India AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

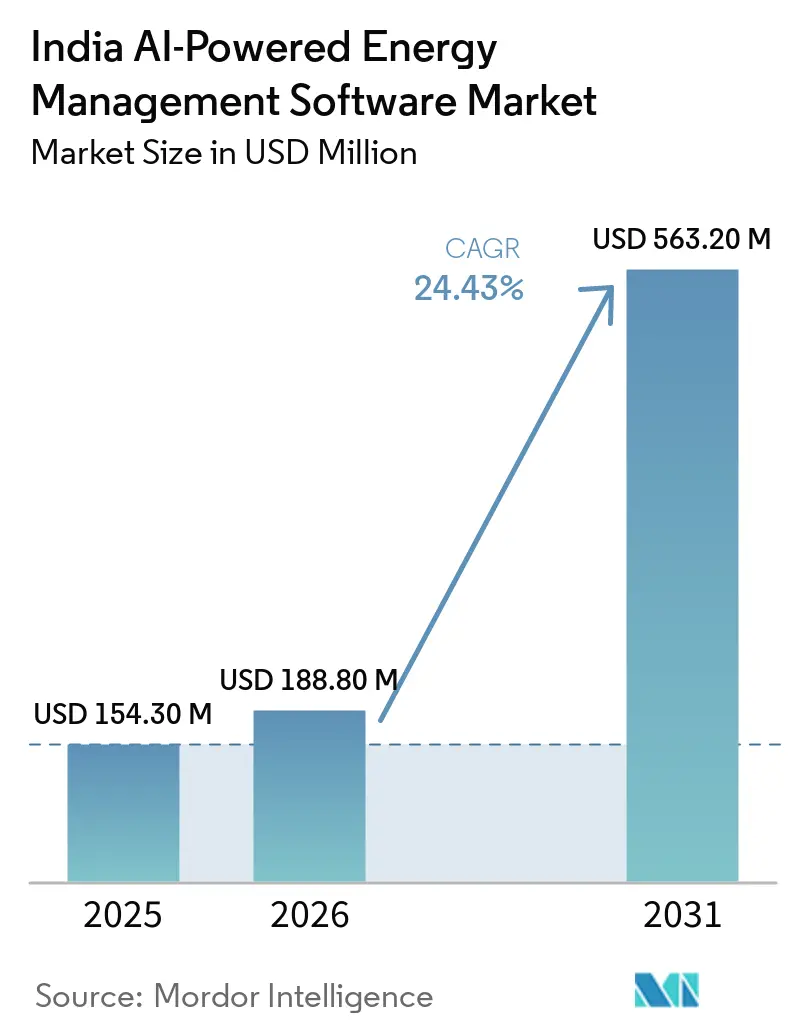

| Base Year Market Size (2025) | USD 154.30 Million |

| Market Size (2026) | USD 188.80 Million |

| Market Size (2031) | USD 563.20 Million |

| Growth Rate (2026 - 2031) | 24.43% CAGR |

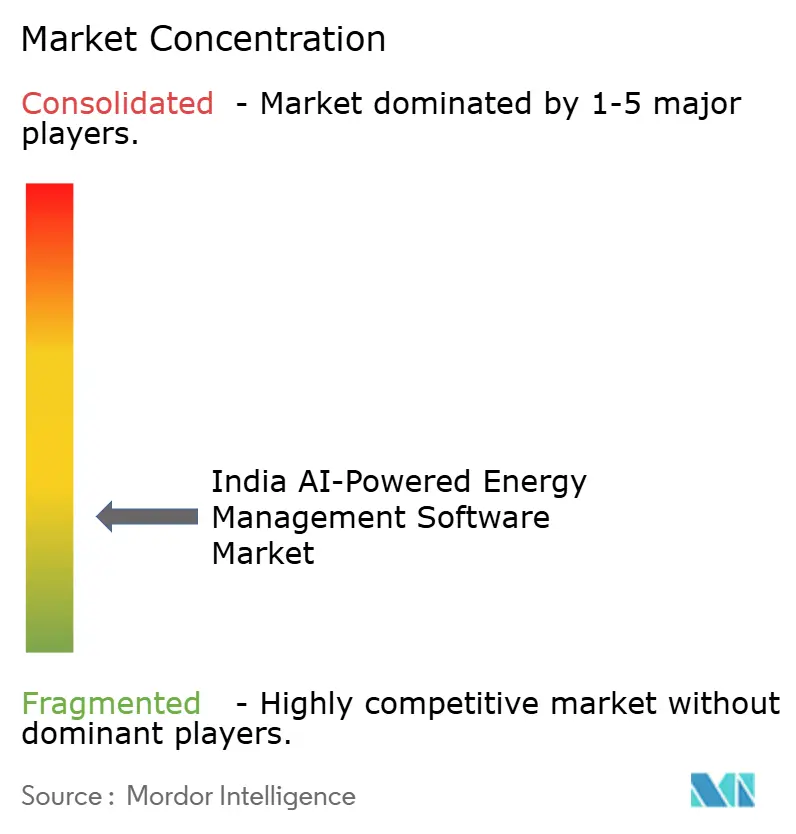

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The India AI-powered energy management software market size was USD 154.3 million in 2025 and is projected to reach USD 563.2 million by 2031, registering a CAGR of 24.43% during 2026-2031. Growth is supported by a power distribution system moving through a large capital-spending cycle, a faster renewable energy buildout, and higher electricity costs for commercial and industrial users. The market is also benefiting from the widening gap between smart meter deployment and the analytics capacity needed to use that data effectively, making AI-led software increasingly necessary for utilities and large energy users. India’s clean energy and emissions targets are adding another layer of demand, as energy optimization is now more closely tied to reporting, compliance, and board oversight. Competition in the Indian AI-powered energy management software market is moderate to high, with global automation firms, enterprise software vendors, and India-focused specialists all trying to secure long-term platform relationships. Legacy operational systems and data sovereignty rules still slow some deployments, but the India AI-powered energy management software market continues to move forward because utilities, industrial users, and commercial facilities all have clear reasons to invest.

Key Report Takeaways

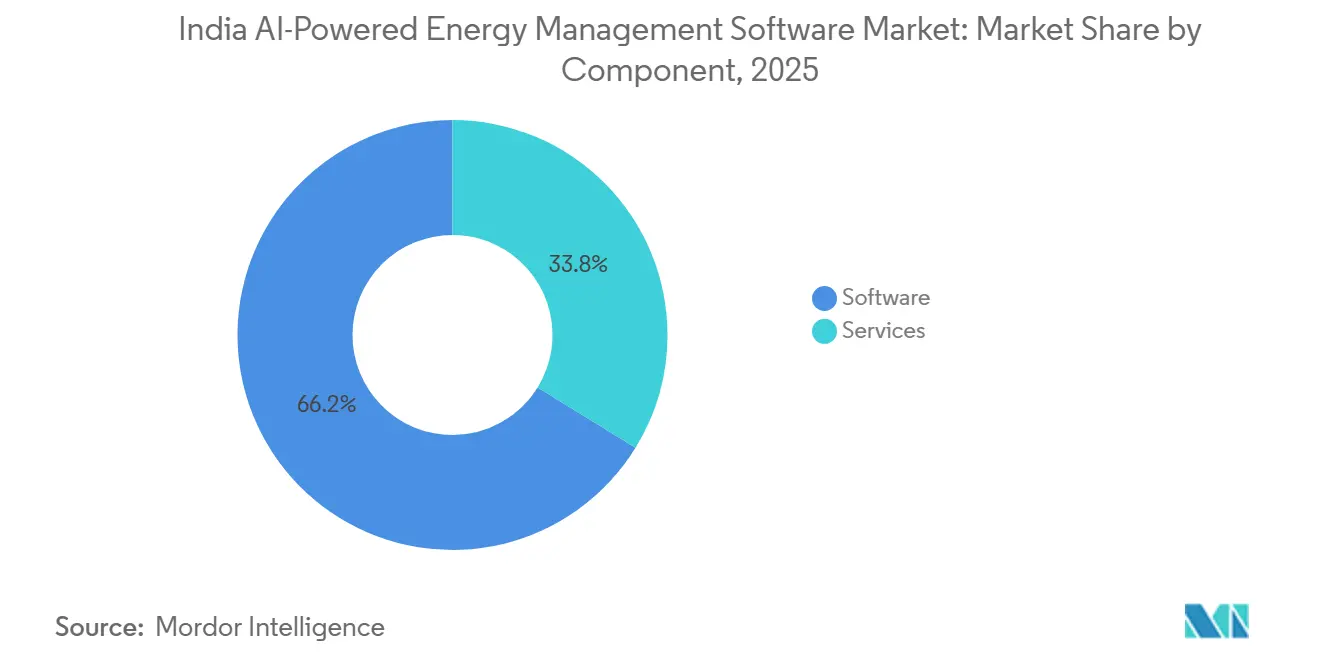

- By component, software accounted for 66.21% of the India AI-powered energy management software market in 2025, while services are projected to expand at a 25.47% CAGR through 2031.

- By deployment mode, cloud-based solutions led with a 56.17% share in 2025, while hybrid deployment is expected to record the fastest growth at a 25.58% CAGR through 2031.

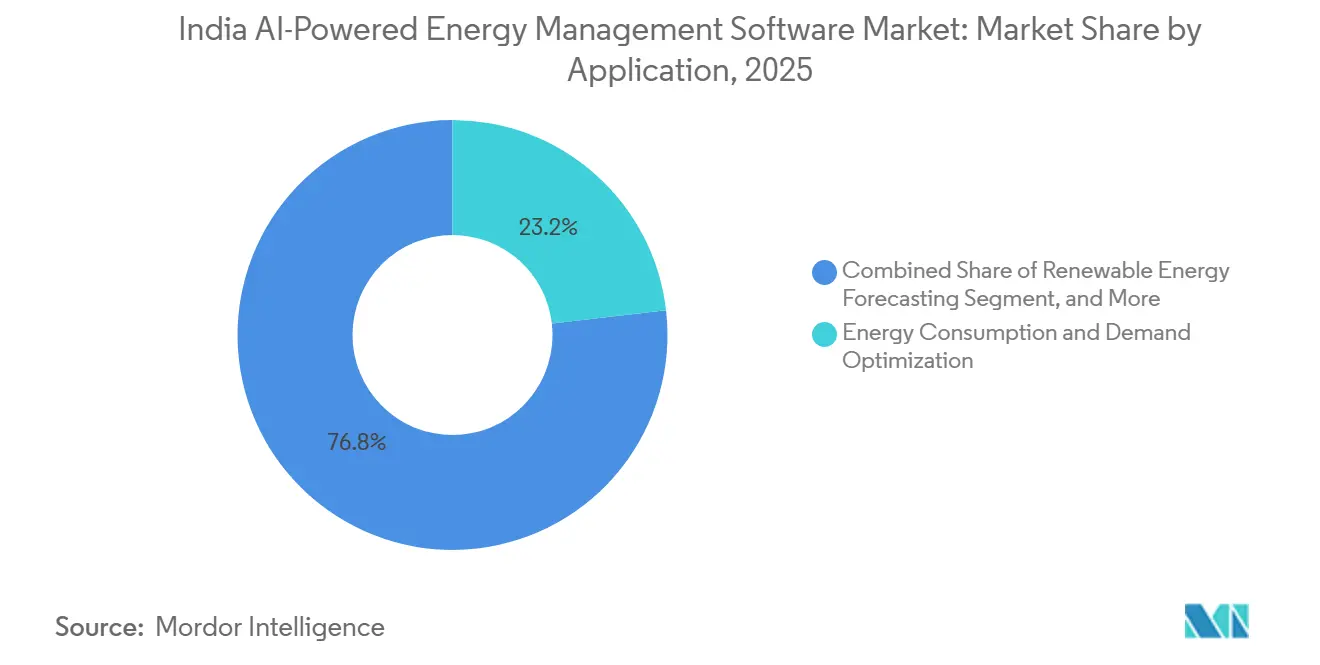

- By application, energy consumption and demand optimization accounted for 23.16% of the India AI-powered energy management software market size in 2025, while renewable energy forecasting and integration are projected to advance at a 25.71% CAGR through 2031.

- By end user, utilities held 35.12% of the India AI-powered energy management software market share in 2025, while industrial facilities are projected to grow at a 25.82% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Energy Tariffs and Peak-Demand Charges Across Commercial Facilities | +4.5% | National, with early concentrated gains in Maharashtra, Tamil Nadu, and Karnataka | Short term (≤ 2 years) |

| Smart Meter Rollout Expands High-Frequency Energy Data Availability | +4.0% | National, with early gains in Bihar, Assam, Chhattisgarh, and Uttar Pradesh | Medium term (2-4 years) |

| Net-Zero Commitments Push Continuous Energy Optimization Programs | +3.8% | National, with early adoption in Bengaluru, Hyderabad, and Pune | Medium term (2-4 years) |

| Expansion of Distributed Energy Resources Raises Need for AI Orchestration | +3.2% | National, with strong momentum in Gujarat, Rajasthan, and Andhra Pradesh | Long term (≥ 4 years) |

| Retrofit-Heavy Building Stock Creates Large Software-First Efficiency Opportunity | +2.5% | National, with early gains in Delhi NCR, Mumbai, and Bengaluru commercial corridors | Medium term (2-4 years) |

| Demand for Remote Monitoring in Multi-Site Enterprises Accelerates Adoption | +2.2% | National, concentrated in large industrial zones across Gujarat, Maharashtra, and Tamil Nadu | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Energy Tariffs and Peak-Demand Charges Across Commercial Facilities

Electricity tariff revisions across states have made energy costs harder to manage for large commercial and industrial users. The Tamil Nadu Electricity Regulatory Commission raised industrial tariffs by 3.4% to INR 7.5 per kWh (USD 0.079 USD per kWh) and increased demand charges to INR 608 per kVA (USD 6.43 per kVA) per month for FY2026, effective July 1, 2025.[1]Ministry of New and Renewable Energy, “Overview, Renewable Energy Installed Capacity,” Ministry of New and Renewable Energy, nghm.mnre.gov.in Similar pressure has been building in other high-tension consumer categories across major industrial states, making energy optimization software easier to justify in budget discussions. The direct value comes from AI-led load shifting during 15-minute peak intervals, because that is where India’s tariff structure creates the sharpest billing exposure. In the India AI-Powered Energy Management Software Market, this means demand optimization remains one of the quickest paths to visible savings for commercial campuses and factories.

Smart Meter Rollout Expands High-Frequency Energy Data Availability

India’s smart meter rollout has created a much larger base of interval-level consumption data for utilities and service providers. By December 2025, 52.8 million smart meters had been deployed, and the broader distribution capex pipeline tied to sector modernization reached INR 11.2 trillion (USD 131 billion). In 2026, the Ministry of Power directed utilities to move AI and ML use cases beyond pilot programs, which pushed demand forecasting, loss analysis, and predictive maintenance into a more operational stage. The gap between sanctioned meters and installed meters has also put pressure on AMI providers, as delayed go-live schedules increase the need for stronger forecasting and analytics support. The 2026 amendment to the meter installation and operation rules also improved interoperability conditions, which matters because model accuracy depends on cleaner, more standardized data flows.

Net-Zero Commitments Push Continuous Energy Optimization Programs

India crossed the 50% non-fossil fuel installed power capacity milestone in 2025, bringing the national clean energy policy closer to operational decisions within companies.[2]Press Information Bureau, “India Achieves 50% Clean Energy Capacity Target in 2025, Five Years Ahead of Schedule,” Press Information Bureau, pib.gov.in The Cabinet-approved NDC for 2031–2035 targets 60% non-fossil electricity capacity and a 47% reduction in emissions intensity from 2005 levels. These commitments are flowing into enterprise reporting through SEBI’s BRSR framework, which is turning energy consumption and efficiency data into an auditable management issue rather than a narrow facilities metric. NITI Aayog’s 2026 scenarios work also highlighted time-of-day tariffs and AI-enabled building electrification as part of the path toward India’s long-term net-zero goal. In the India AI-Powered Energy Management Software Market, this underscores the value of platforms that connect energy optimization with emissions disclosure and internal performance tracking.[3]United Nations Framework Convention on Climate Change, “India Nationally Determined Contribution 2031-2035,” UNFCCC, unfccc.int

Expansion of Distributed Energy Resources Raises Need for AI Orchestration

India added close to 50 GW of renewable energy capacity in 2025, and that expansion is increasing the number of sites that both consume and generate electricity. As rooftop solar, storage, and other behind-the-meter systems spread, distribution assets designed for one-way power flow are facing new operating stress. The agreement between NISE and NLDC on a next-generation hybrid solar forecasting framework shows that forecasting infrastructure is also being upgraded at the national level through AI, satellite inputs, and high-frequency weather models. This is important for the India AI-Powered Energy Management Software Market because utilities and asset owners now need software that can coordinate generation, storage, and demand in near real time. It also explains why DERMS-linked use cases are moving from pilot activity toward larger operational programs in places such as Mumbai, Karnataka, and Tamil Nadu.[4]Honeywell International Inc., “Honeywell and TCS Collaborate to Enhance Autonomous Operations for Buildings and Industries with AI,” Honeywell, honeywell.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy OT and BMS Data Slows Model Deployment | -2.8% | National, with acute impact in older industrial belt states such as Uttar Pradesh, Bihar, and Odisha | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns Limit Cloud Adoption in Critical Sites | -2.3% | National, critical at distribution utilities and transmission entities operating SCADA-enabled substations | Medium term (2-4 years) |

| Weak Internal AI and Energy Analytics Skills Reduce Implementation Velocity | -1.8% | National, with acute skill gaps in Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Long Sales Cycles and Low-Capex Prioritization Delay Enterprise Purchases | -1.5% | National, concentrated in public-sector utilities and state-owned enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy OT and BMS Data Slows Model Deployment

Much of India’s power and large-building infrastructure still runs on older SCADA, BMS, and PLC environments that were not built for smooth IT and OT integration. That creates data normalization issues across sites, vendors, and protocol generations, pushing deployment timelines from weeks to several months. In utilities and large industrial facilities, this problem is more difficult because different generations of control systems often operate side by side, and each one can produce data in a different format. Honeywell’s February 2026 partnership with TCS in India was aimed directly at this problem by combining OT connectivity, cloud modernization, and AI-led operations support. In the India AI-Powered Energy Management Software Market, integration capability has therefore become a core product differentiator rather than an implementation detail.

Cybersecurity and Data Sovereignty Concerns Limit Cloud Adoption in Critical Sites

Cybersecurity policy is now affecting software architecture decisions across the power system. Grid-connected entities are operating under tighter cybersecurity governance requirements, which have made some buyers more cautious about moving sensitive operational data into public cloud environments. The MNRE’s July 2025 compliance rules under PM Surya Ghar required inverter communication devices to connect only to national servers, which made local data handling a more visible issue. Draft sovereign cloud rules under MeitY have added to that caution by treating operational data from the energy sector as sensitive. As a result, the India AI-Powered Energy Management Software Market is seeing stronger demand for hybrid and edge-ready products that let buyers keep critical data closer to the asset.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Platform Stickiness in Enterprise Deployments

Software accounted for 66.21% of India AI-Powered Energy Management Software Market in 2025, keeping the category centered on platform-led buying patterns rather than isolated tools. Buyers have favored software because it enables demand forecasting, asset diagnostics, and renewable integration to be housed in a single operating layer rather than separate applications. This matters because utilities and large industrial groups typically want a single system of record for energy performance across multiple sites. The recurring-revenue nature of software contracts also fits the preference for long-term platform control in regulated and energy-intensive sectors.

Services are projected to expand at a 25.47% CAGR through 2031, indicating that implementation work is becoming increasingly important as deployments move into more complex operating environments. Companies that have already purchased software increasingly need managed analytics, integration support, and site-level model tuning before operational value becomes visible. The Honeywell and TCS partnership reflected that shift by treating convergence between legacy OT and newer cloud analytics as an ongoing service task rather than a one-time setup. BEE’s ECBC-linked metering and management requirements also create a baseline that vendors can build on through software upgrades and associated services.

By Deployment Mode: Cloud Leads as Hybrid Deployment Closes the Architecture Gap

Cloud-based deployment accounted for 56.17% of India AI-Powered Energy Management Software Market in 2025, supported by lower upfront costs and easier access to analytics-intensive computing. Commercial building operators and mid-sized industrial users have leaned toward the cloud because it shortens deployment time and avoids heavy local infrastructure investment. For the market, that has helped cloud become the default option in less sensitive operating environments where speed and cost carry more weight than strict data control. The growing presence of hyperscale cloud infrastructure in India has also made cloud-based delivery more practical for software vendors that rely on real-time analytics.

Hybrid deployment is expected to grow at a 25.58% CAGR through 2031 because it addresses the tension between cloud efficiency and local control. In regulated power and utility settings, buyers often want sensitive OT data to remain on-site while less critical analytics workloads move to the cloud. That is why architecture flexibility is becoming a procurement requirement, especially for discoms, generators, and transmission-linked users. ABB’s 2026 launch of BuildingPro Suites, which supports edge, on-premises, and cloud deployment, reflected this hybrid-first direction.

By Application: Demand Optimization Anchors Adoption as Renewable Forecasting Accelerates

Energy consumption and demand optimization accounted for 23.16% of India AI-Powered Energy Management Software Market in 2025, making it the largest application area. The segment has stayed in front because it offers the clearest financial return under tariff structures that place real pressure on peak demand. In many facilities, AI-based load shifting can lower bills without waiting for major hardware replacement or broader grid upgrades. That shortens approval cycles and keeps this use case central to the market.

Asset performance and predictive maintenance remained the next major application area, as India continues to operate a broad installed base of generation and industrial assets that require closer monitoring. Toshiba JSW’s 2025 contract for EtaPRO deployment across up to 165 NTPC thermal and renewable plants showed how predictive maintenance software is now being adopted at a national scale. Renewable energy forecasting and integration is projected to grow at a 25.71% CAGR through 2031, driven by the July 2025 requirement for grid-connected solar and wind plants to submit compliance forecasts to State Load Despatch Centers. Energy trading, pricing, and smart grid and DER management are also gaining ground, with platforms such as Vidyut AI linking grid, weather, and smart meter data to enable faster operational decisions.

By End User: Utilities Drive Scale While Industrial Facilities Lead Growth Velocity

Utilities held 35.12% of India AI-Powered Energy Management Software Market share in 2025, reflecting their scale of buying and policy importance. The Ministry of Power’s push for AI and ML use cases in discom operations has made utilities an anchor customer for vendors seeking long-term contracts and larger deployment footprints. In this market, utility-led demand is especially important because software procurement by a few large entities can influence standards, integration practices, and reference cases across the sector. Adani Energy Solutions’ acquisition of IntelliSmart for INR 30.5 billion (USD 357 million) demonstrated that smart metering and analytics capabilities are now strategic enough to support major utility-focused M&A activity.

Industrial facilities are projected to grow at a 25.82% CAGR through 2031, driven by higher tariff pressure, stronger disclosure requirements, and a rising need to coordinate captive renewable assets with plant demand. Commercial buildings also hold a significant share because connected loads above 100 kW fall within ECBC-linked efficiency and metering expectations, and many existing sites are good candidates for software deployment through retrofit. Residential buildings remain smaller today, but demand response use cases are becoming more visible as smart meters spread into prosumer settings. Tata Power’s Mumbai program targeting 200 MW of peak load reduction through the AutoGrid platform shows how residential and distributed flexibility can become part of broader utility demand management.

Geography Analysis

The India AI-Powered Energy Management Software Market shows different demand patterns across states because grid maturity, tariff design, and renewable penetration vary widely within the national power system. Northern and eastern states, where public-sector utilities remain central, and RDSS implementation has progressed unevenly, are still closer to the platform evaluation and pilot stages in many cases. Bihar and Assam showed stronger progress in smart meter installations than several larger states, suggesting uneven readiness for data-driven software adoption nationwide. Falling AT&C losses, from 21.9% in FY2021 to 15% in FY2025, have also helped state utilities see the value of digital infrastructure with more confidence.

Southern and western India remain the most commercially active areas. Karnataka, Tamil Nadu, Maharashtra, and Gujarat combine large industrial electricity demand, dense commercial building clusters, and stronger adoption of time-of-day pricing for high-tension users. The TNERC tariff revision, which took effect on July 1, 2025, including demand charges of INR 608 per kVA per month, shows why southern manufacturing and commercial clusters are moving faster toward software adoption. Tata Power’s Mumbai demand response program and Adani Electricity’s use of AspenTech’s SCADA and ADMS platform at the Hiranandani Powai network operations center demonstrate that western India is operating at a scale beyond pilot. Schneider Electric’s January 2026 investment of INR 6.23 billion (USD 72.8 million) in Telangana further shows that global vendors expect stronger demand from India’s southern operating base.

Renewable-heavy states are creating a separate layer of demand. Rajasthan, Gujarat, and Andhra Pradesh host large solar and wind capacity, and the CEA-linked forecasting requirement has made compliance-oriented forecasting tools more necessary in these states. The NISE and NLDC forecasting initiative, which combines weather models, satellite inputs, and AI-based nowcasting, shows that the national support system for renewable forecasting is also being strengthened. As India moves toward its 2035 non-fossil capacity target, western and southern renewable hubs are likely to need software that can manage generation, storage, grid coordination, and prosumer participation together.

Competitive Landscape

The India AI-Powered Energy Management Software Market is fragmented at the top, with Schneider Electric, Siemens, Honeywell, and ABB competing alongside IBM, Microsoft, SAP, and Oracle. Global automation firms still hold an advantage in sites where OT credibility, system integration depth, and relationships with installed hardware matter most. Enterprise software firms remain relevant because they already sit inside many large customer IT environments and can extend into energy management through existing data and analytics layers. At the same time, the market remains fragmented below the top tier because local specialists can move faster on tariff engines, utility integration, and India-specific deployment needs.

Schneider Electric’s July 2025 move to acquire the remaining 35% stake in its Indian subsidiary for EUR 5.5 billion (USD 5.89 billion) showed that India is being treated as a strategic operating hub rather than a peripheral sales market. Honeywell’s February 2026 partnership with TCS demonstrated a second route to scale, enabling vendors to deepen implementation and enhance OT-IT integration capabilities without waiting for the slower organic buildup. ABB’s April 2026 integration of Genix with NVIDIA Omniverse and Microsoft Azure showed that product competition is also moving toward digital twin visualization and richer operational context. These moves suggest that leadership in the Indian AI-Powered Energy Management Software Market will depend on both software capabilities and the ability to align with increasingly stringent customer architecture requirements.

Architecture alignment is becoming one of the clearest competitive dividing lines. Buyers at critical sites increasingly prefer hybrid, edge, or private cloud options because public cloud alone may not satisfy cybersecurity and data residency expectations. That is why vendors that can combine local OT processing with cloud analytics are improving their position. Capability-building is also happening through acquisitions, including Bidgely’s March 2025 acquisition of Grid4C, which brought consumer-side disaggregation and grid-side predictive analytics into one utility AI stack. Open areas remain in energy trading intelligence, residential prosumer response, and carbon accounting linked to BRSR disclosures, as current portfolios do not yet fully cover those needs.

India AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Schneider Electric SE

Johnson Controls International plc

Honeywell International Inc.

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Adani Energy Solutions announced the acquisition of IntelliSmart Infrastructure for INR 30.5 billion (approximately USD 357 million), positioning itself as India's largest smart metering platform and signaling aggressive utility-sector investment in AI-enabled metering and analytics software.

- April 2026: Tata Power announced enterprise-wide adoption of the Databricks Data Intelligence Platform to build a future-ready data and AI infrastructure, enabling intelligent grid management, accurate renewable energy forecasting, advanced power planning, and the deployment of Genie, a natural-language AI agent for operational analytics, the initiative marks one of India's largest utility-sector AI platform investments.

- April 2026: ABB integrated its Genix Industrial IoT and AI Suite with NVIDIA Omniverse and Microsoft Azure at Hannover Messe 2026, advancing ABB Genix beyond traditional digital twins to deliver immersive 3D operational visualization for energy and industrial asset management.

- March 2026: Tata Power and Salesforce announced a strategic collaboration deploying Agentforce AI agents across Tata Power's rooftop solar, electric vehicle charging, and smart home solutions businesses, creating an AI-powered customer and partner engagement layer tied to clean energy management and utility-scale digital transformation.

India AI-Powered Energy Management Software Market Report Scope

The India AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions include predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The India AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the size of the India AI-powered energy management software market?

The India AI-powered energy management software market was valued at USD 154.3 million in 2025 and is projected to reach USD 563.2 million by 2031, at a 24.43% CAGR during 2026-2031.

What is driving adoption of AI-based energy management software in India?

Higher electricity tariffs, rising peak-demand charges, smart meter expansion, renewable integration, and tighter energy reporting requirements are the main demand drivers.

Which application area leads current demand in India?

Energy consumption and demand optimization led with a 23.16% share in 2025 because it gives facilities a direct and measurable path to lower electricity bills.

Which end-user group is growing the fastest?

Industrial facilities are projected to grow at a 25.82% CAGR through 2031 as manufacturers deal with tariff pressure, disclosure obligations, and captive renewable coordination.

Why is hybrid deployment gaining importance in India?

Hybrid deployment is projected to grow at a 25.58% CAGR because it balances cloud analytics efficiency with the need to keep sensitive operational data on-site.

How competitive is the vendor landscape in India?

Competition is moderate to high, with global automation companies, enterprise software vendors, and local specialists all active, while no single group fully controls the field.

Page last updated on: