India Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

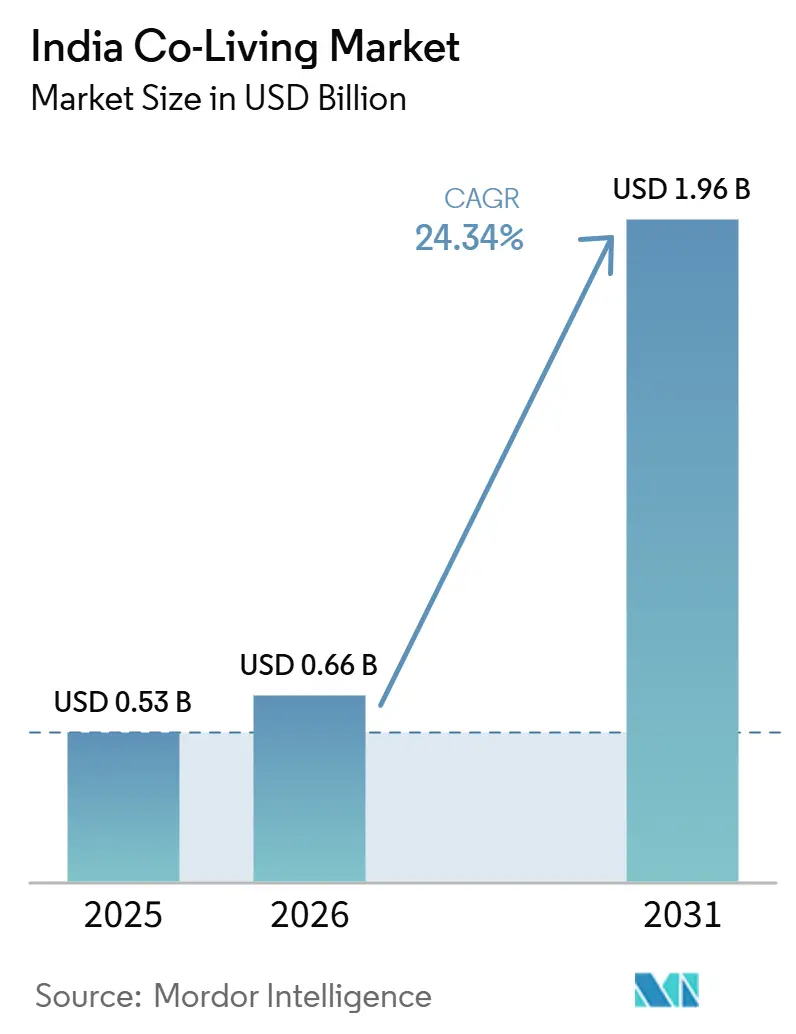

| Base Year Market Size (2025) | USD 0.53 Billion |

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.96 Billion |

| Growth Rate (2026 - 2031) | 24.34% CAGR |

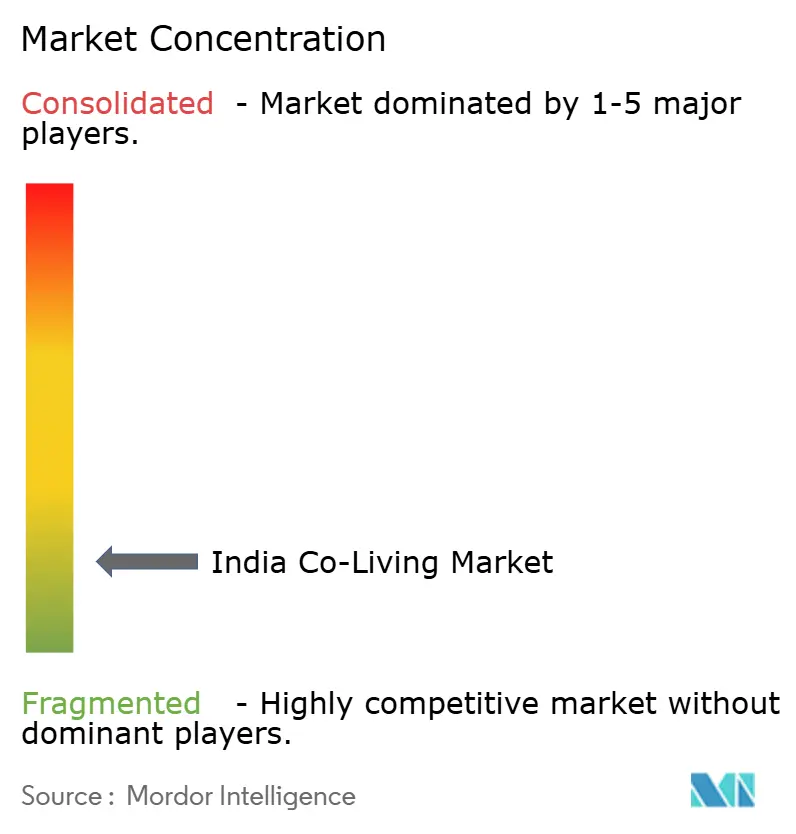

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Co-Living Market Analysis by Mordor Intelligence

The India Co-Living Market size is expected to increase from USD 0.53 billion in 2025 to USD 0.66 billion in 2026 and reach USD 1.96 billion by 2031, growing at a CAGR of 24.34% over 2026-2031.

The India co-living market is expanding because a large base of students and working professionals continues to move across cities for education and jobs. At the same time, traditional rental housing remains uneven in quality, service, and safety. The India co-living market is also benefiting from the shift toward professionally managed housing, where operators compete on furnishings, service reliability, location access, and flexible lease terms rather than just rent. Demand is expanding beyond the largest metro markets because new education centers, manufacturing corridors, and office hubs are creating similar housing needs in secondary cities, giving the India co-living market a broader growth base over the forecast period. Competitive strategy is moving away from simple bed aggregation toward stronger property management models, targeted city expansion, digital tenant engagement, and premium formats that meet the needs of the Global Capability Center workforce. Policy clarity on residential lease treatment and the arrival of institutional rental housing platforms are improving the long-term operating case for the India co-living market, even as high urban lease costs and uneven state-level rules remain pressure points for smaller operators.

Key Report Takeaways

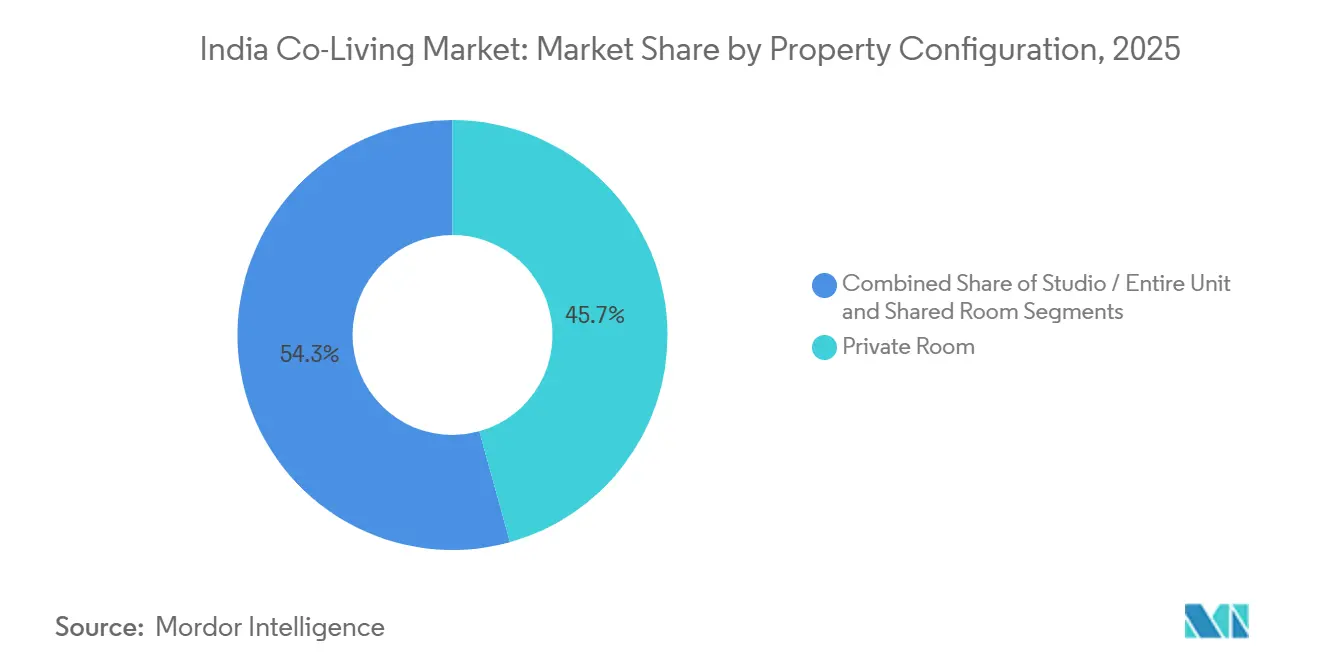

- By property configuration, private rooms held 45.7% share in 2025, while studio and entire unit formats are forecast to expand at 25.11% CAGR through 2031.

- By business model, the asset-light master lease and lease arbitrage segment held 45.5% share in 2025, while management agreements are projected to grow at 26.10% CAGR through 2031.

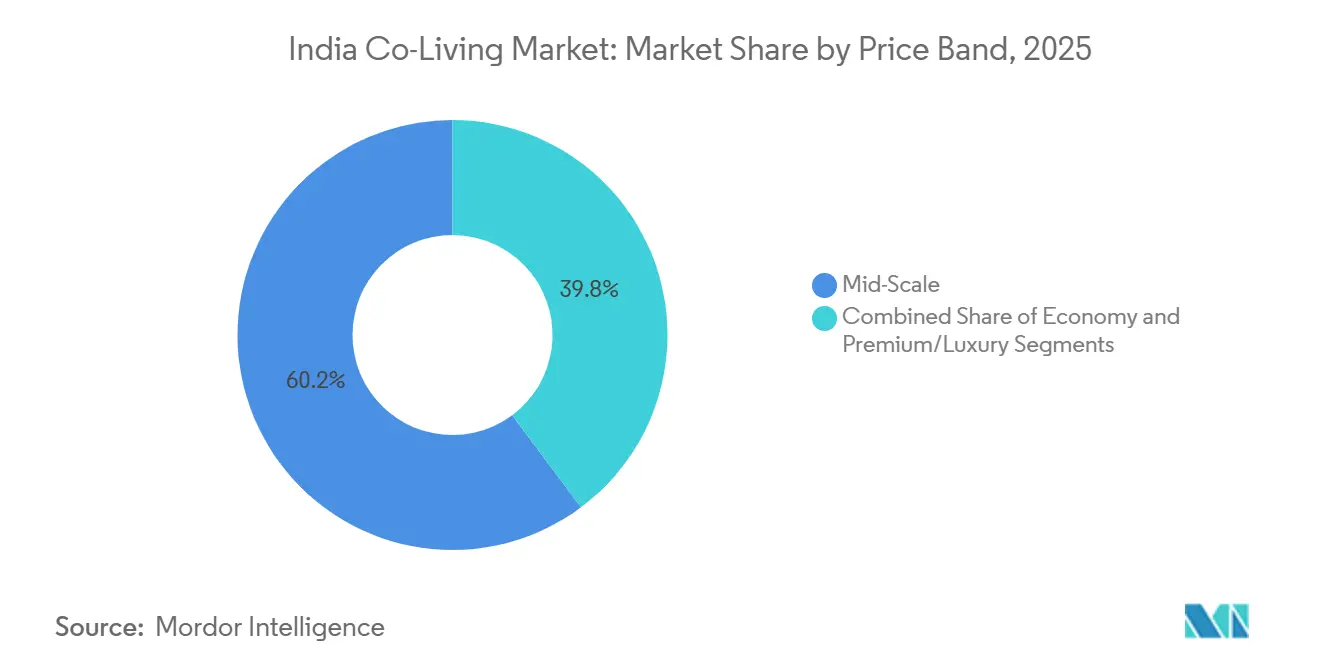

- By price band, mid-scale held 60.2% share in 2025, while premium and luxury are forecast to grow at 26.91% CAGR through 2031.

- By end user, working professionals accounted for 65.7% of demand in 2025, while students are projected to expand at 25.89% CAGR through 2031.

- By city, Bengaluru led with 30.4% share in 2025, while the Rest of India cluster is forecast to grow at 27.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban migration and the young renter movement | +5.8% | Pan-India, with concentration in Bengaluru, Mumbai Metropolitan Region, Delhi National Capital Region, Hyderabad, and Pune | Medium term (2-4 years) |

| Rising housing costs in major metros | +4.5% | Bengaluru, Mumbai Metropolitan Region, Delhi National Capital Region, Hyderabad, and Pune | Short term (≤ 2 years) |

| Global Capability Center and corporate hub expansion | +4.2% | Bengaluru, Hyderabad, Pune, Chennai, Delhi National Capital Region, and Ahmedabad | Medium term (2-4 years) |

| Preference for furnished and community-led living | +3.5% | Pan-India, with concentration in metros and youth-heavy Tier II cities | Medium term (2-4 years) |

| Institutional capital and organized supply expansion | +3.0% | Pan-India, led by Bengaluru, Mumbai Metropolitan Region, Hyderabad, and Pune, then widening to Tier II cities. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Migration Creates Structural Demand That Outpaces Organized Supply

The core support for the India co-living market comes from the steady flow of young people into cities for work and education. Urban migrants aged 20 to 34 were concentrated in major Indian cities in 2025, while national higher education enrollment reached 43.3 million students, indicating a significant out-of-home housing need[1]The Economic Times, “India's Co-Living Sector Poised for Massive Growth, Inventory Set to Triple by 2030,” The Economic Times, economictimes.indiatimes.com. For many renters, a furnished unit with utilities, maintenance, and access to the location solves the upfront costs and setup issues that come with a standard apartment lease. That gap matters because organized supply still covers only a small share of total demand, leaving branded operators room to scale across both work-led and campus-led city clusters. As Tier II cities add new education centers and industrial projects, the India co-living market is likely to see demand grow faster than in earlier metro-led cycles, as operator models and investor interest are already in place.

Rising Housing Costs Widen the Affordability Gap and Support Co-Living Uptake

The India co-living market is also benefiting from the sharp rise in urban rental costs across key micro-markets. Prime city rents rose by as much as 25% in 2025, making shared and private co-living formats more competitive with standard apartment leasing for new migrants and younger office workers. The Bengaluru comparison shows monthly co-living single-occupancy pricing at USD 132 to USD 268, versus USD 175 to USD 412 for a traditional one-bedroom apartment in similar locations. When Wi-Fi, housekeeping, maintenance, and common amenities are bundled into one payment, the value gap becomes easier for renters to see and compare. The January 2026 proposal for a dedicated affordable rental housing fund also suggests that rental stress has become a recognized policy issue, which could help the India co-living market gain broader acceptance in housing policy and urban planning.

Global Capability Center Expansion Concentrates Premium Demand in Key Urban Clusters

The India co-living market is seeing a clear demand lift from the expansion of the Global Capability Center base in major office corridors. India recorded 31.3 million sq ft of Global Capability Center leasing in 2025, and more than 200 new centers entered the country over the prior 2 years, indicating a larger pool of relocating professionals seeking managed housing near work nodes[2]CNBC TV18, “India GCC Leasing Hits Record in 2025, Bengaluru, Hyderabad, Pune Lead Growth,” CNBC TV18, cnbctv18.com. This tenant group usually prefers private rooms, studios, or full units with higher amenity standards, stronger security, and shorter move-in timelines than in a traditional rental. The effect is strongest in Bengaluru, Hyderabad, and Chennai because these cities captured a large share of office demand tied to this segment, which helps explain why they also show deeper organized co-living coverage. Operators that secure properties within a short commute of large office parks can charge better rates and defend occupancy more effectively. That pattern is pushing the India co-living market toward more location-selective growth rather than broad citywide expansion.

Community-Centric Living Helps Branded Platforms Stand Apart from Informal Options

The India co-living market is not competing only on rent, because many tenants now weigh community and daily convenience in the same decision. In 2025, operators with occupancy in the 85% to 90% range linked stronger retention to programming such as fitness sessions, gaming nights, coworking access, and networking events. This matters because informal paying guest housing can often match a low headline price, but it usually does not offer the same service consistency or social environment. Larger operators are also using digital tools for maintenance requests, event bookings, and peer interaction to improve retention. Amenity expectations are moving up in student-led formats, with luxury student residences in Mumbai offering features such as swimming pools, jacuzzis, juice bars, and on-call doctors in 2025. That shift is helping the India co-living market justify premium pricing in select locations where service quality has become part of the product itself.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory ambiguity across states | -0.8% | Pan-India, with state-specific differences in Karnataka, Maharashtra, Tamil Nadu, and Uttar Pradesh | Short term (≤ 2 years) |

| High leasing costs in prime urban markets | -0.6% | Bengaluru, Mumbai Metropolitan Region, and Delhi National Capital Region | Medium term (2-4 years) |

| Tenant turnover and occupancy volatility | -0.5% | Pan-India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation Across States Raises Compliance Friction

The Indian co-living market still lacks a single, uniform operating framework that applies across states and cities. State rent laws continue to differ in how they affect lease structures, property use, and operating obligations, which makes scale execution more complex for multi-city platforms. The Model Tenancy Act 2021 established a more standardized structure for tenancy agreements, but adoption remains uneven across states, limiting the benefits of a central template[3]Mondaq, “Changes Introduced by the Karnataka Rent Amendment Act, 2025,” Mondaq, mondaq.com. Local enforcement can also be disruptive, as seen when the Bruhat Bengaluru Mahanagara Palike took action against more than 100 paying guest properties in Bengaluru in 2024 for safety violations, highlighting the risks associated with fragmented local oversight. The India co-living market will remain more favorable to larger operators until policy consistency improves, because they are better placed to absorb the legal and compliance costs that smaller operators struggle to carry.

Prime Urban Lease Costs Pressure Margin Stability

High lease costs in top urban corridors remain a direct operating restraint for the India co-living market. The dominant master lease model works best when operators can maintain a healthy spread between the rent paid to property owners and the rent charged to residents. Still, that spread tightens quickly when local rents rise sharply. This is especially evident in office-led micro-markets in Bengaluru, where proximity to large employers supports both stronger tenant demand and higher property-owner expectations. Operators can respond through repricing, but that may hurt retention if competing brands absorb part of the increase to protect occupancy. The faster growth expected for management agreements reflects this reality, as that model reduces fixed-lease exposure and provides the India co-living market a cleaner path to scale in expensive neighborhoods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Private Rooms Hold the Base While Studios Move Up

Private rooms held 45.7% of the India co-living market share in 2025, which made them the largest property format in the category. This lead reflects the needs of working professionals who want privacy, predictable monthly costs, and a lower commitment than a full apartment. Private rooms also work well for operators because they balance density and yield without the service gaps often seen in informal shared units. Shared rooms still matter for price-sensitive renters, especially students and early-career tenants, but their appeal weakens as incomes rise and privacy expectations improve.

Studio and entire-unit formats are forecast to grow at a 25.11% CAGR through 2031, making them the fastest-growing configuration in the portfolio mix. The India co-living market is seeing this shift mainly in office-heavy corridors where Global Capability Centre employees, digital nomads, and relocating managers prefer a self-contained layout with managed services. The profile of co-living tenants is widening, with mid-level executives and mobile professionals increasingly represented in branded properties. That trend gives operators a reason to add more studio-led inventory in Bengaluru, Hyderabad, and Pune, where higher daily convenience and shorter commute times can support premium pricing. Over time, the India co-living market is likely to keep private rooms as its volume anchor, while studios and full units are likely to account for a rising share of revenue growth.

By Business Model: Lease-Led Expansion Is Giving Way to Lower-Risk Structures

The asset-light master lease and lease arbitrage segment captured 45.5% of the India co-living market in 2025, which shows how the sector first scaled through rented inventory rather than owned development. Under this model, an operator leases a full property and then rents rooms or units to end users, enabling rapid entry with limited real estate ownership. That approach helped early operators build bed count quickly in major cities where speed mattered more than long-term asset control. It also exposed them to lease inflation, occupancy shifts, and renewal risk, especially in micro-markets where corporate demand pushed rent levels higher.

Management agreements are projected to grow at a 26.10% CAGR through 2031, making them the fastest-growing business model in the India co-living market. This structure allows property owners to retain the asset while bringing in operators to run the building, reducing fixed-cost pressure on the operator and limiting vacancy risk for the owner. The May 2026 launch of a large institutional rental housing platform by HDFC Capital Advisors and Curated Living Solutions shows that this structure is becoming more attractive at scale, with an initial corpus of USD 113 million and a focus on co-living, student housing, and worker accommodation. The own-develop-operate model remains smaller because it needs more capital, but it offers stronger control over product quality and long-term asset value. As institutional capital becomes more active, the India co-living industry is likely to favor management-led, purpose-built structures over simple lease arbitrage.

By Price Band: Mid-Scale Drives Volume While Premium Lifts Value

Mid-scale held a 60.2% share in 2025, making it the largest price band in the India co-living market. This reflects the spending range of entry-level and mid-level professionals, as well as postgraduate students, who want managed housing but remain budget-conscious. The supplied rent data suggests that co-living can offer a clearer value equation than a standard apartment when service bundles are included in the monthly payment. Mid-scale also benefits from broader city coverage, because it can work in both office-led and campus-led micro-markets where demand is diverse and consistent.

Premium and luxury are forecast to grow at a 26.91% CAGR through 2031, making it the fastest-growing price band. The India co-living market for premium and luxury formats is growing as Global Capability Center expansion, returning Indian professionals, and mobile senior employees drive demand for higher-specification properties. Luxury student housing in Mumbai had monthly rents starting at USD 565 per bed and included a much richer amenity set than standard accommodation. That pricing ceiling shows that premium demand is no longer a narrow niche in select micro-markets. The India co-living market is therefore likely to keep mid-scale as its core volume. At the same time, premium tiers generate stronger revenue per bed as tenant incomes and amenity expectations rise.

By End User: Working Professionals Anchor Demand While Students Accelerate Faster

Working professionals accounted for 65.7% of end-user demand in 2025, making them the primary revenue base of the India co-living market. Their priorities align well with the managed housing model because they value commute efficiency, service reliability, security, and flexibility more than long lease tenure. This segment is also becoming more varied, because the tenant mix now includes not only early-career workers but also mid-level professionals and digital nomads in some city markets. As a result, operators are shaping room formats, common areas, and service bundles around work-led lifestyles rather than only around budget housing.

Students are projected to grow at a 25.89% CAGR through 2031, making them the fastest-growing end-user group in the India co-living market. The demand base is supported by rising out-of-station enrollment and the continuing shortage of institutionally managed student accommodation. The India co-living market for student-led formats gains traction when university hostels cannot accommodate new intake, prompting students to shift to organized housing near campus clusters. The student demand cycle is recurring rather than one-time, since each academic year brings a fresh pool of renters into the same locations. Operators that build close to campuses and secure direct university relationships are likely to gain more durable occupancy than those relying only on open-market walk-ins.

Geography Analysis

Bengaluru led with a 30.4% share in 2025, making it the largest geography in the India co-living market. The city has built a strong lead because office demand, especially from Global Capability Centers, has created a steady base of mobile tenants seeking managed housing close to work clusters. Record Global Capability Center leasing in 2025 reinforced Bengaluru’s role as the deepest professional demand pool for this category, and that helps operators maintain stronger occupancy in major corridors. Hyderabad also remains one of the strongest markets because its office districts in Gachibowli and HITEC City continue to attract relocating professionals with similar housing preferences. Chennai is growing on a steadier path, supported by employment in automotive, healthcare, and information technology. At the same time, Pune continues to benefit from its blend of office and student demand, which gives it a better year-round occupancy balance than a purely academic city.

Mumbai Metropolitan Region and Delhi National Capital Region form the next major demand layer in the India co-living market. Mumbai stands out because high housing costs and strong workforce mobility make deposit-light, all-inclusive co-living formats more competitive against standard renting. Delhi National Capital Region has a different profile, with Gurugram and Noida drawing demand from consulting, analytics, technology services, and related office functions. Pune remains important because it combines campus-driven mobility with employment in large information technology parks, broadening the addressable renter base year-round. Kolkata is still at an earlier stage of organized adoption. Still, lower real estate entry costs and student inflows from neighboring states create room for mid-scale platforms to establish a presence before the market becomes crowded.

The Rest of India cluster is forecast to grow at a 27.19% CAGR through 2031, making it the fastest-growing geography in the India co-living market. This group includes education-heavy and industrially active cities where student flows, Production-Linked Incentive investments, and local infrastructure upgrades are improving the case for organized rental housing. HooLiv’s expansion plans after its 2025 fundraise, along with its February 2026 institutional tie-up in Jammu, show that operators are already treating secondary cities as a serious growth corridor rather than a side opportunity. These markets offer lower acquisition and lease costs than the top metros, so operators can often achieve healthier unit economics even when rents are lower in absolute terms. As organized employers and private universities spread further beyond the core metros, the India co-living market is likely to keep widening geographically and become less dependent on a small set of legacy city hubs.

Competitive Landscape

The India co-living market remains moderately fragmented, with a few scaled national brands operating alongside a long list of regional and city-focused players. Stanza Living remains one of the most visible large operators, operating more than 50,000 beds across 450 residences in 15 cities and achieving its first-ever net profitability in the financial year 2025. In November 2025, the company raised USD 32 million in a Series E round led by Accel, which indicates that investors still see expansion potential in scaled brands with improving operating discipline. The same broad pattern appears in the wider India co-living market, where scale alone is no longer enough, and investors are looking more closely at occupancy stability, property-level economics, and the ability to move beyond a basic aggregation model. Technology also matters more now because larger platforms are using tenant apps, service tracking, and community tools to improve retention and reduce friction in daily operations.

Strategic partnerships have become one of the clearest signs of the India co-living market's maturation. In September 2025, Colive announced a strategic partnership with Bain Capital and Sattva Group to build a pan-India co-living real estate platform, with an initial commitment of at least USD 100 million and a USD 20 million Series B funding round. In May 2026, HDFC Capital Advisors and Curated Living Solutions launched an institutional rental housing platform with an initial corpus of USD 113 million, which signals growing comfort with more structured, real estate-led operating models. These moves show that developer and capital-provider partnerships are becoming more central to expansion than stand-alone startup growth. They also support the view that future winners in the India co-living market will likely combine location discipline, operating control, and access to patient capital.

Niche positioning is also shaping competition in the India co-living market. Experion launched VLIV in August 2025 as a women-only co-living offering with 730 twin-sharing beds and a broader development commitment of USD 300 million, demonstrating that differentiated formats can attract serious capital when they solve a clear user need. Smaller brands such as Settl, CoHo, Housr, Union Living, TruLiv, and HooLiv are pursuing a tighter city focus, premium micro-market positioning, student housing links, or safety-led propositions instead of trying to copy the biggest platforms across all segments. The investor mix is also changing, as shown by Nexus Venture Partners’ 2025 exit from its 27% stake in Zolostays after a decade, indicating a shift from early venture ownership toward more mature capital expectations. That shift should favor operators with a defensible city network, a clear segment focus, and stronger evidence that their portfolios can maintain occupancy and pricing amid changing local market conditions.

India Co-Living Industry Leaders

Stanza Living

Zolo

Colive

Housr

Settl.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Colive raised USD 20 million in a Series B funding round led by Bain Capital, while Bain Capital and Sattva Group also formed a USD 100 million joint venture to develop purpose-built co-living projects across Bengaluru, Pune, and Hyderabad.

- April 2026: The Hosteller raised INR 150 crore (approximately USD 16 million) in a Series B funding round to expand its co-living portfolio to 25,000 beds across India and launch a travel and co-living app.

- February 2026: Truliv launched its first co-living property in Bengaluru, marking its entry into the city and supporting its expansion target of 15,000 beds across seven cities by FY2028–29.

India Co-Living Market Report Scope

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light: Master Lease / Lease Arbitrage |

| Asset-Light: Management Agreement |

| Asset-Heavy: Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Ahmedabad |

| Rest of India |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light: Master Lease / Lease Arbitrage |

| Asset-Light: Management Agreement | |

| Asset-Heavy: Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Ahmedabad | |

| Rest of India |

Key Questions Answered in the Report

What is the current size and growth outlook for co-living in India?

The India co-living market was valued at USD 0.53 billion in 2025, USD 0.66 billion in 2026, and is projected to reach USD 1.96 billion by 2031, at a 24.34% CAGR.

Which tenant group drives the most revenue in India co-living?

Working professionals accounted for 65.7% of demand in 2025, making them the main revenue base for operators across major office-led cities.

Which segment is growing fastest in India co-living?

By price band, premium and luxury is the fastest-growing segment, with a 26.91% CAGR through 2031, while the Rest of India city cluster is the fastest-growing geography, with a 27.19% CAGR.

Why are private rooms still the largest format?

Private rooms held 45.7% share in 2025 because they offer a better balance of privacy, affordability, and managed services for the largest renter base, especially working professionals.

Which cities matter most for expansion plans?

Bengaluru remains the largest city with 30.4% share. Still, operators are increasingly targeting Tier II and Tier III education and employment hubs such as Indore, Jaipur, Coimbatore, and Dehradun for faster growth.

What are the main risks for operators in this space?

The main risks are uneven state-level regulation, high lease costs in prime micro-markets, and pressure on margins when operators rely heavily on long-term master leases in fast-rising rental corridors.

Page last updated on: