North America Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

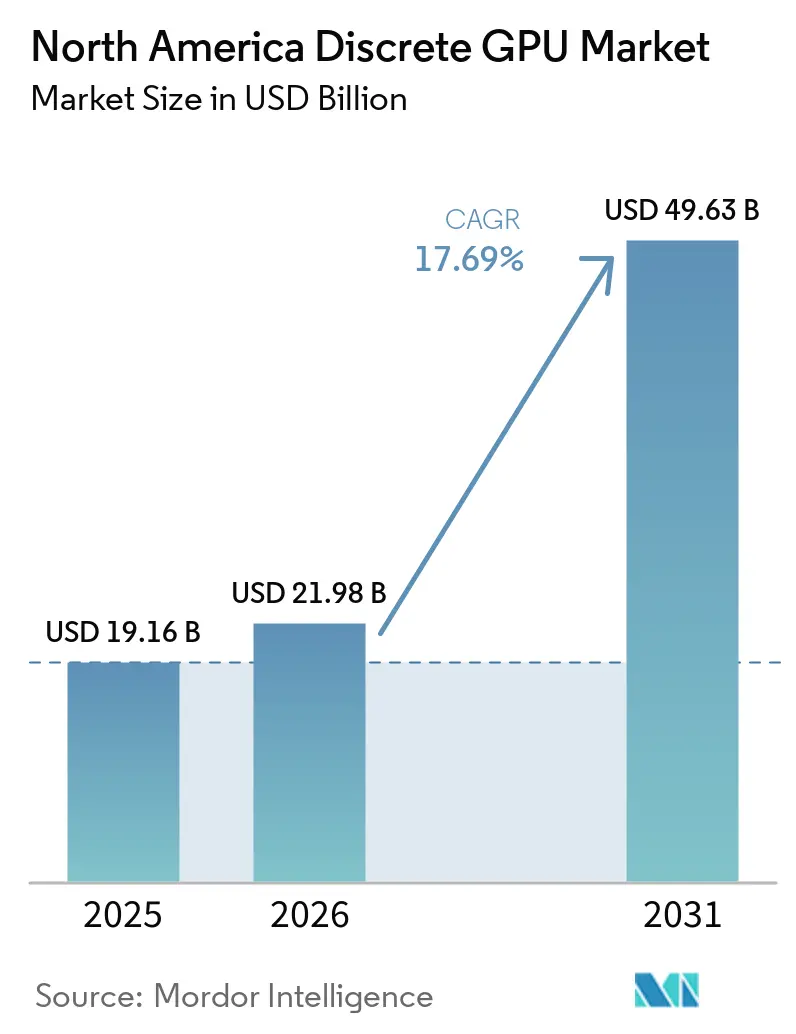

| Base Year Market Size (2025) | USD 19.16 Billion |

| Market Size (2026) | USD 21.98 Billion |

| Market Size (2031) | USD 49.63 Billion |

| Growth Rate (2026 - 2031) | 17.69% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Discrete GPU Market Analysis by Mordor Intelligence

The North America discrete GPU market size is projected to expand from USD 19.16 billion in 2025 and USD 21.98 billion in 2026 to USD 49.63 billion by 2031, registering a 17.69% CAGR between 2026 to 2031. A sharp pivot toward generative-AI workloads in hyperscale data centers, fast-tracking sovereign-AI buildouts in public-sector clouds, and the migration of automotive electronics to centralized zonal architectures together underpin the steep growth curve. Enterprise procurement is now dominated by multi-year take-or-pay contracts that bundle GPUs, software, and advanced packaging services, displacing the short-cycle upgrade culture of the cryptocurrency era. Meanwhile, integrated mobile GPUs from Apple and Qualcomm are shrinking the consumer notebook addressable base, persuading discrete GPU vendors to double down on servers, workstations, and premium desktops. Despite near-term supply bottlenecks in high-bandwidth memory (HBM) packaging, the North America discrete GPU market continues to attract record levels of venture and government capital, ensuring robust innovation pipelines across hardware, firmware, and liquid-cooling ecosystems.

Key Report Takeaways

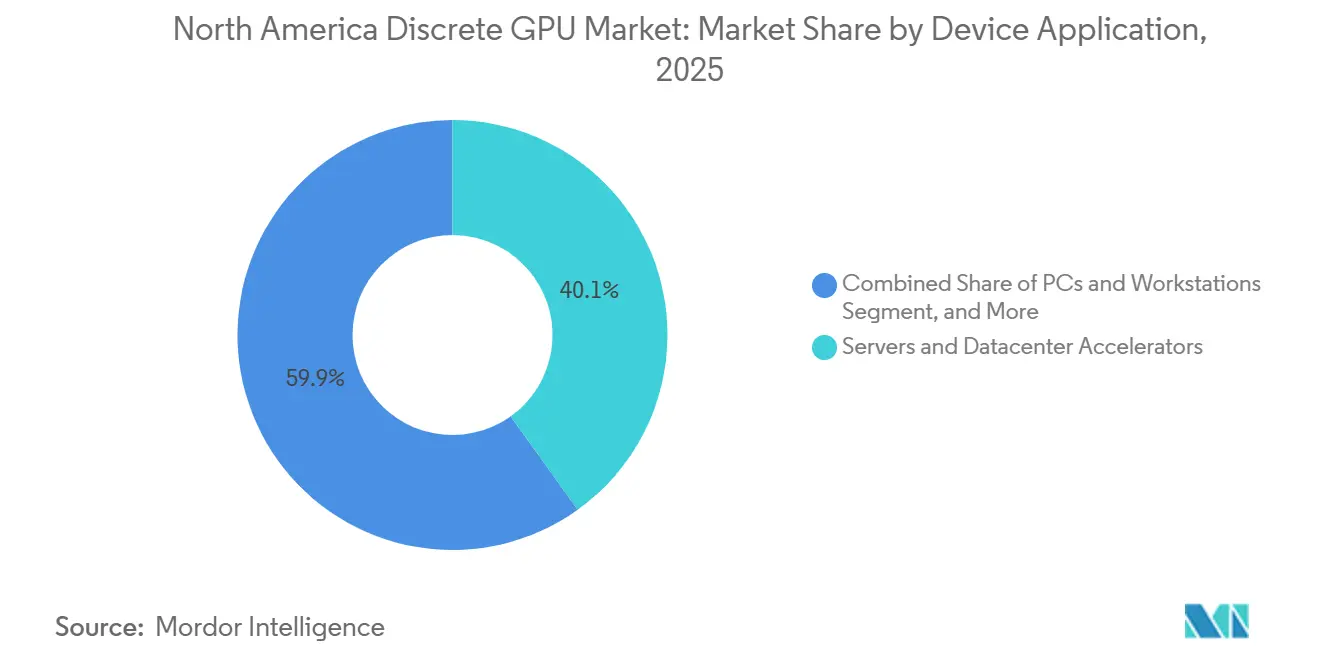

- By device application, servers and datacenter accelerators led the North America discrete GPU market with 40.11% market share in 2025 and are advancing at a 18.22% CAGR through 2031.

- By memory type, HBM-equipped GPUs held 28.71% of the North America discrete GPU market size in 2025 and are growing at an 18.34% CAGR, outpacing GDDR-based cards.

- By performance tier, data-center and AI accelerator GPUs priced above USD 1,200 post the fastest tier growth at 18.03% CAGR through 2031.

- By country, the United States accounted for 87.58% of regional revenue in 2025, while Canada is the fastest riser, with a 18.16% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding AI and ML Workloads in Data Centers | +5.2% | United States and Canada AI clusters | Long term (≥ 4 years) |

| Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles | +3.1% | United States and Canada gaming hubs | Medium term (2-4 years) |

| Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS | +2.8% | United States automotive corridors, Mexico manufacturing clusters | Long term (≥ 4 years) |

| Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers | +2.3% | United States and Canada | Medium term (2-4 years) |

| Government-Funded Semiconductor Initiatives Boosting Domestic GPU Manufacturing | +1.9% | The United States CHIPS Act states that Canada, Quebec | Long term (≥ 4 years) |

| Increasing Penetration of High-Refresh-Rate E-Sports Monitors Raising GPU Upgrade Cycles | +1.4% | United States and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding AI and ML Workloads in Data Centers

North American hyperscalers are executing multi-gigawatt purchase frameworks that front-load deliveries of top-bin GPUs, locking in allocation across several silicon generations. AMD’s 2026-2030 supply agreement with Meta vests equity warrants against shipment milestones, intertwining vendor balance sheets with customer roadmaps. NVIDIA’s integration of Groq’s LP30 into the Vera-Rubin platform splits clusters into high-throughput training GPUs and ultra-low-latency inference arrays, forcing rivals to compete on cost-per-token rather than raw FLOPS. New installations at the U.S. Department of Energy and the National Institute of Standards and Technology ensure a baseline of federally funded demand.[1]United States Department of Energy, “DOE Expands AI Research Clusters,” energy.gov CoreWeave and other independent cloud providers are broadening infrastructure footprints into secondary U.S. metros and Canadian provinces, further localizing GPU capacity.

Surging Demand for Real-Time Ray Tracing in AAA Gaming Titles

The RTX 50 Series enables multi-frame generation, quadrupling ray-traced frame rates, making real-time path tracing the default in big-budget titles. Intel’s Arc Battlemage targets the USD 250-USD 400 band with second-generation ray-tracing cores, positioning the brand as a cost-conscious alternative, though software ecosystem gaps remain.[2]Intel Corporation, “Intel Launches Arc Battlemage GPUs,” intel.com Growth in cloud gaming compounds hardware pull-through as services such as GeForce NOW shift from shared to dedicated virtual GPUs per subscriber. Widespread adoption of 240 Hz and 360 Hz monitors compresses consumer upgrade cycles, anchoring premium desktop spend even as notebook demand migrates to integrated solutions.

Automotive OEM Shift to Centralized Zonal Architectures Demanding Discrete GPU Co-Processors for ADAS

Level 3 autonomy requirements for real-time sensor fusion have pushed carmakers toward discrete GPU co-processors that meet ISO 26262 ASIL-D. NVIDIA’s DRIVE Thor leads current design wins, yet AMD’s Versal automotive SoCs are entering evaluation at Tier-1 suppliers seeking a dual-sourcing buffer. Foxconn’s Guadalajara complex, originally aimed at AI servers, is being tooled to handle automotive GPU assembly once tariff structures stabilize. Pending revisions to U.S. Federal Motor Vehicle Safety Standards are expected to codify higher redundancy thresholds, which would elevate per-vehicle GPU content and lock in long-dated revenue streams.

Rapid Growth of Cloud Gaming Platforms Requiring GPU Servers

Cloud gaming economics favor amortizing discrete GPU capital across thousands of subscriber hours. GeForce NOW racks employ RTX 50 GPUs, while Xbox Cloud Gaming deploys AMD RDNA 4 accelerators to stream 4K120 HDR, a profile that integrated graphics cannot sustain at scale. Qualcomm’s Dragonwing QCS8550 handles low-complexity scenes at the network edge, offloading ray-traced frames to central GPU farms and reducing backhaul strain.[3]Qualcomm Technologies, “Qualcomm Introduces Dragonwing QCS8550,” qualcomm.com Wi-Fi 7 and 5G mmWave blanket coverage across North America lowers the latency ceiling, accelerating discrete GPU server rollouts in suburban and rural exchanges.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Volatility of Advanced Nodes Capacity Constraints | -2.7% | The United States, Canada, and Mexico are dependent on overseas packaging | Medium term (2-4 years) |

| Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers | -1.8% | United States and Canada | Short term (≤ 2 years) |

| Escalating Data Center Energy Regulations Limiting GPU Rack Density | -1.2% | United States high-population states | Medium term (2-4 years) |

| Antitrust Scrutiny on GPU Vendor Bundling Practices | -0.9% | United States Department of Justice | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility of Advanced Nodes Capacity Constraints

TSMC’s CoWoS packaging is the principal bottleneck, with HBM3 GPU lead times exceeding 6 months. Although pilot wafer output in Arizona has started, the lack of on-shore packaging still forces costly trans-Pacific loops. The U.S. International Technology Security and Innovation Fund is subsidizing new lines in Canada and Mexico, yet geopolitical and yield uncertainties persist.[4]Innovation, Science and Economic Development Canada, “Government of Canada Invests in IBM Bromont,” ised-isde.canada.ca Samsung’s delayed 3 nm ramp narrows alternative sourcing, further concentrating risk.

Rising ASPs Making High-End GPUs Unaffordable for Mainstream Consumers

NVIDIA’s RTX 5090 debut at USD 1,999 widens the affordability gap, channeling many gamers toward Apple’s M5 Max notebooks that bundle 40-core GPUs and 614 GB/s unified memory at a lower system cost. Integrated Adreno GPUs inside Qualcomm Snapdragon X Elite laptops deliver 4.6 teraflops, cannibalizing discrete boards below USD 300. As household budgets tighten, cloud gaming subscriptions are absorbing price-sensitive segments, tempering retail demand for entry-level discrete cards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Anchor Growth

The servers and accelerators segment accounted for 40.11% of the North America discrete GPU market share in 2025, a position it is expected to reinforce with an 18.22% CAGR. This sub-sector remains the preferred deployment target for trillion-parameter model training and real-time inference clusters. The resulting procurement scale is attracting value-chain partners in optics, liquid cooling, and advanced packaging, deepening entry barriers. Consumer PCs and workstations, while still sizeable, face a substitution effect from Apple’s integrated GPUs and Qualcomm-powered thin-and-light designs that meet most professional creation workloads without discrete cards.

Automotive ADAS nodes, though starting from a smaller base, exhibit the sharpest slope within the North America discrete GPU market, helped by zonal architectures that require safety-certified co-processors. Gaming consoles and handhelds adopt hybrid strategies, such as AMD Ryzen Z1 APUs paired with external GPU docks, blurring segment lines but keeping discrete revenue modest. Edge devices, industrial drones, and video collaboration appliances increasingly rely on Qualcomm system-on-chips, trimming prospective unit volumes for low-power discrete boards.

By Memory Type: HBM Transition Accelerates

GDDR solutions still account for 71.29% of the North America discrete GPU market as of 2025, driven by cost-sensitive gaming and mainstream workstation demand. Yet HBM-based GPUs are compounding at 18.34% owing to hyperscaler priorities that prioritize bandwidth over capacity. NVIDIA’s Blackwell, AMD’s MI450, and Intel’s next-gen Ponte Vecchio all rely on HBM3 or HBM4 stacks, entrenching the technology in data-center nodes.

GDDR7's introduction in 2026 lifts per-pin speeds to 32 Gbps and may slow HBM's encroachment into enthusiast desktops priced between USD 400 and USD 1,200. However, unit economics still favor HBM for workloads above 1 TB/s. Supply dynamics hinge on CoWoS throughput and TSV yields, variables outside the direct control of GPU vendors yet pivotal for shipment cadence.

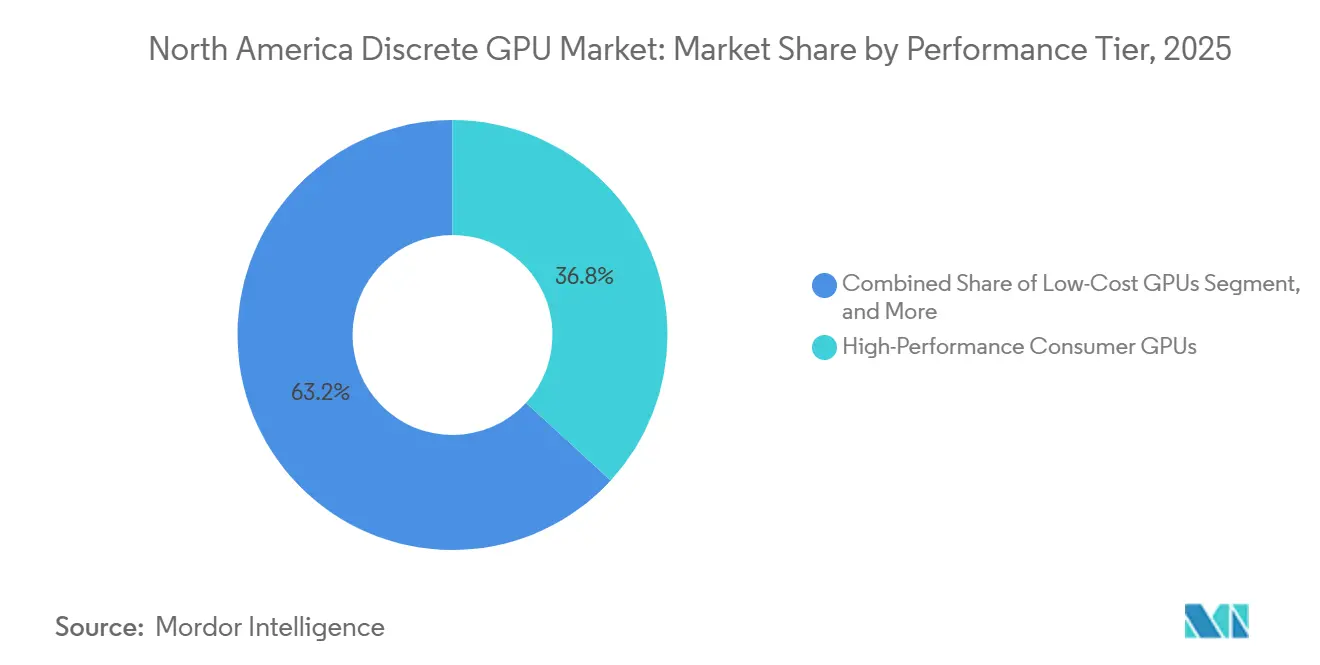

By Performance Tier: AI Accelerators Command Premium Growth

High-performance consumer GPUs at USD 400-USD 1,200 accounted for 36.83% of revenue in 2025. They attract hobbyist gamers and mid-tier creators who demand real-time ray tracing but reject HEDT price tags. Data-center GPUs priced above USD 1,200 are growing fastest at a 18.03% CAGR, driven by contracts for NVIDIA H100 and AMD MI300X accelerators that fetch USD 25,000 to USD 40,000 per unit.

Mainstream cards under USD 400 confront intense competition from integrated solutions with 4-6 teraflops throughput. Low-cost discrete units below USD 100 continue to shrink because modern integrated graphics can now deliver stable 1080p performance. NVIDIA’s Groq-derived LP30 architecture is carving out a separate inference-optimized tier that prioritizes deterministic latency over headline FLOPS, setting the stage for a bifurcated pricing map within the data-center cohort.

Geography Analysis

The United States accounted for 87.58% of North America's discrete GPU market revenue in 2025. Data-center buildouts in Virginia, Oregon, and Texas account for most capacity additions, while federal CHIPS Act incentives finance fabs in Arizona, Ohio, and New Mexico. Regulatory headwinds include Department of Justice antitrust probes into bundling practices and tightening rack-density rules in California and New York, which are pushing hyperscalers toward liquid cooling and, in some cases, small modular nuclear reactors for on-site power.

Canada, though smaller in base, leads growth at an 18.16% CAGR to 2031. A CAD 210 million (USD 155 million) federal grant to IBM’s Bromont site and the MiQro Innovation Collaborative Center is establishing a domestic advanced-packaging beachhead.[5]Innovation, Science and Economic Development Canada, “Canadian Semiconductor Strategy,” ised-isde.canada.ca The Toronto and Montreal clusters host AI researchers and startups that consume substantial inference cycles, encouraging local colocation centers to stockpile discrete GPUs.

Mexico is emerging as an assembly-and-test hub as Foxconn pours USD 900 million into a Guadalajara campus geared for NVIDIA GB200 servers. NVIDIA is also investing USD 1 billion in a green AI data center in Nuevo León, reinforcing the cross-border GPU supply web. The Trump-era 25% tariffs on advanced computing chips risk altering landed costs, yet regional value-add may secure exemptions under USMCA once negotiations mature.

Competitive Landscape

NVIDIA, AMD, and Intel dominate the North America discrete GPU market, but rivalry is intensifying as hyperscalers demand open interconnects and semi-custom silicon. NVIDIA’s USD 20 billion Groq buyout and USD 2 billion stakes in Coherent and Marvell expand control over inference silicon, optical links, and NVLink Fusion fabrics. AMD counterbalances with Meta-linked equity warrants that guarantee foundry allocation for future Instinct generations, weaving customer commitments into capital markets.

Intel’s Arc Battlemage relaunch underscores a strategic pivot: address mainstream gamers through aggressive pricing while investing in oneAPI to bridge driver perception gaps. Meanwhile, Qualcomm’s integrated Adreno GPUs threaten the sub-USD 300 discrete tier by packing respectable 4K performance into energy-efficient SoCs.

Open standards such as UALink, fronted by Broadcom and Intel, challenge NVIDIA’s proprietary NVLink, giving hyperscalers leverage in volume negotiations. The market’s consolidation at the top contrasts with a vibrant tail of accelerator start-ups, Cerebras, Graphcore, Tenstorrent, whose wafer-scale and dataflow approaches court specialized niches but struggle against the gravity of the CUDA ecosystem.

North America Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Qualcomm Technologies Inc.

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: NVIDIA announced a USD 2 billion equity placement in Marvell Technology to co-develop NVLink Fusion, linking semi-custom accelerators into the NVLink fabric at up to 1.8 TB/s.

- March 2026: NVIDIA and Coherent entered a multi-year pact, with NVIDIA investing USD 2 billion to expand U.S. photonics manufacturing for AI interconnects.

- March 2026: Apple released the M5 Pro and M5 Max SoCs, featuring 40-core integrated GPUs and 614 GB/s of unified memory bandwidth.

- February 2026: AMD and Meta agreed on a 6-gigawatt GPU deployment roadmap, with Meta receiving performance-based warrants of up to 160 million AMD shares.

North America Discrete GPU Market Report Scope

The North America Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-Based GPUs |

| HBM-Based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| United States |

| Canada |

| Mexico |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-Based GPUs |

| HBM-Based GPUs | |

| By Performance Tier | Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) | |

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) | |

| By Counrty | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America discrete GPU market in 2026?

It stands at USD 21.98 billion and is poised to expand rapidly at a 17.69% CAGR through 2031.

Which application contributes the most revenue today?

Servers and datacenter accelerators account for 40.11% of 2025 revenue and maintain leadership through 2031.

What memory technology is growing the fastest?

GPUs using high-bandwidth memory are compounding at 18.34% as hyperscalers prioritize bandwidth for AI workloads.

Why is Canada the fastest-growing geography?

Federal backing for advanced packaging and a flourishing AI venture scene lift Canada to an 18.16% CAGR over 2026-2031.

Are rising GPU prices limiting consumer demand?

Yes, retail ASPs above USD 1,999 are steering mainstream gamers toward integrated GPUs or cloud gaming subscriptions.

How are automotive trends influencing GPU demand?

Centralized zonal vehicle architectures now require discrete GPU co-processors certified to ISO 26262, fueling a high-growth automotive sub-segment.

Page last updated on: