GPU Foundry Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.73 Billion |

| Market Size (2031) | USD 54.86 Billion |

| Growth Rate (2026 - 2031) | 25.35% CAGR |

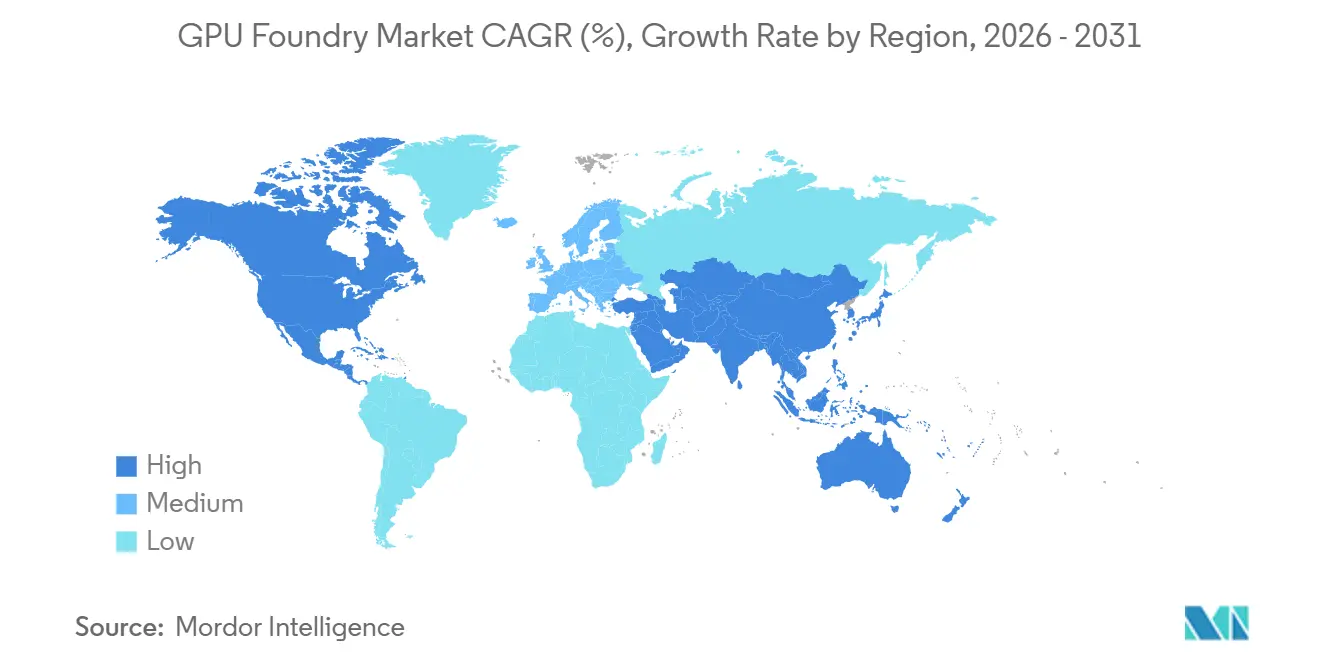

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Foundry Market Analysis by Mordor Intelligence

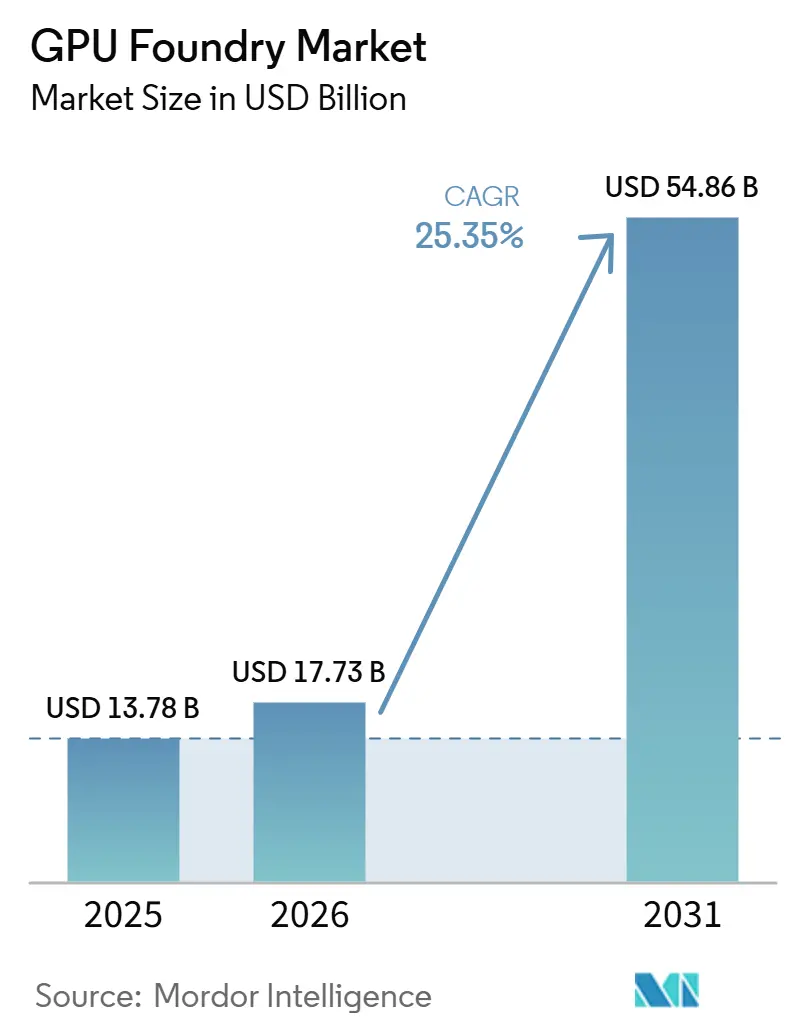

The GPU foundry market size is expected to increase from USD 13.78 billion in 2025 to USD 17.73 billion in 2026 and reach USD 54.86 billion by 2031, growing at a CAGR of 25.35% over 2026-2031. The GPU foundry market is moving through a structural shift where advanced-node wafer fabrication and chiplet-ready packaging have become core infrastructure for large-scale AI computing. Order visibility remains unusually strong across leading-edge nodes, and that keeps capacity planning, customer qualification, and packaging access at the center of commercial decision making in the GPU foundry market. Hyperscale AI buildouts, sovereign compute procurement, and domestic semiconductor programs are widening the demand base beyond a single customer group and are giving the GPU foundry market a more durable demand profile than earlier semiconductor cycles. Competitive strategy is now centered on node leadership, advanced packaging integration, trusted manufacturing geography, and the ability to support more than one tape-out path across AI, automotive, and edge programs. The clearest opportunities in the GPU foundry market remain tied to suppliers that can align front-end process technology, packaging readiness, and regional manufacturing footprints with the deployment schedules of AI infrastructure customers.

Key Report Takeaways

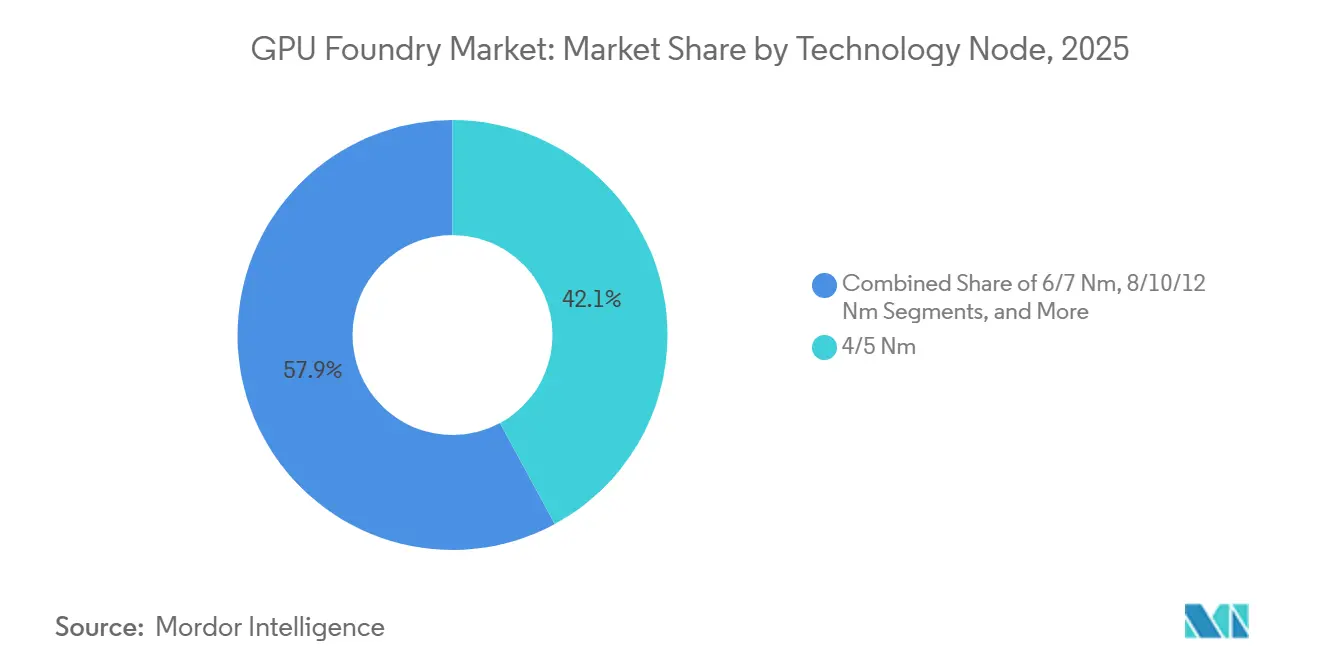

- By technology node, 4/5 nm held 42.11% of the GPU foundry market share in 2025, and 3 nm and below is projected to expand at a 26.21% CAGR through 2031.

- By wafer size, 300 mm accounted for 96.33% of the GPU foundry market size in 2025, and the same segment is projected to grow at a 26.62% CAGR through 2031.

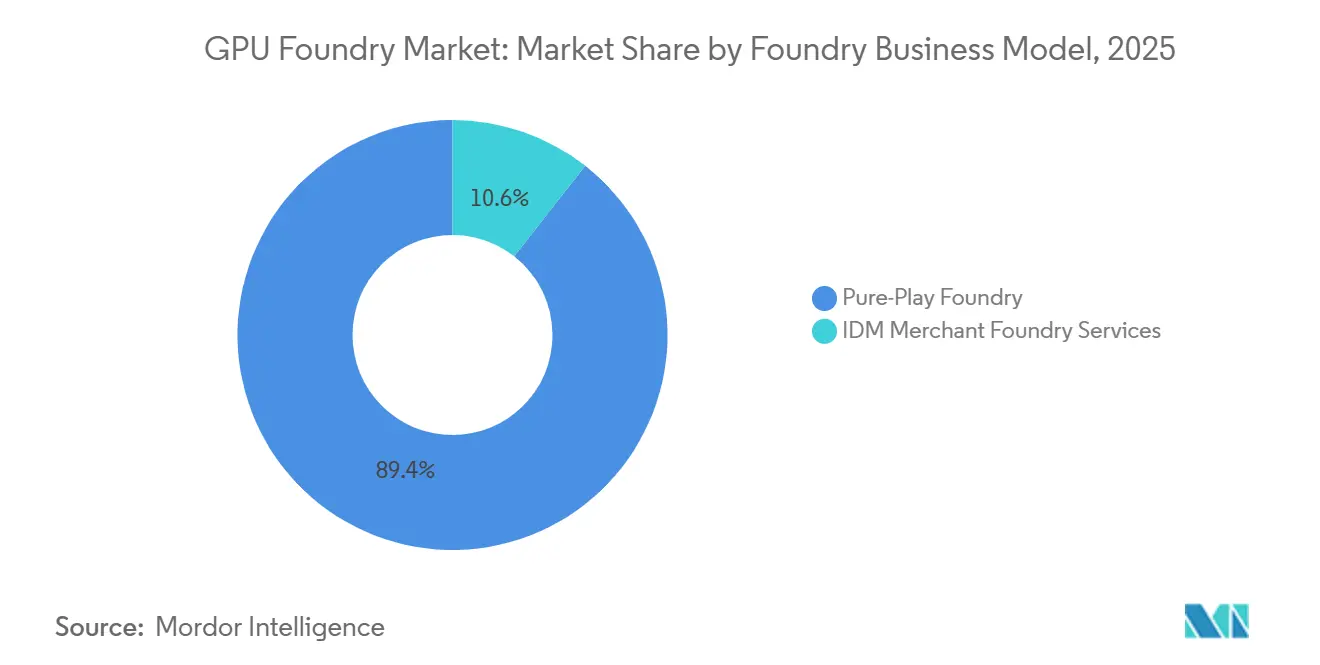

- By foundry business model, pure-play foundries held 89.42% share in 2025, and IDM Merchant Foundry Services is expected to record the fastest CAGR at 26.53% through 2031.

- By application, Data Center AI and HPC accounted for 63.12% share of the GPU foundry market size in 2025, and automotive is projected to expand at a 26.32% CAGR through 2031.

- By geography, North America held 68.44% share in 2025, and Asia-Pacific is projected to post the highest regional CAGR at 26.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Foundry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale AI Training and Inference Cluster Expansion | +8.0% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Enterprise AI Factory and Sovereign Compute Procurement | +5.5% | Global, with early intensity in North America, Middle East, and India | Short term (≤ 2 years) |

| AI Accelerator Race for Sub-5 nm Advanced Nodes | +4.5% | Global, led by North America fabless designers and manufactured in Asia-Pacific | Short term (≤ 2 years) |

| Chiplet-Based GPU Roadmaps Improving Yield and Product Scaling | +2.5% | Global, with advanced packaging clusters in Taiwan, South Korea, and Arizona | Medium term (2-4 years) |

| Industry Demand for Trusted Domestic Fabs | +2.0% | North America and Europe, with spillover to Japan and India | Medium term (2-4 years) |

| Foundry Capacity Lock-In Through Long-Term AI Supply Agreements | +1.5% | Global, anchored in North America and East Asia supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale AI Training and Inference Cluster Expansion

Hyperscale spending remains the main demand engine for the GPU foundry market because cloud platforms are building AI capacity at the same time that enterprise customers are broadening inference use cases. The GPU foundry market now supports both large training clusters and recurring inference deployments, and that creates a steadier replenishment cycle for high-end wafer demand than one-off procurement waves. This matters because the installed base of AI systems has to be refreshed, expanded, and regionally duplicated as performance requirements rise and service latency becomes more important. The growth of in-house accelerators at major cloud firms also means the GPU foundry market is no longer tied to a single chip designer, since more custom silicon programs now compete for advanced-node capacity. NVIDIA stated that Blackwell wafer production is underway in Phoenix and that it plans to produce up to USD 500 billion of AI infrastructure in the US with partners, which shows how AI demand is now pulling on both leading-edge wafer starts and downstream system manufacturing capacity.[1]NVIDIA Corporation, “The Engines of American-Made Intelligence, NVIDIA and TSMC Celebrate First NVIDIA Blackwell Wafer Produced in the US,” NVIDIA Blog, blogs.nvidia.com

Enterprise AI Factory and Sovereign Compute Procurement

Enterprise AI factory programs and sovereign compute plans are giving the GPU foundry market a broader demand base that is less dependent on pure commercial optimization. Procurement is increasingly shaped by resilience, domestic production preferences, and the need for trusted supply, which raises the value of foundries that can point to certified capacity across more than one geography. TSMC expanded its planned US investment to USD 165 billion in March 2025, and that package includes three new fabs, two advanced packaging facilities, and a major R&D center in Arizona.[2]TSMC, “TSMC Intends to Expand Its Investment in the United States to USD165 Billion to Power the Future of AI,” TSMC, pr.tsmc.comNVIDIA also said its US manufacturing network for AI infrastructure now spans partners across semiconductors, boards, systems, and racks, which supports the view that sovereign and enterprise buyers want more local control over the AI hardware stack. GlobalFoundries added another domestic signal with a USD 16 billion US investment focused on facility expansion, packaging innovation, silicon photonics, and next-generation GaN, and that supports a wider sourcing field inside the GPU foundry market even where leading-edge share remains concentrated.

AI Accelerator Race for Sub-5 Nm Advanced Nodes

Competition among AI chip designers is keeping the GPU foundry market focused on sub-5 nm nodes because training accelerators, inference chips, and custom AI processors all need higher performance per watt. The GPU foundry market is therefore being shaped by parallel roadmaps rather than a single flagship product cycle, and that keeps qualification pipelines active across more than one manufacturing option. Intel said Intel 18A entered production in 2025 and that Intel 18A-P entered risk production in 2026, which signals that another leading-edge path is becoming more credible for future GPU and AI designs.[3]Intel Corporation, “Intel Foundry Details Process Milestones and Future Innovation at VLSI Symposium,” Intel Newsroom, newsroom.intel.com Intel also said 18A-P delivers 9% higher performance at iso-power or 18% lower power at iso-performance than 18A, and that gives customers another benchmark when they evaluate medium-term node migration choices in the GPU foundry market. Even so, the GPU foundry market still rewards suppliers that can pair advanced process technology with proven yield learning, packaging readiness, and customer trust over several product generations.

Chiplet-Based GPU Roadmaps Improving Yield and Product Scaling

Chiplet design is changing the economics of the GPU foundry market because one finished processor can now drive demand across several nodes and multiple manufacturing steps instead of a single monolithic die. That shift improves design flexibility for customers and also raises the value of foundries that can coordinate compute dies, I/O dies, interposers, and advanced packaging in one aligned production plan. The GPU foundry market benefits from this structure because revenue opportunities expand beyond front-end wafer fabrication and move deeper into the packaging and integration stack. Cadence and Samsung Foundry expanded their collaboration in 2026 around second-generation 2 nm and 3D-IC flows, including support for NVLink-C2C and GPU-accelerated design libraries, which shows that packaging-aware design ecosystems are becoming a competitive requirement rather than a side capability. As chiplet adoption rises, the GPU foundry market is likely to favor suppliers that can reduce handoff risk between node selection, design enablement, packaging qualification, and final system delivery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export Controls And Tariff Volatility | -3.0% | Global, with highest impact in China, North America, and East Asia trade corridors | Short term (≤ 2 years) |

| HBM And Advanced Packaging Allocation Bias Toward AI Racks | -2.5% | Global, concentrated in Taiwan and South Korea | Short term (≤ 2 years) |

| Elevated GPU And Memory ASPs Slowing Mainstream Adoption | -1.5% | Global, disproportionately in mid-market enterprise and emerging economies | Medium term (2-4 years) |

| Grid Interconnection Delays for High-Density GPU Campuses | -1.2% | North America and Europe, with early-stage constraints in Asia-Pacific core and spillover to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export Controls and Tariff Volatility

Export controls remain the most disruptive external restraint for the GPU foundry market because they affect end-destination approval, customer mix, and allocation planning at the same time. The US Bureau of Industry and Security changed its policy on certain advanced computing chip exports to China and Macau in January 2026, shifting from a presumption of denial to a case-by-case review for specified products. That policy also requires exporters to certify that global foundry capacity for similar or more advanced chips for US end users will not be diverted, which ties foundry allocation directly to export compliance. The result is that the GPU foundry market faces more documentation, more screening, and less certainty around which advanced products can move through the pipeline without delay. This uncertainty does not stop demand, but it does make customer prioritization, production planning, and revenue timing harder to manage across the GPU foundry market.

HBM and Advanced Packaging Allocation Bias Toward AI Racks

Advanced packaging remains a practical bottleneck for the GPU foundry market because high-end AI systems require logic, memory, interconnect, and assembly capacity to scale together. TSMC said its expanded US plan includes its first US advanced packaging investments, and that confirms packaging is no longer a secondary issue in the growth path of the GPU foundry market. NVIDIA also outlined a domestic manufacturing network that spans semiconductors, boards, systems, and racks, which underlines how many production layers must move in sync before wafer demand turns into deployed AI infrastructure. When packaging access tightens, the GPU foundry market can carry a large order book without converting all of it into recognized revenue on the same schedule. This bottleneck is especially important in the GPU foundry market because customers increasingly need complete system delivery, not only finished wafers, before they can monetize AI capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Node: Sub-5 Nm Nodes Drive Premium Foundry Demand

The 4/5 nm segment held 42.11% of the GPU foundry market share in 2025, and that position reflected the main production generation for current AI accelerators, high-performance inference chips, and custom silicon from large cloud customers. In the GPU foundry market, this node band remains the commercial center because it balances transistor density, yield maturity, and ecosystem readiness better than older nodes and better than very early next-generation ramps. It also sits at the point where flagship AI products can be produced at scale without forcing every customer onto the highest-cost node before packaging, software, and system design are ready. Mature clusters such as 6/7 nm and 8/10/12 nm still matter in the GPU foundry market because gaming products, client graphics, automotive controllers, and industrial inference devices continue to ship on longer refresh cycles.

The 3 nm and below segment is projected to expand at a 26.21% CAGR through 2031, and that makes it the fastest node category as the GPU foundry market moves toward more power-efficient AI compute. NVIDIA and TSMC said the first Blackwell wafer was produced in Phoenix and that TSMC Arizona will produce 2 nm, 3 nm, 4 nm, and A16 technologies, which reinforces the practical link between advanced AI products and a widening sub-5 nm manufacturing footprint. Intel added another signal when it said Intel 18A entered production in 2025 and Intel 18A-P entered risk production in 2026, which shows that future leading-edge competition is becoming more credible even if the current GPU foundry market remains concentrated. In practice, the GPU foundry industry is likely to run with a layered node structure where 4/5 nm remains a large commercial base, 3 nm and below captures the premium AI migration, and mature nodes keep serving cost-sensitive and qualification-heavy products. This means the GPU foundry market is not moving away from older nodes entirely, but it is placing more of its value growth in the advanced-node tier where design complexity and pricing power are strongest.

By Wafer Size: 300 Mm Wafers Anchor the AI Chip Supply Chain

The 300 mm segment commanded 96.33% of GPU foundry market size in 2025, and it also stands as the fastest-growing wafer size segment with a 26.62% CAGR through 2031. That dominance is expected because the GPU foundry market relies on 300 mm economics for large die designs, better output per run, and more efficient use of expensive advanced-node capacity. In the GPU foundry industry, 200 mm production still has a role in specialty controllers, power components, and older graphics-related devices where migration to larger wafers would not improve returns enough to justify the shift. The 150 mm and below tier remains marginal in the GPU foundry market and is mainly tied to supporting substrates or adjacent components rather than mainstream GPU wafer fabrication.

The importance of 300 mm wafers in the GPU foundry market extends beyond front-end logic production and into the broader packaging ecosystem that supports modern AI devices. TSMC said its Arizona expansion includes two advanced packaging facilities, which means the 300 mm footprint is being reinforced across both wafer fabrication and back-end integration. GlobalFoundries also committed funding to packaging innovation and silicon photonics in the US, which shows that domestic semiconductor strategy is being built around broader manufacturing chains and not just standalone fab shells. As a result, the GPU foundry market is likely to remain overwhelmingly tied to 300 mm infrastructure because that is where process maturity, packaging compatibility, and capacity investment are all moving together.

By Foundry Business Model: Pure-Play Foundries Command the Leading Edge

Pure-play foundries held 89.42% of the 2025 GPU foundry market, which shows how strongly customers still prefer suppliers whose business model does not compete with them in end products. In the GPU foundry market, that neutrality matters because customers share sensitive design IP, roadmap timing, yield expectations, and packaging plans that are difficult to separate from commercial trust. The pure-play model also fits the current shape of the GPU foundry market because leading-edge AI programs need large capital spending, long learning cycles, and coordinated packaging support that only a small number of firms can sustain. That is why the segment remains dominant even as alternative merchant options become more visible.

IDM Merchant Foundry Services represented the smaller portion of the GPU foundry market in 2025, but it is projected to grow at a 26.53% CAGR through 2031, which makes it the fastest-moving business model segment. Intel said Intel 18A entered production in 2025 and that Intel 18A-P entered risk production in 2026, and that progress gives external customers a more credible advanced-node alternative than they had in earlier years. Cadence and Samsung Foundry also expanded collaboration around second-generation 2 nm and 3D-IC design flows, which strengthens the merchant foundry value proposition by improving the design enablement stack around Samsung's process roadmap. Even so, customer movement in the GPU foundry market is likely to stay gradual because dual sourcing at the leading edge requires years of qualification, not just a new process announcement. This leaves the GPU foundry market with a clear pattern where pure-play leadership remains intact, but merchant IDMs gain share at the margin as their process roadmaps, packaging links, and design ecosystems become harder to dismiss.

By Application: Data Centers Lead While Automotive Accelerates

Data Center AI and HPC held 63.12% of the 2025 GPU foundry market, and that concentration reflects the central role of large-scale training clusters, inference deployment, and cloud service expansion in current demand. The GPU foundry market is especially tied to this application because no other segment consumes the same mix of advanced nodes, advanced packaging, and high-bandwidth system integration at comparable speed. At the same time, the application mix inside the GPU foundry market is becoming more diverse because training chips, inference processors, and custom cloud silicon do not all use the same die size, power envelope, or node path. Client computing, gaming, professional visualization, and consumer graphics still provide useful utilization support, especially where product cycles remain aligned with mature-node or mid-node production.

Automotive is projected to expand at a 26.32% CAGR through 2031, and that makes it the fastest-growing application segment in the GPU foundry market. This shift is tied to domain controllers, ADAS compute platforms, in-vehicle AI features, and software-defined vehicle architectures that now need more graphics and parallel processing capability than earlier electronic control systems. The automotive path also broadens the GPU foundry market because vehicle programs often combine advanced compute chips with mature-node support components, which spreads demand across more than one manufacturing tier. Qualification cycles remain long in this segment, and that tends to favor suppliers that already have stable process control, durable customer relationships, and repeatable manufacturing documentation. Over time, that should help the GPU foundry market build a second major demand engine beyond data centers, even if automotive volumes scale on a different timetable and under stricter certification requirements.

Geography Analysis

North America held 68.44% of the GPU foundry market share in 2025, and that lead came from the region's concentration of fabless AI chip designers, hyperscalers, and system developers that drive most leading-edge demand. The GPU foundry market in North America is therefore demand-heavy and design-heavy, even though a large share of wafer fabrication has historically remained concentrated in East Asia. TSMC expanded its planned US investment to USD 165 billion in March 2025, and the package covers three new fabs, two advanced packaging facilities, and a major RandD center in Arizona. NVIDIA also said Blackwell wafer production is underway in Phoenix and that it plans to produce up to USD 500 billion of AI infrastructure in the US with partners, which shows that the regional footprint is extending from silicon design into physical manufacturing and system buildout. This makes North America the commercial center of the GPU foundry market even as cross-border manufacturing dependence remains an important strategic risk.

Asia-Pacific is projected to expand at a 26.42% CAGR, making it the fastest-growing contributor to GPU foundry market size through 2031. The GPU foundry market in this region remains anchored by Taiwan's central role in leading-edge fabrication, but it is also being widened by investment paths linked to Japan, South Korea, and India. Cadence and Samsung Foundry deepened their 2 nm and 3D-IC collaboration in 2026, which supports South Korea's effort to stay relevant in next-generation AI design and manufacturing flows. The region's growth profile in the GPU foundry market comes from scale, supply chain depth, and the fact that most practical advanced-node manufacturing capacity is still clustered there.

Europe remains a smaller part of the GPU foundry market, but it is gaining relevance through policy support, trusted manufacturing, and specialty semiconductor capabilities. GlobalFoundries announced a USD 16 billion US investment in 2025 that included packaging and photonics expansion, and that kind of industrial policy response mirrors the broader push for resilient semiconductor capacity across allied regions. South America, the Middle East, and Africa still represent a limited share of the GPU foundry market, although the Middle East is becoming more important as a demand center for sovereign AI infrastructure. The long-term role of these regions in the GPU foundry market is likely to depend more on compute deployment, connectivity upgrades, and trusted sourcing partnerships than on near-term creation of large domestic leading-edge fab capacity.

Competitive Landscape

The GPU foundry market remains structurally concentrated at the advanced-node tier because only a very small number of suppliers can combine process leadership, large capital intensity, and packaging coordination at the scale AI customers require. TSMC sits at the center of the GPU foundry market because its manufacturing roadmap, packaging presence, and customer list place it on the main path for current-generation AI accelerators. That advantage is not only a node issue, since the GPU foundry market also rewards suppliers that can offer advanced packaging, geographic trust, and operational reliability across several product cycles. Intel is emerging as a more visible contender after moving Intel 18A into production in 2025 and Intel 18A-P into risk production in 2026, but the GPU foundry market still requires long customer qualification periods before share shifts meaningfully. Merchant alternatives are becoming more credible, yet the GPU foundry market continues to show a wide gap between having a technical roadmap and having a proven commercial position at scale.

TSMC's decision to lift planned US investment to USD 165 billion is one of the clearest strategic moves in the GPU foundry market because it links domestic fabs, packaging, and RandD in one program. NVIDIA's Blackwell wafer milestone in Phoenix is another important move because it turns US manufacturing from a policy goal into an operating proof point inside the GPU foundry market. Intel's 18A and 18A-P process milestones form a third strategic move because they provide external customers with a more tangible leading-edge alternative than they had in earlier cycles. GlobalFoundries also strengthened its position through a USD 16 billion US investment that extends beyond fabs into advanced packaging, photonics, and power technologies, which broadens the domestic supplier base around the GPU foundry market.

The next phase of competition in the GPU foundry market will likely be shaped by who can align node migration, packaging access, and regional manufacturing resilience with customer deployment schedules. Cadence and Samsung Foundry's expanded 2 nm and 3D-IC collaboration matters here because the GPU foundry market increasingly depends on strong design ecosystems as much as on raw process claims. Export policy will also influence rivalry because capacity allocation and customer prioritization now face a tighter compliance framework for certain advanced products. For that reason, the GPU foundry market should remain concentrated, but it also leaves room for targeted gains by suppliers that can offer trusted geography, consistent yields, and packaging-backed execution in selected customer programs.

GPU Foundry Industry Leaders

Taiwan Semiconductor Manufacturing Company Limited

Samsung Electronics Co., Ltd.

Intel Corporation

GlobalFoundries Inc.

United Microelectronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Intel Foundry disclosed that Intel 18A-P, the first performance enhancement to its 18A node, entered risk production, delivering 9% higher performance or 18% lower power relative to 18A. The VLSI Symposium presentation also detailed long-term research into CFET and subtractive ruthenium interconnects for sub-18A scaling.

- June 2026: GlobalFoundries completed one year of its USD 16 billion US investment plan, the largest single commitment in the company's history, encompassing expansions in New York and Vermont and the establishment of the first US-based silicon photonics packaging center. Collaborating customers include Apple, SpaceX, AMD, Qualcomm, NXP, and GM.

- March 2026: TSMC completed one year of announcement of its intention to expand US investment to USD 165 billion, adding three new fabs, two advanced packaging facilities, and a major R&D center in Arizona, the largest single foreign direct investment in US history at the time of announcement, expected to support 40,000 construction jobs.

- January 2026: The US Bureau of Industry and Security issued a final rule effective January 15, 2026, revising export license review policy for advanced AI chips including the NVIDIA H200 and AMD MI325X, shifting from a presumption of denial to case-by-case review for exports to China and Macau. The rule embeds foundry allocation verification requirements directly into the export compliance process.

Global GPU Foundry Market Report Scope

The Global GPU Foundry Market refers to the industry segment dedicated to the design, manufacturing, and fabrication of Graphics Processing Units (GPUs) through specialized semiconductor foundries that provide advanced production capabilities for high-performance computing and graphics hardware.

The GPU Foundry Market Report is Segmented by Technology Node (3 Nm and Below, 4/5 Nm, 6/7 Nm, 8/10/12 Nm, 14/16 Nm, 20/22/28 Nm, 40/45/55 Nm, and 65 Nm and Above), Wafer Size (300 Mm, 200 Mm, and 150 Mm and Below), Foundry Business Model (Pure-Play Foundry and IDM Merchant Foundry Services), Application (Data Center AI and HPC, Client Computing and Gaming, Professional Visualization and Workstations, Automotive, Industrial, Edge AI, IoT, and Robotics, Consumer Electronics and Mobile Graphics, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are in Value (USD).

| 3 Nm and Below |

| 4/5 Nm |

| 6/7 Nm |

| 8/10/12 Nm |

| 14/16 Nm |

| 20/22/28 Nm |

| 40/45/55 Nm |

| 65 Nm and Above |

| 300 Mm |

| 200 Mm |

| 150 Mm and Below |

| Pure-Play Foundry |

| IDM Merchant Foundry Services |

| Data Center AI and HPC |

| Client Computing and Gaming |

| Professional Visualization and Workstations |

| Automotive |

| Industrial, Edge AI, IoT, and Robotics |

| Consumer Electronics and Mobile Graphics |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Russia | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Technology Node | 3 Nm and Below | |

| 4/5 Nm | ||

| 6/7 Nm | ||

| 8/10/12 Nm | ||

| 14/16 Nm | ||

| 20/22/28 Nm | ||

| 40/45/55 Nm | ||

| 65 Nm and Above | ||

| By Wafer Size | 300 Mm | |

| 200 Mm | ||

| 150 Mm and Below | ||

| By Foundry Business Model | Pure-Play Foundry | |

| IDM Merchant Foundry Services | ||

| By Application | Data Center AI and HPC | |

| Client Computing and Gaming | ||

| Professional Visualization and Workstations | ||

| Automotive | ||

| Industrial, Edge AI, IoT, and Robotics | ||

| Consumer Electronics and Mobile Graphics | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the GPU foundry market?

The GPU foundry market is valued at USD 17.73 billion in 2026 and is forecast to reach USD 54.86 billion by 2031 at a CAGR of 25.35%.

Which technology node leads GPU manufacturing demand today?

The 4/5 nm segment led in 2025 with 42.11% share, reflecting its role in current AI accelerator and high-performance GPU production.

Which application is growing fastest in GPU wafer fabrication?

Automotive is the fastest-growing application, with a projected CAGR of 26.32% through 2031 as domain controllers and ADAS compute demand rises.

Why does North America hold the largest regional position?

North America held 68.44% share in 2025 because the region concentrates leading GPU designers, hyperscalers, and AI infrastructure buyers.

What is driving growth in merchant foundry services?

IDM Merchant Foundry Services is projected to grow at 26.53% CAGR as Intel and Samsung improve their leading-edge process and ecosystem offerings.

What is the main bottleneck facing suppliers in this space?

Export compliance and advanced packaging constraints are the main bottlenecks because they affect capacity allocation, delivery timing, and the conversion of wafer demand into deployed AI systems.

Page last updated on: