Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

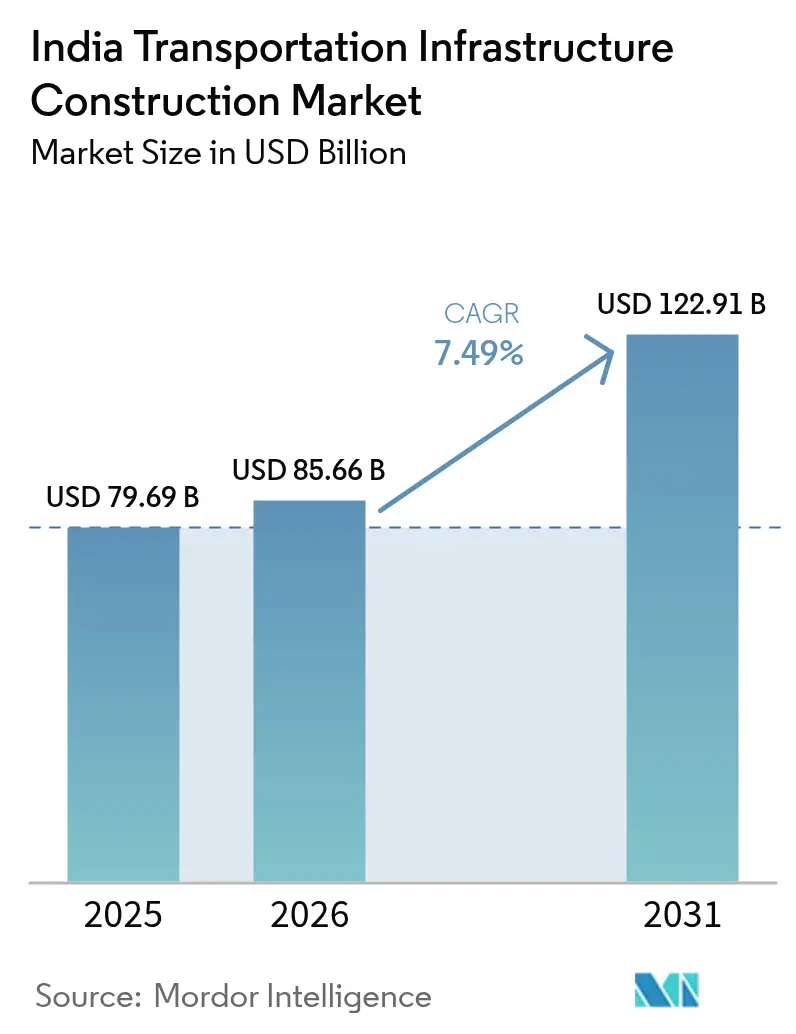

| Base Year Market Size (2025) | USD 79.69 Billion |

| Market Size (2026) | USD 85.66 Billion |

| Market Size (2031) | USD 122.91 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Transportation Infrastructure Construction Market Analysis by Mordor Intelligence

The India Transportation Infrastructure Construction Market size was valued at USD 79.69 billion in 2025 and is estimated to grow from USD 85.66 billion in 2026 to reach USD 122.91 billion by 2031, at a CAGR of 7.49% during the forecast period (2026-2031).

The jump is powered by record highway bidding under the Hybrid Annuity Model, near-completion of the 2,843-kilometer Dedicated Freight Corridor, and sustained airport terminal upgrades. Contractors are accelerating digital adoption because the Ministry of Road Transport and Highways now requires Building Information Modeling on every project worth more than USD 12 million, cutting design errors and shortening schedules. Ports are also drawing larger civil contracts as 574 Sagarmala projects move from planning to execution, and the greenfield Vadhavan Port clears its final approvals. At the same time, public agencies are experimenting with toll-operate-transfer bundles and rail station public-private partnerships to recycle capital, gradually widening the space for private financing.

Key Report Takeaways

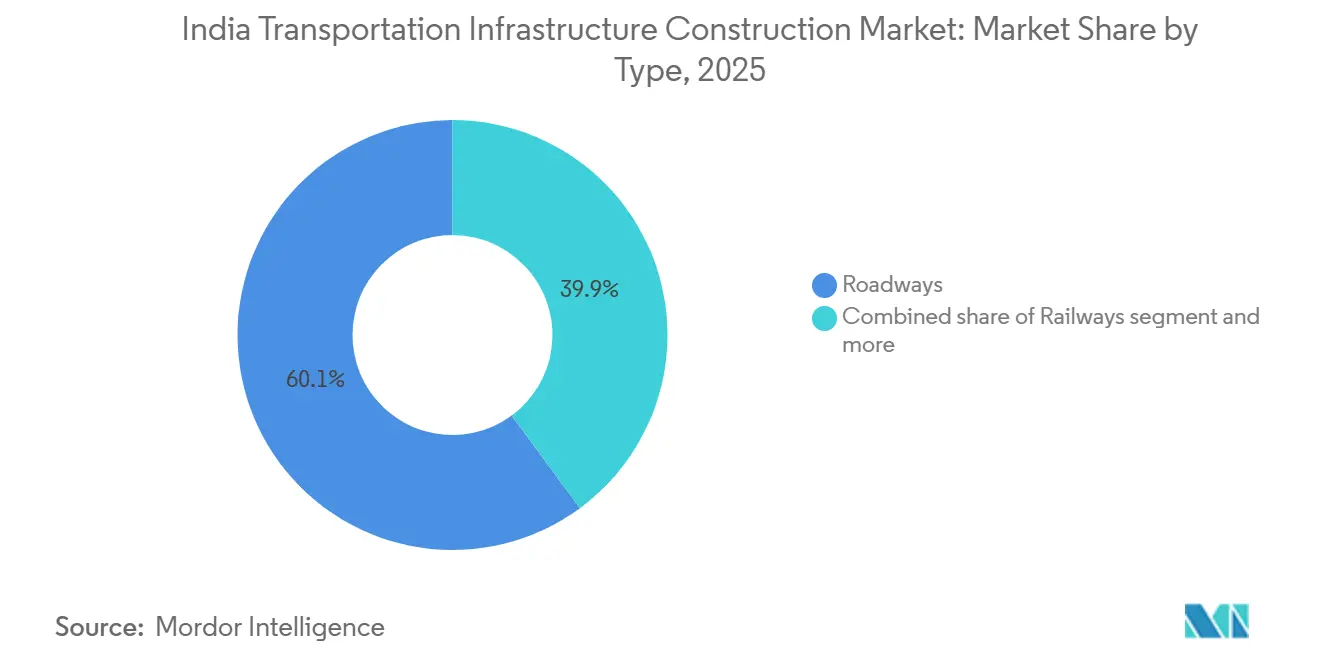

- By type, roadways led with 60.1% of the India transportation infrastructure construction market share in 2025, while ports and inland waterways posted the highest forecast growth at an 8.04% CAGR to 2031.

- By construction type, new builds accounted for 76.9% of the India transportation infrastructure construction market size in 2025; renovation is projected to advance at a 7.97% CAGR through 2031.

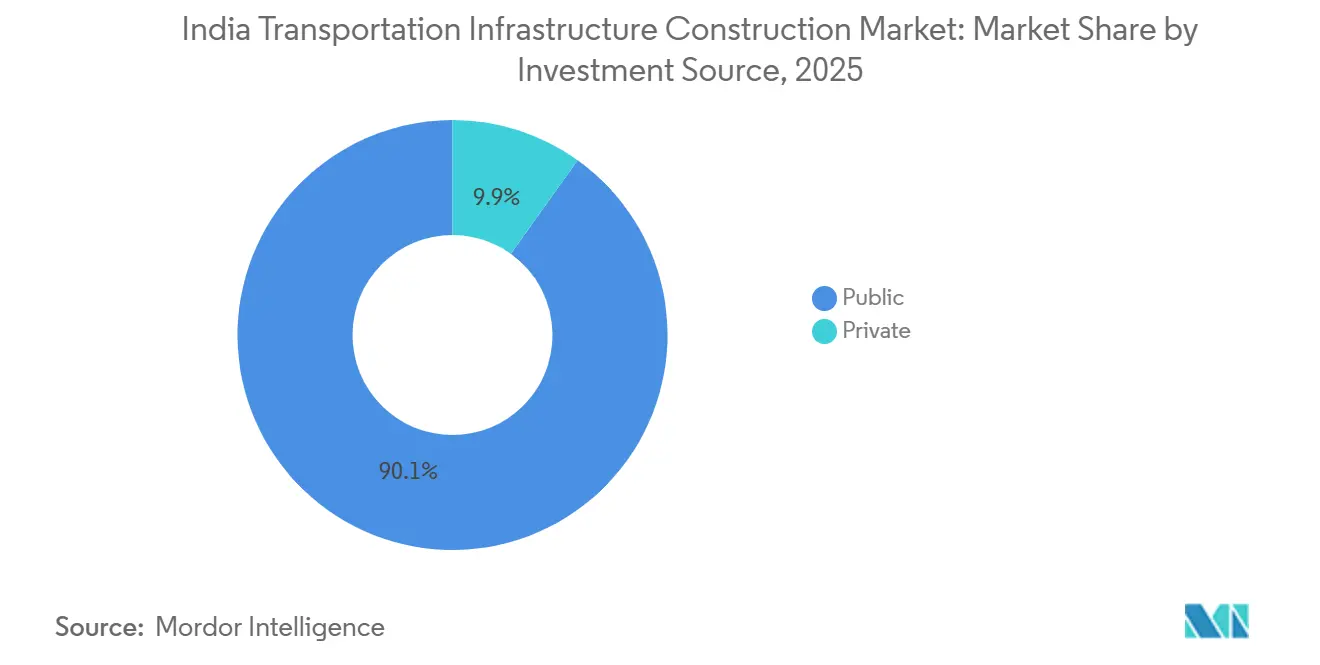

- By investment source, public spending formed 90.1% of 2025 outlays, yet private investment is on track for a 7.89% CAGR as more toll-operate-transfer and airport concession deals close.

- By city, the Mumbai Metropolitan Region held a 21.2% share of 2025 spending, whereas Hyderabad is forecast to record the fastest rise with an 8.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Transportation Infrastructure Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Freight rail upgrades and dedicated freight corridors | +1.8% | Nationwide, led by the Delhi–Mumbai and Howrah-Ludhiana routes | Medium term (2-4 years) |

| National highway and expressway expansion | +1.6% | All states, early traction in Uttar Pradesh and Maharashtra | Short term (≤2 years) |

| Metro network build-out in major cities | +1.4% | Delhi NCR, Mumbai, Bengaluru, Hyderabad, Chennai | Medium term (2-4 years) |

| Port connectivity and multimodal logistics corridors | +1.2% | Coastal states such as Gujarat and Tamil Nadu | Long term (≥4 years) |

| Airport modernization and capacity additions | +1.0% | Tier-1 and tier-2 airports, including Delhi and Guwahati | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Freight Rail Upgrades and Dedicated Freight Corridors

The Eastern and Western Dedicated Freight Corridors were 96.4% complete by December 2025 and pushed freight train trips up by 47% versus the prior year[1]Dedicated Freight Corridor Corporation of India, “Project Status December 2025,” dfccil.com . Indian Railways approved a fresh 1,100-kilometer Dankuni–Surat link in 2025 that needs USD 5.4 billion in civil works. Federal railway outlays for fiscal 2026-2027 stand at USD 33.4 billion, much of which targets high-speed track laying and station makeovers. Contractors like AFCONS Infrastructure and KEC International have secured multiyear electrification packages, locking revenue visibility. Faster double-stack operations now cut transit times by up to 40%, driving more shippers from road to rail.

National Highway and Expressway Expansion

The National Highways Authority of India opened bidding for 52 projects worth USD 13.8 billion for fiscal 2026 after clearing 124 schemes the previous year[2]National Highways Authority of India, “Project Bidding Data FY 2026,” nhai.gov.in . Hybrid Annuity Model awards make up roughly 65% of new mileage because they balance state budgets and private risk. HG Infra, Ceigall, and Dilip Buildcon grabbed large orders in 2024-2025, confirming a healthy contractor appetite. India’s highway length reached 146,572 kilometers by end-2025, up from 142,000 kilometers in 2024. Bharatmala Phase II pledges another 20,000 kilometers, concentrating on border and coastal corridors, and will cost USD 24 billion across five years.

Metro Network Build-Out in Major Cities

Chennai Metro Phase II covers 118.9 kilometers, carries a USD 7.59 billion budget, and moved into full construction in 2025. Delhi Metro Phase V secured approval the same year, while Bengaluru aims for 175 kilometers in service by 2027. Hyderabad Metro Phase II was awarded in September 2024 for USD 2.91 billion to a Larsen & Toubro–Megha Engineering joint venture. Public-private models for station redevelopment allow developers to monetize retail zones, trimming public capital needs and accelerating completion.

Port Connectivity and Multimodal Logistics Corridors

Sagarmala now covers 574 active schemes worth USD 72 billion[3]Ministry of Ports, Shipping & Waterways, “Sagarmala Dashboard,” shipmin.gov.in . The flagship Vadhavan Port demands USD 9.15 billion in civil works and targets 23.2 million tonnes per annum capacity. Chennai Port’s new rail link, opened in 2025 for USD 228 million, ties terminals straight to the freight corridor and cuts dwell time by 25%. Inland waterways get a lift from the Jal Marg Vikas project, which dredged 1,620 kilometers of the Ganga channel and built five multimodal hubs, enabling year-round 2,000-tonne barge operations.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land acquisition and right-of-way delays | -1.2% | Nationwide hot spots in Delhi NCR and Pune | Short term (≤2 years) |

| Funding constraints and delayed public payments | -0.9% | More acute for mid-tier contractors | Short term (≤2 years) |

| Commodity price volatility and supply shocks | -0.7% | Steel-intensive rail and metro packages | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land Acquisition and Right-of-Way Delays

Roughly 30% of highway jobs faced land handover slippages in 2024-2025, adding up to 18 months to build cycles. Pune Metro Phase II lost eight months when tunneling under dense neighborhoods. The 2013 Land Acquisition Act obliges social impact studies and consent clauses, hence bids now carry a 15-20% contingency for title issues. States are trialing land pooling, where owners swap raw land for serviced plots, but adoption is uneven.

Funding Constraints and Delayed Public Payments

The highways authority owed contractors USD 1.2 billion in pending bills by February 2025, and arbitration awards waiting for settlement totaled USD 17.2 billion in March 2024. Payment cycles on some metro projects have stretched to 120 days, pushing contractors toward short-term loans at 9-11% interest. A newly introduced escrow mechanism for annuity highways promises steadier cash flow, yet legacy projects still lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Freight Corridors Propel Rail Resurgence

Roadways commanded 60.1% of the 2025 value, anchored by steady Hybrid Annuity Model flow. Ports and inland waterways hold the fastest future trajectory with an 8.04% CAGR on the back of Sagarmala and Vadhavan builds, while rail wins momentum from dedicated freight links. The integration of double-stack container services on new corridors cuts door-to-door times by up to 40%, steering high-value cargo away from trucks. The India transportation infrastructure construction market size for seaports is expected to widen as Chennai and Paradip complete berth expansions, and the Jal Marg Vikas river channel stays navigable all year. Together, these shifts rebalance capital away from pure highways toward rail and port assets.

The India transportation infrastructure construction market is also witnessing strong airport upgrades. Airports Authority of India has lined up USD 1.8 billion for air traffic control and another USD 548 million for terminals, while Tata Projects races to finish Navi Mumbai International Airport by 2026. These works, though smaller in value than highways, bring complex systems packages that attract technology partners such as Siemens for baggage and passenger tracking. Contractors that mastered elevated viaducts for metros now leverage that expertise on airside taxiways, diversifying order books and smoothing revenue volatility.

By Construction Type: Station Upgrades Accelerate Renovation

New builds absorbed 76.9% of 2025 spending and remain the anchor of the India transportation infrastructure construction market. More than 50 highway packages worth USD 13.8 billion entered tender in December 2024, and new metro lines in Chennai, Delhi, and Hyderabad add over 200 kilometers of track through 2027. Contractors welcome these larger parcels because they bundle civil, systems, and utilities work into single contracts that improve scale.

Renovation, however, is moving faster at a forecast 7.97% CAGR. Indian Railways is refurbishing 1,309 stations under the Amrit Bharat program for USD 4.92 billion and has tapped private partners to monetize retail zones. Airport retrofits follow the same logic: Delhi Terminal 1 is being rebuilt for USD 288 million, and Bengaluru’s Terminal 2 upgrade will lift capacity to 50 million passengers a year by 2028. Prefabricated components now dominate concourse extensions, slicing project time by about 30% and capping passenger disruption.

By Investment Source: TOT Bundles Unlock Private Capital

Public funding supplied 90.1% of 2025 dollars, but private inflows are rising as the National Highways Authority of India auctions more toll-operate-transfer bundles. Bundle 11, sold in 2024 to IRB Infrastructure for USD 882 million, allowed the authority to plough proceeds into fresh builds. The India transportation infrastructure construction industry is also seeing Infrastructure Investment Trust structures that let builders drop mature assets and recycle equity. Station and airport concessions follow similar logic, transferring operational risk to developers in exchange for long leases.

Private capital will grow at a projected 7.89% CAGR through 2031. Adani’s addition of Thiruvananthapuram Airport under a long-term lease and GMR’s Bhogapuram greenfield project illustrate how large conglomerates now treat transport as a core vertical. Rising comfort with escrow-backed annuity highways and passenger-fee indexed airport concessions should pull global pension funds into asset recycling platforms, boosting liquidity for tier-1 contractors.

Geography Analysis

The Mumbai Metropolitan Region delivered 21.2% of 2025 spending because of overlapping metro, coastal road, and airport works. Hyderabad is set for the quickest advance with an 8.11% CAGR thanks to its ring roads and Phase II metro, while Delhi NCR stays a strong second on the back of metro Phase V, the Delhi-Meerut rapid rail, and the Noida airport. Pune continues its dual metro phases and a USD 1.92 billion ring road, whereas Bengaluru presses ahead with 175 kilometers of metro track and a terminal expansion that will hit 50 million passengers a year by 2028. Chennai completed its airport Phase 2 in 2026 and is digging 118.9 kilometers of metro Phase II lines.

Tier-2 clusters like Ahmedabad, Jaipur, and Indore are next in line, using multilateral loans and federal grants to bridge funding gaps. Expressways in Uttar Pradesh and coastal roads in Gujarat are already shrinking freight costs by up to 15%. Although right-of-way hurdles linger, these projects expand the contractor universe beyond the six largest metros, easing regional disparities in construction orders.

Hyderabad’s edge stems from synchronized road, rail, and airport programs. The Regional Ring Road, budgeted at USD 2.16 billion, will divert heavy vehicles outside the city core and unlock industrial land. Together with the metro build-out and airport capacity lift, the corridor reduces logistics times by a third and draws life sciences exporters looking for multimodal hubs. That virtuous loop promises steady demand for civil works, signaling, and real-estate add-ons well into the next decade.

Competitive Landscape

Competition is moderate. The top five contractors—Larsen & Toubro, Tata Projects, Megha Engineering, IRB Infrastructure, and Adani Ports—hold more than USD 60 billion in combined backlogs, but over 50 mid-tier builders still chase state metro and airport jobs. Mandated BIM and environmental standards now favor firms with deeper digital and compliance teams, so tier-1 operators often price bids aggressively to lock volume and spread fixed overhead.

Strategic moves revolve around asset recycling and technology. IRB teamed with KKR on an Infrastructure Investment Trust that monetizes toll roads and frees capital for new Hybrid Annuity Model bids. L&T and Megha formed a joint venture to capture Hyderabad Metro Phase II, merging civil, systems, and local stakeholder skills. Tata Projects employs drones and IoT sensors on both Navi Mumbai and Noida airports to flag defects early, trimming rework by one-fifth. Smaller challengers like NCC Ltd. and Ashoka Buildcon seek niches in inland waterways and tier-2 city metros, banking on lower entry barriers.

Margin pressure keeps consolidation in play. Payment lags hit mid-tier firms hardest, prompting some to exit low-yield highway packages and others to merge for scale. Contractors that own quarry, precast, or logistics arms cushion commodity swings better than pure-play civil firms, and those with InvIT platforms recycle equity fastest, sustaining their bid pipelines.

India Transportation Infrastructure Construction Industry Leaders

Larsen & Toubro Limited

TATA Projects

KEC International Limited

Shapoorji Pallonji

Megha Engineering & Infrastructures Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Chennai Airport Phase 2 finished, adding 15 million passengers a year capacity and biometric boarding systems.

- March 2025: Chennai Port opened a USD 228 million rail link to the Dedicated Freight Corridor, cutting container dwell time by 25% and lowering door-to-door logistics costs for exporters by up to 20%.

- February 2025: Double-stack container trains started full service on both Dedicated Freight Corridor routes, trimming transit times by 30-40% and allowing 2,500-tonne payloads per rake.

- February 2025: The National Highways Authority of India confirmed USD 1.2 billion in delayed contractor payments and rolled out an escrow system to secure future Hybrid Annuity Model disbursements.

India Transportation Infrastructure Construction Market Report Scope

By Type

| Roadways |

| Railways |

| Airways |

| Ports and Inland Waterways |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By City

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Rest of India |

| By Type | Roadways |

| Railways | |

| Airways | |

| Ports and Inland Waterways | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Chennai | |

| Kolkata | |

| Rest of India |

Key Questions Answered in the Report

How large will India’s transportation infrastructure construction market be by 2031?

It is projected to reach USD 122.91 billion by 2031, expanding at a 7.49% CAGR from 2026 to 2031.

Which segment is growing fastest inside this market?

Ports and inland waterways show the quickest climb, with an 8.04% CAGR forecast through 2031 as Sagarmala and Vadhavan Port projects move ahead.

Why is private investment expected to rise?

Toll-operate-transfer highway bundles, airport concessions, and Infrastructure Investment Trust structures give investors stable cash flows and let agencies recycle capital.

What makes Hyderabad the fastest-growing city market?

The city is simultaneously adding a new metro phase, widening its ring roads, and expanding the airport, which together shorten travel times and attract logistics and tech firms.

How are contractors mitigating payment delays?

Large builders shift mature assets into InvITs, adopt escrow-backed annuity models, and use drones and BIM to cut execution costs and protect margins.

What risks still threaten project timelines?

Land acquisition hurdles and commodity price swings remain the top threats, each capable of extending schedules or squeezing profit unless escalation clauses and pooling models succeed.

Page last updated on: