Customer Service Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

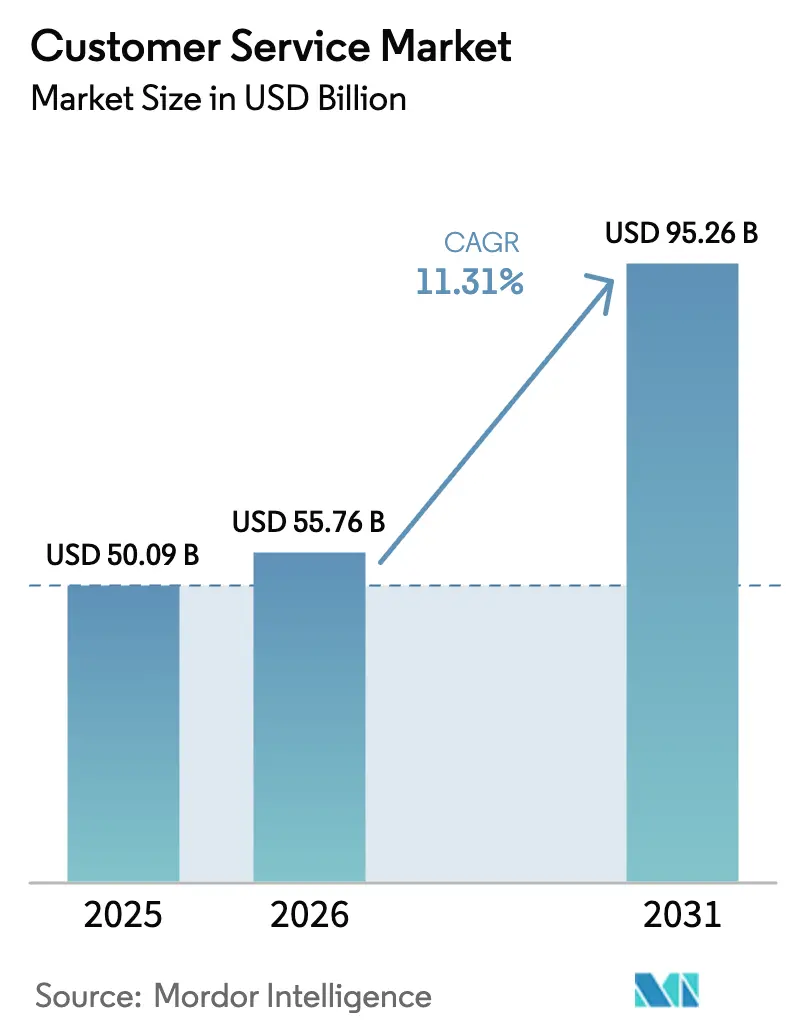

| Market Size (2026) | USD 55.76 Billion |

| Market Size (2031) | USD 95.26 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

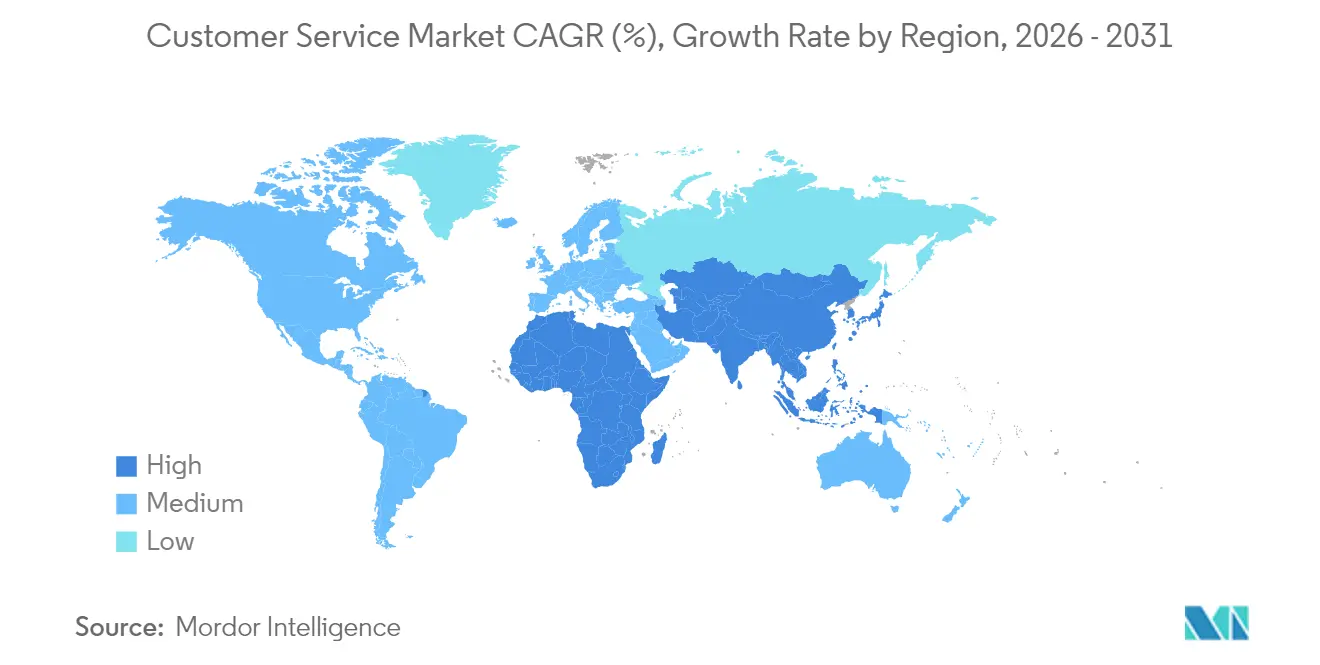

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Customer Service Market Analysis by Mordor Intelligence

The customer service market size was valued at USD 50.09 billion in 2025 and estimated to grow from USD 55.76 billion in 2026 to reach USD 95.26 billion by 2031, at a CAGR of 11.31% during the forecast period (2026-2031). Sustained growth is tied to enterprises replacing legacy contact centers with AI-enabled, cloud-native solutions that cut operating costs while boosting customer satisfaction. Business-to-consumer brands now deploy generative AI assistants that solve routine queries without human intervention, freeing agents to focus on complex issues. Industry leaders also exploit unified data platforms to move seamlessly between sales, service, and marketing touchpoints, creating a single view of each customer. Meanwhile, small and medium enterprises (SMEs) adopt subscription-based Contact Center as a Service (CCaaS) offerings to gain enterprise-grade functionality without heavy capital outlays. On the supply side, mergers and acquisitions near USD 10 billion are consolidating capabilities in conversational AI, sentiment analytics, and workflow automation, accelerating innovation cycles and heightening competitive pressure.

Key Report Takeaways

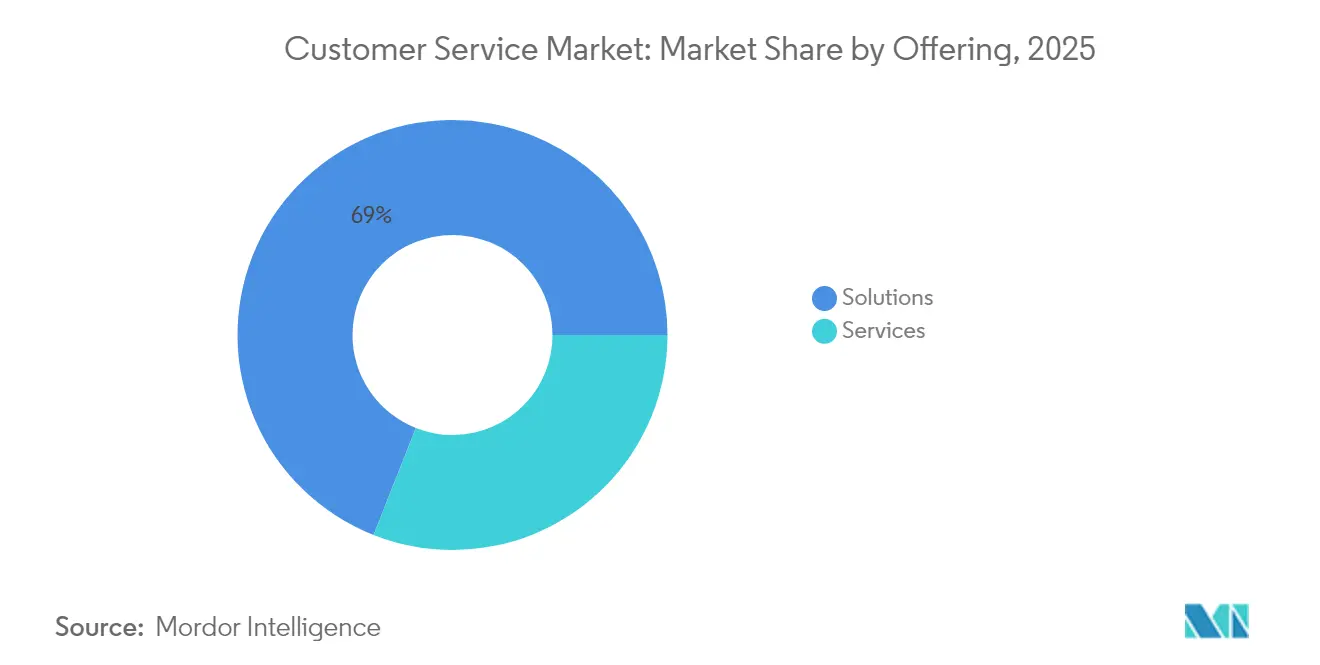

- By offering, solutions held 69.02% of customer service market share in 2025, whereas services are projected to grow at a 12.05% CAGR to 2031.

- By deployment mode, the cloud segment accounted for 64.66% of the customer service market size in 2025 and is set to expand at 12.96% CAGR through 2031.

- By end-user industry, IT & Telecommunications led with 24.28% revenue share in 2025, while healthcare is forecast to deliver the fastest 13.62% CAGR by 2031.

- By end-user enterprise size, large enterprises captured 58.86% share of the customer service market size in 2025; SMEs exhibit the highest 12.74% CAGR through 2031.

- By geography, North America commanded 38.74% of customer service market share in 2025; Asia-Pacific is advancing at a 13.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Customer Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative AI-enhanced self-service automation | +2.8% | Global; early uptake in North America and EU | Short term (≤ 2 years) |

| Cloud-native CCaaS adoption by SMEs | +2.1% | Global; strongest in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Convergence of CRM and customer-service platforms | +1.7% | North America and EU; spreading to Asia-Pacific | Medium term (2-4 years) |

| Real-time sentiment analytics for proactive support | +1.4% | Global; led by enterprise segments | Short term (≤ 2 years) |

| EU “right-to-talk-to-a-human” mandate | +0.9% | EU primary; global spillover | Long term (≥ 4 years) |

| Autonomous AI agents reducing operating costs | +2.6% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generative AI-enhanced self-service automation

Klarna’s AI assistant resolved 2.3 million conversations in its first month, demonstrating how natural-language engines handle scale without performance loss [1]Klarna Communications, “Klarna AI Assistant Resolves 2.3 Million Chats in First Month,” Klarna, klarna.com. Enterprises that sustain accuracy above 95% report double-digit reductions in average handling time, while freeing live agents for high-value interactions. Continuous model retraining and robust data pipelines remain prerequisites for success, giving companies with mature governance a durable lead. Front-office productivity gains anchor the 2.8% uplift in the customer service market’s forecast CAGR.

Cloud-native CCaaS adoption by SMEs

SMEs now provision cloud contact centers in 24 minutes on average, as illustrated by Royal Bank of Canada’s API-first deployment that trimmed maintenance costs 50% [2]RBC Digital Team, “Royal Bank of Canada Modernizes Contact Center,” MuleSoft, mulesoft.com. Subscription pricing converts capital expense into operational outflow, easing budget constraints and driving the 2.1% contribution to CAGR. Low-code connectors and managed services lower integration costs, though complex legacy estates can still reach USD 30,000 per deployment. Demand is strongest in Asia-Pacific, where mobile-first consumers press smaller firms to match enterprise service levels.

Convergence of CRM and customer-service platforms

ServiceNow’s entry into CRM and its alliances with Five9 and Genesys exemplify a market pivot toward unified experience clouds that merge sales, marketing, and service data. Integrated routing, knowledge-embedded workspaces, and shared analytics eliminate channel handoffs that frustrate customers. Vendors that deliver end-to-end suites capture larger wallet share and accelerate cross-sell, adding 1.7% to overall growth. Stand-alone point solutions face mounting replacement risk unless they plug seamlessly into broader ecosystems.

Real-time sentiment analytics enabling proactive support

AirHelp cut response times 65% after deploying SentiOne’s omni-channel automation that flags negative sentiment in real time. Modern engines parse voice inflection, text cues, and social chatter to prioritize high-risk cases, curbing churn and increasing upsell. Feedback loops feed product teams with longitudinal emotion data, while accuracy above 85% warrants human review only for edge cases. The capability’s 1.4% CAGR lift rests on cross-channel data integration and culture-specific model tuning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-sovereignty and privacy costs | -1.8% | Global; strictest in EU and privacy-forward regions | Long term (≥ 4 years) |

| Skill gaps in AI governance | -1.3% | Global; most acute in developing markets | Medium term (2-4 years) |

| Rising API and integration complexity | -0.9% | Global; concentrated in enterprise segments | Short term (≤ 2 years) |

| Regulatory push-back on voice biometrics | -0.7% | North America and EU; expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating data-sovereignty and privacy compliance costs

Illinois’ Biometric Information Privacy Act and similar statutes expose violators to steep fines, while EU directives restrict cross-border transfers. Deepfake studies from the University of Waterloo show 99% bypass rates on voice biometrics, intensifying regulatory scrutiny. Organizations now budget for dedicated privacy officers, geo-fenced data stores, and multi-factor authentication layers. These expenses pare 1.8% from growth but also raise entry barriers that favor well-capitalized suppliers.

Skill gaps in AI governance for service operations

Demand for prompt-engineering, bias-monitoring, and model-lifecycle experts far exceeds supply, lifting salary premiums and slowing deployments. OECD research warns that ungoverned AI degrades accuracy below 90%, risking compliance violations and customer attrition. Upskilling programs span 6–12 months, during which productivity dips as staff adjust to AI-augmented workflows. The talent crunch trims 1.3% from projected CAGR yet opens opportunities for managed AI-operations providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Segment Accelerates Despite Solutions Dominance

Solutions generated the largest revenue stream in 2025, holding 69.02% customer service market share as firms licensed core platforms to modernize contact centers. However, the services segment is widening faster at a 12.05% CAGR because organizations now require continuous optimization, customized integrations, and model-training expertise. Managed-service contracts increasingly guarantee outcome metrics such as first-contact resolution, signaling a shift from labor-based billing to value-based pricing. As enterprises mature, they seek partners to manage AI drift, data labeling, and regulatory audits, making services pivotal to sustained performance.

Recurring revenue from professional and managed services underpins vendor profitability as platform licenses plateau. The customer service market continues to reward providers that combine domain know-how with technical depth, particularly in healthcare and public sector verticals that mandate strict compliance. Service firms that invest in proprietary accelerators—prebuilt bots, data connectors, or industry templates—compress time-to-value and secure multi-year contracts. As a result, services revenue will outpace core software growth through 2031.

By Deployment Mode: Cloud Supremacy Reinforced by SME Adoption

Cloud deployments captured 64.66% of customer service market size in 2025, reflecting user preference for rapid provisioning and elastic scalability. CCaaS users report 30% cost savings versus on-premises, while implementation cycles shrink from months to weeks. Hybrid architectures allow sensitive data to reside on-premises yet exploit cloud AI for routing and analytics, easing regulatory barriers for financial and public sector entities.

On-premises systems persist in ultra-regulated niches but face rising total cost of ownership, averaging USD 40,000 per year in maintenance and patching. Low-code integration tools and prebuilt connectors now slash API costs, widening the cloud appeal for SMEs whose budgets cannot absorb lengthy custom projects. As mobile commerce surges in emerging markets, cloud platforms able to spin up voice, chat, and social channels on demand will extend their lead, sustaining a 12.96% CAGR.

By End-User Industry: Healthcare Leads Growth While IT Maintains Scale

IT and Telecommunications remained the largest sector with 24.28% revenue in 2025, leveraging mature digital infrastructures to integrate AI agents seamlessly. The segment relies on deep analytics to manage large subscriber bases and complex device portfolios. Yet Healthcare is the breakout opportunity, forecast to grow 13.62% annually as patient engagement platforms close communication gaps that drive provider switching. Talkdesk’s healthcare-specific AI agent underscores the appetite for HIPAA-compliant automation that handles appointment scheduling, claims, and triage.

Public sector agencies also accelerate adoption to manage benefit surges and crisis communications, as seen when Rhode Island’s Labor and Training department scaled to 1,000 concurrent calls in days via Amazon Connect. Manufacturing links IoT telemetry to customer service workflows for predictive maintenance, while hospitality rebounds with multilingual chatbots that personalize travel planning. Industry-specific compliance, data models, and integrations give niche vendors room to differentiate.

By End-User Enterprise Size: SME Growth Outpaces Enterprise Adoption

Large enterprises commanded 58.86% customer service market size in 2025, driven by complex omnichannel footprints and compliance demands that favor best-in-class suites. They invest heavily in AI orchestration layers that harmonize bots, agents, and knowledge bases across regions. However, SMEs are the fastest-growing cohort at a 12.74% CAGR because cloud vendors package sophisticated tools into turnkey bundles. Microsoft reports over 230,000 organizations using Copilot to build custom agents without writing code.

SMEs value ease of use, predictable subscription tiers, and quick wins over deep customization. Peer pressure and rising customer expectations spur adoption, while managed service partners address AI governance gaps. Bundled compliance checks and industry templates further remove friction, positioning SMEs as a major engine of incremental demand in the customer service market.

Geography Analysis

North America retained 38.74% customer service market share in 2025 thanks to early cloud adoption and a supportive regulatory environment that balances innovation with consumer protection. Technology giants host extensive partner networks that streamline deployments and provide localized compliance expertise. As platform penetration deepens, growth shifts from green-field installations to advanced use cases such as autonomous agents, predictive routing, and hyper-personalized upsell offers. Enterprises now benchmark customer-lifetime value gains rather than pure cost reduction, signaling a mature phase focused on optimization and value extraction.

Asia-Pacific is the fastest-growing region at 13.28% CAGR through 2031, propelled by booming e-commerce, expanding middle classes, and mobile-first behaviors. China’s super-app ecosystems normalize AI-led service, prompting regional brands to match experience standards. India’s Digital Public Infrastructure initiative lowers data-cost barriers, enabling startups and SMEs to leapfrog legacy systems. Southeast Asian markets benefit from rising internet penetration and government incentives for digital transformation. The prevalence of single-person households across advanced Asian economies intensifies demand for always-available digital support that alleviates the “lonely economy.”

Europe presents a multifaceted environment shaped by stringent data-sovereignty mandates and accessibility requirements. The European Accessibility Act, effective June 28 2025, obliges companies to redesign digital support channels for perceivability and operability . Anticipated “right-to-talk-to-a-human” rules by 2028 will accelerate investment in seamless AI-to-agent handoffs that preserve context. Eastern Europe’s continued EU integration and digitalization open new growth corridors, while Brexit alters data-transfer mechanics for UK-centric deployments. Ethical AI and sustainability considerations gain prominence, rewarding vendors with transparent model governance and low-carbon infrastructure commitments.

Competitive Landscape

The customer service market is moderately consolidated yet fiercely competitive. Salesforce leads through its Customer 360 platform, posting USD 37.9 billion in fiscal 2025 revenue and expanding Agentforce autonomous capabilities across industries. Microsoft pursues a platform strategy that embeds Dynamics 365 Customer Service within the broader productivity cloud, generating USD 13 billion in AI services revenue while leveraging Azure infrastructure. Amazon Web Services capitalizes on its compute scale and the Connect platform, contributing materially to USD 29.3 billion Q1 2025 revenue.

Strategic acquisitions intensify as incumbents seek specialized AI and regional reach. Concentrix purchased Webhelp for USD 4.8 billion, forming a USD 9.8 billion service powerhouse, while Zendesk added Ultimate to infuse conversational AI across its suite. ServiceNow broadened alliances with Five9 and Genesys to deliver unified experience clouds, underscoring platform convergence trends. These moves compress the vendor landscape, but dynamic startups still find whitespace by targeting vertical niches, compliance automation, and advanced analytics.

Emerging challengers attract venture funding by solving pinpoint pain points. Decagon raised USD 35 million for domain-tuned AI agents, and Crescendo acquired PartnerHero to pioneer outcome-based pricing models. Patent filings in conversational AI, emotional analytics, and AI operations surge as companies lock in intellectual property. Buyers increasingly favor partners that demonstrate transparent model governance, low bias scores, and verifiable carbon footprints, adding non-technical criteria to vendor evaluations.

Customer Service Industry Leaders

ServiceNow, Inc.

Salesforce, Inc.

Zendesk, Inc.

NICE Ltd.

Genesys Telecommunications Laboratories, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CallMiner acquired VOCALLS to infuse voice-first conversational AI into its interaction-analytics platform, expanding automation workflows across channels.

- May 2025: Weave Communications purchased TrueLark for USD 35 million, integrating AI receptionist capabilities that offer 24/7 scheduling for healthcare practices.

- May 2025: Press Ganey Forsta acquired InMoment, blending natural-language analytics with a 43,000-client base across healthcare and retail.

- November 2024: ServiceNow and Five9 deepened their partnership to launch an AI-powered solution combining Customer Service Management with an Intelligent CX Platform for unified routing and single-agent experiences.

Global Customer Service Market Report Scope

Customer service is the help provided by a company to its customers before or after their purchase or use of products or services. Customer service involves tasks like solving problems and addressing complaints, providing product recommendations or answering common inquiries.

The customer service market is segmented by offering (solutions, services [managed, professional]), deployment type (on-premise, cloud),end-user (BFSI, media and entertainment, government, IT and telecommunication, healthcare, manufacturing, others), geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The Report Offers Market Forecasts and Size in Value (USD) for all the Above Segments.

| Solutions | |

| Services | Managed Services |

| Professional Services |

| On-Premise |

| Cloud |

| BFSI |

| Retail and E-Commerce |

| Government and Public Sector |

| IT and Telecommunication |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Travel and Hospitality |

| Others |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Solutions | ||

| Services | Managed Services | ||

| Professional Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By End-User Industry | BFSI | ||

| Retail and E-Commerce | |||

| Government and Public Sector | |||

| IT and Telecommunication | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Travel and Hospitality | |||

| Others | |||

| By End-user Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the customer service market?

The customer service market stands at USD 55.76 billion in 2026 and is on track to reach USD 95.26 billion by 2031.

Which region is growing fastest in the customer service market?

Asia-Pacific leads growth with a 13.28% CAGR, driven by rapid digitalization and rising consumer service expectations.

Which industry vertical shows the highest growth potential?

Healthcare is forecast to expand at 13.62% CAGR as providers invest in AI-powered patient engagement solutions.

How are SMEs impacting customer service technology adoption?

SMEs are the fastest-growing customer cohort, adopting cloud-native CCaaS platforms that convert capital expense into manageable subscription fees.

Page last updated on: