Market Overview

| Study Period | 2020 - 2031 |

|---|---|

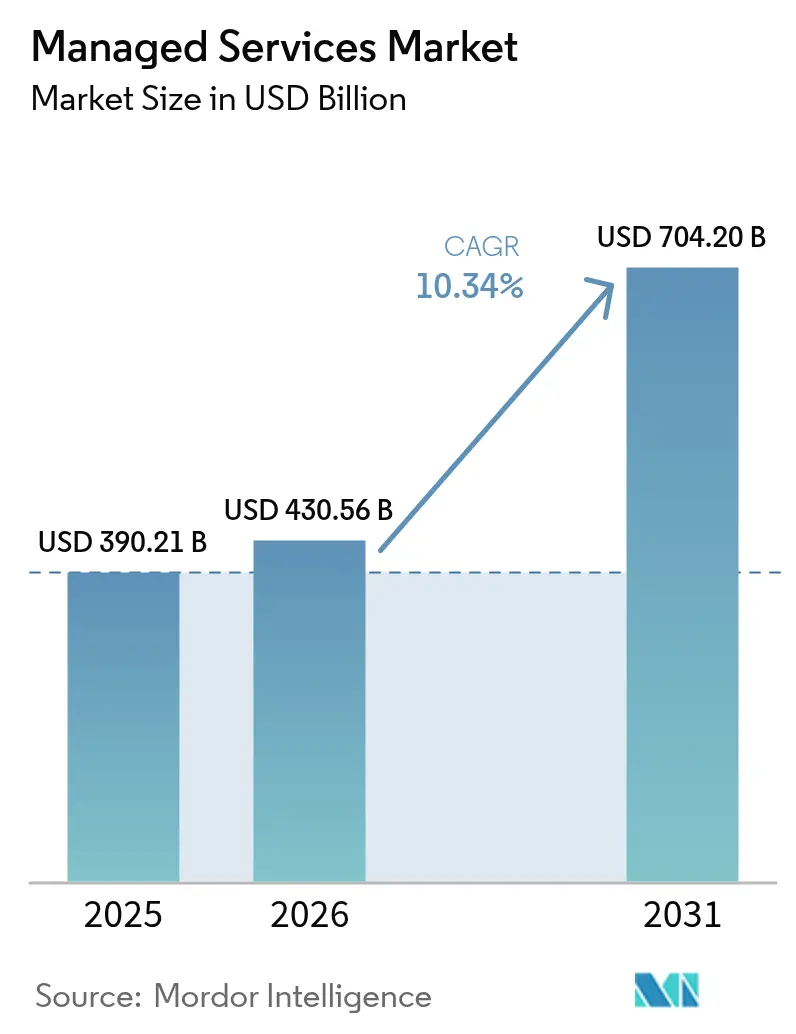

| Market Size (2026) | USD 430.56 Billion |

| Market Size (2031) | USD 704.2 Billion |

| Growth Rate (2026 - 2031) | 10.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Managed Services Market Analysis by Mordor Intelligence

Managed services market size in 2026 is estimated at USD 430.56 billion, growing from 2025 value of USD 390.21 billion with 2031 projections showing USD 704.2 billion, growing at 10.34% CAGR over 2026-2031. The strong growth reflects enterprises’ pivot toward outsourced IT operations as they juggle hybrid-cloud complexity, rising cyber threats, and ongoing budget scrutiny. Cloud-centric delivery models, wider AI adoption, and regulatory pressures are reshaping provider offerings, while competitive differentiation now hinges on intelligent automation and vertical expertise. Strategic outsourcing has shifted from pure cost reduction to a core pillar of digital transformation, accelerating provider investments in security operations centers, multi-cloud orchestration tools, and edge management platforms. M&A activity underscores the appeal of scale, with providers pursuing inorganic growth to fill technology gaps and expand geographic reach.

Key Report Takeaways

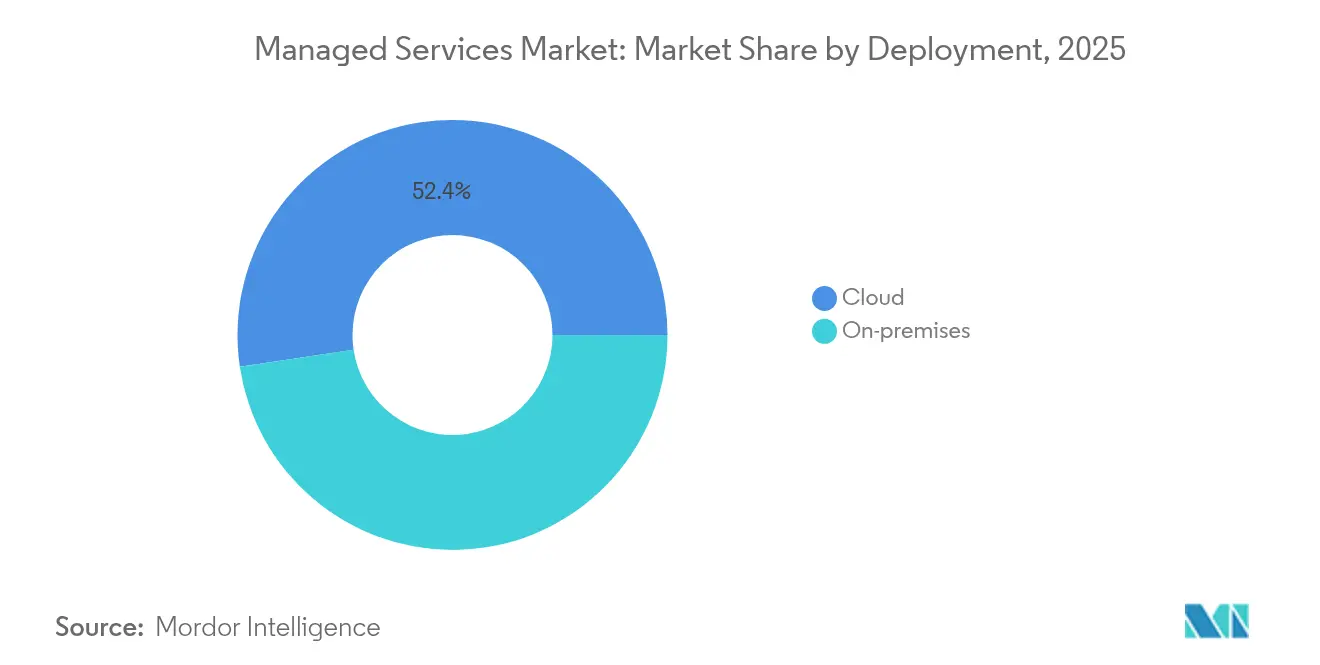

- By deployment, cloud models led with 52.35% revenue share in 2025, while hybrid cloud is projected to log a 11.92% CAGR through 2031.

- By service type, managed infrastructure services accounted for 38.40% of the managed services market share in 2025, whereas managed security services are advancing at an 11.72% CAGR to 2031.

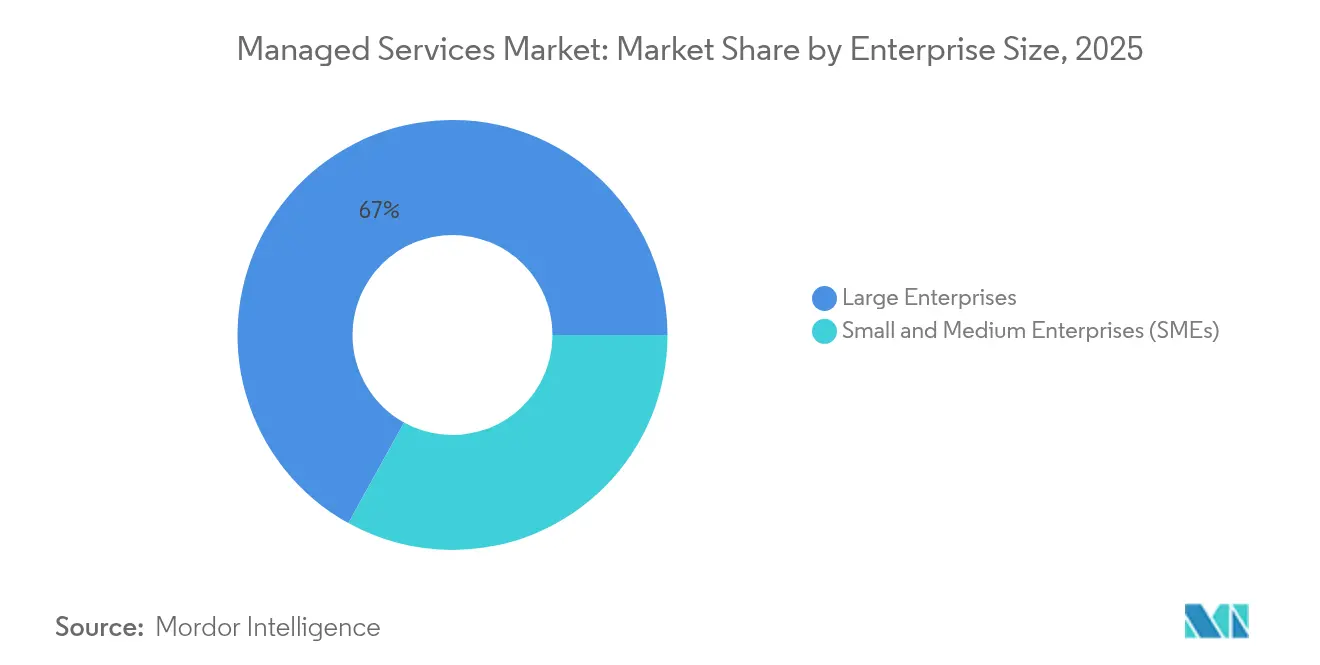

- By enterprise size, large enterprises held 66.95% share of the managed services market size in 2025, but small and medium enterprises are expected to grow at a 10.41% CAGR between 2026-2031.

- By end-user vertical, BFSI captured 34.10% revenue share in 2025; healthcare is forecast to expand at an 11.03% CAGR through 2031.

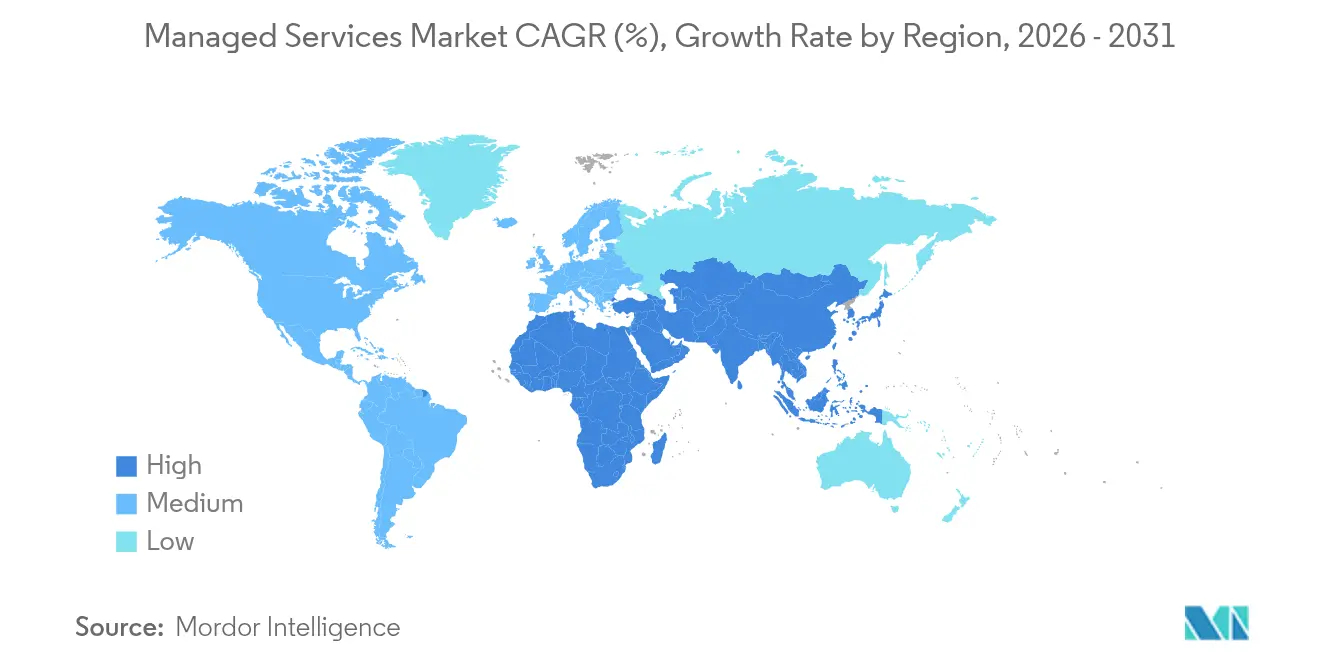

- By geography, North America led with 32.40% revenue share in 2025, while Asia-Pacific is set to post an 11.28% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to hybrid-cloud operating models | +2.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cost-optimization pressure on enterprise IT budgets | +2.1% | Global, particularly acute in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Rising cyber-threat volume and compliance mandates | +1.9% | Global, with heightened impact in BFSI and healthcare | Long term (≥ 4 years) |

| Edge-computing roll-outs demanding remote managed services | +1.4% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Cyber-insurance prerequisites for 24/7 managed detection and response | +1.2% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Sustainability and green-IT regulations driving managed power/cooling | +0.8% | EU leading, with adoption in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid-cloud complexity drives managed services adoption

Hybrid-cloud architectures combine on-premises, private, and multiple public clouds, elevating operational complexity that internal teams struggle to master. Regulatory initiatives such as the Microsoft EU Data Boundary require localized data handling, pushing enterprises toward providers that can guarantee compliance, portability, and unified security policies.[1]Microsoft, “EU Data Boundary Now Available,” microsoft.comSeamless workload portability and real-time policy enforcement across distributed environments cement long-term demand for managed infrastructure and security offerings.

Cost optimization pressures accelerate outsourcing decisions

Persistent margin pressure turns fixed IT overhead into a variable line item through managed services. Large transformation deals such as Accenture’s USD 1.6 billion Cloud One contract with the U.S. Air Force illustrate how enterprises view outsourcing as strategic, not merely tactical.[2]Accenture, “Accenture Federal Services Wins USD 1.6 Billion Cloud One Task Order,” accenture.com Providers bundle automation, AI tooling, and certified talent pools, allowing buyers to avoid up-front capital outlays while still accessing emerging capabilities.

Cybersecurity threat evolution demands specialized response capabilities

Advanced persistent threats, ransomware variants, and strict disclosure mandates require 24/7 monitoring, threat intelligence, and rapid containment actions. Providers with dedicated security operations centers and AI-driven analytics attract enterprises that now face cyber-insurance clauses mandating managed detection and response. The shift underscores why managed security services are the fastest-growing segment of the managed services market.

Edge computing expansion creates remote management requirements

Manufacturing, retail, and telecom firms deploy edge nodes far from data-center hubs. Dell’s alliances with Ericsson and Nokia illustrate how providers package remote monitoring, over-the-air updates, and predictive maintenance to keep dispersed assets online.[3]Dell Technologies, “Dell, Ericsson, Nokia Partner on Edge Innovation,” delltechnologies.com The trend increases demand for managed services that can monitor thousands of micro-sites without local staff.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-sovereignty and privacy regulations | -1.8% | EU leading, expanding globally | Long term (≥ 4 years) |

| Multi-vendor integration and legacy interoperability challenges | -1.4% | Global, particularly acute in large enterprises | Medium term (2-4 years) |

| Vendor lock-in risk and high exit costs of long-term MSP contracts | -1.1% | Global, with heightened concern in North America | Short term (≤ 2 years) |

| Talent shortages within MSPs limiting service-quality scalability | -0.9% | Global, most severe in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty regulations constrain service delivery models

Mandates requiring localized processing force providers to duplicate infrastructure in each jurisdiction, reducing economies of scale and complicating global delivery. Microsoft’s EU Data Boundary illustrates the additional capital and operational overhead that providers must absorb to serve multi-region clients.

Vendor lock-in concerns limit long-term commitments

Enterprises fear switching costs tied to proprietary tooling and custom workflows housed within long contracts. Buyers increasingly demand modular service catalogs, open APIs, and termination flexibility, pressuring providers to rethink pricing and contract terms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Models Drive Market Evolution

Cloud deployment held 52.35% share of the managed services market in 2025 and is widening its lead as hybrid cloud posts a 11.92% CAGR through 2031. The ability to spin up resources on demand, comply with data regulations, and integrate edge workloads explains why enterprises migrate from on-premises models. Hyperscaler alliances, like Accenture’s engagement on Cloud One, show how co-innovation can unlock large multiyear deals.

The managed services market benefits as cloud deployment allows providers to pool infrastructure, automate patches, and roll out AI-driven cost-optimization at scale. Private cloud remains relevant for data-sensitive sectors, while on-premises services persist for legacy workloads that cannot be refactored easily. Providers that master multi-cloud orchestration and FinOps reporting are best positioned to capture new spend.

By Service Type: Infrastructure and Security Lead Growth

Managed infrastructure services owned 38.40% revenue in 2025, reflecting the baseline need to keep heterogeneous estates running. Yet managed security services lead growth with an 11.72% CAGR, mirroring board-level concern over ransomware and compliance fines. AI-enabled threat hunting, zero-trust rollouts, and automated incident containment set market winners apart.

The managed services market size for security offerings is expected to accelerate as cyber-insurance carriers tighten underwriting criteria. Providers are bundling SOC-as-a-service with compliance reporting and tabletop exercises, creating high-margin recurring revenue. Network and communication services gain from 5G roll-outs, while data-center energy management products ride sustainability mandates.

By Enterprise Size: SME Adoption Accelerates

Large enterprises accounted for 66.95% of 2025 revenue, but SME uptake is growing faster at 10.41% CAGR as packaged offerings hit price points from USD 99 to USD 250 per user per month. Standardized bundles covering endpoint management, backup, and SOC access remove entry barriers.

The managed services market is turning into a volume play, with providers investing in self-service portals and AI chatbots to support thousands of smaller customers efficiently. SME buyers value predictable monthly costs and turnkey compliance over bespoke customization, rewarding providers that can deliver scale without sacrificing service quality.

By End-user Vertical: BFSI Leadership with Healthcare Acceleration

BFSI held 34.10% of revenue in 2025, underpinned by stringent data protection laws and real-time payment platforms. The sector’s focus on zero-downtime operations drives demand for advanced resiliency and risk reporting. Healthcare, however, shows an 11.03% CAGR as telehealth, electronic health records, and device security create acute expertise gaps.

The managed services market share in healthcare is poised to rise as governments fund digital hospital programs and mandate strict breach disclosures. Providers offering HIPAA-aligned architectures, clinical IoT monitoring, and patient-data analytics gain a competitive edge. Manufacturing and retail also accelerate adoption to support Industry 4.0 and unified commerce initiatives.

Geography Analysis

North America retained 32.40% revenue share in 2025, buoyed by early cloud migration, cyber regulations, and high IT spend. Federal programs such as the U.S. Air Force Cloud One create visibility for large managed services contracts. BFSI and healthcare customers continue to anchor demand, and providers use the region as a launchpad for AI and edge pilots.

Asia-Pacific is the fastest-growing region at 11.28% CAGR to 2031. China’s manufacturing upgrades, India’s digital-public-infrastructure push, and Japan’s aging plant modernization funnel spend toward providers capable of bridging legacy and cloud workloads. Hyperscalers team with local MSPs to address sovereign-cloud requirements, while ASEAN governments adopt cloud-first mandates that shorten sales cycles.

Europe shows steady expansion as GDPR, Digital Operational Resilience Act, and sustainability rules heighten compliance complexity. Germany drives Industry 4.0 managed services, the United Kingdom leans on MSPs for post-Brexit financial regulation, and France emphasizes sovereign-cloud frameworks. Providers differentiate through localized data centers and green-energy sourcing to meet environmental targets. The Middle East and Africa remain nascent but grow quickly on smart-city and e-government projects.

Competitive Landscape

Competition is intensifying as global SIs, hyperscalers, and pure-play MSPs vie for wallet share. Consolidation hit 182 transactions in Q2 2024, with acquirers seeking AI, security, and industry-vertical depth. Scale matters, yet niche specialists prosper by focusing on high-growth micro-verticals such as renewable-energy monitoring or clinical IoT security.

Technology investment creates moats. Accenture has built a USD 450 million generative-AI pipeline that automates code remediation and policy compliance, improving delivery margins and client outcomes. Dell aligns with Ericsson and Nokia to embed edge orchestration into 5G roll-outs, while IBM unveils renewable-energy monitoring suites that merge OT and IT data for sustainability governance.

Partner ecosystems influence share gains. Providers with strong hyperscaler certifications secure co-sell opportunities and preferential funding. Others bet on open-source automation and FinOps tooling to cut operating costs and pass savings to clients. Talent wars persist, pushing vendors to invest in learning academies and global delivery centers to ensure scalable, 24/7 support.

Managed Services Industry Leaders

Fujitsu Ltd

Cisco Systems Inc.

IBM Corporation

AT&T Inc.

HP Development Company LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Accenture Federal Services won a USD 1.6 billion task order to enhance the U.S. Air Force Cloud One environment, including automated financial governance.

- March 2025: Arrow Electronics launched an AI platform for North American channel partners, adding managed AI deployments to its security and cloud catalog.

- December 2024: Accenture posted USD 17.7 billion Q1 FY2025 revenue, with managed services up 11% to USD 8.6 billion.

- November 2024: Dell expanded 5G and edge collaborations with Ericsson and Nokia to bolster edge-management services.

Global Managed Services Market Report Scope

Managed service is the practice of outsourcing on a proactive basis certain processes and functions intended to improve operations and cut expenses. It simplifies IT operations, increases user satisfaction, and improves service quality while reducing operating costs. Managed services options range from short-term post-go-live assistance to long-term application operations.

The scope of the study includes segmentation by deployment, type, enterprise size, end-user vertical, and geography. Under the segmentation by type, managed data center, managed security, communications, network, infrastructure, and mobility have been considered. The market estimates indicate the revenues accrued through the above-managed service types across various geographies. The impact of COVID-19 has also been considered for market estimation and future projections.

Under the end-user vertical, BFSI, IT and telecommunication, healthcare and hospitality, entertainment and media, retail, manufacturing, government, and other end-user verticals have been considered. The deployment has been considered through on-premise and cloud-type solutions. The enterprise size considered includes small and medium enterprises and large enterprises. North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa have been considered under geography.

The market sizes and forecasts are provided in terms of value (USD billion) for all the above segments.

By Deployment

| On-premise | |

| Cloud | Public Cloud |

| Private Cloud | |

| Hybrid Cloud |

By Service Type

| Managed Data Center |

| Managed Security |

| Managed Communications |

| Managed Network |

| Managed Infrastructure |

| Managed Mobility |

| Others |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By End-user Vertical

| BFSI |

| IT and Telecommunication |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Energy and Utilities |

| Media and Entertainment |

| Others (Education, Non-Profit) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment | On-premise | ||

| Cloud | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Service Type | Managed Data Center | ||

| Managed Security | |||

| Managed Communications | |||

| Managed Network | |||

| Managed Infrastructure | |||

| Managed Mobility | |||

| Others | |||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-user Vertical | BFSI | ||

| IT and Telecommunication | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Media and Entertainment | |||

| Others (Education, Non-Profit) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the managed services market?

The managed services market is valued at USD 430.56 billion in 2026.

How fast is the managed services market expected to grow?

It is projected to reach USD 704.2 billion by 2031, translating to a 10.34% CAGR.

Which deployment model is most popular in managed services?

Cloud deployment models dominate with 52.35% share in 2025, and hybrid cloud shows the fastest growth trajectory.

Why are managed security services growing faster than other service types?

Rising cyber-threat levels and stricter compliance mandates require 24/7 monitoring and specialized expertise that most enterprises lack internally.

Which region offers the highest growth potential for providers?

Asia-Pacific is forecast to expand at an 11.28% CAGR through 2031 thanks to rapid digital transformation across manufacturing, financial services, and public sectors.

Page last updated on: