India Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

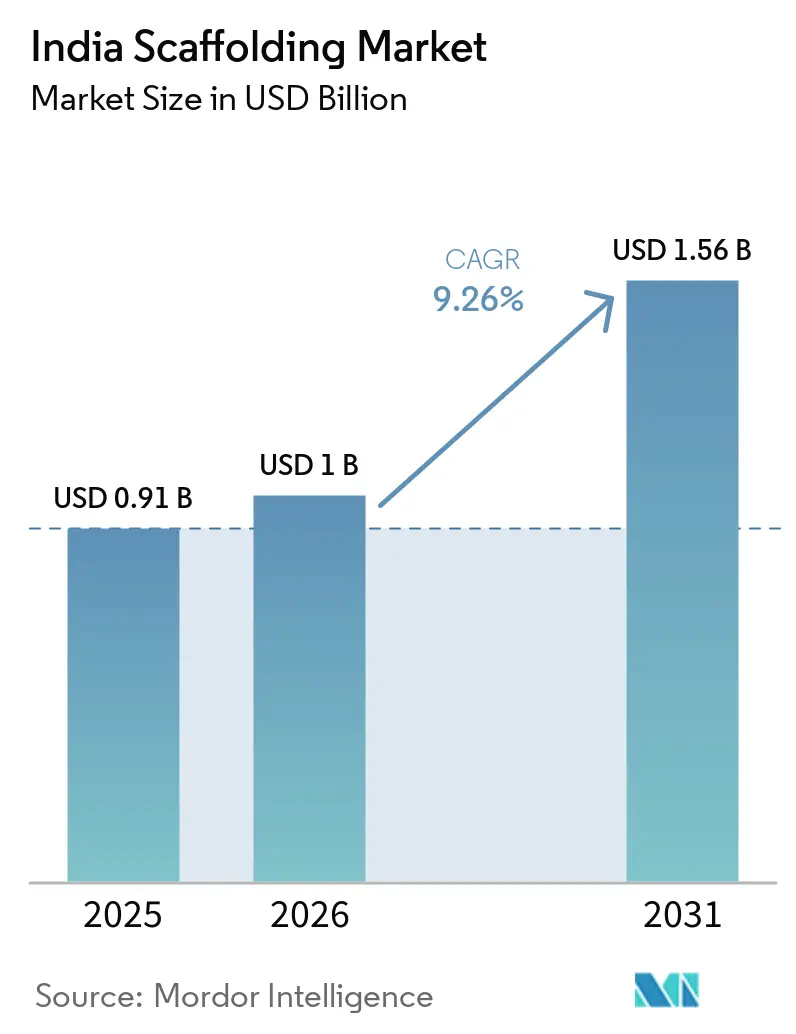

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 9.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Scaffolding Market Analysis by Mordor Intelligence

The India Scaffolding Market size is expected to increase from USD 0.91 billion in 2025 to USD 1 billion in 2026 and reach USD 1.56 billion by 2031, growing at a CAGR of 9.26% over 2026-2031.

Public investment remains a major support for the India scaffolding market, with the Union Budget 2026-27 raising capital expenditure to USD 145 billion and allocating USD 35 billion to road transport and highways and USD 33 billion to railways. Construction activity is broadening beyond housing and commercial buildings, as transport corridors, metro systems, industrial assets, and data centers advance simultaneously. The India scaffolding market is also supported by recurring shutdown work in refineries and petrochemical plants, which keeps demand steady even when parts of the construction cycle soften. Organized suppliers are gaining ground in complex projects because safety documentation, engineered systems, and faster assembly now matter more on large contracts. At the same time, price pressure from informal operators and swings in steel costs continue to shape buying decisions across the India scaffolding market.

Key Report Takeaways

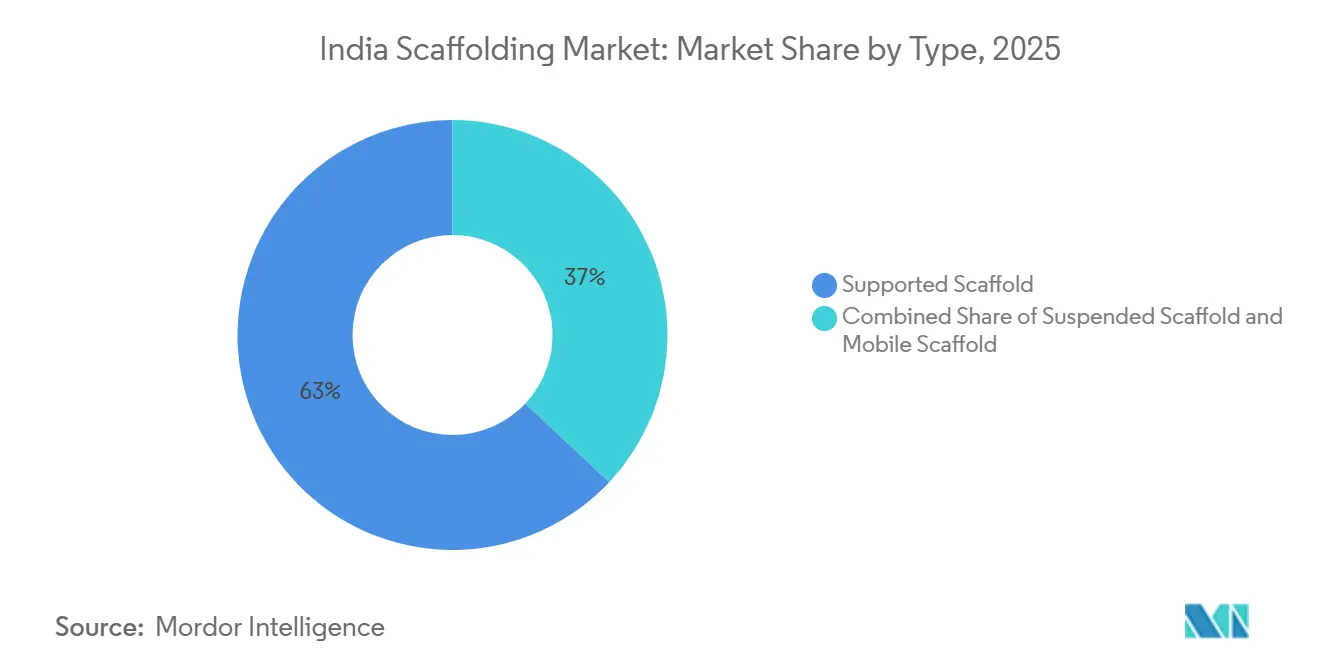

- By type, supported scaffolds held 63.0% of the India scaffolding market share in 2025, while suspended scaffold is projected to record the highest CAGR of 9.1% during 2026-2031.

- By system, cuplock accounted for 38.0% of the market in 2025, while modular / ringlock is forecast to expand at the fastest CAGR of 10.4% through 2031.

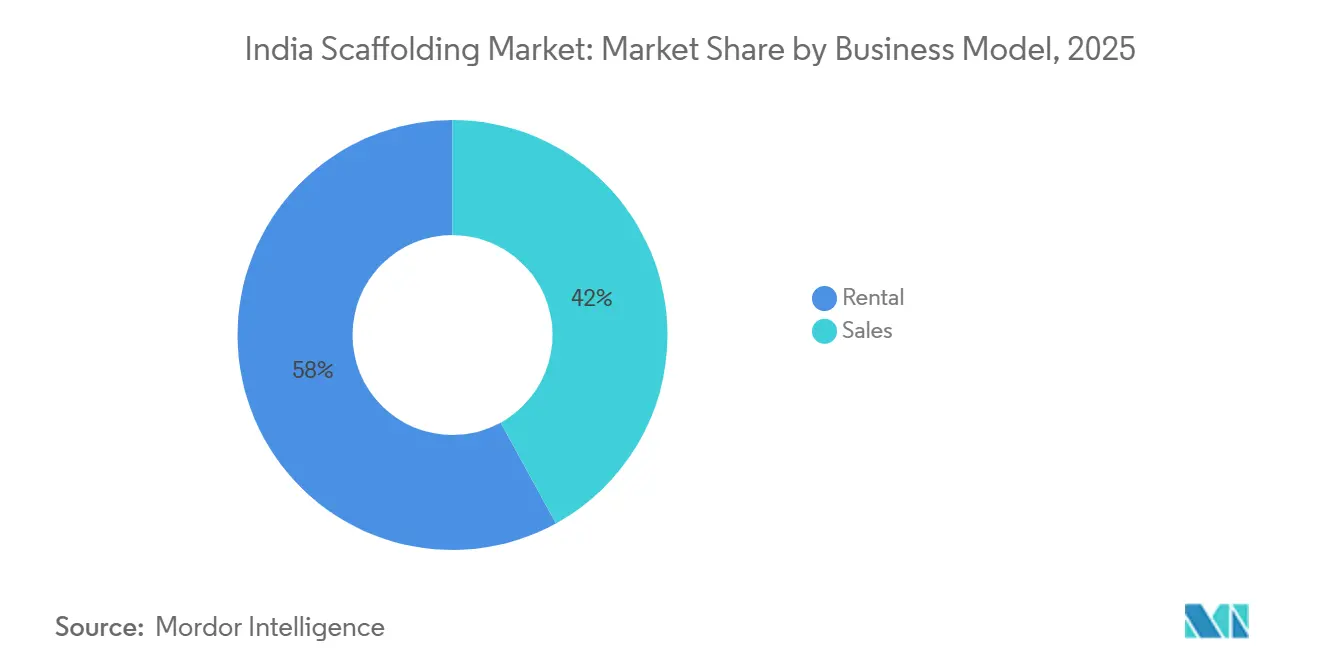

- By business model, rental captured 58.0% of the India scaffolding market share in 2025 and is also expected to grow at the highest CAGR of 9.8% between 2026 and 2031.

- By material type, steel accounted for 71.0% of the market in 2025, while aluminum is projected to register the fastest CAGR of 10.4% over 2026-2031.

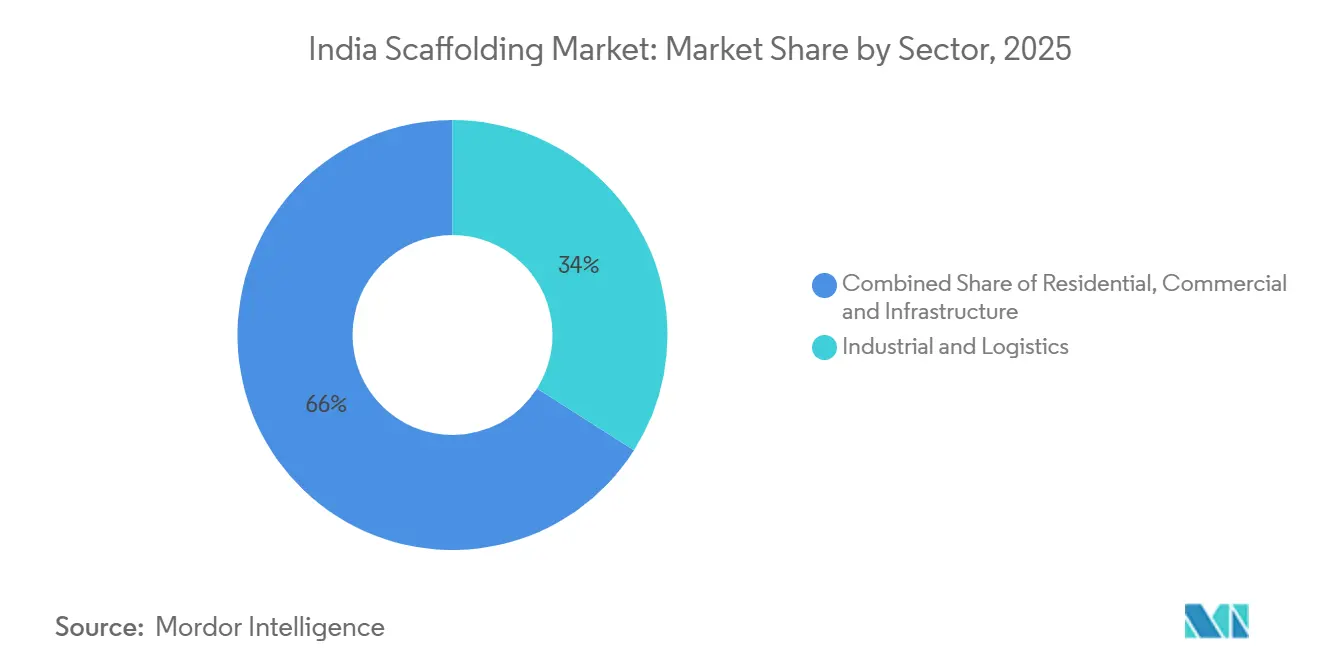

- By sector, industrial and logistics accounted for 34.0% of the India scaffolding market size in 2025, while infrastructure is expected to advance at the highest CAGR of 10.6% through 2031.

- By city, Mumbai Metropolitan Region held 18.5% of the market in 2025, while Delhi NCR is forecast to grow at the fastest CAGR of 10.2% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Commercial and Infrastructure Construction Boosts Scaffolding Demand | +2.8% | National, with the strongest demand in the Mumbai Metropolitan Region, Delhi NCR, Pune, and Bengaluru | Medium term (2-4 years) |

| Industrial Maintenance and Shutdown Projects Increase Scaffolding Usage | +1.6% | National, with concentration in Gujarat, Maharashtra, West Bengal, and refinery clusters | Medium term (2-4 years) |

| Stricter Safety Compliance Drives Adoption of Standardized Scaffolding Systems | +1.2% | National, with stronger enforcement in large metros and public engineering, procurement, and construction contracts | Long term (≥ 4 years) |

| Shift Toward Modular and Reusable Systems Enhances Market Growth | +0.9% | National, with early uptake in infrastructure corridors and metro rail projects | Medium term (2-4 years) |

| Rental Model Expansion Improves Access to Scaffolding Equipment | +0.7% | National, especially in Tier 1 and Tier 2 cities | Short term (≤ 2 years) |

| Growing Urban Development Expands Scaffolding Requirements Across Cities | +0.5% | Delhi NCR, Bengaluru, Hyderabad, Pune, and emerging Tier 2 hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial and Infrastructure Construction Boosts Scaffolding Demand

Public capital spending gives the India scaffolding market a strong base over the forecast period. Union Budget 2026-27 raised capital expenditure to USD 145 billion, including USD 35 billion for road transport and highways, and USD 33 billion for railways[1]Ministry of Finance, “Expenditure Budget 2026-27,” Government of India, indiabudget.gov.in. Housing construction remains active as well, with Pradhan Mantri Awas Yojana Urban 2.0 having sanctioned 1.36 million additional urban housing units by February 2026. The project mix is also getting heavier in data centers, metro structures, and large urban transport schemes, which require dense access systems during civil works and fit-out stages. India’s construction sector is projected to record 8-10% revenue growth in fiscal year 2027, following 6-8% growth in fiscal year 2026, suggesting continued order flow for access equipment suppliers.

Industrial Maintenance and Shutdown Projects Increase Scaffolding Usage

Industrial shutdown work provides the India scaffolding market with a demand stream that is not dependent on new building starts. Refineries and petrochemical plants must complete periodic maintenance turnarounds, and those events require safe access to elevated pipework, vessels, and internal process units. Haldia Petrochemicals completed a 45-day turnaround in 2025 at its West Bengal facility, Indian Oil’s Gujarat refinery carried out a phased shutdown through mid-2025, and Reliance shut a crude unit for 21 days at Jamnagar in 2025[2]Staff Reporter, “Construction Industry Poised to Hit $1.4 Tn by 2030 on Govt Infra Spending,” The Hindu BusinessLine, thehindubusinessline.com. Bharat Petroleum is also scheduled to shut a crude unit at its Mumbai refinery for 3-4 weeks in November 2026. Because these events are tied to safety and operating rules, they help organized contractors keep utilization and pricing firmer than the broader construction cycle alone would suggest.

Stricter Safety Compliance Drives Adoption of Standardized Scaffolding Systems

The India scaffolding market is moving toward better-documented, more standardized systems as safety rules gain weight in procurement. The Bureau of Indian Standards governs steel tubular scaffolding through IS 2750 and safety practices through IS 3696, while the National Building Code 2016 requires designed scaffold schemes with load calculations for tubular scaffolds above 30 meters[3]Bureau of Indian Standards, “IS 2750 Steel Tubular Scaffolding,” Bureau of Indian Standards, bis.gov.in. The Building and Other Construction Workers Act and the Occupational Safety, Health and Working Conditions Code also place clearer responsibilities on employers to provide safer working platforms[4]Comptroller and Auditor General of India, “Chapter 4 Performance Audit on Welfare of Building and Other Construction Workers,” Comptroller and Auditor General of India, cag.gov.in. A 2025 performance audit by the Comptroller and Auditor General of India documented repeated violations of scaffold safety standards, indicating that enforcement gaps persist on the ground. That gap now works in favor of certified suppliers on larger projects, since developers and engineering contractors increasingly want compliance records and lower liability exposure.

Shift Toward Modular and Reusable Systems Enhances Market Growth

The India scaffolding market is also shifting toward modular systems where project geometry is more complex, and schedules are tighter. Ringlock and other modular systems help contractors reconfigure working platforms faster, and that matters on metro viaducts, elevated highways, and bridge jobs that do not follow simple layouts. Doka India used automatic climbing and large-area formwork systems on the Missing Link section of the Mumbai-Pune Expressway in 2025, including custom solutions for 182-meter diamond-shaped pylons on a 650-meter cable-stayed bridge. That project reflects the kind of engineering demands that are becoming more common in the national pipeline. As infrastructure projects rise as a share of total construction work, modular systems are likely to take a larger share of the India scaffolding market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unorganized Market Competition Creates Pricing Pressure | -1.5% | National, with the strongest pressure in Tier 2 and Tier 3 cities, and in residential construction | Long term (≥ 4 years) |

| Safety Compliance Gaps Restrict Adoption of Quality Systems | -1.2% | National, with a concentration on private residential and smaller commercial sites | Medium term (2-4 years) |

| Fluctuating Raw Material Prices Increase Equipment Costs | -1.0% | National, with added pressure in regions with higher logistics or import dependence | Medium term (2-4 years) |

| High Initial Cost of Advanced Scaffolding Systems Limits Uptake | -0.7% | National, with greater pressure on small and medium contractors in Tier 2 and Tier 3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Unorganized Market Competition Creates Pricing Pressure

A large informal supply base remains one of the main brakes on the Indian scaffolding market. Small local operators often use non-certified material, skip testing records, and compete on low prices that organized suppliers cannot easily match. This pressure is strongest in residential and mid-scale commercial work, where site managers often choose nearby vendors who can deliver quickly and offer flexible credit terms. That makes price competition harder to solve with scale alone, because local relationships still matter in many cities. The result is a slower shift toward higher quality fleets and a lower average selling price in parts of the India scaffolding market.

Safety Compliance Gaps Restrict Adoption of Quality Systems

Safety enforcement still varies sharply across project types, and that limits faster migration toward better systems in the India scaffolding market. The Comptroller and Auditor General of India found repeated cases of unsafe platforms and missing protection in its 2025 review of construction worker welfare. This creates a two-track market where formal public contracts and large developers buy certified systems, while many smaller sites still purchase based solely on upfront price. The gap narrows the potential market for engineered products even when overall construction activity is strong. It also delays replacement demand, since buyers on informal sites have less incentive to replace older or undocumented equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Scaffolds Lead the Market While Suspended Scaffolds Gain Momentum

Supported scaffolds accounted for 63.0% of the market in 2025, making it the largest type in the India scaffolding market. Its lead comes from broad use across residential towers, office projects, industrial structures, and bridge substructure work. It remains the default choice on many sites because it is familiar, flexible, and easier to source at scale across cities. Suspended scaffolds are the fastest-growing type and are forecast to expand at a 9.1% CAGR through 2031, as façade work, bridge rehabilitation, and tall industrial assets require access where ground support is less practical.

Supported systems should keep their lead because most construction volume in India still comes from applications where ground-based access works well. Housing, standard commercial buildings, and many industrial additions continue to favor simple and proven setups over highly specialized equipment. The faster growth in suspended systems does not change that base, but it does show that the India scaffolding market is becoming more balanced across new construction and maintenance work. Older high-rise stock is also entering repair cycles, increasing the need for façade access over time. Storage terminals and tank farms add another recurring use case, since inspection and repainting work often depend on suspended access methods during scheduled maintenance.

By System: Cuplock Remains Dominant as Modular Systems Gain Traction

Cuplock accounted for 38.0% of the value in 2025, maintaining its leading position in the India scaffolding market. Its strength comes from wide contractor familiarity, broad availability, and competitive pricing on standard building work. Cuplock is still well-suited to residential blocks, commercial shells, and many repetitive layouts where speed and cost matter more than custom engineering. Modular / ringlock is the fastest-growing category, projected to grow at a 10.4% CAGR through 2031, as complex infrastructure projects require greater flexibility and clearer load documentation.

The shift is most visible on metro rail corridors, elevated expressways, and bridge contracts where geometry changes from span to span. On those jobs, rosette-based systems help crews adapt faster without relying on improvised site modifications. The India scaffolding industry is therefore moving toward a two-speed system mix, with cuplock staying strong in mainstream work and modular systems taking a growing share of high-value contracts. Regulatory pressure also supports this shift, because formal infrastructure procurement increasingly prefers systems with tested performance and documented load ratings.

By Business Model: Rental Stays Ahead as Formal Channels Expand

Rental accounted for 58.0% of value in 2025, giving it the largest position in the India scaffolding market. Contractors prefer rental because it reduces upfront ownership costs, avoids storage and maintenance burdens, and lowers the risk of idle inventory during seasonal slowdowns. That model also fits multi-project operators that shift equipment across sites and cities. Rental is forecast to grow at 9.8% CAGR through 2031, so the segment that already leads in size is also expected to grow the fastest.

That pattern suggests the market is still early in the shift from ownership to professional access services. Large industrial users still buy equipment for recurring shutdown work, especially when internal mobilization speed matters during refinery and petrochemical maintenance. Even so, the stronger capital flow is moving toward organized rental operators with larger fleets and better service coverage. The Indian scaffolding industry should therefore see more value shift toward managed access platforms, compliance support, and site logistics rather than solely product sales. MTandT Rentals reported USD 45 million in revenue for fiscal year 2026 and announced a USD 119 million capital expenditure plan for fiscal year 2026-27 to expand its fleet from 2,000 to 4,000 units. That scale-up shows that investors expect formal rental demand to deepen across the India scaffolding market.

By Material Type: Steel Holds the Base While Aluminum Gains in Faster Cycles

Steel retained 71.0% of revenue in 2025, which made it the clear material leader in the India scaffolding market. Its position reflects a stronger load-bearing capacity for the cost, wide domestic availability, and long use across contractor fleets. Steel remains the practical first choice for many heavy-duty and price-sensitive applications. Aluminum is the fastest-growing material, and it is expected to expand at 10.4% CAGR through 2031 as lighter systems help reduce assembly time and manual handling on specialized work.

Aluminum is gaining most where repeated erection and dismantling cycles change the cost equation. Bridge rehabilitation and selected National Highways Authority of India tenders favor lighter systems when dead-load limits matter on older structures. The India scaffolding market for steel remained larger in 2025, but Aluminum is gaining ground on projects where speed and labor efficiency carry more weight in contractor decisions. Knest Manufacturers secured USD 35.2 million in June 2025 to expand research and production, and to pursue backward integration in Aluminum construction systems. That investment shows growing confidence that lightweight systems will capture more value in the India scaffolding industry over time.

By Sector: Industrial and Logistics Give Stability While Infrastructure Drives Growth

Industrial and logistics accounted for 34.0% of the India scaffolding market in 2025, making it the largest sector. This segment benefits from refinery turnarounds, petrochemical maintenance, power plant servicing, and the expansion of warehousing assets linked to modern supply chains. Those use cases create recurring demand that does not rely only on fresh project launches. Infrastructure is the fastest-growing sector and is forecast to grow at a 10.6% CAGR through 2031 as metro lines, highways, bullet train projects, and port-related construction expand across the country.

Industrial and logistics should remain important because maintenance work is mandatory and often time-bound. India has 23 operational refineries with a combined capacity of over 5 million barrels per day, which supports a steady pipeline of shutdown-related access work. At the same time, the infrastructure segment is raising the technology level of the India scaffolding market through more demanding layouts and stricter safety requirements. The India scaffolding industry is also seeing stronger support from logistics parks and high-bay warehouses, where taller clear heights increase the need for reliable access systems during construction. Government support for affordable housing remains relevant too, with Budget 2026-27 allocating USD 714.3 million for beneficiary-led construction and USD 1.5 billion for affordable housing in partnership.

Geography Analysis

Mumbai Metropolitan Region accounted for 18.5% of the value in 2025, giving it the largest geographic share and the leading position in the India scaffolding market. This concentration comes from overlapping demand in metro construction, high-rise housing, industrial maintenance, and a growing data center pipeline in Navi Mumbai. The Missing Link section of the Mumbai-Pune Expressway shows the technical profile of work in this region, with Doka India using advanced climbing systems on a cable-stayed bridge with 182-meter pylons in 2025. Delhi NCR is the fastest-growing city, with an expected 10.2% CAGR through 2031. Tender activity supports that outlook, with highway and expressway awards in Delhi valued at USD 2.7 billion during the 2025-26 surge, while the Aqua Line extension tender for an elevated viaduct and 10 stations was valued at USD 154.8 million in 2025. These two metro regions together shape both current volume and future growth in the India scaffolding market.

Pune, Bengaluru, and Hyderabad form the next major demand cluster. Pune stands out because it combines project activity with local product capabilities, including PERI, India’s research and development center, and Knest Manufacturers’ base in the city. Bengaluru continues to support steady rental demand through office, residential, and technology-led construction. Hyderabad adds strength through large residential projects and ongoing expansion in its pharmaceutical and industrial clusters. Budget 2026-27 also placed added emphasis on urban infrastructure in cities with populations above 500,000, which should support civic, mobility, and utility projects across these centers.

The rest of India is becoming increasingly important as public works expand into Tier 2 and Tier 3 cities. The largest metro clusters still lead the India scaffolding market share, but growth is spreading through industrial corridors, logistics parks, and urban services projects outside the top cities. The Smart Cities Mission and the Atal Mission for Rejuvenation and Urban Transformation had completed 94% of the approved projects across 100 cities by March 2025, indicating that construction activity has already expanded geographically. Eastern Dedicated Freight Corridor-linked manufacturing and warehousing nodes are also opening fresh demand pockets in Uttar Pradesh, Bihar, and Jharkhand. Refinery and petrochemical clusters in Gujarat and Haldia add another layer of recurring access work, helping keep regional demand less volatile than in a purely residential market.

Competitive Landscape

The India scaffolding market remains fragmented. Global engineering-led firms such as PERI India, Doka India, Layher Scaffolding Systems Pvt Ltd, RMD Kwikform India, and ULMA Formwork and Scaffolding Systems India Pvt Ltd are strongest in premium infrastructure, industrial work, and technically demanding commercial projects. Domestic companies such as Technocraft Industries, AMCO Exports, Finomax Scaffolding, Translite Scaffolding, and Iron Ridge Scaffolding serve a broader mid-market that still spans a wide range of project sizes and budgets. This split means both engineering capability and pricing discipline shape the competitive field. It also means organized players need to prove their value through safety, speed, and site support rather than just product supply.

One clear strategy is deeper technical differentiation. PERI India continues to work through its Pune research and development center on systems suited to local site conditions. At the same time, Doka India demonstrated advanced deployment capability on the Missing Link expressway project in 2025. Another strategy is fleet-led expansion in organized rental, where scale, turnaround speed, and compliance records can build customer stickiness over time. MTandT Rentals added fresh capital in March 2026 and outlined a major fleet expansion plan in May 2026, showing how access providers are using funding to build national coverage. These moves suggest that the India scaffolding market is rewarding firms that can combine equipment access with service reliability.

Another theme is capacity building among domestic organized suppliers. MSafe Equipment completed its initial public offering in January 2026 and is expanding manufacturing at its Mathura facility to support its integrated manufacturing, rental, and sell model across 18 warehouses. Knest Manufacturers also attracted USD 35.7 million in June 2025 to scale research, production, and integration of aluminum systems, signaling rising interest in differentiated construction access products. These moves do not eliminate fragmentation, because informal suppliers remain active in many local markets. Still, they show that the India scaffolding market is slowly moving toward stronger, more organized competition in higher-value segments. Over time, tighter safety expectations and more complex project design should continue to favor companies that can document performance, serve multiple cities, and respond quickly to industrial shutdown schedules.

India Scaffolding Industry Leaders

PERI India Pvt. Ltd.

Doka India Private Limited

RMD Kwikform India Private Limited

ULMA Formwork and Scaffolding Systems India Pvt. Ltd

Layher Scaffolding Systems Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: MTandT Rentals announced a USD 119 million capital expenditure plan for fiscal year 2026-27 to expand its Mobile Elevating Work Platform and Spider Lift fleet from 2,000 to 4,000 units. The company also reported USD 45 million in consolidated revenue for fiscal year 2025-26 and is in talks for a third private equity round worth USD 35.7 million.

- March 2026: MTandT Rentals raised USD 11.9 million from ValueQuest S.C.A.L.E. Fund II to expand its fleet and strengthen its presence across India. The funding followed INR 62 crore (USD 7.4 million) raised through private placements in fiscal year 2024-25, showing continued investor interest in organized access equipment rental.

- February 2026: MSafe Equipment was listed on the BSE SME platform and raised USD 7.9 million through an oversubscribed initial public offering. The proceeds will support a new manufacturing facility in Noida and additional production of rental fleet units.

India Scaffolding Market Report Scope

The India Scaffolding Market Report is Segmented by Type (Supported, Suspended, and Mobile Scaffold), System (Tube & Coupler, Cuplock, and More), Business Model (Sales and Rental), Material Type (Timber / Plywood, Steel, Aluminum, and More), Sector (Residential, Commercial, and More), and City (Mumbai Metropolitan Region, Delhi NCR, Pune, Bengaluru, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Rest of India |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By City | Mumbai Metropolitan Region |

| Delhi NCR | |

| Pune | |

| Bengaluru | |

| Hyderabad | |

| Rest of India |

Key Questions Answered in the Report

What is the forecast value of the India scaffolding sector by 2031?

The India scaffolding market is projected to reach USD 1.56 billion by 2031, rising from USD 1.00 billion in 2026 at a 9.26% CAGR.

Which scaffolding type is most used in India today?

Supported scaffold led with 63.0% share in 2025 because it fits the widest range of residential, commercial, industrial, and infrastructure applications.

Which business model is growing fastest in the scaffolding industry in India?

Rental is both the largest and fastest-growing model, with 58.0% share in 2025 and a projected 9.8% CAGR through 2031.

Why is infrastructure so important for scaffolding demand in India?

Infrastructure is the fastest-growing sector, with a 10.6% CAGR through 2031, supported by highways, metro rail, high-speed rail, and other public works.

Which city has the highest demand for scaffolding in India?

Mumbai Metropolitan Region led with 18.5% share in 2025 because it combines metro construction, high-rise development, industrial work, and data center projects.

What is changing competition among scaffolding suppliers in India?

Competition is still fragmented, but organized firms are gaining ground through modular systems, larger rental fleets, compliance support, and city-wide service capability.

Page last updated on: