Germany Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

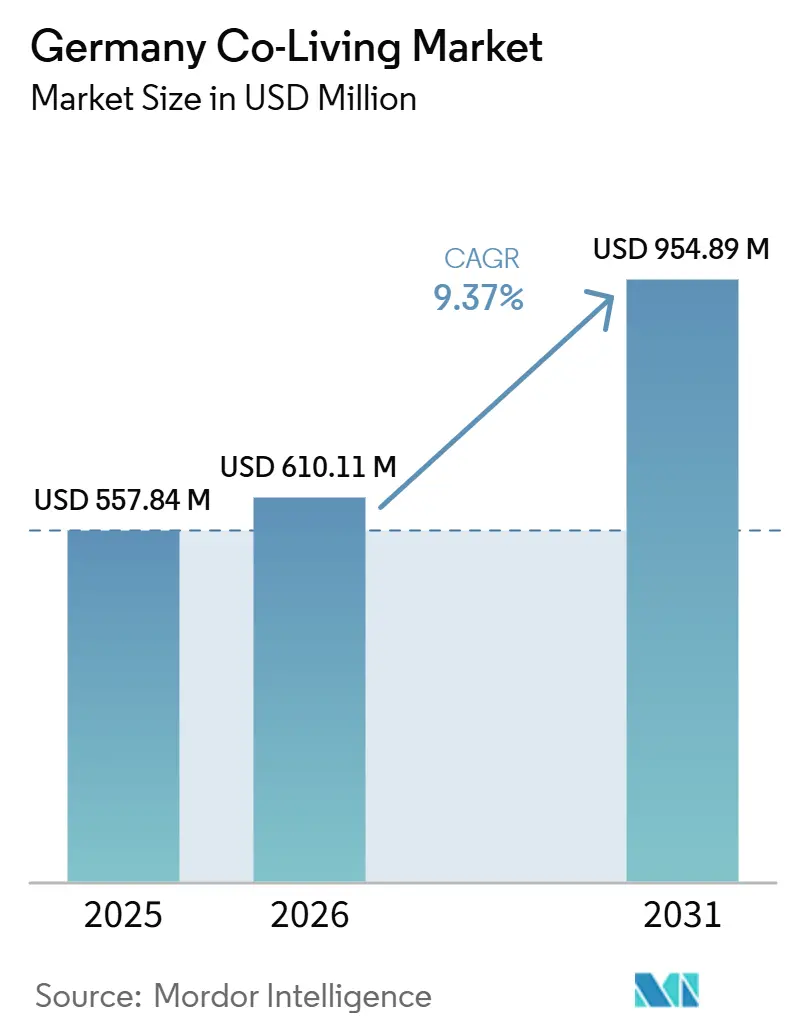

| Base Year Market Size (2025) | USD 557.84 Million |

| Market Size (2026) | USD 610.11 Million |

| Market Size (2031) | USD 954.89 Million |

| Growth Rate (2026 - 2031) | 9.37% CAGR |

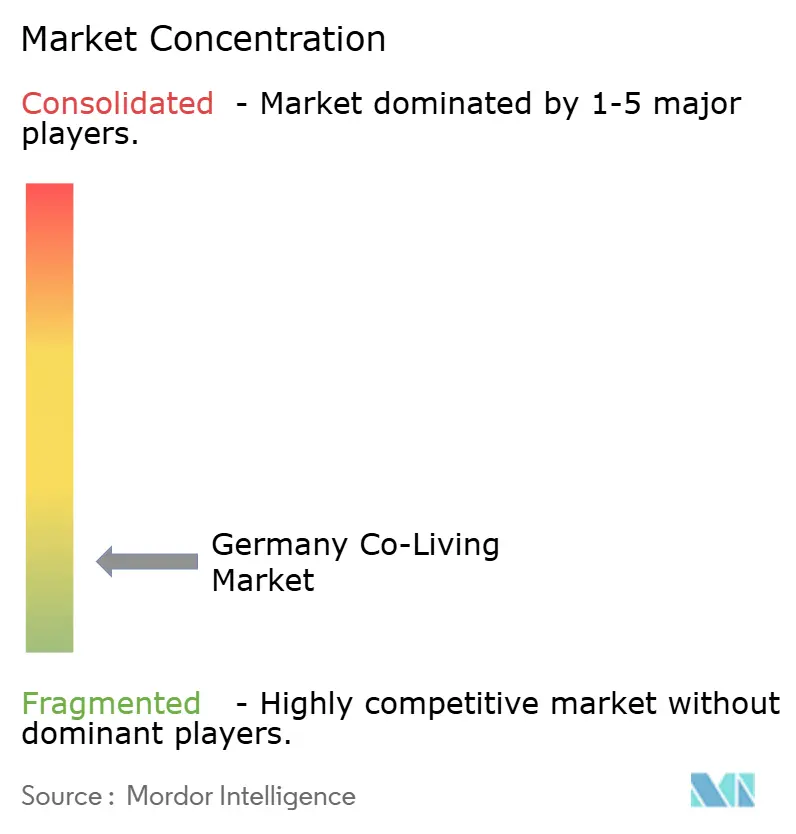

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Co-Living Market Analysis by Mordor Intelligence

The Germany Co-Living Market size is projected to be USD 557.84 million in 2025, USD 610.11 million in 2026, and reach USD 954.89 million by 2031, growing at a CAGR of 9.37% from 2026 to 2031.

The Germany co-living market continues to expand because housing shortages in major cities are keeping pressure on renters who need ready-to-move, managed accommodation. Demand is also widening beyond students, as recent migration and labor mobility changes are driving a broader inflow of mobile workers who need flexible housing as they settle into Germany cities. The Germany co-living market is also benefiting from a clear shift toward furnished and fixed-term rentals, which shows that managed rental formats are becoming more normal across the urban housing system. Competition is becoming sharper as larger operators pursue asset-light expansion, institutional investors back platform growth, and owner-operator partnerships move more supply into branded portfolios. Even so, the Germany co-living market still operates under a tougher revenue setting because the rent brake extension limits pricing freedom in stressed rental areas and keeps operators focused on product mix, furnishings, services, and location quality rather than simple rent increases.

Key Report Takeaways

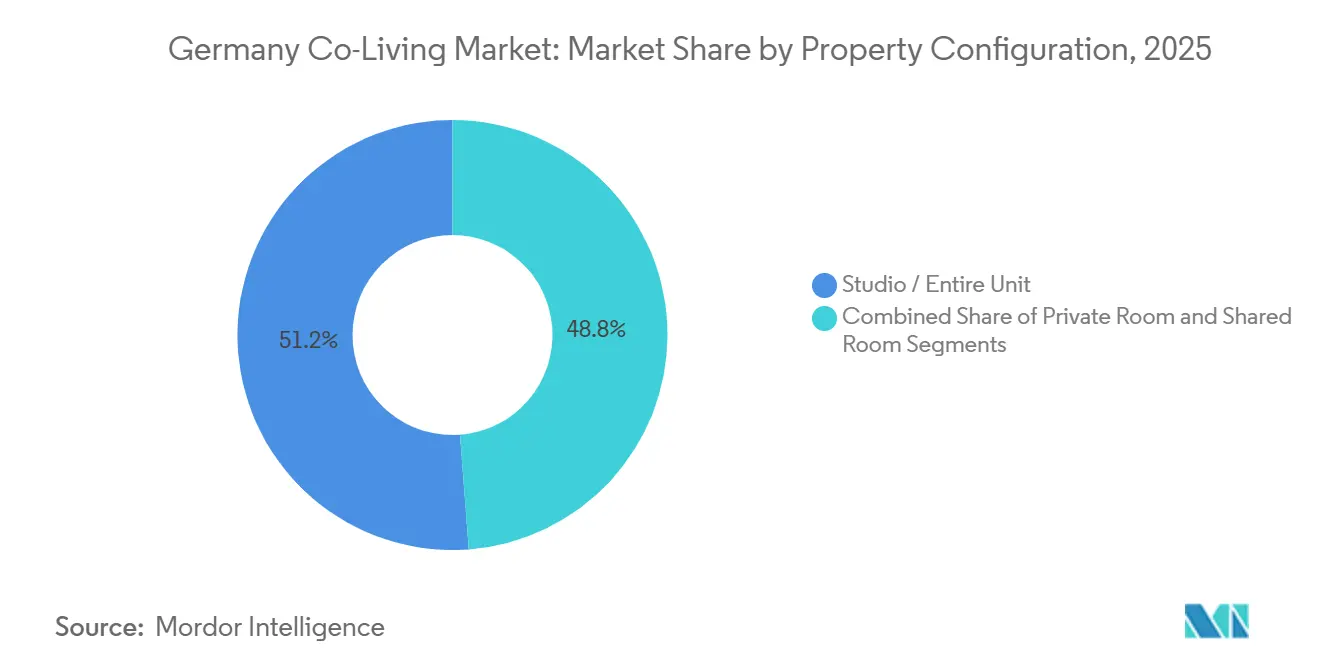

- By property configuration, Studio / Entire Unit led with 51.2% of the Germany co-living market share in 2025, while Shared Room is forecast to expand at 10.44% CAGR through 2031.

- By business model, Master Lease / Lease Arbitrage held 47.6% of the Germany co-living market size in 2025, while Management Agreement is projected to grow at 10.67% CAGR through 2031.

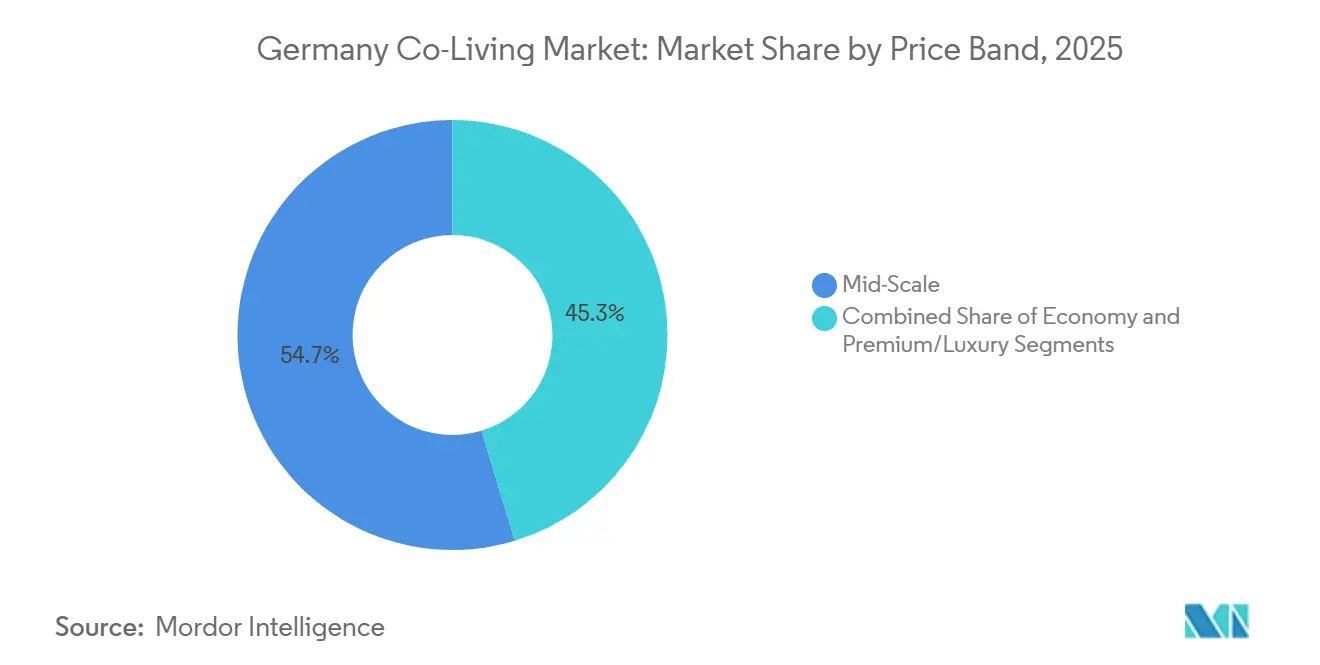

- By price band, Mid-Scale accounted for 54.7% of the Germany co-living market size in 2025, while Premium / Luxury is forecast to advance at 11.12% CAGR through 2031.

- By end user, Working Professionals captured 57.0% share of the Germany co-living market size in 2025 and are projected to grow at 11.34% CAGR through 2031.

- By geography, Berlin represented 30.8% of the Germany co-living market share in 2025 and is set to expand at 11.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe housing shortages in Berlin, Munich, and Hamburg are driving demand for alternative housing formats | +2.8% | National, with the highest demand-supply imbalance in Berlin, Munich, and Hamburg | Short term (≤ 2 years) |

| Growing student, expatriate, and young professional populations are increasing the demand for flexible living arrangements | +2.2% | Berlin, Frankfurt, Hamburg, Munich, university-dense secondary cities | Medium term (2-4 years) |

| Rising rental prices are encouraging the adoption of shared and managed accommodation solutions | +1.9% | National, with the sharpest pressure in major urban centers | Short term (≤ 2 years) |

| Increasing investment from real estate funds and operators in purpose-built co-living assets | +1.5% | Berlin, Munich, Hamburg, Frankfurt, selective secondary city expansion | Medium term (2-4 years) |

| Growing preference for furnished, all-inclusive housing options among mobile urban residents | +1.1% | National, strongest across major urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Deficits In Berlin, Munich, And Hamburg Create Persistent Co-Living Demand

The Germany co-living market is gaining steady support, as housing shortages in leading cities have become persistent rather than temporary. Residential construction in strong economic regions continues to lag demand because building activity is too weak, land is scarce, and regulation remains heavy[1]Sachverständigenrat Wirtschaft, “Chapter 4, Housing in Germany, Address Shortages and Facilitate Access,” Annual Report 2024/25, sachverstaendigenrat-wirtschaft.de. This matters for co-living because renters who arrive in these cities cannot wait for the conventional market to loosen, so they often choose furnished and managed units that are ready immediately. Rental market speed remained very high in 2025, with listings moving quickly and leaving less time for new arrivals to secure standard leases through traditional channels. As a result, co-living is becoming less of a niche lifestyle product and more of a practical housing answer for renters who need speed, access, and lower setup friction.

Growing Student, Expatriate, And Young Professional Populations Sustain Flexible Living Demand

The Germany co-living market is also being lifted by a broader renter base that now includes students, expatriates, and working professionals who need mobility and shorter commitment periods. Recent migration and labor policy changes are expected to sustain labor inflows over the coming years, supporting demand for housing formats that can quickly accommodate new arrivals[2]Organisation for Economic Co-operation and Development, “International Migration Outlook 2025, Germany,” OECD, oecd.org. The student housing shortage also remains significant, which means flexible living options are serving not only international workers but also students who cannot easily access dedicated student beds. This combination matters because both groups value furniture, digital booking, and simpler move-in terms, even if their income levels and stay lengths differ. Operators that shape room mix, lease terms, and amenity packages for both cohorts are likely to capture deeper occupancy than those tied to only one renter profile.

Rental Price Escalation Accelerates Adoption of Managed Accommodation

The Germany co-living market is benefiting from rental inflation, as rising asking rents are pushing more renters to compare total living costs rather than just base rent. Asking rents rose 4.5% year over year by the fourth quarter of 2025, while furnished and fixed-term listings reached a record 17% share of new advertisements, which shows that the market is already moving toward the type of offer co-living operators provide[3]Kiel Institute for the World Economy, “GREIX Rental Price Index Q4 2025, Rental Prices Are Rising Faster Again,” IfW Kiel, ifw-kiel.de. As standard apartments become harder to secure and more expensive to set up, renters place greater value on utilities, furniture, internet, and the convenience of having everything wrapped into one monthly payment. This is especially relevant for international arrivals, project-based employees, and younger professionals who do not want to spend time and money building a household from scratch. The result is that managed accommodation becomes easier to justify, even when the sticker rent is higher than that of a conventional empty unit.

Institutional Capital Reshapes Germany’s Purpose-Built Co-Living Landscape

The Germany co-living market is moving into a more structured phase as larger pools of capital and more formal operating models enter the space. Company announcements from 2025 and 2026 show that scale is becoming a serious advantage, with ActivumSG taking a majority stake in Centralis, Limehome securing fresh funding for expansion, and Habyt narrowing its focus to larger flex-living assets in core European markets. This wave not only adds funding but also brings stronger reporting standards, digital operating systems, and greater ability to work with landlords who want stable occupancy and professional asset management. Smaller operators can still compete in local pockets, but they face a harder path when owners increasingly prefer brands with established systems, broader demand capture, and institutional governance. Over time, this should push the sector toward a smaller group of larger operators without eliminating regional specialists.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent building regulations and permitting requirements are slowing project development | -1.8% | National, most acute in Berlin, Munich, Stuttgart | Medium term (2-4 years) |

| High land acquisition and construction costs are reducing project profitability | -1.5% | National, most severe in Munich, Berlin, Frankfurt | Long term (≥ 4 years) |

| Rent control measures and regulatory interventions limit revenue growth potential for operators | -1.2% | Berlin, Munich, Hamburg, and other rent brake stress areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity and Permitting Timelines Constrain New Supply

The Germany co-living market still faces a tight supply ceiling because regulations slow the conversion of demand into deliverable units. The housing shortage in strong regions is tied not only to demand pressure but also to limited land and strict regulatory settings, which continue to slow the expansion of residential supply. For co-living operators, this means growth depends not just on finding demand but on navigating planning rules, local approvals, and property-use restrictions that can stretch timelines and raise legal costs. Even where demand is clear, operators cannot always bring a product to market quickly enough to capture it, especially in dense urban areas with more oversight and more competing uses for the same buildings. This keeps the Germany co-living market attractive on paper, while uneven execution across cities and business models makes it less attractive in practice.

High Land Acquisition and Construction Costs Compress Developer Returns

The Germany co-living market also remains constrained by the cost of bringing new supply to market, especially in top cities where land prices already start from a high base. When land, fit-out, financing, and compliance costs rise together, operators need higher room yields to make new projects work, and that shifts a greater share of viable product toward mid-scale and premium formats. This effect is stronger for owner-developers because they absorb the full cost risk. At the same time, asset-light operators can expand with lower balance sheet exposure by leasing or managing existing stock. That difference is one reason the market’s business model mix favors master lease and management agreement structures over more capital-heavy development strategies. The Germany co-living market, therefore, shows strong demand potential, but the path to profitable supply remains narrower than the demand picture alone would suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Studio Units Hold The Core Demand Base While Shared Rooms Extend Affordability

Studio/Entire Unit formats held 51.2% of the Germany co-living market in 2025, indicating that privacy remains the strongest demand driver even within a managed, community-oriented housing format. This lead reflects the fact that many residents want a self-contained unit because they are working, relocating, or staying for longer periods and need a stable living setup rather than a purely social one. The segment also aligns well with the needs of corporate assignees and independent professionals who value furniture, housekeeping support, digital leasing, and common amenities but still want separation between private and shared space. Private Room formats sit between privacy and affordability, making them useful for international students and younger urban renters who want a lower monthly cost without sacrificing the quality of location or services. Shared Room formats are forecast to expand at a 10.44% CAGR through 2031, making them the fastest-growing property type as affordability pressure pushes a larger share of renters toward lower-cost room configurations.

That growth pattern does not weaken the role of studios, because the two segments serve different pressure points inside the Germany co-living market. Studio-led assets are likely to remain the revenue anchor because they attract renters with stronger monthly budgets and longer average stays. At the same time, shared rooms give operators a way to widen demand capture and fill buildings more flexibly during cost-sensitive periods. The broader shift toward furnished and fixed-term rentals supports all 3 room formats by normalizing shorter, managed occupancy structures across the housing market. Operators that can balance studios, private rooms, and shared rooms within the same portfolio are better positioned to match demand across different income levels, stay lengths, and mobility needs. In practice, that makes property configuration less about a single winning format and more about having the right mix for each city and renter group.

By Business Model: Asset-Light Structures Support Faster And Safer Expansion

Master Lease / Lease Arbitrage held 47.6% of the Germany co-living market in 2025, which shows that operators and landlords still favor models that can scale without tying up large amounts of capital in property ownership. This structure provides owners with a predictable income stream. It enables operators to expand faster across multiple buildings, which is especially important in a market where attractive supply is limited and timing matters. The model also fits a period in which co-living demand is strong. Still, development conditions remain difficult because leasing an existing asset is often easier than building a new one from scratch. The Management Agreement is forecast to grow at a 10.67% CAGR through 2031, indicating a rising preference among owners to retain the asset while outsourcing operations, branding, and occupancy management to specialist platforms. That shift suggests that landlords are increasingly viewing co-living less as a one-off leasing arrangement and more as an operating model that requires dedicated expertise.

This pattern is reinforced by company moves already visible across the Germany co-living market. Habyt announced in May 2026 that it was focusing on larger assets in core markets and leaning into scale-friendly formats that fit management agreements and master lease structures, indicating where one of the best-known operators sees future efficiency. Asset-heavy ownership models still matter for operators seeking long-term control, premium positioning, or development upside, but they entail greater exposure to land, financing, and construction risks. That leaves the Germany co-living market in a position where asset-light structures are better aligned with present market conditions, especially for operators expanding into multiple cities or working with institutional landlords. Over time, the ability to manage buildings well may become more valuable than owning them outright, because operating quality is increasingly central to pricing, retention, and partnership wins.

By Price Band: Mid-Scale Anchors Volume While Premium Formats Capture Faster Momentum

Mid-Scale accounted for 54.7% of the Germany co-living market in 2025, indicating that the center of demand remains renters seeking convenience and acceptable quality without moving into a luxury price point. This segment works because it speaks to the broadest user base, including working professionals, graduate students, and international arrivals who need furnished housing but still compare costs carefully against standard rentals. Mid-scale products are also easier to place across a broader range of neighborhoods, helping operators expand supply capture rather than relying solely on prime districts. Premium / Luxury is projected to advance at a 11.12% CAGR through 2031, making it the fastest-growing price tier as more operators target relocation budgets, high-income professionals, and residents willing to pay more for design, services, and smoother onboarding. The premium tier also offers some protection against cost pressure, as higher-priced rooms give operators more room to absorb fit-out and service expenses.

This split between volume and growth is one of the clearer features of the Germany co-living market. Mid-scale remains the base scale because it offers the broadest affordability range. Still, premium formats are growing faster because they align with user groups least constrained by deposit requirements, furniture setup costs, and administrative burden. The strategic actions of major operators point toward larger, more standardized, service-rich assets, which supports the view that companies see more upside in products that can justify a higher monthly rate through stronger amenities and smoother occupancy management. At the same time, the Germany co-living industry cannot move too far upmarket, as the market still depends on urban renters who are choosing co-living partly as a response to housing stress, not solely as a premium lifestyle option. The likely outcome is a market where mid-scale stays dominate by volume, while premium gains ground as the more attractive growth segment for branded operators.

By End User: Working Professionals Lead Both Current Demand And Future Expansion

Working Professionals accounted for 57.0% of the Germany co-living market in 2025, indicating this is already a professional-led market rather than one centered solely on students. That matters because working professionals generally have stronger payment capacity, longer stay potential, and a greater need for quick access to housing when they move for employment. The segment also aligns with the product design of most branded operators, since studios, private rooms, digital check-in, work-friendly common areas, and all-inclusive billing map naturally to employment-linked relocation. Working Professionals are forecast to grow at a 11.34% CAGR through 2031, making them the largest and fastest-growing user group. This combination gives the Germany co-living market a more stable demand profile than markets where the largest user group is more seasonal or more dependent on a single academic calendar.

The demand case for professionals is closely linked to Germany’s labor inflow policies and the operational choices of major operators. These policy changes are expected to support continued inflows of job seekers and workers, and these groups often need housing that can be secured quickly and used immediately upon arrival. Students remain important to occupancy, especially in university cities and in more affordable room formats. Still, the working professional segment is stronger because it aligns more closely with the market’s current rent levels and service structure. Operators are increasingly packaging co-living with shared work areas, gyms, and hospitality-style resident services, which makes the offer more relevant to corporate budgets and self-funded professionals alike. That keeps the Germany co-living market positioned less as overflow student housing and more as a practical urban housing format for a mobile workforce.

Geography Analysis

Berlin accounted for 30.8% of the Germany co-living market in 2025 and is projected to expand at a 11.88% CAGR through 2031, making it both the largest and fastest-growing geography in the current market map. The city’s lead is tied to strong, varied demand, as it attracts students, startup workers, international professionals, and creative-sector renters who often need immediate access to furnished housing rather than a lengthy apartment search. Berlin remained one of the fastest-moving rental markets in 2025, which supports the view that new arrivals are pushed toward formats that reduce search time and move-in friction. Operator activity also remains strong in Berlin, with Habyt moving ahead with the DOXS NKLN scheme and STAYERY committing to a large serviced apartment project at Gesundbrunnen Center, which signals confidence in long-term absorption.

Munich is a premium-heavy geography in the Germany co-living market because its renter base includes engineering, life sciences, and corporate professionals with stronger spending power and less tolerance for housing setup delays. Habyt’s January 2026 partnership with STRABAG Real Estate for a 148-room flex-living location in Munich shows that major operators believe the city can support larger service-rich properties aimed at this profile. Frankfurt remains important because its financial and business services base creates a steady need for short- and medium-term managed accommodation, especially for relocations and project assignments. Hamburg is increasingly attractive because company expansion and institutional partnerships are now visible there as well, including Limehome’s announced project with Deka Immobilien at Metropolis-Haus am Gänsemarkt. Together, these cities give the Germany co-living market a strong, top-tier urban base with distinct demand drivers but a common preference for furnished, operationally smooth housing.

The broader national picture shows that the Germany co-living market is no longer limited to only the biggest gateway cities. Secondary locations such as Karlsruhe, Bonn, Cologne, and other employment or university hubs are drawing attention because they combine renter mobility with buildings that may be easier to secure and reposition than prime-city stock. STAYERY’s Karlsruhe expansion and Bonn conversion activity, along with Limehome’s multi-city growth strategy, show that operators are seeking repeatable formats that travel well across diverse local conditions. That shift should help the Germany co-living market reduce its dependence on 1 or 2 headline cities while maintaining exposure to the same core demand themes: mobility, affordability pressure, and faster move-in needs.

Competitive Landscape

The Germany co-living market remains fragmented, but the competitive center is moving toward larger branded operators with stronger funding, better systems, and broader landlord relationships. This change is visible in how leading companies are approaching expansion: they are no longer relying solely on individual site launches and instead building platform scale through capital raises, portfolio concentration, and structured partnerships. Centralis gained strong backing when ActivumSG acquired a majority stake in July 2025 and outlined a portfolio target of gross asset value above USD 550 million, signaling that scaled institutional capital is now willing to build around managed accommodation platforms in Germany. Limehome also strengthened its position in December 2025 when it secured USD 82.5 million in strategic financing and pushed its live and contracted portfolio above 12,500 units across Europe, which supports broader operating leverage and faster city coverage.

Habyt’s strategy offers another clear example of how competition is changing in the Germany co-living market. In May 2026, the company exited selected non-core portfolios outside its priority markets. It said future assets would target larger room counts, indicating a preference for scale, stronger amenity density, and a tighter operational focus. In January 2026, it also partnered with STRABAG Real Estate on a 148-room Munich project, demonstrating how branded operators are using development alliances to secure high-quality urban assets without relying solely on direct ownership. STAYERY’s Berlin, Karlsruhe, and Bonn projects point to a similar pattern in which operators are combining leases, conversions, and selective co-investment structures to grow across different city profiles. These moves suggest that competitive advantage now depends on more than occupancy, as operators need access to financing, design consistency, digital operations, and the ability to work with institutional property owners.

At the same time, the Germany co-living market is not becoming a winner-takes-all space. Regional operators and niche specialists can still compete where they understand local demand, can convert unusual assets, or can serve a specific renter group better than a broad platform. What is changing is that the bar for expansion is rising, as landlords increasingly expect reliable reporting, a consistent resident experience, and the ability to fill buildings with less friction. The rent brake extension also puts pressure on operators to compete through product design, services, furnishings, and building-use strategy rather than relying on simple rent growth in regulated markets. That should keep the Germany co-living market open to multiple players, while still favoring the operators that can scale carefully and execute with discipline.

Germany Co-Living Industry Leaders

Habyt

Wunderflats

Medici Living

The Base

STAYERY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Habyt divested its co-living portfolios in France, Portugal, and Spain to 3 separate local operators, following the April 2026 sale of its Asia-Pacific portfolio to Mitsubishi Estate. The strategic refocus concentrates the Habyt brand exclusively on core markets in Germany, Austria, Switzerland, and Southern Europe, with future assets targeting a minimum of 150 rooms and an average of 300 rooms per property to achieve hospitality-grade amenity standards at scale.

- January 2026: Habyt and STRABAG Real Estate announced a partnership to anchor a new flex-living location at Hanauer Strasse, Munich, with 148 rooms across 6,000 square meters, including gym, sauna, and café amenities. Beyond Hospitality Consulting brokered the transaction and represents Habyt’s largest new commitment in Munich, with a scheduled opening in 2028.

- December 2025: Limehome secured a USD 82.5 million strategic investment from Cheyne Strategic Value Credit, comprising growth financing and an equity component. The investment supported Limehome’s 2025 milestone of signing more than 3,500 units across Europe, bringing its total live and contracted portfolio to more than 12,500 units, with plans to deliver more than 1,000 additional live units in the first half of 2026.

Germany Co-Living Market Report Scope

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light, Master Lease / Lease Arbitrage |

| Asset-Light, Management Agreement |

| Asset-Heavy, Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| Berlin |

| Munich |

| Frankfurt |

| Hamburg |

| Rest of Germany |

| By Property Configuration | Studio / Entire Unit |

| Private Room | |

| Shared Room | |

| By Business Model | Asset-Light, Master Lease / Lease Arbitrage |

| Asset-Light, Management Agreement | |

| Asset-Heavy, Own-Develop-Operate | |

| By Price Band | Economy |

| Mid-Scale | |

| Premium/Luxury | |

| By End User | Students |

| Working Professionals | |

| By City | Berlin |

| Munich | |

| Frankfurt | |

| Hamburg | |

| Rest of Germany |

Key Questions Answered in the Report

What is the 2026 size of Germany's co-living?

The Germany co-living market is valued at USD 610.11 million in 2026 and is forecast to reach USD 954.89 million by 2031, with a 9.37% CAGR.

Which room format drives demand for co-living in Germany?

Studio/Entire Unit is the leading property configuration, with a 51.2% share in 2025, reflecting strong demand for privacy in managed accommodation.

Which renter group drives the strongest demand for co-living in Germany?

Working professionals are the largest end-user group, with a 57.0% share in 2025, and they are also the fastest-growing group, with a 11.34% CAGR through 2031.

Why is Berlin so important for Germany's co-living?

Berlin held 30.8% share in 2025 and is forecast to grow at 11.88% CAGR through 2031, supported by persistent housing pressure and active operator expansion.

Which business model is scaling fastest in Germany's co-living?

Management Agreement is the fastest-growing business model, with a 10.67% CAGR, while Master Lease/Lease Arbitrage remains the largest, with a 47.6% share in 2025.

What is the biggest growth opportunity for operators in Germany's co-living?

The clearest opportunity is to serve mobile professionals with furnished, flexible, and service-led housing, while expanding through asset-light partnerships in both major and secondary cities.

Page last updated on: