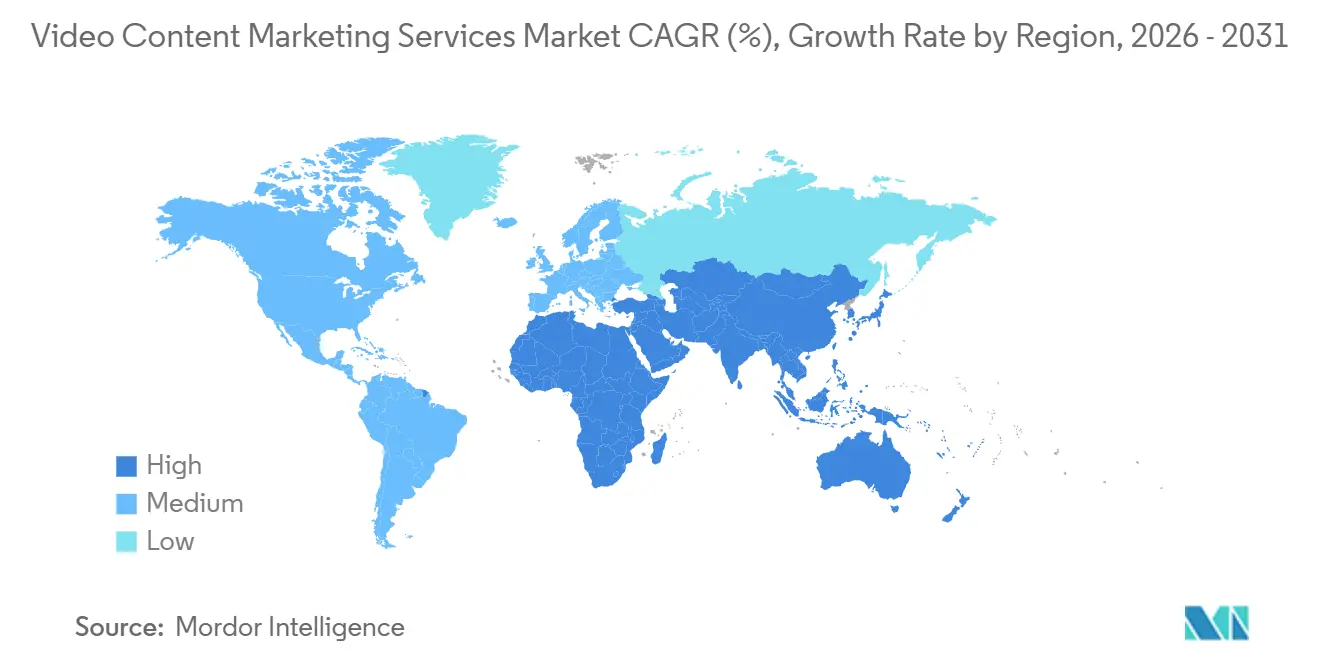

- By geography, North America held 34.56% revenue share in 2025, yet Asia-Pacific is on track for the highest regional CAGR of 16.52%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Content Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Short-Form Video Budget Reallocation | +3.2% | Global, with North America and Asia-Pacific core | Short term (≤ 2 years) |

| Growing Enterprise Demand for AI-Assisted Production and Versioning | +2.8% | North America and Europe primarily, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Creator-Led and Employee-Led Video Campaigns | +2.1% | Global, with North America, Asia-Pacific, and South America elevated | Short term (≤ 2 years) |

| Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing | +1.8% | North America and Europe, with emerging traction in Asia-Pacific | Medium term (2-4 years) |

| Growth of Shoppable Video and Retail Media Video Workflows | +1.4% | North America, Asia-Pacific core, spill-over to Europe | Medium term (2-4 years) |

| Acceleration of AI Dubbing and Multilingual Localization for Mid-Market Expansion | +1.1% | Global, led by Asia-Pacific and Europe multilingual markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Short-Form Video Budget Reallocation

Short-form video has moved from a supporting tactic to the center of social and performance planning in the video content marketing services market. Wistia reported that 57% of marketing budgets globally included a dedicated short-form video line item in 2026, and videos under 60 seconds generated 2.5x more engagement per impression than other content formats.[1]Wistia Inc., “State of Video 2025, Business Video Benchmarks and Trends,” Wistia, wistia.comThis shift is raising outsourced demand because platform-native short-form programs need repeated edits, multiple aspect ratios, and frequent refresh cycles that many internal teams cannot sustain at scale. The IAB stated that social video spending in the United States rose 13% in 2026, which confirms the pace of budget movement toward formats that rely on continuous managed execution. As brands create 4 to 6 platform-specific cuts from one source asset, providers that can version, optimize, and distribute content efficiently are capturing more recurring work in the video content marketing services market.

Growing Enterprise Demand for AI-Assisted Production and Versioning

Enterprise buyers are using AI-assisted workflows in the video content marketing services market to expand output without matching headcount growth. Goldcast and Redpoint found that 89% of B2B marketers and 94% of C-suite executives viewed video as important to strategy in 2025, and nearly 75% were increasing video production budgets.[2]Goldcast and Redpoint Ventures, “The 2025 State of AI in B2B Video Marketing,” Goldcast, goldcast.io Organizations using advanced AI video strategies were 4.5 times more likely to increase video creation output, and 77% of CIOs said they were willing to pay a premium for AI-enhanced video production solutions. This demand is rewarding service providers that pair AI generation with approval workflows, brand controls, and output quality checks rather than selling automation alone. The result is a market environment where enterprise contracts increasingly value speed, versioning, and governance together.

Expansion Of Creator-Led And Employee-Led Video Campaigns

Creator-led and employee-led formats are reshaping what buyers procure in the video content marketing services market. Instead of relying only on studio-produced brand assets, marketers increasingly seek creator sourcing, content governance, paid amplification, and performance support around more natural video formats. Dentsu stated in its 2026 Media Trends report that attention quality mattered more than sheer viewing volume for video effectiveness, thereby strengthening the role of creator-native viewing environments.[3]Dentsu Group Inc., “2026 Media Trends, Human Truths in the Algorithmic Era,” Dentsu, insight.dentsu.com This change is separating the value chain, because creator management and amplification are expanding faster than pure production work in many campaign models. As this model expands, providers with creator networks and media activation capabilities are taking a larger share of demand than firms that offer production alone.

Rising Adoption of Video for B2B Education, Product Demos, and Webinar Repurposing

B2B teams are using video more heavily for education, demos, and webinar repurposing across the video content marketing services market. One long webinar is now commonly turned into demo clips, short social assets, FAQ snippets, and sales enablement material, which increases repeat service demand instead of one-time project work. Goldcast and Redpoint found that 90% of B2B teams that successfully applied AI in video production started with repurposing, which shows how this workflow has become a practical entry point for scaled video programs. Adobe reinforced this operating model when it introduced GenStudio for Content Marketing in April 2026 with tools that convert long-form assets into campaign-ready derivatives. This pattern is especially important in software and IT categories where product demo libraries influence pipeline movement, onboarding, and customer communication over long buying cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent ROI Attribution Gaps Across Walled Gardens | -1.8% | Global, most acute in North America and Europe where multi-platform buying is standard | Medium term (2-4 years) |

| High-Volume Creative Refresh Requirements Raising Delivery Complexity | -1.2% | Global, especially in North America and Asia-Pacific where platform-native versioning demands are highest | Short term (≤ 2 years) |

| Tightening AI Disclosure and Synthetic Media Compliance Rules | -0.9% | Europe, North America | Short term (≤ 2 years) |

| Platform Algorithm Volatility Reducing Predictability of Organic Reach | -0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent ROI Attribution Gaps Across Walled Gardens

Persistent ROI attribution gaps remain a near-term brake on spending in the video content marketing services market. Large platforms still measure exposure and conversion through separate systems, which lets multiple channels claim credit for the same sale and complicates cross-channel evaluation. That makes it harder for agencies and service providers to prove the full value of upper-funnel video to finance and procurement teams. In practice, the problem reduces confidence in outcome-based pricing and can keep contract sizes below what content volume alone would justify. Providers with stronger analytics, testing frameworks, and measurement governance are better positioned to defend margins as clients scrutinize ROI more closely.

High-Volume Creative Refresh Requirements Raising Delivery Complexity

High-volume creative refresh requirements are raising delivery complexity across the video content marketing services market. Short-form campaigns lose performance quickly when creative versions are not updated often, especially when brands run simultaneous programs across TikTok, Meta, YouTube, LinkedIn, and connected TV. This expands the amount of production, editing, captioning, rights management, and compliance review needed for each active campaign. It also pushes some enterprise clients toward modular vendor networks because no single partner can always absorb every versioning need at the required speed. Providers that automate aspect ratios, localized captions, and metadata packaging are in a stronger position to manage this workload without hurting unit economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Video Production Anchors Revenue, Animation Outpaces the Field

Video production accounted for 34.22% of the video content marketing services market size in 2025, which kept it as the largest service category. That position is structural because strategy, SEO, distribution, and promotional work all depend on production output as their starting asset. The segment continued to attract enterprise, agency, and direct-brand spending because live capture, editing, and post-production remain difficult to remove from commercial video programs. At the same time, AI-assisted tools are reducing the cost of some routine production tasks, which is changing how providers price base execution and differentiate premium work.

Animation and motion graphics is projected to grow at 16.12% CAGR through 2031 in the video content marketing services market, making it the fastest-growing service type. Demand is rising because animated explainers and product visuals help SaaS, healthcare, and other regulated categories communicate clearly without relying on complex live-action shoots. Strategy and consulting, content ideation and scripting, video SEO, and distribution and promotion are also expanding as buyers move toward always-on service contracts instead of isolated projects. This shift shows that the video content marketing services industry is rewarding providers that combine production with discoverability, repurposing, and campaign management rather than selling creative output alone.

By Video Type: Branded Storytelling Holds Share as Explainer Videos Scale Fastest

Branded storytelling and promotional videos represented 29.56% share in the video content marketing services market in 2025, which made them the largest video type. Their staying power comes from continued enterprise spending on brand equity across connected TV, YouTube, and programmatic video placements. This format remains important because it carries the main burden of expressing brand identity and building recall across long buying cycles. Dentsu reported in 2025 that digital video, including short-form, could deliver multi-year brand-building effects comparable to linear TV when attention quality was optimized.

Explainer videos are projected to grow at 15.89% CAGR through 2031 in the video content marketing services market, making them the fastest-growing video type. Growth is strongest where companies need to reduce complex product ideas into simple assets that can work across sales, marketing, and customer success. Product demonstration videos and tutorial formats are also expanding because they support onboarding, support deflection, and product adoption. This mix shows that the video content marketing services market is balancing long-term brand storytelling with high-utility formats that answer practical buyer questions.

By Video Size: Short-Form Commands Budgets and Accelerates Fastest

Short-form videos held 60.77% of the video content marketing services market share in 2025, which gave them the clearest lead among video sizes. Their dominance reflects both platform design and advertiser behavior, since TikTok, Instagram Reels, and YouTube Shorts prioritize short, mobile-native delivery. Wistia said videos under 60 seconds posted an 85% average completion rate and 47% more shares than long-form equivalents in its 2025 benchmark work. Retail, consumer goods, and beauty brands remain heavily skewed toward this format because it supports product discovery, seasonal pushes, and creator-style content at high frequency.

Short-form videos are also projected to expand at 16.56% CAGR through 2031 in the video content marketing services market, making them the fastest-growing size segment as well. Platform investment in short-form ad inventory and the spread of shoppable placements continue to support that pace. Long-form video still matters in the consideration stage, especially for B2B purchases that require more education and trust-building before conversion. The balance between the two formats keeps the video content marketing services industry tied to both rapid refresh execution and deeper funnel content planning.

By End-User Industry: Retail Anchors Revenues as IT and Telecom Outpaces All Verticals

Retail and e-commerce accounted for 24.38% share in the video content marketing services market in 2025, which kept it as the largest end-user group. The segment leads because video now sits closer to product discovery and conversion, not only brand awareness. Retail media networks are widening the role of video across on-site, social, and connected TV placements, which keeps production and optimization demand elevated. This makes managed video support more commercially relevant for merchants and direct-to-consumer brands that need frequent creative updates tied to merchandising cycles.

IT and telecom is projected to grow at 16.68% CAGR through 2031 in the video content marketing services market, making it the fastest-growing end-user vertical. The segment is expanding as enterprise software sellers use product walkthroughs, onboarding clips, and renewal communication to move prospects and customers through long decision processes. Vidyard highlighted broad adoption of AI avatar tools in B2B video messaging workflows in 2026, which shows how video is being embedded into revenue-team activity rather than confined to brand campaigns. Healthcare and life sciences, media and entertainment, consumer goods and beauty, and BFSI also remain important, with healthcare growing quickly as compliant product video programs expand.

Geography Analysis

By geography, North America held 34.56% revenue share in 2025, yet Asia-Pacific is on track for the highest regional CAGR of 16.52%. North America remained the largest regional segment in the video content marketing services market in 2025. The region benefits from dense enterprise marketing budgets, strong demand from IT and SaaS buyers, and the presence of major holding company networks with large content production operations. Omnicom completed its acquisition of Interpublic in November 2025, creating the world’s leading marketing and sales company and expanding large-scale managed video capacity for enterprise clients. The United States continued to account for most regional demand, while Canada showed solid momentum in B2B technology video services. Mexico also gained relevance as nearshore production capacity expanded in support of U.S. brand work.

Asia-Pacific is the fastest-growing regional segment in the video content marketing services market. Japan’s digital video advertising market exceeded JPY 1.0275 trillion (USD 6.76 billion) in 2025, and CARTA Holdings, Dentsu, Dentsu Digital, and Septeni forecast it would reach JPY 1.1783 trillion (USD 7.86 billion) in 2026. CyberAgent reported that Japan’s broader domestic video advertising market stood at JPY 885.5 billion (USD 5.83 billion) in 2025 and would rise to JPY 1.0437 trillion (USD 6.96 billion) in 2026, while vertical video advertising grew to JPY 204.9 billion (USD 1.35 billion) and represented 29.1% of smartphone video advertising. China, India, South Korea, and Australia are also supporting growth as short video, live commerce, and multilingual localization demand expand across the region.

Europe showed steady growth in the video content marketing services market, led by Germany, the United Kingdom, and France, where automotive, consumer goods, and financial services buyers continue to invest in premium brand video. The United Kingdom remained an important center for branded storytelling and animation work, while European marketers also faced tighter scrutiny around AI-generated video disclosure as Article 50 of the EU AI Act moved toward enforcement in 2026. South America remained an emerging opportunity led by Brazil and Argentina, with demand tied mainly to consumer goods, retail, and social commerce campaigns. The Middle East and Africa stayed earlier in development, but the UAE, Saudi Arabia, South Africa, Nigeria, and Egypt continued to attract more advertiser interest as mobile-first video consumption and content investment increased.

Competitive Landscape

The video content marketing services market operates with a concentrated top tier and a fragmented middle and lower tier. Global holding companies, consultancy-led groups, and platform-native specialists compete for enterprise budgets through integrated production, data, and activation capabilities. Omnicom’s Interpublic acquisition in 2025 materially increased scale at the top end of the video content marketing services market. Publicis added creator, sports marketing, data collaboration, and measurement assets through its Captiv8, 160over90, and LiveRamp transactions across 2025 and 2026. These moves show that scale in content infrastructure and proprietary data is becoming as important as creative execution in winning large accounts.

WPP answered with WPP Production in February 2026, combining Hogarth with content producers across its network into a single AI-powered operating unit. That model is designed to standardize workflows, reduce duplication, and improve delivery capacity for global brand video programs. The competitive result is not full consolidation, because specialist studios, animation boutiques, and platform-focused agencies still shape pricing and niche expertise across the video content marketing services market. Buyers therefore continue to split spend between scaled partners for global execution and specialist firms for speed, category knowledge, or channel-specific work.

Technology-native and specialist providers remain effective in narrow use cases across the video content marketing services market, especially in AI-augmented production, avatar-led generation, and B2B sales enablement. Kaltura agreed to acquire PathFactory in March 2026, which showed how platform vendors are moving toward content intelligence and personalization around video workflows. White-space remains most visible in multilingual localization, compliance-ready synthetic media services, and shoppable video support for retailers outside top-tier media networks. That leaves the video content marketing services market moderately consolidated at the top but structurally fragmented in the broader delivery base.

Video Content Marketing Services Industry Leaders

WPP plc

Publicis Groupe S.A.

Omnicom Group Inc.

Dentsu Group Inc.

Interpublic Group of Companies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Brightcove launched Prism, its most significant platform redesign in years, developed with input from over 100 customers. The launch followed a period of accelerated AI product development under Bending Spoons' ownership and included expanded AI Suite capabilities targeting video monetization, accessibility, and marketing automation workflows.

- May 2026: Kaltura launched the general availability of its Avatar Video Production Studio, enabling enterprises to convert organizational knowledge into avatar-narrated video experiences at scale in minutes. The launch targeted technology, healthcare, financial services, and media verticals with self-serve purchasing planned for Q3 2026.

- April 2026: Adobe introduced GenStudio for Content Marketing at Adobe Summit (April 20, 2026), a new module enabling enterprises to convert long-form documents and video into tailored multi-channel campaign derivatives, with integrated performance insights on leads generated, follower growth, and audience reach.

- April 2026: Publicis Groupe entered a definitive agreement to acquire 160over90, the premier global sports and culture-first agency, extending its branded content and entertainment marketing capabilities. The acquisition complemented prior 2025 acquisitions of sports agencies Adopt and Bespoke.

Global Video Content Marketing Services Market Report Scope

The Video Content Marketing Services Market refers to the industry that provides specialized solutions and strategies for creating, distributing, and optimizing video content to promote brands, products, and services across digital platforms. This market includes services such as video production, editing, animation, live streaming, and performance analytics, all aimed at enhancing customer engagement, boosting online visibility, and driving conversions.

The Video Content Marketing Services Market Report is Segmented by Service Type (Strategy and Consulting, Content Ideation and Scripting, Video Production, Animation and Motion Graphics, Video SEO and Metadata Optimization, Distribution and Promotion, and Others), Video Type (Explainer Videos, Product Demonstration Videos, Tutorial and How-To Videos, Branded Storytelling and Promotional Videos, and Others (Educational and Webinar, etc.)), Video Size (Short-Form Videos, and Long-Form Videos), End-User Industry (Retail and E-commerce, Consumer Goods and Beauty, Media and Entertainment, IT and Telecom, BFSI, Healthcare and Life Sciences, and Others (Education, Travel and Hospitality, Industrial, Automotive)), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Strategy and Consulting |

| Content Ideation and Scripting |

| Video Production |

| Animation and Motion Graphics |

| Video SEO and Metadata Optimization |

| Distribution and Promotion |

| Other Service Types |

| Explainer Videos |

| Product Demonstration Videos |

| Tutorial and How-To Videos |

| Branded Storytelling and Promotional Videos |

| Other Video Types (Educational and Webinar, etc.) |

| Short-Form Videos |

| Long-Form Videos |

| Retail and E-commerce |

| Consumer Goods and Beauty |

| Media and Entertainment |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Strategy and Consulting | |

| Content Ideation and Scripting | ||

| Video Production | ||

| Animation and Motion Graphics | ||

| Video SEO and Metadata Optimization | ||

| Distribution and Promotion | ||

| Other Service Types | ||

| By Video Type | Explainer Videos | |

| Product Demonstration Videos | ||

| Tutorial and How-To Videos | ||

| Branded Storytelling and Promotional Videos | ||

| Other Video Types (Educational and Webinar, etc.) | ||

| By Video Size | Short-Form Videos | |

| Long-Form Videos | ||

| By End-User Industry | Retail and E-commerce | |

| Consumer Goods and Beauty | ||

| Media and Entertainment | ||

| IT and Telecom | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Other End-User Industries (Education, Travel and Hospitality, Industrial, Automotive) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the video content marketing services market?

The video content marketing services market stands at USD 12.88 billion in 2026 and is projected to reach USD 25.18 billion by 2031 at a CAGR of 14.35%.

Which service category leads revenue in this space?

Video production led service type revenue with a 34.22% share in 2025, supported by its central role in content capture, editing, and post-production.

Why are short-form videos so important for service providers?

Short-form videos held 60.77% share in 2025 and are projected to grow at 16.56% CAGR through 2031, which keeps demand high for versioning, optimization, and rapid creative refresh.

Which video format is growing the fastest?

Explainer videos are projected to grow at a 15.89% CAGR through 2031 because they help B2B, healthcare, and financial services firms simplify complex offerings.

Which end-user group creates the largest demand?

Retail and e-commerce was the largest end-user segment in 2025 with 24.38% share, reflecting the deeper use of video in product discovery and purchase workflows.

Which region offers the strongest growth outlook?

Asia-Pacific is the fastest-growing region, supported by strong digital video advertising expansion in Japan and broader demand growth across China, India, South Korea, and Australia.

Page last updated on: