United Kingdom Co-Living Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

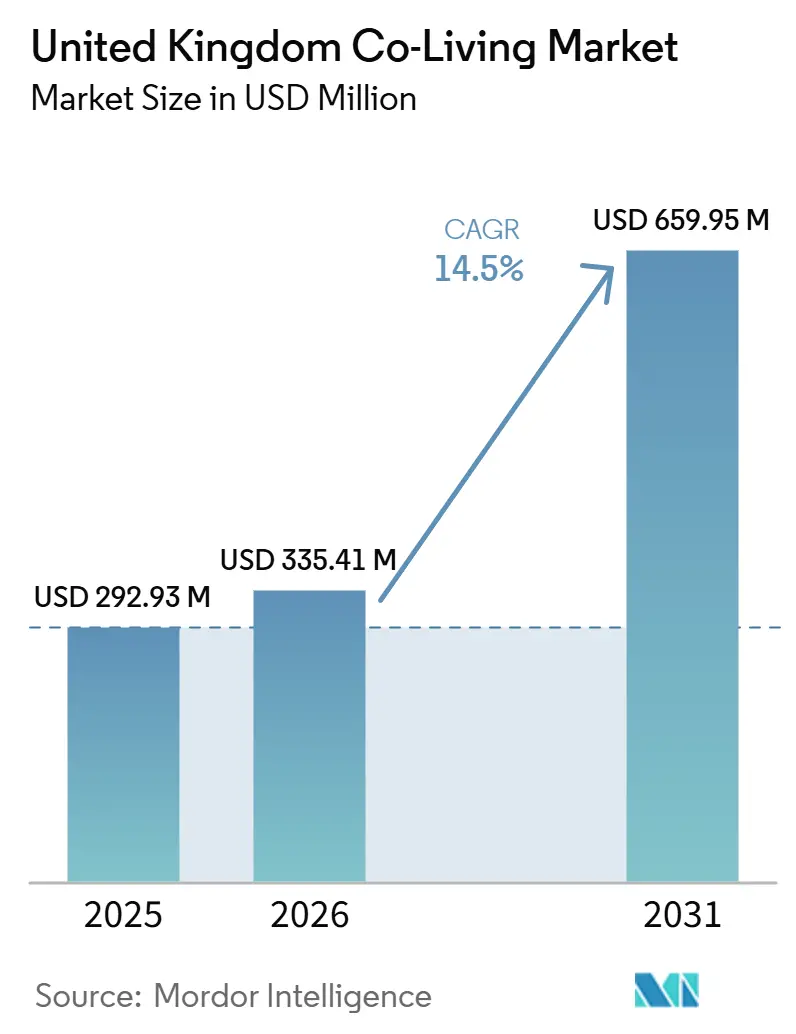

| Base Year Market Size (2025) | USD 292.93 Million |

| Market Size (2026) | USD 335.41 Million |

| Market Size (2031) | USD 659.95 Million |

| Growth Rate (2026 - 2031) | 14.50% CAGR |

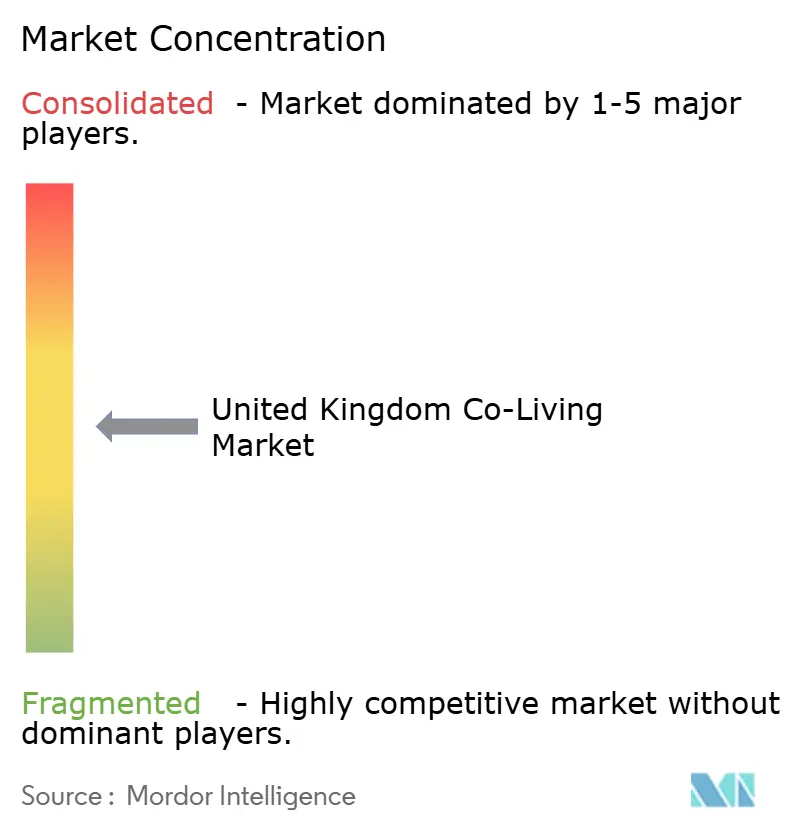

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Co-Living Market Analysis by Mordor Intelligence

The United Kingdom Co-Living Market size is projected to be USD 292.93 million in 2025, USD 335.41 million in 2026, and reach USD 659.95 million by 2031, growing at a CAGR of 14.5% from 2026 to 2031.

The United Kingdom co-living market is expanding because housing affordability remains strained, rental supply is tight, and bundled living costs still compare well with conventional private renting in major cities. The format is also moving beyond its earlier shared-housing image, as self-contained units, stronger management standards, and amenity-led schemes attract a wider professional renter base. In the United Kingdom co-living market, investor interest is now aligning with a clear preference for capital-light operating structures, helping brands scale without taking on full development ownership risk. Premium formats are gaining traction because their predictable monthly pricing, privacy, and community spaces better align with the needs of mobile urban workers than standard renting. Near-term delivery will still face pressure from planning complexity, building safety requirements, and higher project costs. Yet, the United Kingdom co-living market still has room to grow, as current stock remains small relative to its addressable renter base.

Key Report Takeaways

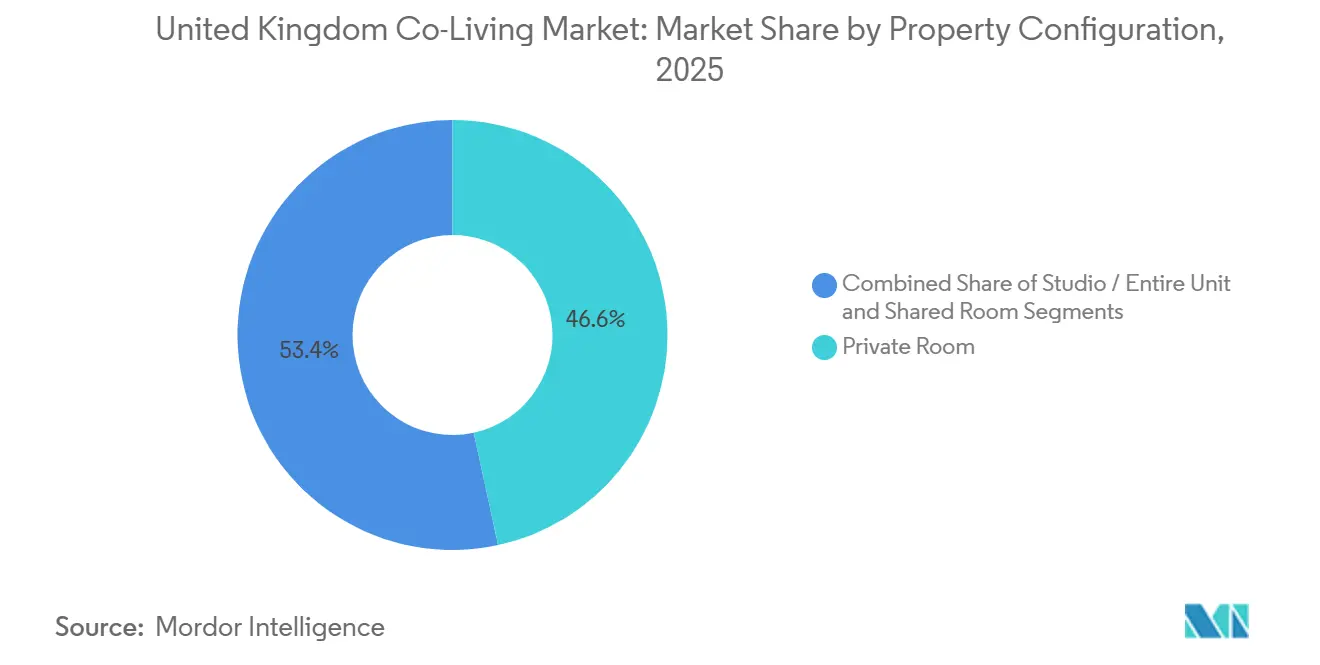

- By property configuration, studio and entire unit formats held 53.4% of the United Kingdom co-living market share in 2025, while the same format is projected to expand at a 15.76% CAGR through 2031.

- By business model, own-develop-operate held 47.1% of the market in 2025, while management agreements are forecast to grow at a 16.10% CAGR through 2031.

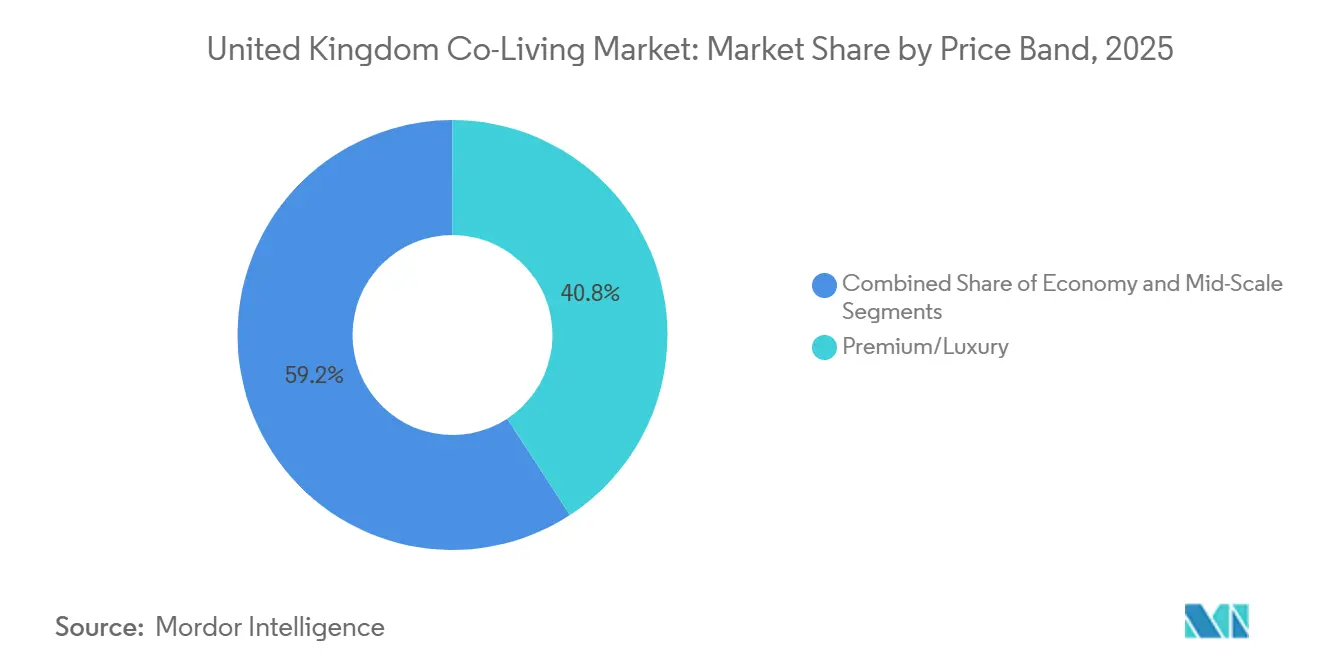

- By price band, premium and luxury held 40.8% of the market in 2025, while the same tier is projected to rise at a 16.31% CAGR through 2031.

- By end user, working professionals accounted for 58.9% of demand in 2025, while the same segment is set to grow at a 15.44% CAGR through 2031.

- By geography, England held 40.1% of the market in 2025, while Scotland is forecast to expand at a 17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Co-Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Housing Affordability Pressure In Major Cities | +3.8% | National, with the strongest effect in London, Manchester, and Bristol | Short term (≤ 2 years) |

| Growing Young Professional And International Worker Demand | +2.6% | National, with early gains in London, Edinburgh, and Manchester | Medium term (2-4 years) |

| Rising Institutional Investment In Purpose-Built Co-Living | +2.4% | England-led, with spillover into Scotland and Wales | Medium term (2-4 years) |

| Strong Preference For Amenity-Rich Community Living | +1.9% | National, especially London and large university cities | Long term (≥ 4 years) |

| Build-to-Rent Expansion Supporting Managed Co-Living Supply | +1.7% | England-led, with regional diversification underway | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Housing Costs Create Structural Co-Living Demand

Housing costs continue to support the United Kingdom co-living market because bundled rent, utilities, and shared amenities reduce budgeting uncertainty for urban renters. Average private rents across the United Kingdom reached USD 1,790.1 per month in March 2026, while London exceeded USD 2,860 per month, keeping pressure on single renters with limited room for large upfront housing costs[1]Office for National Statistics, “Index of Private Housing Rental Prices, UK: March 2026,” Office for National Statistics, ons.gov.uk. This cost gap matters even more in cities where standard renting also brings separate utility bills, deposits, and furnishing costs. Operators are therefore selling co-living less as a discount product and more as a clearer monthly living package with fewer cost surprises. That shift helps the United Kingdom co-living market appeal to renters who want cost control without giving up location or service quality.

Young Professionals and International Workers Demand Lengthening Residency Cycles

The United Kingdom co-living market is attracting a larger share of working professionals and internationally mobile residents who want flexibility without the instability of short-term stays. This renter group tends to value simple onboarding, furnished homes, and a clear service model more than older shared-housing formats can offer. The result is a longer resident stay pattern than the sector once carried in its early reputation. Longer stays matter because they cut reletting friction, protect occupancy, and make pricing discipline easier during renewals. That resident mix is helping the United Kingdom co-living market move toward a steadier income profile that suits both operators and capital partners.

Institutional Capital Accelerates Sector Maturation

Institutional capital is helping the United Kingdom co-living market move from a niche living format into a more structured operating category. Investors are showing stronger interest in platforms that separate building ownership from brand, leasing, and resident management. This is why management agreement models are gaining momentum faster than fully integrated structures. In practice, operators can scale across more sites by providing systems, pricing, and occupancy services to third-party owners rather than funding the full development risk themselves. That shift is likely to make the United Kingdom co-living market more competitive, because better-funded platforms can grow faster. At the same time, specialist developers stay focused on land, approvals, and delivery.

Community And Wellbeing Amenities Drive Retention Beyond Accommodation Basics

Amenity depth is becoming a core demand factor in the United Kingdom co-living market, especially for renters comparing co-living with modern multifamily housing. Fitness rooms, coworking spaces, shared kitchens, communal lounges, and event programming now shape how residents judge value, not just convenience. This matters because co-living works best when privacy inside the unit is matched by useful shared space outside it. Prominent schemes are now treating community-oriented design as a central part of the product rather than an optional add-on[2]Bridges Fund Management, “City of London’s First Co-Living Homes Move Ahead,” Bridges Fund Management, bridgesfundmanagement.com. As more schemes follow this model, the United Kingdom co-living market is likely to reward operators that invest in both physical amenities and resident programming.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction And Financing Cost Pressure | -1.8% | National, with the strongest effect in London | Short term (≤ 2 years) |

| Planning And Zoning Approval Complexity | -1.6% | National, with a sharper impact in cities lacking a clear co-living policy | Short term (≤ 2 years) |

| Limited Public Acceptance And Evolving Regulation | -1.3% | National, with notable risk outside established co-living hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction Cost Pressures and Building Safety Requirements Compress Project Viability

Construction and funding pressures remain a real brake on the United Kingdom co-living market because high-density schemes entail significant upfront complexity. Most larger co-living buildings sit above the threshold where Gateway 2 approval from the Building Safety Regulator is required before construction starts, which adds time and uncertainty to delivery. The Building Safety Levy also starts on 1 October 2026, and the burden is heavier for communal-space-rich layouts because the cost is tied to gross internal area. That matters for co-living because more shared space is central to the product, yet it also raises the effective cost base per lettable unit. Developers and operators in the United Kingdom co-living market, therefore, need tighter feasibility discipline before projects can move from planning into active buildout.

Planning Inconsistency Creates an Uneven Development Environment

Planning remains one of the clearest barriers in the United Kingdom co-living market, as schemes are usually classified as sui generis and require case-by-case review. That makes delivery slower and less predictable in cities without clear local guidance. London is in a stronger position because it already provides planning guidance for large-scale purpose-built shared living, which gives developers a clearer path than many regional markets can currently offer[3]Greater London Authority, “Large-Scale Purpose-Built Shared Living London Plan Guidance,” Greater London Authority, london.gov.uk. Outside that environment, inconsistent policy can divert capital toward places where approval risk is easier to assess. This leaves the United Kingdom co-living market with uneven geographic growth, not because renter demand is absent, but because policy clarity still varies too widely by city.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Configuration: Studios Consolidate Leadership As Self-Contained Formats Broaden Occupier Appeal

Studio and entire-unit formats held 53.4% of the market in 2025, making them the leading configurations across the United Kingdom co-living market. This lead reflects a clear shift in renter preferences toward privacy inside the unit and shared amenities outside it. The strongest schemes now combine a self-contained sleeping and bathroom setup with managed communal areas that still preserve the social side of the product. That mix works especially well for professionals who would not accept older shared-room formats but still want flexible, service-led housing. London planning guidance also supports a more formal product standard for large-scale, purpose-built shared living, reinforcing the position of better-designed studio-led schemes.

Private room formats remain relevant in regional cities where some renters still accept shared elements in return for a lower monthly outlay. Shared rooms sit at the most price-sensitive end of the spectrum and remain the least scalable option for institutionally backed portfolios. In the United Kingdom co-living industry, this leaves studio-heavy assets better placed to compete with modern Build-to-Rent housing rather than only with traditional shared accommodation. The United Kingdom co-living market size for studio and entire-unit formats is projected to grow at a 15.76% CAGR through 2031, confirming that the strongest product is also the fastest-moving one. As resident stays lengthen and privacy becomes harder to trade away, studio-led schemes should remain the format that anchors the next stage of the United Kingdom co-living market.

By Business Model: Management Agreements Gain Ground As Capital Efficiency Matters More

Own-develop-operate held 47.1% of the market in 2025, demonstrating that the first wave of the United Kingdom co-living market was built by groups that controlled land, delivery, and operations. That model gave early operators tight control over brand standards and resident experience. It also required large capital commitments, longer hold periods, and direct exposure to planning and construction risk. Those features suited early movers, but they are less attractive as the sector attracts a broader set of institutional owners. As a result, the United Kingdom co-living market is now shifting toward structures that allow operating platforms to grow without taking on full asset ownership.

Management agreements are forecast to rise at a 16.10% CAGR through 2031, making them the fastest-growing model in this category. Under that structure, the operator provides branding, leasing systems, pricing tools, and resident management to a third-party owner for a fee-based return. This reduces equity requirements and makes expansion more feasible when debt and build costs remain difficult to underwrite. Master lease and lease arbitrage models still occupy a middle ground because they allow operators to leverage local demand knowledge without funding full development. In the United Kingdom co-living industry, the longer-term winners are likely to be platforms that combine operational discipline with pricing transparency, because scale alone will not protect weaker business models in a more crowded field.

By Price Band: Premium And Luxury Lead Demand as Value Shifts Beyond Rent Alone

Premium and luxury co-living accounted for 40.8% of the market in 2025, giving this tier the largest share of the United Kingdom co-living market. The lead comes from a simple value equation, because renters in major cities often compare all-inclusive co-living costs with higher or similar total spending in conventional renting. That comparison is strongest when a co-living scheme offers private units, modern design, coworking space, and strong service standards in central locations. Premium formats also benefit from the fact that residents who pay for convenience often place real value on time saved, simplified billing, and predictable living standards. This gives higher-tier operators a broader appeal than a narrow luxury label might suggest.

The United Kingdom co-living market for premium and luxury formats is projected to expand at a 16.31% CAGR through 2031, making it the fastest-growing price band. Mid-scale products reach a wider renter pool, but they face more direct competition from multifamily projects that now include shared amenities as standard. Economy-tier co-living remains constrained because room size expectations and communal space needs are difficult to reconcile with very low rents. That leaves a visible gap between strong premium demand and the limited delivery of truly low-cost co-living supply. Over time, the United Kingdom co-living market may reward operators that can bridge that gap with disciplined mid-scale models that still meet planning and design standards.

By End User: Working Professionals Shape the Core Demand Base

Working professionals accounted for 58.9% of end-user demand in 2025, making them the dominant resident group in the United Kingdom co-living market. Their lead reflects the sector’s repositioning toward residents who want flexibility, privacy, and managed service in city locations close to work and transport. This audience is also more responsive to all-inclusive pricing because it reduces friction around deposits, furnishing, utilities, and setup time. Corporate relocation channels and graduate hiring flows strengthen that demand in larger urban centers where employers need fast housing solutions for new staff. These patterns indicate that the United Kingdom co-living market is now being shaped more by professional mobility than by short-term transitional living.

Working professionals are also forecast to expand at a 15.44% CAGR through 2031, keeping the same user group at the forefront of both share and growth. Students still matter in mixed-occupancy buildings, especially in cities with strong university demand and year-round leasing needs. A balanced resident mix can improve asset utilization by broadening the pool of potential occupants across different seasons. Even so, operators need to maintain a clear distinction between co-living and Purpose-Built Student Accommodation, as tenancy structures, planning treatments, and investor positioning differ. The United Kingdom co-living market share held by working professionals in 2025 shows that the sector’s future is now most closely tied to the needs of urban employees rather than a student-led model.

Geography Analysis

England accounted for 40.1% of the market in 2025, which made it the largest geography in the United Kingdom co-living market. London remains the operational center because it holds the deepest supply base, the strongest rent support, and the clearest planning route for large-scale shared living. That clarity matters because co-living schemes are easier to fund and deliver when design expectations and review standards are clear in advance. The United Kingdom co-living market share, concentrated in England, also reflects the role of London-led regeneration areas, where co-living is increasingly treated as part of wider mixed-use urban development rather than as a side format.

Scotland is projected to grow at a 17% CAGR through 2031, making it the fastest-growing geography in the United Kingdom co-living market. Glasgow leads that momentum because policy support and investor attention are moving in the same direction. The city is attracting a stronger pipeline of proposals, while its planning stance provides developers with a clearer path than some competing cities currently offer. Edinburgh remains slower because the absence of equally clear guidance makes capital deployment harder to underwrite at this stage.

Wales forms the next emerging tier, with Cardiff showing the strongest visibility among markets outside the main English and Scottish hubs. The pipeline there shows that co-living can also unlock stalled or repurposed urban sites when other living formats lose momentum. Northern Ireland remains at an earlier stage because the city scale is smaller and the institutional operator presence is still limited. Even so, the United Kingdom co-living market has room to expand geographically if policy clarity improves and large operators continue to look beyond the London-centered core.

Competitive Landscape

The United Kingdom co-living market is moderately concentrated, with a relatively small group of established and institutionally backed operators controlling much of the large-scale bed base. At the same time, a longer list of regional and asset-light players competes through local site knowledge, pricing discipline, and community programming. This means competition is not defined solely by scale, because execution quality can still shape leasing performance and renewal stability. Technology is becoming more important as operators use resident apps, pricing systems, and building management tools to improve occupancy and service consistency. In the United Kingdom co-living market, operational credibility is also becoming a competitive edge because planning, delivery, and resident management now need to work more closely together than before.

One of the clearest strategic moves came in March 2026, when Greystar acquired Native Communities and merged Native’s third-party management operations into its existing United Kingdom platform. That move widened Greystar’s reach in co-living management and strengthened its position across adjacent living formats. It also showed how larger residential operators can use acquisitions to add operating capacity rather than build it slowly from scratch. In a market where management agreements are growing faster than full ownership models, that kind of move can quickly reshape competitive depth.

Another visible move came from Bridges Fund Management and HUB, which advanced the City of London’s first co-living development at 45 Beech Street in January 2026 with a USD 101.5 million development facility and practical completion targeted for 2028. That example matters because it links capital, progress on planning, and a high-profile location in a single scheme. The market is also seeing operators reassess where they take direct asset exposure and where they focus on platform and distribution strengths, which supports further consolidation around the most durable business models. Overall, the United Kingdom co-living market is entering a stage where strong execution, not just early entry, will determine which platforms keep gaining ground.

United Kingdom Co-Living Industry Leaders

The Collective

Mason & Fifth

Node Living

Vonder

Folk Co-Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Greystar acquired Native Communities from Ares Real Estate funds, merging Native's third-party property management operations with Greystar's existing United Kingdom platform managing approximately 44,000 Purpose-Built Student Accommodation and Build-to-Rent homes, substantially expanding its co-living management reach across England.

- February 2026: Olympian Homes cleared Gateway 2 Building Safety Regulator approval for its 46-storey Vivus Living co-living tower at 56 Marsh Wall, Canary Wharf, marking an important step for delivery of a large-format London scheme.

- January 2026: Bridges Fund Management and HUB advanced the City of London's first co-living development, Cornerstone at 45 Beech Street, with JJ Rhatigan appointed as main contractor and a USD 101.5 million development facility provided by Firma Partners. Practical completion is scheduled for 2028.

United Kingdom Co-Living Market Report Scope

| Studio / Entire Unit |

| Private Room |

| Shared Room |

| Asset-Light, Master Lease / Lease Arbitrage |

| Asset-Light, Management Agreement |

| Asset-Heavy, Own-Develop-Operate |

| Economy |

| Mid-Scale |

| Premium/Luxury |

| Students |

| Working Professionals |

| England | London |

| Rest of England | |

| Scotland | |

| Wales | |

| Northern Ireland |

| By Property Configuration | Studio / Entire Unit | |

| Private Room | ||

| Shared Room | ||

| By Business Model | Asset-Light, Master Lease / Lease Arbitrage | |

| Asset-Light, Management Agreement | ||

| Asset-Heavy, Own-Develop-Operate | ||

| By Price Band | Economy | |

| Mid-Scale | ||

| Premium/Luxury | ||

| By End User | Students | |

| Working Professionals | ||

| By Country | England | London |

| Rest of England | ||

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the 2031 outlook for co-living in the United Kingdom?

The United Kingdom co-living market is forecast to reach USD 660 million by 2031, rising from USD 335.4 million in 2026 at a 14.5% CAGR.

Which resident group drives the strongest demand?

Working professionals lead demand with a 58.9% share in 2025 and are also the fastest-growing end-user segment, with a 15.44% CAGR through 2031.

Which property format is gaining the most traction?

Studio and entire-unit formats led with a 53.4% share in 2025 and are projected to grow at a 15.76% CAGR, reflecting stronger demand for privacy in managed communal buildings.

Why does London remain central to this space?

London has the deepest operating base, strong rent support, and a clearer planning route for purpose-built shared living.

What is the main risk to new project delivery?

Planning complexity, Gateway 2 approval requirements, and the Building Safety Levy are increasing time and cost pressures on new developments.

Which geography is growing the fastest after England’s lead?

Scotland is the fastest-growing geography, with a projected 17% CAGR through 2031, driven by stronger policy support in Glasgow and rising investor interest.

Page last updated on: