India Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

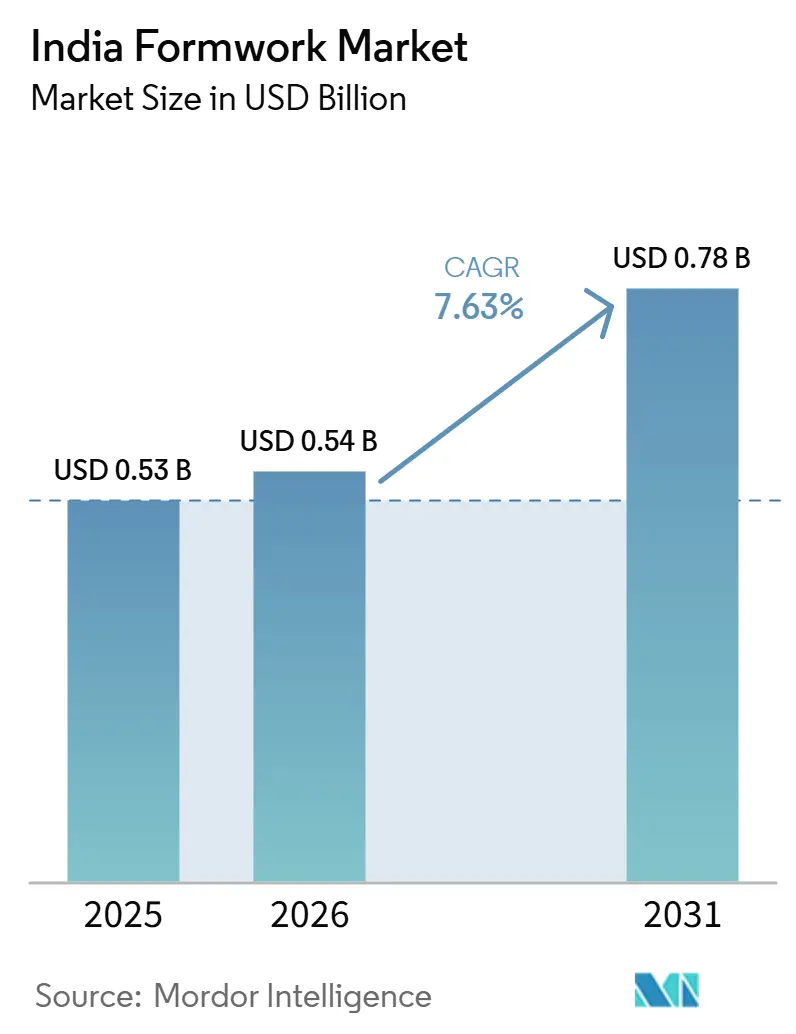

| Base Year Market Size (2025) | USD 0.53 Billion |

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 0.78 Billion |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

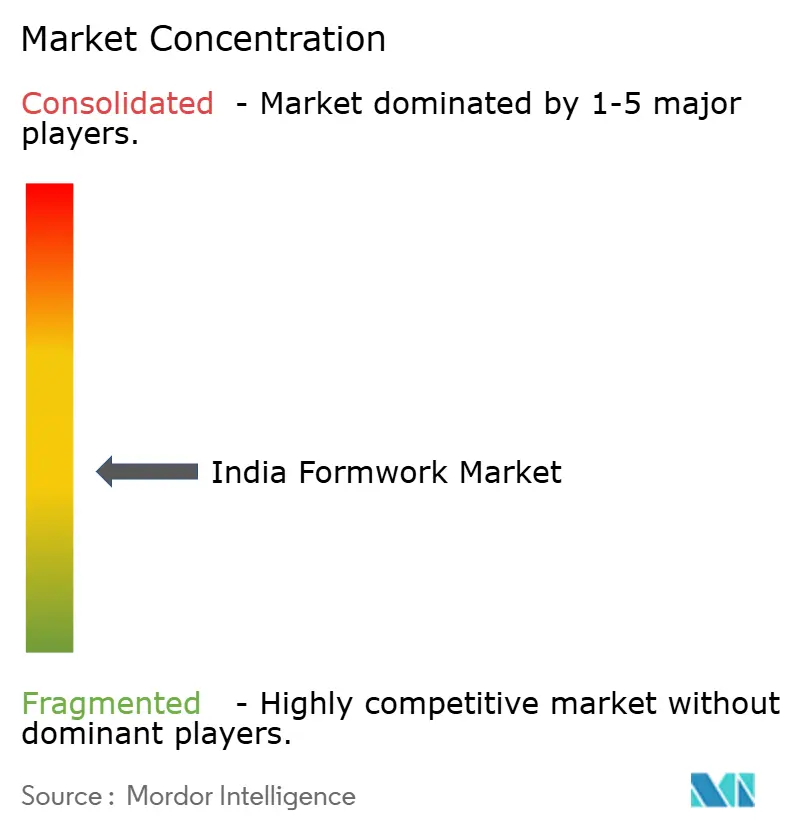

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Formwork Market Analysis by Mordor Intelligence

The India Formwork Market size is expected to increase from USD 0.53 billion in 2025 to USD 0.54 billion in 2026 and reach USD 0.78 billion by 2031, growing at a CAGR of 7.63% over 2026-2031.

Public spending continues to shape the direction of the India formwork market, as infrastructure capital expenditure in the Union Budget 2026-27 rose to INR 12.22 lakh crore (USD 132.8 billion), keeping road, rail, metro, and urban projects active across major states. Demand in the India formwork market is also moving toward engineered systems because more projects now involve taller cores, longer spans, bridge pylons, and repetitive concrete structures that need faster cycles and tighter site control. The National Infrastructure Pipeline remained a major support base in 2026, with 14,563 tracked projects and a projected investment of INR 213 trillion (USD 2.6 trillion), keeping the medium-term opportunity broad even as individual project awards move unevenly across states. Compliance standards are becoming more relevant in the India formwork market because engineered falsework design, inspection practices, and stripping rules are pushing contractors toward better-documented systems on larger jobs. Demand still carries concentration risk because revenue remains centered in a small group of large cities, so utilization can tighten quickly when project approvals or site mobilization slow in those hubs.

Key Report Takeaways

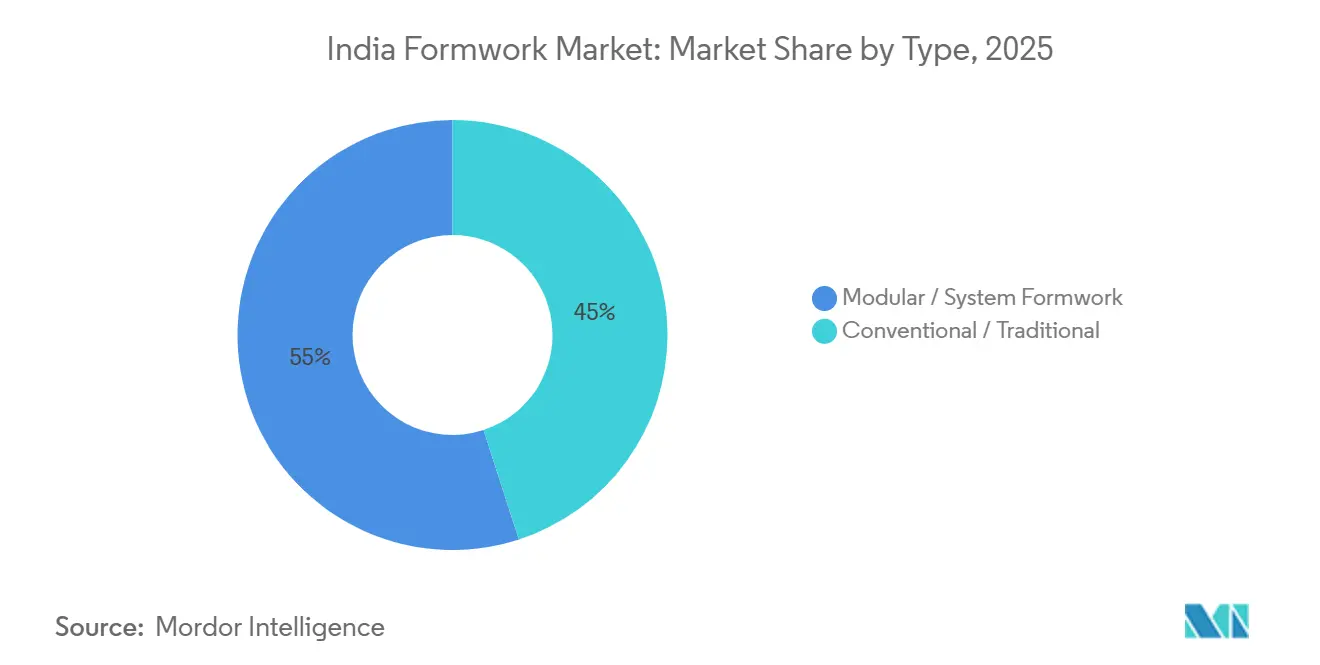

- By type, modular / system formwork led with 55% share in 2025 and was also the fastest-growing type with an 8.20% CAGR through 2031.

- By configuration, climbing formwork held the largest 34% share in 2025, while tunnel formwork recorded the fastest projected CAGR at 8.00% through 2031.

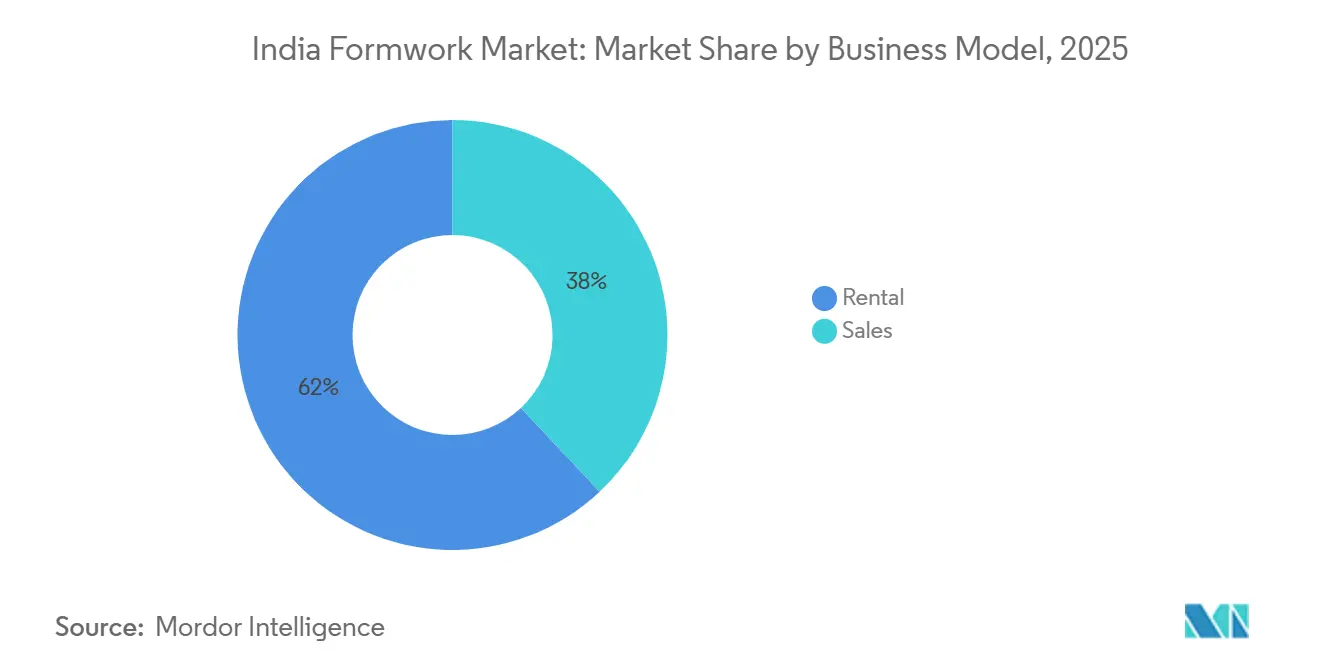

- By business model, rental held 62% of the India formwork market share in 2025, and this segment also expanded the fastest at 8.45% through 2031.

- By sector, infrastructure accounted for 39% share of the India formwork market size in 2025 and also posted the highest forecast CAGR at 9.00% through 2031.

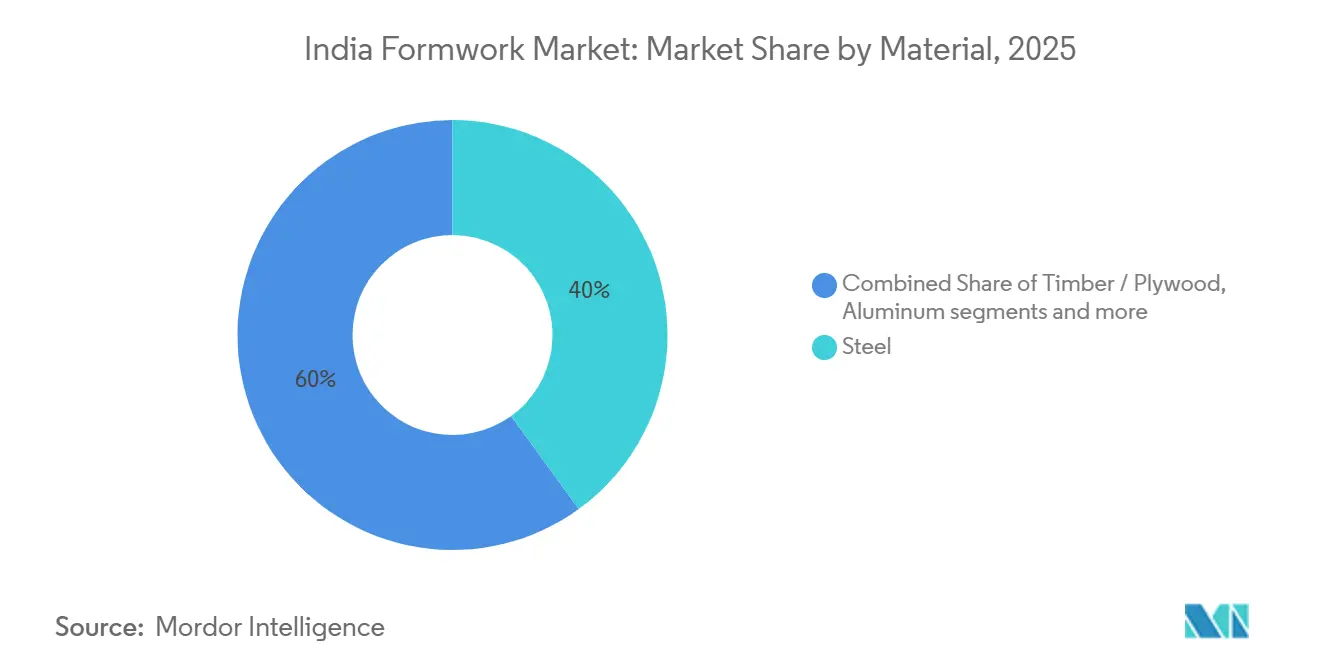

- By material, steel led with 40% share in 2025, while aluminum was the fastest-growing material at 8.20% through 2031.

- By geography, Mumbai Metropolitan Region held the largest 26% share in 2025, while Delhi NCR recorded the highest projected CAGR at 8.50% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Residential and Commercial Construction | +1.5% | Pan-India, with concentration in Mumbai MMR, Bengaluru, Pune, Delhi NCR | Short term (≤ 2 years) |

| Growth in Infrastructure and Mega Projects | +1.3% | National highway, metro, and port corridors, concentrated in Maharashtra, Uttar Pradesh, Karnataka | Long term (≥ 4 years) |

| Faster Project Execution Accelerates Engineered Formwork Adoption | +1.2% | National, with early gains in metro infrastructure corridors | Medium term (2-4 years) |

| Shift Toward Reusable and Modular Systems | +1.1% | National, stronger in Tier I and Tier II cities | Medium term (2-4 years) |

| Increasing High-Rise Construction | +0.9% | Mumbai, Delhi NCR, Bengaluru, Hyderabad high-rise clusters | Long term (≥ 4 years) |

| Labor Productivity and Quality Requirements | +0.8% | National, with above-average impact in high-rise markets of Mumbai and Delhi NCR | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Residential and Commercial Construction

Housing delivery schedules are keeping the India formwork market active because large concrete programs need steady slab, wall, and column cycles across many parallel towers. The strongest effect is visible where completion discipline is stricter, since projects with fixed launch and handover commitments cannot absorb long delays in structure work. Commercial construction also supports the India formwork market, as office and mixed-use assets require regular floor plates, core walls, transfer structures, and repeated concrete sequencing in dense urban areas. This raises the value of systems that can reduce assembly variability and shorten the gap between pours. The result is that suppliers serving premium residential and commercial corridors are seeing demand shaped less by unit count alone and more by schedule certainty, repetition intensity, and the ability to keep crews productive across multiple active fronts.

Growth in Infrastructure and Mega Projects

Large infrastructure programs are widening the demand base of the India formwork market beyond residential towers. The Ministry of Statistics and Programme Implementation (MoSPI) tracked 1,981 central sector infrastructure projects with a revised cost of INR 42.78 lakh crore (USD 513 billion), as of April 2026, and project additions in the final quarter of FY2026 rose sharply, with roads and highways taking the largest share of added project cost[1]Ministry of Statistics and Programme Implementation, “Flash Report on Central Sector Infrastructure Projects,” PIB, pib.gov.in. That mix matters because bridge decks, viaducts, pylons, and transport structures need more specialized systems than ordinary slab work. Doka’s July 2025 deployment on the Mumbai-Pune Expressway Missing Link showed how technically demanding bridge packages require climbing systems, large-area formwork, and engineered support rather than simple shuttering supply. This keeps infrastructure as one of the clearest long-run demand anchors for the India formwork market.

Faster Project Execution Accelerates Engineered Formwork Adoption

The India formwork market is benefiting from the push for shorter slab cycles, as developers and contractors are under greater pressure to complete repetitive structures on time. A 2025 peer-reviewed study on Indian high-rise construction found that aluminum formwork reduced construction time by 45% and lowered total project cost by 3% against conventional methods on suitable repetitive projects. That time advantage matters even more in the India formwork market, where projects feature multiple towers or deep structural packages, because even small delays at the shell stage ripple through the rest of the schedule. The practical limitation is that faster systems still need trained installation teams, disciplined sequencing, and better site planning. Even so, the operating logic is clear, and contractors are increasingly choosing formwork that prioritizes speed rather than minimizing initial purchase cost.

Shift Toward Reusable and Modular Systems

Reusable systems are changing the economics of the India formwork market by spreading costs over many cycles and reducing material loss. Aluminum systems sustain far more reuse cycles than conventional plywood-based methods under Indian site conditions, making them more cost-effective for highly repetitive projects. In the India formwork market, suppliers have also strengthened their service role by focusing on layout planning, load checks, sequencing, and stripping support, which matter more when contractors work with engineered systems. Compliance adds another layer because standards-based execution favors documented materials and more structured engineering practice. As a result, reusable and modular solutions are not only replacing timber on technical grounds, but they are also deepening customer dependence on organized suppliers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial CAPEX for Engineered Systems | -0.9% | National, most acute in Tier II cities and among small contractors | Medium term (2-4 years) |

| Price Sensitivity across the Construction Sector | -0.8% | National, intensified in volume residential segments | Short term (≤ 2 years) |

| Skilled Labor and Installation Dependency | -0.7% | Pan-India, particularly acute in Delhi NCR, Mumbai, Bengaluru high-rise clusters | Medium term (2-4 years) |

| Project-Based Demand Volatility | -0.6% | National, with greater severity in road-focused contractor segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX for Engineered Systems

The India formwork market still faces a significant entry barrier because engineered systems require higher upfront costs than conventional plywood-based approaches. Aluminum formwork typically costs INR 8,000-9,000 per square meter (USD 96-108 per square meter), making it difficult for smaller developers and contractors to absorb the upfront investment without financing. This cost gap keeps a large share of the volume base tied to traditional methods, even when modular systems offer better long-term economics for repetitive jobs. Standards for falsework design and stripping practice also increase the implementation burden, as contractors need either internal competence or paid technical support to use these systems properly. Until financing or leasing access improves more broadly, high upfront system cost will continue to slow full conversion in the India formwork market.

Price Sensitivity across the Construction Sector

Price competition remains a structural restraint in the India formwork market because many contractors still purchase or rent formwork as a cost item rather than as a productivity tool. Domestic suppliers continue to compete intensely with imported systems, while Technocraft's formwork business generated INR 550 crore (USD 66 million) in the nine months to December 2025, with operating margins of 9.15%. That pricing pressure makes it harder for suppliers to invest in engineering support, training, and service depth. When service quality remains thin, contractors see fewer visible gains and become even more price-driven in the next buying cycle. This loop keeps the India formwork market competitive, but it also limits value capture for suppliers that are trying to move customers toward better systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular / System Formworks Commands Structural Share

Modular / system formwork held 55% of the India formwork market in 2025 and is forecast to grow at 8.20% through 2031, keeping it ahead of the overall market pace. This lead reflects the steady move away from jobsite-fabricated timber on projects where repetition, quality control, and speed matter more than the lowest initial spend. Organized contractors and Engineering, Procurement, and Construction (EPC) firms have been the main force behind this shift because they work on larger packages where standardization reduces delays and site rework. The India formwork market has therefore become more favorable to suppliers that can provide engineered layouts, technical support, and reusable inventory across several project cycles. Conventional / traditional formwork remains relevant where building heights are lower and project repetition is limited.

That continued role for traditional systems is strongest in Tier II and Tier III locations, where contractors often rely on local carpentry skills and lower-budget site practices. The replacement process is gradual because conventional methods still suit custom shapes, smaller structures, and projects with too few floors to recover the cost of a modular system. Even so, the relative position of this segment is weakening as customer expectations move toward faster shell completion and cleaner concrete finish. A 2025 peer-reviewed comparison found that modular systems reduced project time by 45% and cut total project costs by up to 3% for repetitive high-rise structures, which helps explain why large residential and housing programs are writing modular systems into execution plans more often. In the India formwork market, this means the type mix is now being shaped by structural repetition, compliance discipline, and contractor ability to plan reuse rather than by material familiarity alone.

By Configuration: Climbing Systems Define the Premium Tier

Climbing formwork held the largest 34% share in 2025, underscoring the importance of vertical concrete work in the India formwork market. Its position is tied to high-rise residential cores, bridge pylons, dam structures, and other projects where continuous height progression requires controlled lifting and stable working platforms. These systems also reduce the crane's dependence on suitable sites, improving sequencing when tower crane time is heavily contested. In practice, climbing solutions sit at the premium end of the market because they combine equipment, engineering, and site-method support in a single offer. Their role has expanded with the rise of mixed-use towers and the increasingly technical nature of transport infrastructure.

Tunnel formwork is the fastest-growing configuration, with an 8.00% CAGR through 2031, and its growth is linked to the execution of repetitive housing projects. Government Light House Project demonstrations helped move tunnel systems from a niche method into a visible reference point for larger housing programs. Studies indicate that tunnel systems can achieve 450-500 reuse cycles under Indian conditions, far exceeding the 200-250 reuse cycles typically reported for aluminum formwork in comparable analyses. Static and slipform configurations remain in place in tanks, silos, and utility structures, where demand is lower but the work is technically challenging. As a result, configuration choices in the India formwork market increasingly reflect the concrete geometry and repetition profile of each job rather than a one-system-fits-all approach.

By Business Model: Rental Dominance Reflects Capital Discipline

Rental held 62% of the India formwork market share in 2025 and is also the fastest-growing business model with an 8.45% CAGR through 2031. That position is logical because many contractors manage several projects with different durations, start dates, and structural mixes, which creates large idle inventories that are expensive to own. Renting gives them access to better systems without requiring a full capital commitment for every project. This has made the India formwork market more service-oriented, especially for customers who need equipment, planning assistance, and rapid redeployment between sites. Large suppliers benefit because they can move fleets across cities and sectors as demand shifts.

The sales model still matters for large Engineering, Procurement, and Construction (EPC) firms and contractors that keep permanent captive fleets for recurring work. Ownership is more attractive when project pipelines are visible, storage and maintenance are controlled, and crews are trained on a narrow set of systems. Even so, rental remains structurally stronger because it fits an asset-light operating model and lowers the adoption barrier for engineered formwork. A broader shift toward construction equipment rental in India supports the same logic across adjacent equipment categories. In the India formwork market, this means business model preference is driven less by product ideology and more by cash flow discipline, project turnover, and the need to match inventory flexibility with uneven site mobilization.

By Sector: Infrastructure Rewrites the Demand Mix

Infrastructure accounted for 39% share of the India formwork market size in 2025 and is set to grow at 9.00% through 2031, making it both the largest and fastest-growing sector. This segment stands apart because its structures often require higher load ratings, unusual geometry, and more engineered support than the slab-heavy work common in ordinary housing. The National Infrastructure Pipeline remained a major source of continuity, with 14,563 projects and a projected investment of INR 213 trillion (USD 2.6 trillion) in March 2026, supporting roads, logistics, energy, and transport packages over a multiyear horizon. The Ministry of Statistics and Programme Implementation (MoSPI) also reported that India’s construction gross value added expanded by 8.4% year on year in the fourth quarter of FY2026, reinforcing the broad construction base supporting formwork demand. The India formwork market, therefore, gains not only from project volume in infrastructure, but also from the higher technical value of each package.

Residential remains the second-largest sector and continues to support broad utilization, driven by housing completions and government housing programs. Commercial, industrial, and logistics projects add another layer of stability by creating consistent demand for core walls, podiums, transfer slabs, warehouses, and utility blocks. What changes the revenue mix is that infrastructure often commands more value per square meter of active formwork than standard apartment construction. That is why sector share by volume does not fully describe earnings opportunities for organized suppliers. Across the India formwork market, sector demand is now less about counting sites and more about understanding which structures require premium engineering and which ones can still be served with simpler modular fleets.

By Material: Steel Holds Ground; Aluminum Rewrites Economics

Steel held a 40% share in 2025, making it the leading material in the India formwork market. Its position reflects strong performance in columns, walls, and heavy infrastructure structures, where durability and resistance to high concrete pressure are critical. Steel also fits jobs where contractors want robust systems that can handle demanding site conditions and repeated handling. This keeps it central to industrial, transport, and large civil packages even as other materials gain traction. Its leadership shows that the market is not shifting to lightweight materials uniformly across all applications.

Aluminum is the fastest-growing material, growing at 8.20% through 2031, because it supports faster slab cycles and more repetitions in repetitive structures. This growth is supported by the increasing adoption of Mivan-style construction and its wider use in large housing programs. At the same time, the Ministry of Housing and Urban Affairs' progress report on Pradhan Mantri Awas Yojana - Urban (PMAY-U) shows the scale of urban housing activity that continues to support the use of reusable concrete construction methods[2]Ministry of Housing and Urban Affairs, “Pradhan Mantri Awas Yojana Urban Progress Reports,” Government of India, pmay-urban.gov.in. A 2025 peer-reviewed study also showed clear time and cost savings with aluminum formwork for repetitive high-rise structures, reinforcing its advantage when floor plates repeat across many levels. Timber or plywood, plastic or fiberglass, and other materials still serve low-rise, custom, and niche requirements, but their role is narrowing as project complexity rises. In the India formwork market, material choice is increasingly driven by life-cycle productivity, repetition count, and engineering reliability rather than a simple comparison of initial panel cost.

Geography Analysis

Mumbai Metropolitan Region held a 26% share in 2025, making it the largest regional contributor to the India formwork market. Its project mix is more technically demanding than most other city clusters because premium towers, mixed-use developments, and transport works run side by side. That combination lifts demand for self-climbing systems, large-area slab formwork, and more carefully engineered support packages. The Missing Link bridge package near Mumbai demonstrated this clearly in 2025, where Doka supplied Xclimb60 Short Track, SKE100 Plus automatic climbing systems, and Top 50 large-area formwork for very tall diamond-shaped pylons[3]Doka GmbH, “Doka Supports the Delivery of the Mumbai-Pune Expressway’s Missing Link Cable-Stayed Bridge Pylons,” Doka, doka.com. In revenue terms, Mumbai benefits not only from project count but also from the higher value intensity of the jobs being executed.

Delhi NCR is forecast to grow at 8.50% through 2031, making it the fastest-growing city-level geography in the India formwork market. The region is benefiting from premium residential launches, urban transport development, and industrial corridor activity that together sustain a larger pipeline of reinforced concrete structures. Larsen and Toubro’s April 2026 award for seven high-rise towers in Gurugram supports this direction, as it creates a significant demand for shell-and-core formwork in one of the region’s most active submarkets. Delhi NCR also tends to reward systems that can support faster erection and tighter schedule management on multi-tower developments. That is why the India formwork market is seeing stronger pull in this region for certified engineered systems and structured rental support rather than ad hoc timber-based approaches.

Pune, Bengaluru, and the rest of the country together form the wider growth reserve for the India formwork market. Their role matters because they broaden demand beyond the 2 largest urban centers and create a larger volume base for domestic suppliers. Pune and Bengaluru are well placed for modular and aluminum deployment, where residential repetition and commercial expansion make better cycle economics possible. The rest of India adds steady volume through housing programs and urban infrastructure, even if project values and technical complexity are lower than in Mumbai or Delhi NCR. This spread reduces some dependence on the biggest cities, but the India formwork market remains meaningfully concentrated in the leading metros where the highest-value applications are located.

Competitive Landscape

The India formwork market is moderately fragmented, with a small group of international specialists operating alongside a long tail of domestic manufacturers and rental companies. International suppliers such as PERI India Pvt. Ltd., Doka India Private Limited, ULMA Formwork and Scaffolding Systems India Pvt. Ltd., and RMD Kwikform India Private Limited compete mainly on engineering capability, product range, and integrated rental-plus-service support. Their advantage is strongest on bridge pylons, climbing-core high-rises, tunnel form housing, and other projects where design input matters as much as panel supply. Domestic players remain important because they offer lower-cost alternatives and are often better placed for regional distribution and price-sensitive work. This creates a clear two-tier structure inside the India formwork market rather than a single uniform field.

Competitive positioning is increasingly tied to localization rather than simple import of global systems. Technocraft stands out among domestic manufacturers because its formwork business reached INR 550 crore (USD 66 million) in the nine months to December 2025, and the company reported full utilization of its backward-integrated aluminum extrusion plant by early 2026, along with planned expansion. Doka provided another example in July 2025 by supporting the Missing Link bridge pylons with advanced climbing and large-area systems, thereby reinforcing its position in technically demanding infrastructure work. PERI India’s localization push also matters because India-specific product development and local engineering support improve fit for local site conditions and customer budgets. These moves show that scale alone is not enough in the India formwork market, since suppliers also need engineering relevance, faster service response, and inventory suited to Indian project mixes.

White-space opportunities remain strongest in organized rental for Tier II cities, digital fleet management, and specialized systems for data centers, logistics buildings, and repetitive housing. The market is also becoming more compliance-sensitive because structured quality systems and documented engineering practice matter more on government-linked and large private projects. This favors companies that can combine certification discipline with technical support and redeployable inventory. The overall effect is a competitive field where no single supplier dominates the India formwork market. Still, the gap between organized engineering-led providers and price-led local operators is becoming more visible.

India Formwork Industry Leaders

PERI India Pvt. Ltd.

Doka India Private Limited

ULMA Formwork and Scaffolding Systems India Pvt. Ltd.

RMD Kwikform India Private Limited

Technocraft Industries (India) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Tata Projects secured construction contracts worth INR 1,100 crore (approximately USD 132 million) from Godrej Properties for three luxury residential developments on Golf Course Road, Gurgaon (Godrej Sora, Godrej Astra, Godrej Samaris), involving RCC shell and core construction for high-rise towers, each project requiring engineering-grade climbing and slab formwork systems across multiple basement-plus-55-floor structures.

- April 2026: Larsen & Toubro's Buildings & Factories business won multiple significant orders in the INR 1,000-2,500 crore range (USD 108.7-271.7 million), including the construction of seven high-rise residential towers in Gurugram for Oberoi Realty, encompassing RCC shell and core construction, earthworks, and piling within stringent timelines, directly creating structured formwork demand in Delhi NCR's premium residential segment.

- February 2026: Technocraft Industries' aluminum formwork business, Mach One, achieved 100% utilization of its backward-integrated aluminum extrusion plant in Aurangabad. The company also announced a second phase of capacity expansion toward the end of FY2027 and projected that its scaffolding and formwork segment would cross INR 2,000 crore (USD 240 million) in revenue within 3 years.

- July 2025: Doka India provided formwork expertise and systems, including Xclimb60 Short Track, Automatic Climbing SKE100 Plus, and Large-area Top 50 formwork, for the construction of 4 diamond-shaped pylons, each 181.77 meters tall, on the Mumbai-Pune Expressway Missing Link cable-stayed bridge. The project is executed by Afcons Infrastructure for MSRDC and represents one of the technically most demanding formwork deployments in India to date.

India Formwork Market Report Scope

The India Formwork Market Report is Segmented by Type (Conventional / Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and Tunnel), Business Model (Sales and Rental), Sector (Residential, Commercial, Industrial & Logistics and Infrastructure), Material (Timber / Plywood, and More), and City (Mumbai Metropolitan Region, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fiberglass |

| Others |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Rest of India |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fiberglass | |

| Others | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Rest of India |

Key Questions Answered in the Report

What is the projected value of the India formwork market by 2031?

The India formwork market is forecast to reach USD 0.78 billion by 2031, rising from USD 0.54 billion in 2026 at a 7.63% CAGR over 2026-2031.

Which segment leads by type in India?

Modular / system formwork led by type with 55% share in 2025 and also remained the fastest-growing type at 8.20% through 2031.

Why is rental the dominant business model in India?

Rental held 62% share in 2025 because many contractors prefer asset-light access to engineered systems instead of owning and storing full fleets between projects.

Which end-user sector creates the strongest demand?

Infrastructure was the largest and fastest-growing sector, with 39% share in 2025 and a 9.00% CAGR through 2031, supported by roads, metro, ports, and other large civil works.

Page last updated on: