Service Integration And Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

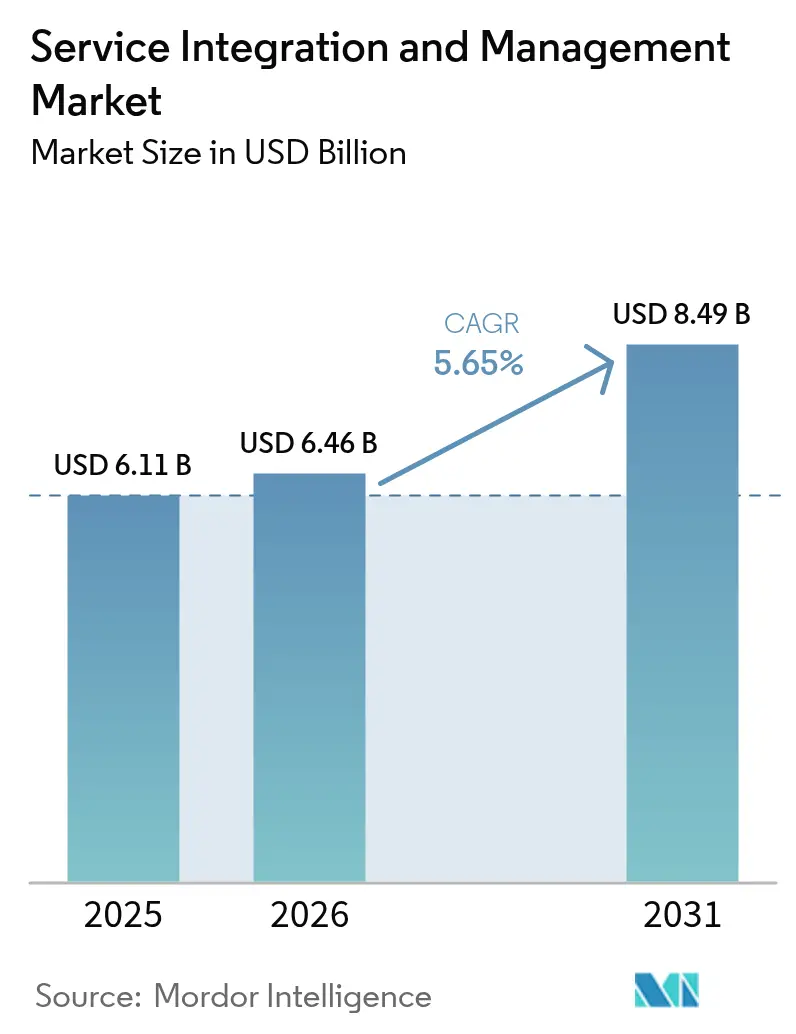

| Market Size (2026) | USD 6.46 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

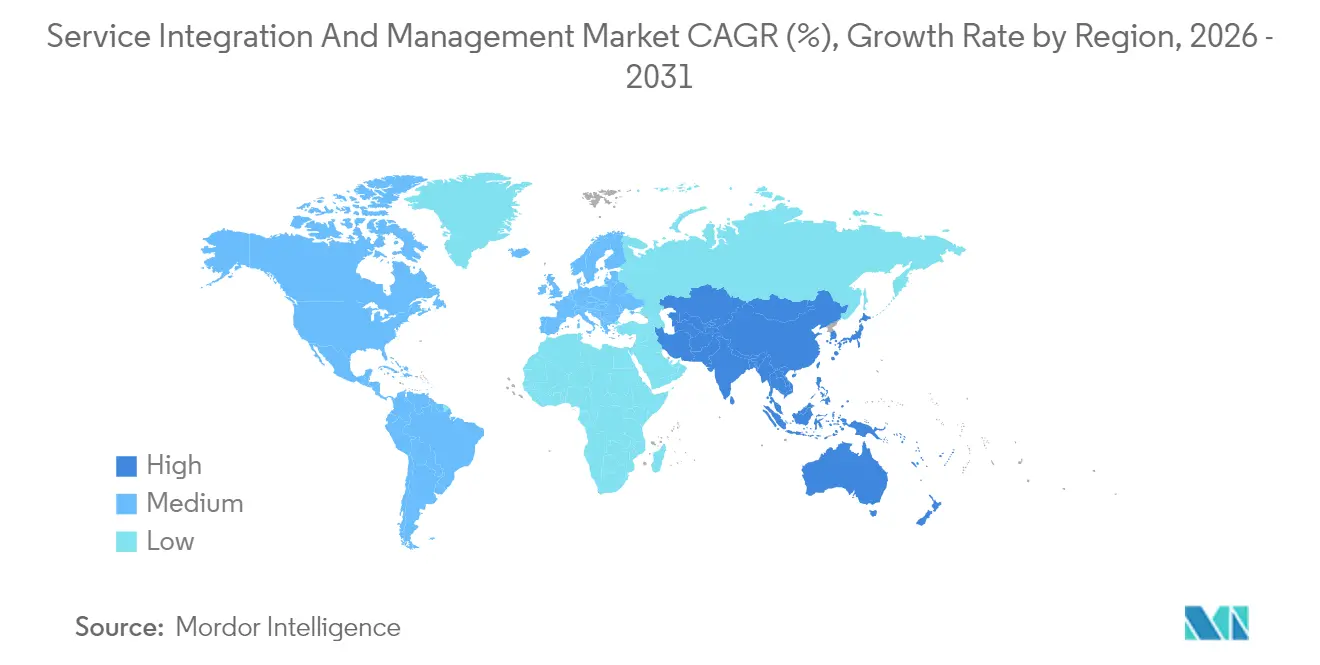

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

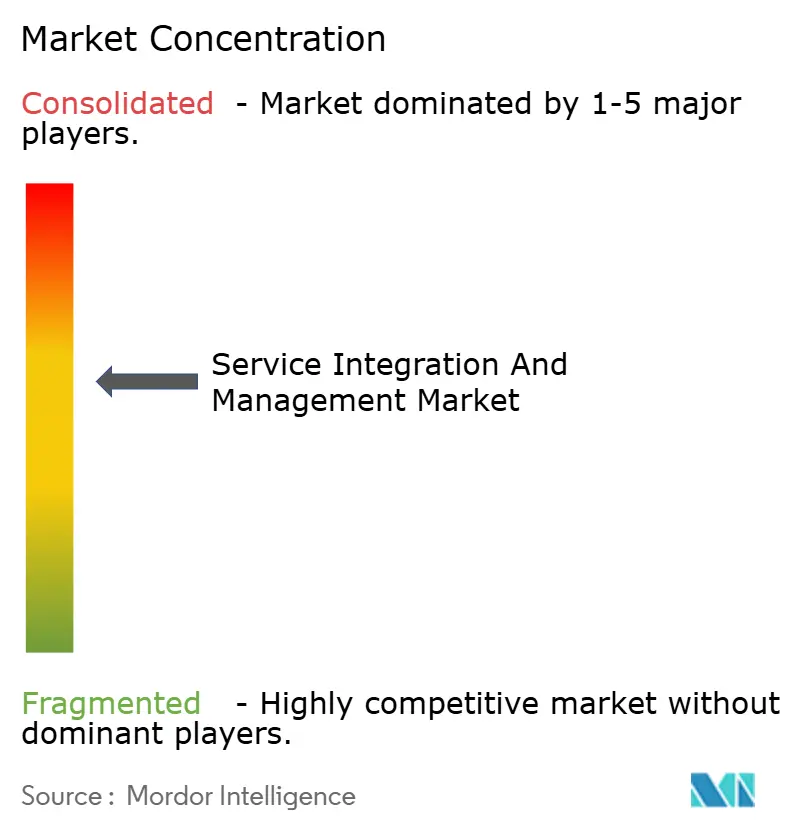

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Service Integration And Management Market Analysis by Mordor Intelligence

The global service integration and management market size in 2026 is estimated at USD 6.46 billion, growing from 2025 value of USD 6.11 billion with 2031 projections showing USD 8.49 billion, growing at 5.65% CAGR over 2026-2031. Growing reliance on hybrid IT estates, the average use of 2.6 public-cloud providers, and mounting regulatory scrutiny are compelling enterprises to adopt unified orchestration platforms that improve vendor coordination and SLA compliance.[1]IBM Security, “Cost of a Data Breach Report 2024,” IBM.com Escalating cloud-native application rollouts, particularly those involving containerized microservices, intensify integration touchpoints and increase demand for real-time service mapping. Enterprises also acknowledge that traditional siloed vendor oversight prolongs incident resolution and inflates governance costs, thus reinforcing the need for centralized, automation-driven SIAM frameworks that safeguard business continuity across distributed environments.

Key Report Takeaways

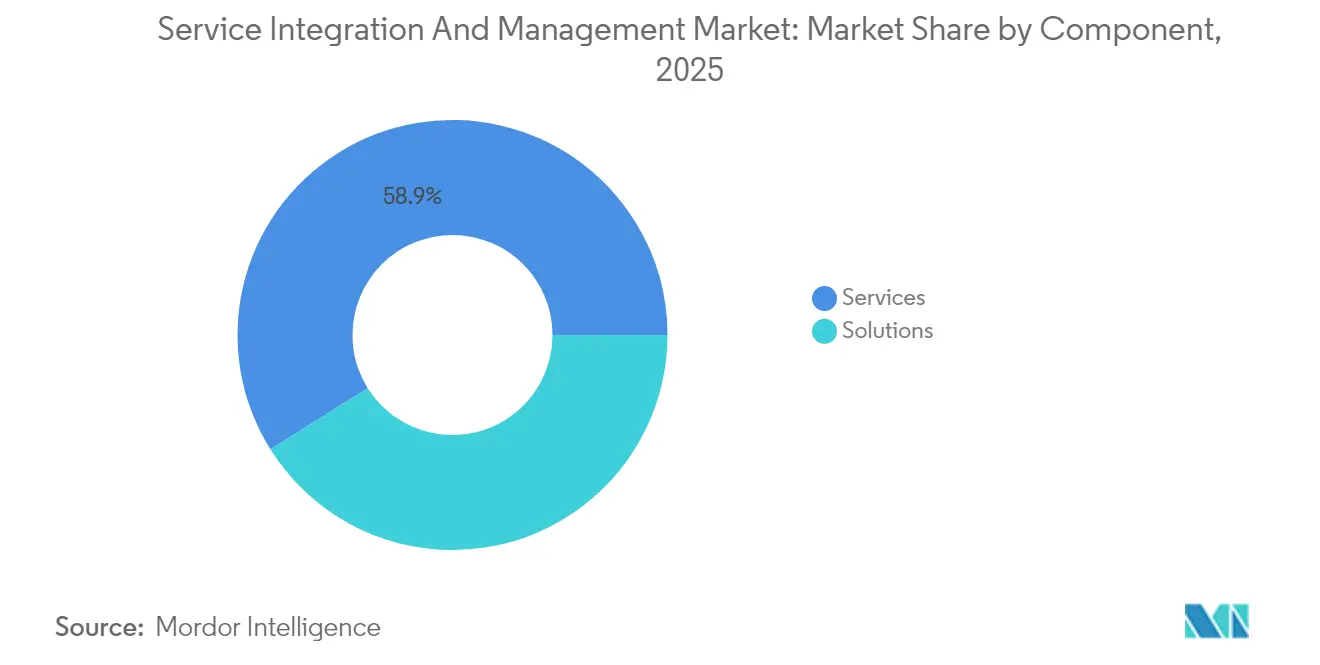

- By component, services retained 58.92% of 2025 revenue of the service integration and management market; however, the solutions segment is expanding at the fastest rate, with a 6.42% CAGR through 2031.

- By service model, the hybrid-provider model led with a 39.20% share of the service integration and management market in 2025, while the internal service integrator model is expected to advance at a 7.29% CAGR through 2031.

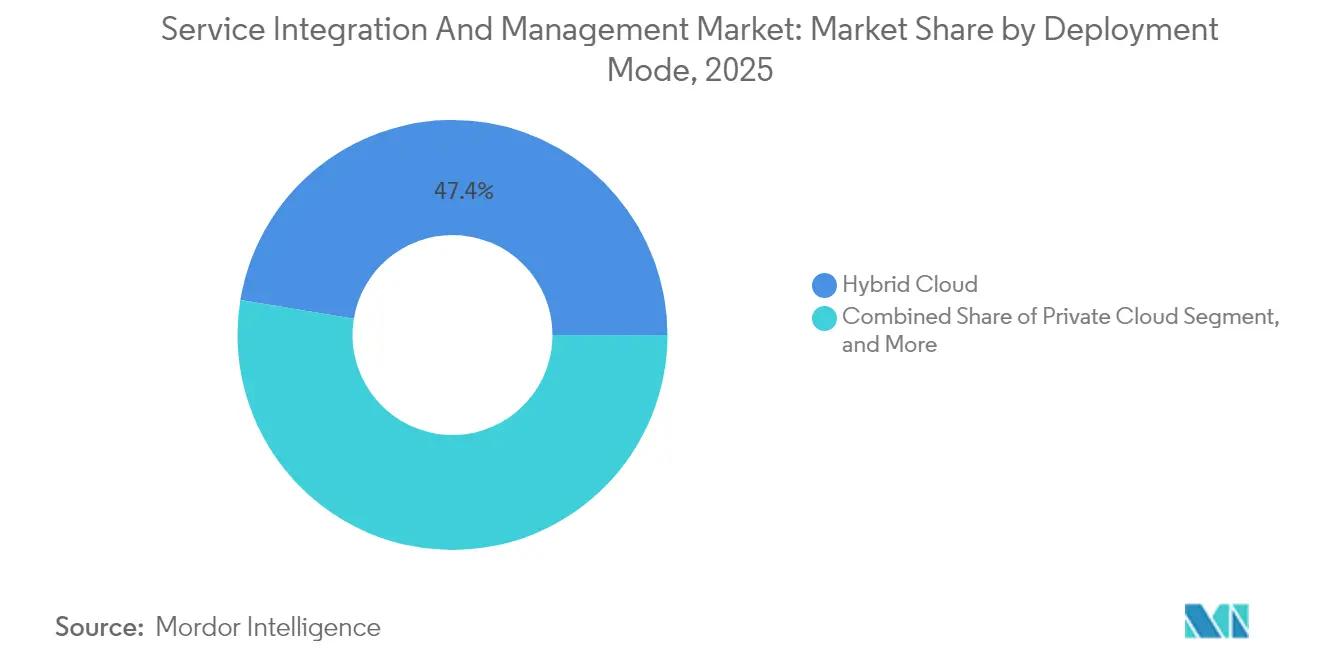

- By deployment mode, hybrid cloud accounted for 47.40% of 2025 deployments of the service integration and management market; public-cloud rollouts are accelerating at a 7.66% CAGR.

- By organization size, large enterprises captured 67.12% of the 2025 demand of the service integration and management market; SME uptake is climbing at a 6.29% CAGR as subscription-based offerings lower entry barriers.

- By end-user industry, BFSI dominated end-user adoption, with a 27.08% share of the service integration and management market in 2025. In contrast, healthcare showed the fastest growth, at an 8.07% CAGR through 2031.

- By geography, North America commanded 35.91% of the service integration and management market's 2025 revenue, but the Asia Pacific is set to grow at a 6.98% CAGR, eroding the leadership gap.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Service Integration And Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising multi-vendor IT outsourcing complexity | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Surge in cloud-native microservices architectures | +1.0% | Global, led by Asia Pacific and North America | Short term (≤ 2 years) |

| Growing demand for unified SLA governance platforms | +0.8% | Global, notably regulated industries | Medium term (2-4 years) |

| Acceleration of digital transformation in regulated industries | +0.7% | North America and Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Hybrid-work operating model adoption | +0.5% | Global, early uptake in developed markets | Short term (≤ 2 years) |

| Adoption of AIOps for proactive service orchestration | +0.6% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Multi-Vendor IT Outsourcing Complexity

Enterprises typically manage 5-7 major IT providers plus multiple niche vendors, generating exponential integration touchpoints that legacy vendor management cannot control effectively. IBM’s 2024 study reveals that organizations with four or more primary providers incur 40% higher operational overhead and 60-80% longer outage resolution times, underscoring the financial risks associated with fragmented governance. SIAM platforms establish single-pane visibility, standardized KPIs, and dispute-avoidance protocols that eliminate finger-pointing, accelerate root-cause isolation, and strengthen compliance audit trails across the vendor ecosystem.

Surge in Cloud-Native Microservices Architectures

Kubernetes penetration reached 96% in 2024, yet containerized workloads spawn transient service dependencies spanning on-premises clusters and multiple public clouds.[2]Cloud Native Computing Foundation, “CNCF Annual Survey 2024,” CNCF.io Conventional ITSM catalogs become obsolete in this fluid landscape. Modern SIAM solutions embed real-time service discovery, automated dependency mapping, and policy-driven orchestration that dynamically recalibrates performance baselines as microservices scale, ensuring a consistent user experience despite frequent infrastructure changes.

Growing Demand for Unified SLA Governance Platforms

Enterprises increasingly insist on granular, end-to-end performance guarantees, but disparate vendor SLAs impede accountability. Advanced SIAM suites ingest telemetry across provider boundaries, correlate events, and auto-generate compliance dashboards that satisfy auditors in regulated verticals such as banking and healthcare. Unified governance mitigates cascading penalty clauses triggered by SLA breaches, enhancing executive confidence in multi-sourced operating models.

Acceleration of Digital Transformation in Regulated Industries

BFSI and healthcare must modernize legacy estates while respecting PCI DSS, SOX, HIPAA, and emerging digital banking mandates. SIAM frameworks overlay ITIL and ISO 20000 foundations with vertical-specific compliance controls, ensuring seamless data governance as workloads traverse hybrid clouds.[3]International Organization for Standardization, “ISO/IEC 20000-1:2018,” ISO.org Continuous monitoring, automated remediation, and immutable audit logs make SIAM essential for sustaining transformation momentum without compromising regulatory posture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of SIAM-skilled professionals | -0.8% | Global, acute in Asia Pacific and emerging markets | Long term (≥ 4 years) |

| Absence of global standardized SLA frameworks | -0.6% | Global; regional compliance variations | Medium term (2-4 years) |

| Legacy toolchain interoperability challenges | -0.5% | Global, concentrated in mature IT environments | Medium term (2-4 years) |

| Perceived loss of direct vendor control | -0.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of SIAM-Skilled Professionals

The demand for SIAM talent outstrips supply by roughly 40% in North America and Europe, resulting in extended implementation cycles of 18-24 months for many programs. Effective practitioners blend deep ITSM expertise, cloud architecture fluency, and vendor-negotiation acuity capabilities rarely found in a single resource. Enterprises are establishing internal academies and sponsoring external certifications to close the gap, yet near-term capacity constraints inflate cost structures and slow time-to-value.

Absence of Global Standardized SLA Frameworks

Multinationals struggle to harmonize measurement baselines because vendor SLAs differ by region, industry, and service tier. Custom reconciliation models inflate governance overhead and obscure apples-to-apples performance comparisons. While ITIL and ISO 20000 provide templates, their scope does not address microservice latency metrics or cross-cloud workload commitments, thereby perpetuating fragmentation and limiting the effectiveness of benchmarking.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Momentum Shifts Toward Automation-Centric Solutions

The services tranche accounted for 58.92% of 2025 revenue, thanks to consulting-heavy change-management engagements. However, platform-centric solutions are scaling faster at a 6.42% CAGR, signaling an enterprise pivot toward automation as multi-vendor ecosystems expand. The service integration and management market size for solutions is forecast to hit USD 3.64 billion by 2031, reflecting a strong appetite for pre-built governance engines that lower dependency on scarce human expertise. AI-driven orchestration modules, API-first architectures, and out-of-the-box compliance packs cut configuration time and support self-service onboarding, making technology investments more attractive than ongoing consultancy fees.

Enterprises are increasingly combining lightweight advisory engagements with subscription platforms, thereby blending knowledge transfer and repeatable automation. This hybrid spend pattern underpins sustained growth for system integrators offering solution accelerators rather than pure consulting hours.

As maturity rises, the service integration and management market share of solutions is poised to overtake services in the longer term if current adoption curves persist.

By Service Model: Internal Competence Centers Gain Ground

Hybrid-provider arrangements accounted for 39.20% of 2025 revenue, striking a balance between internal stewardship and selective outsourcing for niche skills. Yet the internal service integrator model is outpacing all peers, advancing at a 7.29% CAGR as organizations formalize in-house SIAM centers of excellence. Catalysts include increased access to certified training, declining tooling complexity, and executive recognition that service integration constitutes a strategic core competence.

External service integrator contracts still flourish where budget constraints or talent shortages prevail, particularly among mid-market firms in highly regulated sectors. Nevertheless, continuous investment in workforce upskilling and automation may tilt the mix toward internal governance over the forecast period, aligning with board-level mandates for tighter oversight of third-party risk.

By Deployment Mode: Public Cloud Closes the Gap on Hybrid Dominance

Hybrid cloud remained the deployment archetype of choice at 47.40% in 2025, allowing sensitive workloads to reside on-prem while elastic capacity bursts to the cloud. However, public-cloud SIAM subscriptions are growing at the fastest rate, with a 7.66% CAGR, supported by hardened security postures, sovereign-cloud zones, and pay-as-you-go economics. The service integration and management market size attributable to public-cloud deployments is expected to reach USD 3.25 billion in 2031, narrowing the difference with hybrid footprints.

Private-cloud and on-prem installations serve retrofit-averse incumbents in defense and critical infrastructure, yet face subdued demand amid capital-expense pressures. SaaS-based orchestration suites also offer instant updates, reducing technical debt and luring organizations that previously deferred platform refreshes due to lengthy upgrade cycles.

By Organization Size: Cloud-Native Platforms Democratize Adoption

Large enterprises accounted for 67.12% of 2025 spending, largely due to their sprawling vendor ecosystems and high compliance exposure. Nonetheless, SME adoption is accelerating at a rate of 6.29% annually, buoyed by low-touch SaaS propositions and consumption-based pricing. SMEs favor pre-configured playbooks and no-code connectors that mask underlying complexity, enabling lean IT teams to enforce unified governance without hiring SIAM veterans.

Vendor roadmaps that prioritize guided workflows, embedded AI support bots, and marketplace plug-ins further lower onboarding friction. As a result, the service integration and management industry now addresses a broader total addressable market than during its consultancy-centric origins.

By End-User Industry: Healthcare Surges While BFSI Retains Primacy

BFSI held 27.08% of 2025 revenue, as stringent operational risk mandates sustain robust demand for end-to-end visibility and audit-ready reporting. Electronic trading platforms, core-banking migrations, and fintech partnerships deepen multi-vendor reliance, elevating SIAM to a board-level imperative.

Healthcare is projected to post the highest CAGR of 8.07% through 2031, driven by the expansion of telehealth, EHR modernization, and connected medical devices that span institutional and cloud boundaries. HIPAA and emerging data-interoperability mandates push providers toward centralized orchestration to guarantee patient-safety SLAs. Manufacturing, retail, and government sectors continue to experience steady uptake as Industry 4.0, omnichannel commerce, and public-sector digitalization introduce complex vendor webs that require meticulous governance.

Geography Analysis

North America maintained its leadership position with a 35.91% share in 2025, driven by early-mover enterprise adoption, an abundance of SIAM talent, and stringent regulatory requirements such as SOX and HIPAA. Growth at a 5.14% CAGR indicates sustained investment as companies modernize legacy estates and integrate multi-cloud strategies. Mature consultancy ecosystems and favorable procurement budgets support sophisticated, large-scale rollouts, reinforcing the region’s status as an innovation hub.

The Asia Pacific is the fastest-growing region, with a 6.98% CAGR through 2031. National digital economy programs in India, China, and key ASEAN nations are driving multi-vendor transformation projects that overwhelm traditional ITSM processes. Foreign direct investment and hyperscaler data-center expansions further complicate service chains, catalyzing demand for SIAM. Enterprises in Japan and South Korea, already steeped in lean operations, are now layering SIAM on top of DevOps pipelines to enhance cross-provider accountability.

Europe demonstrates consistent annual growth of 5.71%, propelled by the GDPR, emerging AI regulations, and tightening third-party risk requirements. ISO 20000 certification drives baseline alignment across providers, while Brexit-driven data-flow uncertainties heighten the need for transparent governance. Germany and the United Kingdom spearhead adoption, whereas Eastern European enterprises accelerate uptake to meet EU harmonization goals. Sustainability directives are adding an environmental-performance dimension to vendor scorecards, extending SIAM KPIs beyond cost and uptime.

Competitive Landscape

Market concentration is moderate. Consulting majors Accenture, IBM, and Tata Consultancy Services capitalize on end-to-end portfolios that blend advisory, implementation, and managed services. ServiceNow differentiates itself through platform depth, acquiring Celonis for USD 2.1 billion to embed process-mining insights and shorten value realization cycles. HCL and Wipro enhance regional coverage via targeted acquisitions and plug-and-play SIAM-as-a-Service offerings that appeal to mid-market buyers.[4]HCL Technologies, “Quarterly Results Q2 2025,” HCLTech.com

Strategic emphasis is shifting to AI-infused orchestration. IBM’s USD 500 million Watson AIOps for SIAM suite predicts disruptions 72 hours in advance, slashing MTTR and boosting customer satisfaction. Capgemini and Tech Mahindra focus on sector-specific accelerators, embedding pre-configured compliance controls tailored to banking, healthcare, and manufacturing sectors. Consulting-heavy incumbents are increasingly bundling tooling subscriptions to fend off platform-first challengers, while hyperscalers hint at integrated SIAM layers within cloud management consoles, foreshadowing the commoditization of baseline features but opening advisory niches for complex, regulated workloads.

Service Integration And Management Industry Leaders

Accenture plc

AtoS SE

Capgemini SE

Fujitsu Limited

HCL Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ServiceNow acquires Celonis for USD 2.1 billion to extend process-mining capabilities across its SIAM platform.

- August 2025: IBM unveils Watson AIOps for SIAM following a USD 500 million R&D outlay to advance predictive incident management.

- July 2025: Accenture partners with Microsoft, allocating USD 300 million to pre-packaged SIAM frameworks for healthcare and BFSI verticals.

- June 2025: TCS inaugurates a USD 150 million SIAM Center of Excellence in Singapore to serve the Asia Pacific clientele.

- May 2025: HCL acquires DXC Technology’s SIAM practice for USD 400 million, boosting North American regulated-industry coverage.

- May 2025: Tech Mahindra debuts an AI-driven analytics suite that forecasts vendor-performance trajectories.

Global Service Integration And Management Market Report Scope

Global Service Integration and Management Market is Segmented By Component (Solutions, Services), Organization Size (Small and Medium Enterprises, Large Enterprises), End-user Industry (BFSI, IT and Telecom, Healthcare, Retail), and Geography.

Service Integration and Management (SIAM) is a management method adopted by organizations that need to manage multiple third-party and internal service providers. It provides the basis for effective governance and management of a multi-service-provider ecosystem by introducing a 'service integrator' role that effectively aggregates and consolidates the services provided (by the multiple service providers) to deliver a cohesive and reliable portfolio of services to the business.

| Solutions | Business Solutions |

| Technology Solutions | |

| Services |

| Single-Provider Model |

| Hybrid-Provider Model |

| Internal Service Integrator Model |

| External Service Integrator Model |

| On-Premise |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Healthcare |

| Retail |

| Manufacturing |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solutions | Business Solutions |

| Technology Solutions | ||

| Services | ||

| By Service Model | Single-Provider Model | |

| Hybrid-Provider Model | ||

| Internal Service Integrator Model | ||

| External Service Integrator Model | ||

| By Deployment Mode | On-Premise | |

| Public Cloud | ||

| Private Cloud | ||

| Hybrid Cloud | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | |

| Information Technology and Telecom | ||

| Healthcare | ||

| Retail | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the service integration and management market in 2031?

It is forecast to reach USD 8.49 billion, growing at a 5.65% CAGR between 2026 and 2031.

Which component segment is growing fastest?

The Solutions segment is expanding at a 6.42% CAGR as enterprises favor automation over exclusive reliance on consulting.

Why is SIAM adoption surging in healthcare?

Telehealth expansion, EHR modernization, and interoperability mandates are pushing healthcare providers toward centralized vendor orchestration, driving an 8.07% CAGR through 2031.

Which region will grow quickest through 2031?

Asia Pacific leads with a 6.98% CAGR thanks to aggressive digital-economy programs and hyperscale cloud expansion.

How are vendors differentiating in the market?

Leading providers embed AI-powered predictive orchestration, acquire process-mining assets, and release sector-specific accelerators to shorten deployment cycles and enhance compliance.

What is the primary talent-related challenge?

A global shortage of SIAM-skilled professionals—estimated at 40% undersupply—extends project timelines and elevates implementation costs.

Page last updated on: