Heart Transplantation Therapeutic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

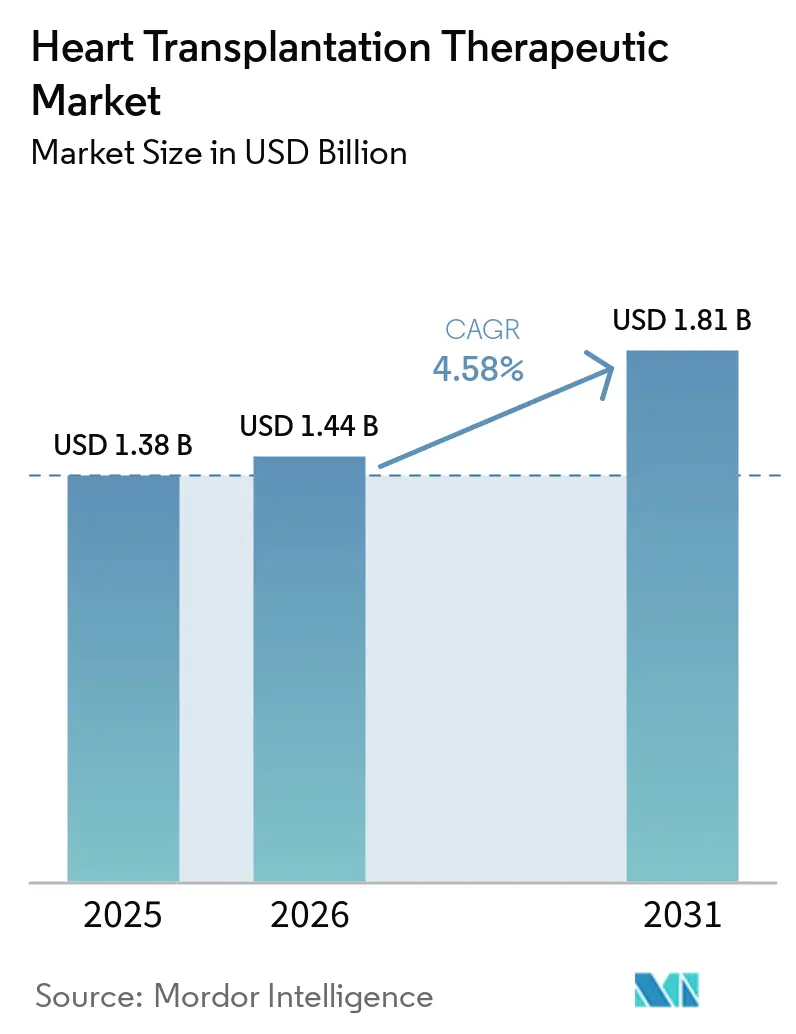

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 4.58% CAGR |

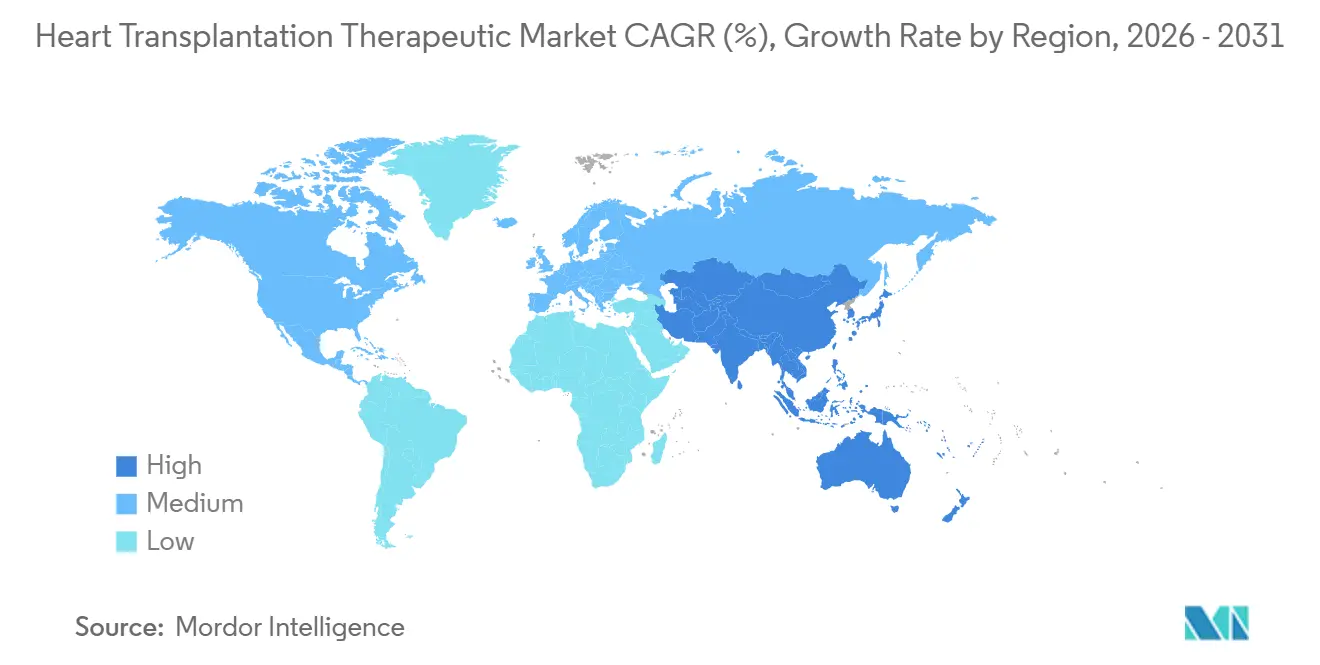

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

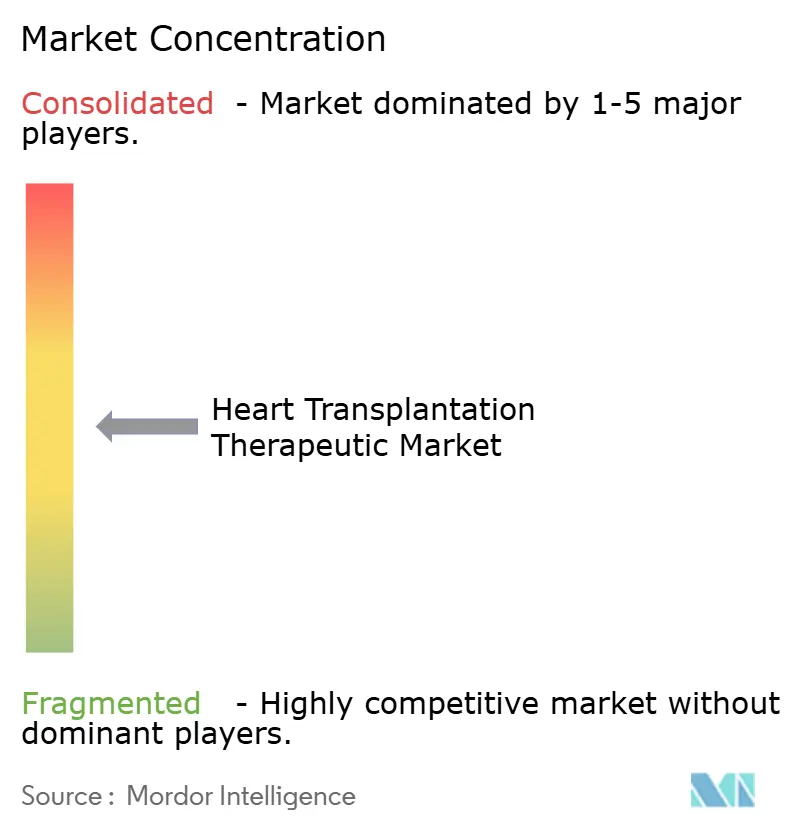

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heart Transplantation Therapeutic Market Analysis by Mordor Intelligence

The Heart Transplantation Therapeutic Market size is expected to increase from USD 1.38 billion in 2025 to USD 1.44 billion in 2026 and reach USD 1.81 billion by 2031, growing at a CAGR of 4.58% over 2026-2031.

The heart transplantation therapeutic market is expanding due to the long treatment cycles associated with each transplant, extending beyond surgery into years of maintenance therapy. In 2024, 10,287 heart transplants were performed across 59 countries, with major centers like Vanderbilt conducting 210 adult and pediatric transplants in 2025. Market growth is supported by improved rejection monitoring, increased use of anti-infective prophylaxis, and structured treatment pathways at high-volume academic hospitals. Competition in the market is divided between generic suppliers focusing on tacrolimus and related therapies and a premium segment centered on targeted biologics, biomarker-guided dosing, and transplant preservation technologies.

Key Report Takeaways

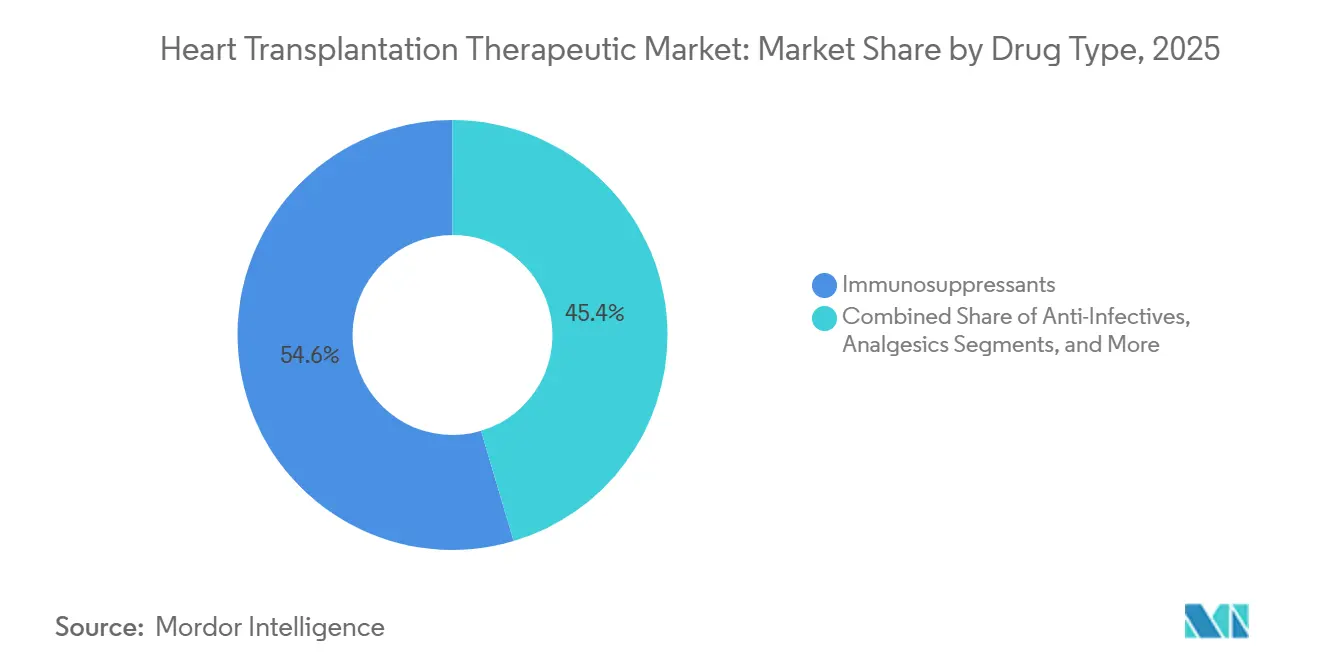

- By drug type, immunosuppressants held 54.60% of revenue in 2025, while anti-infectives are projected to expand at a 6.90% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 61.30% of revenue in 2025, while online pharmacies are projected to record the fastest 5.95% CAGR through 2031.

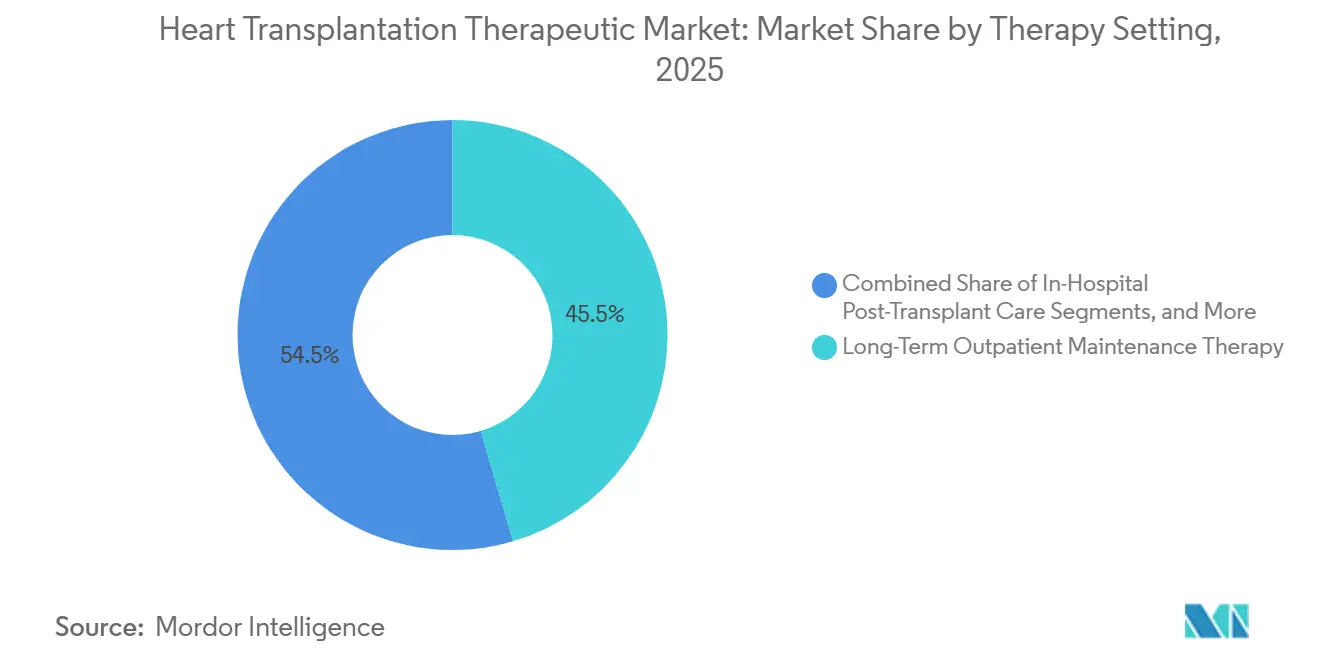

- By therapy setting, long term outpatient maintenance therapy captured 45.45% of revenue in 2025, while in hospital post transplant care is expected to grow at a 7.69% CAGR through 2031.

- By patient age group, adults represented 65.45% of revenue in 2025 and are also projected to the fastest 7.45% CAGR through 2031.

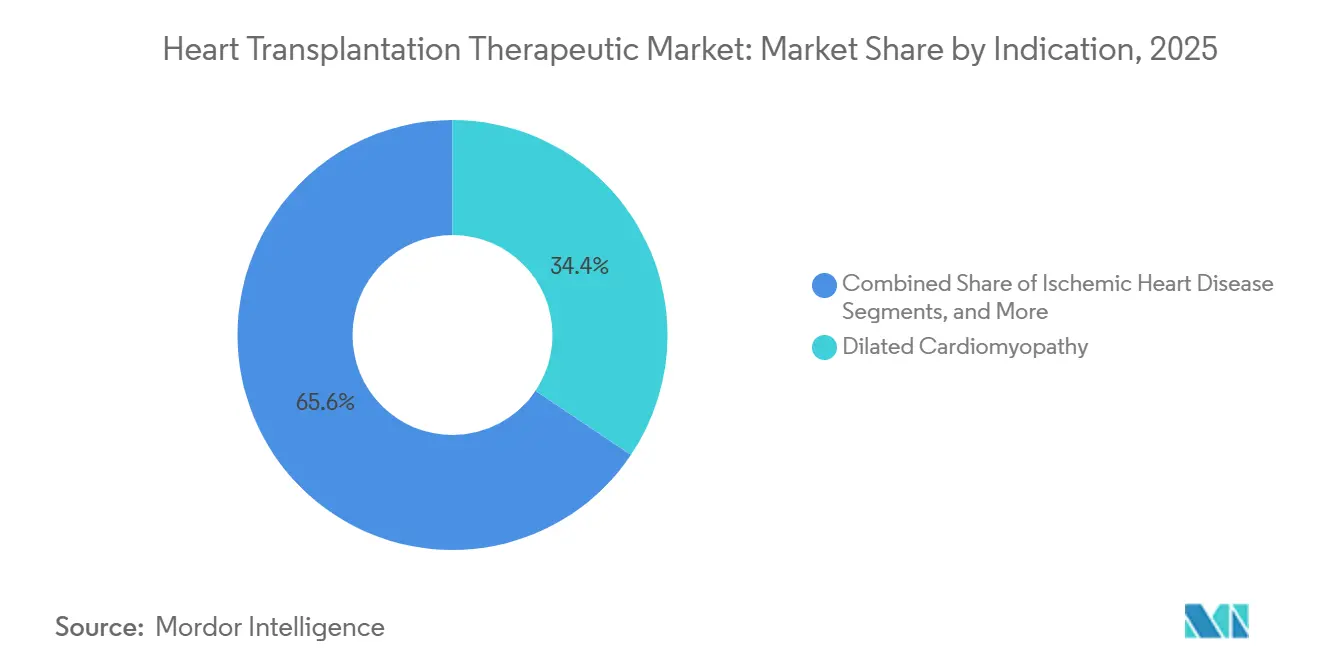

- By indication, dilated cardiomyopathy led with 34.44% of revenue in 2025, while hypertrophic cardiomyopathy is projected to advance at a 6.76% CAGR through 2031.

- By geography, North America held 40.65% of the heart transplantation therapeutic market share in 2025, while Asia Pacific is forecast to grow at the fastest 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Heart Transplantation Therapeutic Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising end-stage heart failure burden | +1.4% | Global | Long term (≥ 4 years) |

| Expanding use of immunosuppressive maintenance therapies | +1.1% | North America & Europe | Medium term (2-4 years) |

| Wider adoption of ex-vivo organ perfusion and preservation | +0.7% | North America, Europe, APAC early adopters | Medium term (2-4 years) |

| Personalized immunosuppression guided by biomarkers | +0.6% | North America, EU | Long term (≥ 4 years) |

| Donor-heart logistics pressure from time-to-transplant reduction | +0.4% | North America, EU | Short term (≤ 2 years) |

| Post-transplant infection prevention protocol intensification | +0.4% | Global, with early gains in US, Germany, Spain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising End-Stage Heart Failure Burden

The heart transplantation therapeutic market is driven by the increasing prevalence of advanced heart failure. A 2026 analysis highlighted a rise in age-standardized prevalence and years lived with disability due to cardiovascular disease-related heart failure from 1990 to 2025, with significant increases among individuals aged 20 to 54 and in middle to high Socio Demographic Index countries.[1]Global Observatory on Donation and Transplantation, “Organ Donation and Transplantation Worldwide, The Global Observatory on Donation and Transplantation 2024 Report,” PMC, pmc.ncbi.nlm.nih.gov Global heart failure prevalence remains high at 64 million individuals, ensuring a broad pool of potential transplant candidates, though only a fraction progresses to surgery. In the U.S., heart transplants increased by 101.1% from 2012 to 2024, reaching 4,599 procedures in 2024, with 424 additional adult transplants between 2023 and 2024. The 2025 World Heart Report also identified obesity-linked cardiomyopathy as a growing contributor to heart failure, emphasizing the need for tailored post-transplant treatment plans.[2]Weng Kin Lim et al., “Global Trends and Projections in Cardiovascular Disease-Related Heart Failure, 1990-2050, An Analysis of the Global Burden of Disease 2021 Data,” Internal and Emergency Medicine, link.springer.com

Expanding Use of Immunosuppressive Maintenance Therapies

The heart transplantation therapeutic market, anchored in tacrolimus-based multi-drug maintenance therapy, is expanding through improved access and treatment refinement. In January 2025, Biocon Pharma received NMPA approval in China for tacrolimus capsules in 0.5 mg, 1 mg, and 5 mg strengths, broadening the generic supply base. Research on tacrolimus intra-patient variability supports closer monitoring and formulations ensuring steadier exposure. A 2025 study linked tacrolimus variability to inferior allograft outcomes, while a 2026 paper identified ABCC2 rs2273697 as a determinant of this variability. These findings promote structured dosing programs at high-complexity centers, balancing price competition in standard agents with value-based differentiation in specialized regimens.

Wider Adoption of Ex-Vivo Organ Perfusion and Preservation

Advancements in organ preservation are enhancing the heart transplantation therapeutic market by converting marginal or distant organs into viable transplant options. A UNOS thoracic registry analysis from January 2019 to April 2025 showed ex vivo heart perfusion mitigated survival penalties tied to prolonged agonal periods in donors after circulatory death. Each transplant supported by this method adds a long-term maintenance patient to the market. Investments reflect this trend, with Terumo acquiring OrganOx for USD 1.5 billion in October 2025 and TransMedics receiving FDA IDE approval in February 2026 for the OCS ENHANCE Heart trial, targeting over 650 patients. As this infrastructure expands, it strengthens demand for immunosuppressants, anti-infectives, and monitoring services.

Personalized Immunosuppression Guided by Biomarkers

The heart transplantation therapeutic market is shifting toward personalized post-transplant treatments to reduce toxicity while maintaining rejection control. Donor-derived cell-free DNA (dd cfDNA) testing offers a less invasive alternative to traditional biopsies. A 2025 Spanish study found that dd cfDNA testing could eliminate over 80% of planned biopsies in stable heart transplant recipients. This approach alters drug use, with high-risk patients transitioning earlier to stronger regimens and stable patients moving toward minimization. The FDA granted Orphan Drug Designation in April 2026 to Veloxis Pharmaceuticals for pegrizeprument to prevent heart allograft rejection. Sanofi advanced frexalimab in 2026 through Phase II and III trials against tacrolimus in kidney transplantation, signaling broader interest in costimulatory pathway blockade across transplant care.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Shortage of suitable donor hearts | -1.0% | Global | Long term (≥ 4 years) |

| Lifelong immunosuppression safety burden | -0.7% | North America & Europe | Medium term (2-4 years) |

| High total cost of transplant care and follow-up | -0.5% | APAC, MEA, South America | Medium term (2-4 years) |

| Limited center capacity and specialist availability | -0.4% | MEA, South America, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Donor Organ Scarcity

The heart transplantation market continues to face limitations as its growth depends on donor availability rather than clinical demand. In 2024, 10,287 heart transplants were performed globally, yet a significant supply gap remains due to the standard cold ischemia time of 4 to 6 hours. Donation after circulatory death (DCD) donors accounted for 28% of all deceased donors in 2024, a 17% year-over-year increase, but DCD hearts were utilized in only 9 countries. This limited geographic adoption restricts market growth. Additionally, the updated ISHLT candidate evaluation guidance in 2024 emphasizes stricter risk stratification, potentially reducing listings at centers applying the framework rigorously. While United Therapeutics received FDA clearance in May 2026 for the EXPRESS xenotransplantation trial with UHeart, it represents a long-term solution to donor scarcity.

Lifelong Immunosuppression Safety Burden

The heart transplantation market is further constrained by the challenges of lifelong immunosuppression. Issues such as tacrolimus-related nephrotoxicity, fungal and viral co-infections, post-transplant malignancies, and metabolic complications limit the escalation of therapies. A 2025 study revealed that heart transplant centers relied on echinocandins like anidulafungin (27.8%) and caspofungin (22.2%), along with fluconazole, for antifungal prophylaxis. This layered drug regimen increases monitoring needs and interaction risks, complicating long-term adherence, especially for stable recipients. These complexities also raise multi-year healthcare costs, particularly in regions with incomplete public reimbursement and inconsistent specialty follow-up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Immunosuppressants Anchor Revenue, Anti Infectives Fastest Growing

In 2025, immunosuppressants dominated the heart transplantation therapeutic market, accounting for 54.60% of the revenue. This dominance underscores the reliance on calcineurin inhibitor-based regimens, the gold standard for heart transplant recipients. Spending heavily leans towards tacrolimus formulations and mycophenolate combinations, both of which necessitate prolonged use and frequent adjustments. Such dynamics ensure the centrality of this category in the market, even amidst only moderate growth in procedures.

Anti-infectives are set to be the fastest-growing segment, with a projected CAGR of 6.90% through 2031. This growth is driven more by heightened prophylaxis protocols than mere increases in patient volume. Research highlights that heart transplant patients, who are donor positive and recipient negative, face a heightened risk of CMV infection after three months on valganciclovir prophylaxis, compared to six months. Such findings advocate for extended antiviral treatment durations, especially during the crucial first year post-transplant.

By Distribution Channel: Hospital Pharmacies Dominate, Online Dispensing Gains Ground

In 2025, hospital pharmacies secured 61.30% of the revenue, underscoring the heart transplantation therapeutic market's strong ties to tertiary care. Key processes like induction therapy, early tacrolimus titration, and therapeutic drug monitoring are integral to specialist hospital workflows. This positions hospital pharmacies as the primary and most regulated dispensing point for new transplant recipients. Their dominance is further bolstered by the concentration of procedures at major academic transplant centers, which often feature integrated pharmacy teams.

Online pharmacies are projected to expand at a 5.95% CAGR through 2031, marking the highest growth rate in this segment. This trend is driven less by convenience and more by specialized services like mail order handling, home delivery, and coordination for stable patients' monitoring needs. As recipients progress beyond the immediate post-surgery phase, there's a noticeable shift of prescriptions from hospital settings to channels that ensure consistent long-term refills.

By Therapy Setting: Long Term Maintenance Drives Revenue, In Hospital Care Grows Fastest

Long-term outpatient maintenance therapy constituted 45.45% of the revenue in 2025, solidifying its position as the leading therapy setting in the heart transplantation market. This segment's significance stems from the prolonged treatment journey that extends years post-transplant. Key contributors to this sustained spending include tacrolimus, mycophenolate, corticosteroids, anti-infectives, and routine monitoring. Consequently, the market's size in long-term maintenance is less susceptible to short-term fluctuations in surgery scheduling, unlike categories primarily linked to the initial hospitalization.

In-hospital post-transplant care is anticipated to grow at the fastest rate, with a projected CAGR of 7.69% through 2031. This surge is attributed to the complexities of early management, including the use of induction biologics, a rise in DCD organ utilization, and heightened oversight for patients at risk of primary graft dysfunction. The broader acceptance of extended criteria donor hearts, especially through ex vivo perfusion, intensifies this early management phase, necessitating meticulous first-line treatment for more recipients.

By Patient Age Group: Adults Define Revenue, Pediatric Care Remains Specialized

In 2025, adults represented 65.45% of the revenue, solidifying their dominant role in the heart transplantation therapeutic market. This trend aligns with the prevalence of end-stage heart disease in middle-aged and older demographics. Furthermore, as post-transplant survival rates improve at established centers, adult recipients tend to have extended treatment episodes. This positions adults as the primary commercial base for the market, spanning immunosuppressants, anti-infectives, and follow-up monitoring.

Forecasts indicate adults will experience the swiftest growth, with a projected CAGR of 7.45% through 2031. Data highlights a consistent annual uptick in adult heart transplant activities, culminating in 5,887 procedures reported by 2023. This trend is bolstered by the rising prevalence of heart failure, often linked to obesity, hypertension, and post-viral cardiomyopathy. While pediatric transplantation commands a smaller revenue share, it presents unique challenges due to differing dosing, development, and formulation needs compared to adult care.

By Indication: Dilated Cardiomyopathy Leads, Hypertrophic Cardiomyopathy Expands Faster

Dilated cardiomyopathy, accounting for 34.44% of the 2025 revenue, emerged as the leading indication in the heart transplantation therapeutic market. This prominence aligns with clinical findings that identify dilated cardiomyopathy as a primary driver for non-ischemic heart transplants in both the U.S. and Europe. The sustained market share for this indication is largely due to patients typically following standard long-term immunosuppressive pathways post-surgery. While ischemic heart disease stands as another significant indication, its trajectory is influenced by advancements in revascularization and the selective use of ventricular assist devices.

Hypertrophic cardiomyopathy is on track to witness the most rapid growth, with a projected CAGR of 6.76% through 2031. The 2024 ISHLT evaluation guidance introduced nuanced risk stratification for both obstructive and non-obstructive phenotypes, potentially expanding the transplant listing pathway for patients previously managed without a transplant. While restrictive cardiomyopathy and congenital heart disease are smaller categories, they present significant clinical challenges due to their intricate post-surgery treatment needs.

Geography Analysis

In 2025, North America accounted for 40.65% of the heart transplantation therapeutic market revenue, securing its leading position. The U.S. led globally with 4,636 heart transplants performed in 2024. Medicare reimbursements and established specialty pharmacy networks drive high per-patient drug spending post-surgery. Concentration at academic hospitals enhances protocol standardization and supports large-scale monitoring of treatment outcomes. Vanderbilt exemplified this by performing 210 adult and pediatric heart transplants in 2025, reinforcing the role of high-throughput centers in shaping treatment practices.

Europe remains the second-largest market for heart transplantation therapeutics. Eurotransplant member states reported 1,102 heart transplants in the first five months of 2026, up from 1,046 during the same period in 2025. Spain increased cardiac transplant volumes by 12% in 2025 and maintained a high donation rate of 50.7 donors per million inhabitants. Germany and the U.K. contribute significantly to procedure volumes, while stringent manufacturing and pharmacovigilance standards sustain strong demand for branded and regulated formulations.

Asia Pacific is projected to grow at the fastest CAGR of 6.55% through 2031, emerging as the most dynamic regional market. China and India drive growth, supported by expanding institutional capacities, broader access to generic tacrolimus, and favorable policies for transplant and immune regulation therapeutics. Biocon’s tacrolimus approval and rollout in China in 2025 demonstrated how access expansion supports institutional procurement growth. Japan, South Korea, and Australia, though smaller in transplant numbers, maintain high treatment expenditures due to national coverage supporting post-surgery immunosuppressive use. Growth in the Middle East, Africa, and South America remains uneven, with countries like Saudi Arabia, the UAE, Brazil, and Argentina improving capabilities but facing challenges such as donor shortages, funding constraints, and limited specialist availability.

Competitive Landscape

The heart transplantation therapeutic market is moderately concentrated, with immunosuppressant franchises driving competition. Astellas and Novartis maintain strong branded positions in calcineurin inhibitor revenue through products like Prograf, Envarsus, and Advagraf. Generic manufacturers such as Teva, Viatris, Glenmark, Intas, Sun Pharmaceutical, and Biocon are intensifying competition in cost-sensitive regions. This dynamic splits the market between branded differentiation in specialized formulations and volume-driven competition in standard maintenance agents.

Strategic developments in 2025 and 2026 highlight the market's expansion beyond traditional drug supply. Terumo entered the transplant preservation segment with its USD 1.5 billion acquisition of OrganOx in October 2025, strengthening competition in normothermic machine perfusion. TransMedics advanced its OCS ENHANCE Heart program after receiving full FDA IDE approval in February 2026 and launched the CHOPS preservation system in April 2026. These advancements emphasize the growing link between preservation technology and long-term demand for immunosuppressants and related therapies.

Innovation is reshaping the premium segment of the heart transplantation therapeutic market. Veloxis secured FDA Orphan Drug Designation in April 2026 for pegrizeprument, targeting heart allograft rejection prevention. In January 2026, Veloxis partnered with PIRCHE to integrate epitope matching analysis, connecting molecular diagnostics with drug development. Sanofi’s frexalimab study reflects the exploration of alternatives to tacrolimus-based protocols. These developments indicate that future competition will focus on biomarker integration, mechanism differentiation, and precision in long-term treatment strategies.

Heart Transplantation Therapeutic Industry Leaders

Abbott Laboratories

Medtronic plc

Astellas Pharma Inc.

TransMedics Group, Inc.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: United Therapeutics received FDA clearance under an IND application to initiate the EXPRESS clinical trial for a pig-derived heart with 10 gene edits, enrolling up to 2 participants and targeting a Biologics License Application pathway.

- April 2026: Veloxis Pharmaceuticals announced FDA Orphan Drug Designation for pegrizeprument (VEL-101), a pegylated monoclonal antibody fragment targeting CD28-mediated T-cell costimulation, for heart allograft rejection prevention, positioning it as the first CD28-selective agent in cardiac transplant immunosuppression.

- February 2026: TransMedics received full FDA IDE approval for the Next-Generation OCS ENHANCE Heart trial, a two-part study enrolling over 650 patients to demonstrate the superiority of warm perfusion over static cold storage for standard criteria DBD hearts.

- January 2026: PIRCHE AG partnered with Veloxis Pharmaceuticals to provide epitope-matching analysis, integrating advanced HLA molecular diagnostics into pegrizeprument's clinical development for rejection prevention.

- January 2025: Biocon Pharma received NMPA approval in China for tacrolimus capsules in 0.5 mg, 1 mg, and 5 mg strengths, expanding access to affordable generic calcineurin inhibitors in the transplant pharmaceutical market.

Global Heart Transplantation Therapeutic Market Report Scope

As per the scope of the report, a heart transplant is a major surgery that replaces a failing heart with a healthy donor heart. It is used for end-stage heart failure when all other medical options fail. Heart transplantation therapeutics include the medical care and drugs needed before, during, and after a heart transplant.

The heart transplantation therapeutic market is segmented by drug type, distribution channel, therapy setting, patient age group, and indication. By drug type, the market includes immunosuppressants, anti-infectives, analgesics, and other heart transplant therapeutics. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By therapy setting, the market is categorized into pre-transplant care, in-hospital post-transplant care, and long-term outpatient maintenance therapy. By patient age group, the market is segmented into adults and pediatrics. By indication, the market is categorized into dilated cardiomyopathy, ischemic heart disease, hypertrophic cardiomyopathy, restrictive cardiomyopathy, congenital heart disease, and other indications. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Immunosuppressants |

| Anti-Infectives |

| Analgesics |

| Other Heart Transplant Therapeutics |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Pre-Transplant Care |

| In-Hospital Post-Transplant Care |

| Long-Term Outpatient Maintenance Therapy |

| Adult |

| Pediatric |

| Dilated Cardiomyopathy |

| Ischemic Heart Disease |

| Hypertrophic Cardiomyopathy |

| Restrictive Cardiomyopathy |

| Congenital Heart Disease |

| Other Indications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Immunosuppressants | |

| Anti-Infectives | ||

| Analgesics | ||

| Other Heart Transplant Therapeutics | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Therapy Setting | Pre-Transplant Care | |

| In-Hospital Post-Transplant Care | ||

| Long-Term Outpatient Maintenance Therapy | ||

| By Patient Age Group | Adult | |

| Pediatric | ||

| By Indication | Dilated Cardiomyopathy | |

| Ischemic Heart Disease | ||

| Hypertrophic Cardiomyopathy | ||

| Restrictive Cardiomyopathy | ||

| Congenital Heart Disease | ||

| Other Indications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the heart transplantation therapeutic space?

It stands at USD 1.44 billion in 2026 and is forecast to reach USD 1.81 billion by 2031 at a 5.58% CAGR.

Which therapy category generates the most revenue after heart transplant procedures?

Immunosuppressants lead the revenue mix with 54.60% share in 2025 because they remain the standard long term treatment backbone.

Which product area is growing the fastest through 2031?

Anti infectives are projected to post the fastest 6.90% CAGR, supported by longer CMV and fungal prophylaxis protocols.

Which region leads global revenue and which one is expanding the fastest?

North America held 40.65% of revenue in 2025, while Asia Pacific is forecast to grow at the fastest 6.55% CAGR through 2031.

Why does long term outpatient care matter so much in this field?

Long term outpatient maintenance held 45.45% of 2025 revenue because treatment continues for years after the transplant surgery itself.

What is changing competition among companies in this space?

Competition is broadening from generic tacrolimus supply into organ preservation, targeted biologics, and biomarker guided dosing, with notable 2025 and 2026 moves by Terumo, TransMedics, and Veloxis.

Page last updated on: