Automotive GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 21.64 Billion |

| Growth Rate (2026 - 2031) | 22.99% CAGR |

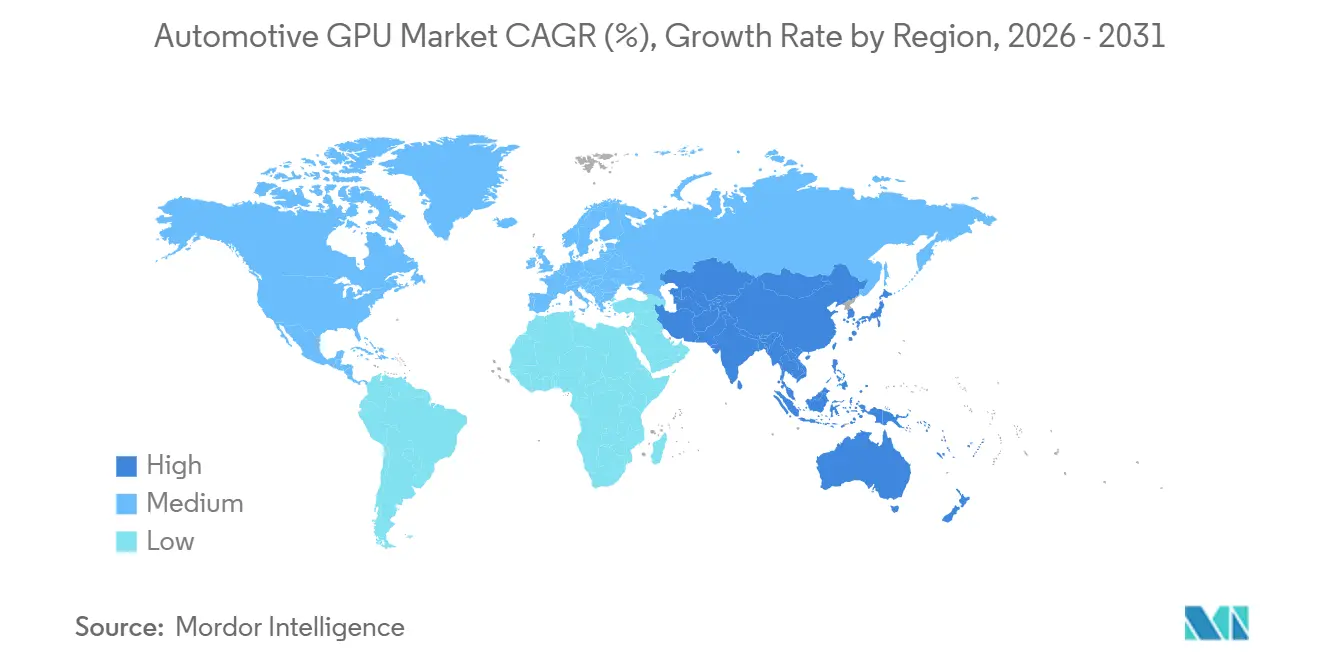

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive GPU Market Analysis by Mordor Intelligence

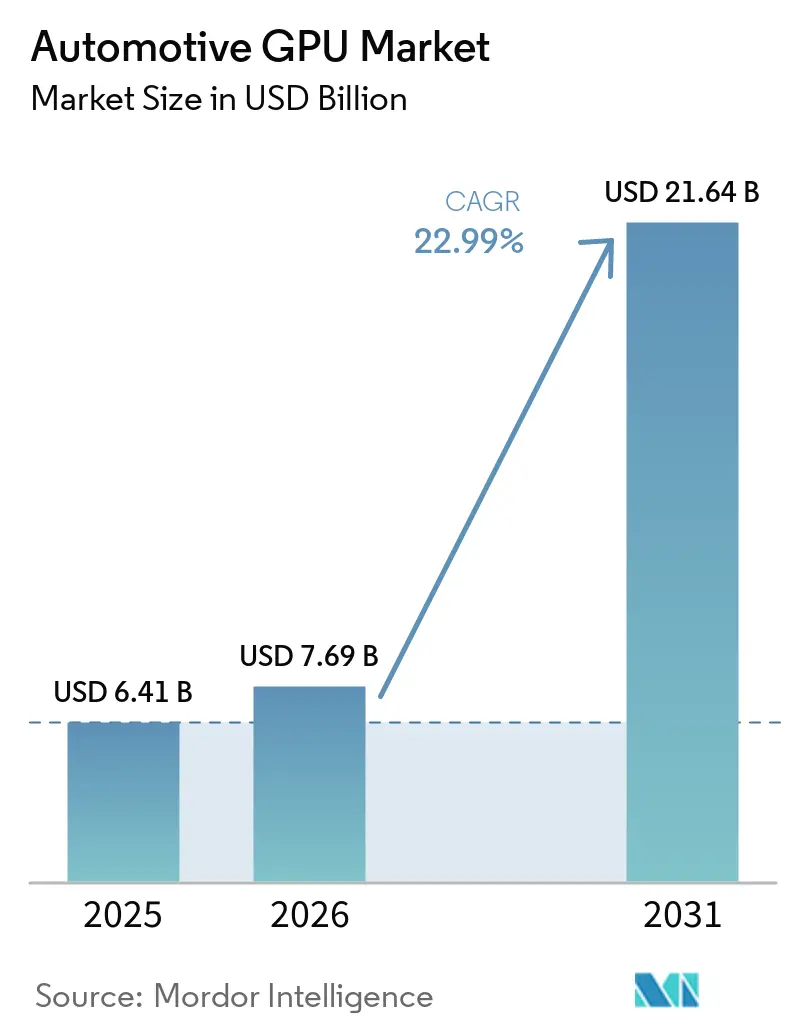

The Automotive GPU market size is expected to grow from USD 6.41 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 21.64 billion by 2031 at a 22.99% CAGR over 2026-2031. Expanding compute needs for camera-based driver assistance, cockpit digitalization, and software-defined vehicle architectures are lifting silicon content per vehicle. Integrated solutions dominate shipments today, yet discrete accelerators are capturing new design wins as original equipment manufacturers (OEMs) provision headroom for Level 3 functions and subscription-based feature unlocks. Centralized compute domains are compressing development cycles, prompting closer collaboration between automakers and GPU vendors, while lingering supply constraints for advanced memories add cost pressure. Asia-Pacific remains the volume anchor due to China’s electric vehicle build-out and regional wafer fabrication programs, but North America and Europe continue to set the pace on regulatory mandates that push real-time perception workloads into lower price bands.

Key Report Takeaways

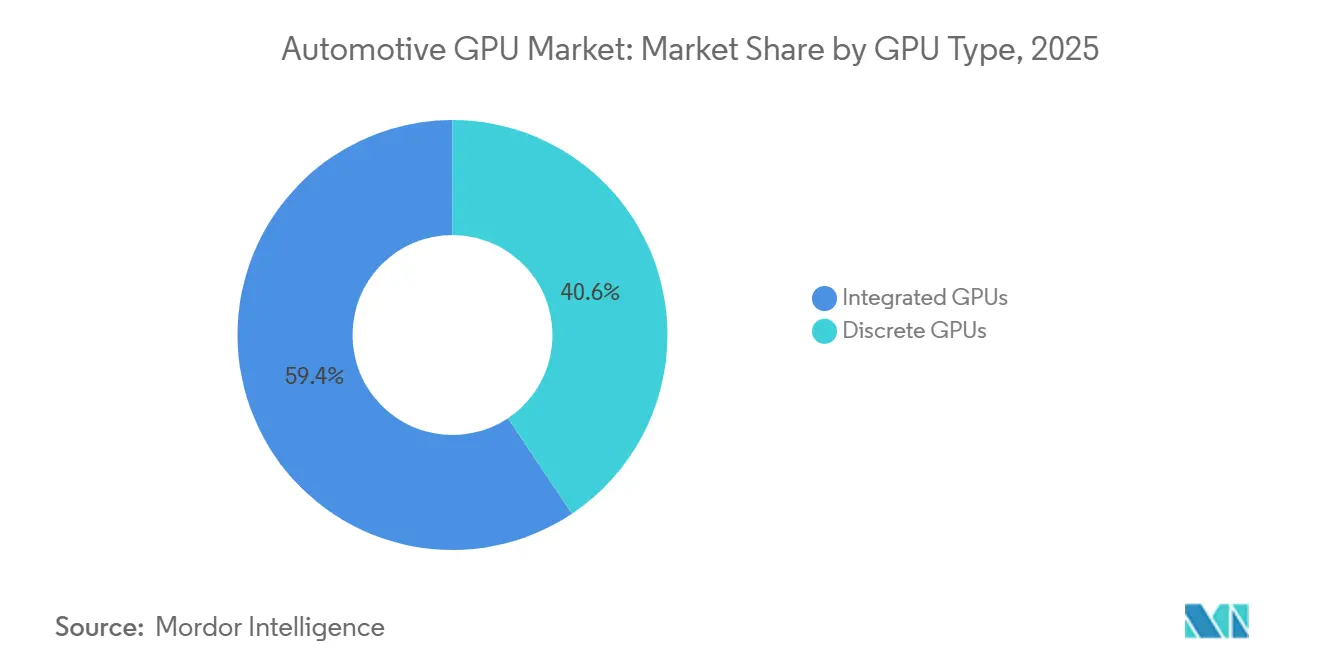

- By GPU type, integrated devices held 59.38% of the Automotive GPU market share in 2025, whereas discrete devices are projected to expand at a 23.68% CAGR through 2031.

- By application, infotainment accounted for a 39.52% share of the Automotive GPU market in 2025, whereas ADAS and autonomous driving are advancing at a 23.55% CAGR through 2031.

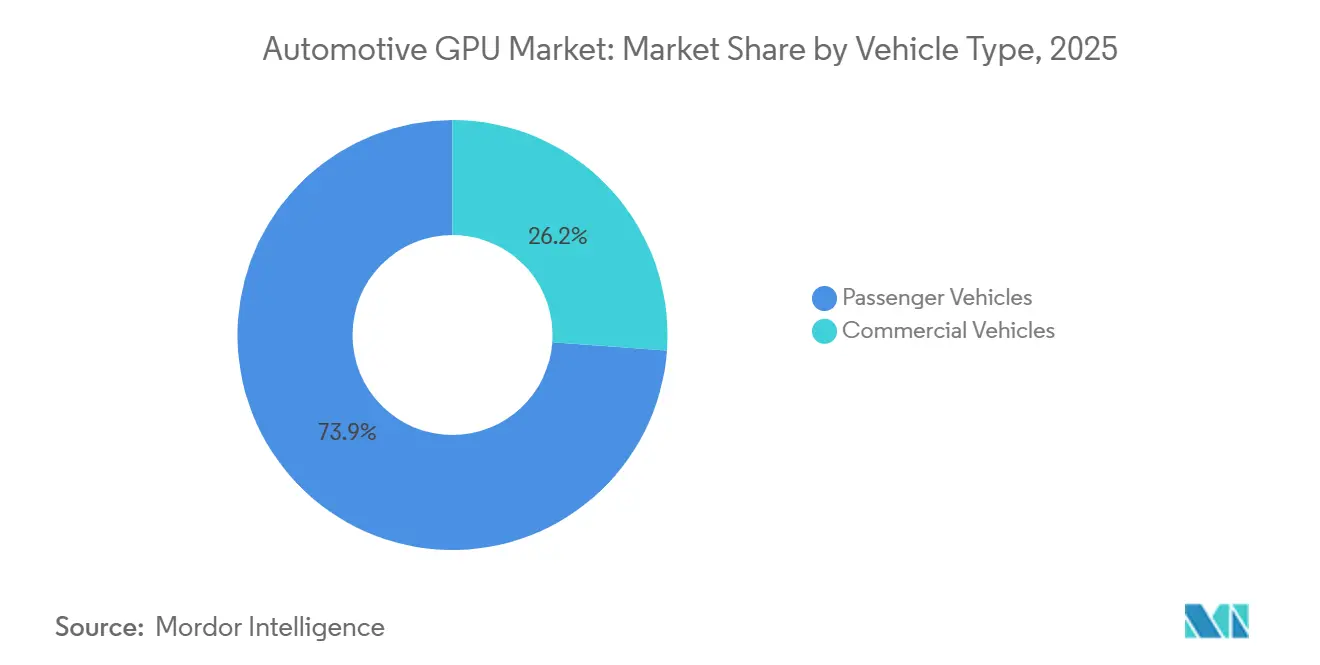

- By vehicle type, passenger cars accounted for 73.85% of revenue in 2025, while commercial vehicles recorded the highest projected CAGR at 23.81% through 2031.

- By region, Asia-Pacific accounted for 67.41% of 2025 revenue and is expected to grow at a 23.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive GPU Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing GPU-Accelerated ADAS Adoption | +5.5% | Global, high intensity in Europe, China, and North America | Medium term (2-4 years) |

| Shift Toward Software-Defined Vehicles | +4.8% | Global, led by North America, Europe, and China | Long term (≥ 4 years) |

| Demand for High-Resolution Digital Cockpits | +3.2% | Asia-Pacific, North America, Europe | Short term (≤ 2 years) |

| Automakers’ Partnerships with Semiconductor Suppliers | +2.5% | Global, strong in North America and Asia-Pacific | Medium term (2-4 years) |

| Rise of Zonal Architectures Enabling Centralized Computing | +2.0% | North America and Europe, and emerging in China | Long term (≥ 4 years) |

| Emergence of Open-Source GPU Compute Frameworks | +1.5% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing GPU-Accelerated ADAS Adoption

Euro NCAP five-star scoring now rewards hands-free braking, driver monitoring, and camera redundancy, creating a pull for programmable graphics cores capable of running vision transformers and sensor fusion. Mobile-first architectures have given way to automotive-grade chips such as NVIDIA DRIVE Hyperion that deliver several hundred teraFLOPS while meeting functional-safety targets.[1]NVIDIA Corporation, “Introducing NVIDIA DRIVE Hyperion,” nvidia.com Chinese urban navigation-on-autopilot programs use similar compute to manage multilane roundabouts, and regional OEMs are designing 2028 models around discrete accelerators so that features can be enabled over the air. The trend is global, yet penetration is fastest where insurance discounts for active safety offset the cost of the hardware. As volume scales, economies of scale reduce unit pricing and further widen the adoption curve.

Shift Toward Software-Defined Vehicles

Consolidating dozens of electronic control units into a central compute stack lowers wiring mass, eases over-the-air update management, and lets OEMs amortize silicon across trim levels. NVIDIA DRIVE Thor integrates CPU, GPU, and accelerated networking on a single die so that cockpit graphics, battery thermal control, and path planning can run concurrently. MediaTek’s 3-nanometer Dimensity Auto Cockpit platform follows a similar blueprint, pairing an NVIDIA Blackwell GPU with a dedicated neural engine for voice and vision applications.[2]MediaTek Incorporated, “Dimensity Auto Cockpit Platforms,” mediatek.com The commercial logic is compelling: software unlocks monetizable options and keeps vehicles current for a decade, protecting residual value. Regulatory frameworks such as ISO 26262 and the newer ISO/SAE 21434 cybersecurity rule set supply the compliance backbone needed for continuous deployment.

Demand for High-Resolution Digital Cockpits

Pillar-to-pillar displays, augmented-reality head-up projections, and rear-seat gaming each raise frame-buffer counts and push GPU utilization. Renesas R-Car Gen5, powered by Imagination’s IMG BXS graphics, allows secure partitioning so that an instrument cluster can share the same core as passenger entertainment without cross-domain faults.[3]Imagination Technologies, “IMG BXS GPU for Automotive,” imaginationtech.com Texas Instruments’ AM62P targets cost-sensitive trims by decoding 4K video inside a 4 W envelope, opening the door for wide adoption in compact vehicles. OEMs see premium display packages as high-margin optional extras, and programmable pipelines enable paid upgrades long after the initial sale. As screen real estate rises, so does the appetite for power-efficient yet performance-dense GPU silicon.

Automakers’ Partnerships with Semiconductor Suppliers

General Motors, Hyundai Motor Group, and others now co-define silicon roadmaps with GPU vendors to lock in capacity and tailor functional-safety features. Hyundai and Kia extended their pact with NVIDIA in March 2026 to roll out Level 4-ready compute across multiple brands.[4]Hyundai Motor Group, “Hyundai and Kia Expand Strategic Partnership with NVIDIA,” hyundaimotorgroup.com In India, Tata Electronics and Qualcomm struck a fabrication and advanced-packaging agreement that localizes module production, lowering logistics cost and lead time. Tier-1 suppliers such as Magna provide validation and launch services around these platforms, compressing vehicle programs by several months. The outcome is a tighter, more resilient supply chain and faster commercialization of new compute architectures.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Supply Chain Volatility for Advanced Node GPUs | -2.8% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Thermal Management Challenges in Automotive Environments | -1.5% | Global, higher in hot-climate markets | Medium term (2-4 years) |

| Cost Sensitivity in Mass-Market Vehicle Segments | -1.2% | Asia-Pacific, South America, and emerging Europe | Short term (≤ 2 years) |

| Certification Lag for Safety-Critical GPU Software | -0.8% | Global, stringent in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for Advanced Node GPUs

Foundries continue to prioritize data-center accelerators over automotive volumes, leaving vehicle programs exposed to longer lead times. High-bandwidth memory remains in tight supply, and spot prices have doubled since early 2025, prompting some OEMs to ship with reduced RAM footprints. Mature-node shortages compound the issue as power-management ICs and sensor interfaces share the same capacity pool. Governments in Japan, India, and the United States are subsidizing new fabrication plants, but build-out timelines mean relief is unlikely before late 2027. Until then, buffer inventories and multi-sourcing remain the main mitigation levers.

Thermal Management Challenges in Automotive Environments

Discrete accelerators exceeding 150 W must fit under dashboards or in trunk enclosures that often see 85 °C ambient peaks. Liquid loops add cost and weight, while passive heat sinks struggle in stop-and-go city traffic. Imagination Technologies introduced distributed safety mechanisms that lessen duplication overhead and cut die size, yet junction temperatures still approach automotive limits in compact cars. Wide-bandgap semiconductors help reduce inverter heat, indirectly freeing cooling budget for compute, but remain expensive for mass deployment. Suppliers are therefore optimizing packaging, die thinning, and dynamic voltage scaling to squeeze more headroom from existing envelopes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Integrated Solutions Dominate, Discrete Gains Traction

Integrated devices accounted for 59.38% of the Automotive GPU market share in 2025, serving infotainment clusters and entry-level ADAS within power envelopes below 15 W. Their single-die construction reduces bill-of-materials costs and simplifies thermal design. NXP’s i.MX 95, which mates an Arm Mali GPU with a small neural engine, exemplifies this balance by meeting ASIL-B targets without a hypervisor. In volume regions such as India and Southeast Asia, these attributes align with price-sensitive segments, ensuring continued dominance through the middle of the decade.

Discrete accelerators, however, are forecast to grow at a 23.68% CAGR as premium OEMs future-proof designs for Level 3 features. NVIDIA DRIVE Thor powers Gatik and Isuzu’s Level 4 trucks, aggregating over 2 petaFLOPS in a centralized node. MediaTek’s cockpit platform embeds an NVIDIA GPU, blurring the line between discrete and integrated GPUs and enabling high-fidelity ray tracing for gaming and visualization. The Automotive GPU market size attributed to discrete boards will thus expand disproportionately in North America, Europe, and China, where autonomy roadmaps are most aggressive.

By Application: ADAS Workloads Overtake Infotainment

Infotainment retained a 39.52% revenue share in 2025, driven by steady demand for streaming media, navigation, and voice assistants. Qualcomm’s Elite Cockpit and similar system-on-chips combine graphics and AI inside a modest thermal envelope, keeping content relevant at lower trim levels. Yet ADAS and autonomous driving units are advancing at a 23.55% CAGR, reallocating GPU cycles toward perception, path planning, and sensor fusion. NVIDIA’s Hyperion platform runs camera, radar, and LiDAR inputs on a unified fabric, supporting continuous learning and fleetwide updates. As regulatory pressure widens, more compute shifts from entertainment to safety-critical tasks, permanently altering workload distribution.

Digital cockpit rendering sits between the two poles. Texas Instruments and Imagination Technologies supply efficient cores that drive triple displays while staying beneath 5 W thermal design power, a sweet spot for compact cars. Over time, cockpit modules are expected to absorb augmented-reality overlays and advanced UI elements, further raising baseline graphics needs even in price-sensitive geographies. Consequently, the Automotive GPU market size for multi-display dashboards is poised for steady expansion, though its growth curve will lag that of safety-driven ADAS demand.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars delivered 73.85% of revenue in 2025, driven by the sheer scale of personal mobility production. Premium marques such as Mercedes-Benz and Tesla equip high-performance GPUs to enable subscription-based upgrades, while value brands prioritize integrated silicon that satisfies mandatory safety rules. The Automotive GPU market share in this segment will narrow modestly as fleet growth outpaces private sales growth.

Commercial vehicles are growing at a 23.81% CAGR, propelled by logistics operators targeting driver-out use cases. Autonomous trucks can double daily utilization, dropping per-mile cost despite higher upfront silicon spend. PlusAI and Aurora have already demonstrated revenue service on fixed corridors, and most new platforms specify redundant GPU nodes for fail-operational safety. Although annual truck volumes are far lower than passenger-car volumes, the bill-of-materials delta means each heavy-duty unit generates two to three times more GPU revenue, lifting the Automotive GPU market size for commercial fleets disproportionately over the forecast horizon.

Geography Analysis

Asia-Pacific captured 67.41% of 2025 revenue and is projected to expand at a 23.88% CAGR. China anchors demand through aggressive electric vehicle penetration and domestic chip incentives; Horizon Robotics leads the front-camera ADAS market while NVIDIA holds a significant share of urban autopilot compute contracts. Japan and South Korea supply memory and power devices, sustaining the regional value chain, whereas India’s semiconductor mission funds fabrication and advanced packaging lines that will come online from 2027 onward.

North America pairs premium vehicle launches with strong Level 2+ uptake. General Motors is committed to NVIDIA compute across upcoming models and relies on synthetic data generated with Omniverse for validation. Regulatory focus on hands-free highway driving stimulates adoption even in mid-tier trims. Canada’s cold-climate testing grounds add credibility to sensor-fusion stacks, indirectly boosting design-win volume for discrete accelerators.

Europe trails Asia-Pacific in volume yet leads in functional-safety rigor. Euro NCAP’s 2025 assessment protocols place automated braking and driver monitoring on par with crashworthiness, accelerating demand for programmable GPUs in compact cars. Germany, France, and the United Kingdom dominate value contribution through software-defined platform investments by Volkswagen Group, Stellantis, BMW, and Mercedes-Benz. Regional carbon-emission targets reinforce electric vehicle sales, further enlarging the addressable GPU pool.

South America, the Middle East, and Africa remain relatively small demand regions. Brazil’s infotainment upgrades and Saudi Arabia’s premium electric imports create pockets of demand, but limited semiconductor infrastructure and lower average selling prices keep penetration modest. Over time, localized assembly of knock-down kits that include integrated GPUs may boost shipments, yet discrete-accelerator uptake will remain niche until total cost declines.

Competitive Landscape

The ecosystem shows moderate concentration, with NVIDIA, Qualcomm, Huawei Technologies Co., Ltd., Intel, and AMD controlling most platform revenue. NVIDIA’s automotive sales climbed 39% year-over-year to USD 2.3 billion in fiscal 2026 on the back of DRIVE Thor design wins and expanding software royalties. Qualcomm and MediaTek compete on cost-efficient integrated silicon that bundles graphics, AI, and connectivity, giving mainstream brands a turnkey path to cockpit digitization. Arm and Imagination license safety-capable GPU IP to second-tier chipmakers, extending choice for OEMs pursuing in-house silicon strategies.

Vertical integration is on the rise. Hyundai Motor Group co-develops inference stacks with NVIDIA, while Tata Motors' subsidiaries draw on Qualcomm technology manufactured at a new domestic facility. DENSO’s licensing deal with Quadric underscores its tier-1 intent to own neural acceleration IP.

Chinese brands, including BYD and Xpeng, are funding proprietary chip projects to mitigate export-control risks. Meanwhile, AUTOSAR Adaptive’s Safe Hardware Abstraction APIs ease migration between vendors, encouraging a multi-sourcing approach that may progressively dilute incumbents’ hold on the Automotive GPU market.

Automotive GPU Industry Leaders

Nvidia Corporation

Qualcomm Technologies, Inc.

Intel Corporation

Advanced Micro Devices, Inc.

Huawei Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hyundai Motor Company and Kia Corporation broadened their collaboration with NVIDIA, confirming the roll-out of NVIDIA DRIVE Hyperion across series-production vehicles from Level 2 to Level 4.

- March 2026: NVIDIA entered a multiyear agreement with Lumentum Holdings and will invest USD 2 billion in advanced laser components and silicon photonics capacity in the United States.

- February 2026: Qualcomm Technologies and Tata Electronics agreed to produce Qualcomm Automotive Modules at Tata’s USD 3 billion outsourced semiconductor assembly and test facility in Jagiroad, Assam.

- January 2026: Magna deepened its relationship with NVIDIA to provide system integration, validation, and launch services for DRIVE Hyperion control units and sensor suites.

Global Automotive GPU Market Report Scope

The Automotive GPU Market Report is Segmented by GPU Type (Integrated GPUs and Discrete GPUs), Application (Infotainment Systems, Digital Cockpit/Instrument Cluster, and ADAS and Autonomous Driving), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Integrated GPUs |

| Discrete GPUs |

| Infotainment Systems |

| Digital Cockpit / Instrument Cluster |

| ADAS and Autonomous Driving |

| Passenger Vehicles |

| Commercial Vehicles |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Type | Integrated GPUs | |

| Discrete GPUs | ||

| By Application | Infotainment Systems | |

| Digital Cockpit / Instrument Cluster | ||

| ADAS and Autonomous Driving | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Automotive GPU market?

It stands at USD 7.69 billion in 2026 and is on track to reach USD 21.64 billion by 2031.

Which segment is expanding the fastest?

Discrete GPUs record the highest CAGR at 23.68% over 2026-2031, driven by Level 3 and Level 4 autonomy needs.

Why is Asia-Pacific so dominant in shipments?

China's electric vehicle boom, domestic chip incentives, and regional manufacturing scale give Asia-Pacific 67.41% of 2025 revenue.

Which companies lead the space?

NVIDIA, Qualcomm, MediaTek, Intel, and AMD currently capture most Automotive GPU revenue through platform ecosystems.

What role do software-defined vehicles play?

Centralized compute architectures reduce wiring complexity, enable over the air feature updates, and increase per vehicle GPU demand, strengthening overall market growth.

Page last updated on: