India Folding Carton Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

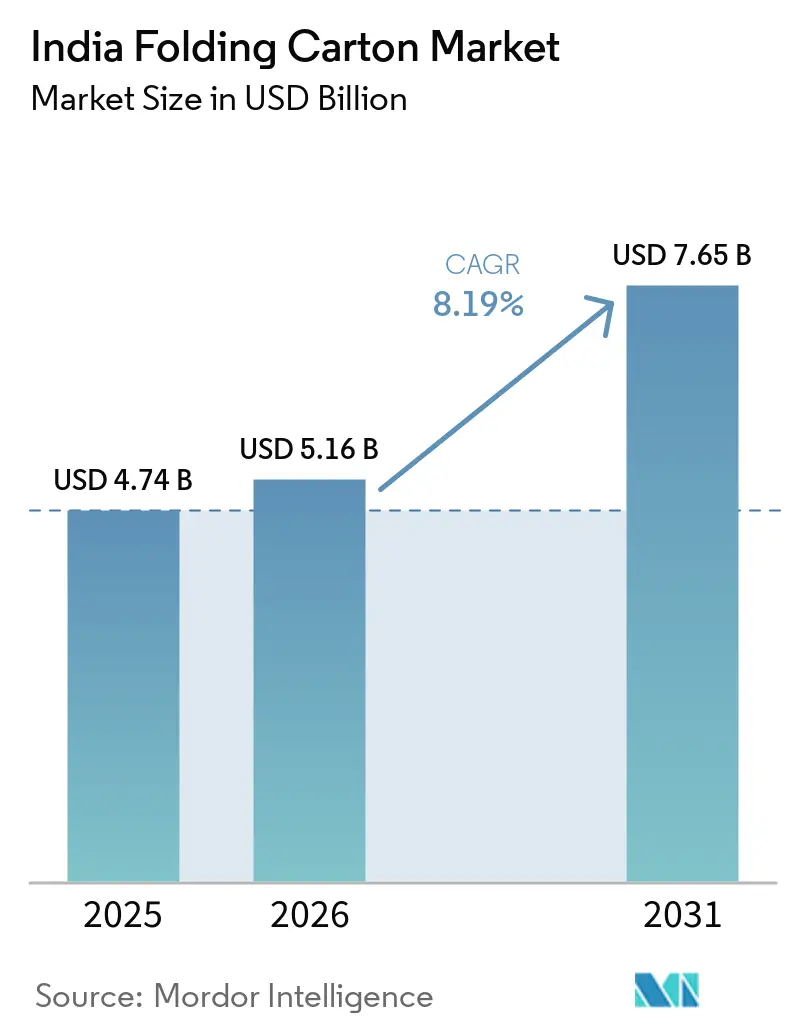

| Base Year Market Size (2025) | USD 4.74 Billion |

| Market Size (2026) | USD 5.16 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

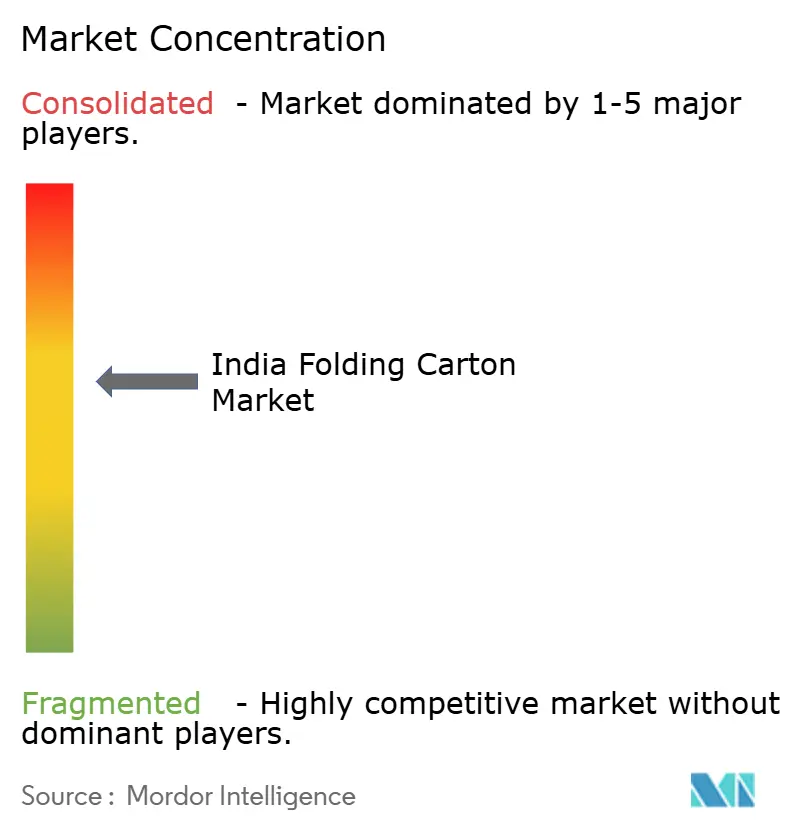

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Folding Carton Market Analysis by Mordor Intelligence

The India folding carton market size is expected to increase from USD 5.16 billion in 2026 to reach USD 7.65 billion by 2031, growing at a CAGR of 8.19% over 2026-2031. Brand owners are balancing cost and sustainability while racing to place products on the shelf or doorstep faster than ever. Quick-commerce operators have reduced order-to-delivery windows to 10 minutes, so converters must now supply shelf-ready formats that survive multiple handling points without scuffing graphics. Government incentives for pharmaceutical manufacturing have stimulated demand for tamper-evident cartons, and corporate sustainability pledges are pulling natural-brown substrates into mainstream use. At the same time, converters face pulp-price volatility and tight recycled-fiber supply, making backward integration and automation critical to margin defense.

Key Report Takeaways

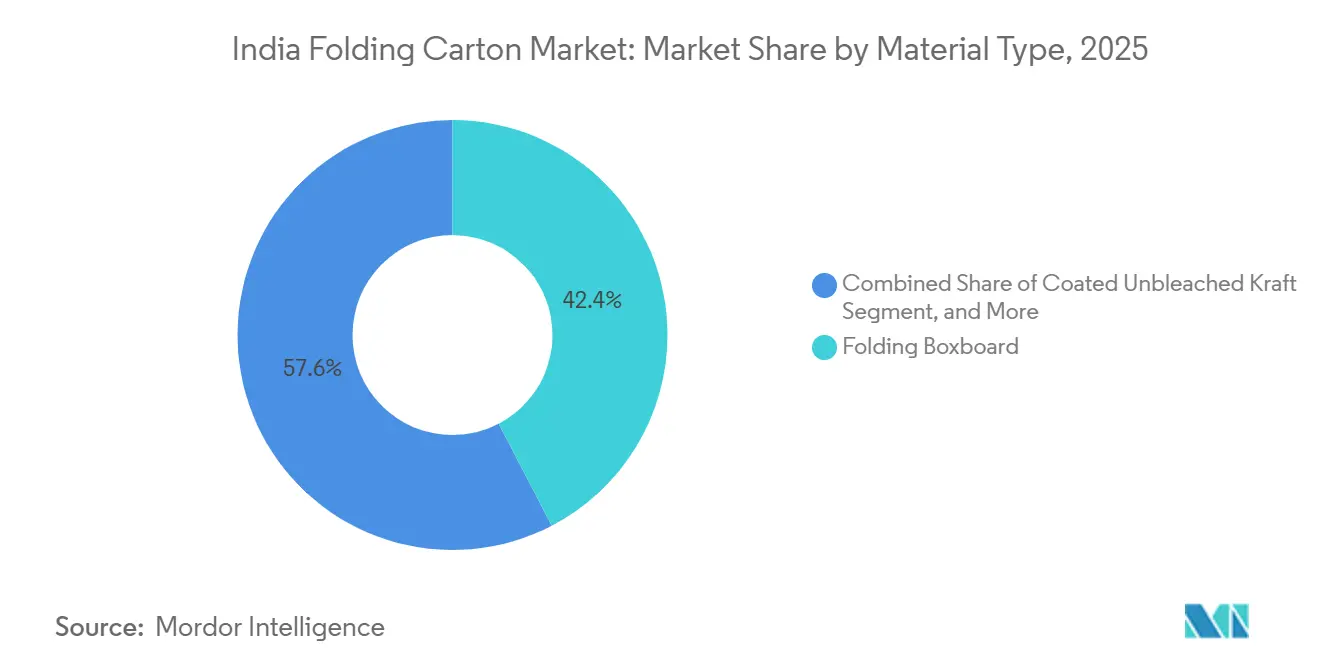

- By material type, folding boxboard captured with 42.37% of the India folding carton market share in 2025.

- By printing technology, the India folding carton market size for digital printing is projected to grow at a 9.67% CAGR to 2031.

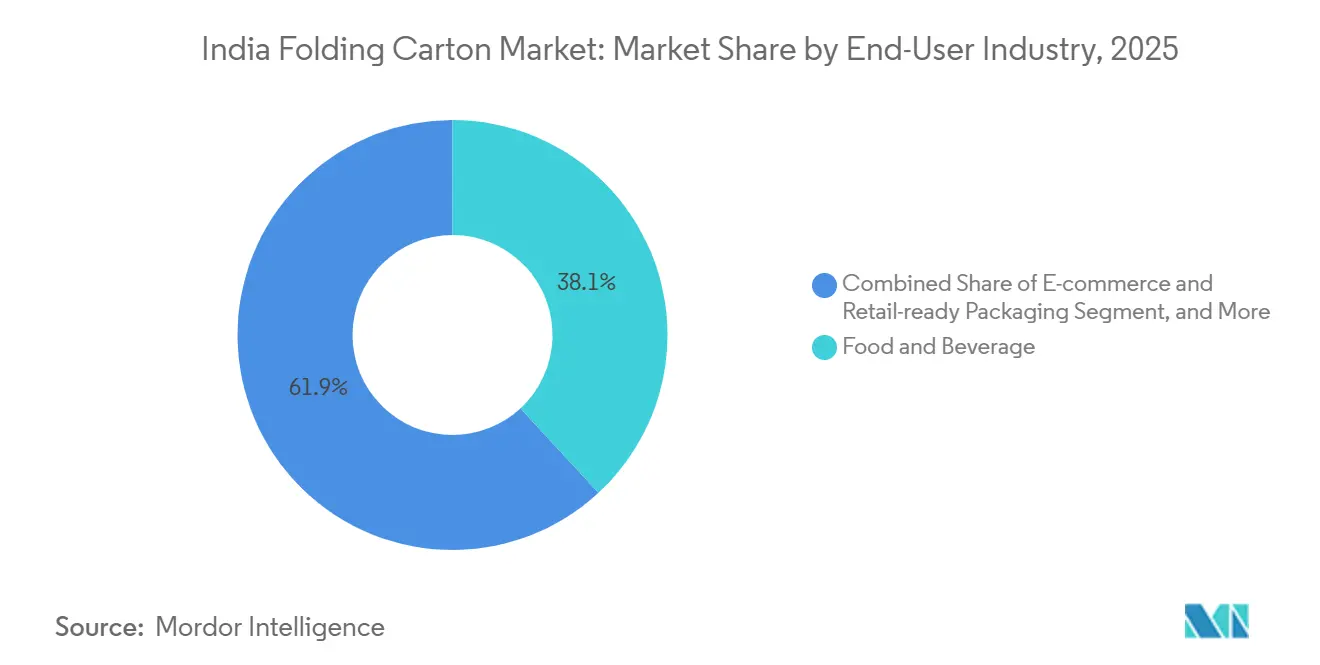

- By end-user industry, the food and beverage industry captured 38.12% of the India folding carton market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Folding Carton Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dominance of E-commerce and Last-Mile Delivery | +2.2% | National; high concentration in Seoul Capital Area (SCA) and Incheon logistics hubs | Short term (≤ 2 years) |

| Regulatory Shift Toward Eco-Friendly & Plastic-Free Packaging | +1.9% | National; enforced by the Ministry of Environment with focus on major retail centers | Medium term (2-4 years) |

| Expansion of Premium Cosmetics and "K-Beauty" Exports | +1.4% | Concentrated in Gyeonggi-do and Incheon beauty manufacturing clusters | Long term (≥ 4 years) |

| Growth in Specialized Electronics & Semiconductor Packaging | +1.2% | Specialized industrial corridors (Hwaseong, Pyeongtaek, and Icheon) | Medium term (2-4 years) |

| Adoption of Smart Packaging & Digital Printing for Pharma | +1.0% | National; led by pharmaceutical hubs in Seoul and Osong Bio Valley | Medium term (2-4 years) |

| Rising Demand for Sustainable Food Service & QSR Solutions | +0.7% | Major urban Tier-1 cities (Seoul, Busan, Daegu) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Driving Shelf-Ready Folding Cartons

Online grocery, personal care, and consumer electronics now demand cartons that withstand automated sortation, motorcycle courier drops, and direct customer presentation. Dark-store counts surpassed 2,000 locations by late 2026, compressing delivery windows and eliminating the buffer for secondary repackaging. Shelf-ready designs cut retail labor costs, giving brands a 15-20% logistics saving and rewarding converters that invest in rotary die-cutting and inline gluing. E-commerce and retail-ready packaging is therefore advancing 217 basis points faster than the overall Indian folding carton market. Micro-batch changeovers, now as high as 12 per shift at leading plants, have become a competitive necessity rather than a luxury.

Sustainability Push from Consumer Packaged Goods Brands

Large fast-moving consumer goods companies have moved from pledges to purchase orders. ITC, Hindustan Unilever, and Dabur collectively collected more than 100,000 metric tons of post-consumer plastic in 2025, and each is driving suppliers toward 100% recyclable or compostable packaging. Folding cartons, already recyclable, now must include recycled content under the 2026 Extended Producer Responsibility rules.[1]Central Pollution Control Board, “Extended Producer Responsibility for Packaging,” Central Pollution Control Board, cpcb.nic.in Converters unable to secure certified recycled fiber pay 10-15% more for imports, underlining why backward integration into pulp is gaining boardroom urgency.

Government Ban on Single-Use Plastics Accelerating Carton Adoption

The 2022 prohibition on 19 single-use plastic items shows uneven enforcement, yet it has pushed high-visibility categories such as quick-service restaurants and dairy to shift to paper formats. A 2025 audit found that 84% of surveyed outlets still used banned items, yet brands nonetheless accelerated voluntary substitution where consumer scrutiny is highest. New EPR mandates require on-pack QR codes for traceability, and state pollution boards in Maharashtra, Tamil Nadu, and Kerala are already imposing penalties, giving compliant converters an early-mover advantage.

Rapid Expansion of Quick-Commerce Dark Stores

Blinkit, Zepto, and Swiggy Instamart are rolling out micro-fulfillment centers that carry 2,000-3,000 SKUs in just 3,000-5,000 square feet. Packaging now acts as primary merchandising, because there is no time for shelf restocking or secondary display. Folding cartons gain here by providing tamper-evidence, compact footprints, and printable brand surfaces that are superior to those of plain shipper boxes. Quick-commerce revenue is growing at 40% CAGR, well ahead of traditional e-commerce, and is expected to exceed USD 10 billion before 2028. Converters able to deliver design iterations in days secure premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Raw Material & Pulp Costs | -1.5% | National; high impact on non-integrated converters in Gyeonggi and North Chungcheong | Short term (≤ 2 years) |

| Inconsistent Enforcement of Plastic Bans | -1.1% | National; primarily affecting food service hubs in Seoul and Busan | Short term (≤ 2 years) |

| Competition from High-Barrier Flexible Packaging | -0.8% | Industrial clusters in Gyeongsang and Jeolla; high impact in frozen food and snacks | Medium term (2-4 years) |

| Technical Challenges in Fiber-Based Barrier Coatings | -0.6% | National; impacting R&D centers in the Seoul Capital Area | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp and Paper Prices

Hardwood pulp touched USD 600 per metric ton in December 2025, while domestic wood feedstock jumped from INR 8,000 (USD 96.4) to INR 14,000-15,000 (USD 168.7-180.7) per ton, squeezing converters on 30-day payment cycles. Government floor prices of INR 67,220 (USD 809.9) per ton on imported board protect mills but prevent opportunistic sourcing when local supply runs tight. Integrated players with captive pulp hedge margins; non-integrated converters risk tender losses and margin erosion.

Competition From Flexible Packaging Formats

Stand-up pouches and laminated films weigh 30-40% less than equivalent cartons, lowering freight costs and making them well-suited for portion-pack snacks. Although flexible-packaging revenues fell 3% in FY2024, metalized barriers and resealable features keep the format attractive in snack foods, confectionery, and dry grocery. Carton converters are countering with shorter runs, tactile varnishes, and digital printing, but must absorb higher unit costs to compete in mass snack segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Natural Kraft Steadily Displaces Bright White Grades

Folding boxboard captured 42.37% of India's folding carton market share in 2025, thanks to its bright coating, which delivers photo-quality graphics demanded by cosmetics, confectionery, and regulated pharmaceutical customers. Brand owners, however, increasingly prefer substrates that signal environmental responsibility, pushing coated unbleached kraft toward a forecast 9.05% CAGR through 2031. That growth rate comfortably outstrips the overall market and reflects e-commerce shippers that want higher strength-to-weight ratios without plastic laminations. As these premium digital-commerce channels widen, recycled white grades maintain volume in price-sensitive foods, but Kraft steadily captures margin-rich launches that highlight a natural-brown aesthetic.

India's folding carton market for kraft grades accelerates further after Java Paper Mills commercialized Oak Duo, an aqueous-coated board with water-vapor transmission below 5 g/m² for 48 hours, eliminating the polyethylene overwrap many dairies still specify.[2]Java Paper Mills Technical Team, “Oak Duo - Coated Unbleached Kraft,” Java Paper Mills, javapapermill.com The extended Producer Responsibility rules, effective April 2026, impose 30% recycled-content targets on rigid packaging, encouraging converters to blend post-consumer fiber in folding boxboard and white line chipboard. Even so, kraft keeps gaining premium slots because its virgin fibers deliver higher tear strength and rustic shelf appeal valued by organic snack, artisanal bakery and craft-beer brands. Mill investments in chlorine-free bleaching and forestry certification strengthen kraft’s sustainability story, easing brand compliance audits and locking in long-term supply contracts.

By Printing Technology: Digital Capacity Fills the Micro-SKU Vacuum

Lithographic presses accounted for 45.78% of 2025 revenue because they run multi-million-carton programs with tight register and standardized Pantone libraries, critical for national fast-moving consumer goods launches. The format’s plate costs, however, become uneconomic when brands release 50 or more festival variants, each ordered in 5,000-carton lots. Consequently, digital printing is forecast to rise at a 9.67% CAGR, with converters installing HP Indigo and similar presses to serve influencer collaborations and direct-to-consumer trial packs. As the SKU explosion continues, litho retains core volumes, while digital harvests profitable short-run and variable-data segments that demand serialization or localized storytelling.

India's folding carton market is also tied to digital workflows, and it is expanding as hybrid presses now bolt inkjet heads onto conventional offset towers, combining low-cost flood coats with on-demand personalization in a single pass. Spectalpack leverages two HP Indigo 200K machines to deliver 12-hour order-to-ship windows, inserting unique QR codes that comply with pharmaceutical Track and Trace laws without a second-label operation. Gravure remains indispensable for tobacco’s anti-counterfeit guilloché patterns, but its cylinder investments and long setup times preclude entry into hyper-granular e-commerce work. Energy-saving LED-UV curing further tilts economics toward digital and hybrid lines by trimming power consumption up to sixty percent while preventing lightweight kraft from heat-related warping.

By End-User Industry: Omnichannel Retail Tightens Specifications

Food and beverage delivered 38.12% of 2025 revenue, driven by aseptic carton placements such as Hamdard’s SIG XSlim 24 line that fills 24,000 packs per hour across nine volumes. Retailers simultaneously demand tear-strip openings, microwave-safe coatings and grease barriers that comply with Food Safety and Standards Authority migration limits, increasing value per ton of board sold. Although legacy categories remain important, India's folding carton market size devoted to e-commerce and retail-ready applications is projected to climb at a 10.36% CAGR through 2031, outperforming the parent market by more than two percentage points. Packaging now doubles as a fulfillment container and a brand billboard, forcing converters to master design for both shelf visibility and last-mile resilience within the same dieline.

Pharmaceutical investment worth INR 38,543 crore (USD 4.6 billion) under the Production Linked Incentive scheme expands serialized and tamper-evident demand corridors in Baddi, Haridwar, and Aurangabad. Personal care labels, chasing premium unboxing moments, willingly pay twenty to thirty percent price uplifts for soft-touch coatings, holographic foils, and spot-gloss effects. Electrical and electronics brands increasingly specify anti-static inserts and print-embedded NFC tags that assist warranty registration, pulling cartons deeper into the connected-packaging ecosystem. Collectively, these high-spec sectors insulate margins and diversify revenue away from commoditized institutional food-service accounts that still favor low-grade white line chipboard.

Geography Analysis

West India generated 29.34% of 2025 folding carton revenue, leveraging Maharashtra’s processed-food ecosystem that produces 21.6% of the nation’s packaged foods and benefits from proximity to Jawaharlal Nehru Port for export consolidation.[3]Invest India Analysts, “Maharashtra - Food Processing,” Invest India, investindia.gov.in Huhtamaki’s 89,350 m² Khopoli facility alone exports up to 40% of its 36,000 metric-ton capacity, supplying Middle Eastern and Southeast Asian snack and dairy brands that specify Indian board on price and lead-time grounds. The Pimpri-Chinchwad belt houses roughly 175 converters; its dense supplier matrix enables just-in-time plate production and rerouting emergency orders when transport bottlenecks occur. Smaller players such as Jay Kailash Namkeen recently leased capacity in Pune, paying INR 132,000 (USD 1,590) monthly, because dark-store grocers in Mumbai and Nashik need same-day replenishment of shelf-ready snack cartons.

North India is forecast to expand at a 10.14% CAGR through 2031, driven by fulfillment warehouses in Delhi-NCR and PLI-induced pharmaceutical corridors in Baddi, Haridwar, and Dehradun that require serialized cartons with tamper-evident glue lines. Gurugram and Noida dark stores already shorten replenishment lead times to under 6 hours, granting a competitive advantage to converters within a 300-kilometer trucking radius. Regional authorities in Haryana aggressively audit Extended Producer Responsibility submissions, so plants there have installed fiber-trace software to avoid penalties and preserve multinational purchase orders. This regulatory vigilance, while costly upfront, accelerates technology upgrades and tilts share toward compliant medium-scale printers.

South India benefits from Bengaluru’s vibrant direct-to-consumer ecosystem and Chennai’s automotive and electronics clusters, which demand electrostatic-safe board and multi-language print for export kits. Although East India currently lags on per-capita packaged-food consumption, upcoming freight-corridor investments and state tax holidays may entice converters to greenfield plants near Kolkata ports. Enforcement of the 2026 recycled-content mandate remains patchy nationwide, yet Maharashtra, Tamil Nadu and Kerala already levy fines for non-compliance, nudging converters in Uttar Pradesh and Bihar to pre-emptively certify supply chains. These regional compliance gradients influence capital allocation, with investors favoring jurisdictions that pair strict rules with transparent approval timelines and reliable utility infrastructure.

Competitive Landscape

India’s folding carton sector shows moderate concentration, with ITC, Huhtamaki, TCPL Packaging, WestRock India, and Parksons Packaging together accounting for roughly 35-40% of total revenue. ITC’s five-year INR 20,000 crore (USD 2.4 billion) program reserves INR 7,000 crore (USD 840 million) for fully integrated pulp-to-carton capacity, insulating earnings from pulp price spikes and enhancing circularity credentials. TCPL Packaging’s 100,000 ft² Chennai plant, commissioned in March 2025, operates seven-color presses and automated folding-gluing lines that achieve twelve changeovers per shift, lifting FY 2026 EBITDA margin to 17%. Such throughput flexibility allows TCPL to court micro-batch e-commerce brands without sacrificing large FMCG contracts.[4]TCPL Packaging Finance Team, “Investor Updates,” TCPL Packaging, tcplpackaging.com

Parksons Packaging expanded to thirteen facilities through three strategic acquisitions, using ISO 15378 accreditation to enter regulated pharmaceutical and premium personal-care segments that demand documented clean-room protocols. Huhtamaki leverages its global footprint to roll out aqueous barrier coatings developed in European R&D centers, helping Indian beverage clients meet single-use plastic bans without sacrificing shelf life. Regional specialists thrive by outsourcing lithography to toll printers, focusing internal effort on graphic design, dieline engineering and forty-eight-hour prototyping services that resonate with direct-to-consumer founders. Their proximity to urban fulfillment hubs offsets smaller print runs, enabling premium pricing even when unit costs exceed those of integrated majors.

Technology competition now revolves around digital presses, robotic palletizers, vision-based quality inspection and ERP dashboards that feed real-time capacity data to brand portals. Plants adopting LED-UV curing cut power consumption by up to 60%, while preventing heat-induced warp on thinner coated unbleached kraft sheets, reducing waste and improving first-pass yield. Compliance software that authenticates recycled-fiber certificates has emerged as a purchasing criterion for multinational brands keen to avoid EPR penalties, placing traceability on par with price and lead time. Collectively, these digital investments widen the gap between well-capitalized groups and smaller converters that still rely on manual inspections and spreadsheet scheduling, driving gradual consolidation through capability-driven M&A.

India Folding Carton Industry Leaders

Parksons Packaging Ltd.

TCPL Packaging Limited

Huhtamaki India Limited

Smurfit Westrock plc

Edelmann India Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Java Paper Mills released Oak Duo coated unbleached kraft with an aqueous barrier suitable for direct food contact, targeting e-commerce and organic food brands.

- December 2025: TCPL Packaging began commercial production at a new gravure-cylinder plant with 12,000-unit annual capacity, cutting artwork led times to 10 days.

- December 2025: Jay Kailash Namkeen leased a 20,000-square-foot site in Pune, paying INR 132,000 (USD 1,590) monthly to scale snack production for quick-commerce channels.

- September 2025: Hamdard commissioned a SIG XSlim 24 aseptic line at Aurangabad, producing 24,000 cartons per hour across nine volume formats.

India Folding Carton Market Report Scope

The India folding carton market is defined as the industry focused on the production and conversion of paperboard into collapsible containers used for protective and promotional packaging across diverse commercial sectors. It further evaluates the market based on dominant printing technologies, including lithographic, flexographic, digital, and gravure.

The India Folding Carton Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, Household and Industrial Goods, Tobacco, E-commerce and Retail-ready Packaging, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Food and Beverage |

| Healthcare/Pharmaceuticals |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Household and Industrial Goods |

| Tobacco |

| E-commerce and Retail-ready Packaging |

| Other End-User Industries |

| By Material Type | Solid Bleached Sulfate |

| Folding Boxboard | |

| Coated Unbleached Kraft | |

| White Line Chipboard | |

| Other Material Types | |

| By Printing Technology | Lithographic Printing |

| Flexographic Printing | |

| Digital Printing | |

| Gravure Printing | |

| Other Printing Technologies | |

| By End-User Industry | Food and Beverage |

| Healthcare/Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Electrical and Electronics | |

| Household and Industrial Goods | |

| Tobacco | |

| E-commerce and Retail-ready Packaging | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the projected size of the India folding carton market by 2031?

The market forecasts the value to reach USD 7.65 billion, reflecting an 8.19% CAGR during 2026-2031.

Which region is expanding fastest and why?

North India is on track for a 10.14% CAGR through 2031, powered by Delhi-NCR fulfillment hubs and PLI-backed pharmaceutical corridors that need serialized cartons.

Why are coated unbleached kraft grades gaining traction with brand owners?

Natural-brown aesthetics signal sustainability while delivering high tear strength, driving a 9.05% CAGR and winning premium e-commerce and organic-food launches.

How is quick-commerce reshaping folding-carton specifications?

10-minute delivery windows force shelf-ready formats that survive automated sorting and bike-courier drops, rewarding converters with rapid die-change and inline gluing capability.

What technology upgrades are converters prioritizing to stay competitive?

Investments focus on digital presses, LED-UV curing, robotic palletizers and traceability software that authenticates recycled-fiber inputs.

How do April 2026 Extended Producer Responsibility rules influence demand?

Mandatory recycled-content thresholds of 30% for rigid packaging accelerate orders for carton grades that can verify fiber provenance and meet audit requirements.

Page last updated on: