France AI-powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

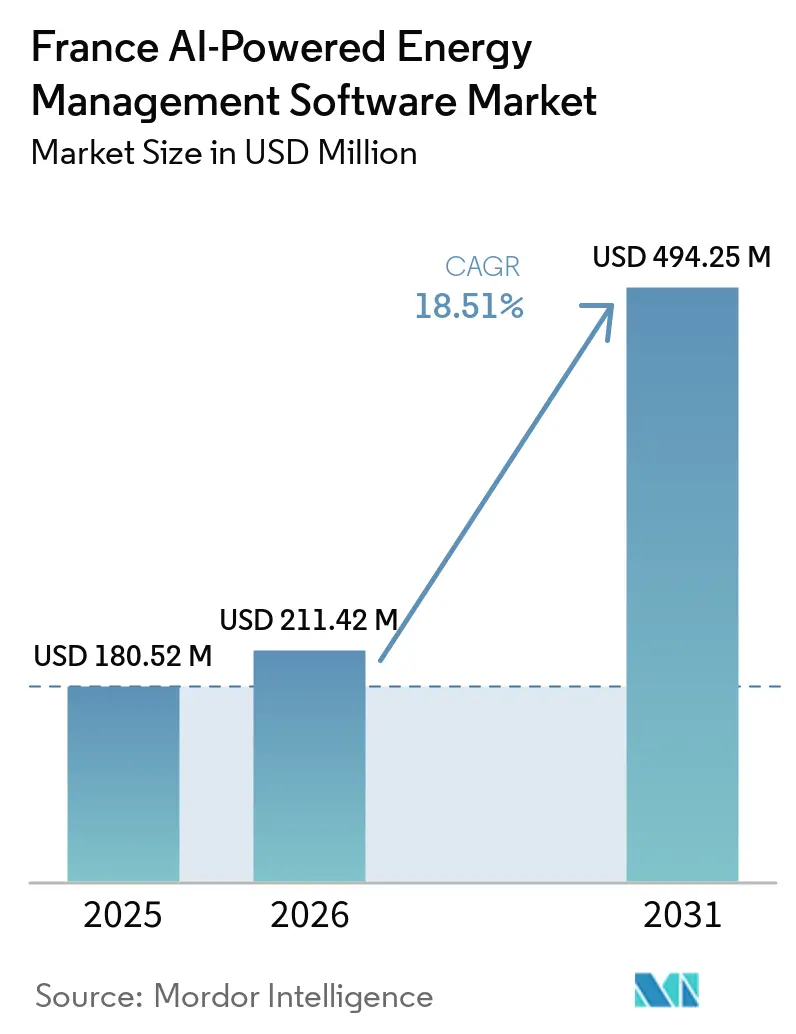

| Base Year Market Size (2025) | USD 180.52 Million |

| Market Size (2026) | USD 211.42 Million |

| Market Size (2031) | USD 494.25 Million |

| Growth Rate (2026 - 2031) | 18.51% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France AI-powered Energy Management Software Market Analysis by Mordor Intelligence

The France AI-powered Energy Management Software Market size is expected to increase from USD 180.52 million in 2025 to USD 211.42 million in 2026 and reach USD 494.25 million by 2031, growing at a CAGR of 18.51% over 2026-2031. The January 1, 2026, expiry of the ARENH mechanism and the May 29, 2026, EPBD transposition deadline have made energy software both a compliance tool and a cost-control tool for French buyers. France also has a dense regulatory stack, including décrets tertiaires, BEGES, DPE, and CSRD-linked reporting, which supports demand across large enterprises, commercial property operators, and public-sector users. The 2026 deadline for declaring 2025 energy consumption data on the ADEME OPERAT platform keeps reporting workflows active and makes it harder to delay software integration. The January 2026 revision to the DPE primary energy factor for electricity has sparked a second wave of recalibration and re-audit demand, favoring vendors that can pair digital monitoring with field execution. Rising intra-day grid volatility is also improving the payback case for AI-based demand scheduling, while competition is intensifying between French specialists and global OEM platforms that now target the same buyer groups.

Key Report Takeaways

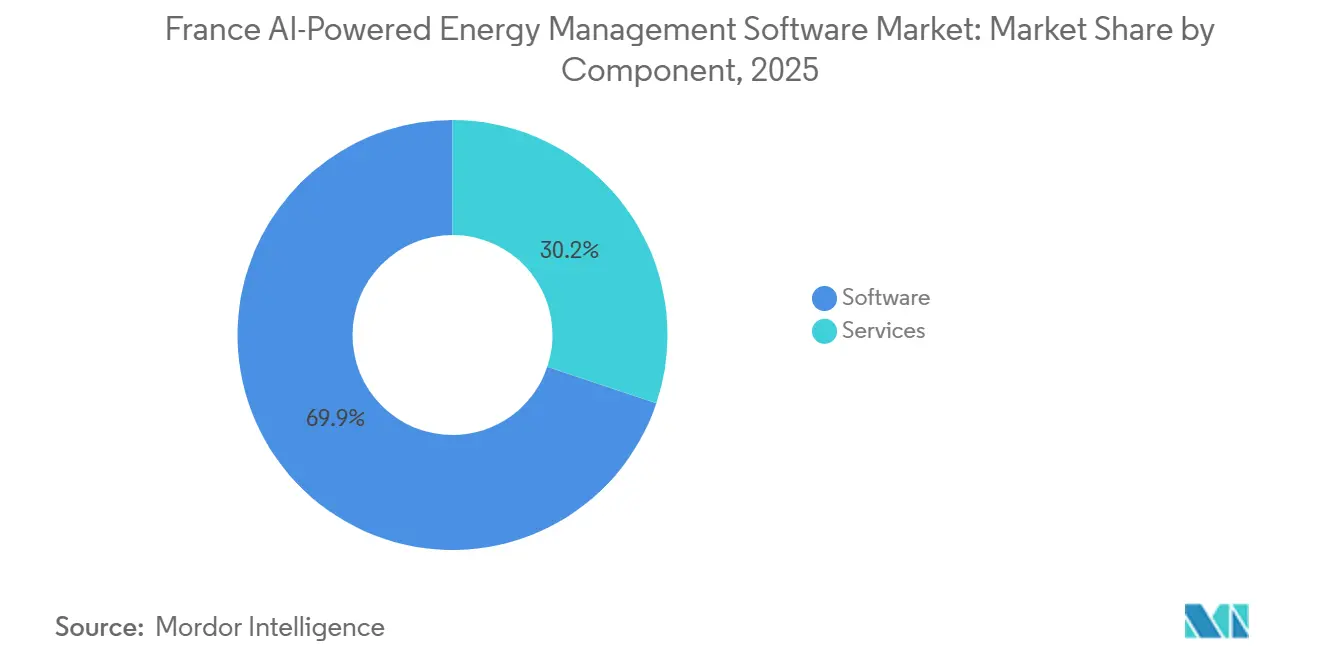

- By component, software held 69.85% of the France AI-powered Energy Management Software Market share in 2025, while services are projected to expand at a 19.23% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 66.41% of the market in 2025, while hybrid deployment is expected to grow at a 20.34% CAGR through 2031.

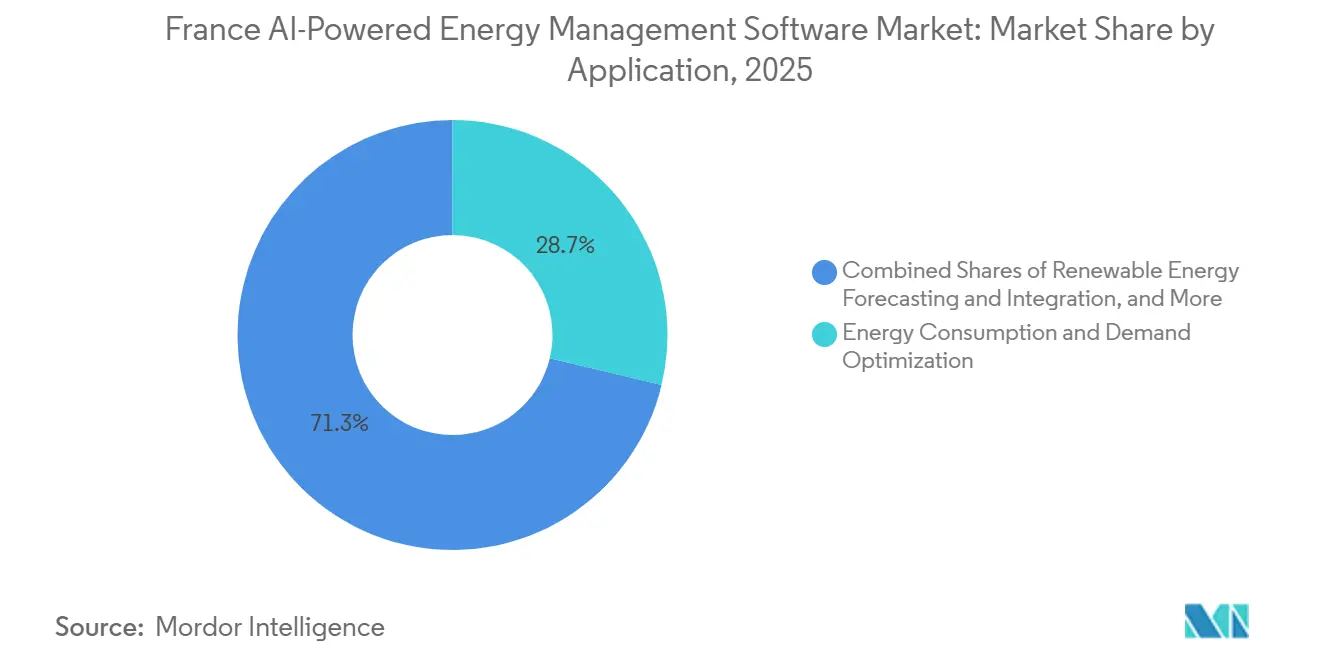

- By application, energy consumption and demand optimization captured 28.74% of the market in 2025, while energy trading, pricing, and market intelligence is projected to expand at a 21.42% CAGR through 2031.

- By end user, utilities held 30.12% share in 2025, while commercial buildings are expected to grow at a 19.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France AI-powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Cost Pressure Across Commercial and Industrial Sites | +4.5% | National, with early gains in Île-de-France, Auvergne-Rhône-Alpes, and Grand Est | Short term (≤ 2 years) |

| EU Building Performance Compliance Deadlines Accelerating Software Adoption | +3.8% | EU-wide, centered on France transposition deadline May 2026 | Short term (≤ 2 years) |

| AI-Enabled Peak Load Forecasting Reducing Grid and Site-Level Penalty Exposure | +3.2% | National, spill-over to cross-border EU balancing mechanism participants | Medium term (2-4 years) |

| Edge AI and Meter Data Granularity Improving Real-Time Optimization | +2.5% | Global, APAC core, spill-over to France and EU | Medium term (2-4 years) |

| Scope 3 and Carbon Reporting Automation Increasing Demand for Energy Intelligence | +1.8% | EU-wide, Île-de-France and major industrial corridors | Medium term (2-4 years) |

| Retrofit-Led Digitization of Existing Building Portfolios | +1.2% | National, with early gains in Paris, Lyon, and Marseille | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Cost Pressure Across Commercial And Industrial Sites

The January 1, 2026, expiry of the ARENH mechanism replaced a regulated nuclear price ceiling with the versement nucléaire universel model, which no longer provides a fixed volume or price guarantee for commercial and industrial electricity buyers in France.[1]Veille de Presse, “Électricité Des Entreprises En 2026: Après L'ARENH, Comment Sécuriser Sa Facture,” Veille de Presse, veilledepresse.com The Commission de Régulation de l'Énergie set nuclear production costs at EUR 60.3/MWh (USD 68.14/MWh) at the 2026 EUR 1 (USD 1.14) rate for the 2026-2028 period, while wholesale baseload prices in 2026 have stabilized within a band that keeps procurement costs exposed to market conditions. Large industrial sites on Tarif Vert, above 250 kVA, face supply costs of EUR 0.12 to EUR 0.15/kWh HT (USD 0.136 to USD 0.170/kWh), and the 2026 accise rate of EUR 26.58/MWh (USD 30.41/MWh)means that a 20 GWh site carries EUR 531,600 (USD 600,708) in annual tax burden before any peak-load optimization.[2]Capitole Énergie, “Tarif Professionnel EDF: Grille D'Électricité 2026,” Capitole Énergie, capitole-energie.com This cost structure gives AI-driven peak-shift scheduling a direct, measurable role in reducing avoidable electricity costs at the site level. In the France AI-powered Energy Management Software Market, the removal of a regulated floor has changed avoided peak demand from a soft efficiency benefit into a hard financial return for commercial buyers. That change has shortened evaluation cycles because buyers now treat scheduling, forecasting, and load orchestration as procurement tools rather than optional sustainability add-ons.

EU Building Performance Compliance Deadlines Accelerating Software Adoption

The revised EPBD entered into force on May 28, 2024, and requires member states to transpose it by May 29, 2026, with minimum energy performance standards that target the 16% worst-performing non-residential buildings by 2030 and the 26% worst-performing by 2033.[3]European Commission, “Energy Performance of Buildings Directive,” European Commission Energy, energy.ec.europa.eu France also transposed the EU Energy Efficiency Directive through Law No. 2025-391 of April 30, 2025, which added a 3% annual renovation requirement for public-sector buildings and tightened audit obligations for major operators. The European Commission released an implementation support package on June 30, 2025, including a delegated regulation, an implementing regulation, and guidance on minimum energy performance standards and the Smart Readiness Indicator. France's OPERAT platform has supported direct API connections for EMS software since 2023, turning annual reporting into a recurring software integration point for building operators. In the France AI-powered Energy Management Software Market, each OPERAT-linked declaration cycle deepens switching costs because the reporting workflow becomes embedded in building operations. That gives early vendors with compliant reporting modules a durable advantage through 2031 because removal becomes harder once reporting, audit, and optimization tools sit in the same process chain.

AI-Enabled Peak Load Forecasting Reducing Grid And Site-Level Penalty Exposure

Law No. 2025-391 of April 30, 2025, requires electricity generation assets above 10 MW, including renewable installations, to participate in France's balancing mechanism from January 1, 2026.[4]Pexapark, “France Mandates Renewables Participation in Balancing Mechanism From 2026,” Pexapark, pexapark.com This reform extends the software buying case from utility trading desks to industrial and commercial operators that run on-site renewable generation and now need real-time forecasting and activation interfaces. RTE's OpenSTEF pipeline already provides an open-source short-term forecasting path that combines historical grid data, weather inputs, and market pricing into automated load models. The European Parliament's 2025 brief on AI and the energy sector stated that AI processing of meter and sensor data improves the accuracy of demand response activation and supports more resilient grid operations under weather and cyber stress. In the French AI-powered energy management software market, operators that once optimized only consumption now also need to shape injection profiles, expanding the software's role from cost control to revenue-linked market participation. That shift supports demand for forecasting, dispatch, pricing, and grid response functions in the same platform stack.

Edge AI And Meter Data Granularity Improving Real-Time Optimization

France's Linky smart meter base, combined with Zigbee-based Émetteur Radio Local units, is turning installed meters into local data hubs that can communicate directly with in-building equipment at near-instant latency. This reduces the need for cloud round-trips before an optimization command is issued, making local inference more practical in buildings and industrial sites. The France AI-powered Energy Management Software Market is therefore moving toward compact edge models that can process 15-minute data streams on gateways with sub-second response times. Kerlink launched the Wirnet iStation M2 gateway in March 2026 with an i.MX 8XLite CPU and upgraded RAM to support local edge computing in remote operating environments such as islands, mines, and rural infrastructure. That matters because low-latency local computing is well-suited to sites where connectivity, sovereignty, or operational continuity prevent full reliance on public cloud workflows. In the France AI-powered Energy Management Software Market, sub-minute data handling has become a commercial differentiator, as buyers now compare local execution capability rather than only analytics depth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy Building and Industrial Control Systems | -2.5% | Global | Short term (≤ 2 years) |

| Data Quality, Meter Coverage, and Interoperability Constraints | -1.8% | National, with concentration in rural areas and secondary cities | Medium term (2-4 years) |

| Cybersecurity, Data Sovereignty, and OT Risk Concerns | -1.2% | EU-wide, with compliance focus on ANSSI-certified operators and NIS2 scope | Medium term (2-4 years) |

| Payback Sensitivity in Small Sites and Fragmented Facility Portfolios | -0.8% | National, SME-heavy regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy Building And Industrial Control Systems

A major barrier in the France AI-powered Energy Management Software Market is the need to connect modern AI tools with legacy BMS, DCS, and SCADA systems that still operate on older protocols such as Modbus, BACnet, DNP3, and OPC-UA. Legacy estates often lack modern API layers, which means software deployments still start with protocol mapping, middleware work, and site-specific integration logic. Siemens has continued to position its autonomous building software around practical brownfield transition paths, reflecting the fact that much of the French installed base still needs hybrid architectures rather than full replacement. Procurement also slows because large industrial buyers often require third-party system integrators, which raises project costs and spreads accountability across more parties. The input indicates that integration overhead can absorb 40-60% of total project budgets in brownfield cases, which weakens the payback case at the bid stage. Vendors with middleware, pre-certified adapters, or established building controls partnerships therefore enter French chemicals, automotive, and metals projects with a clear commercial edge.

Data Quality, Meter Coverage, and Interoperability Constraints

France's Linky rollout has improved sub-hourly visibility in urban and peri-urban areas, but machine-level and production-line sub-metering remains uneven in older industrial facilities. ADEME-linked OPERAT reporting cycles have also exposed recurring data declaration gaps and non-homogeneous measurement periods among tertiary building operators. That means many buyers still need to solve basic data completeness before they can rely on AI models for optimization or forecasting. Communication standards such as LoRaWAN, NB-IoT, Zigbee, BACnet, and KNX create fragmented data environments that require normalization before site-level models can learn consistently. Fludia's FM442e sensor addresses part of this issue by enabling optical reading of legacy electricity meters through NB-IoT or LTE-M with direct MQTT upload to EMS platforms. In the France AI-powered Energy Management Software Market, vendors that bundle sensing, connectivity, and platform analytics avoid much of the data-quality problem that general-purpose software still has to solve site by site.[5]Fludia, “FM442e, NB-IoT/LTE-M Sensor, Electricity,” Fludia, fludia.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads, Services Expand Execution

Software captured 69.85% of the market in 2025, and it held 69.85% of the France AI-powered Energy Management Software Market share because buyers still start with platforms that combine data ingestion, AI analytics, reporting, and decarbonization planning in a single interface. METRON's software layer is deployed on more than 25,000 sites globally, including 250 industrial sites across more than 30 countries, which shows the scale advantage of established analytics platforms. The Dalkia Analytics, powered by the METRON model, also shows how software gains distribution strength when paired with EDF Group's large service network.[6]METRON, “METRON Et Dalkia Prolongent Leur Partenariat Stratégique Pour Accélérer La Performance Énergétique Des Industriels Européens,” METRON, metron.energy In the France AI-powered Energy Management Software Market, compliance-linked software remains sticky because reporting modules tied to OPERAT, BEGES, and CSRD workflows are hard to replace once they are embedded. That stickiness supports premium pricing and lower churn for vendors that already localize around French and EU reporting requirements.

Services are the fastest-growing component, and the France AI-powered Energy Management Software Market size for services is projected to expand at a 19.23% CAGR between 2026 and 2031 as buyers move beyond license purchase into continuous performance delivery. Honeywell's February 2026 partnership with Tata Consultancy Services shows how vendors are combining AI platforms with integration and consulting capabilities to support IT-OT convergence in large building and industrial environments. METRON and Dalkia reported that their Decarb Fast Track program across 60 industrial sites in 8 European countries identified more than 250 decarbonization projects with potential savings of 190,000 tonnes of CO₂, while more than 100 ongoing projects had already avoided 60,000 tonnes of CO₂. Those results show why French buyers increasingly want implementation support, measurement validation, and operational follow-through, not only dashboards and alerts. The France AI-powered Energy Management Software Market is therefore entering a phase where service depth can shape renewal rates as much as product functionality.

By Deployment Mode: Cloud Holds The Base, Hybrid Gains Ground

Cloud-based deployment held a 66.41% share in 2025, accounting for 66.41% of the France AI-powered Energy Management Software Market, as commercial property operators and medium-sized facility managers still favor SaaS speed and lower setup burden. The France AI-powered Energy Management Software Market still shows a strong preference for the cloud among buyer groups that do not have high OT isolation requirements. Hybrid deployment is the fastest-growing mode, with a 20.34% CAGR, because many regulated industrial users need local processing before selectively uploading data to the cloud. Industrial operators working under strict cybersecurity and operational continuity rules treat local data handling as a compliance need rather than an architectural preference. On-premises deployment remains relevant for a narrower group, including nuclear subcontractors, chemical manufacturers, and grid infrastructure operators, where isolated networks still shape procurement decisions.

Hybrid deployment is projected to grow at a 20.34% CAGR through 2031, indicating that the market is not moving away from the cloud but toward mixed edge-cloud architectures that address real site constraints. Schneider Electric introduced EcoStruxure Foresight Operation in November 2025 with a design that unifies energy, power, and building systems and claims a 40% reduction in engineering workflow time, together with a 50% improvement in operational efficiency. Siemens also continued to present its building software strategy around the shift from smart to autonomous buildings, underscoring the need for brownfield-friendly digital layers rather than abrupt infrastructure replacement. These moves show that major vendors now treat hybrid architecture as a core product requirement in France, especially when buildings and plants carry older control infrastructure. The vendor that closes the OT gap without reducing analytics depth will hold a stronger position in large regulated accounts through 2031.

By Application: Demand Optimization Leads, Trading Tools Grow Fast

Energy consumption and demand optimization accounted for 28.74% of the market share in 2025, as most buyers still begin with visibility, monitoring, and direct efficiency control before adopting more advanced market-facing functions. That installed base matters because measurement-led adoption keeps optimization software as the entry point for broader platform expansion in the France AI-powered Energy Management Software Market. The European Parliament identified predictive maintenance as a priority AI use case in the energy sector, which supports adjacent demand for asset performance applications that sit close to energy monitoring and control. CRE also called for the accelerated deployment of flexible connection standards for batteries and solar projects, underscoring the need for smart grid and distributed energy resource management software. Renewable energy forecasting and integration are gaining ground among utility and industrial prosumers because balancing obligations now requires more accurate site- and asset-level predictions.

Energy trading, pricing, and market intelligence is projected to grow at a 21.42% CAGR through 2031, which makes it the fastest-growing application in this market. The main demand signal is no longer limited to specialist trading desks because industrial consumers with on-site generation now need pricing and dispatch tools to manage both consumption and injection. RTE's OpenSTEF model shows that forecasting frameworks once used around grid operations can now inform enterprise-level software workflows as well. In the France AI-powered Energy Management Software Market, the boundary between energy management and market participation software is narrowing as buyers ask for a single platform to monitor load, forecast output, and respond to price signals. Vendors that combine optimization, forecasting, and market intelligence functions are therefore better placed to capture the fastest-expanding application demand.

By End User: Utilities Hold Scale, Commercial Buildings Advance Fast

Utilities held a 30.12% share in 2025, meaning they remained the largest end-user group in the France AI-powered Energy Management Software Market, as grid-facing analytics, demand response orchestration, and network visibility continued to anchor software demand. RTE's OpenSTEF pipeline confirms that utility-grade AI forecasting already has a validated operational role in French power system management. Industrial facilities still represent an important demand pool, but legacy DCS and SCADA estates often require middleware and long integration cycles of 6-18 months before the software delivers full value. Residential buildings remain the smallest end-user segment at present because adoption is still in pilot mode. The SmartCORE project in Les Pays de Vilaine plans a demand flexibility experiment involving 450 households and 50 buildings in the second half of 2026, demonstrating that software-mediated residential participation is becoming more practical at the local level.

Commercial buildings are projected to grow at a 19.12% CAGR through 2031, making them the fastest-growing end-user group in the France AI-powered Energy Management Software Market. Their momentum comes from overlapping décret tertiaire deadlines, Scope 3 reporting pressure, and EPBD-led renovation requirements that are more immediate for large real estate portfolios than for many industrial sites. BeeBryte's rollout of building technical management systems across 60 Intermarché retail stores shows how standardized commercial assets can support multi-site AI deployment at repeatable scale. Commercial buildings also move faster because their infrastructure is often newer and their procurement cycles are shorter than in brownfield industrial environments. That combination reduces integration friction and improves time-to-revenue for vendors that focus on portfolio-style deployment.

Geography Analysis

The France AI-powered Energy Management Software Market was valued at USD 211.42 million in 2026 and is expected to reach USD 494.25 million by 2031, which reflects a stronger compliance-led demand structure than in many neighboring European markets. France benefits from domestic frameworks such as the décret tertiaire, BEGES, DPE, and the transposition of the EPBD, which create a deeper policy base for software adoption than a single EU directive could on its own. Germany shares France's industrial energy intensity, but the input indicates that it did not have a binding tertiary building energy consumption reduction framework comparable to décret tertiaire by mid-2026. The UK also sits outside the EPBD and CSRD frameworks after Brexit, which reduces regulatory alignment as a direct software demand trigger relative to France. The France AI-powered Energy Management Software Market has therefore become a reference point for vendors that want to export a compliance-linked go-to-market model into other European countries as those frameworks mature.

France's January 2026 revision to the DPE electricity primary energy factor, which reduced it from 2.3 to 1.9, reclassified part of the building stock and created fresh demand for recalibration and re-optimization work. Île-de-France accounts for a disproportionate share of early adoption because it concentrates large commercial real estate portfolios, major corporate headquarters, and a dense cleantech and AI ecosystem. The Choose France 2026 summit identified AI as the top investment sector and drew record commitments in infrastructure, software, and industrial AI. That matters in this market because new data centers and digital infrastructure assets create additional demand for power, cooling, and software for monitoring and optimization. The France AI-powered Energy Management Software Market is therefore likely to see a second layer of demand from compute-heavy facilities that have tighter operating requirements than standard commercial buildings.

Industrial corridors in Auvergne-Rhône-Alpes, Grand Est, and Hauts-de-France hold the highest concentration of energy-intensive sites outside the Paris region, especially in chemicals, automotive, and metals processing. METRON's deployments for clients such as ArcelorMittal, Safran, and Danone show that industrial expansion is moving into these corridors through national account relationships rather than local pilot-led selling. Rural and secondary cities still lag in sub-metering density and interoperable data infrastructure, which slows adoption in smaller portfolios. Sensor-first models using French-made gateways and remote connectivity can partly narrow that gap, where local programs support deployment economics.

Competitive Landscape

The France AI-powered Energy Management Software Market shows a dual-tier structure with French pure-play vendors on one side and global OEM platform vendors on the other. Local specialists such as Deepki, METRON, BeeBryte, Energisme, SpinalCom, and Ubiant compete with stronger localization around French reporting requirements, French-language support, and faster pilot execution. Global OEMs such as Schneider Electric, Siemens, Honeywell, and Johnson Controls compete with broader installed bases across buildings, power systems, and controls infrastructure. In the French AI-powered energy management software market, this split keeps competition active, as buyers often choose between deep local compliance and broader enterprise platform integration. The market still remains fragmented across many specialized platforms, and the input does not indicate that any single vendor holds a dominant share across all verticals.

Strategic moves in 2025 and 2026 show that vendors are extending beyond software alone and into execution, controls, and algorithm depth. Johnson Controls acquired Nantum AI in April 2026 to strengthen OpenBlue with occupancy-based airflow optimization algorithms and deeper energy-control capabilities. Honeywell and Tata Consultancy Services formed a February 2026 partnership around AI-led IT-OT convergence for building and industrial operations, which added integration strength to Honeywell Forge and related digital tools. Schneider Electric's EcoStruxure Foresight Operation also showed how global vendors are converging energy, power, and building systems into a single AI environment rather than selling separate software layers. These moves raise the competitive bar for smaller vendors because product differentiation now depends on integration depth, execution support, and measurable operational outcomes as much as on analytics alone.

White-space remains visible in industrial sites below EUR 5 million (USD 5.72 million) annual energy spend because long payback periods and integration effort can still block adoption. Mid-market commercial landlords with portfolios of 5 to 50 buildings also remain underserved because they face the same reporting obligations as larger owners but usually lack enterprise-scale IT resources. The France AI-powered Energy Management Software Market is therefore likely to reward vendors that simplify deployment, package services, and reduce the burden of legacy integration without removing regulatory reporting capability. AI capability is now becoming standard across the vendor field, so companies that cannot connect software intelligence with operational delivery are more exposed to pricing pressure over time.

France AI-powered Energy Management Software Industry Leaders

IBM Corporation

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Johnson Controls International plc acquired Nantum AI, a New York-based AI algorithm specialist, to strengthen its OpenBlue digital ecosystem. Nantum AI's proprietary algorithms optimize real-time HVAC airflow based on occupancy signals and have delivered more than 10% energy savings at existing client sites. A first combined OpenBlue-Nantum offering is currently in pilot.

- February 2026: METRON and Dalkia, EDF Group subsidiary, renewed their strategic partnership on February 13, 2026, continuing the "Dalkia Analytics powered by METRON" platform. The Decarb Fast Track program, deployed across 60 industrial sites in 8 European countries, has identified more than 250 decarbonization projects with potential savings of 190,000 tonnes of CO₂. More than 100 ongoing projects have already avoided more than 60,000 tonnes.

- February 2026: Honeywell International Inc. and Tata Consultancy Services, TCS, announced a strategic partnership on February 11, 2026 for AI-led IT-OT convergence in building and industrial operations. The collaboration integrates Honeywell Forge's IoT platform, with AI-powered analytics, dashboards, and OT cybersecurity products, with TCS cloud integration and consulting capabilities, targeting building operators seeking enterprise-wide autonomous operations.

- November 2025: Schneider Electric SE unveiled EcoStruxure Foresight Operation at its Innovation Summit North America on November 18, 2025. The platform unifies energy, power, and building systems in a single AI-powered interface, claiming a 40% reduction in engineering workflow time, a 50% boost in operational efficiency, and a 90% faster resolution of interrelated electrical and mechanical issues. Wider availability is planned for Q3 2026.

France AI-powered Energy Management Software Market Report Scope

The France AI-powered Energy Management Software Market is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Control, Asset Performance, Smart Grid Analytics, Renewable Energy Management, and Energy Trading), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the current and future size of the France AI-powered energy management software space?

It stood at USD 211.42 million in 2026 and is expected to reach USD 494.25 million by 2031, growing at a CAGR of 18.51% over 2026-2031.

What is driving adoption in France right now?

The main drivers are post-ARENH electricity cost exposure, EPBD and décret tertiaire compliance, and the need for better forecasting, reporting, and demand optimization across buildings and industrial sites.

Which component category leads demand?

Software led with 69.85% share in 2025 because buyers still begin with integrated platforms for data ingestion, analytics, compliance reporting, and optimization.

Which deployment model is growing the fastest?

Hybrid deployment is projected to grow at a 20.34% CAGR through 2031 as industrial and critical infrastructure users need local processing with selective cloud connectivity.

Which application area is expanding the fastest?

Energy trading, pricing and market intelligence is expected to grow at a 21.42% CAGR through 2031 as more industrial operators manage both consumption and on-site generation.

Which end-user group offers the strongest growth potential?

Commercial buildings are projected to grow at a 19.12% CAGR through 2031 because reporting deadlines, renovation rules, and repeatable multi-site rollouts create faster buying cycles than many industrial sites.

Page last updated on: