Europe Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

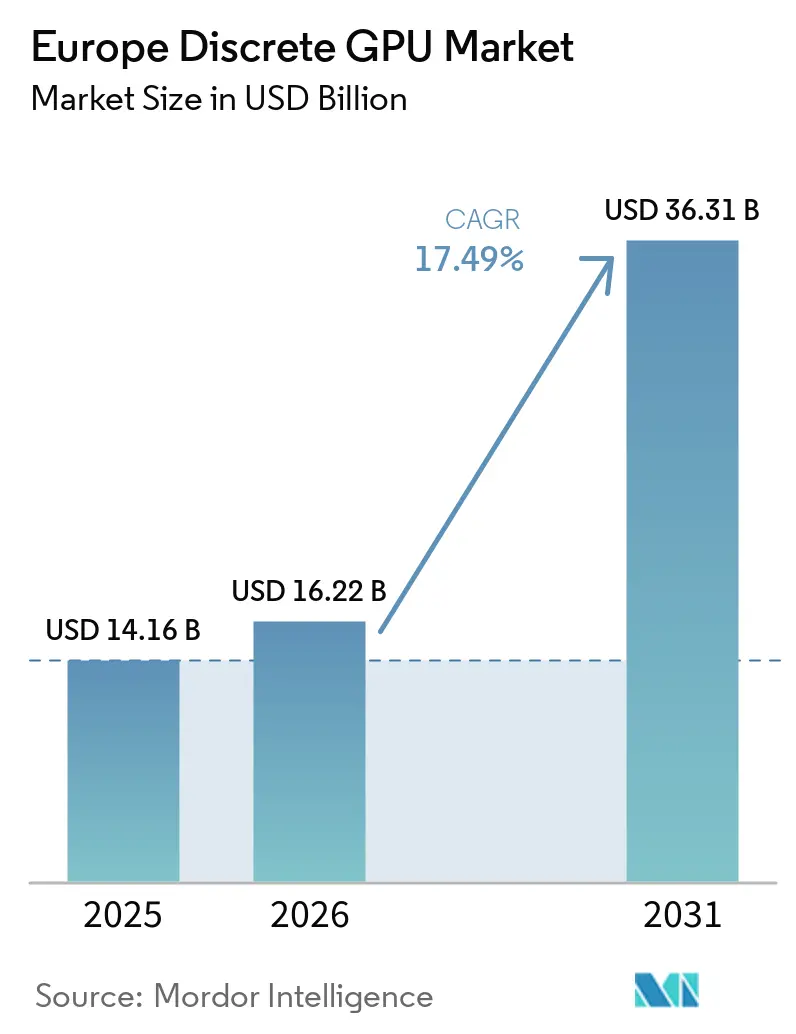

| Base Year Market Size (2025) | USD 14.16 Billion |

| Market Size (2026) | USD 16.22 Billion |

| Market Size (2031) | USD 36.31 Billion |

| Growth Rate (2026 - 2031) | 17.49% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Discrete GPU Market Analysis by Mordor Intelligence

The discrete GPU market size is projected to expand from USD 16.22 billion in 2026 to USD 36.31 billion by 2031, registering a CAGR of 17.49% over 2026-2031. Robust demand stems from European generative-AI buildouts, accelerated electric-vehicle compute requirements, and EUR 43 billion (USD 46.01 billion) in EU Chips Act incentives that are steering local fabrication capacity toward high-margin accelerators. Growth is notably different from prior cryptocurrency-driven peaks because hyperscale operators are constructing multi-gigawatt clusters that prioritize inference throughput rather than gaming frame rates. Servers and datacenter accelerators already command the largest revenue share, while high-bandwidth memory (HBM) adoption is surging as model training workloads expose memory-bandwidth bottlenecks. Meanwhile, competitive dynamics remain oligopolistic at the silicon level, yet European fabless vendors are exploiting open-source driver ecosystems and vertical integration to carve profitable niches.

Key Report Takeaways

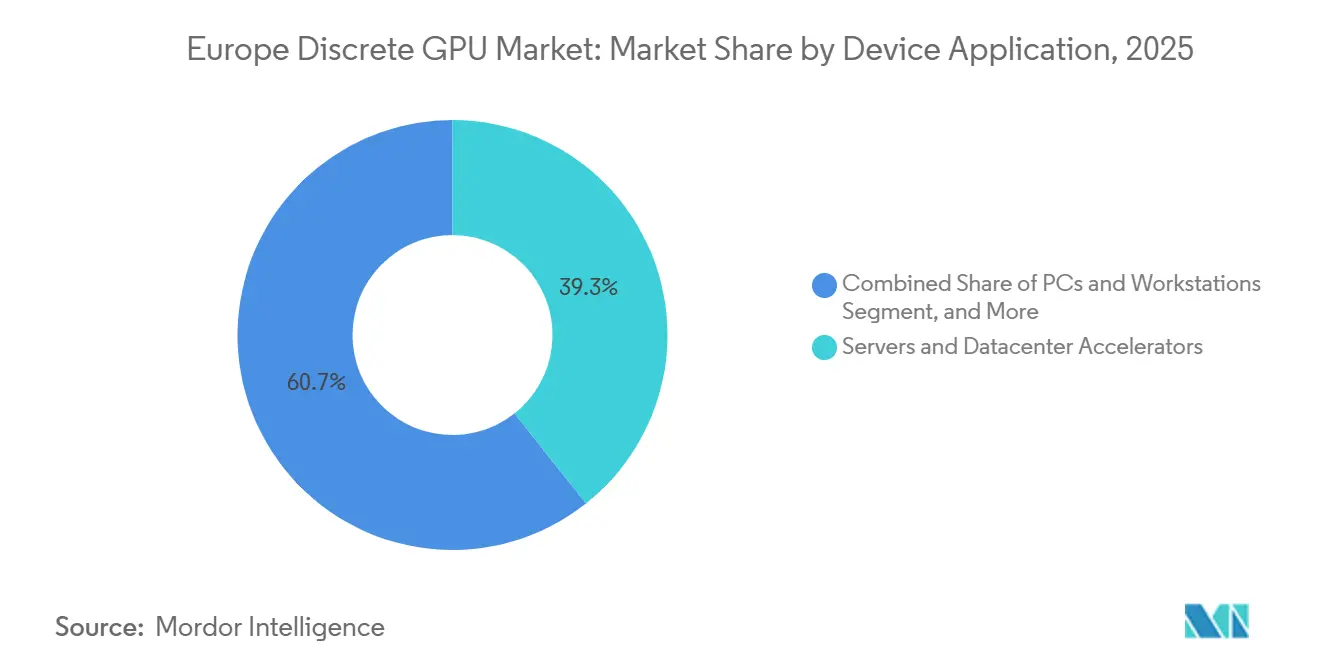

- By device application, servers and datacenter accelerators captured 39.61% of the discrete GPU market share in 2025 and are expanding at an 18.11% CAGR through 2031.

- By memory type, GDDR held 71.25% of the discrete GPU market size in 2025, while HBM is the fastest-growing at a 17.94% CAGR.

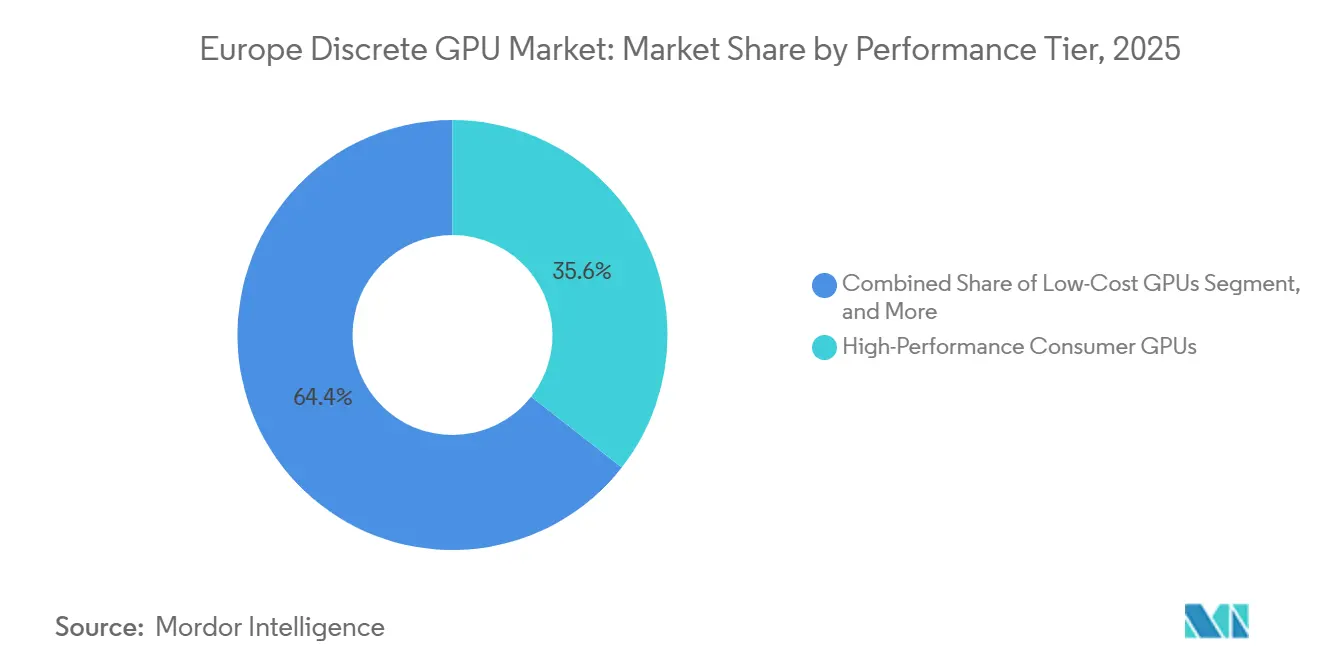

- By performance tier, data-center and AI-accelerator GPUs held a 35.57% share in 2025 and are advancing at a 18.05% CAGR through 2031.

- By country, Germany led the discrete GPU market with 26.83% share in 2025, while France is the fastest-growing at an 18.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Adoption of Generative AI Workloads in European Data Centers | +4.2% | Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| EU Climate Targets Accelerating EV and ADAS Compute Requirements | +3.1% | Germany, France, Italy | Long term (≥ 4 years) |

| Subsidies Under the EU Chips Act for Local GPU Manufacturing | +2.8% | Pan-Europe, especially Germany, France, and Ireland | Long term (≥ 4 years) |

| Proliferation of Real-Time Ray Tracing in AAA Games | +2.3% | United Kingdom, Germany, France | Medium term (2-4 years) |

| CPU-GPU Integration Constraints Add Stand-Alone GPU Demand | +1.9% | Global, early uptake in enterprise workstations | Short term (≤ 2 years) |

| Open-Source GPU Driver Maturity Lowering Total Cost of Ownership | +1.2% | Europe-wide, Linux-dominant enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Generative AI Workloads in European Data Centers

European hyperscalers and sovereign cloud providers are deploying discrete GPUs at unprecedented scale to meet privacy-centric AI inference and training mandates. Deutsche Telekom’s Munich AI Factory came online in early 2026 with 10,000 Blackwell GPUs, demonstrating the need for localized compute sovereignty.[1]Deutsche Telekom, “Munich AI Factory Fact Sheet,” telekom.com Fragmented regulatory regimes prevent cross-border pooling, inflating per-unit GPU requirements and lengthening purchase commitments. Even U.S. platforms such as Meta now provision 6 gigawatts of MI450 capacity in Europe to meet localization rules.[2]AMD, “MI450 Deployment Partnership with Meta,” amd.comA forthcoming AI liability directive will further push enterprises toward on-premises inference stacks, reinforcing multiyear demand visibility.

EU Climate Targets Accelerating EV and ADAS Compute Requirements

Strict net-zero and internal-combustion-phase-out timelines compel automakers to embed discrete GPUs for Level 3-4 autonomy. NVIDIA’s DRIVE Thor system-on-chip samples in 2025, but tier-one suppliers still pair it with discrete Ada-generation GPUs to manage real-time sensor fusion.[3]NVIDIA, “DRIVE Thor Technical Brief,” nvidia.com German plants have already retrofitted their digital twin production lines with Omniverse RTX 6000 Ada boards, while French OEMs continue to rely on GPU-accelerated model retraining for over-the-air updates. Expected Euro 7 particulate rules will push discrete GPUs into mass-market vehicles within two model cycles.

Subsidies Under the EU Chips Act for Local GPU Manufacturing

The EU Chips Act reimburses up to 35% of capital outlays for first-of-a-kind facilities, prioritizing advanced packaging and heterogeneous integration. Kalray leveraged a EUR 14 million (USD 14.98 million) Openchip partnership to localize a RISC-V-based accelerator, illustrating how grants derisk European fabless projects. Ireland’s new assembly-and-test incentives shorten logistics chains otherwise exposed to geopolitical tensions in East Asia. These subsidies directly address CoWoS and HBM bottlenecks, enabling startups to launch domain-specific accelerators that diversify the discrete GPU market.

Proliferation of Real-Time Ray Tracing in AAA Games

European AAA game releases have embraced ray tracing as a standard feature, but frame-rate penalties have hindered its widespread adoption. NVIDIA's DLSS 4 technology can upscale a 1080p input to a native 4K output, but it requires RTX 40-series hardware, sidelining users still reliant on older GTX 16-series cards. By 2025, GPUs in Europe will be equipped for ray tracing, signaling a push toward parity with consoles like the PlayStation 5 and Xbox Series X. To mitigate frame-rate drops, developers are opting for a blend of full-path tracing and hybrid modes, ensuring that enthusiasts continue to upgrade their discrete GPUs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Volatility in Advanced Node Foundries | -2.7% | Global, acute in Europe | Short term (≤ 2 years) |

| Escalating HBM Pricing Pressures on Board OEM Margins | -2.1% | Europe-wide, mid-tier partners | Medium term (2-4 years) |

| Tightened EU Energy-Efficiency Regulations on Data Centers | -1.6% | Germany, the Netherlands, and France | Medium term (2-4 years) |

| Channel Inventory Gluts Post-Crypto Down-Cycles | -1.3% | United Kingdom, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility in Advanced Node Foundries

Europe relies heavily on a single Asian foundry for sub-5-nanometer capacity. TSMC, prioritizing 2-nanometer orders for smartphones and hyperscaler ASICs, risks quarterly cutbacks to discrete GPU allocations. Meanwhile, Samsung's struggles with yields at the 3-nanometer node have dissuaded dual sourcing. Additionally, while advanced CoWoS packaging sees high demand, it is currently oversubscribed. Looking ahead, Intel Foundry Services aims for 18-angstrom production by 2027. However, their lack of expertise in HBM integration poses challenges, restricting immediate supply diversification for GPU vendors in Europe.

Escalating HBM Pricing Pressures on Board OEM Margins

In 2025, prices for HBM3E stacks increased, with a 96 GB stack priced at approximately USD 1,200. SK Hynix and Samsung dominate output, while Micron's late-2025 production ramp accounted for a small share of global demand.[4]SK Hynix, “HBM3E Pricing and Capacity Outlook,” skhynix.com Board partners, bound by take-or-pay GPU contracts, find themselves unable to negotiate memory costs, which in turn squeezes their margins. Looking ahead, the anticipated shift to HBM4 in 2027 promises enhanced bandwidth but comes with a steep cost premium, further challenging profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Datacenter Accelerators Dominate Amid Automotive Gains

Servers and datacenter accelerators captured 39.61% of the discrete GPU market share in 2025 and will rise at an 18.11% CAGR through 2031. This expansion mirrors hyperscaler and sovereign-cloud commitments such as Mistral AI’s EUR 830 million (USD 888.1 million) Paris cluster. Meanwhile, consumer PCs offload routine tasks to integrated graphics, pushing discrete GPUs into specialized content-creation niches. Automotive and ADAS demand, although smaller, records double-digit growth as Mercedes-Benz and BMW embed discrete GPUs for Level-3 autonomy validation.

Gaming consoles remain flat because PlayStation 5 and Xbox Series X hardware cycles run until 2028. Mobile devices rely on integrated GPUs, limiting discrete penetration to niche gaming tablets. Industrial vision and medical-imaging systems contribute steady but modest revenue, slowed by lengthy certification timelines.

By Memory Type: GDDR Dominance Erodes as HBM Gains in AI Workloads

GDDR-based products accounted for 71.25% of the discrete GPU market in 2025, buoyed by GDDR7’s late-2025 debut, which delivered 32 Gbps per pin and improved power efficiency. NVIDIA’s GeForce RTX 5060 packed 16 GB of GDDR7 and offered sub-USD 400 pricing for 4K gaming, maintaining cost-sensitive dominance.

HBM-equipped accelerators grew at a 17.94% CAGR, propelled by memory-bound AI training. AMD’s MI350, sampling with 288 GB of HBM3E, underscores the primacy of bandwidth for large-language-model workloads. However, HBM pricing volatility fosters hybrid architectures pairing HBM-heavy training nodes with GDDR inference accelerators to manage the total cost of ownership.

By Performance Tier: AI Accelerators Outpace Consumer Segments

Data centers and AI accelerators priced above USD 1,200 outpace all other tiers with an 18.05% CAGR, as enterprises internalize AI workloads to comply with European data-residency rules. High-performance consumer GPUs still held 35.57% market share in 2025, yet gamers increasingly defer upgrades until ray-tracing performance swings justify the premium.

Mainstream cards between USD 100-400 confront integrated-graphics encroachment and inventory overhangs from prior generations. Intel’s Arc Pro B70 workstations, launched at USD 949, blur lines between gaming and professional segments, refocusing discrete GPUs on AI inference and visualization. Low-cost sub-USD 100 units linger in legacy desktop refreshes but contribute negligible revenue.

Geography Analysis

Germany retained 26.83% of the discrete GPU market share in 2025, driven by demand from automotive, industrial automation, and financial services. Deutsche Telekom’s Munich AI Factory, operational since early 2026 with 10,000 Blackwell GPUs, positions the country as a GPU-as-a-service hub. Yet stringent 2027 PUE rules accelerate the retirement of older, air-cooled GPU clusters, intensifying capital needs.

France, expanding at an 18.09% CAGR through 2031, benefits from France 2030’s EUR 2.5 billion (USD 2.68 billion) semiconductor allocation and Mistral AI’s sovereign-cloud push. AMD’s ROCm collaboration with Silo AI and the University of Modena further diversifies the compute ecosystem, reducing single-vendor lock-in.

The United Kingdom benefits from CoreWeave’s EUR 1 billion (USD 1.07 billion) GPU-cloud venture, which anchors clusters around NVIDIA H100 and Blackwell. Italy emerges as an automotive-simulation hotspot serving Stellantis and Ferrari, while the Nordics and Benelux prioritize ultra-efficient data centers but struggle with legacy facilities upgrades.[5]CoreWeave, “London Data-Center Expansion Press Release,” coreweave.com Eastern Europe’s growth parallels regional averages yet is capped by slower hyperscale expansions.

Competitive Landscape

Europe’s discrete GPU market remains oligopolistic, with NVIDIA, AMD, and Intel accounting for the majority of silicon design wins. Still, board partners and regional fabless designers exploit vertical integration, open-source drivers, and sovereign-cloud mandates to unlock margin pools. NVIDIA’s Nebius partnership secures capacity by 2030, reducing reliance on North American hyperscalers. AMD’s ROCm 6.0 parity with CUDA catalyzes switch-over momentum, and MI300X deployments in academic clusters signal credible alternatives.

Kalray positioned its MPPA3 data-processing unit for deterministic-latency edge inference. Imagination Technologies scrapped upfront IP fees, luring tier-two automotive suppliers that resist NVIDIA royalties. Graphcore maintains its position in graph neural network workloads, illustrating niche survivability.

Board partners such as ASUS, MSI, and Gigabyte compressed launch cycles, showcasing factory-overclocked RTX 5090 designs in early 2026. However, their dependence on NVIDIA and AMD allocation caps pricing power. Opportunities persist in EU-mandated energy-efficient edge deployments that require sub-250-watt accelerators, a gap incumbents have yet to fully address.

Europe Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Imagination Technologies Ltd.

Graphcore Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA and Amsterdam-based Nebius unveiled a USD 2 billion plan to deploy more than 5 GW of GPU capacity by 2030, creating GDPR-compliant inference alternatives.

- March 2026: Mistral AI raised EUR 830 million (USD 888.1 million) in debt to install 13,800 GB300 GPUs at a 44 MW Paris facility, Europe’s largest sovereign-AI project to date.

- March 2026: Intel launched Arc Pro B70 and B65 workstation GPUs with 32 GB GDDR6 at USD 949, targeting AI inference and visualization workloads.

- March 2026: AMD joined Silo AI and the University of Modena to deploy MI300X GPUs for physical-AI research on ROCm stacks.

Europe Discrete GPU Market Report Scope

The Europe Discrete GPU Market Report is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and Data Center/AI Accelerator GPUs), and Country (Germany, United Kingdom, France, Italy, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Rest of Europe |

| By Device Application | Mobile Devices and Tablets |

| PCs and Workstations | |

| Servers and Datacenter Accelerators | |

| Gaming Consoles and Handhelds | |

| Automotive / ADAS | |

| Other Embedded and Edge Devices | |

| By Memory Type | GDDR-based GPUs |

| HBM-based GPUs | |

| By Performance Tier | Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) | |

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is discrete GPU revenue growing in Europe?

The discrete GPU market is forecast to grow at a 17.49% CAGR from 2026 to 2031, expanding from USD 16.22 billion to USD 36.31 billion.

Which application will contribute the most incremental revenue through 2031?

Servers and datacenter accelerators should generate the most revenue, as they already hold a 39.61% share and are growing at an 18.11% CAGR.

Why are HBM-based GPUs important for European AI clusters?

HBM delivers the bandwidth required for large-language-model training, and HBM-equipped GPUs are expanding at a 17.94% CAGR despite higher memory costs.

Which countries will lead future demand?

Germany remains the largest buyer, while France posts the fastest growth at an 18.09% CAGR, driven by sovereign-AI investments.

What is the main supply-side risk over the next two years?

Volatility at advanced-node foundries and limited CoWoS packaging capacity may extend GPU lead times up to six months.

Page last updated on: