Organ Transplant Rejection Medication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.70 Billion |

| Market Size (2031) | USD 6.80 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

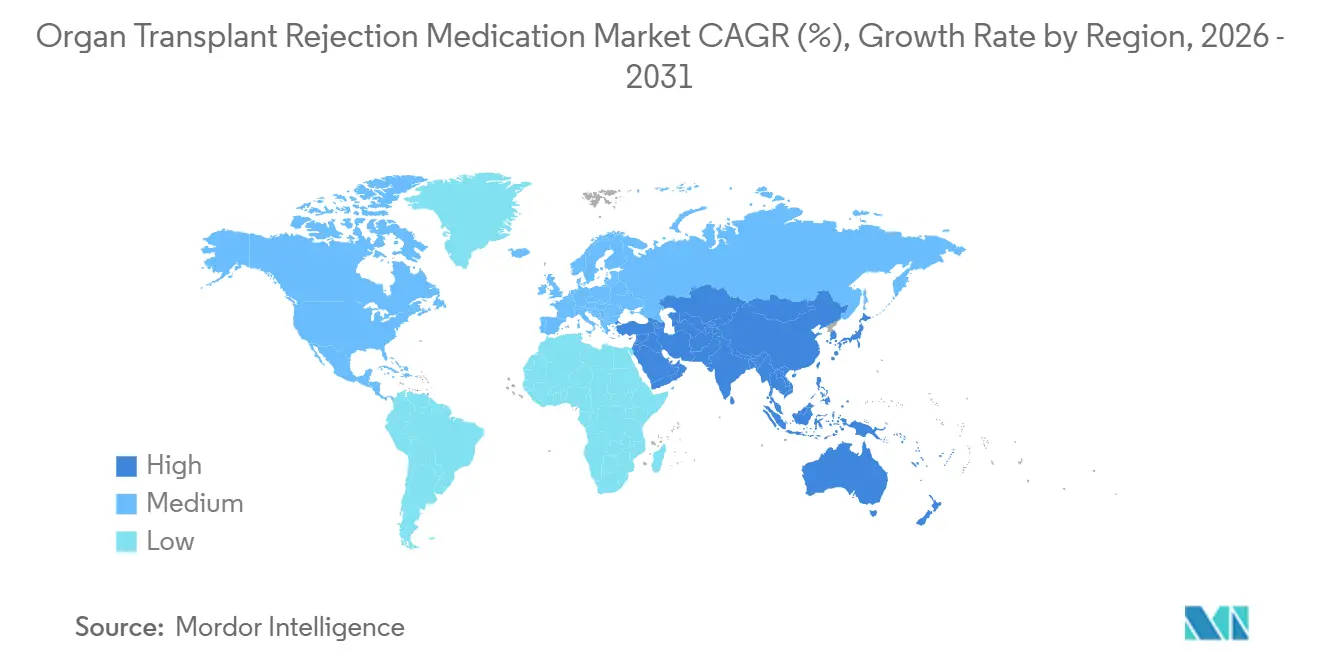

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

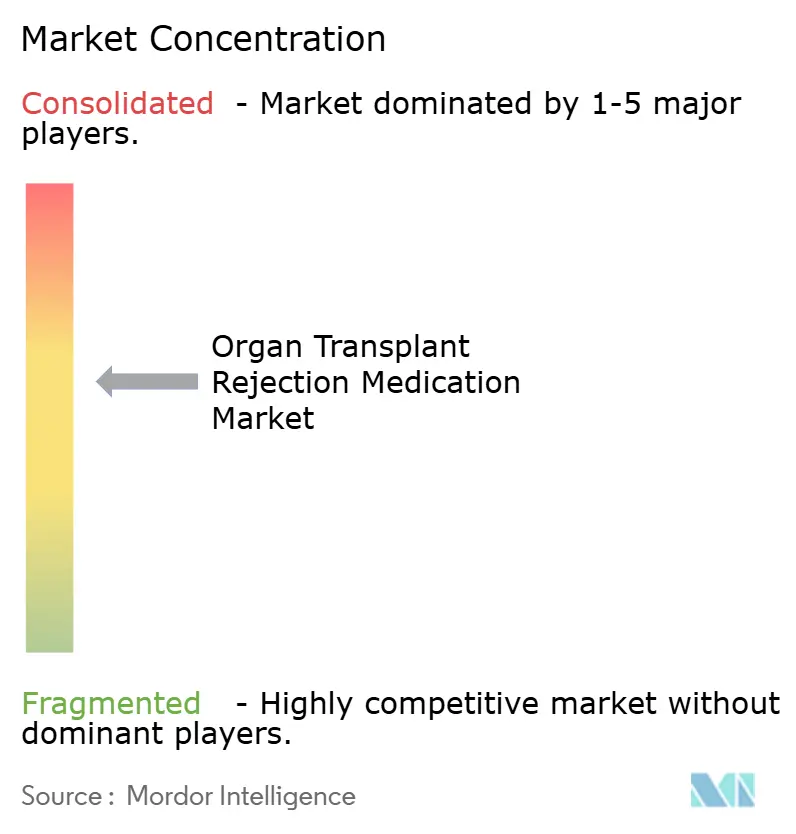

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organ Transplant Rejection Medication Market Analysis by Mordor Intelligence

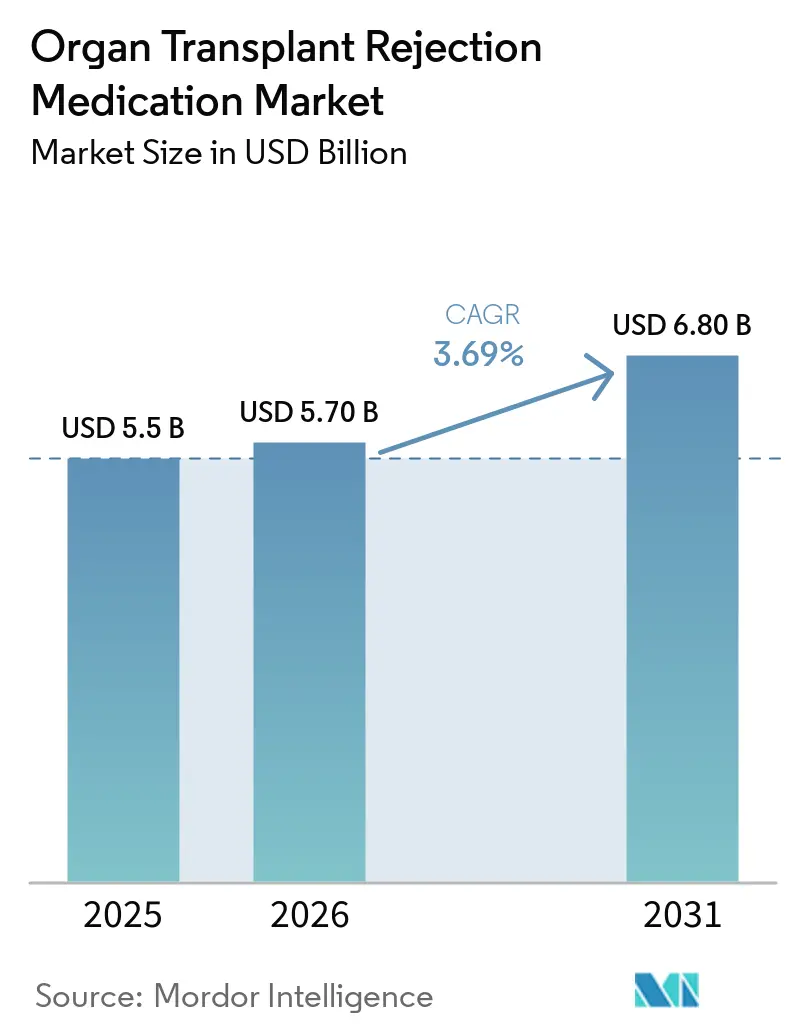

The Organ Transplant Rejection Medication Market size was valued at USD 5.5 billion in 2025 and is estimated to grow from USD 5.70 billion in 2026 to reach USD 6.80 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031).

Sustained procedure growth, especially kidney transplants, keeps demand for chronic immunosuppression resilient even as widespread generic entry weighs on pricing. Therapeutic-equivalence downgrades for certain tacrolimus generics have slowed automatic substitution and preserved a modest premium for brand-name formulations. At the same time, antibody-mediated rejection (AMR) protocols that rely on high-dose IVIG and complement inhibition are enlarging the clinical need for biologics. Payer-driven specialty-pharmacy models and Medicare’s coverage extension are stabilizing adherence in the United States, while rapid infrastructure build-outs in China and India position Asia-Pacific as the fastest-growing geography within the organ transplant rejection medication market.

Key Report Takeaways

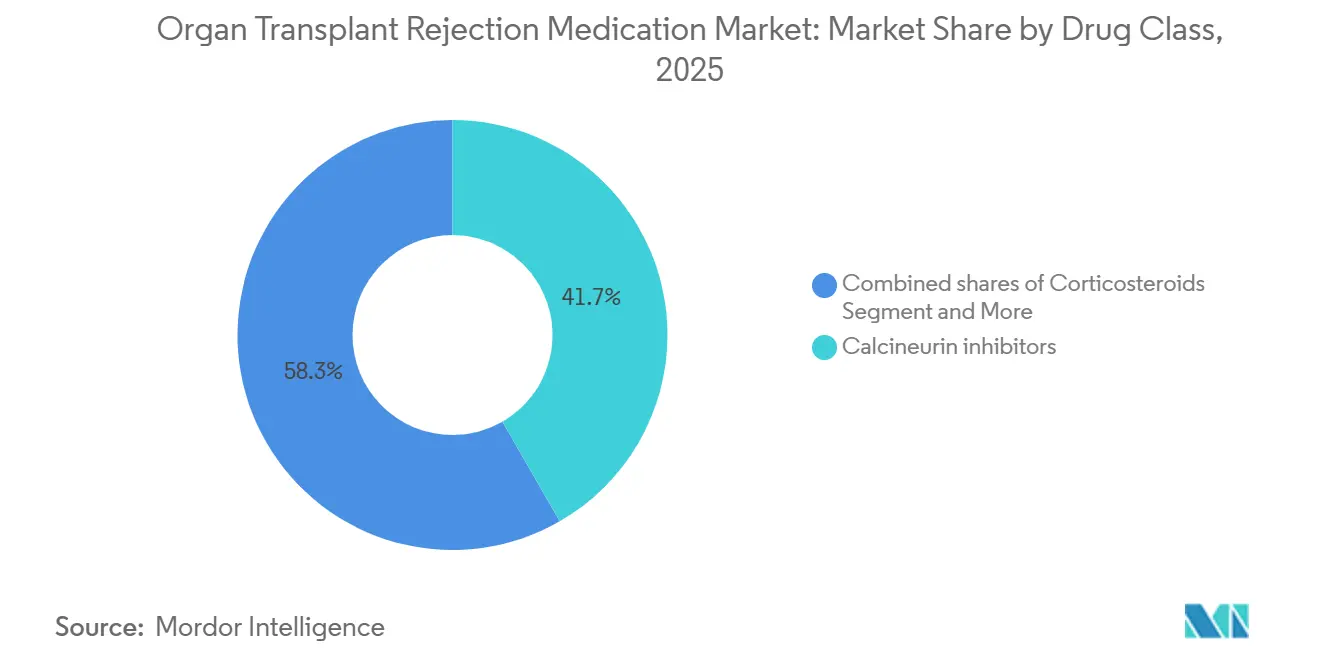

- By drug class, calcineurin inhibitors held 41.68% of the organ transplant rejection medication market share in 2025, and mTOR inhibitors are forecast to rise at 3.98% by 2031.

- By transplant type, kidney procedures commanded 48.19% of 2025 revenue and are advancing at a 4.05% CAGR through 2031.

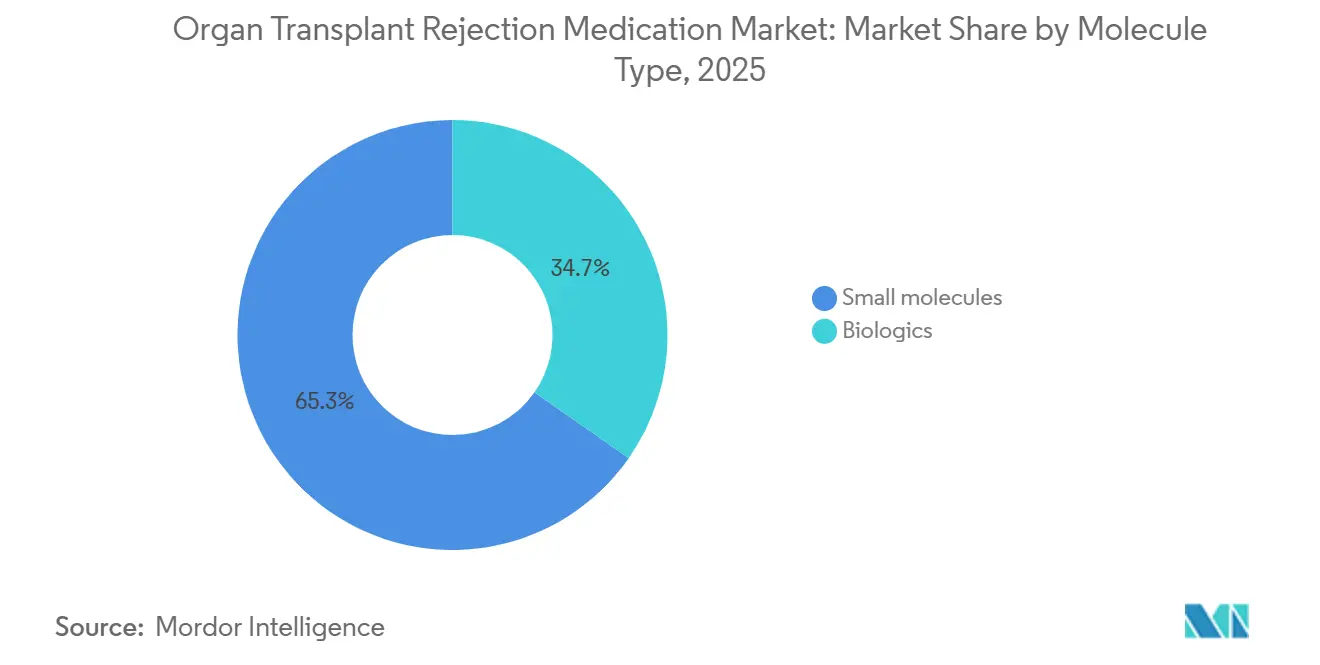

- By molecule type, small molecules accounted for 65.29% of the organ transplant rejection medication market size in 2025 and are forecast to expand at a 3.90% CAGR over 2026-2031.

- By distribution channel, transplant centers/hospital pharmacies captured 53.98% revenue in 2025 and specialty pharmacies represent the fastest-growing channel with a 3.85% CAGR over 2026-2031.

- By geography, North America captured 43.19% of global 2025 revenue, whereas Asia-Pacific is projected to grow at a 3.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organ Transplant Rejection Medication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising transplant volumes; kidney accounts for the majority of solid organ procedures | +1.2% | Global, with North America and Asia-Pacific leading absolute growth | Medium term (2-4 years) |

| Tacrolimus-based CNI regimens remain the maintenance backbone across SOTs | +0.9% | Global | Long term (≥ 4 years) |

| North America leads revenue share; coverage expansions sustain chronic therapy adherence | +0.7% | North America, spill-over to Europe | Medium term (2-4 years) |

| Oral maintenance dominance; hospital/specialty channels anchor dispensing | +0.5% | Global | Long term (≥ 4 years) |

| Extended-release tacrolimus adoption improves exposure stability and adherence | +0.4% | North America, Europe | Short term (≤ 2 years) |

| AMR management intensifies use of IVIG and complement-targeted adjuncts | +0.6% | Global, with North America and Europe early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Transplant Volumes Anchor Chronic Immunosuppression Demand

Kidney transplantation accounted for a significant share of 2025 revenue and continues to outpace the liver and heart segments, as 27,573 kidney procedures were performed in the United States in 2025 and 22,814 in China in 2023[1]United Network for Organ Sharing, “Transplants in America,” UNOS.org. Medicare’s coverage reforms eliminated the 36-month payment cliff, cutting non-adherence-driven graft loss by roughly 15% and expanding the treated population. India’s National Organ and Tissue Transplant Organization reports 15,000-20,000 annual kidney transplants, underscoring Asia-Pacific’s pivotal role in the organ transplant rejection medication market. Japan remains supply-constrained with only about 2,000 kidney transplants per year because its deceased-donor rate is just 1.7 per million people. Volume growth thus delivers the single-largest positive increment to CAGR forecasts through 2031.

Tacrolimus-Based CNI Regimens Remain the Global Workhorse

Calcineurin inhibitors held a significant share in 2025, with tacrolimus accounting for the majority of CNI prescriptions. Although generic penetration surged significantly, the FDA’s 2023 downgrade of one tacrolimus generic from AB to BX slowed new substitutions, prompting most U.S. programs to sign single-source agreements to avoid formulation variability. Extended-release tacrolimus, marketed as Envarsus XR, offers higher bioavailability and once-daily dosing, yet payer reluctance toward its price premium limits broad adoption. This mixed pricing-and-volume strategy contributes to the market's growing CAGR.

North American Coverage Keeps Adherence High

North America produced a major global revenue in 2025, in part because Medicare’s immunosuppressive-drug extension immediately added about 50,000 chronically treated kidney recipients [2]Centers for Medicare & Medicaid Services, “Medicare Coverage of Immunosuppressive Drugs,” CMS.gov. CVS Specialty, Accredo, and Walgreens Specialty collectively managed the majority of U.S. dispensing by 2025, reinforcing payer oversight through prior authorization and therapeutic-drug-monitoring programs. Medicaid expansion in 12 additional U.S. states since 2024 offers incremental growth, though this effect is expected to fade after 2028.

Extended-Release Tacrolimus Boosts Adherence, Faces Cost Barriers

Envarsus XR captured a modest share of tacrolimus prescriptions in 2025 and showed acute-rejection rates lower than those with immediate-release tacrolimus in a 2024 cohort study. Despite these gains, step-therapy requirements and higher prices slow uptake. Unless long-term outcomes translate into payer savings, the driver’s incremental impact is projected to plateau by 2029.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price erosion from widespread generics across tacrolimus/MMF/sirolimus | -0.8% | Global | Long term (≥ 4 years) |

| Infection, malignancy, and metabolic risks drive minimization and regimen switches | -0.5% | Global | Medium term (2-4 years) |

| Regulatory/quality frictions (e.g., TE-rating changes) slow generic substitution in some markets | -0.3% | North America, Europe | Short term (≤ 2 years) |

| IV infusion logistics and EBV-serostatus limits cap uptake of certain biologics | -0.2% | Global, with North America and Europe most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Erosion Compresses Per-Patient Revenue

Generics seized the majority of the mycophenolate segment by 2025, while tacrolimus prices fell significantly since patent expiry, cutting Roche’s CellCept sales from USD 2.4 billion in 2010 to roughly USD 350 million in 2026 [3]F. Hoffmann-La Roche, “Annual Report 2025,” Roche.com. Similar patterns afflict sirolimus and everolimus following multiple generic launches. Although single-source contracts curb interchangeability, they also lock in discounted rates, amplifying the negative CAGR contribution.

Infection and Malignancy Concerns Drive Minimization

Opportunistic infections and de novo malignancies affect up to a notable share of thoracic-organ recipients, spurring early steroid withdrawal and lower tacrolimus trough targets. Belatacept gained notable sales growth in Q3 2025 but remains limited to EBV-seropositive patients and requires monthly infusions. Such regimen tailoring trims overall drug volumes, exerting a pull on the organ transplant rejection medication market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: CNIs Dominate but mTOR Inhibitors Accelerate

CNIs accounted for 41.68% of 2025 revenue in the organ transplant rejection medication market, yet widespread generic availability slashed per-unit revenue. Meanwhile, mTOR inhibitors are forecast to rise at 3.98% annually as physicians pair sirolimus or everolimus with reduced-dose tacrolimus to mitigate nephrotoxicity. Triple-therapy protocols involving antiproliferatives such as mycophenolate still account for a notable share of market revenue, highlighting the entrenched nature of clinical practice. Co-stimulation blockade and IL-2 receptor antagonists together hold a modest share, largely driven by belatacept’s significant year-over-year gains.

By Transplant Type: Kidney Holds Nearly Half the Market

Kidney transplants accounted for 48.19% of 2025 revenue and are projected to grow at a 4.05% CAGR through 2031, outpacing the liver and heart segments. Medicare’s coverage extension and sizable living-donor programs in India reinforce this trajectory. Liver transplantation, roughly ntable share of the 2025 value, benefits from rising non-alcoholic steatohepatitis prevalence but faces marginally lower immunosuppression intensity. Heart and lung segments account for a combined modest share but command higher per-patient spending due to stringent rejection prophylaxis.

By maintaining volume leadership, kidney transplantation will keep the organ transplant rejection medication market anchored in regions where deceased-donor systems are robust or living-donor programs expand. Novel tolerance-induction regimens under study may eventually rebalance segment weightings past 2030.

By Molecule Type: Small-Molecule Dominance With Gradual Biologic Uptake

Small molecules commanded 65.29% of the 2025 organ transplant rejection medication market share, underpinned by oral tacrolimus, mycophenolate, and sirolimus regimens that cost USD 3,000–5,000 per patient each year and are forecast to grow at a 3.90% CAGR through 2031, keeping this segment the primary contributor to the organ transplant rejection medication market size. Widespread generic penetration for tacrolimus and for mycophenolate compressed average selling prices, but absolute prescription volumes rose as transplant activity expanded in China and India.

Biologics accounted for a significant share in 2025, constrained by infusion logistics, cold-chain requirements, and acquisition costs exceeding USD 15,000 per patient annually. Within this cohort, belatacept posted notable year-over-year sales growth in Q3 2025, while IVIG demand for AMR protocols is set to rise after CSL Behring’s USD 1.5 billion U.S. fractionation expansion that adds 4 million L of Privigen capacity by 2031

By Distribution Channel: Specialty Pharmacies Gain Momentum in High-Cost Biologics

Transplant centers and hospital pharmacies retained 53.98% of the 2025 organ transplant rejection medication market share, reflecting their gatekeeper role for induction agents such as rATG and basiliximab, as well as their control over inpatient IV formulations. However, maintenance prescriptions for organ transplant rejection medications are migrating to external networks as payers push for tighter utilization oversight.

Specialty pharmacies led by CVS Specialty, Accredo, and Walgreens Specialty are the fastest-growing channel, expected to expand at a 3.85% CAGR through 2031 as prior-authorization rules and therapeutic-drug-monitoring programs become prerequisites for coverage of belatacept, extended-release tacrolimus, and high-dose IVIG. Retail and online pharmacies, which handle a modest share of 2025 revenue mainly for low-cost generics, face shrinking margins because step-therapy protocols restrict 90-day fills and therapeutic substitution. The ongoing shift toward biologics will therefore continue to tilt dispensing volume toward specialty networks while transplant centers preserve their dominance in the acute-care setting.

Geography Analysis

North America held 43.19% of 2025 revenue, underpinned by Medicare’s policy change that permanently funds immunosuppressants for kidney recipients, a reform that slashed graft failure due to non-adherence by 15%. CVS Specialty, Accredo, and Walgreens Specialty manage the majority of high-cost biologic dispensing, linking reimbursement to monitoring adherence metrics. Specialty-pharmacy growth thus parallels biologic uptake, further entrenching payer oversight.

Europe contributed a significant share of global sales, leveraging coordinated procurement through Eurotransplant and Scandiatransplant. However, high generic penetration for tacrolimus and mycophenolate mofetil unit prices are below North American levels. EMA’s 2025 biosimilar guidance for monoclonal antibodies still excludes rATG, allowing incumbent brands to defend price points on induction agents.

Asia-Pacific is the fastest-growing geography, expanding at 3.91% annually through 2031. China conducted 22,814 kidney transplants in 2023, and India performs up to 20,000 each year, yet Japan’s low deceased-donor rate constrains its share of the market. Regulatory heterogeneity and aggressive local generic manufacturers temper per-patient revenue, but absolute volume gains will raise the baseline for the organ transplant rejection medication market across the region.

Competitive Landscape

Astellas, Novartis, and Bristol Myers Squibb defend branded niches such as extended-release tacrolimus and belatacept, but generics supplied by Sandoz, Viatris, Teva, Dr. Reddy’s, and others commanded the majority of tacrolimus and mycophenolate volumes. CSL Behring, Grifols, and Takeda retain oligopolistic control over IVIG thanks to complex plasma-fractionation requirements, illustrated by CSL’s USD 1.5 billion Illinois expansion.

Strategic moves reflect divergent priorities: Bristol Myers Squibb is building infusion-center alliances to accelerate Nulojix growth, while Astellas is reallocating capital toward oncology following a USD 1.7 billion collaboration with Vir Biotechnology in 2026. Emerging disruptors include MorphoSys-licensed felzartamab for AMR and Singulera Therapeutics’ autologous Treg platforms now in Phase 2. Regulatory events also shape competition; Accord Healthcare’s 2023 downgrade of tacrolimus to BX status hindered its U.S. uptake and temporarily bolstered pricing for other suppliers.

Organ Transplant Rejection Medication Industry Leaders

Astellas Pharma

Novartis AG

Bristol Myers Squibb

Sandoz

Viatris

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Eledon Pharmaceuticals reported that its anti-CD40L antibody has moved into Phase 3 testing, positioning the candidate as a potential substitute for tacrolimus that could lower the metabolic and cardiovascular side-effect burden now associated with long-term calcineurin-inhibitor use.

- June 2025: The U.S. FDA granted Orphan Drug Designation to riliprubart, a first-in-class monoclonal antibody directed at the C1s complement component, for treating antibody-mediated rejection after solid-organ transplantation.

Global Organ Transplant Rejection Medication Market Report Scope

As per the scope of the report, organ transplant rejection medications, broadly known as immunosuppressants, are vital drugs that prevent a recipient's immune system from attacking a transplanted organ as a "foreign" object. Because the immune system's natural role is to identify and destroy foreign invaders, such as bacteria and viruses, it must be carefully suppressed to allow the body to accept a new heart, liver, or kidney.

The organ transplant rejection medications market is segmented by drug class/mechanisms, transplant type, molecule type, distribution channel, and geography. Based on drug class/mechanisms, the market is segmented into Calcineurin inhibitors (tacrolimus, cyclosporine), Antiproliferatives (mycophenolate mofetil, mycophenolic acid, azathioprine), mTOR inhibitors (sirolimus, everolimus), Corticosteroids, Co-stimulation blockers / IL-2R antagonists (belatacept, basiliximab), Lymphocyte-depleting antibodies (rATG/ATG-F, alemtuzumab), IVIG/plasmapheresis adjuncts. By transplant type, the market is segmented into kidney, liver, heart, lung, pancreas, and hematopoietic stem cell (HSCT). Based on molecule type, the market is segmented into small molecules and biologics. By distribution channel, the market is segmented into transplant centers / hospital pharmacies, specialty pharmacies, and retail / online pharmacies.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Calcineurin inhibitors (tacrolimus, cyclosporine) |

| Antiproliferatives (mycophenolate mofetil, mycophenolic acid, azathioprine) |

| mTOR inhibitors (sirolimus, everolimus) |

| Corticosteroids |

| Co-stimulation blockers / IL-2R antagonists (belatacept, basiliximab) |

| Lymphocyte-depleting antibodies (rATG/ATG-F, alemtuzumab where used) |

| IVIG/plasmapheresis adjuncts |

| Kidney |

| Liver |

| Heart |

| Lung |

| Pancreas |

| Hematopoietic stem cell (HSCT) |

| Small molecules |

| Biologics |

| Transplant centers / hospital pharmacies |

| Specialty pharmacies |

| Retail / online pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class / Mechanism | Calcineurin inhibitors (tacrolimus, cyclosporine) | |

| Antiproliferatives (mycophenolate mofetil, mycophenolic acid, azathioprine) | ||

| mTOR inhibitors (sirolimus, everolimus) | ||

| Corticosteroids | ||

| Co-stimulation blockers / IL-2R antagonists (belatacept, basiliximab) | ||

| Lymphocyte-depleting antibodies (rATG/ATG-F, alemtuzumab where used) | ||

| IVIG/plasmapheresis adjuncts | ||

| By Transplant Type | Kidney | |

| Liver | ||

| Heart | ||

| Lung | ||

| Pancreas | ||

| Hematopoietic stem cell (HSCT) | ||

| By Molecule Type | Small molecules | |

| Biologics | ||

| By Distribution Channel | Transplant centers / hospital pharmacies | |

| Specialty pharmacies | ||

| Retail / online pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the organ transplant rejection medication market in 2031?

It is forecast to reach USD 6.8 billion by 2031, growing at a 3.69% CAGR from 2026.

Which drug class currently holds the largest share of revenue?

Calcineurin inhibitors, led by tacrolimus, commanded 41.68% of 2025 revenue.

Why is kidney transplantation the main growth driver?

Kidney procedures make up 48.19% of 2025 revenue and benefit from permanent Medicare coverage and high living-donor activity in Asia-Pacific.

How are specialty pharmacies influencing therapy access?

CVS Specialty, Accredo, and Walgreens Specialty manage most high-cost biologic dispensing, enforcing prior authorization and adherence monitoring to contain costs.

Page last updated on: