Targeted Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 187.30 Billion |

| Market Size (2031) | USD 423.30 Billion |

| Growth Rate (2026 - 2031) | 17.69% CAGR |

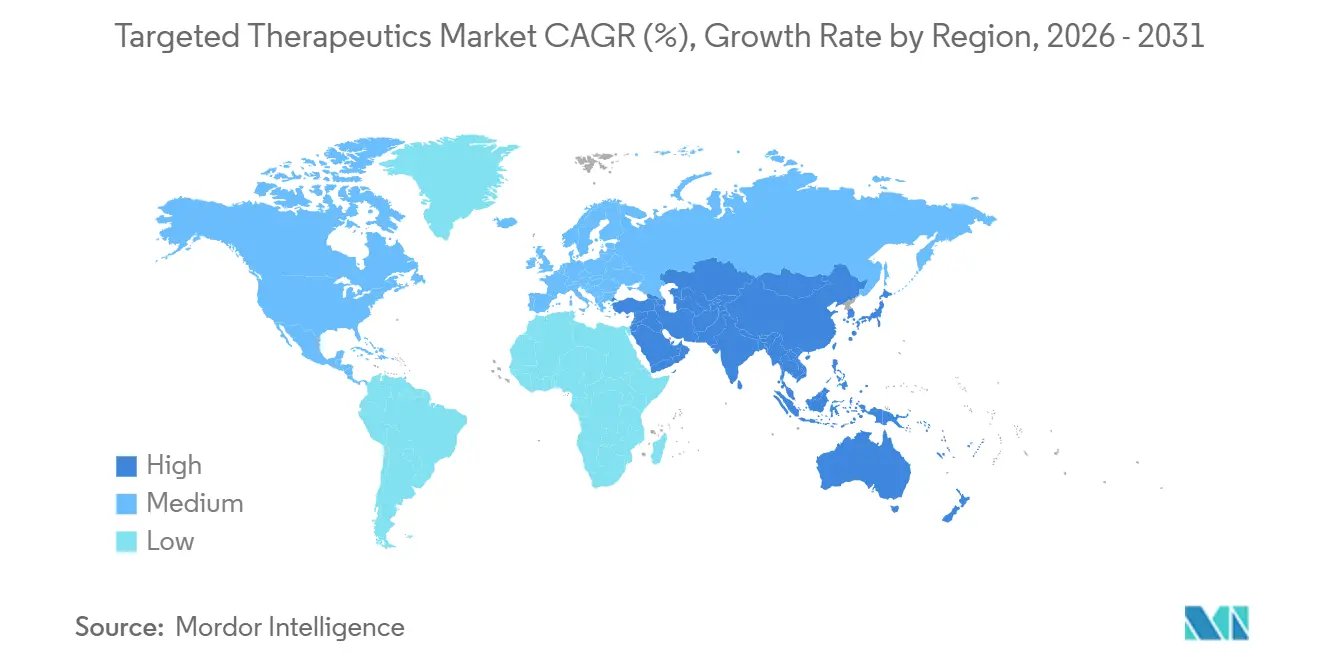

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

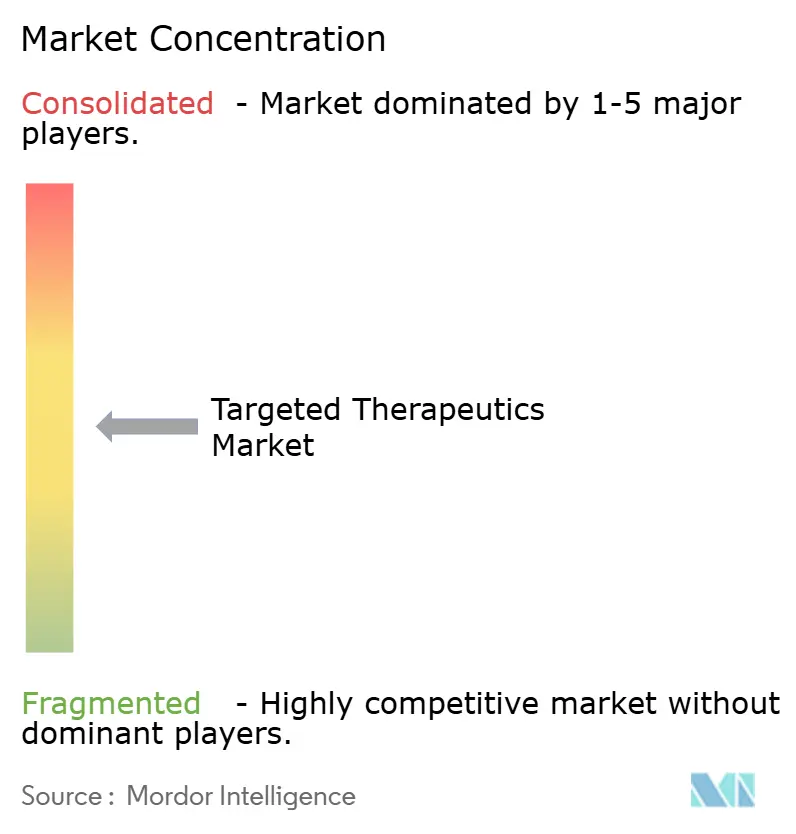

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Targeted Therapeutics Market Analysis by Mordor Intelligence

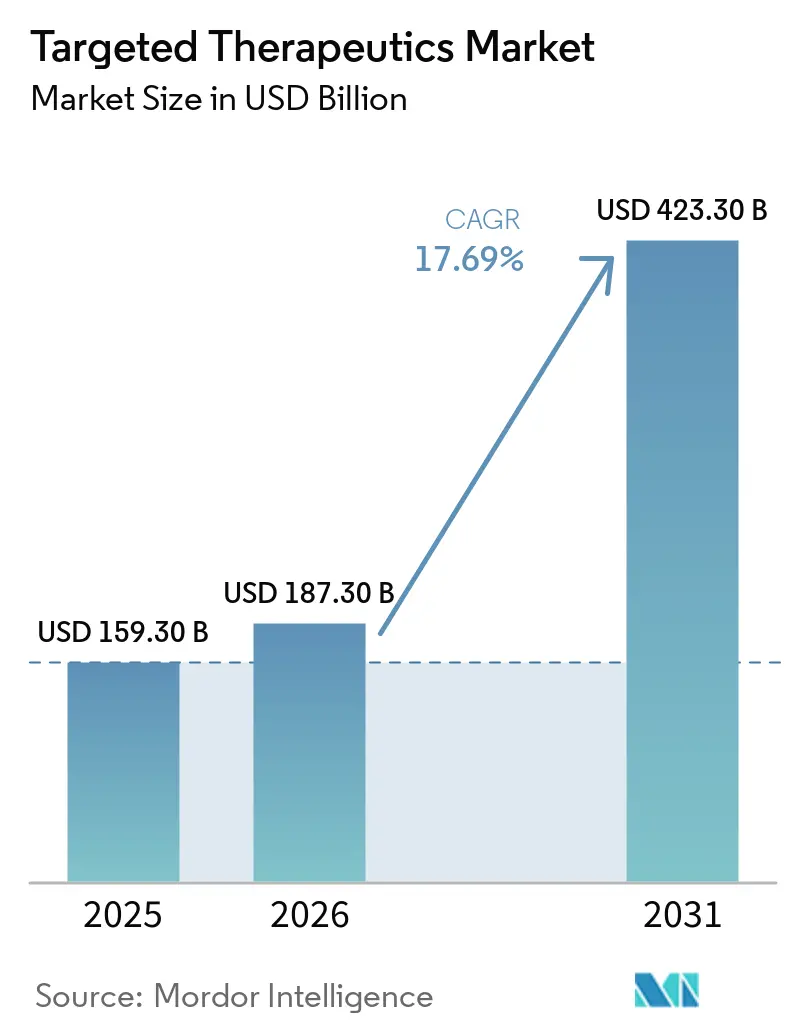

The Targeted Therapeutics Market size is expected to increase from USD 159.30 billion in 2025 to USD 187.30 billion in 2026 and reach USD 423.30 billion by 2031, growing at a CAGR of 17.69% over 2026-2031.

An oncology-heavy revenue mix, rapid monoclonal antibody (mAb) lifecycle extensions, and the steady roll-out of bispecifics and RNA-targeted drugs are widening the high-value patient pool even as biomarker stratification narrows individual indications. Payers in the United States and Europe are shifting reimbursements toward subcutaneous and long-acting formulations that trim facility fees and nursing time, accelerating the site-of-care migration from hospital infusion suites to physicians’ offices [1]Janssen Pharmaceutical Companies, “Amivantamab Subcutaneous Formulation,” JANSSEN.COM. Breakthrough and accelerated approval programs compressed regulatory review timelines by roughly four months for 15 targeted oncology drugs cleared in 2025, speeding cash-flow realization for new entrants. Meanwhile, biosimilar erosion in legacy biologic classes such as adalimumab and trastuzumab is forcing innovators to diversify into antibody-drug conjugate (ADC) and bispecific platforms, raising near-term capital spending on bioconjugation capacity.

Key Report Takeaways

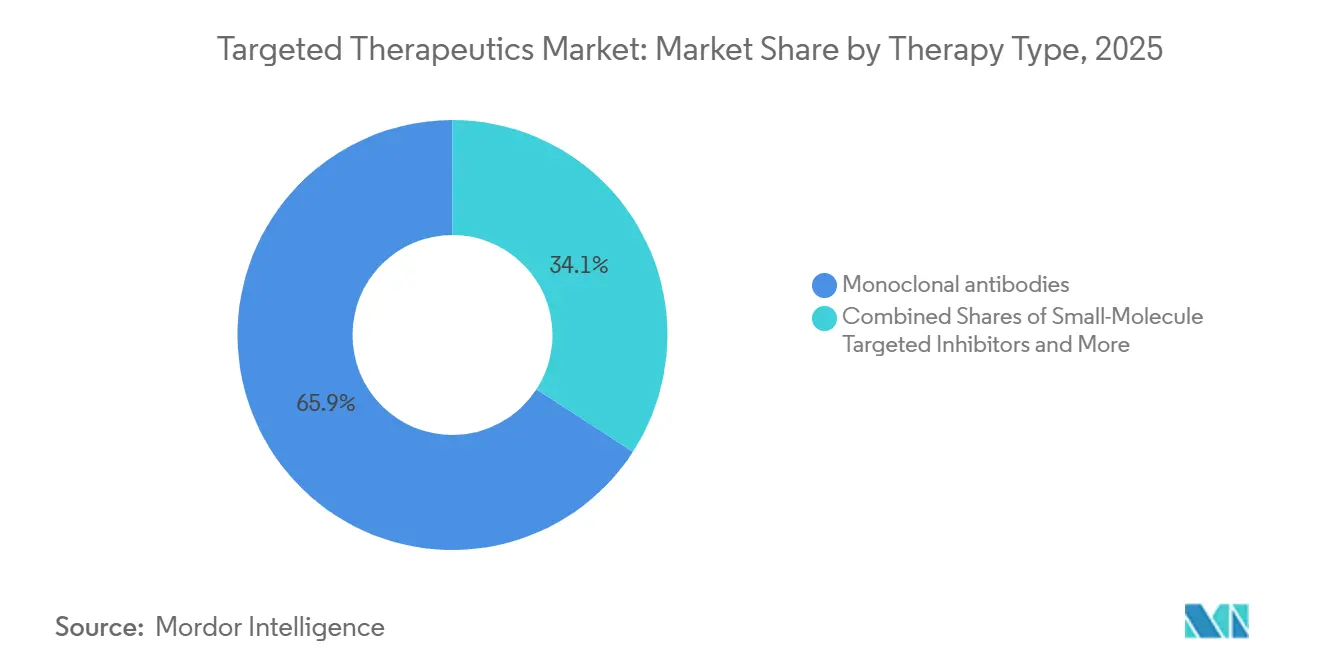

- By therapy type, monoclonal antibodies led with 65.87% revenue share in 2025 and are forecast to grow at a 24.19% CAGR to 2031, benefiting from subcutaneous launches that reduce infusion-related reactions.

- By application, oncology accounted for 68.90% of 2025 revenue, while the oncology segment is expected to expand at a 25.67% CAGR through 2031.

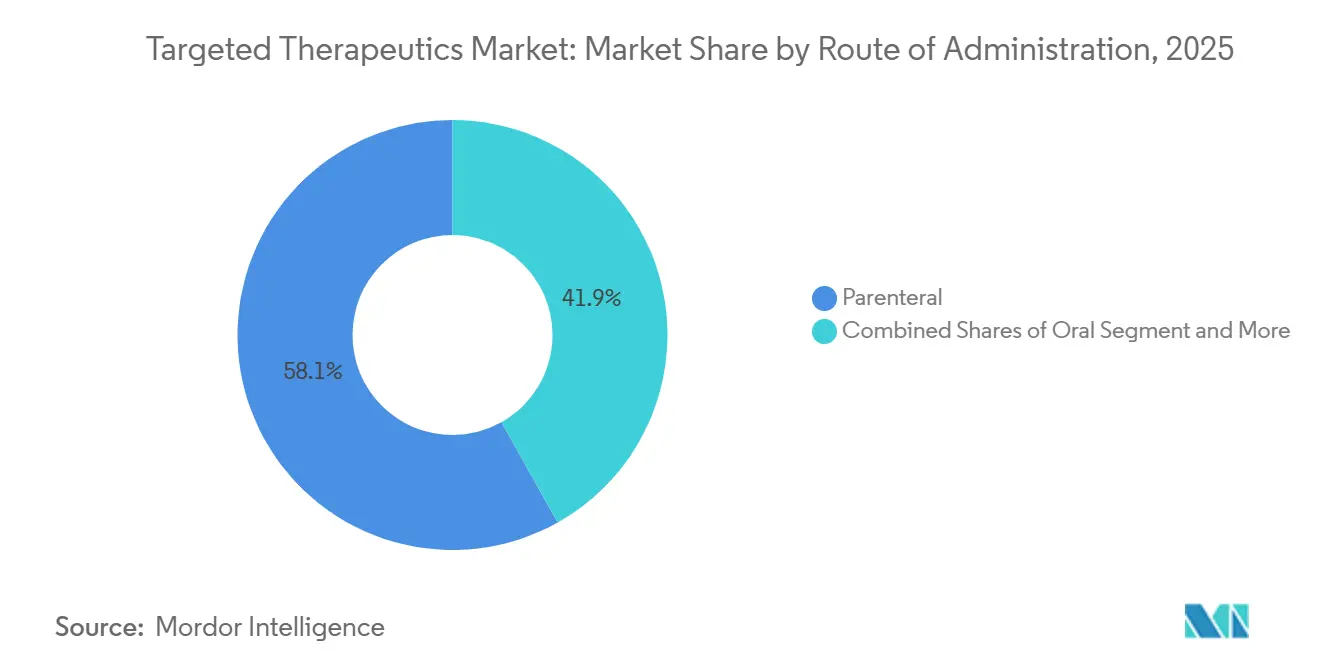

- By route of administration, the parenteral segment led with 58.15% revenue share in 2025, and is forecasted to grow at 25.28% CAGR through 2031.

- By distribution channels, the hospital pharmacies led with 61.39% market share in 2025, and online pharmacies are expected to grow at 26.87% CAGR in 2031.

- By geography, North America captured 47.30% of 2025 revenue, whereas Asia-Pacific is forecast to register the fastest regional growth at 22.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Targeted Therapeutics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding oncology adoption of biomarker-guided regimens | +4.2% | Global, with North America and the EU leading; APAC tier-1 cities catching up | Medium term (2-4 years) |

| Monoclonal antibody innovation and lifecycle extensions | +3.8% | Global, concentrated in North America, the EU, and Japan | Long term (≥ 4 years) |

| Label expansions and expedited approvals | +2.9% | North America, EU, Japan; spillover to South Korea, Australia | Short term (≤ 2 years) |

| North America scales with APAC acceleration | +2.6% | North America steady; China, India, South Korea rapid growth | Medium term (2-4 years) |

| ADC platform and deal momentum | +2.1% | U.S., Japan, China, and Ireland are manufacturing hubs | Medium term (2-4 years) |

| Shift to subcutaneous/long-acting formats | +1.7% | North America, Western Europe; gradual APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Oncology Adoption of Biomarker-Guided Regimens

Companion diagnostic approvals jumped 40% in 2025, enabling smaller, mutation-defined trials that lower late-stage attrition and boost per-patient revenue [2]Foundation Medicine, “FoundationOne CDx Comprehensive Genomic Profiling,” FOUNDATIONMEDICINE.COM. Medicare’s 2025 decision to reimburse next-generation sequencing (NGS) panels at up to USD 3,200 per test accelerated uptake among community oncology clinics. ACT Genomics’ April 2026 launch of a 101-gene, seven-day-turnaround panel is narrowing Asia-Pacific’s testing gaps and lifting the region’s patient eligibility ceiling. Broader testing has, in turn, raised demand for niche inhibitors such as KRAS G12C and RET fusions, supporting premium pricing despite smaller cohorts. The feedback loop between diagnostics and therapeutics is therefore expanding the targeted therapeutics market even as precision narrows individual indications.

Monoclonal Antibody Innovation and Lifecycle Extensions

Regulators cleared subcutaneous amivantamab in 2026, cutting chair time from five hours to under ten minutes and slashing infusion-related reactions by up to 80%. Similar launches, including subcutaneous nivolumab in December 2024 and ocrelizumab in 2024, illustrate an industry-wide shift toward patient-friendly formats. Japan’s Pharmaceuticals and Medical Devices Agency logged its 100th approved mAb in June 2025, confirming regulatory capacity to keep pace with complex biologics[3]Pharmaceuticals and Medical Devices Agency, “Approved Products,” PMDA.GO.JP. Lifecycle extensions now bundle long-acting delivery, novel linkers, and ADC conversions, prolonging exclusivity windows as originators brace for biosimilar erosion. As a result, mAbs remain the growth anchor within the targeted therapeutics market despite looming patent cliffs.

Label Expansions and Expedited Approvals Across Major Markets

The U.S. FDA’s breakthrough and accelerated pathways shaved roughly four months off median oncology review times in 2025, with 15 targeted agents benefiting from truncated cycles. Regeneron’s linvoseltamab-gcpt secured accelerated approval the same year after delivering a 70% overall response rate in multiple myeloma. Orphan-drug exclusivity extensions under revised 2025 guidance postpone biosimilar entry for premium assets such as pembrolizumab, reinforcing near-term pricing power. Rapid-fire label expansions enlarge total addressable populations without the cost of new pivotal trials. Consequently, expedited pathways are translating scientific breakthroughs into commercial returns faster, propelling the targeted therapeutics market.

North America Scale with APAC Acceleration in Access and Manufacturing

North America’s entrenched reimbursement and diagnostic infrastructure underpins a 47.30% revenue share, but the Inflation Reduction Act (IRA) price negotiations are squeezing launch prices and forcing manufacturers to capture value earlier in the product life cycle. Asia-Pacific manufacturers are filling global capacity gaps; Daiichi Sankyo committed USD 1.9 billion to ADC facilities spanning Japan, the United States, and China, while WuXi Biologics supports 252 ADC and 196 bispecific programs in its 7,000 m² network. Regulatory harmonization in China and Japan trimmed clinical start-up times by six to nine months, redirecting more trial activity to the region. The resulting production access flywheel is re-balancing the geography of the targeted therapeutics market over the next four years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability and payer controls on high-cost specialty drugs | -2.3% | Global, most acute in North America and EU; emerging in APAC | Short term (≤ 2 years) |

| Biosimilar erosion in key targeted biologic classes | -1.8% | EU leading; North America accelerating; APAC selective uptake | Medium term (2-4 years) |

| Capacity and CMC constraints for complex biologics (e.g., ADCs) | -1.5% | Global, with bottlenecks in North America, EU, Japan; gradual APAC build-out | Medium term (2-4 years) |

| Uneven biomarker testing and access limiting addressable populations | -1.2% | APAC, Middle East & Africa, South America; pockets in rural North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Affordability and Payer Controls on High-Cost Specialty Drugs

Medicare’s first IRA negotiation cycle set price ceilings for 10 Part D drugs in 2026, delivering USD 6 billion in federal savings but squeezing manufacturers’ lifetime revenue curves. European health technology assessment bodies, led by NICE, reject therapies exceeding GBP 50,000 per quality-adjusted life year, pressuring list prices of next-in-class inhibitors. Prior authorization hurdles delay treatment initiation by up to two weeks, cutting real-world adherence and reducing peak-year sales. Emerging markets, once pricing havens, are moving toward central procurement and external reference pricing, narrowing the arbitrage window. Collectively, these trends temper the otherwise high-growth trajectory of the targeted therapeutics market.

Biosimilar Erosion in Key Targeted Biologic Classes

Biosimilar trastuzumab and adalimumab captured 35% unit share in Europe by late 2025, slicing originator prices by up to 40%. The U.S. FDA’s 2024 interchangeability rulings on Amjevita and Renflexis unlocked pharmacy-level substitution without prescriber intervention, accelerating volume shifts. Herceptin biosimilars saved U.S. payers USD 15,000-25,000 per patient annually in 2025, redirecting budget toward new-generation agents. While innovators counter with ADC spin-outs and bispecific launches, erosion of flagship revenues still clips overall CAGR. This biosimilar drug underscores why lifecycle management remains pivotal within the targeted therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Monoclonal Antibodies Anchor Growth Through Format Innovation

Monoclonal antibodies held 65.87% of 2025 therapy-type revenue, and the targeted therapeutics market size for this segment is projected to expand at a 24.19% CAGR through 2031. The 2026 approval of five-minute subcutaneous amivantamab exemplifies how delivery upgrades protect margins even as biosimilars nibble at first-generation assets. ADC conversions further extend exclusivity: Daiichi Sankyo’s deruxtecan linker technology underpins multibillion-dollar deals with AstraZeneca and Merck, embedding future royalties into the segment’s growth curve.

Small-molecule targeted inhibitors, once the workhorses of precision oncology, now face cross-platform competition from bispecifics and ADCs that combine tumor-specific binding with cytotoxic payloads. Elevated manufacturing lead times, 18 months for GMP bioconjugation suites, signal tight capacity but also erect barriers to entry, consolidating short-term advantage among cash-rich incumbents. Collectively, these forces secure monoclonal antibodies’ role as the revenue backbone of the targeted therapeutics industry while encouraging portfolio diversification into next-generation constructs.

By Application: Oncology Dominates, While Non-Malignant Indications Accelerate

Oncology accounted for 68.90% of 2025 application revenue, and the targeted therapeutics market share for this segment is expected to climb further as oncology revenues grow at a 25.67% CAGR to 2031. Companion diagnostic coverage expansions under Medicare removed a major cost barrier, raising NGS uptake by community oncologists and expanding the treatable patient base.

Outside oncology, autoimmune and inflammatory diseases are catching up as IL-17 and JAK inhibitors gain reimbursement traction; the April 2025 FDA nod for Dupixent in chronic spontaneous urticaria opened a multi-billion-dollar market extension. Hematologic malignancies benefit from BCMA-targeted bispecifics like linvoseltamab, which posted a 70% overall response rate, hinting at blockbuster potential. Cardiometabolic disorders, once peripheral, are drawing attention through PCSK9 and Lp(a)-targeting siRNAs, aligning the pipeline with broad chronic-disease budgets. This diversification softens portfolio risk while preserving oncology’s centrality to the targeted therapeutics market.

By Route of Administration: Subcutaneous Shift Redefines Parenteral Delivery

Parenteral administration captured 58.15% of 2025 revenue and is projected to grow at a 25.18% CAGR through 2031, lifting its share of the targeted therapeutics market size as subcutaneous formats displace traditional infusions. The U.S. FDA cleared subcutaneous amivantamab in 2026, trimming chair time to roughly five minutes from the prior five-hour intravenous protocol and cutting infusion-related reactions fivefold. Bristol Myers Squibb’s Opdivo Qvantig reached the market in December 2024, and Genentech secured European approval for subcutaneous ocrelizumab the same year, confirming broad regulatory support for shorter, simpler dosing.

Intravenous delivery remains the default for antibody-drug conjugates and bispecific antibodies that need close cytokine-release monitoring, yet sponsors are piloting rapid-infusion protocols that cut administration from 90 to under 30 minutes. Intramuscular routes stay niche, limited to long-acting depots for chronic psychiatric and hormonal disorders. Oral therapies, led by small-molecule inhibitors such as tyrosine kinase and PARP agents, sidestep bioavailability hurdles that still constrain biologic capsules; adagrasib earned accelerated approval in 2024 for KRAS G12C-mutant colorectal cancer as part of an oral–IV combination

By Distribution Channels: Online Pharmacies Surge on Specialty Mail-Order Momentum

Hospital pharmacies held 61.39% of 2025 revenue, reflecting their role in managing cold-chain, reimbursement, and patient education for complex biologics. Online channels, however, are forecast to expand at a 26.87% CAGR through 2031, the fastest among distribution channels, as payers steer costly targeted therapies toward centralized mail-order models that cut plan spending by 12-15%.

Retail pharmacies face margin pressure as payers limit their role with high-cost biologics, yet they retain share in oral inhibitors and maintenance regimens that carry lower risk profiles. Specialty pharmacies' hybrid operations with both physical and online footprints manage roughly 75% of antibody-drug conjugate and bispecific prescriptions because they handle prior authorizations, copay support, and toxicity monitoring. Hospital pharmacies typically dominate the first 12-18 months after a drug’s launch, when clinicians prefer on-site oversight, but their share slips once real-world safety data mature and payers negotiate lower site-of-care fees.

Geography Analysis

North America held 47.30% of 2025 revenue, buoyed by early diagnostic adoption and payer support for site-of-care shifts to physician offices following subcutaneous roll-outs. The FDA cleared 15 breakthrough oncology agents in 2025, reinforcing the region’s innovation hub status. Samsung Biologics’ April 2025 expansion to 784,000 liters and Bristol Myers Squibb’s USD 40 billion, five-year U.S. investment signal long-term manufacturing anchorage.

Asia-Pacific is forecast to grow at 22.18% through 2031, powered by Chinese and Japanese regulatory streamlining that cut clinical start-up times by up to nine months. WuXi Biologics supports 252 ADC and 196 bispecific programs, making the region indispensable for global supply. India’s Shilpa Biologics and Syngene added OEB-5 bioconjugation suites in 2025, while ACT Genomics’ 101-gene panel upgrade addresses biomarker testing deficits, boosting patient eligibility.

Europe maintained a steady share in 2025 due to EMA biosimilar streamlining that shortened approval timelines by up to 18 months. Health technology assessments continue to constrain high-priced launches, yet reimbursement of subcutaneous formats that trim facility costs has broadened patient access. Infrastructure gaps persist in the Middle East & Africa and South America, where fewer than 25% of eligible patients receive NGS, keeping regional uptake muted despite high unmet need.

Competitive Landscape

The top 10 manufacturers controlled a significant share of 2025 revenue, indicating moderate concentration as portfolio breadth rather than single-asset dominance defines leadership. Bristol Myers Squibb’s USD 11.1 billion BioNTech tie-up, Takeda’s USD 11.4 billion Innovent licensing, and AbbVie’s USD 5.6 billion RemeGen outlay underscore a pivot to external innovation over in-house discovery. Biosimilar entrants, empowered by 2024 interchangeability designations, are peeling share from legacy mAbs, while originators fight back with ADC and bispecific launches.

Contract development and manufacturing organizations (CDMOs) are strategic king-makers. WuXi Biologics backs 945 integrated projects, including 99 at Phase III or commercial stages, offering turnkey scale to cash-strapped biotechs. Samsung Biologics’ record 18-month orderbook illustrates chronic capacity pinch points that could delay launches despite regulatory fast-tracking. Artificial-intelligence-based target discovery and antibody optimization platforms are proliferating, yet are largely embedded within big-pharma alliances rather than stand-alone disruptors at present. Collectively, these dynamics make the competitive terrain of the targeted therapeutics market both collaborative and fiercely contested.

Targeted Therapeutics Industry Leaders

Bristol Myers Squibb Company

AbbVie Inc.

Samsung Biologics

WuXi Biologics

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Celltrion received FDA Fast Track designation for CT-P71 and won Japanese approval for Stekimah IV, strengthening its global biosimilar footprint.

- April 2026: ACT Genomics launched a 101-gene NGS panel with a seven-day turnaround, improving testing access across Asia-Pacific.

- April 2025: Regeneron and Sanofi secured FDA approval for Dupixent to treat chronic spontaneous urticaria, opening a new autoimmune niche.

Global Targeted Therapeutics Market Report Scope

As per the scope of the report, targeted therapy is a type of precision medicine that uses drugs to identify and attack specific molecules, such as genes or proteins, that drive the growth and survival of cancer cells. Unlike traditional chemotherapy, which broadly kills all rapidly dividing cells, targeted therapy is designed to interfere with specific cellular processes unique to cancer cells while largely sparing healthy tissues.

The targeted therapy market is segmented by therapy type, application, route of administration, distribution channels, and geography. Based on therapy type, the market is segmented into oncology, autoimmune & inflammatory diseases, hematologic malignancies, respiratory & allergy, hematology, cardiovascular & metabolic, rare genetic & metabolic disorders, and infectious diseases. By therapy type, the market is segmented into monoclonal antibodies, small-molecule targeted inhibitors, antibody-drug conjugates (ADCs), bispecific and multispecific antibodies, and RNA-targeted therapeutics. By route of administration, the market is segmented into parental, oral, and others. By distribution channels, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Monoclonal Antibodies |

| Small-Molecule Targeted Inhibitors |

| Antibody-Drug Conjugates |

| Bispecific And Multispecific Antibodies |

| RNA-Targeted Therapeutics |

| Oncology |

| Autoimmune & Inflammatory Diseases |

| Hematologic Malignancies |

| Respiratory & Allergy |

| Hematology |

| Cardiovascular & Metabolic |

| Rare Genetic & Metabolic Disorders |

| Infectious Diseases |

| Parenteral |

| Oral |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Monoclonal Antibodies | |

| Small-Molecule Targeted Inhibitors | ||

| Antibody-Drug Conjugates | ||

| Bispecific And Multispecific Antibodies | ||

| RNA-Targeted Therapeutics | ||

| By Application | Oncology | |

| Autoimmune & Inflammatory Diseases | ||

| Hematologic Malignancies | ||

| Respiratory & Allergy | ||

| Hematology | ||

| Cardiovascular & Metabolic | ||

| Rare Genetic & Metabolic Disorders | ||

| Infectious Diseases | ||

| By Route of Administration | Parenteral | |

| Oral | ||

| Others | ||

| By Distribution Channels | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the targeted therapeutics market?

The targeted therapeutics market size stood at USD 187.3 billion in 2026 and is set to reach USD 423.3 billion by 2031.

Which therapy type holds the largest share in targeted therapeutics?

Monoclonal antibodies commanded 65.87% of 2025 revenue and are forecast to grow at a 24.19% CAGR, cementing their lead through 2031.

Which region is projected to grow fastest in targeted therapeutics?

Asia-Pacific is expected to advance at a 22.18% CAGR through 2031, boosted by large-scale ADC manufacturing investments and streamlined regulatory pathways.

How is U.S. price negotiation impacting targeted therapies?

Medicare’s Inflation Reduction Act negotiations lowered prices for 10 Part D drugs in 2026, saving USD 6 billion and compelling companies to accelerate value capture.

Page last updated on: