North America Botanical Extracts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

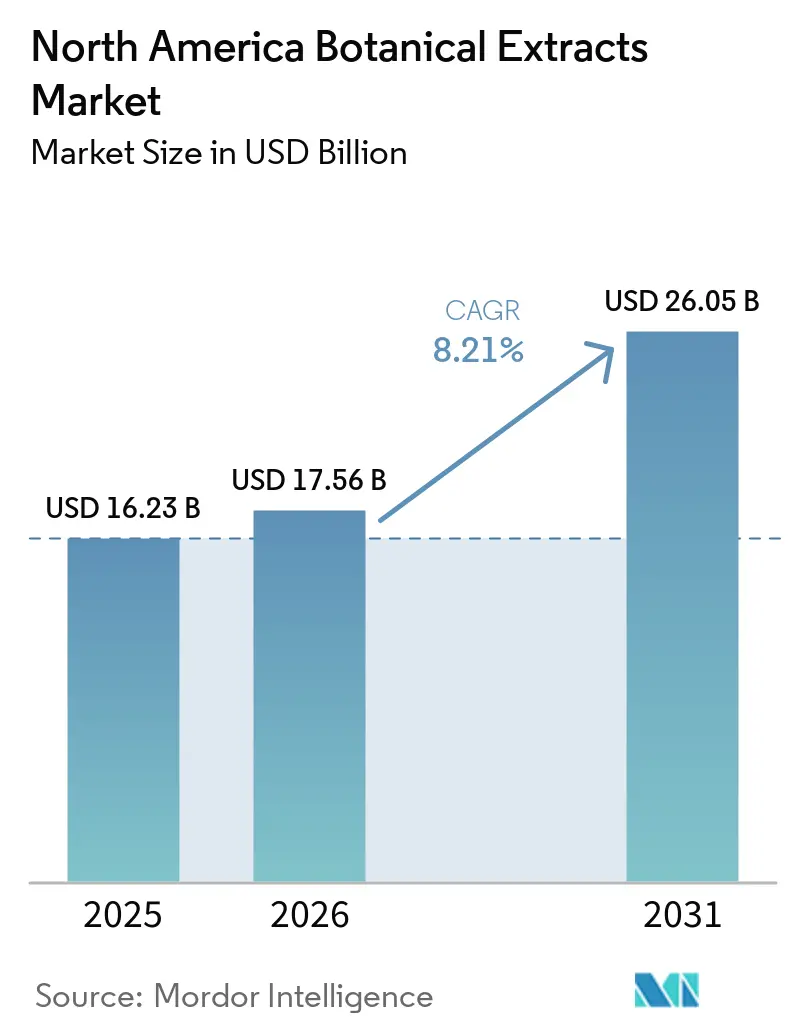

| Base Year Market Size (2025) | USD 16.23 Billion |

| Market Size (2026) | USD 17.56 Billion |

| Market Size (2031) | USD 26.05 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Botanical Extracts Market Analysis by Mordor Intelligence

The North America botanical extracts market size is projected to expand from USD 16.23 billion in 2025 and USD 17.56 billion in 2026 to USD 26.05 billion by 2031, registering a CAGR of 8.21% between 2026 to 2031. Health-conscious buying trends, clean-label preferences, and increased use of plant-based ingredients in food, fragrances, and personal care products are driving this growth. The U.S. has strong demand, while rising manufacturing investments in Mexico help companies position capacities closer to customers and regional supply chains. Companies are adopting eco-friendly extraction methods and stricter compliance measures to meet solvent regulations and safety standards. However, cheaper synthetic alternatives challenge growth in price-sensitive sectors where cost outweighs ingredient origin. These trends favor suppliers with better sourcing control, strong documentation, and broader application support.

Key Report Takeaways

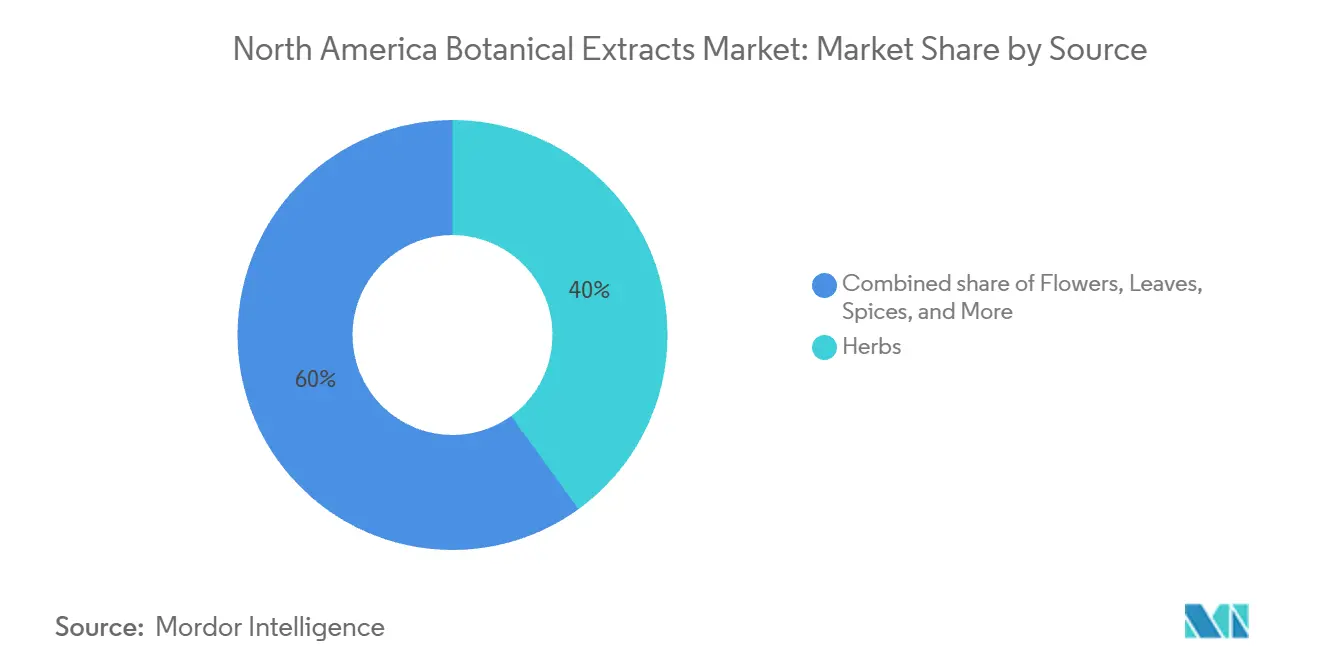

- By source, herbs led with 40.03% revenue share in 2025, while flowers are forecast to expand at a 10.13% CAGR through 2031.

- By technology, solvent extraction held 35.86% share in 2025, while enfleurage is projected to grow at an 8.53% CAGR through 2031.

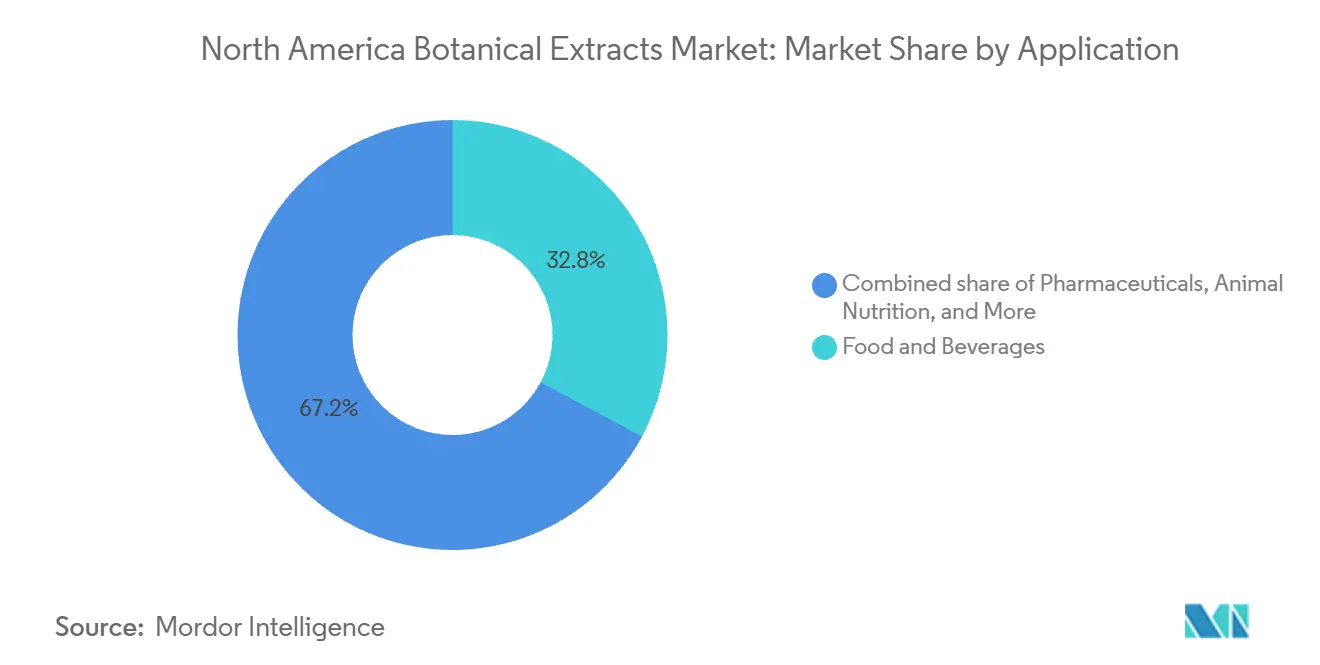

- By application, food and beverages accounted for 32.83% of the North America botanical extracts market size in 2025, while pharmaceuticals are advancing at a 9.01% CAGR through 2031.

- By geography, the United States held 75.46% of the North American botanical extracts market share in 2025, while Mexico is forecast to grow at an 8.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Botanical Extracts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Preference for Clean-Label Products | +1.8% | US, Canada | Short term (≤ 2 years) |

| Growth of the Personal Care and Cosmetics Sector | +1.5% | US, Mexico | Medium term (2-4 years) |

| Technological Advancements in Extraction Methods | +1.2% | US, Canada | Medium term (2-4 years) |

| Demand for Plant-Based and Organic Products | +1.0% | US, Canada | Short term (≤ 2 years) |

| Health-Conscious Population and Wellness Culture | +0.9% | US, Canada, Mexico | Medium term (2-4 years) |

| Integration of Digitalization, AI, and Supply Chain Innovation | +0.7% | US, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Clean-Label Products

Clean-label preferences have grown from a niche trend to a mainstream purchasing standard in packaged food and beverage categories. In North America, the botanical extracts market is experiencing rising demand for natural flavors, colors, and preservation systems. Major brands are speeding up reformulation efforts, replacing synthetic inputs with traceable botanical alternatives. This shift benefits suppliers offering integrated solutions, including raw material sourcing, extraction, and application support. As a result, the gap between standardized extracts and lower-grade commodity materials is widening. Sensient's 2026 expansion plan for natural color production reflects producers' confidence in the continued activity of this conversion cycle during the current planning period.

Growth of the Personal Care and Cosmetics Sector

In North America, the botanical extracts market is witnessing a surge in the commercial value of documented botanical actives, driven by evolving regulations in the beauty and personal care sector. Suppliers are now mandated to bolster traceability, maintain comprehensive safety files, and implement stringent quality controls to align with premium brands. The MoCRA initiative has amplified FDA's oversight on cosmetic safety, facility registrations, and reporting of adverse events, complicating the defense of informal sourcing[1]Source: U.S. Food and Drug Administration, “Modernization Of Cosmetics Regulation Act Of 2022”, fda.gov. In Canada, the framework governing natural and non-prescription health products underscores the significance of quality documentation, especially for products straddling the line between topical care and health claims. Consequently, suppliers boasting standardized actives and advanced delivery systems are finding themselves competing on performance rather than price. This shift is amplifying the demand for clinically validated plant ingredients in skincare and hair care throughout the region.

Technological Advancements in Extraction Methods

Processing technology is becoming a key competitive factor as producers aim to improve quality, yield, and compliance. In North America's botanical extracts market, capital is shifting from traditional solvent systems to cleaner extraction platforms. Stricter EPA regulations on methylene chloride have increased compliance challenges for older methods and accelerated the need for process upgrades[2]Source: U.S. Environmental Protection Agency, “Methylene Chloride, Regulation Under The Toxic Substances Control Act (TSCA)”, federalregister.gov. Advances in sustainable solvents and eco-friendly processing support the adoption of methods suitable for food, supplements, and fragrances. Early adopters can lower regulatory risks while enhancing their sustainability image. This shift is critical as buyers increasingly prefer extraction partners who ensure both performance and process transparency.

Integration of Digitalization, AI, and Supply Chain Innovation

Digital tools are transforming product development cycles and the discovery of new botanical actives. In North America, these advancements are accelerating the process from discovery to formulation and commercialization. For example, Evra Ingredients and Brightseed announced a 2026 collaboration to use AI for plant bioactive discovery, marking a shift from traditional screening methods. Digitalization also impacts supply chain documentation, as buyers increasingly demand verifiable origin and production records. This trend strengthens the position of organized suppliers with major consumer goods and health product manufacturers. Over time, these tools are expected to favor North America's botanical extracts market players who combine data transparency with ingredient performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance and Evolving Standards | -0.8% | US, Canada, Mexico | Short term (≤ 2 years) |

| Availability of Synthetic Substitute Products | -0.6% | US, Canada | Medium term (2-4 years) |

| Fluctuating Raw Material Prices and Supply Volatility | -0.9% | Global, with concentration in US | Short term (≤ 2 years) |

| Quality Inconsistency Across Botanical Sources | -0.5% | US, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance and Evolving Standards

As compliance requirements grow stricter across supplements, cosmetics, and pharmaceutical sectors, larger companies in North America's botanical extracts market manage the added costs and time pressures more effectively than smaller firms. The FDA requires manufacturers to ensure the safety and accurate labeling of dietary supplement ingredients, increasing the need for testing, documentation, and supplier control. In Canada, regulations emphasize licensing and product support for companies aiming to enter or expand. The challenges intensify when botanical extracts shift toward therapeutic applications, as proof standards become more demanding. This slows the scaling of some promising products and directs buyers to suppliers with stronger regulatory capabilities.

Availability of Synthetic Substitute Products

Synthetic substitutes remain a persistent commercial obstacle in flavor and fragrance applications. In the North American botanical extracts market, this matters most where buyers serve large-volume products with tight cost targets. Synthetic aroma chemicals and artificial flavor compounds often remain cheaper at an industrial scale, especially when provenance adds little value to the finished product. That cost gap forces botanical suppliers to compete on traceability, phytochemical complexity, and quality consistency instead of price alone. The risk increases during periods of crop disruption or raw material inflation, when buyers can move back to synthetic options more quickly than they move toward botanicals. This keeps margin pressure elevated for suppliers that do not have strong brand positioning or differentiated application support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Herbs Anchor Volumes, Flowers Reframe the Premium Tier

In 2025, herbs commanded a 40.03% share of the source segment, solidifying their dominance in North America's botanical extracts market. Their prominence stems from their dual utility in food formulations and supplements. Furthermore, established contract farming for herbs like rosemary, sage, peppermint, and lavender ensures a more reliable supply. The U.S. supplement landscape, shaped by the DSHEA framework, dictates the commercial journey of herb-based actives and the pace of new formulations. This regulatory backdrop facilitates the large-scale commercialization of herbs, outpacing many less-established botanical categories in routine applications.

Flowers are set to be the fastest-growing source category, with a projected CAGR of 10.13% from 2026 to 2031. Their ascent is fueled by premium fragrance demands, functional skincare, and nutraceutical applications that rely on their delicate aromatic and bioactive profiles. However, demand varies: while marigold and hibiscus cater to broader applications, jasmine and tuberose command the higher-margin fragrance segment. IFF's bioprospecting deal in Brazil in 2025, followed by cultivation efforts in Grasse in 2026, underscores the industry's push to fortify supply chains for unique plant and flower materials. Meanwhile, spices, leaves, and other sources contribute to the volume, but their future hinges more on crop location and the mix of applications.

By Technology: Solvent Extraction Defines Scale, Enfleurage Captures Premium Demand

In 2025, solvent extraction held a 35.86% share of the technology segment, maintaining its position as the leading commercial method in North America's botanical extracts industry. Its importance stems from its ability to produce high outputs of oleoresins, botanical colorants, and flavor concentrates. Additionally, its established use and lower changeover risks help large processors protect unit economics. However, this dominance is under pressure as the EPA tightens compliance rules on methylene chloride, prompting processors to reassess legacy solvent systems. Sensient’s Certasure screening program highlights how major companies are turning solvent control into a quality management advantage.

Enfleurage is projected to grow at an 8.53% CAGR through 2031, making it the fastest-growing technology in North America's botanical extracts market. Its growth is driven by premium fragrance buyers valuing its gentle capture of heat-sensitive flower compounds. Recent solvent-free or low-impact refinements have also boosted its commercial appeal. A 2026 peer-reviewed study showed that optimizing enfleurage settings enhances targeted compound yields, expanding its use beyond a niche artisan role. Steam distillation and CO2 extraction are expected to maintain stable positions, while supercritical CO2 remains attractive for producers seeking greener processing and broader regulatory acceptance.

By Application: Food And Beverages Lead Demand, Pharmaceuticals Grow Fastest

In 2025, food and beverages led the North American botanical extracts market, holding 32.83% of the market share. This segment's demand stems from natural flavor systems, botanical colorants, fortified food formats, and plant-based preservation. Brands focus on ingredients that enhance both taste and health, making functional beverages and condition-led foods particularly important. The supplement and functional food channel further drives demand, especially when suppliers validate ingredient quality and safety under the U.S. dietary supplement framework. Although smaller, animal nutrition is creating opportunities for phytogenic additives in feed and pet formulations. Symrise's strategic positioning in animal nutrition ingredients highlights the value of expertise in this area.

Pharmaceuticals are projected to be the fastest-growing application in the North American botanical extracts market, with a CAGR of 9.01% from 2026 to 2031. This growth reflects rising interest in standardized botanical actives for therapeutic and clinical nutrition. Suppliers combining extraction capabilities with regulatory support and clinical documentation are well-positioned in this segment. Consistency is critical, as pharmaceutical buyers demand reproducible compositions and stricter evidence standards than food applications. Cosmetics and personal care remain key, with brands expanding clean beauty products featuring plant-derived actives under stricter safety requirements.

Geography Analysis

In 2025, the United States led the North American botanical extracts market with a 75.46% share. U.S. demand spans supplements, food ingredients, fragrance inputs, and personal care actives. The DSHEA framework supports a strong market for botanical supplements while ensuring manufacturers maintain product safety and compliance. Strict regulatory oversight on ingredient safety drives demand for suppliers offering traceable and well-documented extract systems. The U.S. remains central to the market due to its advanced manufacturing, formulation, and testing capabilities.

Mexico is the region's fastest-growing market, with an 8.72% CAGR projected through 2031. Consumer familiarity with herbal remedies boosts acceptance of botanical products in wellness and personal care. Increased manufacturing investments are positioning Mexico as a key production hub for regional customers. Givaudan’s expansion in Pedro Escobedo highlights Mexico’s growing importance as a center for fragrance and botanical ingredient operations serving North and Latin America. Canada, while stable, benefits from a regulatory framework that rewards quality-focused, documented ingredients and disciplined market entry.

The rest of North America contributes only a limited volume to the regional total. Its main role is as a sourcing and distribution corridor between larger production and demand nodes. Niche tropical botanicals and aromatic crops still matter, but the commercial weight of the North American botanical extracts market remains concentrated in the United States, Mexico, and Canada.

Competitive Landscape

The North American botanical extracts market features a mix of global ingredient manufacturers and specialized suppliers competing through innovation, proprietary extraction methods, and strong ties with nutraceutical, food and beverage, pharmaceutical, and personal care sectors. Key players like ADM, International Flavors & Fragrances, and Sensient Technologies Corporation. utilize extensive distribution networks, R&D capabilities, and diverse botanical portfolios to strengthen their positions. These companies focus on clean-label ingredients, natural flavors, and plant-based functional solutions to meet changing consumer demands.

Competition centers on innovation in standardized extracts, sustainability, and traceable sourcing. Companies invest in advanced extraction technologies, clinically validated botanicals, and organic-certified products to stand out. Specialized players such as Bio-Botanica Inc., Martin Bauer Group, and Akay Bioactives emphasize high-quality formulations, customized solutions, and vertically integrated supply chains to serve dietary supplement and functional food manufacturers.

Strategic partnerships, acquisitions, and portfolio expansion are key strategies in the region. Leading companies are targeting high-growth areas like herbal supplements, immunity-boosting ingredients, adaptogens, and plant-based wellness products. Regulatory compliance, quality certifications, and scientifically backed health benefits are critical competitive advantages. As demand for natural and plant-based ingredients grows, global suppliers and specialized producers are expected to intensify competition through innovation, capacity expansion, and targeted product development.

North America Botanical Extracts Industry Leaders

Givaudan SA

International Flavors & Fragrances Inc (IFF)

Symrise AG

Sensient Technologies Corporation

Archer Daniels Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sensient Technologies commenced expansion of its largest natural color manufacturing plant in St. Louis, Missouri, under Project Prism, adding 28,800 square feet of specialized botanical color processing capacity. The company announced plans to invest up to USD 250 million across natural color capacity, supply chain, and personnel during the coming years to address the U.S. food industry's conversion from synthetic to natural colors.

- December 2025: Sami-Sabinsa Group officially opened Hassan Unit-2, its 9th manufacturing facility, in the Pharma SEZ Industrial Area of Hassan, Karnataka, India. Representing a planned USD 15 million investment, the facility focuses on herbal ingredient production and active pharmaceutical ingredient manufacturing, expanding the group’s North American supply capacity.

- August 2025: IFF and Reservas Votorantim signed a strategic bioprospecting agreement granting IFF’s LMR Naturals subsidiary exclusive research access to the native flora of Legado das Águas, a 31,000-hectare private Atlantic Forest reserve in Brazil, for developing new and unique botanical extracts for perfumery and cosmetics applications.

North America Botanical Extracts Market Report Scope

| Herbs |

| Spices |

| Flowers |

| Leaves |

| Others |

| CO2 Extraction |

| Solvent Extraction |

| Steam Distillation |

| Enfleurage |

| Others |

| Food and Beverages |

| Dietary Supplements and Functional Foods |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Animal Nutrition |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Source | Herbs |

| Spices | |

| Flowers | |

| Leaves | |

| Others | |

| By Technology | CO2 Extraction |

| Solvent Extraction | |

| Steam Distillation | |

| Enfleurage | |

| Others | |

| By Application | Food and Beverages |

| Dietary Supplements and Functional Foods | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Animal Nutrition | |

| By Country | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

What is the current outlook for North America botanical extracts through 2031?

The North America botanical extracts market is projected to rise from USD 17.56 billion in 2026 to USD 26.05 billion by 2031 at an 8.21% CAGR.

Which application leads demand in North America botanical extracts?

Food and beverages led with 32.83% share in 2025, supported by natural flavors, botanical colors, and functional food formulations.

Which application is growing the fastest in botanical extracts across North America?

Pharmaceuticals is the fastest-growing application, with a projected 9.01% CAGR through 2031, driven by demand for standardized and clinically supported botanical actives.

Why does the United States dominate regional demand for botanical extracts?

The United States held 75.46% share in 2025 because it combines large supplement demand, broad food and personal care manufacturing, and a strong testing and formulation base.

Page last updated on: