Global Cardiac Arrest Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

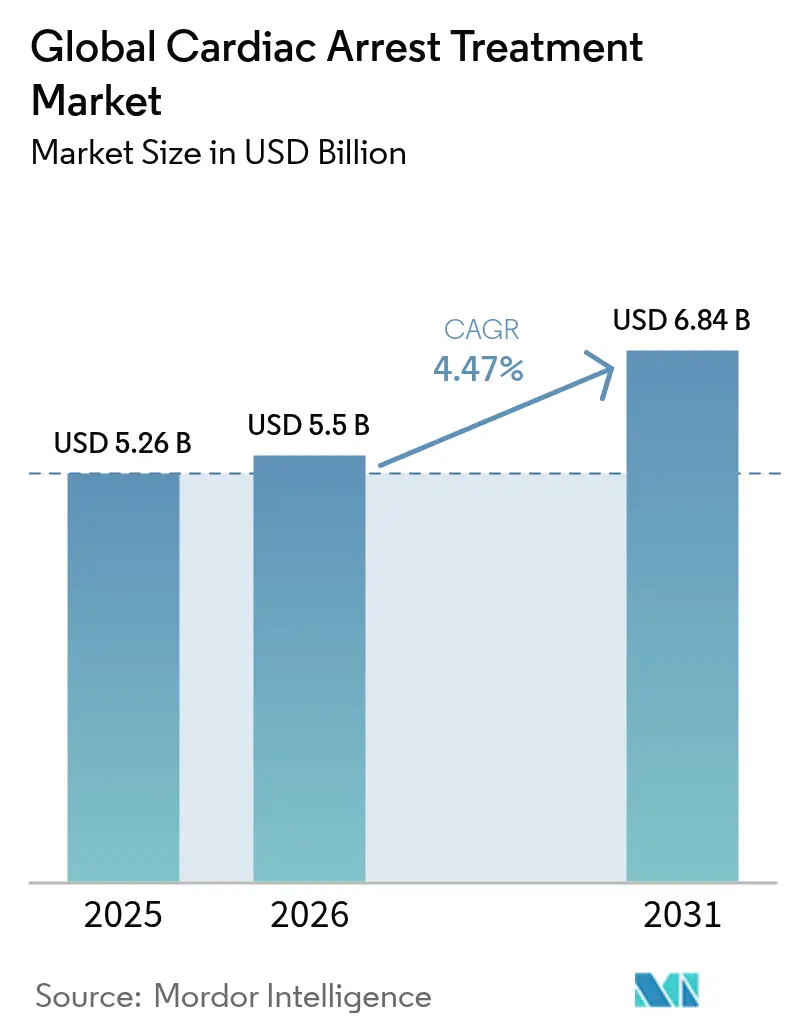

| Market Size (2026) | USD 5.5 Billion |

| Market Size (2031) | USD 6.84 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

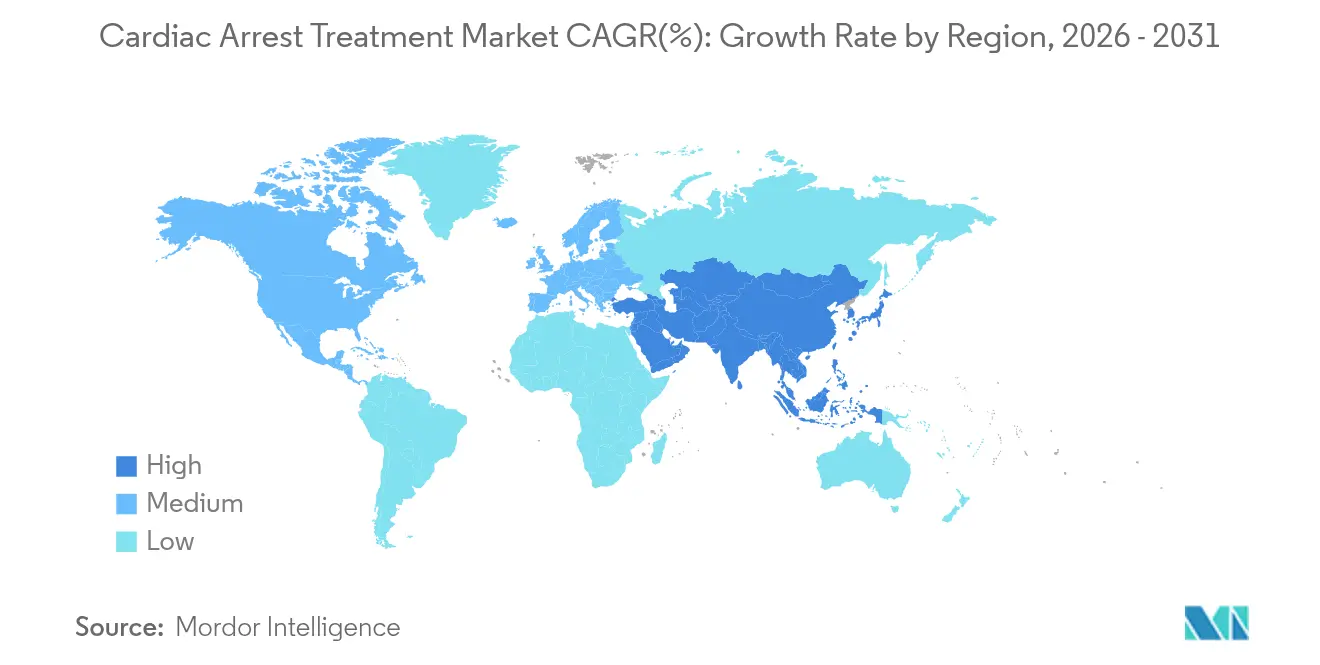

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

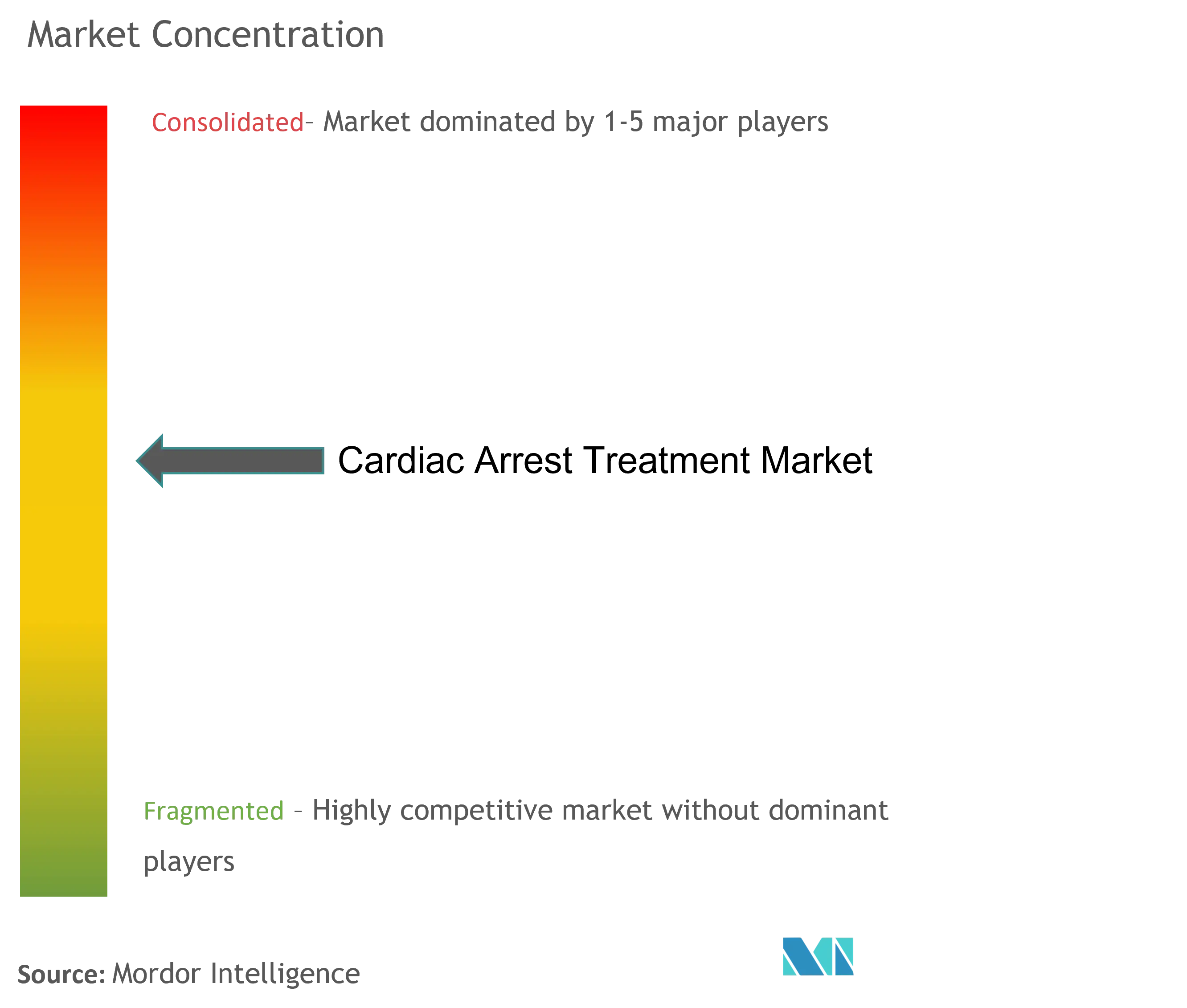

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Cardiac Arrest Treatment Market Analysis by Mordor Intelligence

The global cardiac arrest treatment market size in 2026 is estimated at USD 5.5 billion, growing from 2025 value of USD 5.26 billion with 2031 projections showing USD 6.84 billion, growing at 4.47% CAGR over 2026-2031. Consistent demand from ageing populations, wider public-access defibrillator programs, and rapid advances in miniaturised extracorporeal systems support this upward trajectory. Vendors also benefit from AI-enabled rhythm-prediction tools that integrate into emergency medical service (EMS) dispatch software, allowing faster, data-driven triage. Parallel innovations—such as drone-delivered automated external defibrillators (AEDs), mRNA-based anti-arrhythmic pipelines, and field-deployable therapeutic hypothermia packs—signal a clear shift from reactive to predictive care models. At the same time, heightened post-recall vigilance by regulators and continued supply-chain diversification strategies increase compliance costs but help restore clinician confidence. Overall, competitive pressure ropes leading firms into continuous R&D cycles that keep the cardiac arrest treatment market responsive to evolving clinical guidelines and public-health mandates.

Key Report Takeaways

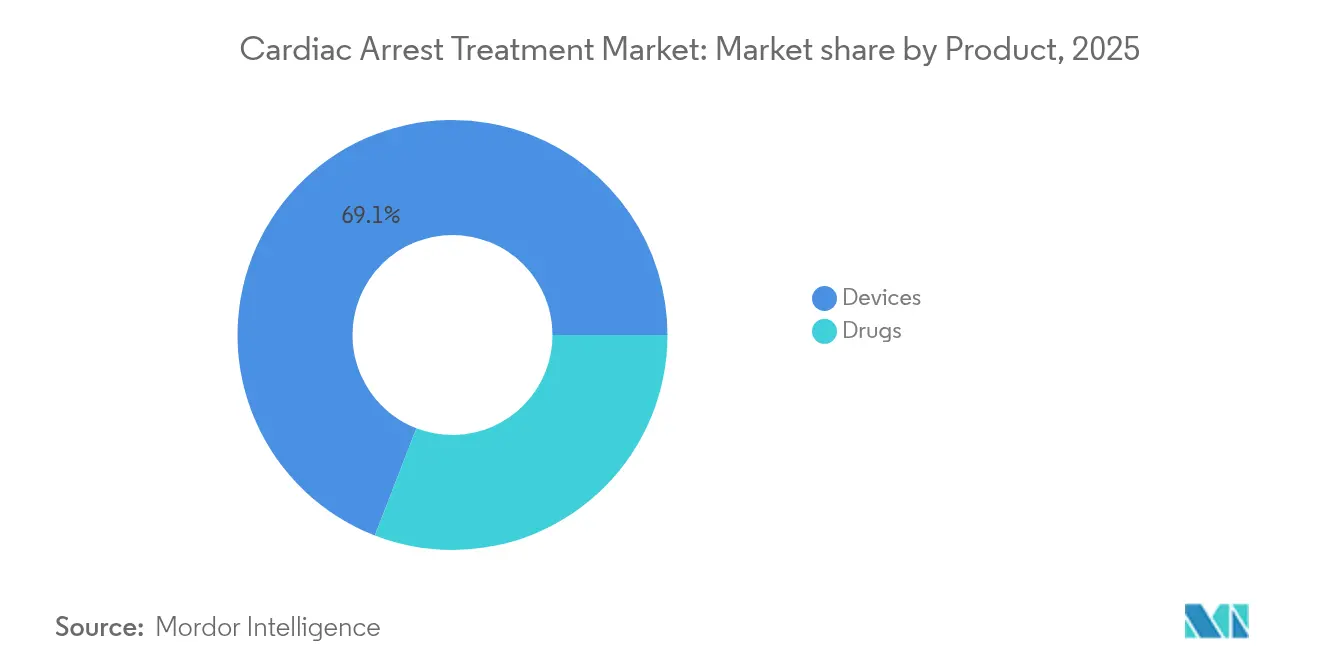

- By product category, devices led with 69.12% revenue share in 2025, while the same segment is forecast to grow at a 6.33% CAGR through 2031.

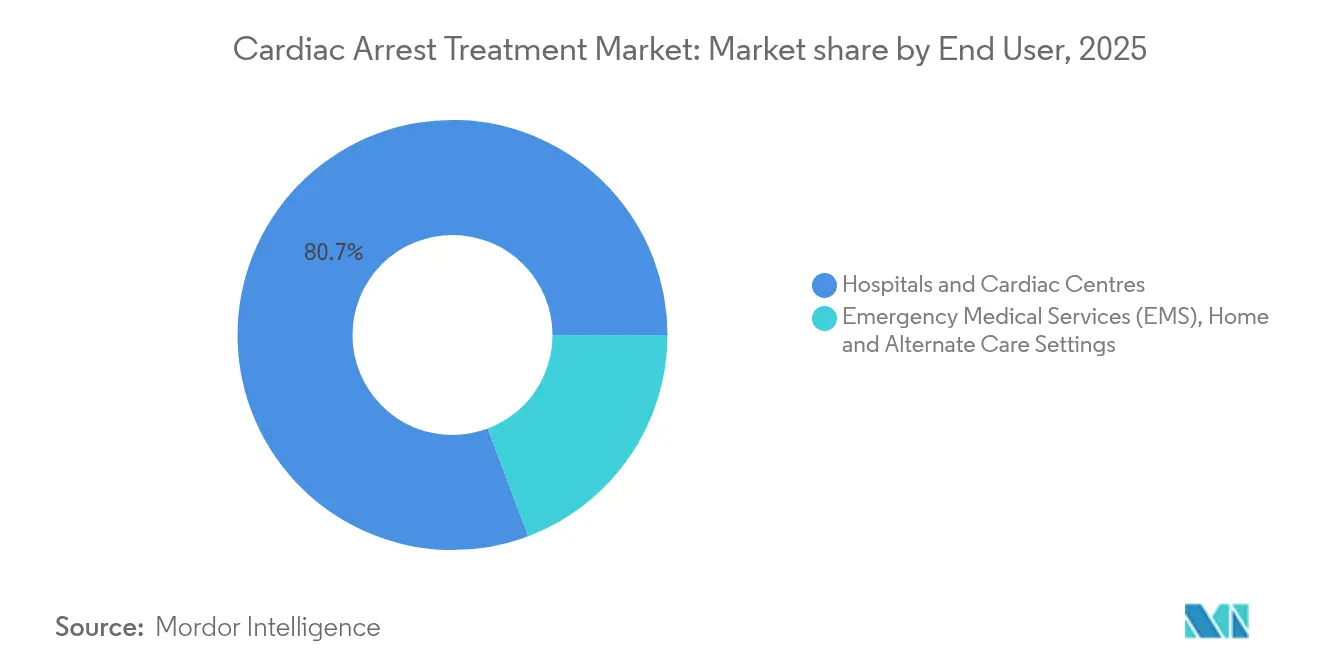

- By end user, hospitals and cardiac centres held 80.73% of the cardiac arrest treatment market share in 2025, whereas home and alternate care settings record the highest projected CAGR at 5.72% through 2031.

- By region, North America accounted for 41.83% of 2025 revenue, while Asia-Pacific is advancing at a 7.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Arrest Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of Sudden Cardiac Arrest & ageing Populations | +1.20% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Public-access defibrillator programmes and Legislation | +0.80% | North America & EU leading, APAC emerging | Medium term (2-4 years) |

| Advances in implantable & wearable Defibrillator Technology | +1.10% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Miniaturised ECMO for refractory cardiac arrest | +0.60% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| AI-powered rhythm-prediction integrated into EMS workflows | +0.50% | North America leading, EU following | Short term (≤ 2 years) |

| mRNA-based anti-arrhythmic therapeutics in pipeline | +0.30% | Global, pending regulatory approvals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Sudden Cardiac Arrest & Ageing Populations

Population ageing increases sudden cardiac death incidence, especially among adults over 65. The American Heart Association notes that 356,000 Americans experience out-of-hospital cardiac arrest each year, with survival remaining at 8-10%. Its 2030 Impact Goals target more than 50% bystander CPR and 20% AED use before EMS arrival to offset the 10% survival decline that occurs for every untreated minute. These goals push health systems to procure integrated device ecosystems rather than one-off equipment. Growing recognition of COVID-19-related myocardial micro-scarring in younger age groups further broadens the addressable patient pool. Consequently, the cardiac arrest treatment market continues to prioritize scalable platforms that combine monitoring, predictive software, and therapy delivery in a single continuum of care.

Public-Access Defibrillator Programmes and Legislation

State-mandated AED deployment in schools, sports arenas, and transit hubs expands device density and improves lay-rescuer readiness. South Carolina’s Smart Heart Act and Ohio’s House Bill 47 require both AED placement and cardiac emergency response plans, lowering legal barriers that once deterred facility managers. The Centers for Disease Control and Prevention offers a 13-point implementation toolkit that standardises procurement and maintenance, while federal proposals to reauthorise the Cardiac Arrest Survival Act strengthen liability protections. Connected AED platforms that feed status data into 911 dispatch networks therefore enjoy higher adoption, especially when bundled with subscription-based training modules.

Advances in Implantable & Wearable Defibrillator Technology

Device miniaturisation reduces implant risk and opens therapy to moderately at-risk cohorts. Medtronic’s 4.7 French OmniaSecure lead achieved a 97.5% defibrillation success rate during pivotal trials[1]Source: Medtronic plc, “OmniaSecure Clinical Trial Results,” medtronic.com . Boston Scientific’s modular mCRM system links a subcutaneous ICD with a leadless pacemaker, posting a 98.8% inter-device communication success metric. Meanwhile, AI-enabled wearable defibrillators such as Element Science’s Jewel Patch extend protection past hospital discharge, bolstering the cardiac arrest treatment market by lowering rehospitalisation costs. Predictive algorithms embedded in cloud dashboards also alert clinicians before malignant arrhythmias manifest, shifting resource allocation from crisis response to prevention.

Miniaturised ECMO for Refractory Cardiac Arrest

Extracorporeal cardiopulmonary resuscitation (ECPR) yields 29.4% survival for refractory cases versus 2.4% with conventional CPR, per a multicentre propensity study. Medtronic’s portable VitalFlow ECMO system brings circuit priming and monitoring to the ambulance bay, letting teams initiate support within minutes of collapse. Registry data from the Extracorporeal Life Support Organization now list more than 100,000 survivors, validating field use when paired with rigorous training. Advances in biocompatible coatings and heparin-sparing circuits further counter previous bleeding risks, encouraging policy makers to reimburse ECPR in specialised EMS units.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product recalls & device-related adverse events | -0.90% | Global, with concentrated impact in regulated markets | Short term (≤ 2 years) |

| High capital cost & reimbursement gaps in emerging markets | -1.10% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| API shortages for key vasopressors | -0.30% | Global, with supply chain concentration in Asia | Short term (≤ 2 years) |

| Ethical & regulatory hurdles for field-deployed hypothermia drones | -0.20% | North America & EU leading regulatory frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Recalls & Device-Related Adverse Events

Quality lapses remain a central concern. Boston Scientific issued a Class I recall for certain Accolade pacemakers after 832 injuries and 2 deaths were linked to devices entering Safety Mode[2]Source: U.S. Food and Drug Administration, “Accolade Pacemaker Recall Notice,” fda.gov . Abbott simultaneously recalled HeartMate pump accessories due to power unit failures, triggering the FDA’s pilot programme that accelerates public safety alerts for cardiovascular implants. These incidents reduce clinician confidence, delay new-product clearances, and push companies to allocate larger budgets to post-market surveillance, thereby slowing the overall cardiac arrest treatment market.

High Capital Cost & Reimbursement Gaps in Emerging Markets

Advanced defibrillators and ECMO circuits command premium price tags, yet reimbursement pathways in many emerging economies cover only basic resuscitation supplies. India’s device market still depends on 70% imports, creating affordability barriers for public hospitals. Variable evidence requirements across regulators also lengthen approval timelines, adding financing pressure on smaller exporters. Although private insurers in urban centres partly offset these gaps, rural populations often rely on out-of-pocket spending, limiting broader penetration of next-generation therapies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Devices Drive Innovation While Drugs Face Pipeline Constraints

Devices contributed USD 3.64 billion in 2025, equal to 69.12% of total revenue. Technological leaps like AI-driven arrhythmia prediction and miniaturised ECMO propel this category toward a 6.33% CAGR, keeping the cardiac arrest treatment market size for devices ahead of pharmacologic alternatives. Defibrillators dominate hospital code carts, while drone-mounted AEDs extend reach to remote communities. Portable ECMO platforms win guideline endorsements for refractory cases, and mechanical circulatory support systems such as Impella add incremental hemodynamic stability. FDA approval of the VARIPULSE pulsed-field ablation system confirms regulators’ willingness to fast-track high-impact devices, reinforcing vendor confidence in sustained R&D.

The drug segment accounts for the remaining revenue and grows at a slower pace as formulary constraints and generic competition bite. Class III agents like amiodarone remain standard for ventricular arrhythmias, yet shortages of vasopressors such as epinephrine sporadically disrupt critical-care supply chains nih.gov. Investigational mRNA therapies, including AZD8601, mark the first significant mechanistic shift since dronedarone’s 2009 launch, but large-scale efficacy data are pending. RNAi approaches that silence arrhythmogenic pathways show promise in preclinical settings, although commercial timelines extend beyond the current forecast window.

By End User: Hospital Dominance Challenged by Home Care Emergence

Hospitals and specialist cardiac centres captured 80.73% of 2025 revenue, underpinned by 24/7 catheterisation labs, ECMO suites, and intensive telemetry. Adoption of extracorporeal CPR protocols further solidifies this lead, with survival rates for in-centre ECPR reaching 29.4% compared with 2.4% for conventional approaches. Consolidation among health-system networks streamlines bulk purchases of connected defibrillators, elevating enterprise-wide uptime and maintenance compliance across multiple campuses.

The home and alternate care segment records a 5.72% CAGR and is forecast to gain incremental cardiac arrest treatment market size through 2031, driven by AI-enabled wearables that safeguard high-risk patients during the vulnerable post-discharge period. ZOLL Medical’s ResQCPR system reports a 49% one-year survival improvement when used with impedance threshold devices, encouraging payers to reimburse home-based solutions. Telemedicine legislation passed during the pandemic now supports remote programming of implantable devices, enlarging the data pipeline that clinicians use to anticipate deterioration. This decentralised model lowers rehospitalisation costs and aligns with value-based-care incentives, thereby accelerating adoption in both mature and emerging healthcare systems.

Geography Analysis

North America holds 41.83% of 2025 revenue, benefiting from established EMS protocols, widespread AED saturation, and an FDA ecosystem that offers breakthrough device designations for life-saving tools. Federal liability shields under the Cardiac Arrest Survival Act nurture community responders, and the American Heart Association’s targets push states to intensify public-access programmes. Integrated delivery networks negotiate fleet-wide service contracts for defibrillators and monitoring platforms, which sustains predictable replacement cycles. In parallel, large-scale field trials of drone-delivered AEDs in rural regions demonstrate response-time cuts of 4-6 minutes, materially improving neurological outcomes nih.gov.

Asia-Pacific is the fastest-growing territory at 7.55% CAGR, chiefly due to rising cardiovascular mortality and expanded emergency-care funding in urban provinces. Domestic manufacturers from China and Japan increase exports of cost-effective AEDs, challenging Western incumbents on price while meeting International Electrotechnical Commission (IEC) standards. Nevertheless, fragmented reimbursement landscapes still slow uptake of high-ticket ECMO and conduction-system pacing devices, keeping the cardiac arrest treatment market share for expensive capital equipment modest. Multilateral regulatory harmonisation projects, including the Asian Harmonisation Working Party, aim to trim approval times by synchronising dossier requirements—a factor that gradually reduces entry hurdles for global brands.

Europe delivers steady but cautious growth under unified medical-device regulations that emphasise clinical-evidence depth. The region champions clinical quality registries that feed outcome data into guideline updates, guiding hospitals toward evidence-backed purchases. Pilot drone networks in the Netherlands achieved sub-5-minute AED delivery to cardiac arrest scenes, prompting the European Union to fund cross-border replication studies nhs.uk. Budget pressures keep purchasing decisions under health-technology assessment review, yet outcome-based procurement models reward platforms that present clear reductions in out-of-hospital mortality. EU MDR transition costs remain a factor, but established suppliers with robust post-market surveillance capabilities maintain favourable status on tender lists

Competitive Landscape

The cardiac arrest treatment industry features moderate consolidation. Top device makers—Medtronic, Boston Scientific, and Abbott—control broad portfolios ranging from implantable cardioverter-defibrillators to catheter-based ablation tools. In 2025, Medtronic secured FDA clearance for its OmniaSecure lead, reinforcing its leadership in transvenous systems. Boston Scientific acquired Bolt Medical for USD 664 million to add intravascular lithotripsy capabilities that enhance its structural-heart toolbox. Abbott launched the ASCEND CSP trial, underscoring its bet on conduction-system pacing that merges pacing and defibrillation within a single modular ecosystem .

Investment flows exceed USD 60 billion across rhythm management, mechanical support, and coronary intervention subfields, signalling confidence in long-run demand for integrated solutions. Patent filings centre on algorithmic risk scoring, fault-tolerant battery chemistries, and low-profile vascular access routes. Post-recall scrutiny drives firms to elevate supplier-quality audits and diversify component sourcing, with several relocating capacitor production from single-site Asian foundries to dual-source models in North America and Europe. Mid-tier players such as ZOLL and Stryker compete aggressively in public-access AED tenders by bundling cloud-based maintenance dashboards and certified training platforms, enhancing stickiness among municipal buyers.

Start-ups focus on wearable, patch-based defibrillators that pair always-on ECG analytics with autonomous shock delivery, positioning themselves as adjuncts rather than full replacements for implantable systems. Strategic alliances between software vendors and EMS providers create end-to-end data ecosystems that feed machine-learning engines, continuously refining rhythm-prediction accuracy. Larger incumbents respond by opening API gateways to harmonise data flows, thus protecting installed bases while facilitating interoperability demanded by hospital IT departments.

Global Cardiac Arrest Treatment Industry Leaders

Koninklijke Philips N.V

Abbott Laboratories

Medtronic plc

Boston Scientific Corporation

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Medtronic received FDA approval for the OmniaSecure defibrillation lead, the smallest transvenous lead yet cleared for right-ventricle placement.

- April 2025: Abbott initiated the ASCEND CSP pivotal trial for investigational conduction-system pacing leads following strong feasibility-study outcomes.

- February 2025: Teleflex agreed to acquire BIOTRONIK’s vascular-intervention unit for EUR 760 million, expanding its coronary and peripheral portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the cardiac arrest treatment market as the annual revenue generated worldwide from pharmacological interventions (anti-arrhythmic agents, vasopressors, inotropes and related emergency drugs) alongside therapeutic devices that deliver, support or restore circulation during sudden cardiac arrest, including external and implantable defibrillators, extracorporeal membrane oxygenation (ECMO), intra-aortic balloon pumps, temporary percutaneous ventricular assist devices and similar life-sustaining platforms.

Scope exclusion: The study does not quantify post-resuscitation rehabilitation, diagnostic-only consumables or stand-alone training services.

Segmentation Overview

- By Product (Value)

- Devices

- Defibrillators

- Extracorporeal Membrane Oxygenation (ECMO)

- Intra-aortic Balloon Pump (IABP)

- Percutaneous VAD (Impella)

- Other Devices

- Drugs

- Anti-arrhythmic Drugs

- Class I – Sodium-channel Blockers

- Class II – Beta-blockers

- Class III – Potassium-channel Blockers

- Class IV – Calcium-channel Blockers|||

- Others (Digoxin, Adenosine)

- Vasopressors & Inotropes

- Anti-arrhythmic Drugs

- Devices

- By End User (Value)

- Hospitals & Cardiac Centres

- Emergency Medical Services (EMS)

- Home & Alternate Care Settings

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with emergency physicians, biomedical engineers, supply-chain managers and reimbursement specialists across North America, Europe, Asia-Pacific and the Gulf. Their insights refined assumed average selling prices, clarified country-level uptake of public-access defibrillator programs and stress-tested growth drivers flagged during desk work.

Desk Research

Our analysts first mapped the treatment pathway using open datasets from the World Health Organization, the American Heart Association, European Resuscitation Council and the National EMS Information System. They then matched incidence figures with export-import codes from UN Comtrade and US ITC to size device flows. Regulatory filings, FDA 510(k) summaries, EUDAMED notifications, peer-reviewed studies on drug efficacy and company 10-Ks strengthened the baseline. Paid feeds such as D&B Hoovers and Dow Jones Factiva helped verify revenue splits and identify emerging suppliers. Numerous additional public sources were assessed; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down construct converts out-of-hospital and in-hospital arrest incidence into treatable patient pools, to be further filtered through survival rates, protocol adherence and device penetration. Results are corroborated with selective bottom-up checks such as sampled ASP-by-volume roll-ups from key OEMs and hospital tenders. Critical model inputs include cardiac arrest incidence per 100,000 population, public AED density, reimbursement coverage ratios, median device replacement cycles and pipeline drug launch probabilities. Forecasts employ multivariate regression blended with scenario analysis so the model responds to shifts in CPR guideline updates, macroeconomic outlook and currency effects. Gaps in bottom-up estimates are bridged using weighted regional analogs reviewed with field experts.

Data Validation & Update Cycle

Before sign-off, we run anomaly searches, variance checks and peer reviews. Any material deviation triggers follow-up calls. The report is refreshed every twelve months, with ad-hoc updates when recalls, landmark trials or reimbursement shocks materially alter demand.

Why our Cardiac Arrest Treatment Baseline stands up to scrutiny

Published estimates often diverge because firms choose different product baskets, price ladders or refresh timelines. Our disciplined scope selection and annual model rebuild keep the baseline tightly aligned with real-world buying patterns.

Key gap drivers include whether advanced mechanical circulatory support is counted, if sales are reported at list or blended transaction prices, and how inpatient drug volumes are normalized across currencies and care settings. By documenting every assumption, Mordor delivers a traceable and balanced view that decision-makers can reproduce.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| US $ 5.26 B (2025) | Mordor Intelligence | - |

| US $ 5.00 B (2024) | Global Consultancy A | Omits ECMO and temporary VAD revenue |

| US $ 16.23 B (2021) | Trade Journal B | Bundles wider cardiovascular devices and hospital service fees |

The comparison shows that once like-for-like scope, currency and year are aligned, our figure sits comfortably between optimistic roll-ups and narrow device-only counts, giving clients a dependable midpoint for strategic planning.

Key Questions Answered in the Report

What is the current size of the cardiac arrest treatment market?

The market stands at USD 5.5 billion in 2026, with a forecast value of USD 6.84 billion by 2031.

Which product category holds the largest share?

Devices account for 69.12% of 2025 revenue, driven by defibrillators and portable ECMO systems.

Which region is growing the fastest?

Asia-Pacific leads growth with a 7.55% CAGR through 2031 as governments scale emergency-care capacity.

How are recalls affecting market growth?

Recent Class I recalls reduce short-term CAGR by an estimated 0.9%, prompting stricter quality controls among manufacturers.

Why are public-access defibrillator programs important?

Legislation mandating AED placement in schools and public venues improves device density and boosts survival rates by enabling earlier shocks.

Page last updated on: