Organ Transplant Immunosuppressant Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

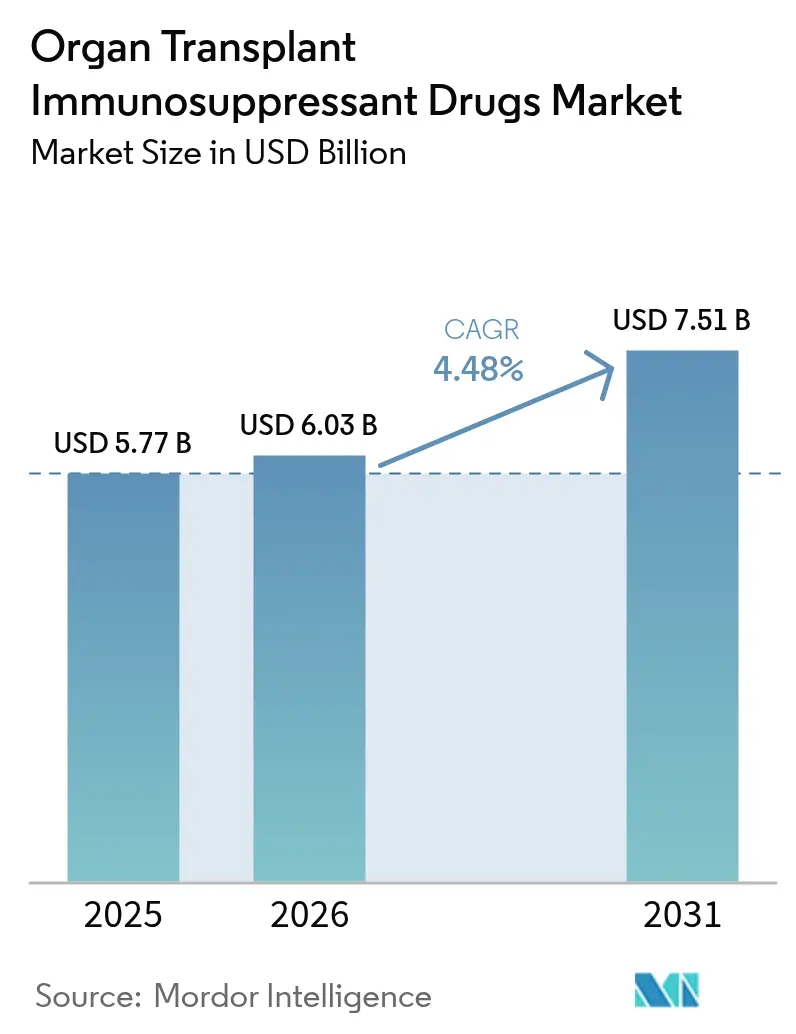

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 7.51 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

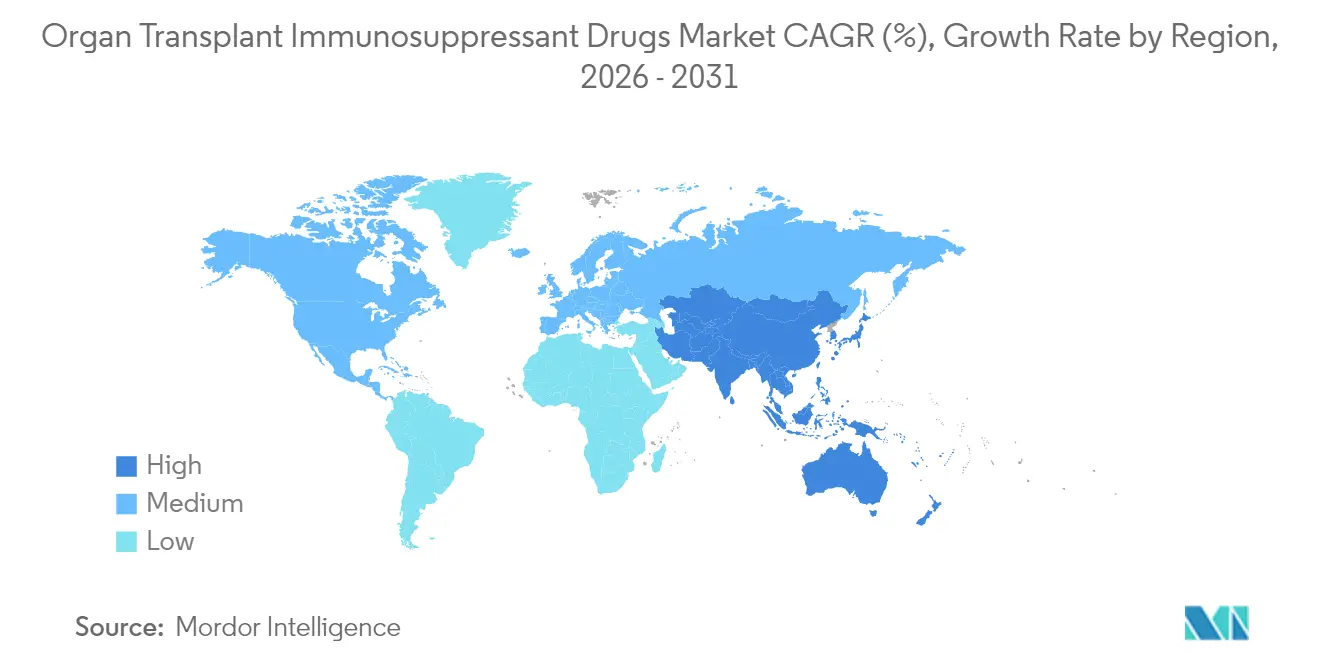

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

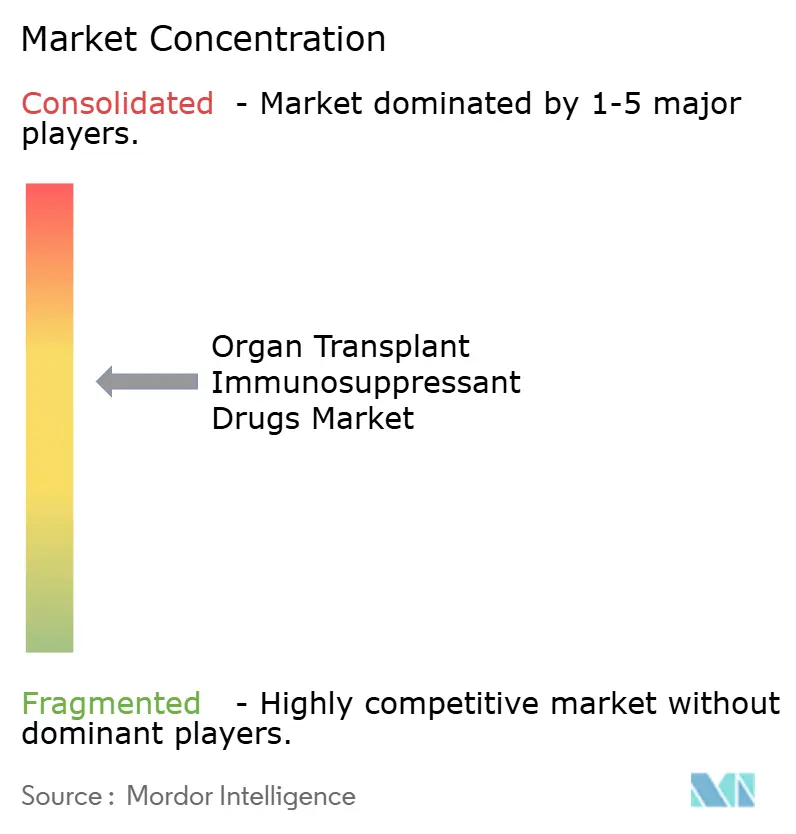

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organ Transplant Immunosuppressant Drugs Market Analysis by Mordor Intelligence

Organ transplant immunosuppressant drugs market size in 2026 is estimated at USD 6.03 billion, growing from 2025 value of USD 5.77 billion with 2031 projections showing USD 7.51 billion, growing at 4.48% CAGR over 2026-2031. Steady transplant volumes, record organ‐donation milestones, and continual protocol upgrades underpin expansion. Accelerated approvals of cost-saving generics broaden patient access, while nephron-sparing regimens and ex vivo perfusion technologies sharpen clinical outcomes. Digital dispensing channels, precision diagnostics, and AI-guided dosing further reinforce demand despite intensifying cost pressures and donor shortages. North America retains volume leadership, but Asia-Pacific’s rapid program build-outs are redefining geographic dynamics, lifting the organ transplant immunosuppressant drugs market toward sustained mid-single-digit growth through the decade.

Key Report Takeaways

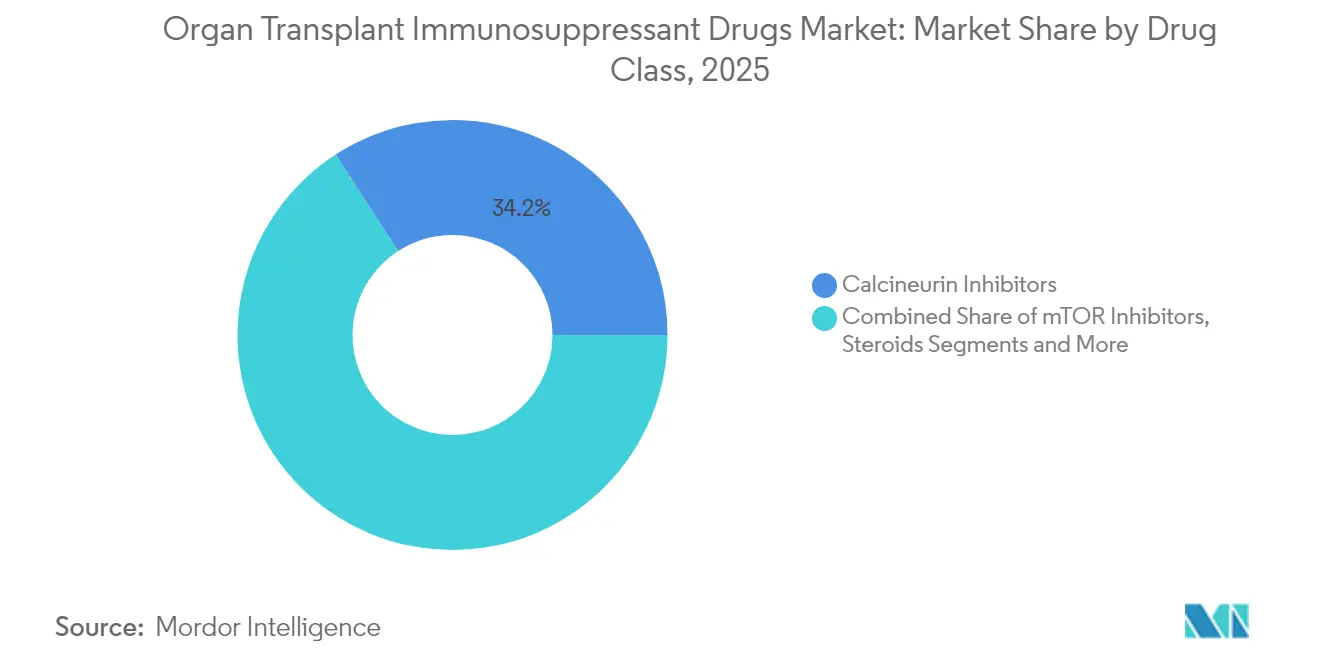

- By drug class, calcineurin inhibitors led with 34.15% of the organ transplant immunosuppressant drugs market share in 2025; mTOR inhibitors are projected to post the fastest 9.72% CAGR to 2031.

- By transplant type, kidney procedures accounted for 61.05% of the organ transplant immunosuppressant drugs market size in 2025, while lung transplants are set to expand at a 9.68% CAGR.

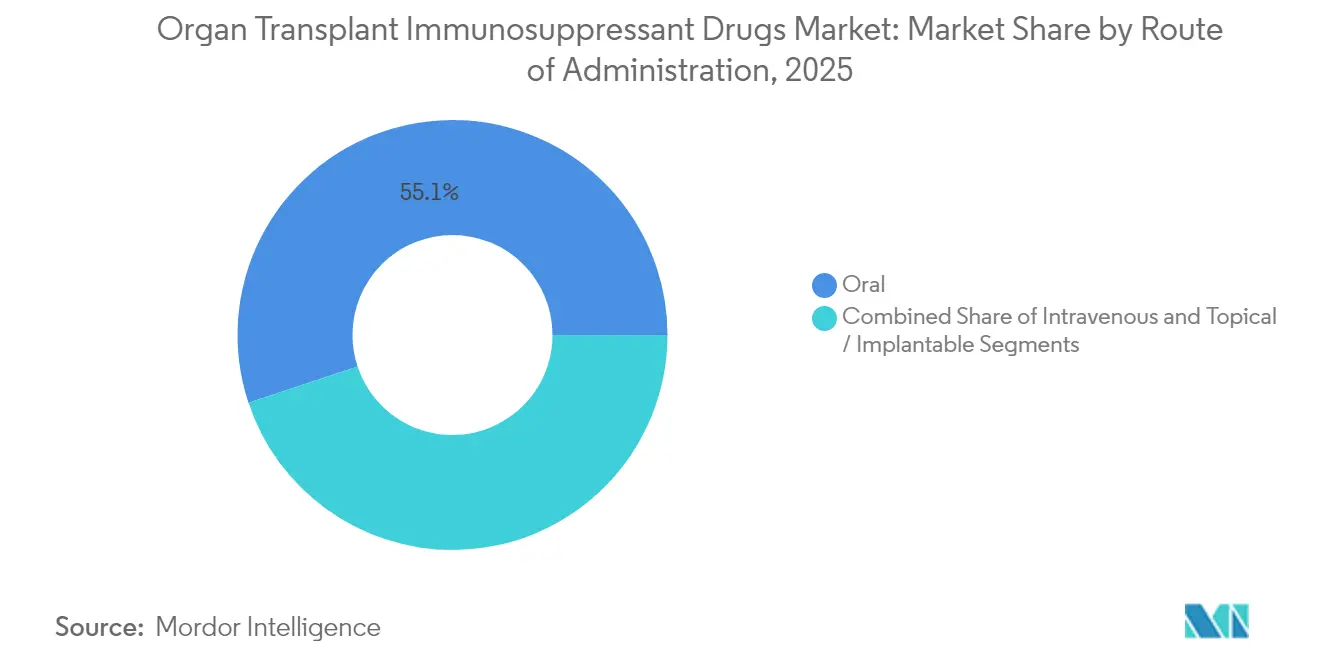

- By route of administration, oral formulations commanded 55.10% revenue share of the organ transplant immunosuppressant drugs market in 2025; intravenous delivery is growing at 9.05% CAGR.

- By distribution channel, hospital pharmacies held 59.55% share of the organ transplant immunosuppressant drugs market size in 2025; online pharmacies are forecast to grow at 9.77% CAGR.

- By geography, North America captured 42.30% of the organ transplant immunosuppressant drugs market share in 2025, while Asia-Pacific is advancing at a 8.84% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organ Transplant Immunosuppressant Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing organ-failure burden boosts transplants | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid approvals of generic tacrolimus & MMF | +0.8% | Global, led by North America & Europe | Short term (≤ 2 years) |

| Improved HLA-typing & transplant diagnostics | +0.6% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Adoption of organ ex-vivo perfusion systems | +0.4% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Implantable local-delivery systems cut toxicity | +0.3% | North America & Europe, research-driven markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Organ-Failure Burden Boosts Transplants

Escalating incidences of end-stage kidney, liver, heart, and lung diseases fuel surgery volumes and, by extension, immunosuppressant uptake. More than 37 million Americans live with chronic kidney disease, while COVID-19 exacerbated liver morbidity. Aging demographics deepen the candidate pool and require more intensive regimens because older patients possess diminished immune resilience. Early diagnostics flag organ failure sooner and feed transplant pipelines once deemed unreachable. Artificial-intelligence matching systems now predict compatibility with 98% accuracy, lowering rejection events and optimizing dosing protocols, thereby creating reinforcing demand cycles.

Rapid Approvals of Generic Tacrolimus & MMF

Uptake of multiple tacrolimus and mycophenolate mofetil generics slashes regimen costs, allowing funding bodies to treat more recipients within fixed budgets. Medicare Part D outlays for key drugs fell 48-67% after successive generic launches, and ready-to-use oral suspensions widened pediatric access. Nonetheless, the FDA’s recent BX rating on an Accord tacrolimus lot highlights vigilance over bioequivalence. Price relief is especially pivotal in emerging economies, where drug expenditure remains the primary bottleneck to post-surgery adherence[1]U.S. Food and Drug Administration, “Tacrolimus Capsules Manufactured by Accord Healthcare Inc.,” pshp.org.

Improved HLA-Typing & Transplant Diagnostics

Next-generation sequencing delivers high-resolution HLA data, uncovering minor compatibility nuances untraceable by serology. Virtual cross-match systems shrink cold-ischemia time, while molecular algorithms such as PIRCHE-II quantify eplet mismatches and estimate rejection risk. Non-HLA antibody screening, now routine at major centers, pinpoints novel rejection pathways, guiding clinicians toward individualized, often lower-toxicity regimens. This precision lessens graft loss risk and sustains long-term demand for maintenance drugs.

Adoption of Organ Ex-Vivo Perfusion Systems

Normothermic perfusion reconditions marginal organs, broadening supply. Ontario’s program raised lung transplant volumes and shortened waitlists; similar liver defatting trials are in progress. Better organ quality curbs ischemia-reperfusion injury, moderating induction-dose spikes and enabling smoother maintenance phases that still rely on steady immunosuppression. Hospitals in North America and Europe now budget perfusion platforms as standard capital expenditure, and Asia-Pacific centers are beginning deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High lifetime cost of multi-drug regimens | -1.1% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Chronic donor-organ shortage | -0.9% | Global, acute in developing regions | Long term (≥ 4 years) |

| Shift to CNI-sparing protocols lowers volumes | -0.7% | North America & Europe, research-driven adoption | Medium term (2-4 years) |

| Emerging xenotransplantation could disrupt demand | -0.5% | North America initially, global expansion potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Lifetime Cost of Multi-Drug Regimens

Annual therapy expenses exceeding USD 30,000 per U.S. liver recipient strain payers and patients alike. Medicare coverage lapses three years post-surgery, leaving 32% of middle-aged recipients without adequate drug insurance. Complication-driven hospitalizations further inflate health-system costs, prompting calls to extend public reimbursement, which economic models show would yield both savings and quality-of-life gains. In low- and middle-income countries, out-of-pocket exposure often forces dose skimping, undermining outcomes and constraining organ transplant immunosuppressant drugs market expansion.

Chronic Donor-Organ Shortage

Despite innovation, donor supply lags need: 103,000 U.S. patients await organs, and roughly 6,000 die annually on lists. India’s donation rate remains below 1 PMP, and ethnic minorities worldwide face lengthier waits. Scarcity caps transplant counts, placing a structural ceiling over the organ transplant immunosuppressant drugs market even as diagnostics and drugs progress. Expanded-criteria donor programs and perfusion tech help, but demographic and cultural hurdles persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: mTOR Inhibitors Gain Momentum Over Calcineurin Standards

Calcineurin inhibitors retained 34.15% revenue in 2025, anchoring the organ transplant immunosuppressant drugs market. Proven agents such as tacrolimus remain first-line for most graft types. Yet mTOR inhibitors are on a 9.72% CAGR trajectory due to nephron-sparing and cardiometabolic benefits. Early conversion to everolimus within 12 months post-liver transplant improved renal function in 55% of patients. Rapamycin-based quadruple therapy delivered 20-year graft survival of 20.9%, eclipsing tacrolimus benchmarks. Co-stimulation blockers like belatacept and antiproliferatives such as mycophenolic acids round out therapeutic backbones, while antibody induction remains situational for high-risk recipients.

Novel delivery systems catalyze growth. Self-assembled rapamycin nanoparticles sustain plasma concentrations with lower systemic toxicity, and pegylated CD28-targeting fragments (VEL-101) progress through Phase 2. As generic penetration rises and patents sunset, price competition will intensify, but innovation in targeted or localized formulations should offset margin pressures, reinforcing the organ transplant immunosuppressant drugs market’s mid-term growth outlook.

By Transplant Type: Lung Procedures Accelerate on Perfusion Breakthroughs

Kidney grafts continued to dominate 61.05% of the organ transplant immunosuppressant drugs market size in 2025, supported by mature protocols and high disease prevalence. Lung transplants, however, register the briskest 9.68% CAGR. Normothermic ex vivo perfusion elevates marginal lungs to transplantable status, eliminating primary graft dysfunction in donation-after-circulatory-death cohorts. Heart graft programs leverage veno-arterial ECMO back-up during acute dysfunction, boosting one-year survival. Liver and pancreas volumes expand steadily but face competition from evolving non-surgical disease-management options. Stem-cell transplants and vascularized composite allografts adopt tailored immunomodulation, indicating future niche demand pockets within the broader organ transplant immunosuppressant drugs market.

Growth in lung and emerging composite procedures will keep overall therapy volumes rising despite xenotransplantation experiments, whose success could either dampen maintenance-drug need or create new induction niches if human graft limitations persist.

By Route of Administration: Intravenous Precision Upshifts but Oral Regimens Stay Core

Oral dosage forms accounted for 55.10% of 2025 revenue, underpinning routine outpatient maintenance. Intravenous options are advancing at 9.05% CAGR as transplant centers embrace precision infusion during early post-op windows and rejection episodes. The organ transplant immunosuppressant drugs market share of IV agents is therefore widening, though patient-friendly oral suspensions like FDA-cleared Myhibbin ensure oral delivery remains the cornerstone.

Longer term, implantable disks providing 100-day tacrolimus release and biodegradable hydrogels for localized therapy promise to redefine adherence and safety. Nanoparticle and macrophage-membrane technologies further illustrate the delivery-innovation pipeline poised to reshape pharmacokinetics while sustaining market value.

By Distribution Channel: Digital Dispensing Scales While Hospital Pharmacies Retain Control

Hospital pharmacies controlled 59.55% of worldwide sales in 2025, reflecting the complexity of post-surgical medication titration. Online channels, however, are expanding at 9.77% CAGR, catalyzed by pandemic-era telehealth normalization and growing patient comfort with remote refills. Retail pharmacies retain relevance for stable recipients, yet specialized digital portals offering integrated adherence support and direct-from-manufacturer models stand to capture incremental share of the organ transplant immunosuppressant drugs market.

Telemedicine has cut medication-error rates among kidney recipients and lifted follow-up compliance. AI-driven portals that link dosing data with wearable biometrics represent the next wave of service differentiation, likely accelerating the online channel’s penetration without dislodging hospital dispensaries for induction therapies.

Geography Analysis

North America commanded 42.30% of 2025 sales on the back of 46,000 transplants and comprehensive payer coverage. The United States posts high tacrolimus utilization despite rising generic substitution, and Canada’s early adoption of machine perfusion further amps volumes. Europe maintains balanced growth, though reimbursement reforms and cross-border harmonization debates shape access in smaller member states.

Asia-Pacific is the fastest-growing contributor at 8.84% CAGR. China’s state-sponsored transplant network, India’s 13,426 kidney operations in 2023, and Japan’s approval of LIVTENCITY for post-transplant CMV all illustrate momentum. Improvements in regulatory clarity, donor-registry digitization, and insurance expansion underline a structural shift that will raise the region’s share of the organ transplant immunosuppressant drugs market through 2031.

South America and the Middle East & Africa remain nascent yet strategic. Brazil’s established liver and kidney centers anchor South American progress, while Saudi Arabia and South Africa spearhead regional adoption of perfusion systems. Limited donor pools and funding constraints temper uptake, but targeted public–private partnerships could unlock incremental opportunity for the organ transplant immunosuppressant drugs market in the later forecast window.

Competitive Landscape

The organ transplant immunosuppressant drugs market displays moderate concentration. Tacrolimus, cyclosporine, mycophenolate, sirolimus, and everolimus franchises are held by a handful of global majors leveraging extensive patent estates, regulatory expertise, and manufacturing economies. Lifecycle extensions pivot on once-daily or extended-release dosing and fixed-ratio combinations. Defensive strategies include authorized generics and selective price cuts to blunt third-party entrants.

Patent cliffs, however, drive rising generic penetration—tacrolimus generics climbed from 15.2% to 22.7% in Bavaria within one year—tightening incumbent margins. Innovator pipelines retaliate with targeted biologics such as CD28 antagonists (VEL-101) and CD38 antibodies (felzartamab), plus local-delivery implants that could reset differentiation. Acquisitions—Biogen’s 2024 purchase of Human Immunology Biosciences—and co-development alliances typify the race to broaden mechanistic diversity and sustain revenue.

Regulators remain influential arbiters. FDA decisions on bioequivalence ratings, pediatric exclusivity, and patent-term restoration alter go-to-market timelines. Post-marketing commitments, especially pharmacoepidemiological safety studies, weigh heavily on resource planning. Meanwhile, xenotransplantation trials, should they mature, could redefine competitive stakes by reducing maintenance-dose requirements or redirecting R&D toward acute immunomodulation.

Organ Transplant Immunosuppressant Drugs Industry Leaders

Astellas Pharma, Inc

Bristol-Myers Squibb Company

Novartis AG

F. Hoffmann-La Roche Ltd

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Biogen launched the Phase 3 TRANSCEND trial of felzartamab in late antibody-mediated kidney rejection, enrolling 120 patients.

- April 2025: Kyoto University reported positive mid-term data from the first allogeneic iPS cell-derived dopaminergic progenitor transplant using tacrolimus immunosuppression.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global organ transplant immunosuppressant drugs market as all branded and generic systemic agents, including calcineurin inhibitors, mTOR inhibitors, antiproliferatives, corticosteroids, costimulation blockers, and antibody-based therapies, prescribed to prevent or treat rejection after solid-organ or hematopoietic stem-cell transplantation.

Scope Exclusions: supportive biologics for graft-versus-host disease, cell or gene tolerance protocols, and surgical devices are excluded.

Segmentation Overview

- By Drug Class

- Calcineurin Inhibitors

- Antiproliferative Agents (IMPDH inhibitors)

- mTOR Inhibitors

- Steroids

- Co-stimulation Blockers (Belatacept)

- Polyclonal/Monoclonal Antibodies

- Other Classes

- By Transplant Type

- Kidney

- Liver

- Heart

- Lung

- Pancreas

- Bone-Marrow / HSCT

- Other Types

- By Route of Administration

- Oral

- Intravenous

- Topical / Implantable

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts held multiple interviews with transplant surgeons, hospital pharmacists, payers, and patient advocates across North America, Europe, and Asia. These conversations validated regimen switches toward CNI-sparing protocols, expected generic erosion rates, and reimbursement ceilings, while short surveys of post-transplant patients highlighted adherence and dose-adjustment realities.

Desk Research

We first consolidated transplant counts from sources such as the Global Observatory on Donation and Transplantation, United Network for Organ Sharing, Eurotransplant, and China's COTRS; these procedure volumes anchor demand by organ type. Our team then mined regulatory approval databases, hospital procurement dashboards, and company 10-Ks for price curves, label changes, and revenue splits, while peer-reviewed journals clarified evolving maintenance regimens.

Mordor analysts complemented these inputs with customs shipment records, Volza import data, Dow Jones Factiva articles, and Questel patent alerts to gauge pipeline depth and generic activity. This list is illustrative, not exhaustive; additional public and subscription data sets informed finer validations.

Market-Sizing & Forecasting

We start with a top-down reconstruction. Yearly transplant counts are multiplied by protocol-specific maintenance-day volumes and weighted average selling prices, generating preliminary demand. We then use sampled hospital purchase audits and manufacturer revenue disclosures as bottom-up checks that fine-tune totals. Key model variables, including graft survival curves, generic penetration trajectories, organ-availability growth, and uptake of once-daily formulations, feed a multivariate regression that projects demand through 2030. Data gaps are bridged by prorating thin country series against regional procedure ratios before final benchmarking.

Data Validation & Update Cycle

Our outputs undergo variance screening against historical CAGR bands and price-volume elasticity norms, followed by multi-level analyst review. Reports refresh annually, with interim updates whenever major drug launches, policy shifts, or currency swings materially alter baselines.

Why Our Organ Transplant Immunosuppressant Drugs Baseline Commands Confidence

Published estimates diverge because firms select different drug baskets, transplant settings, and currency deflators. By anchoring figures to verified procedure counts and audited purchase prices, Mordor Intelligence offers a dependable reference point.

Key gap drivers we observe include some publishers omitting antibody induction doses, others assuming flat generic pricing, and several relying on partial country coverage without mid-year currency re-expression.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.77 B (2025) | Mordor Intelligence | - |

| USD 5.51 B (2024) | Global Consultancy A | Excludes antibody drugs; relies on list prices |

| USD 5.60 B (2024) | Industry Journal B | No route-specific volume splits; limited geography |

| USD 5.55 B (2024) | Healthcare Think-Tank C | Uses claims data from five nations only |

The comparison shows that, by combining broad geographic coverage with transparent variable tracking, we provide a balanced, traceable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the organ transplant immunosuppressant drugs market?

The market stands at USD 6.03 billion in 2026 and is projected to reach USD 7.51 billion by 2031, reflecting a 4.48% CAGR.

Which drug class is growing fastest?

MTOR inhibitors exhibit the highest growth, advancing at a 9.72% CAGR due to renal-preserving and cardio-protective profiles.

Why is Asia-Pacific considered the most dynamic region?

Expanding transplant programs in China, India, and Japan, along with supportive regulatory reforms, are driving a 8.84% CAGR, outpacing all other regions.

How are generics influencing market economics?

Successive approvals of tacrolimus and mycophenolate generics have sliced Medicare drug spending by as much as 67%, widening patient access while intensifying price competition.

Could xenotransplantation shrink immunosuppressant demand?

Early pig-kidney trials are promising but remain experimental; any long-term impact on maintenance-drug volumes will depend on durable clinical success and regulatory endorsement.

Page last updated on: