Brand Activation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

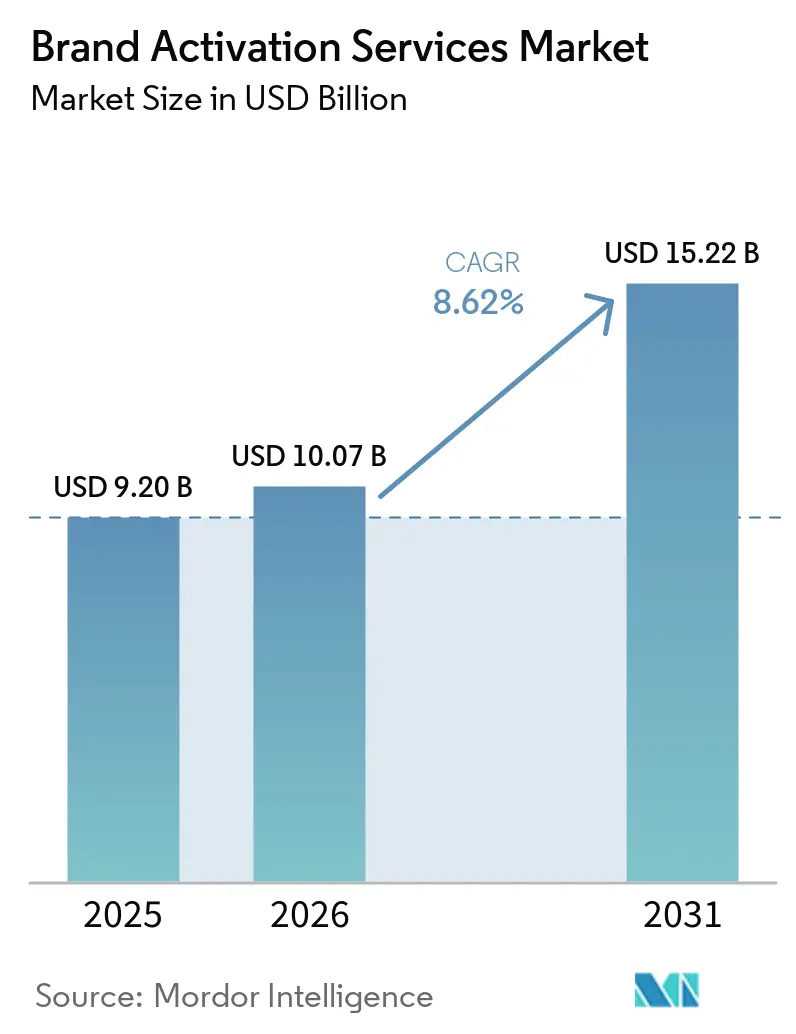

| Market Size (2026) | USD 10.07 Billion |

| Market Size (2031) | USD 15.22 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

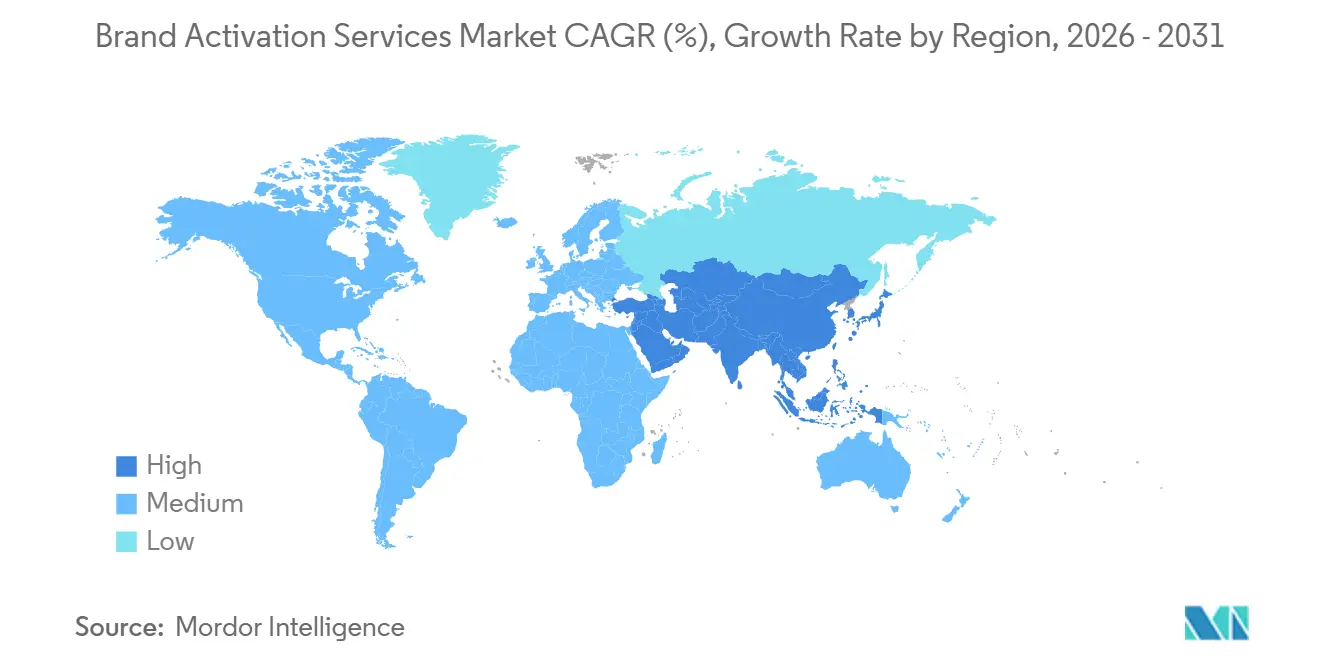

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brand Activation Services Market Analysis by Mordor Intelligence

The brand activation services market size is expected to grow from USD 9.20 billion in 2025 to USD 10.07 billion in 2026 and is forecast to reach USD 15.22 billion by 2031 at 8.62% CAGR over 2026-2031. In 2026, the brand activation services market is at a point where enterprise marketing teams treat activation as a recurring demand-generation line item rather than a discretionary event expense. That shift is raising performance scrutiny and pushing more clients toward formal procurement, longer contracts, and a smaller group of vendors that can manage scale and reporting. Growth in the brand activation services market also reflects a broader shift away from passive media toward formats that drive direct audience participation, clearer purchase signals, and stronger first-party data capture. North America remains the largest revenue base because it combines agency scale, sponsorship depth, and premium event infrastructure, while Asia-Pacific is driving the brand activation services market's fastest regional momentum through digitally fluent consumer behavior and hybrid formats. Competition remains moderate to high, leading agencies in the brand activation services market to balance execution scale, technology integration, and measurable commercial outcomes.

Key Report Takeaways

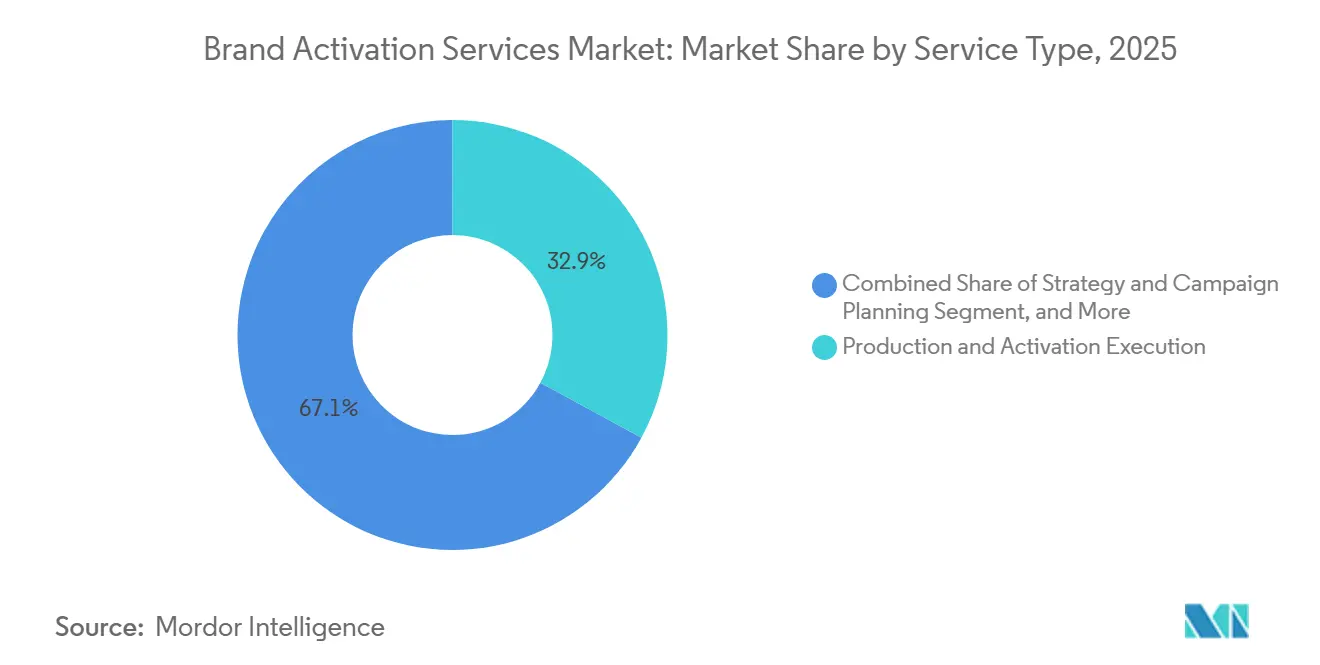

- By service type, Production and Activation Execution held 32.92% of the brand activation services market share in 2025, while Technology and Digital Layer Integration is projected to expand at a 9.42% CAGR through 2031.

- By end-use industry, Retail and Consumer Goods held a 22.74% share in 2025, while Technology and Telecommunications is projected to grow at a 10.58% CAGR through 2031.

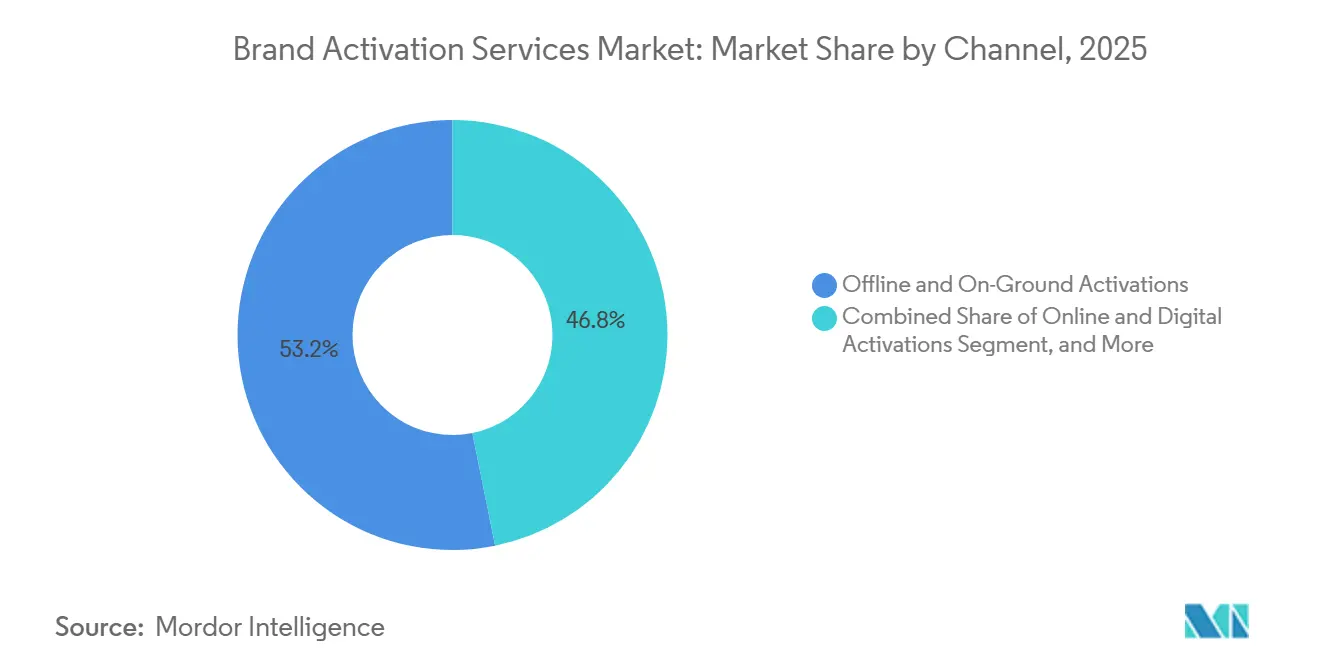

- By channel, Offline and On-Ground Activations accounted for 53.18% of revenue in 2025, while Hybrid Activations are projected to expand at a 9.19% CAGR through 2031.

- By geography, North America held 34.92% share in 2025, while Asia-Pacific is projected to grow at a 9.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Brand Activation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Reallocation Toward Measurable Experiential Spend | +2.5% | Global | Short term (≤ 2 years) |

| Rising Demand for First-Party Data Capture and Consent-Based Engagement | +1.8% | North America and Europe, early, spillover to Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Expansion of Hybrid and Digital Amplification Layers | +1.6% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Higher Brand Trust and Recall From In-Person Participation | +1.2% | Global | Short term (≤ 2 years) |

| Retail Media and Creator Commerce Convergence Expands Shopper Activation Budgets | +1.0% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Micro-Activations and Modular Pop-Ups Improve Unit Economics | +0.7% | Asia-Pacific core, spillover to North America and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Reallocation Toward Measurable Experiential Spend

Marketing teams are allocating more budget to programs that clearly connect to engagement, lead quality, and purchase intent. In the brand activation services market, this matters because activation is no longer being treated as a one-off support activity for large campaigns. Once brands classify activation as an ongoing channel, they apply the same governance as media buying, including procurement reviews, reporting rules, and multi-year planning. That shift is raising the value of agencies that can connect event activity with owned audience data and downstream commercial actions. It is also making the brand activation services market more favorable to vendors that can support large, repeatable programs instead of isolated events.

Rising Demand for First-Party Data Capture and Consent-Based Engagement

Live and live-digital activation formats are gaining value because they generate direct consent signals that are easier to document than those from rented digital audiences. In February 2025, Adobe launched Real-Time CDP Collaboration in the United States, enabling advertisers and publishers to work with consent-driven first-party data without directly exposing identifiable customer information. In July 2025, the California Privacy Protection Agency approved final text for a rulemaking package covering automated decision-making technology, risk assessments, and annual cybersecurity audits.[1]California Privacy Protection Agency, “CPPA Board Approves Final Text of Second Rulemaking Package,” California Privacy Protection Agency, cppa.ca.gov These changes are raising the compliance standard for data-rich event programs and giving an advantage to activation partners with stronger consent and data-handling processes. As a result, the brand activation services market is benefiting from a wider client need for audience acquisition that is both measurable and privacy-aware.

Expansion of Hybrid and Digital Amplification Layers

Hybrid formats are no longer simple livestream extensions of physical events. In the brand activation services market, they are becoming structured systems that turn one activation into both a live audience experience and a stream of reusable digital assets. Brands are using QR interactions, NFC touchpoints, augmented layers, and real-time content capture to extend reach beyond the venue itself. The economics are improving because the added digital layer can reuse the same production spend across owned, earned, and paid channels. This is helping the brand activation services market grow faster in programs where clients want both event engagement and content output from the same budget.

Higher Brand Trust and Recall From In-Person Participation

Physical participation still creates a level of familiarity and recall that passive exposure rarely matches. That effect is especially important in categories where buyers want to handle products, speak with staff, or validate decisions in a social setting. The brand activation services market benefits from this, as in-person environments can move audiences from awareness to qualified interest more directly. George P. Johnson's work at NRF 2026 demonstrated how enterprise technology brands used immersive retail theater to drive stronger purchase engagement among attendees. As more brands compare these outcomes with those of lower-performing passive channels, the brand activation services market is likely to continue gaining budget priority.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Return on Investment Attribution and Measurement Gaps | -1.8% | Global | Short term (≤ 2 years) |

| Rising Production, Venue, Labor, and Logistics Costs | -1.4% | North America and Europe, spillover to Asia-Pacific core markets | Medium term (2-4 years) |

| Privacy Compliance Friction in Data-Rich Activations | -0.9% | Europe, North America | Medium term (2-4 years) |

| Retail Media Fragmentation Raises Execution Complexity | -0.7% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Return on Investment Attribution and Measurement Gaps

Attribution remains the clearest limit on faster spending growth. Many activation programs still capture attendance, scans, or immediate leads, but they do not connect those signals cleanly to purchase behavior that appears weeks later. In the brand activation services market, this creates a reporting gap that makes finance teams less willing to expand budgets at pace. The problem becomes larger when brands plan the experience first and add measurement only after the event is complete. Agencies that build consent capture, behavioral tracking, and CRM linkage into the brief from the start are better placed to protect spending in the brand activation services market.

Rising Production, Venue, Labor, and Logistics Costs

Production, staffing, venue rental, and logistics still take up most of the budget in large activation programs. Cost pressure in these areas is raising clients' break-even points and compressing agency margins. In the brand activation services market, that pressure is pushing agencies toward reusable builds, modular set design, and city-to-city rotation models that lower incremental spend. Smaller pop-up formats are also becoming more attractive to brands seeking frequency without the cost of full-scale touring executions. If this shift continues, the brand activation services market may see average contract values come under pressure even while program volumes keep rising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type, Technology Integration Reshapes The Revenue Mix

Production and Activation Execution held 32.92% of the brand activation services market share in 2025, making it the largest service line. That lead reflects the continuing importance of logistics, fabrication, staffing, and on-site management in large-scale activation programs. The segment remains central because many global clients still need consistent execution across multiple venues and markets. Strategy and Campaign Planning, along with Creative and Experience Design, continue to matter because clients want stronger advisory input before production begins.

Technology and Digital Layer Integration is projected to expand at a 9.42% CAGR from 2026 to 2031, making it the fastest-growing service type in the brand activation services market. The shift is supported by the growing use of immersive digital layers, interactive tools, and audience data systems in live programs. George P. Johnson’s NRF 2026 work reflects how technology-led experience design is becoming part of core activation delivery rather than a peripheral add-on.[2]George P. Johnson, “Powering the Future of Retail at NRF 2026,” George P. Johnson, gpj.com This changes the service mix because digital components can extend the value of a single physical event across multiple content and audience channels. Over time, that trend should continue to elevate the role of technology integration in the brand activation services market.

By End-Use Industry, Retail Scale Anchors Demand While Technology Verticals Accelerate

Retail and Consumer Goods accounted for 22.74% of the brand activation services market in 2025, making it the largest end-use segment. The category depends heavily on in-store sampling, shopper programs, and pop-up experiences to support trial and defend shelf movement. Food and Beverage, Beauty, and Personal Care also remain important because physical interaction often improves conversion rates in sensory product categories. Media and Entertainment, together with Travel and Hospitality, continue to use activations tied to launches, fan engagement, and destination-based experiences.

Technology and Telecommunications is projected to grow at a 10.58% CAGR through 2031, making it the fastest-growing vertical in the brand activation services market. This reflects the need for live product launches, trade event participation, and high-engagement demonstrations in a category where buyers often expect direct interaction. George P. Johnson’s NRF 2026 case study also supports the role of immersive formats in enterprise technology engagement. Automotive, Healthcare and Pharmaceuticals, and Banking, Financial Services, and Insurance remain important mid-tier verticals because activation supports more complex and trust-based purchase journeys in these sectors.

By Channel, Offline Leadership Continues While Hybrid Formats Gain Ground

Offline and On-Ground Activations accounted for 53.18% of revenue in 2025, giving physical formats the largest channel position in the brand activation services market. That lead reflects the continuing role of retail locations, exhibitions, public venues, and event spaces as the main settings for direct brand interaction. Even so, offline formats are evolving as brands increasingly add QR codes, NFC touchpoints, and digital audience-capture tools to physical events. This makes physical activation more measurable and more useful within broader customer acquisition systems.

Hybrid Activations is projected to expand at a 9.19% CAGR from 2026 to 2031, making it the fastest-growing channel in the brand activation services market. The appeal comes from using one production cycle to support live participation, digital engagement, and downstream media use at the same time. That model is becoming more valuable as clients look for content, audience data, and measurable interaction from the same spend. The result is a channel mix in which hybrid programs are increasingly treated as integrated media and experience systems, rather than a simple blend of offline and online elements.

Geography Analysis

North America held 34.92% of the brand activation services market share in 2025, making it the leading regional segment. The region benefits from strong agency density, mature sponsorship culture, premium event infrastructure, and a large base of enterprise clients. The United States remains the main demand center because major sports, entertainment, and corporate calendars support year-round activation planning. This keeps North America at the center of multi-market assignments in the brand activation services market.

Asia-Pacific is projected to grow at a 9.73% CAGR from 2026 to 2031, making it the fastest-growing geography in the brand activation services market. The region is benefiting from urban consumer expansion, mobile-first shopping behavior, and stronger links between creator ecosystems and commerce-led experiences. China’s experience economy reached CNY 18.4 trillion (USD 2.56 trillion) by November 2025, according to the China Academy of Information and Communications Technology. That scale is supporting wider demand for experience-led formats in retail and consumer engagement. Asia-Pacific, therefore, remains an important growth engine for the brand activation services market.

Europe is a mature, privacy-conscious region where compliance requirements shape how first-party data is collected at events. The California privacy rulemaking and Adobe’s consent-focused collaboration model both reflect the wider commercial direction toward stronger governance in audience data use. South America is recovering as consumer-facing sectors rebuild spending momentum, while Africa remains the smallest region but shows early growth in modular and cost-efficient activation formats. This leaves the brand activation services market with a mix of mature regulated regions and faster-growth emerging regions.

Competitive Landscape

The brand activation services market remains fragmented, with global live experience networks, specialized independent agencies, and regional creative groups competing for similar client budgets. Agencies are trying to separate themselves through technology integration, delivery scale, data management, and stronger operational structure. In February 2026, The Freeman Company formally launched a unified parent architecture for nine category-leading live experience brands, bringing them under one integrated service model.[3]The Freeman Company, “The Freeman Company (TFC) Unites Category Leading Brands as the Industry’s Most Comprehensive Live Experience Partner,” The Freeman Company, thefreemancompany.com That move shows how leading firms are trying to simplify enterprise buying and strengthen cross-service delivery within the brand activation services market. It also suggests that organizational structure is becoming a competitive tool alongside creative output.

Measurement capability is becoming another point of separation in the brand activation services market. Adobe’s Real-Time CDP Collaboration launch in 2025 highlighted how advertisers and publishers are building privacy-aware, consent-driven data workflows for audience activation and campaign measurement. Activation agencies that can work within those systems are better placed to support clients who want clearer post-event accountability. This is especially relevant as more brands expect event data to feed into broader CRM, media, and audience management frameworks.

Experience quality still matters as much as platform capability. George P. Johnson’s NRF 2026 case illustrates how immersive environments can turn trade show participation into stronger commercial engagement for enterprise technology brands.[4]George P. Johnson, “Powering the Future of Retail at NRF 2026,” George P. Johnson, gpj.com Momentum Worldwide’s recognition as Campaign US Experiential Agency of the Year for the third straight year in 2025 also reflects the continued importance of strong brand experience design. Together, these examples show that the brand activation services market remains competitive because no single capability set fully defines leadership across all client programs.

Brand Activation Services Industry Leaders

Momentum Worldwide, LLC

George P. Johnson Company

Jack Morton Worldwide

Freeman Expositions, Inc.

GMR Marketing LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cheil Worldwide launched its From Agency to Agentic three-day technology showcase in Seoul, demonstrating AI-powered campaign generation, data-driven personalization, and agentic marketing capabilities designed to deliver measurable activation outcomes for clients. The event signaled a strategic repositioning of the agency from a campaign execution partner to a marketing technology solution provider at scale.

- April 2026: INNOCEAN India delivered the Hyundai Motor Company ICC Men's T20 World Cup 2026 campaign, blending on-ground activation, digital integration, and real-time engagement through its Unified Marketing OS. The program reached 253 million unique users across social platforms and generated 856 million total engagements, demonstrating the scale achievable when a major sports sponsorship activation is designed as a fully integrated physical and digital system.

- March 2026: The Freeman Company launched Freeman Blue Echo, a proprietary AI-assisted 3D venue visualization platform enabling planners and clients to preview event configurations interactively before physical build-out. Developed entirely in-house without third-party licensing, the platform began rolling out to Freeman's full client portfolio at no additional cost, positioning it as a competitive differentiator in the enterprise event management segment.

- March 2026: George P. Johnson delivered the Xiaomi 2026 New Product Launch in Barcelona, executed ahead of Mobile World Congress and spanning strategy, creative, production, fabrication, content, and on-site operations across a cross-functional global team. The project reinforced GPJ's end-to-end capability for time-critical large-scale technology product activations at major international industry events.

Global Brand Activation Services Market Report Scope

The Brand Activation Services Market encompasses specialized marketing services focused on creating, designing, and executing immersive brand experiences to increase consumer engagement, awareness, and loyalty. These services include strategy and campaign planning, creative and experience design, production and activation execution, and integration of technology and digital layers to deliver unified brand interactions across physical and digital touchpoints.

The Brand Activation Services Market is Segmented by Service Type ( Strategy and Campaign Planning, Creative and Experience Design, Production and Activation Execution, and Technology and Digital Layer Integration), End-Use Industry (Retail and Consumer Goods, Food and Beverage, Beauty and Personal Care, Automotive, Technology and Telecommunications, BFSI, Healthcare and Pharmaceuticals, Media and Entertainment, Travel and Hospitality, and Other End-Use Industries), Channel (Offline and On-Ground Activations, Online and Digital Activations, and Hybrid Activations), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Strategy and Campaign Planning |

| Creative and Experience Design |

| Production and Activation Execution |

| Technology and Digital Layer Integration |

| Retail and Consumer Goods |

| Food and Beverage |

| Beauty and Personal Care |

| Automotive |

| Technology and Telecommunications |

| Healthcare and Pharmaceuticals |

| BFSI |

| Media and Entertainment |

| Travel and Hospitality |

| Other End-use Industries |

| Offline and On-Ground Activations |

| Online and Digital Activations |

| Hybrid Activations |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Rest of the Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Strategy and Campaign Planning | |

| Creative and Experience Design | ||

| Production and Activation Execution | ||

| Technology and Digital Layer Integration | ||

| By End-use Industry | Retail and Consumer Goods | |

| Food and Beverage | ||

| Beauty and Personal Care | ||

| Automotive | ||

| Technology and Telecommunications | ||

| Healthcare and Pharmaceuticals | ||

| BFSI | ||

| Media and Entertainment | ||

| Travel and Hospitality | ||

| Other End-use Industries | ||

| By Channel | Offline and On-Ground Activations | |

| Online and Digital Activations | ||

| Hybrid Activations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the brand activation services market?

The brand activation services market stands at USD 10.07 billion in 2026 and is forecast to reach USD 15.22 billion by 2031 at an 8.62% CAGR over 2026-2031.

What is driving demand for brand activation services in 2026?

Demand is being supported by budget reallocation toward measurable experiential programs, stronger demand for first-party data capture, and wider use of hybrid activation formats.

Which service type leads revenue in brand activation services?

Production and Activation Execution led with a 32.92% share in 2025 because large programs still depend on logistics, fabrication, and on-ground delivery at scale.

Which end-use vertical is expanding the fastest?

Technology and Telecommunications is projected to grow at a 10.58% CAGR through 2031 as product launches, developer events, and trade show programs remain central to buyer engagement.

Which channel is growing fastest across activation programs?

Hybrid Activations is projected to expand at a 9.19% CAGR through 2031 because one program can serve live engagement, content creation, and digital amplification at the same time.

Which region offers the strongest growth outlook for activation providers?

Asia-Pacific is projected to grow at a 9.73% CAGR through 2031, supported by urban consumer growth, mobile-first behavior, and stronger creator-commerce ecosystems.

Page last updated on: