Congestive Heart Failure Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

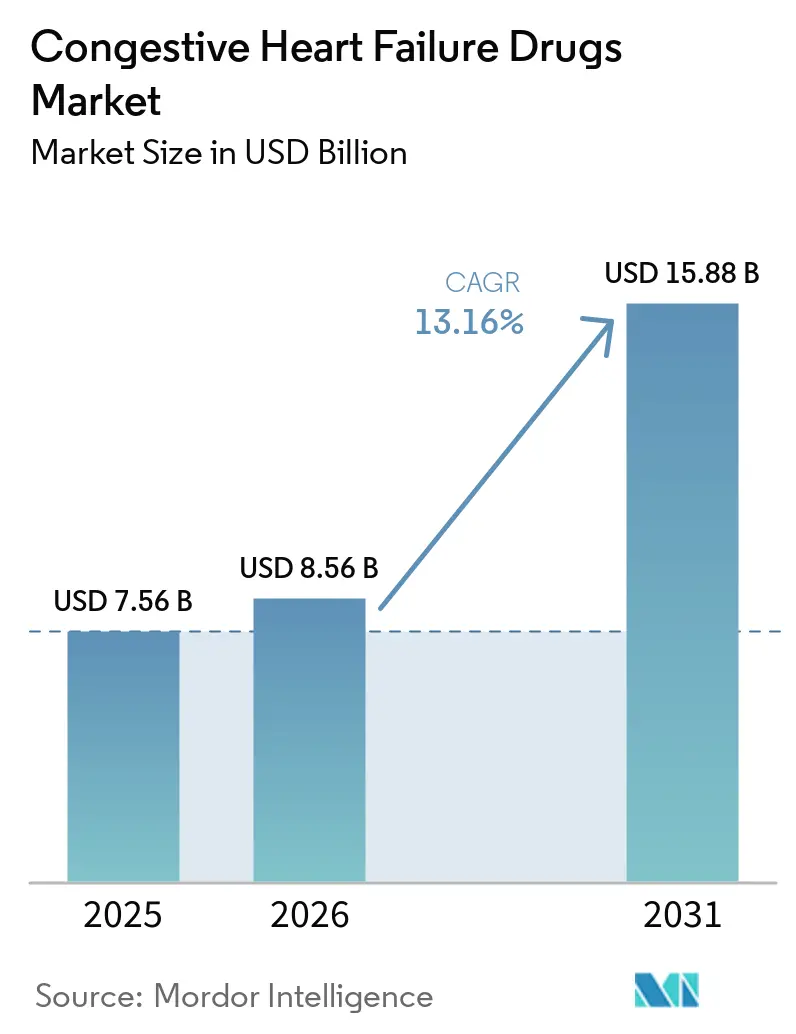

| Market Size (2026) | USD 8.56 Billion |

| Market Size (2031) | USD 15.88 Billion |

| Growth Rate (2026 - 2031) | 13.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Congestive Heart Failure Drugs Market Analysis by Mordor Intelligence

The Congestive Heart Failure Drugs Market size was valued at USD 7.56 billion in 2025 and is estimated to grow from USD 8.56 billion in 2026 to reach USD 15.88 billion by 2031, at a CAGR of 13.16% during the forecast period (2026-2031).

The congestive heart failure drugs market is witnessing growth due to a shift from symptom-focused single-drug treatments to the earlier adoption of multiple guideline-recommended therapies. The global prevalence of heart failure increased from 25.43 million cases in 1990 to 55.50 million in 2024. Rising obesity and diabetes rates are further driving this trend, with 878 million adults living with obesity in 2024 and 11.1% of adults aged 20-79 projected to have diabetes by 2025.[1]Global Burden of Disease Collaborative Network, “Global, Regional, and National Burden of Heart Failure and Its Underlying Causes, 1990–2021: Results from the Global Burden of Disease Study 2021,” European Heart Journal, pmc.ncbi.nlm.nih.gov The market is also supported by care models emphasizing home-based congestion management and streamlined channels for repeat dispensing for long-term users. Additionally, new approvals for finerenone and vutrisiran have expanded the treatment landscape, intensifying competition in HFmrEF, HFpEF, and ATTR-CM.

Key Report Takeaways

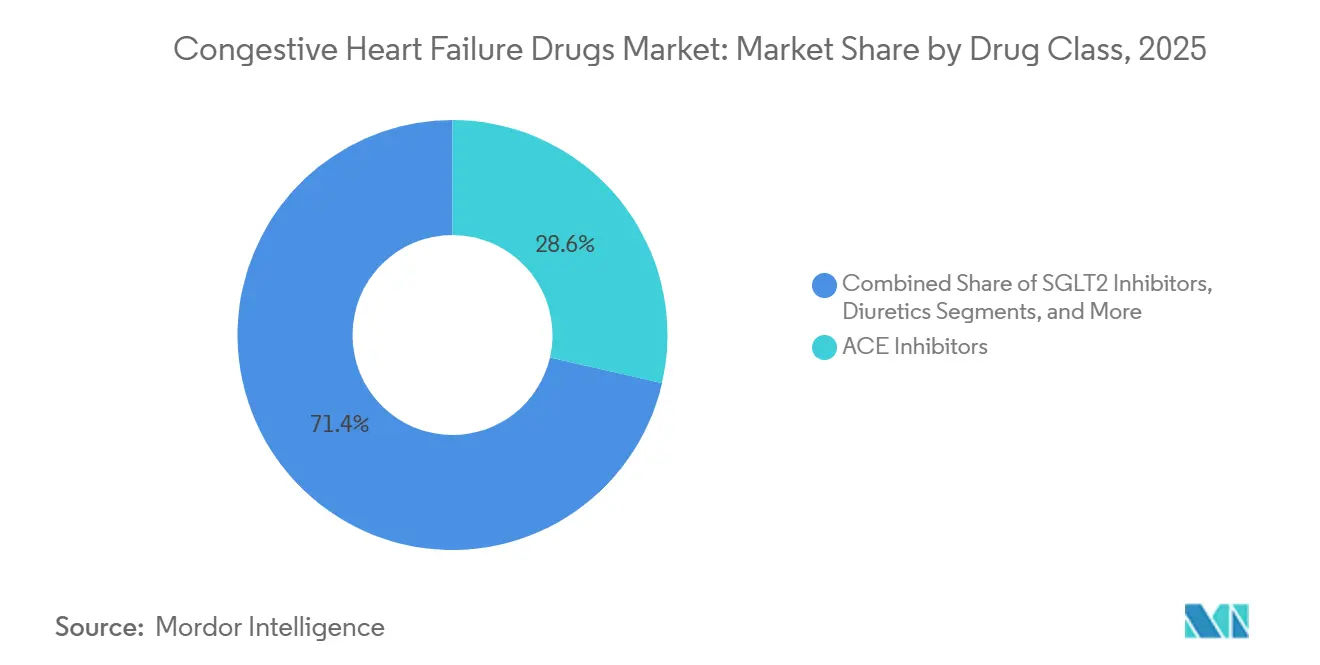

- By drug class, ACE inhibitors held 28.60% of the congestive heart failure drugs market share in 2025, while the congestive heart failure drugs market size for SGLT2 inhibitors is projected to expand at 14.99% CAGR from 2026 to 2031.

- By route of administration, oral formulations accounted for 76.45% of revenue in 2025, while the congestive heart failure drugs market size for injectable formulations is projected to rise at 16.95% CAGR through 2031.

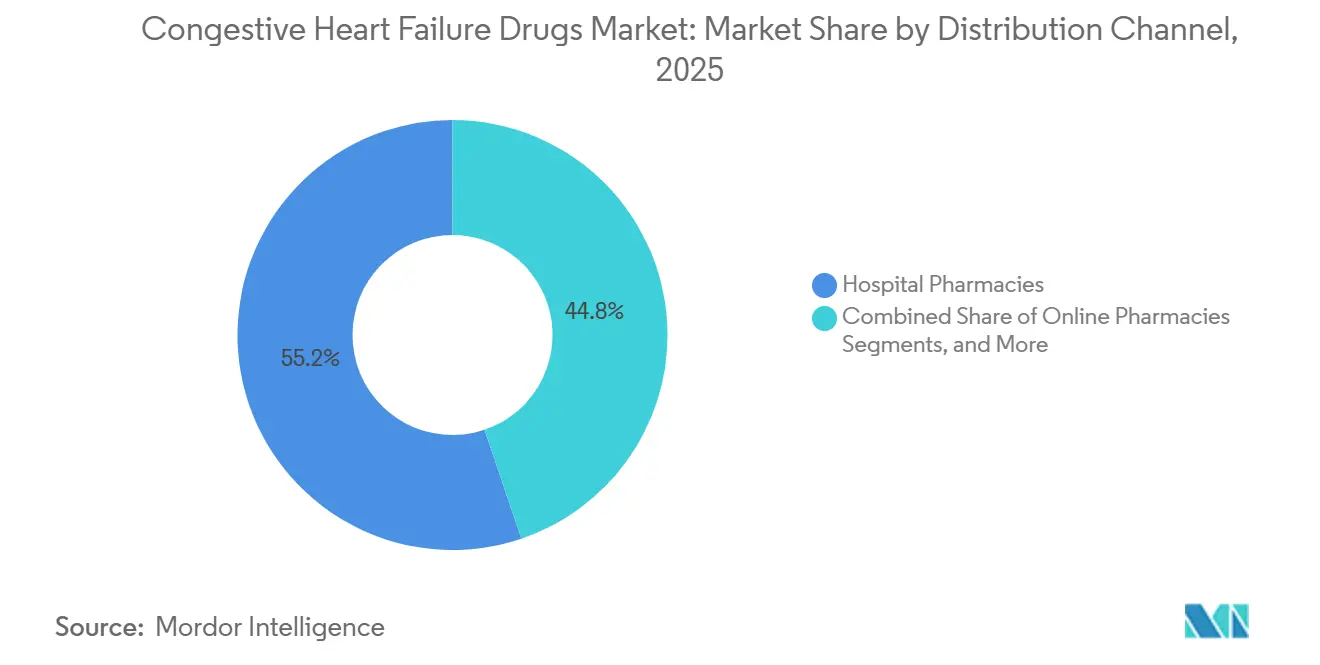

- By distribution channel, hospital pharmacies captured 55.22% of revenue in 2025, while online pharmacies are forecast to grow at 16.55% CAGR through 2031.

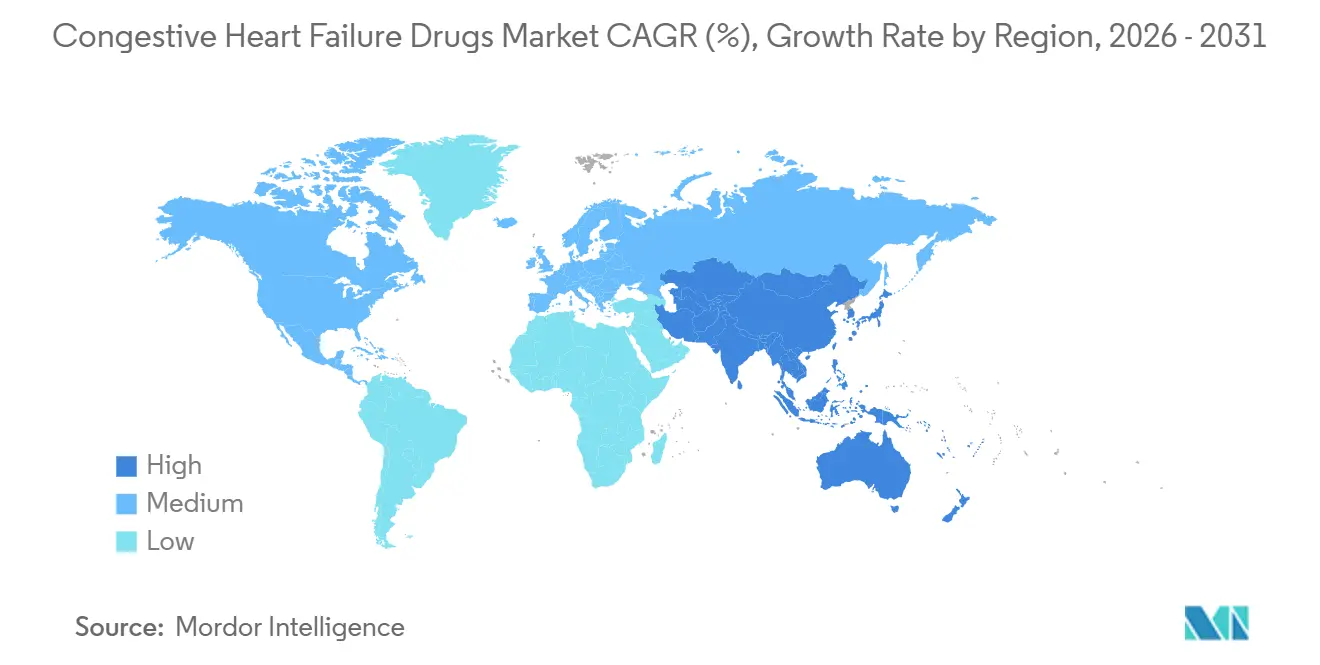

- By geography, North America held 39.52% of the congestive heart failure drugs market share in 2025, while the congestive heart failure drugs market size in Asia-Pacific is projected to advance at 15.26% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Congestive Heart Failure Drugs Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding guideline-directed therapy adoption across HF phenotypes | +2.8% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Rising heart failure prevalence driven by obesity, diabetes, and aging | +2.5% | Global, highest intensity in APAC and MEA | Long term (≥ 4 years) |

| Earlier diagnosis and longer treatment duration in chronic HF | +1.6% | North America, Europe | Medium term (2-4 years) |

| Approval momentum for new indications in HFMREF and HFPEF | +2.3% | US, EU, Japan leading, emerging markets lagged | Short term (≤ 2 years) |

| Shift toward multi-drug, long-term maintenance regimens | +1.5% | Global, higher penetration in developed markets | Medium term (2-4 years) |

| Growth of home-based and outpatient congestion management | +1.1% | North America, Western Europe, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Guideline-Directed Therapy Adoption Across HF Phenotypes

The market for congestive heart failure drugs is benefiting from a treatment model that initiates core therapies earlier in the care pathway. Care teams now implement protocol-led combinations instead of adding medications one at a time as symptoms worsen. The 2025 ESC Focus Update granted dapagliflozin and empagliflozin Class IA status for HFmrEF and HFpEF, broadening treatment options for previously underserved patient groups.[2]M. Al-Sadawi et al., “The Role of SGLT2-Inhibitors Across All Stages of Heart Failure and Mechanisms of Early Clinical Benefit, From Prevention to Advanced Heart Failure,” Biomedicines, mdpi.com Similarly, Chinese expert guidance endorsed SGLT2 inhibitors for symptomatic HFrEF patients regardless of diabetes status, reflecting a global shift in treatment approaches. This has expanded the eligible patient base beyond the traditional HFrEF population, driving market growth.

Rising Heart Failure Prevalence Driven By Obesity, Diabetes, and Aging

The congestive heart failure drugs market is growing due to an increasing disease burden across age groups and risk profiles. In 2024, global obesity affected 878 million adults, with high BMI contributing to nearly 10% of cardiovascular deaths.[3]World Heart Federation, “World Heart Report 2025,” World Heart Federation, world-heart-federation.org By 2025, diabetes impacted 11.1% of adults aged 20-79, with over 40% of cases undiagnosed, leading to delayed treatment and higher drug dependency. Global heart failure prevalence reached 55.50 million cases in 2024, more than doubling since 1990, with a notable rise among younger adults.[4]International Diabetes Federation, “IDF Diabetes Atlas, 11th Edition, Diabetes Facts and Figures,” IDF, idf.org This trend supports market growth as earlier disease onset extends treatment duration and chronic therapy needs.

Approval Momentum For New Indications In HFmrEF And HFpEF

The congestive heart failure drugs market is expanding with approvals targeting underserved patient groups. Bayer’s KERENDIA received FDA approval in July 2025 for heart failure patients with LVEF of 40% or more, followed by European Commission and UK MHRA clearances in March 2026. This expanded the nonsteroidal MRA class to a broader HFmrEF and HFpEF population. Additionally, the FDA approved AMVUTTRA, the first RNAi therapy to reduce cardiovascular mortality and hospitalizations in ATTR-CM. These developments diversify the market, reducing reliance on older drug classes and introducing premium products with advanced mechanisms.

Growth Of Home-Based And Outpatient Congestion Management

The congestive heart failure drugs market is advancing with a shift toward home-based and outpatient congestion management. In October 2025, the FDA approved Lasix ONYU, enabling patients to self-administer subcutaneous furosemide at home without clinician supervision. Phase 3 SUBCUT HF II results in May 2026 showed Lasix ONYU patients spent 4 fewer hospital days compared to standard IV furosemide, strengthening the case for at-home diuresis. Corstasis also received FDA approval in September 2025 for ENBUMYST, a bumetanide nasal spray, expanding outpatient options for edema management. These innovations enhance treatment accessibility and support sustained market growth.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Generic and tender pressure on mature drug classes | -1.8% | Global, most acute in the US and Western Europe | Short term (≤ 2 years) |

| Safety concerns, tolerability limits, and dose-optimization challenges | -0.9% | Global | Medium term (2-4 years) |

| High monitoring burden for patients with multi-morbidity | -0.7% | Developing markets and low-income settings | Long term (≥ 4 years) |

| Reimbursement friction for newer therapies in value-based settings | -1.4% | US, EU, NICE, HTA bodies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generic And Tender Pressure On Mature Drug Classes

The congestive heart failure drugs market, dominated by mature therapies, faces significant pricing pressures. Established classes like ACE inhibitors, beta blockers, and the ARNI class are under growing generic competition, reducing revenue per prescription despite stable patient volumes. Entresto, the leading branded product in this segment, experienced U.S. generic entry in Q3 2025. Novartis reported a 42% year-on-year revenue decline to USD 1.3 billion in Q1 2026, highlighting the rapid revenue erosion following the loss of exclusivity. Volume-based procurement systems further compress prices and shift demand to low-cost suppliers, creating a divide where older drug classes retain large patient bases but contribute minimally to revenue growth, while branded growth relies on newer products.

Reimbursement Friction For Newer Therapies In Value-Based Settings

The congestive heart failure drugs market encounters challenges as newer therapies move from regulatory approval to payer evaluation. Cost-effectiveness comparisons with low-cost generics often delay coverage, even for drugs with strong clinical data. For example, NICE approved dapagliflozin for HFpEF and HFmrEF in the UK, but access delays of over 12 months between regulatory approval and broader formulary adoption hindered early sales momentum. Premium-priced entrants like finerenone, vutrisiran, and sotagliflozin face payer demands for real-world outcomes alongside trial data, causing commercial delays, particularly in HFpEF, where newer products are still building access and comparative histories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: SGLT2 Inhibitors Reorder A Multi-Decade Prescribing Hierarchy

In 2025, ACE inhibitors accounted for 28.60% of revenue, maintaining their position as the leading drug class due to their affordability, widespread availability, and established role in heart failure care. Their dominance reflects long-standing first-line use in national formularies and clinical guidelines, despite mature pricing. ARBs serve as alternatives for patients intolerant to ACE inhibitors, while beta blockers remain essential in guideline-directed therapy for HFrEF. Diuretics continue to see high prescription volumes, though newer delivery formats aim to enhance their value. Finerenone is redefining the aldosterone antagonist category by extending its use to HFmrEF and HFpEF after approvals in the U.S., Europe, and the UK.

The SGLT2 inhibitors market for congestive heart failure drugs is projected to grow at a 14.99% CAGR from 2026 to 2031, making it the fastest-growing drug class during this period. Growth is driven by full guideline support for ejection fraction and the commercial success of Jardiance and Farxiga, which already generate significant global revenues. A meta-analysis reinforced their clinical value in HFpEF, showing reduced hospitalization risks and improved patient outcomes, supporting broader adoption.

By Route Of Administration: Subcutaneous Delivery Disrupts The Volume-Oral Equilibrium

Oral formulations held 76.45% of revenue in 2025, reflecting their dominance in outpatient heart failure maintenance therapies. Drugs like ACE inhibitors, beta blockers, ARBs, SGLT2 inhibitors, and ARNIs support this trend due to their long-term daily use. The treatment model reinforces oral dominance by adding agents to existing regimens rather than replacing them. Other administration routes remain limited, with minimal commercial impact. Oral therapy continues to align with the chronic nature of heart failure care.

Injectable formulations are expected to grow at a 16.95% CAGR through 2031, making them the fastest-growing route despite being smaller than oral therapies. This growth is driven by innovative products enabling home or lower-acuity administration. Lasix ONYU, with Phase 3 data in 2026 showing 4 fewer hospital days compared to standard IV furosemide, offers payers economic incentives for subcutaneous home treatment. Vutrisiran adds growth potential with its quarterly subcutaneous schedule, combining premium pricing with reduced administration frequency. Tools like ENBUMYST further expand outpatient options, making injectables increasingly tied to convenience and site-of-care changes.

By Distribution Channel: Digital Pharmacies Gain Ground Against Institutional Incumbents

Hospital pharmacies captured 55.22% of distribution revenue in 2025, maintaining their lead due to their role in initiating complex therapies. Acute decompensation, first fills for high-value agents, and dose adjustments during monitored treatment support hospital-led dispensing. This channel benefits from the involvement of cardiologists and accredited health systems in multi-drug guideline-based therapy. Retail pharmacies remain vital for repeat prescriptions in mature drug classes like ACE inhibitors, beta blockers, and diuretics, though their growth is steadier. Institutional channels continue to dominate treatment initiation and clinical adjustments.

Online pharmacies are projected to grow at a 16.55% CAGR from 2026 to 2031, making them the fastest-growing distribution channel. Telehealth, e-prescribing, and patient preferences for remote refills are driving this shift. In heart failure care, mobility challenges and fatigue make digital dispensing more appealing for patients with advanced disease. Digital platforms also complement remote monitoring and post-discharge adherence programs, ensuring patients remain on therapy after hospitalization. Consequently, online pharmacies are expected to play a larger role in maintenance dispensing, while hospital pharmacies remain central to specialist-led treatment initiation.

Geography Analysis

In 2025, North America accounted for 39.52% of the congestive heart failure drugs market revenue, securing the largest market share. The U.S. drives this dominance with high drug spending, advanced cardiology infrastructure, and rapid adoption of updated guidelines across major healthcare systems. It was also the first market to approve key drugs in 2025 and 2026, including KERENDIA, AMVUTTRA, Lasix ONYU, and ENBUMYST. While generic sacubitril/valsartan entry in the U.S. is reducing branded ARNI revenue, it is expanding access for price-sensitive payers, maintaining broad treatment coverage.

Europe remains the second-largest region in the congestive heart failure drugs market, supported by the ESC guideline framework and specialist prescribing standards. Germany and the UK lead in adoption due to their influential review systems, which facilitate the transition of new therapies from approval to reimbursed care. In March 2026, the UK MHRA and the European Commission approved finerenone for adults with heart failure and LVEF of 40% or more, boosting the growth potential of the nonsteroidal MRA class. However, health technology assessment processes slow the rollout of premium products, creating a more measured access path compared to the U.S.

Asia-Pacific is projected to grow at a 15.26% CAGR from 2026 to 2031, making it the fastest-growing region in the congestive heart failure drugs market. China drives this growth with its large untreated population and price-led procurement strategies, which enhance access to mature cardiovascular drugs despite branded price pressures. India contributes with a growing patient base linked to aging, diabetes, and hypertension, while South Korea supports premium therapy adoption through its specialist care network. Japan shows steady growth, while South America, the Middle East, and Africa are emerging markets benefiting from urban aging, expanding cardiovascular centers, and improved reimbursement frameworks.

Competitive Landscape

The congestive heart failure drugs market features a moderately concentrated tier of innovators atop a broadly fragmented base of generics. AstraZeneca, along with the alliance of Boehringer Ingelheim and Eli Lilly, stands as the primary holder of the SGLT2 franchise. Their brands enjoy extensive endorsement across the spectrum of heart failure phenotypes. Bayer has strategically maneuvered KERENDIA through a swift approval sequence in the U.S., EU, and UK, achieving early leadership in the nonsteroidal MRA segment for HFmrEF and HFpEF. In contrast, Novartis is navigating a transitional phase post-Entresto's U.S. exclusivity loss, with its 2026 investor communication highlighting Leqvio's scale-up as a cornerstone of its forthcoming cardiovascular growth strategy.

HFpEF presents a relatively untapped opportunity in the congestive heart failure drugs market, given the limited number of agents with approved labels. Bristol Myers Squibb is capitalizing on this void, advancing BMS-986435 (or MYK-224) through Phase 2 in the AURORA program. This move underscores the belief among major players that there's still room for innovative, disease-modifying treatments beyond the current standards. Alnylam, adopting a similar forward-looking stance, is working on next-generation RNAi. They've positioned twice-yearly nucresiran as a potential successor to vutrisiran, contingent on favorable clinical results. Such initiatives indicate that future competition in the congestive heart failure drugs market will hinge not just on pricing and accessibility, but also on dosing convenience and unique mechanisms.

Viatris exemplifies the evolving landscape of the congestive heart failure drugs market. Traditionally seen as a generic player, Viatris made headlines by launching Inpefa in the UAE in January 2026, under an exclusive licensing deal with Lexicon. Both Teva and Viatris operate across the generic and innovative segments, reflecting the increasingly blurred boundaries of these competitive models. Success in this market requires more than product approval; companies must provide robust evidence for payer reviews, implement channel strategies that encourage refill behaviors, and align launch timing with specialist prescribing trends. While FDA-first approvals often set the pace for major launches, the prevalence of established generic classes prevents the market from being dominated by a few firms.

Congestive Heart Failure Drugs Industry Leaders

Novartis AG

AstraZeneca PLC

Boehringer Ingelheim International GmbH

Bayer AG

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SQ Innovation presented Phase 3 SUBCUT HF II trial results, showing Lasix ONYU reduced hospital stays by an average of 4 days compared to standard IV furosemide, strengthening the case for home-based subcutaneous diuresis.

- March 2026: Bayer received approvals for KERENDIA in the EU and UK for adults with heart failure and LVEF of 40% or more, completing a regulatory sweep across the U.S., EU, and UK within 9 months.

- January 2026: Viatris launched Inpefa in the UAE, marking its first commercialization of the dual SGLT1/2 inhibitor outside the U.S. and Europe, following a licensing agreement with Lexicon Pharmaceuticals in October 2024.

- September 2025: Hengrui Pharma signed an exclusive license agreement with Braveheart Bio for HRS-1893, a cardiac myosin inhibitor, with Braveheart leading global development outside China.

Global Congestive Heart Failure Drugs Market Report Scope

As per the scope of the report, congestive heart failure (CHF) is treated using a combination of medications designed to reduce the heart's workload, prevent fluid retention, and stop structural damage to the heart. Treatment generally relies on the "four pillars" of heart failure therapy.

The congestive heart failure drugs market is segmented by drug class, route of administration, distribution channel, and geography. By drug class, the market includes ACE inhibitors, angiotensin 2 receptor blockers, beta blockers, diuretics, aldosterone antagonists, SGLT2 inhibitors, angiotensin receptor-neprilysin inhibitors, inotropes, and other drug classes. By route of administration, the market is segmented into oral, injectable, and other routes of administration. By distribution channel, the market is categorized into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| ACE Inhibitors |

| Angiotensin 2 Receptor Blockers |

| Beta Blockers |

| Diuretics |

| Aldosterone Antagonists |

| SGLT2 Inhibitors |

| Angiotensin Receptor-Neprilysin Inhibitors |

| Inotropes |

| Other Drug Classes |

| Oral |

| Injectable |

| Other Routes of Administration |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | ACE Inhibitors | |

| Angiotensin 2 Receptor Blockers | ||

| Beta Blockers | ||

| Diuretics | ||

| Aldosterone Antagonists | ||

| SGLT2 Inhibitors | ||

| Angiotensin Receptor-Neprilysin Inhibitors | ||

| Inotropes | ||

| Other Drug Classes | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Other Routes of Administration | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the congestive heart failure drugs market?

The congestive heart failure drugs market reached USD 8.56 billion in 2026 and is forecast to reach USD 15.88 billion by 2031 at a CAGR of 13.16%.

Which drug class leads revenue and which one is growing the fastest?

ACE inhibitors led with 28.60% revenue share in 2025, while SGLT2 inhibitors are projected to grow the fastest at 14.99% CAGR through 2031.

Why are SGLT2 inhibitors gaining more use in heart failure treatment?

Their use is rising because guideline support now extends across HFrEF, HFmrEF, and HFpEF, which widens the eligible patient pool and supports faster adoption.

Which route of administration is changing the most?

Oral drugs still dominated with 76.45% share in 2025, but injectables are growing faster at 16.95% CAGR because new products are moving diuresis and specialty care closer to the home.

Which region matters most for growth over the next 5 years?

North America remained the largest region with 39.52% share in 2025, while Asia-Pacific is expected to grow the fastest at 15.26% CAGR through 2031.

What is the biggest commercial risk for branded products?

Generic entry and reimbursement pressure are the main risks, as shown by Entrestos 42% year-on-year revenue decline to USD 1.3 billion in Q1 2026 after U.S. generic entry in Q3 2025.

Page last updated on: