Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

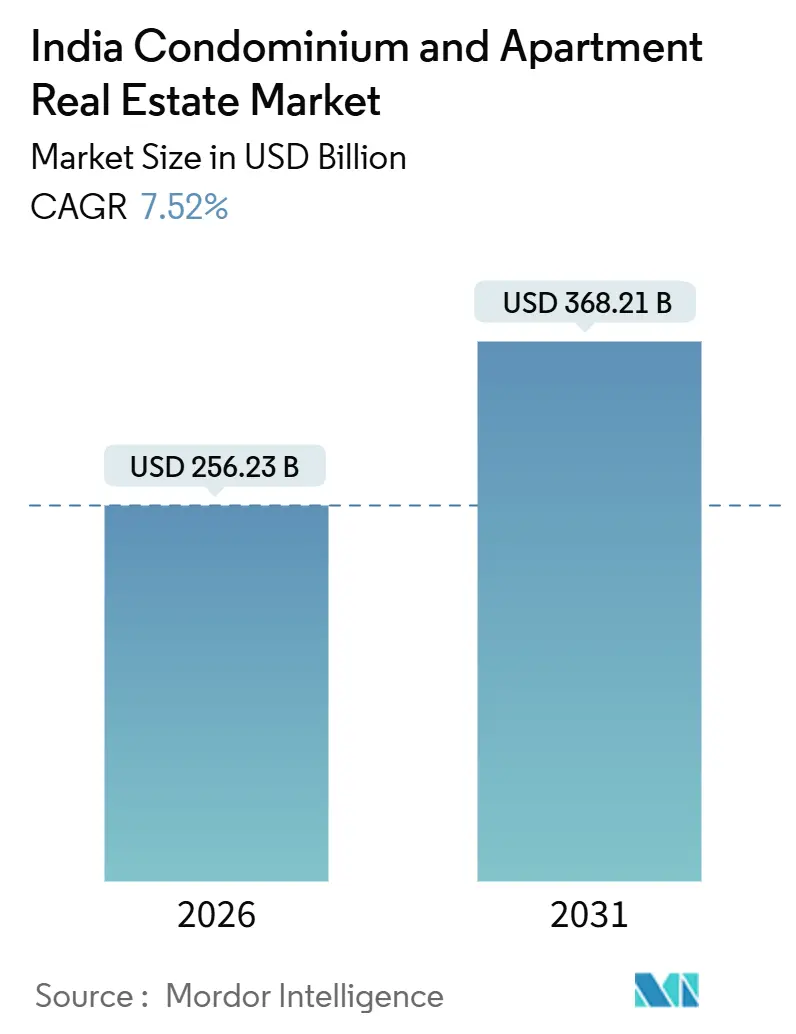

| Market Size (2026) | USD 256.23 Billion |

| Market Size (2031) | USD 368.21 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

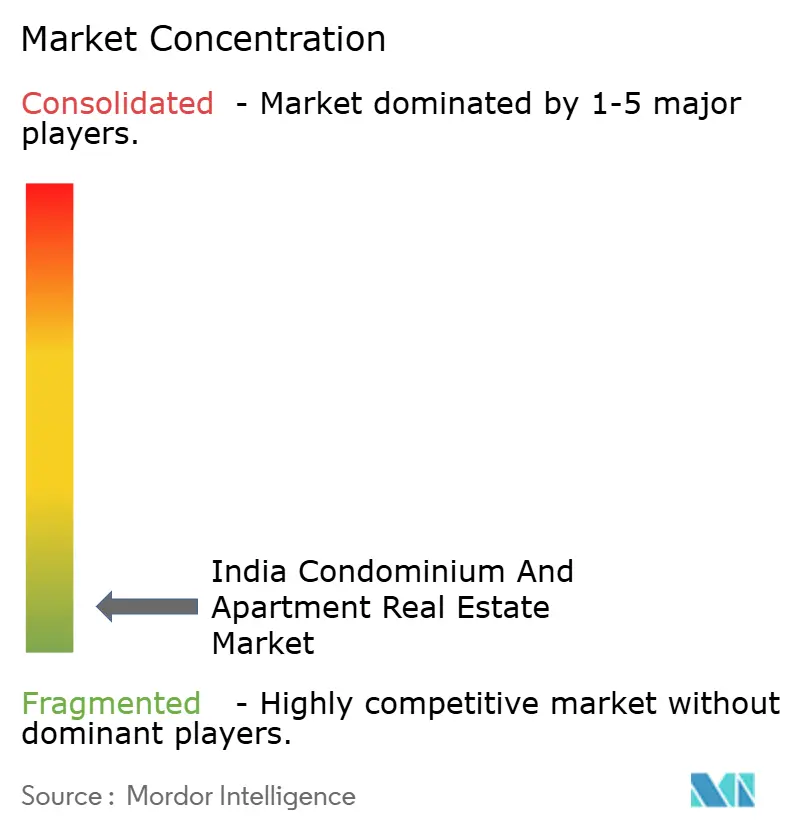

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Condominium And Apartment Real Estate Market Analysis by Mordor Intelligence

The India Condominium and Apartment Real Estate Market size is estimated at USD 256.23 billion in 2026, and is expected to reach USD 368.21 billion by 2031, at a CAGR of 7.52% during the forecast period (2026-2031). A decisive swing toward high-rise living, land scarcity across Tier 1 cores, and the preference for amenity-rich communities among dual-income households form the structural backdrop for this expansion. Consistent GDP growth near 6.5-7.2%, resilient formal job creation, and a supportive regulatory climate under RERA and GST have strengthened buyer confidence while enlarging the financing pipeline[1]International Monetary Fund, “India: 2025 Article IV Consultation,” IMF Country Report, imf.org . Transit corridors in Mumbai, Delhi, and Bengaluru are unlocking new supply pockets, and sustainable, smart-home features now serve as product differentiators for branded developers. At the same time, mortgage affordability strains and land-approval bottlenecks temper volume growth prospects.

Key Report Takeaways

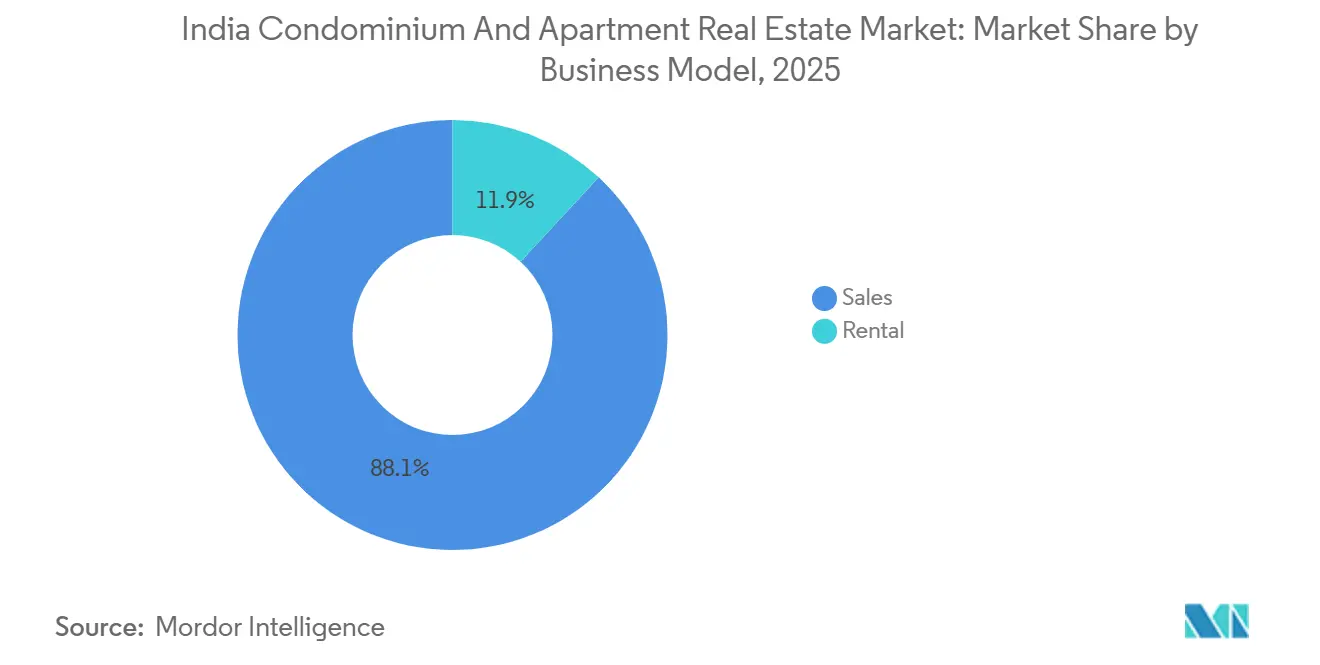

- By business model, the sales segment accounted for 88.1% of the India condominium and apartment real estate market share in 2025, while the rental segment posted the fastest 8.12% CAGR through 2031.

- By price band, the mid-market tier led with a 43.2% revenue share in 2025; the luxury tier is forecast to expand at an 8.67% CAGR to 2031.

- By mode of sale, primary launches held 58.8% of 2025 transactions, whereas secondary resales are advancing at an 8.42% CAGR through 2031.

- By city, the Mumbai Metropolitan Region contributed 32.4% of 2025 sales; Chennai is the fastest-growing metro with a 9.08% CAGR expected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Condominium And Apartment Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained GDP and formal job creation | +1.8% | Mumbai, Delhi NCR, Bengaluru, Hyderabad, Pune | Long term (≥ 4 years) |

| Rapid urbanization and shrinking households | +1.5% | Mumbai, Delhi NCR, Bengaluru | Medium term (2-4 years) |

| Transit corridors and mixed-use townships | +1.2% | Mumbai, Delhi NCR, Bengaluru, Chennai, Hyderabad | Medium term (2-4 years) |

| RERA and GST reforms | +1.0% | Maharashtra, Karnataka, Telangana | Short term (≤ 2 years) |

| NRI and affluent demand for green condos | +0.9% | Mumbai, Bengaluru, Pune, Goa, select NCR | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained GDP and Formal Job Creation Propelling Tier-1/2 Demand

Robust economic momentum sustains salaried employment in IT, finance, and manufacturing hubs, raising household purchasing power in key metros[2]Asian Development Bank, “Asian Development Outlook 2025,” adb.org . Although the Reserve Bank trimmed policy rates in 2025, retail home-loan costs hover near 7.25-8.75%, steering entry-level buyers toward peripheral micro-markets. Premium launches benefit as high-income cohorts absorb rising ticket sizes, lifting the premium segment’s share to 62% in January-September 2025. Demand strength translated into an 11-year high for sales across the top seven cities in H1 2024. The upshot is a stable end-user base supporting the India condominium and apartment real estate market even as financing costs fluctuate.

Rapid Urbanization and Shrinking Household Size Favor Vertical Living

Nuclear families now form half of India’s households, cutting average size to 4.44 members and amplifying appetite for compact, amenity-rich apartments. Mumbai registered 96,187 unit sales in 2024, the highest in 13 years, underscoring the vertical pivot where land scarcity is acute. Developers are responding with 1- and 2-bedroom configurations bundled with co-working areas, gyms, and rooftop gardens to replicate suburban comforts within city cores. Pune’s 1-bedroom share fell as buyers upgraded to 2-bedroom units amid rising incomes. These shifts underpin a steady absorption base for the India condominium and apartment real estate market.

Transit Corridors and Mixed-Use Townships Unlock Supply Pockets

Operational metro lines and rapid-rail corridors compress commute times, elevate land values in peripheral nodes, and enable higher floor-area ratios within 500 meters of stations[3]Mumbai Metro Rail Corporation, “Aqua Line Operational Update,” mmrcl.com . The 33.5 km Aqua Line in Mumbai catalyzed launches in Andheri East and Goregaon, while Delhi’s 82 km regional rapid rail, slated for 2025, stimulates Ghaziabad and Meerut demand. Bengaluru’s Phase 2 extensions have sparked township projects combining residential, retail, and office elements, such as Mahindra Lifespaces’ USD 120 million North Bengaluru site. Transit-oriented development regulations in Maharashtra, Karnataka, and Telangana permit higher density, unlocking parcels once considered unviable. Consequently, well-served corridors act as magnets for both developers and buyers.

Regulatory Reforms and Stronger Governance

Mandatory project registration, escrow norms, and time-bound delivery under RERA have materially reduced information asymmetry, with 138,000 projects and 95,987 agents registered by 2024. GST’s single-tax structure cut documentation friction, aiding faster deal closures. Improved transparency has drawn institutional funds, evidenced by Blackstone’s residential tie-ups with Prestige Estates in Bengaluru and Hyderabad. Compliance still extends project lead times to 18-24 months, but better governance offsets the delay by lowering perceived delivery risk. The cumulative effect lifts the credibility of the India condominium and apartment real estate market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mortgage affordability stress | -1.3% | Mumbai, Delhi NCR, Bengaluru | Short term (≤ 2 years) |

| Land acquisition and approval delays | -0.9% | Maharashtra, Karnataka, West Bengal | Medium term (2-4 years) |

| Construction cost inflation & contractor risk | -0.7% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Affordability Stress from Elevated Mortgage Rates

Retail borrowing costs remain near 7.25-8.75%, discouraging first-time buyers in prime sub-markets. Premium launches captured 62% of sales in early 2025, while the affordable tier fell to 18% of 2024 volumes, underscoring a bifurcated demand curve. Delhi NCR’s 29% sales decline during January-September 2025 illustrates the squeeze when prices surge faster than incomes. Government subsidies under PMAY-Urban 2.0 aim to revive low-ticket demand, but delayed state-level implementation limits near-term relief. Consequently, affordability headwinds cap the upside for the India condominium and apartment real estate market.

Land Acquisition and Approval Bottlenecks

Developers navigate fragmented land titles and multi-layered clearances that stretch launch timelines to 18-24 months versus 6-9 months in developed markets. Maharashtra and Karnataka offer single-window portals, yet inconsistency among other states inflates holding costs. Capital is tied up longer, raising project IRRs and favoring cash-rich branded players who can shoulder the waiting period. Smaller builders often exit via distressed asset sales, consolidating market power but reducing overall supply velocity. The delay tempers the growth trajectory of the India condominium and apartment real estate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales Dominance, Rental Momentum Building

Sales transactions controlled 88.1% of the 2025 value, underscoring India’s ownership bias and the tax benefits linked to mortgage interest deductions. Stable delivery records under RERA-compliant projects lifted consumer trust, enabling giants such as DLF to post USD 530 million in Q2 FY2025 sales from Privana South. Prestige and Lodha registered USD 667 million and USD 547 million, respectively, confirming depth in end-user demand. The rental arm of the India condominium and apartment real estate market, though smaller, is gaining traction at an 8.12% CAGR. Blackstone’s build-to-rent joint ventures aim to capture mobile professionals in Bengaluru and Hyderabad, while co-living platforms validate the appetite for managed inventory.

A growing millennial workforce with average job tenures of 3-4 years values flexibility over ownership, feeding institutional interest in rental yields of 2.5-4% across major metros. Only 9% of property management today is tech-enabled, signaling a sizeable runway for PropTech adoption. As build-to-rent portfolios scale, rental receipts could form a steady annuity stream, diversifying revenue sources for large developers and enlarging the India condominium and apartment real estate market.

By Price Band: Mid-Market Scale, Luxury Pace

The mid-market tier held a 43.2% share in 2025, led by projects such as Godrej’s USD 372 million Pune launch offering 2- and 3-bedroom units at USD 96,000-144,000. Brigade’s USD 156 million Insignia in Bengaluru similarly aligns with mid-income aspirations. Luxury, although smaller, clocks the fastest 8.67% CAGR, fueled by NRI remittances and ESG-driven preferences. India ranked third worldwide for LEED residential space, enabling developers to charge 15-20% premiums.

Affordable units below USD 54,000 now form only 18% of supply, a sharp drop from 40% in 2019, as high land costs erode viability absent subsidies. PMAY-Urban 2.0’s USD 26.4 billion funding pool may revive this bracket; execution speed will determine outcomes. In the interim, premium launches such as Oberoi’s USD 342 million Garden City reinforce upward price migration, shaping the revenue mix of the India condominium and apartment real estate market.

By Mode of Sale: Primary First, Secondary Liquidity Improving

Primary launches retained 58.8% of 2025 transactions, with Sobha’s Neopolis and Puravankara’s Weaves together adding USD 335 million in Q2 FY2025 sales. Buyers favor customization, newer amenities, and tax deductions available on under-construction mortgages. The secondary arena is growing at 8.42% CAGR as RERA-era projects completed between 2020-2024 gain clear titles, attracting risk-averse purchasers seeking immediate occupancy.

Mumbai’s Panvel resale micro-market posted 12% price growth in 2024 on the back of new metro connectivity, showing how transit augments secondary liquidity. Blockchain-based title checks and virtual tours halve closing times to 30-45 days, encouraging investor participation. Over time, a balanced primary-secondary mix will deepen the India condominium and apartment real estate market.

Geography Analysis

Mumbai Metropolitan Region supplied 32.4% of 2025 sales and is projected to compound at 7.52% through 2031. The Aqua Line, operational since October 2024, cut travel to Bandra-Kurla Complex and lifted prices in Goregaon and Malad corridors. Hiranandani’s 1,700-unit Arena and Oberoi’s USD 342 million Garden City anchor this momentum, yet average tickets above USD 180,000 shift mid-income demand to Thane and Navi Mumbai.

Delhi NCR, Bengaluru, and Pune form the next demand tier. Delhi NCR saw a 29% sales slide in early 2025 as prices surged 32% in 2024, with Dwarka Expressway witnessing 63% resale appreciation tied to the rapid-rail rollout. Bengaluru experienced 12% annual price gains in 2024, supported by IT hiring and Metro Phase 2, prompting Mahindra Lifespaces’ USD 120 million land purchase in North Bengaluru for mid-market stock. Pune’s volumes dipped 5% in 2024 amid an 11% price uptick, but Godrej’s USD 372 million launch in Hinjewadi anchors future absorption.

Chennai is the fastest-growing metro with a 9.08% CAGR projected to 2031, aided by lower ticket sizes and industrial-corridor projects. Hyderabad, Kolkata, and Tier 2 circuits such as Ahmedabad, Jaipur, and Kochi round out the landscape. Hyderabad’s premiumisation lifted USD 120,000-plus units to a 14% share in 2024. Kolkata logged 16% price growth in 2024, reflecting metro extensions and logistics investments. Collectively, geographic diversification buoys the India condominium and apartment real estate market even as individual city cycles diverge.

Competitive Landscape

The market remains fragmented, with even the largest developers capturing only a limited share of organized sales, allowing regional specialists to coexist alongside national giants. DLF, Prestige, Lodha, Godrej, and Oberoi dominate premium markets by leveraging brand equity and access to institutional funds. Each has rolled out large-format, IGBC-compliant projects with staggered payment plans to widen the buyer funnel. Brigade, Sobha, and Puravankara focus on mid-market buyers in IT hubs, relying on repeat brand trust and efficient project delivery to win market share.

Institutional capital is making strategic inroads. Blackstone’s build-to-rent venture with Prestige marks a pivotal step toward income-yield models. Technology adoption differentiates players; Tata Housing and Mahindra Lifespaces pilot prefabrication to cut timelines, while PropTech alliances streamline sales, leasing, and after-sales processes. Developers emphasizing green credentials, such as LEED or IGBC certifications, command premiums and attract ESG-oriented funds.

Land aggregation and regulatory navigation remain core competencies. Branded firms with stronger balance sheets absorb long approval cycles and volatile input costs better than smaller rivals. Rising consolidation through distressed asset takeovers by national developers is likely, potentially lifting the combined top-five share and gradually altering the competitive structure of the India condominium and apartment real estate market.

India Condominium And Apartment Real Estate Industry Leaders

DLF Ltd

Prestige Estates Projects Ltd

Godrej Properties Ltd

Lodha (Macrotech Developers)

Oberoi Realty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: DLF launched Privana South, a USD 840 million luxury project in Gurugram featuring IoT controls and solar roofs.

- September 2024: Prestige Estates reported USD 667 million presales for Q2 FY2025, buoyed by its 119-acre Prestige City in Hyderabad.

- August 2024: Lodha posted USD 547 million presales driven by Azur in Bengaluru and Amara in Thane.

- July 2024: Godrej Properties rolled out a USD 372 million Pune project, netting USD 414 million bookings in Q2 FY2025.

India Condominium And Apartment Real Estate Market Report Scope

Condos are very similar to apartments, although they are owned differently. The landlord is the particular condo owner. Either personally or with the aid of a property management company, the condo is managed. The report covers the complete background analysis of the India Condominium and Apartments Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact.

The India Condominium and Apartments Market are segmented By key cities (Mumbai, Pune, Delhi/NCR, Bengaluru, Hyderabad and the Rest of India). The report offers market size and forecasts in value (USD billion) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

What is the current value of the India Condominium and Apartment Real Estate Market?

What is the current value of the India Condominium and Apartment Real Estate Market?

Which business model dominates residential transactions in India?

Sales transactions lead with an 88.1% share in 2025, although rentals are growing at an 8.12% CAGR.

Why are metro corridors important for apartment demand?

Operational metro and rapid-rail lines shorten commutes, raise land values, and stimulate launches along the corridors, supporting both primary and resale demand.

How do RERA and GST benefit homebuyers?

RERA enforces project registration and escrow rules, while GST streamlines taxation, together enhancing transparency and reducing transaction friction.

Which city shows the fastest growth outlook?

Chennai is forecast to expand at a 9.08% CAGR to 2031 due to IT-sector hiring and infrastructure upgrades.

What drives the surge in luxury condominium demand?

Strong NRI remittances and a preference for smart, green-certified homes with concierge amenities are lifting luxury uptake at an 8.67% CAGR.

Page last updated on: