U.S. Cardiovascular & Soft Tissue Repair Patch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

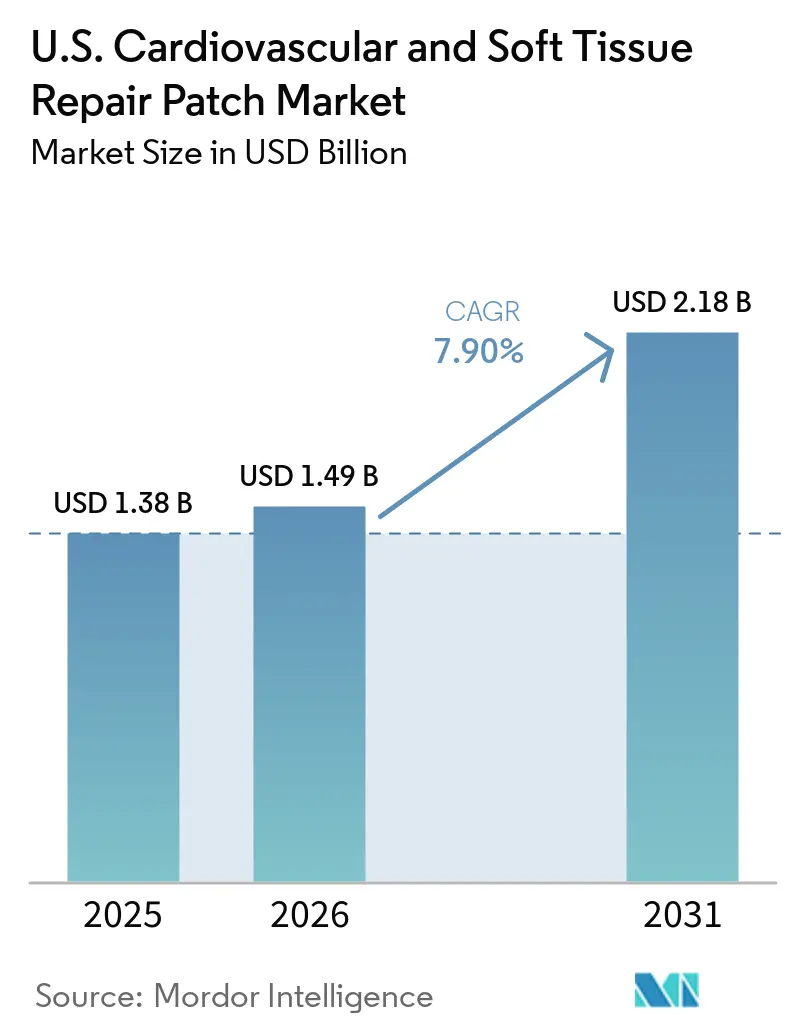

| Base Year Market Size (2025) | USD 1.38 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Cardiovascular & Soft Tissue Repair Patch Market Analysis by Mordor Intelligence

The U.S. Cardiovascular & Soft Tissue Repair Patch Market size is expected to increase from USD 1.38 billion in 2025 to USD 1.49 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 7.90% over 2026-2031.

The United States market for cardiovascular and soft tissue repair patches benefits from diverse clinical applications. These patches are utilized in congenital heart repairs, vascular arteriotomy closures, pericardial reconstructions, dural reinforcements, hernia repairs, and broader soft tissue reconstructions. This versatility stabilizes revenues, reducing exposure to declines in any single procedure category. The prevalence of congenital cardiovascular defects remains a key driver, with birth prevalence in high-income North America at 12.3 per 1,000 and an all-age prevalence of 466,566 individuals in the United States.[1]C.M. Holscher et al., “Impact of the 2023 Centers for Medicare & Medicaid Policy Change on Carotid Artery Stenting Utilization Among Medicare Beneficiaries,” Journal of Vascular Surgery via PubMed Central, pmc.ncbi.nlm.nih.gov Improved survival rates extend treatment needs over a longer patient lifecycle. Reoperation demand also plays a critical role, particularly in coronary artery bypass graft procedures.

Key Report Takeaways

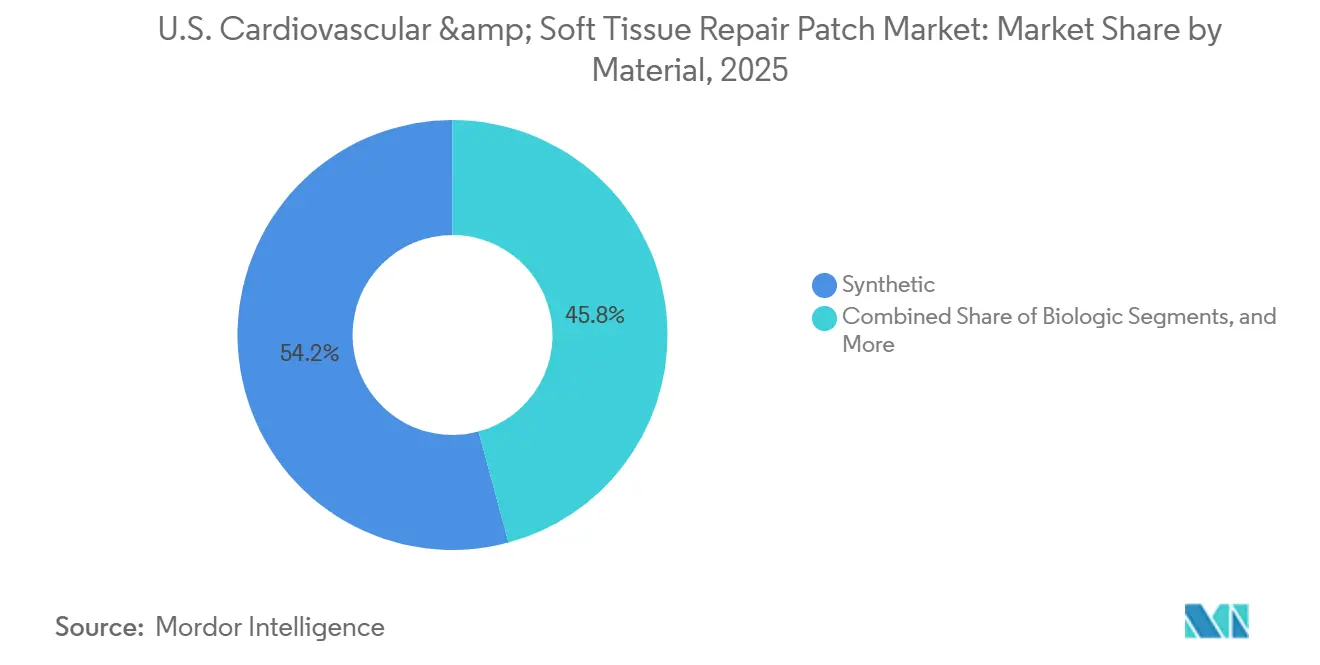

- By material, synthetic patches held 54.20% revenue share in 2025, while biologic patches are projected to expand at an 8.52% CAGR during 2026-2031.

- By application, soft tissue repair accounted for 40.45% of the U.S. cardiovascular and soft tissue repair patch market size in 2025, while cardiac repair is forecasted to grow at an 8.46% CAGR through 2031.

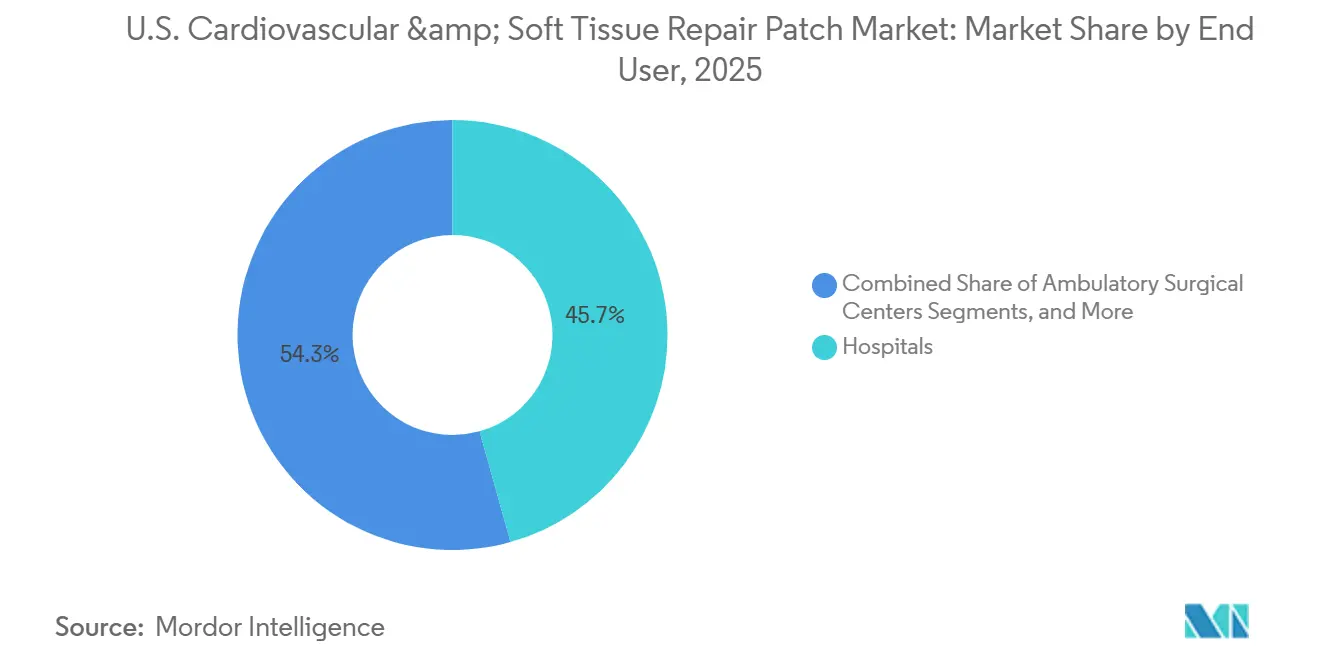

- By end user, hospitals held 45.65% of the U.S. cardiovascular and soft tissue repair patch market share in 2025, while specialty cardiovascular clinics and specialty surgical centers are expected to record the fastest growth at an 8.62% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Cardiovascular & Soft Tissue Repair Patch Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising carotid endarterectomy and open peripheral reconstruction volumes | +1.0% | National, with elevated concentration in Northeast and Mid-Atlantic high-volume vascular surgery programs | Short term (≤ 2 years) |

| Persistent congenital heart defect repair burden | +1.3% | National, with notable pediatric CHD volume at Southeast and Midwest academic cardiac centers | Medium term (2-4 years) |

| Biologic matrices gaining favor in infection-prone or complex cases | +1.8% | National, with higher adoption at high-acuity urban hospital systems and transplant centers | Medium term (2-4 years) |

| ASC migration of select soft tissue repair procedures | +1.5% | National, with early gains in Sun Belt states that have high ASC density and certificate-of-need free regulatory environments | Short term (≤ 2 years) |

| Redo sternotomy adhesion mitigation raising pericardial patch demand | +0.8% | National, concentrated at high-volume adult cardiac surgery programs | Medium term (2-4 years) |

| Pediatric patch selection shifting toward lower-calcification biologics | +0.7% | National, concentrated at pediatric cardiac surgery centers with long-term patient follow-up programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Carotid Endarterectomy and Open Peripheral Reconstruction Volumes

Carotid endarterectomy continues to drive direct patch demand as arteriotomy closure remains integral to the procedure. A 2025 analysis of 395,092 carotid revascularizations among Medicare beneficiaries from January 2017 to September 2024 showed carotid endarterectomy accounted for 76.7% of procedures, while carotid artery stenting represented 23.3%. Despite stenting's rise from 13% in 2017 to 38% by 2024, carotid endarterectomy remains the dominant treatment.[2]Academic Surgical Congress, “Association of Hospital Case Volume with Outcomes of Reoperative Coronary Artery Bypass Graft Surgery,” ASC Abstracts 2025, asc-abstracts.org Although total carotid revascularization volumes declined from 61,280 in 2017 to 43,735 in 2023, carotid endarterectomy cases continue to sustain patch demand. Additionally, open peripheral vascular reconstructions, such as femoral and iliac bypasses, further support patch-assisted closures in complex cases.

Persistent Congenital Heart Defect Repair Burden

Congenital heart defect repairs create long-term demand as patients often require multiple interventions from infancy into adulthood. The American Heart Association reported a birth prevalence of 12.3 per 1,000 in North America, with a 2024 United States prevalence of 466,566 individuals, 60% of whom were under 20 years old.[3]American Heart Association, “2025 Heart Disease & Stroke Statistics Update Fact Sheet, Congenital Cardiovascular Defects,” American Heart Association, professional.heart.org The Society of Thoracic Surgeons' 2024 database update highlighted growth in procedure volumes, with atrial and ventricular septal defect patch repairs among the most common. This recurring demand, influenced by regional cost and stay variations, underscores the importance of flexible pricing and diverse product offerings for suppliers.[4]F. Donato et al., “Treatment of Aorto-iliac and Infrainguinal Vascular Infections with a Prefabricated Bovine Pericardial Graft,” Annals of Vascular Surgery, doi.org

Biologic Matrices Gaining Favor in Infection-Prone or Complex Cases

Biologic materials are gaining traction in high-risk and contaminated surgical fields due to their superior infection control and tissue integration. A 2024 study demonstrated favorable outcomes with bovine pericardial grafts in vascular infections, supporting biologics in complex cases. This trend is expanding the biologic patch market in the United States, particularly for vascular and cardiac repairs where durability and infection resistance are critical. The biologics market is poised for growth from 2026 to 2031, with stringent FDA and tissue bank standards ensuring supply chain discipline.

ASC Migration of Select Soft Tissue Repair Procedures

Reimbursement policies are driving the migration of soft tissue repair procedures to ambulatory surgery centers (ASCs). The 2026 CMS final rule added 86 cardiovascular procedure codes to the ASC-approved list, enabling more outpatient procedures. ASCs prefer lightweight, single-use patches that streamline workflows and reduce turnover time. TELA Bio’s 2024 launch of robotic-compatible OviTex IHR aligns with this trend, catering to minimal-access procedures. Suppliers lacking efficient packaging and ASC-compatible formats risk long-term disadvantages as this shift accelerates.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High biologic patch acquisition cost and reimbursement gaps | -1.0% | National, most acute in rural and community hospital settings with limited GPO leverage and thin operating margins | Medium term (2-4 years) |

| Product failure, recall risk, and durability concerns | -0.8% | National, particularly impactful at high-volume academic centers that conduct systematic post-market surveillance | Long term (≥ 4 years) |

| Endovascular and Transcatheter Substitution Reducing Open-Patch Case Mix | -0.7% | National, most acute in rural and community hospital settings with limited GPO leverage and thin operating margins | Medium term (2-4 years) |

| Single-Source Tissue Processing and Biologic Raw-Material Dependence | -0.5% | National, particularly impactful at high-volume academic centers that conduct systematic post-market surveillance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Biologic Patch Acquisition Cost and Reimbursement Gaps

Biologic cardiovascular patches face adoption challenges due to high acquisition costs, often exceeding those of synthetic alternatives. This pricing disparity complicates value analysis reviews, slows hospital transitions, and extends the commercial cycle for premium products in the United States. Reimbursement remains fragmented, with many biologic patches requiring payer negotiations and institutional approvals, delaying adoption by 6 to 18 months. Suppliers also report revenue pressures when premium products encounter procurement resistance or budget scrutiny.

Product Failure, Recall Risk, and Durability Concerns

Durability is critical in cardiac and vascular surgeries, as patch selection impacts risks like late failure, infection, and calcification. The United States market closely monitors post-market performance, especially in academic centers. Pediatric use raises concerns due to calcification risks with glutaraldehyde-fixed bovine pericardium, driving interest in lower-calcification bioscaffold options. Despite promising results from newer formats, manufacturers face strict FDA and ISO 13485 standards, where recalls or safety issues can quickly affect surgeon confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biologics Accelerating Despite Synthetic Volume Leadership

In 2025, synthetic patches held a 54.20% revenue share in the United States cardiovascular and soft tissue repair patch market. Their dominance is driven by the cost efficiency, dimensional consistency, and clinical familiarity of materials like ePTFE, polyester, and polypropylene. ePTFE remains critical for carotid and peripheral arteriotomy closures due to its reliability and procedural familiarity. Synthetic products also benefit from simplified procurement processes, enabling predictable price-performance alignment.

Biologic patches are projected to grow at an 8.52% CAGR from 2026 to 2031, driven by their use in contaminated fields, infection-prone repairs, and cases requiring better tissue integration. Bovine pericardium is the most widely used biologic material, while porcine SIS and ECM-based formats are gaining traction in reconstruction and cardiac applications, expanding their adoption beyond niche uses.

By Application: Soft Tissue Volume Drives Revenue, Cardiac Repair Accelerating

Soft tissue repair accounted for 40.45% of the United States cardiovascular and soft tissue repair patch market in 2025, driven by frequent procedures like hernia repair, abdominal wall reconstruction, and breast reconstruction. This segment benefits from a diversified demand base across hospital and outpatient settings, addressing both routine and complex needs.

Cardiac repair is the fastest-growing application, with an 8.46% CAGR forecast from 2026 to 2031. Growth is supported by congenital heart defect surgeries, redo cardiac procedures, and the expansion of structural heart programs. Vascular repair remains the second-largest application, driven by carotid endarterectomy closures and peripheral bypasses, with additional demand from vascular graft infections.

By End User: Hospitals Retain Majority, Specialty Centers Outpacing Growth

Hospitals held 45.65% of the revenue in the United States cardiovascular and soft tissue repair patch market in 2025. Their dominance stems from the need for advanced surgical capabilities and multidisciplinary teams for high-acuity procedures. Hospitals also favor products with strong clinical evidence and reliable supply chains.

Ambulatory surgical centers are the second-largest end-user segment, focusing on high-volume, lower-acuity procedures with faster throughput. Specialty cardiovascular clinics and surgical centers are the fastest-growing category, with an 8.62% CAGR projected from 2026 to 2031, driven by a broader procedure mix and efficiency-focused purchasing strategies.

Geography Analysis

The Northeast and Mid-Atlantic remain the highest-intensity demand centers due to their dense academic medical infrastructure, high-volume vascular surgery programs, transplant hospitals, and referral-based congenital heart centers. These regions account for a significant share of premium biologic and extracellular matrix patch usage, particularly in high-acuity procedures where clinical nuances drive procurement decisions over unit price.

The Sun Belt is the fastest-growing regional market within the United States cardiovascular and soft tissue repair patch sector. This growth is fueled by population expansion, a high burden of cardiovascular risk factors, and rapid development of ambulatory surgery infrastructure. States like Texas, Florida, and Arizona combine growing patient pools with policies favoring outpatient procedural migration. Markets without certificate-of-need laws have seen faster ASC expansion, benefiting patch suppliers as outpatient buyers prioritize procedural efficiency and predictable economics.

Rural parts of the Midwest and Mountain West remain the most underserved areas in the United States cardiovascular and soft tissue repair patch market. Limited hospital infrastructure, lower surgeon case volumes, and access barriers restrict referral conversion into advanced procedures. While clinical demand exists, these regions face challenges due to fewer specialists and centers capable of supporting complex cardiac or vascular patch use at scale.

Competitive Landscape

The United States cardiovascular and soft tissue repair patch market is moderately consolidated, with W. L. Gore & Associates, LeMaitre Vascular, Baxter International, and Artivion leading in synthetic and established biologic categories. These companies leverage scale, surgeon familiarity, regulatory expertise, and long-standing hospital relationships, creating significant competitive advantages. Synthetic patch leadership remains strong due to physician preference for familiar handling characteristics and purchasing teams' focus on stable supply and clear evidence reviews.

Competitive opportunities are emerging where biologic performance meets procedural efficiency, attracting niche specialists. TELA Bio has utilized its ovine rumen extracellular matrix platform to establish a presence in inguinal hernia repair, reconstructive surgery, and resorbable formats. By March 2025, the company reported over 45,000 implantations, supported by 35 clinical studies. Its 2024 launch of the robotic-compatible OviTex IHR highlights a focus on minimal-access workflows and outpatient procedure growth.

Barriers to entry remain significant despite a narrowing technical gap. FDA 510(k) and PMA requirements, tissue handling standards, ISO 13485 compliance, and post-market surveillance create high thresholds for smaller players. However, new entrants gain traction by offering superior biocompatibility, better handling in complex cases, or procedure-efficient formats for ambulatory surgical centers and specialty settings. The competitive landscape balances incumbents defending core volumes through scale and specialists targeting unmet needs in specific cases and settings.

U.S. Cardiovascular & Soft Tissue Repair Patch Industry Leaders

Baxter International Inc.

CorMatrix Cardiovascular, Inc.

Becton, Dickinson and Company

W. L. Gore & Associates, Inc.

Edwards Lifesciences Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Artivion acquired Endospan Ltd., developer of the FDA-approved NEXUS Aortic Arch System, for USD 135 million upfront and up to USD 200 million in performance-based payments. This expanded Artivion's portfolio into endovascular aortic arch repair, addressing unmet needs in complex aortic diseases.

- April 2026: Artivion received U.S. FDA premarket approval for the NEXUS Aortic Arch System, the first endovascular therapy for complex aortic arch diseases. The approval enabled Artivion to draw a USD 150 million term loan to fund the acquisition.

- February 2026: W. L. Gore & Associates completed the acquisition of Conformal Medical, developer of the investigational CLAAS AcuFORM System for left atrial appendage occlusion. The deal expanded Gore's cardiovascular portfolio into structural heart interventions.

U.S. Cardiovascular & Soft Tissue Repair Patch Market Report Scope

As per the scope of the report, a cardiovascular and soft tissue repair patch is a specialized medical scaffold used to reinforce, seal, or replace damaged or weakened tissues in the body. These biocompatible patches, often made from biological (e.g., bovine pericardium) or synthetic materials, are critical for repairing congenital heart defects, repairing hernias, and reconstructing blood vessels.

The U.S. cardiovascular & soft tissue repair patch market is segmented by material, application, end-user, and geography. By material, the market includes synthetic (ePTFE, polyester, polypropylene, and other synthetics), biologic (bovine pericardium, porcine SIS/ECM, human acellular dermal matrix), and tissue-engineered/composite (bioengineered ECM scaffolds, hybrid resorbable composites). By application, the market is segmented into cardiac repair, vascular repair and reconstruction, pericardial repair, dural repair, and soft tissue repair. By end-user, the market is segmented into hospitals, ambulatory surgical centers, and specialty cardiovascular clinics & specialty surgical centers. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Synthetic | ePTFE |

| Polyester | |

| Polypropylene and other synthetics | |

| Biologic | Bovine pericardium |

| Porcine SIS / ECM | |

| Human acellular dermal matrix | |

| Tissue-engineered / Composite | Bioengineered ECM scaffolds |

| Hybrid resorbable composites |

| Cardiac Repair |

| Vascular Repair and Reconstruction |

| Pericardial Repair |

| Dural Repair |

| Soft Tissue Repair |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Cardiovascular Clinics and Specialty Surgical Centers |

| By Material | Synthetic | ePTFE |

| Polyester | ||

| Polypropylene and other synthetics | ||

| Biologic | Bovine pericardium | |

| Porcine SIS / ECM | ||

| Human acellular dermal matrix | ||

| Tissue-engineered / Composite | Bioengineered ECM scaffolds | |

| Hybrid resorbable composites | ||

| By Application | Cardiac Repair | |

| Vascular Repair and Reconstruction | ||

| Pericardial Repair | ||

| Dural Repair | ||

| Soft Tissue Repair | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Cardiovascular Clinics and Specialty Surgical Centers | ||

Key Questions Answered in the Report

How large is the U.S. cardiovascular and soft tissue repair patch market in 2026 and 2031?

The U.S. cardiovascular and soft tissue repair patch market size stands at USD 1.38 billion in 2026 and is projected to reach USD 2.18 billion by 2031, growing at a 7.90% CAGR.

Which material segment leads revenue in patch-based cardiovascular and soft tissue repair in the United States?

Synthetic patches led revenue in 2025 with a 54.20% share, helped by cost efficiency, consistent handling, and long clinical use in vascular repair.

Which application area contributes the most revenue in this space?

Soft tissue repair was the largest application in 2025 with a 40.45% share, supported by high volumes in hernia repair, abdominal wall reconstruction, and breast reconstruction.

What is driving faster growth in biologic patches?

Growth is being supported by rising use in contaminated and complex cases where surgeons favor tissue integration and lower infection risk over simple unit-cost advantages.

Why are specialty centers growing faster than hospitals for patch demand?

Specialty cardiovascular clinics and specialty surgical centers are projected to grow at an 8.62% CAGR because more procedures are shifting into outpatient settings and those facilities prefer efficient, standardized products.

What is the biggest commercial challenge for biologic patch suppliers?

High acquisition cost and uneven reimbursement remain major barriers because hospital approval can be slow, especially when buyers compare premium biologics against far cheaper synthetic alternatives.

Page last updated on: