Dilated Cardiomyopathy Therapeutic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

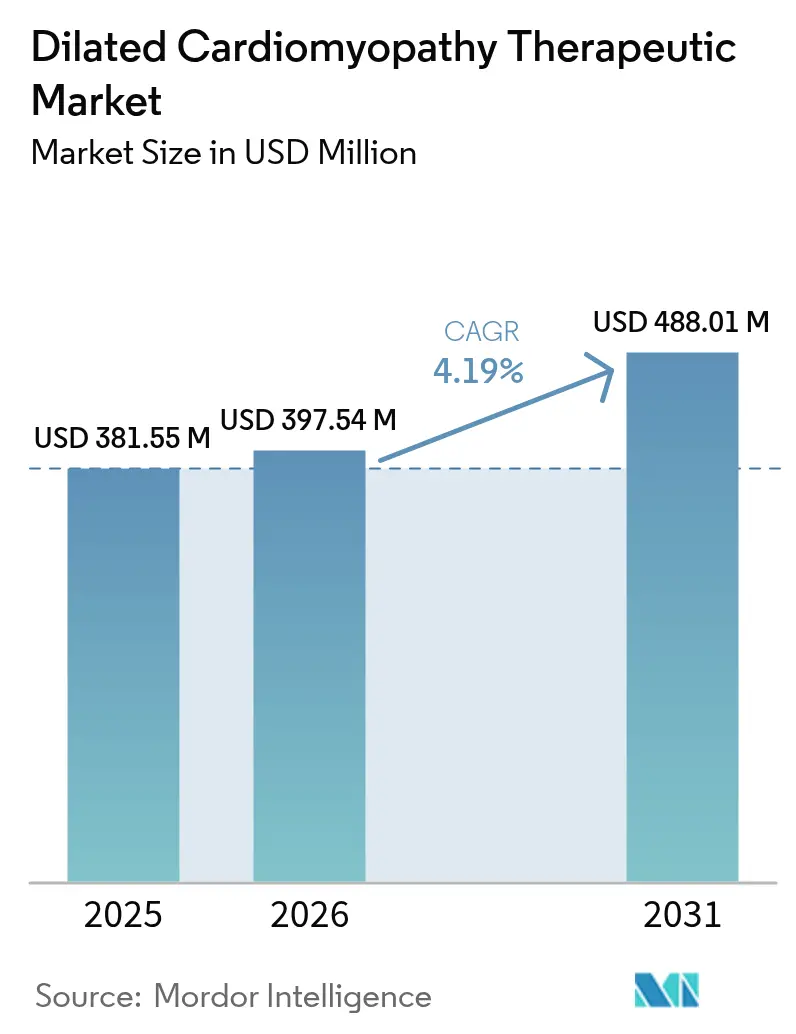

| Market Size (2026) | USD 397.54 Million |

| Market Size (2031) | USD 488.01 Million |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

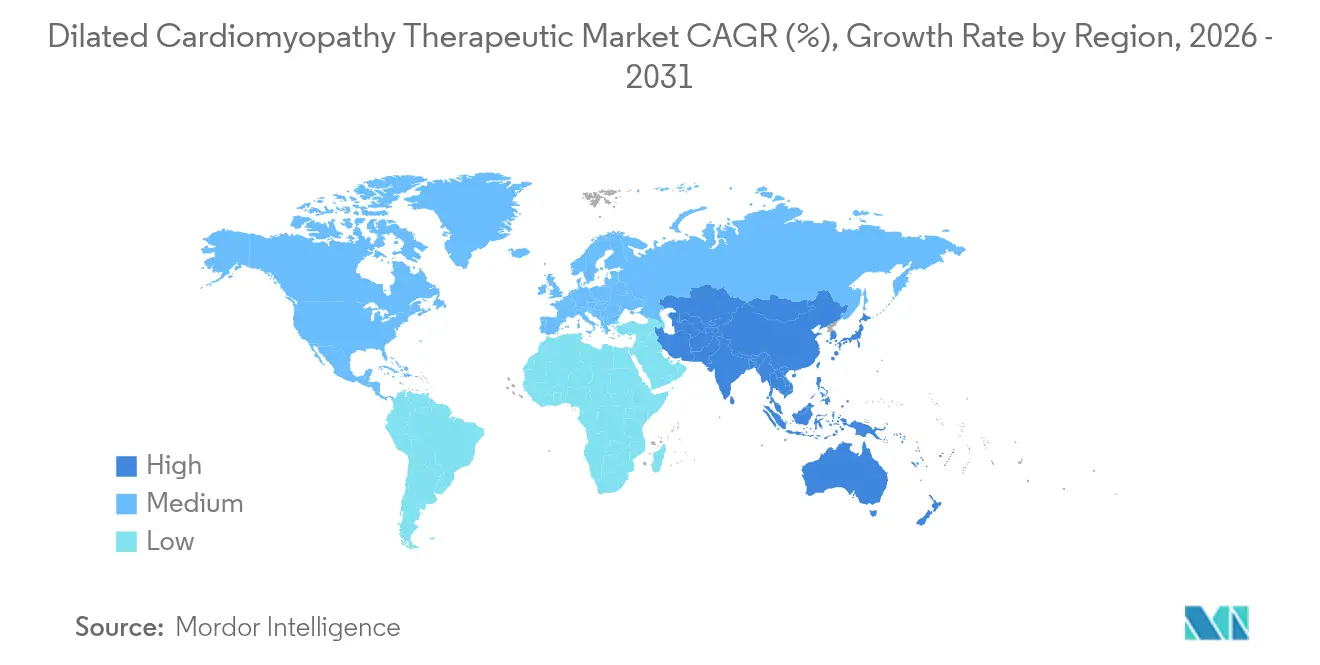

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

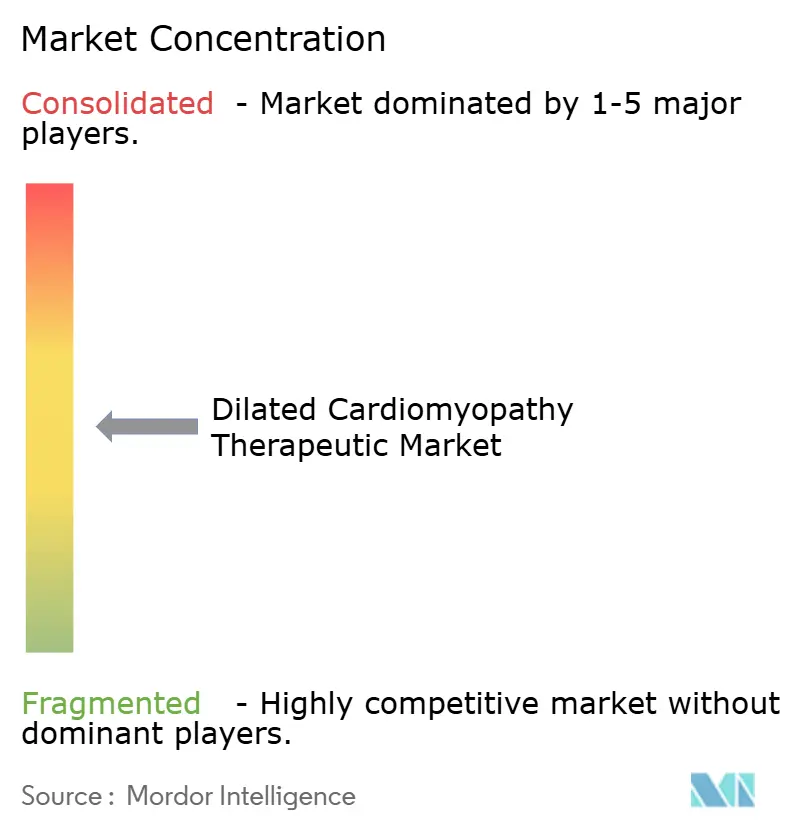

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dilated Cardiomyopathy Therapeutic Market Analysis by Mordor Intelligence

The dilated cardiomyopathy therapeutic market size in 2026 is estimated at USD 397.54 million, growing from 2025 value of USD 381.55 million with 2031 projections showing USD 488.01 million, growing at 4.19% CAGR over 2026-2031. Demand rises as precision medicine converges with legacy heart-failure pharmacology, giving drug developers clear targets that promise disease-modifying benefit rather than symptom relief alone. SGLT-2 inhibitors, originally diabetes agents, now improve cardiovascular survival in dilated cardiomyopathy, signalling a shift toward metabolic modulation. Simultaneously, genetic profiling is carving rare but lucrative sub-segments that reward high-value therapeutics able to match specific molecular defects. Regulators are supporting this evolution with orphan-drug incentives, yet clinicians still rely on ACE inhibitors and beta-blockers as the therapeutic backbone, underscoring the market’s blend of established volume products and high-margin precision assets.

Key Report Takeaways

- By drug class, ACE inhibitors held 34.10% of the dilated cardiomyopathy therapeutic market share in 2025, while SGLT-2 inhibitors are projected to expand at a 6.43% CAGR through 2031.

- By route of administration, oral formulations captured 58.10% of the dilated cardiomyopathy therapeutic market size in 2025, whereas implantable and device-mediated delivery is forecast to grow at 7.74% CAGR between 2026 and 2031.

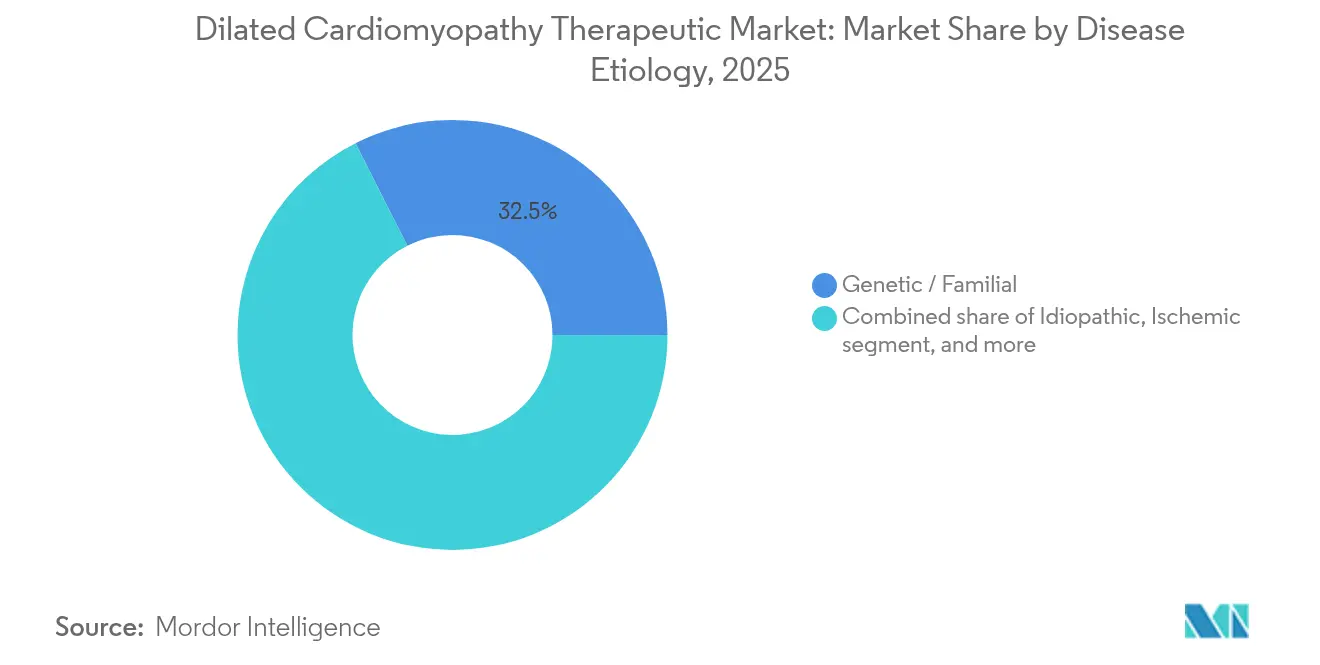

- By disease etiology, genetic and familial cases accounted for 32.45% of the dilated cardiomyopathy therapeutic market size in 2025, while idiopathic dilated cardiomyopathy is advancing at a 6.75% CAGR through 2031.

- By end user, hospitals led with 59.70% of the dilated cardiomyopathy therapeutic market share in 2025, whereas research and academic institutes are predicted to post a 7.53% CAGR over the forecast period.

- By geography, North America commanded 42.10% of the dilated cardiomyopathy therapeutic market size in 2025, and Asia-Pacific is projected to expand at a 5.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dilated Cardiomyopathy Therapeutic Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of cardiovascular diseases | +1.2% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Growing awareness and early diagnosis of dilated cardiomyopathy | +0.8% | Global, early gains in developed markets | Medium term (2-4 years) |

| Technological advances in heart-failure pharmacotherapy | +0.6% | North America & EU core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption of precision medicine and genetic testing | +0.4% | North America & EU primarily | Long term (≥ 4 years) |

| Robust pipeline of novel therapies and regulatory support | +0.3% | Global, with regulatory leadership in the US & EU | Short term (≤ 2 years) |

| Expanding healthcare expenditure in emerging economies | +0.2% | Asia-Pacific core, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Cardiovascular Diseases

Heart-failure prevalence climbed from 25.43 million cases in 1990 to 55.50 million in 2021, increasing the downstream pool of dilated cardiomyopathy patients who survive acute ischemic events yet progress to chronic ventricular dysfunction. Emerging economies accelerate this burden as urban lifestyles raise hypertension, obesity and metabolic syndrome rates. Longevity gains compound incidence because improved acute care keeps vulnerable myocardium alive long enough to decompensate. Clinicians therefore encounter broader phenotypic variation, urging tailored therapy bundles that move beyond one-size-fits-all protocols. Drug makers recognise the opportunity to segment on comorbid metabolic status, offering combination regimens that synchronise neuro-hormonal blockade with metabolic re-programming. Collectively, disease prevalence and survivorship extend the addressable base for the dilated cardiomyopathy therapeutic market.

Growing Awareness and Early Diagnosis of Dilated Cardiomyopathy

The 2024 European Society of Cardiology criteria for nondilated left ventricular cardiomyopathy enable intervention before overt chamber enlargement, potentially expanding the treatable cohort by 30-40%[1]European Society of Cardiology Working Group, “Definition and Classification of Nondilated LV Cardiomyopathy,” springer.com. Cardiac MRI and strain echocardiography detect subclinical fibrosis, guiding earlier drug initiation. Familial screening programmes uncover mutation carriers decades before symptoms, while consumer genetics platforms seed patient self-referral to specialised clinics. These diagnostic shifts pull therapeutic demand forward in the disease timeline, creating longer treatment windows per patient. Early-stage intervention also boosts response rates, bolstering real-world-evidence packages that facilitate reimbursement. Consequently, drug developers integrate biomarker-based enrichment into clinical trials, accelerating time-to-proof and sharpening market positioning.

Technological Advances in Heart Failure Pharmacotherapy

The 2024 American College of Cardiology consensus endorses quadruple therapy—ARNi, beta-blocker, mineralocorticoid antagonist and SGLT-2 inhibitor—delivered simultaneously to maximise synergistic pathway coverage[2]American College of Cardiology, “2024 Expert Consensus Decision Pathway on Cardiomyopathies,” acc.org. SGLT-2 inhibitors demonstrate cardio-protection independent of glucose control, acting through natriuresis, improved energetics and anti-inflammatory effects. ARNi compounds sustain natriuretic peptide activity, reducing ventricular wall stress. These poly-pathway regimens demand precise titration; digital therapeutics now monitor renal function and haemodynamics remotely, prompting dose adjustments that keep adverse events low. Pharmaceutical firms therefore partner with software vendors to embed adherence and monitoring services, turning pills into value-based care packages—an emerging differentiator in the dilated cardiomyopathy therapeutic industry.

Increasing Adoption of Precision Medicine and Genetic Testing

Roughly 35-40% of dilated cardiomyopathy cases have an identifiable genetic driver, with LMNA, BAG3 and titin mutations among the most prevalent. Phase 3 programs such as REALM-DCM (ARRY-371797 in LMNA mutations) epitomise genotype-defined trials. BAG3 gene-replacement therapy RP-A701 recently obtained US IND clearance and targets a 2,000-patient US prevalence segment. Smaller populations justify premium pricing that balances development cost. Companion diagnostics become mandatory, opening ancillary revenue streams and creating co-launch synergies between biotech firms and sequencing companies. Precision cohorts also reduce placebo variability, shortening enrolment and powering efficacy signals that de-risk capital investment in the dilated cardiomyopathy therapeutic market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs and reimbursement barriers | -0.7% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Stringent regulatory requirements and prolonged approval timelines | -0.5% | Global, persistent hurdles in US, EU, Japan | Long term (≥ 4 years) |

| Safety concerns and adverse effects of polypharmacy | -0.4% | Global, especially among elderly, multi-morbid patients | Short term (≤ 2 years) |

| Limited access to advanced therapies in low- and middle-income regions | -0.3% | LMICs across Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Reimbursement Barriers

Mavacamten lists near USD 300,000 annually, while single-dose gene therapies could top USD 1 million, deterring uptake even in insured populations. Payers demand longitudinal outcome data before broad coverage, yet such evidence matures years after launch, delaying revenue inflection. Emerging economies rely on out-of-pocket spending, restricting access to affluent urban consumers and truncating volume growth. Advanced therapies also require serial imaging, genomics and biomarker surveillance, piling ancillary costs onto health systems. Manufacturers are therefore piloting outcomes-based contracts and instalment payment models, yet pricing scepticism persists and tempers the expansion pace of the dilated cardiomyopathy therapeutic market.

Stringent Regulatory Requirements and Prolonged Approval Timelines

Aficamten’s PDUFA date was extended to December 2025 to accommodate detailed REMS discussions, illustrating how safety-monitoring frameworks can hold back launch timelines. Gene therapies face vector integration and off-target editing questions that force regulators to demand decade-long follow-up. Combination protocols must show additive benefit and acceptable interaction profiles, increasing trial complexity and cost. Smaller biotechs often lack the capital to navigate revisions, leading to partnership or acquisition as the only viable exit. Collectively, protracted approvals raise development risk, discourage competitive entry and slow innovation velocity within the dilated cardiomyopathy therapeutic industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: SGLT-2 Inhibitors Drive Metabolic Revolution

Current prescriptions continue to lean on ACE inhibitors, yet their 34.10% share in 2025 is gradually eroding as SGLT-2 inhibitors scale fast on a 6.43% CAGR trajectory, bolstered by robust mortality-reduction data. Neuro-hormonal agents retain guideline primacy, but metabolic re-programming introduces a novel disease-modification layer that resonates with cardiologists treating multi-morbid patients. Development pipelines now spotlight cardiac myosin inhibitors and sarcomere modulators targeting contractile mechanics directly; mavacamten set the precedent, and aficamten follows with REMS refinement. Cell-based therapies such as Deramiocel deliver regenerative cues, whereas ARNi products bridge traditional and emerging paradigms by enhancing natriuretic signalling. This breadth of mechanistic diversity enlarges therapeutic armamentarium and supports a complex competitive mosaic for the dilated cardiomyopathy therapeutic market.

Second-generation SGLT-2 assets pursue once-weekly dosing to heighten adherence. Meanwhile, research into mitochondrial modulators seeks to correct energy deficits intrinsic to dilated myocardium. Combination packs that blend neuro-hormonal blockade with metabolic agents are in early trials, foreshadowing fixed-dose formulations that may dominate future prescriptions. Pricing strategies pivot on additive benefit demonstrated in head-to-head trials, an arena where precision-stratified sub-studies confer advantage. The result is a highly segmented yet synergistic product landscape that gives clinicians flexible algorithms while challenging payers to reconcile overlapping indications across chronic comorbidities.

By Route of Administration: Device Integration Reshapes Delivery

Oral formulations remain the most widely used owing to convenience and familiarity. However, growth momentum is shifting toward device-enabled delivery platforms that supply consistent mechanical or electrical support and circumvent adherence barriers. Leadless left-ventricular pacing, conduction-system pacing and cardiac contractility modulation exemplify minimally invasive implants that augment pharmacotherapy. The 2025 ACC/AHA appropriate-use criteria list 335 clinical scenarios guiding when and how to combine drugs with hardware, reflecting the sophisticated decision tree now facing electrophysiologists [JACC.ORG]. Subcutaneous infusion pumps for novel biologics are also progressing through feasibility studies, promising sustained exposure while avoiding hospital infusion suites.

Digital ecosystems tethered to implants stream haemodynamic data into cloud analytics, permitting algorithm-driven dose adjustment of concomitant oral agents. This closed-loop paradigm blurs the boundary between drug and device markets and invites joint ventures between med-tech and pharmaceutical firms. Though initial capital outlay is high, value-based contracting frameworks linking reimbursement to reduced hospitalisation are emerging, creating economic headroom for premium technologies and expanding total spending within the dilated cardiomyopathy therapeutic market.

By Disease Etiology: Genetic Insights Drive Targeted Approaches

Genetic and familial etiologies accounted for 32.45% of the dilated cardiomyopathy therapeutic market share in 2025, reflecting high diagnostic clarity and organised patient advocacy that accelerates trial enrolment. Idiopathic cases, despite unclear origins, represent the fastest-growing segment as enhanced imaging exposes previously undetected disease; their 6.75% CAGR speaks to a sizeable unmet need in patients who do not map to single-gene defects. Ischemic, toxin-induced and endocrine-metabolic subtypes together form a heterogeneous remainder that still benefits from guideline medical therapy but may soon receive precision options as polygenic risk models mature.

Gene-replacement platforms target monogenic niches such as BAG3 or LMNA, while RNA-modulation therapeutics pursue microRNA pathways implicated across multiple etiologies. Adaptive clinical-trial designs use shared placebo arms and etiological biomarker panels to improve efficiency across these sub-studies, lowering cost per approval. This modular approach is expected to multiply new-drug launches without saturating any single patient pool, thereby sustaining revenue diversity in the dilated cardiomyopathy therapeutic market.

By End User: Research Institutes Accelerate Innovation

Hospitals remain the principal dispensing channel, yet academic medical centres and research institutes are posting the sharpest volume increase as they run precision-therapy trials and compassionate-use programmes. Their participation speeds first-in-human work, attracts philanthropic funding and concentrates rare-disease expertise that primary hospitals lack. Over 500 subjects enrolled in the ACACIA-HCM study illustrate the scale required to validate myosin inhibitors, and similar infrastructure is now repurposed for dilated cardiomyopathy. Specialty clinics subsequently disseminate protocols to community cardiologists, extending reach without diluting care quality.

Integration of artificial intelligence curates large echocardiography archives, flagging potential candidates for research therapies and diverting them into registry cohorts that inform future label expansions. Academic-industry consortia also advocate for adaptive reimbursement that follows evidence maturation, accelerating market adoption once agents win approval. These dynamics position research centres as both innovation hubs and early high-volume customers within the dilated cardiomyopathy therapeutic industry.

Geography Analysis

North America anchors the dilated cardiomyopathy therapeutic market with 42.10% of global revenue in 2025, underpinned by mature reimbursement systems and guideline leadership that endorses rapid uptake of novel classes. The region’s high prevalence of obesity and hypertension sustains a broad pharmacological base, while well-funded academic centres spearhead gene-therapy trials attracting inward investment. Convergence of payer pressure and outcomes-based contracts is gradually shifting economic risk onto manufacturers, yet premium drugs still win adoption where real-world data verify hospitalisation reductions.

Europe follows with steady single-digit growth, supported by cross-border reference pricing and the European Medicines Agency’s rolling-review pathway that accelerates authorisation for breakthrough therapies. Country-level heterogeneity persists—Germany embraces device integration swiftly whereas Southern Europe remains price-sensitive—yet guideline harmonisation maintains consistent clinical practice. The dilated cardiomyopathy therapeutic market benefits from strong patient-advocacy networks in the United Kingdom, Netherlands and Scandinavia, which facilitate registry-driven evidence gathering that convinces public payers to reimburse high-cost precision agents.

Asia-Pacific, growing at 5.39% CAGR, is reshaping the global outlook as China’s heart-failure prevalence rises faster than the world average and governments boost cardiovascular budgets. Japan’s super-aged demographic fuels device uptake, while India’s emerging middle class diversifies demand beyond public tertiary hospitals into private cardiology chains. Regulatory agencies in China and South Korea are launching real-time review pilots to shorten approval lag behind the US and EU, promising earlier revenue capture for multinational sponsors. Nonetheless, variable insurance coverage and price caps compel tiered-pricing models that preserve volume while protecting global list pricing integrity within the dilated cardiomyopathy therapeutic market.

Competitive Landscape

Large cardiovascular incumbents—Novartis, AstraZeneca and Bristol-Myers Squibb—continue to derive significant sales from neuro-hormonal classes but now chase metabolic and genetic targets to sustain growth. Acquisition activity reflects this pivot: Eli Lilly’s USD 1.3 billion purchase of Verve Therapeutics secured adenine-base-editing tools for inherited lipid disorders with cardiomyopathy overlap. Novo Nordisk’s EUR 1 billion buy-out of Cardior Pharmaceuticals added microRNA therapeutics that modulate maladaptive remodelling. These deals underline the premium on platform technologies that can generate multiple pipeline assets rather than single products.

Mid-cap innovators such as Cytokinetics specialise in sarcomere biology and have advanced aficamten into late review, while Rocket Pharmaceuticals focuses exclusively on monogenic cardiomyopathies. Cell-therapy entrants Capricor and Mesoblast explore allogeneic approaches aimed at myocardial regeneration. Competitive intensity is highest in SGLT-2 inhibitors where class members hold interchangeable labels, leading firms to differentiate through fixed-dose combinations and digital-monitoring add-ons. Conversely, gene-therapy and myosin-inhibitor classes show limited head-to-head rivalry, preserving pricing power and margin but requiring substantial education to drive adoption in the dilated cardiomyopathy therapeutic market.

Strategic collaborations bridge diagnostics and therapeutics: Illumina partners with pharma to co-develop next-generation panels that stratify trial enrolment, while med-tech vendors embed pharmacological decision support in implant dashboards. Artificial-intelligence-led drug discovery further blurs sector lines; partnerships with software giants accelerate target identification and shorten preclinical phases. Collectively, these alliances create integrated care ecosystems that extend competitive boundaries beyond traditional formularies into the broader dilated cardiomyopathy therapeutic industry.

Dilated Cardiomyopathy Therapeutic Industry Leaders

AstraZeneca PLC

Pfizer Inc.

Novartis AG

Bristol Myers Squibb (Incl. MyoKardia)

Capricor Therapeutics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Verve Therapeutics reported positive initial data from the Heart-2 Phase 1b trial of VERVE-102, achieving a mean LDL-C reduction of 53% with FDA Fast Track status.

- May 2025: Cytokinetics confirmed FDA extension of aficamten’s PDUFA date to December 26 2025 and completed enrolment of over 500 patients in ACACIA-HCM.

- April 2025: Boston Scientific posted record Q1 2025 cardiovascular revenue of USD 4.663 billion and launched the ELEVATE-PF and OPTION-A trials.

- February 2025: BridgeBio Pharma secured FDA approval for Attruby (acoramidis) to treat transthyretin amyloid cardiomyopathy.

- December 2024: Eli Lilly finalised its USD 1.3 billion acquisition of Verve Therapeutics.

- November 2024: Novo Nordisk bought Cardior Pharmaceuticals for more than EUR 1 billion.

Global Dilated Cardiomyopathy Therapeutic Market Report Scope

As per the scope of the report, dilated cardiomyopathy is a disease of the heart muscle, usually starting in the heart's main pumping chamber (left ventricle). The ventricle stretches and thins (dilates) and can't pump blood as well as a healthy heart can. In general terms, it refers to the abnormality of the heart muscle itself. The Dilated Cardiomyopathy Therapeutic Market is segmented by Drug Class (Aldosterone antagonists, Angiotensin-converting enzyme (ACE) inhibitors, Angiotensin II receptor blockers, Beta-blockers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| ACE Inhibitors |

| Beta-Blockers |

| Angiotensin II Receptor Blockers |

| Aldosterone Antagonists |

| Angiotensin Receptor-Neprilysin Inhibitors (ARNi) |

| SGLT-2 Inhibitors |

| Other / Emerging (Gene, Cell, Myosin Modulators) |

| Oral |

| Intravenous |

| Subcutaneous |

| Implantable / Device-Mediated |

| Genetic / Familial |

| Idiopathic |

| Ischemic |

| Toxin-Induced (Alcohol, Chemotherapy, Etc.) |

| Infectious / Inflammatory |

| Endocrine / Metabolic |

| Other Diseases |

| Hospitals |

| Specialty Cardiology Clinics |

| Research & Academic Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | ACE Inhibitors | |

| Beta-Blockers | ||

| Angiotensin II Receptor Blockers | ||

| Aldosterone Antagonists | ||

| Angiotensin Receptor-Neprilysin Inhibitors (ARNi) | ||

| SGLT-2 Inhibitors | ||

| Other / Emerging (Gene, Cell, Myosin Modulators) | ||

| By Route Of Administration | Oral | |

| Intravenous | ||

| Subcutaneous | ||

| Implantable / Device-Mediated | ||

| By Disease Etiology | Genetic / Familial | |

| Idiopathic | ||

| Ischemic | ||

| Toxin-Induced (Alcohol, Chemotherapy, Etc.) | ||

| Infectious / Inflammatory | ||

| Endocrine / Metabolic | ||

| Other Diseases | ||

| By End User | Hospitals | |

| Specialty Cardiology Clinics | ||

| Research & Academic Institutes | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the dilated cardiomyopathy therapeutic market?

The dilated cardiomyopathy therapeutic market size is USD 397.54 million in 2026.

Which drug class is growing fastest?

SGLT-2 inhibitors lead growth with a 6.43% CAGR through 2031, reflecting cardioprotective benefits beyond glucose control.

Why is Asia-Pacific seen as the key growth region?

Rising cardiovascular prevalence, expanding healthcare investment and accelerated regulatory review are driving a 5.39% CAGR in Asia-Pacific.

How are genetics shaping new therapies?

About 35-40% of cases are mutation-linked, enabling targeted treatments such as LMNA-focused small molecules and BAG3 gene-replacement vectors.

What limits wider adoption of advanced therapies?

High cost, reimbursement delays and lengthy regulatory evaluations slow diffusion despite demonstrated efficacy.

Which companies recently made strategic acquisitions?

Eli Lilly bought Verve Therapeutics for gene-editing capabilities, and Novo Nordisk acquired Cardior Pharmaceuticals for microRNA assets, highlighting the premium on precision-cardiology platforms.

Page last updated on: