Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

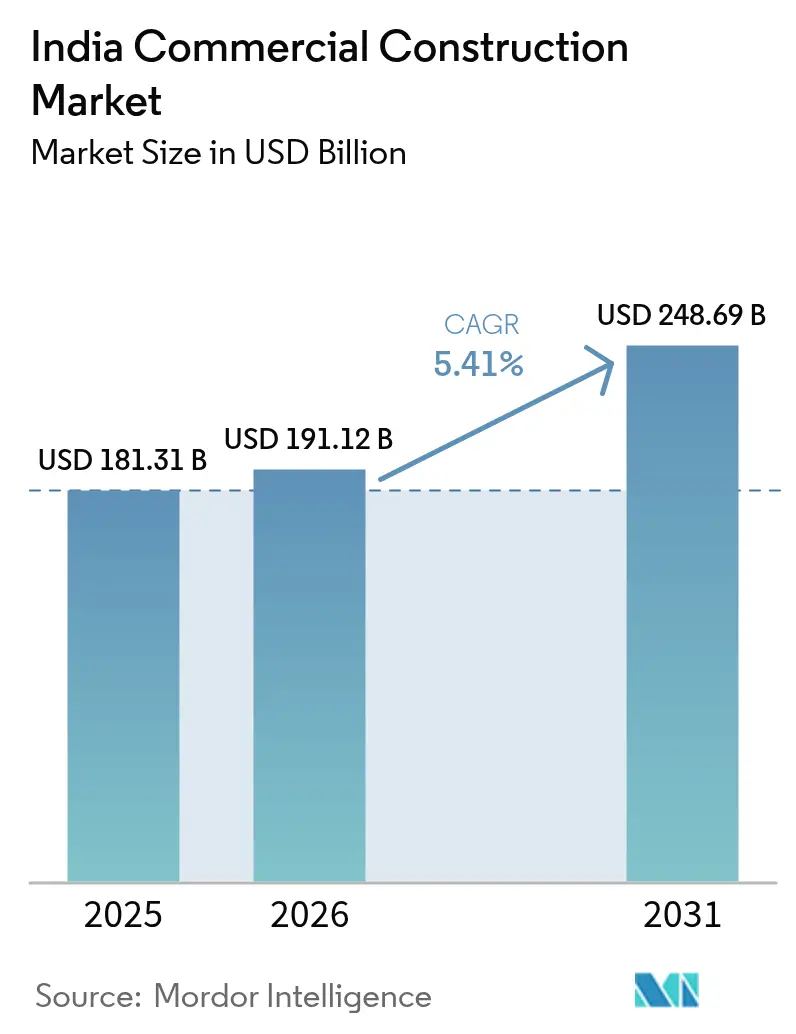

| Base Year Market Size (2025) | USD 181.31 Billion |

| Market Size (2026) | USD 191.12 Billion |

| Market Size (2031) | USD 248.69 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

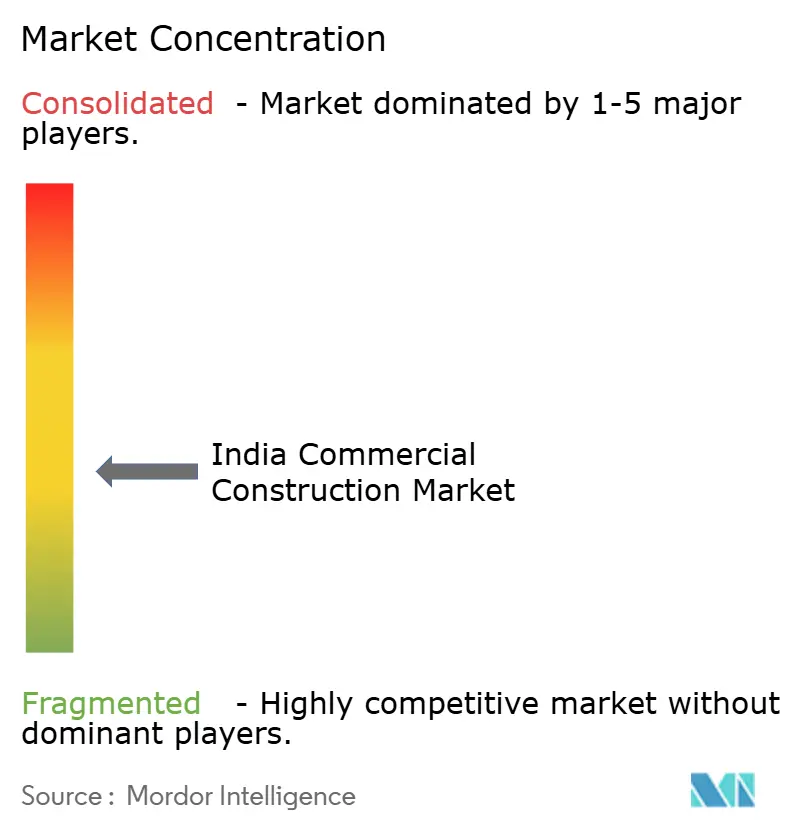

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Commercial Construction Market Analysis by Mordor Intelligence

India Commercial Construction market size in 2026 is estimated at USD 191.12 billion, growing from 2025 value of USD 181.31 billion with 2031 projections showing USD 248.69 billion, growing at 5.41% CAGR over 2026-2031. Ongoing government capital outlays of USD 135.1 billion in FY 2025–26, paired with the Smart Cities Mission’s USD 18.1 billion project pipeline, continue to lift core demand. Liquidity from REITs, surging data-center developments, and sustained private capital inflows sustain project momentum despite near-term cost inflation. Developers refine supply chains and adopt digital site-management tools to counter rising material costs while meeting tighter sustainability mandates. Across regions, the India commercial construction market reflects a pivot toward South India’s technology corridors even as West India retains scale advantages through deep capital pools and dense corporate occupancies.

Key Report Takeaways

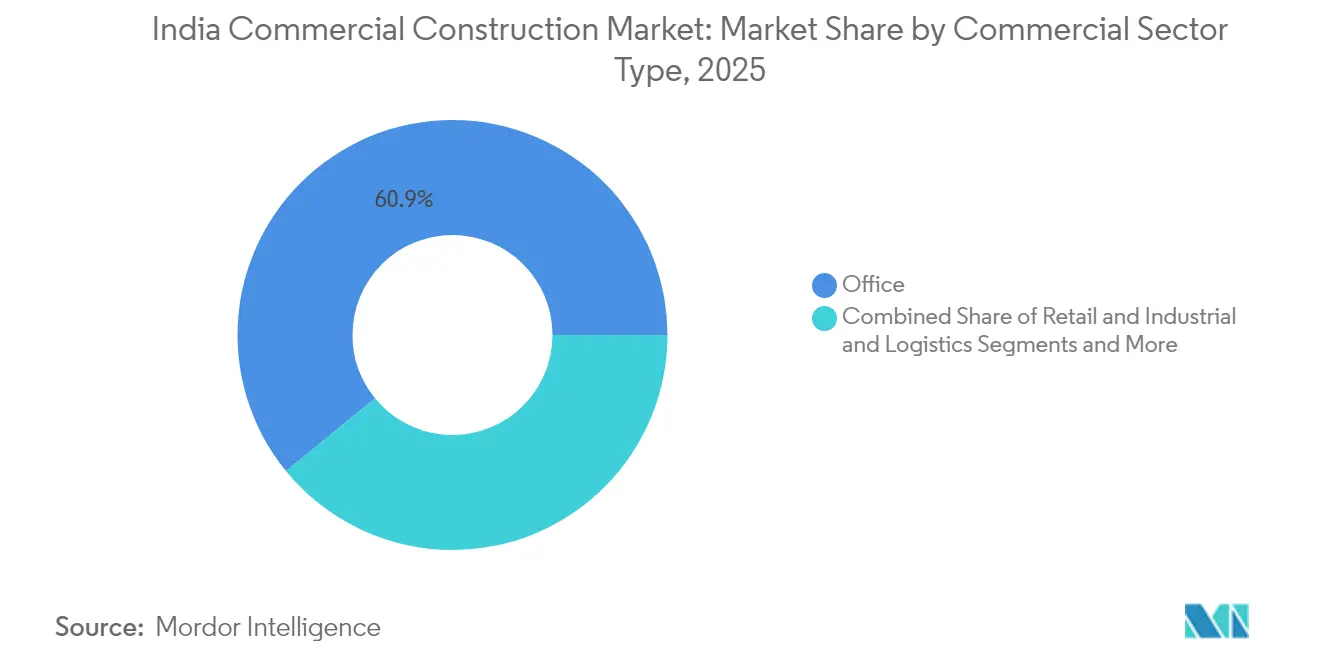

- By commercial sector type, Office led with 60.90% revenue share in 2025; Industrial & Logistics is projected to expand at a 6.84% CAGR through 2031.

- By construction type, new builds accounted for 73.65% of the India commercial construction market size in 2025, while renovation activities are advancing at a 6.93% CAGR to 2031.

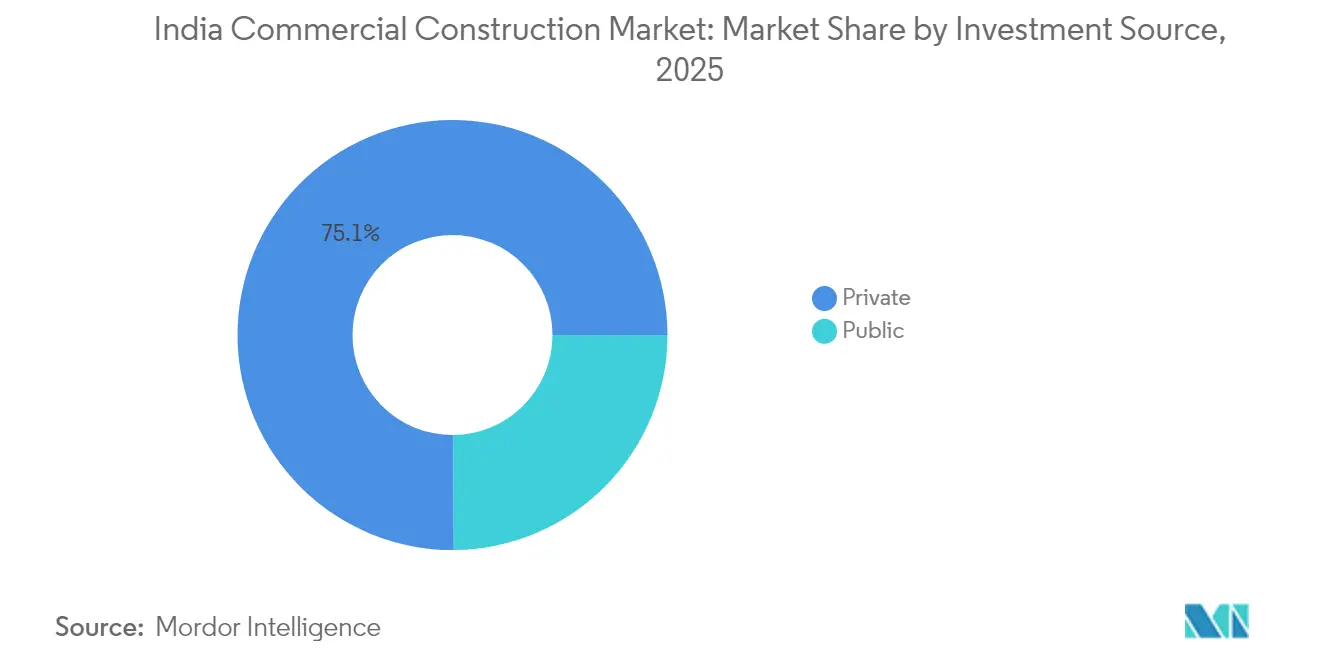

- By investment source, private capital held 75.10% of the India commercial construction market share in 2025; public funding registers the fastest 7.05% CAGR to 2031.

- By region, West India secured 39.20% revenue share in 2025, whereas South India is forecast to rise at a 7.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Commercial Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-Cities & infra push | 1.5% | National, with early gains in Tier-1 cities | Medium term (2-4 years) |

| REIT-led liquidity injection | 1.2% | Mumbai, Bengaluru, Hyderabad, Delhi-NCR | Short term (≤ 2 years) |

| Data-centre build-outs | 0.9% | Mumbai, Chennai, Hyderabad, Gujarat | Short term (≤ 2 years) |

| Flex-space culture | 0.8% | Metro cities, expanding to Tier-2 | Medium term (2-4 years) |

| Net-zero retrofit wave | 0.7% | Global, concentrated in Grade A office stock | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart-Cities & Infrastructure Push

More than 7,500 smart-city projects worth USD 18.1 billion have reached completion, and early successes in Agra and Pune demonstrate replicable models for mixed-use districts. Integrated command centers drive specialty demand for data-rich operations buildings, while transit upgrades spur commercial clusters along new corridors. Land-aggregation hurdles in smaller municipalities still delay timelines, prompting state governments to refine acquisition policies. Public-private partnerships proliferate as municipalities bundle road, utility, and commercial precincts into single concessions. Over the medium term, these initiatives provide a consistent demand floor for the India commercial construction market.

REIT-Led Liquidity Injection

Four active REITs now steward USD 1.72 billion in cumulative distributions and have unlocked a USD 7.47 billion gross asset base for reinvestment. The August 2025 listing of Knowledge Realty Trust raised USD 578 million, signaling maturing investor appetite for yield-oriented commercial portfolios. Roughly 60% of Grade-A office stock meets REIT eligibility, expanding the investable universe for pension and sovereign funds. Fresh equity enables faster ground-breaking for large campuses, especially in corridors with reliable fiber and power links. Wider acceptance of small-and medium-sized REIT structures is poised to funnel retail capital toward mid-tier projects in Tier 2 locations, widening the funding base across the India commercial construction market[1]Bureau of Energy Efficiency, “Star Rating Scheme for Commercial Buildings,” beeindia.gov.in.

Data-Center Build-Outs

National IT load is projected to swell from 0.9 GW in 2023 to nearly 2 GW by 2026, requiring USD 6.02 billion in fresh capital. Reliance’s planned hyperscale campus in Gujarat exemplifies the shift toward multi-tier, liquid-immersion-cooled halls designed for AI workloads. Construction cost per MW has escalated to USD 8–9 million, intensifying focus on value engineering and prefabricated electrical skids. International EPC majors such as CIMIC’s Leighton Asia partner with local specialists to blend global uptime standards with regional permitting fluency. The resulting pipeline continues to enlarge the India commercial construction market, especially in power-rich districts with fiber backbones.

Flex-Space Culture

Gross co-working stock is forecast to more than double to 126 million square feet by 2028 as enterprises hardwire hybrid work policies. Embassy Group’s USD 84.3 million acquisition of WeWork India and its planned IPO validate the asset-light, service-rich operating model. Flexible demand profiles favor modular floorplates, pre-engineered walls, and IoT-driven space-management systems. Older central business district buildings retrofit acoustic pods and wellness zones to stay relevant. Consequently, developers embed move-in-ready suites into new towers, thereby chaining construction timelines to ever-shorter leasing cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-cost inflation | -0.6% | National, acute in metro cities | Short term (≤ 2 years) |

| Regulatory approval delays | -0.4% | State-specific, severe in North & West | Medium term (2-4 years) |

| Grid-capacity bottlenecks (Tier-2) | -0.3% | Tier-2 cities, particularly in North & Central India | Medium term (2-4 years) |

| Flight-to-quality vacancy risk | -0.2% | Metro office markets, concentrated in Hyderabad & Bengaluru | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Construction-Cost Inflation

Average build costs touched USD 33.4 per square foot in 2025 after a 39% four-year climb. Labor alone rose 25% in the past 12 months as migration to urban centers slowed. Volatile steel and cement pricing squeeze smaller developers that lack hedging facilities. Contractors respond by substituting locally quarried aggregates, adopting automated rebar-bending stations, and scheduling pours during off-peak power-tariff windows. Nonetheless, if wage pressures persist into 2026, marginal projects could slip beneath hurdle rates, trimming the headline growth of the India commercial construction market.

Regulatory Approval Delays

While digitized land records and single-window dashboards improve transparency, multistage clearances for environment, heritage, and utilities still stretch beyond 12 months in several states. Delays can erode internal rates of return by up to 200 basis points, prompting developers to preload legal diligence and employ parallel-track design reviews. The central government’s arbitration-settlement scheme aims to unlock stuck payments on public projects, though adoption differs among agencies. Prolonged timelines remain a material risk that tempers near-term expansion across parts of the India commercial construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commercial Sector Type: Office Dominance Amid Industrial Upswing

The Office segment captured 60.90% of 2025 revenue, illustrating the primacy of global capability centers in metros like Bengaluru and Mumbai. Workspace densification, wellness-oriented designs, and pre-certified green cores now define premium absorption patterns. The India commercial construction market size for Office assets is set to advance at a steady clip as multinationals renew long-term commitments and domestic tech firms upscale headquarters footprints. Rising preference for touch-down areas and meeting-rich layouts underpins fit-out flexibility, while landlords deploy smart sensors to track utilization and cut operating expenses.

Industrial & Logistics, energized by e-commerce and production-linked incentives, exhibits the strongest 6.84% CAGR outlook. Grade-A warehouses integrate solar rooftops, high-bay automation, and cold-chain nodes near consumption centers. Developers parcel last-mile hubs into multi-story structures that optimize expensive urban land. The India commercial construction market harmonizes industrial sheds, cross-dock facilities, and collaborative office pods within single parks to shrink tenant commute times and slash emissions. As supply chains regionalize, land acquisition along the Delhi-Mumbai Freight Corridor and Chennai-Bengaluru belt intensifies, further tilting the growth axis toward integrated industrial townships.

By Construction Type: New-Build Leadership with Retrofit Acceleration

New construction contributed 73.65% of 2025 turnover, buoyed by greenfield corridors and airport-anchored business districts. Mega-campuses allocate plugs for solar façades, daylight-harvesting skylights, and micro-grid readiness from blueprint stages. Contractors standardize precast cores and aluminum formwork to compress schedules. Capital expenditure across South India’s tech hubs keeps the India commercial construction market weighted toward fresh builds through mid-decade.

Retrofit demand, however, now rises at a 6.93% CAGR as asset owners race to align with 2030 carbon-neutral pledges. The India commercial construction market size associated with retrofits widens each time marquee towers secure LEED Platinum or GRIHA 5-Star badges. Portfolio landlords deploy digital twins to map energy leaks before prescribing envelope upgrades, high-efficiency chillers, and demand-responsive lighting. Payback periods shorten as power tariffs escalate, making deep-retrofit economics more attractive than tear-down-and-rebuild in premium micro-markets.

By Investment Source: Private Capital Pre-eminence with Public Momentum

Private investors supplied 75.10% of 2025 outlays, guided by proven strata-sale models and predictable REIT exits. Global pension funds co-develop with local giants, insuring against policy shifts while harvesting yield spreads over developed-market bonds. The India commercial construction industry records recurring club deals clustering around special economic zones and transportation overlays.

Public spending, climbing at a 7.05% CAGR, now concentrates on transit-oriented commercial precincts and digital infrastructure hubs. Maharashtra’s Maha InvIT pioneers a blended finance template that packages toll roads and adjacent retail plazas, attracting multi-tranche private commitments. States extend viability-gap grants and land-lease concessions to catalyze mixed-use anchors along highway spines. This shared-risk approach enlarges the investable canvas and mitigates cyclical volatility for the India commercial construction market.

Geography Analysis

West India retained a 39.20% share in 2025 on the strength of Mumbai’s financial ecosystem and Gujarat’s manufacturing estates. Mindspace REIT’s 90.6% committed occupancy anchors investor confidence while USD 7.47 billion in gross assets circulates back into expansion projects. Land scarcity inside Mumbai’s core nudges developers toward Navi Mumbai and Thane, where metro extensions unlock lower-cost parcels. Gujarat’s special investment regions attract battery, semiconductor, and data-center projects, reinforcing the India commercial construction market’s western tilt.

South India, projected to post a 7.48% CAGR, leverages Bengaluru’s deep tech talent and Hyderabad’s policy agility. Hyderabad has 28.7 million square feet under construction, yet vacancy could reach 24% if absorption lags. Chennai’s port-led economy underpins logistics parks that blend container yards with cross-dock pavilions. Tamil Nadu’s 2024 Space Industrial Policy earmarks land banks for aerospace clusters, inviting niche suppliers and doubling commercial demand in peri-urban belts. Power-grid upgrades and renewable corridors are pivotal to sustaining South India’s surge within the India commercial construction market.

North and East India trail in absolute value yet showcase outsized government pipeline potential. The Noida International Airport project, 80% complete on a USD 3.46 billion capex, spurs hospitality and office frontages along the Yamuna Expressway. East India aligns its port-modernization drive with inland logistics hubs, fostering integrated warehousing near Kolkata and Paradip. Central India benefits from mining-linked industrial towns and concessional land parcels. Developers calibrate go-to-market strategies around state-level incentive matrices, cognizant that regulatory throughput and utility reliability vary widely across the India commercial construction market.

Competitive Landscape

Competition remains moderately fragmented as incumbents such as DLF, Prestige, and Lodha sustain multi-city brand equity and institutional funding access. Adani Group’s negotiations to buy Emaar India for USD 482–603 million illustrate a consolidatory impulse that can quickly reshape regional hierarchies. Market leaders differentiate via intelligent building-management platforms, zero-defect handover protocols, and end-to-end project management offices that compress cycle times.

Engineering-procurement-construction conglomerates like Larsen & Toubro reported double-digit revenue growth and USD 9.65 billion in fresh orders for Q2 FY 2025, underlining the advantage of integrated design-to-build capabilities. These giants pilot drone-enabled progress monitoring and 3D concrete printing to elevate productivity. Mid-tier specialists capture niche pockets in data-center fit-outs, façade engineering, and ESG retrofits, often partnering with global contractors to climb the complexity curve.

Regulatory oversight through RERA enhances consumer trust by mandating escrowed customer advances and time-bound delivery covenants. Compliance costs, though, skew in favor of capital-rich platforms, prompting smaller developers to pivot toward joint ventures or exit outright. Green building expertise, advanced modular construction, and pan-India land pipelines will continue to define competitive moats in the India commercial construction market through 2030.

India Commercial Construction Industry Leaders

DLF Ltd.

Prestige Group

Macrotech Developers (Lodha)

Embassy Group

Brigade Enterprises

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Knowledge Realty Trust raised USD 578 million (INR 4,800 crore) in India’s largest REIT IPO, covering 46.3 million square feet across Mumbai, Bengaluru, and Hyderabad.

- July 2025: Construction on the USD 3.46 billion Noida International Airport crossed 80% completion, positioning it as Asia’s largest greenfield aviation hub.

- April 2025: Embassy Group completed a USD 84.3 million (INR 700 crore) stake purchase in WeWork India and unveiled plans for a public float.

- January 2025: Adani Group began advanced talks to acquire Emaar India for USD 482–603 million (INR 4,000–5,000 crore) to reinforce its northern portfolio.

India Commercial Construction Market Report Scope

A complete background analysis of the India Commercial Construction market, which includes an assessment of the economy, market overview, market size estimation for key segments, and emerging trends in the market, market dynamics, and key company profiles are covered in the report.

By Commercial Sector Type

| Office |

| Retail |

| Industrial and Logistics |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Region

| North India |

| South India |

| West India |

| East India |

| Central India |

| By Commercial Sector Type | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Region | North India |

| South India | |

| West India | |

| East India | |

| Central India |

Key Questions Answered in the Report

What is the current value of the India commercial construction market?

The India commercial construction market size is USD 191.12 billion in 2026 and is forecast to reach USD 248.69 billion by 2031.

Which segment is expanding fastest within Indian commercial real estate?

Industrial & Logistics projects lead with a projected 6.84% CAGR through 2031, buoyed by e-commerce fulfillment and manufacturing relocation.

How large is the public spending pipeline that supports commercial building activity?

Government allocations of USD 135.1 billion for FY 2025-26 and state-level initiatives such as Maha InvIT sustain a multi-year pipeline of publicly aided projects.

Why are data centers so pivotal to future commercial construction demand?

National IT load is set to more than double by 2026, requiring over USD 6 billion in specialized construction that incorporates high-density cooling and resilient power.

What strategies help developers mitigate rising construction costs?

Firms increasingly rely on local material substitution, prefab concrete systems, and digital project-management tools to offset inflation and accelerate schedules.

Page last updated on: