Fruit Snack Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

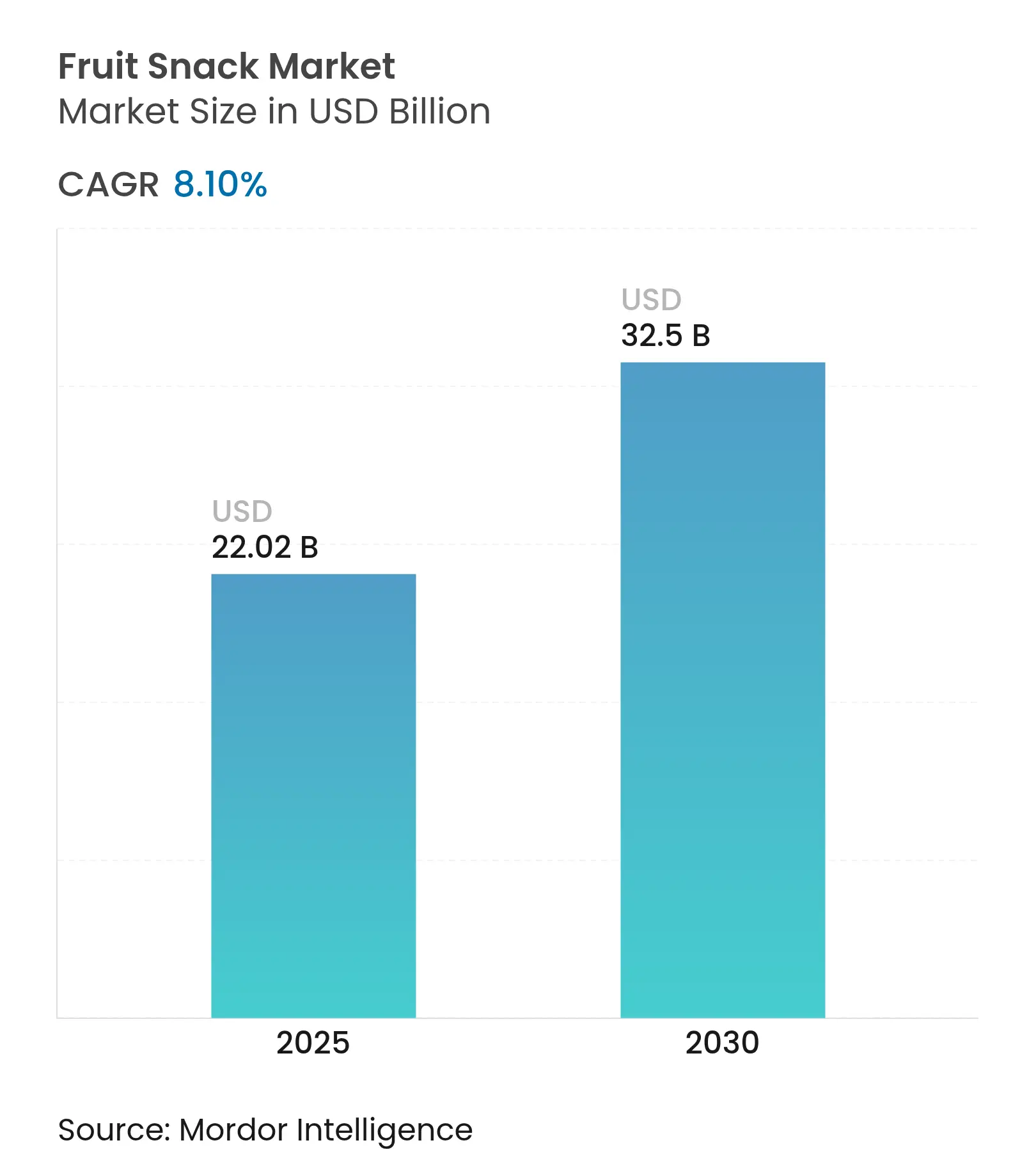

| Market Size (2025) | USD 22.02 Billion |

| Market Size (2030) | USD 32.5 Billion |

| Growth Rate (2025 - 2030) | 8.10 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Fruit Snack Market Analysis by Mordor Intelligence

The Fruit Snack Market size is estimated at USD 22.02 billion in 2025, and is expected to reach USD 32.5 billion by 2030, at a CAGR of 8.10% during the forecast period (2025-2030). This robust expansion reflects fundamental shifts in consumer preferences toward healthier snacking alternatives, driven by rising health consciousness and demand for functional nutrition [1]Source: WHO (World Health Organization), "Healthy diet", who.int. The market's momentum is further amplified by regulatory support for organic certification standards, with USDA organic labeling requirements creating premium positioning opportunities for manufacturers[2]Source: U.S Department of Agriculture, "Regulatory support for organic certification standards", ams.usda.gov. Regulatory clarity, functional ingredient advances, and packaging innovations keep new launches frequent and varied, while tightening producer price trends test operating margins for all but the most efficient manufacturers. E-commerce penetration, especially in Asia-Pacific, supports direct brand–consumer engagement, fostering loyalty and data-driven portfolio refinement. The acceleration in Asia-Pacific, being a dominant market, stems from urbanization trends, rising disposable incomes, and regulatory harmonization efforts, particularly in markets like South Korea where MFDS food labeling reforms enhance consumer trust in processed fruit products.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fruit Snack Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Consumer Demand For Healthier Snack Options

Rising Consumer Demand For Healthier Snack Options

| +1.8% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Global, with strongest impact in North America &

Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

Growth In Vegan, Gluten-Free, And Allergen-Free Fruit

Snack Options

Growth In Vegan, Gluten-Free, And Allergen-Free Fruit

Snack Options

| +1.2% | North America & EU core, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

Growing Trend Of On-The-Go And Convenient Snacking

Growing Trend Of On-The-Go And Convenient Snacking

| +1.5% | Global, with urban concentration in Asia-Pacific & North America | Short term (≤ 2 years) | |||

Innovation In Flavors, Product Formats, And Packaging

Innovation In Flavors, Product Formats, And Packaging

| +1.0% | Global, with premium positioning in developed markets | Medium term (2-4 years) | |||

Rising Awareness About Functional Benefits Like Added

Vitamins, Fiber, Probiotics

Rising Awareness About Functional Benefits Like Added

Vitamins, Fiber, Probiotics

| +1.3% | North America & Europe, emerging in Asia-Pacific | Long term (≥ 4 years) | |||

Expansion of E-Commerce And Online Retail Sales Channels Expansion of E-Commerce And Online Retail Sales Channels | +0.9% | Global, with accelerated adoption in Asia-Pacific & North America | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Consumer Demand For Healthier Snack Options

Health-conscious consumption patterns are fundamentally reshaping fruit snacks positioning as consumers increasingly scrutinize nutritional profiles and ingredient transparency. WHO dietary guidelines recommending reduced sugar intake below 10% of total energy consumption have elevated fruit snacks as preferable alternatives to traditional confectionery, particularly when formulated with natural fruit concentrates and minimal added sugars. This shift creates competitive advantages for manufacturers emphasizing whole fruit content and clean label formulations. USDA organic certification standards provide regulatory framework validation, with certified organic fruit snacks commanding premium pricing despite production cost increases. The trend accelerates in developed markets where health literacy correlates with purchasing power, enabling sustained margin expansion for brands successfully communicating nutritional benefits. Regulatory compliance factors through FDA nutrition labeling requirements enhance consumer confidence in product claims, supporting market penetration strategies.

Growth In Vegan, Gluten-Free, And Allergen-Free Fruit Snack Options

Specialized dietary requirements are driving product innovation beyond traditional fruit snack formulations, creating niche segments with accelerated growth trajectories. NSF International certification standards for gluten-free, non-GMO, and allergen-free products provide third-party validation that reduces consumer skepticism and enables premium positioning [3]Source: NSF International, "International certification standards", nsf.org. Manufacturing complexity increases significantly for allergen-free production, requiring dedicated facilities and supply chain segregation, yet market premiums of 15-25% justify investment costs. Vegan formulations eliminate gelatin and dairy-based binding agents, necessitating alternative texturizing solutions through plant-based hydrocolloids and natural fruit pectins. Cross-contamination prevention protocols aligned with FDA allergen labeling regulations create competitive moats for established manufacturers with appropriate infrastructure. The segment expansion reflects demographic shifts toward plant-based diets and increased allergen awareness, particularly among millennial and Gen Z consumers driving purchasing decisions.

Growing Trend of On-The-Go and Convenient Snacking

Urbanization patterns and lifestyle acceleration are fundamentally altering snacking occasions, with portable fruit snacks capturing incremental consumption beyond traditional meal replacement scenarios. Packaging innovation in resealable pouches and single-serve formats addresses mobility requirements while maintaining product freshness and portion control. The trend intersects with workplace snacking culture, where fruit snacks provide perceived health benefits compared to vending machine alternatives. Supply chain optimization for convenience distribution requires different logistics approaches, with shorter shelf-life products demanding faster inventory turnover and regional distribution strategies. Consumer willingness to pay convenience premiums creates margin expansion opportunities for brands successfully executing portable packaging solutions. E-commerce fulfillment capabilities become critical as on-the-go consumption patterns drive impulse purchasing through mobile platforms and subscription services.

Innovation In Flavors, Product Formats, And Packaging

Product differentiation through sensory innovation is creating competitive separation in an increasingly crowded marketplace, with manufacturers exploring exotic fruit combinations and functional ingredient integration. General Mills' 2024 launch of Minecraft and Disney Moana licensed fruit snacks demonstrates cross-industry collaboration strategies that leverage entertainment properties for market penetration. Packaging technology advances in barrier films and modified atmosphere packaging extend shelf life while maintaining nutritional integrity, enabling broader geographic distribution and reduced waste. Flavor innovation extends beyond traditional fruit profiles to include vegetable-fruit blends and superfruit combinations that command premium pricing. Format diversification into squeezable pouches, freeze-dried chips, and gummy textures addresses different consumption preferences and age demographics. Regulatory compliance factors through FDA food additive approvals influence innovation timelines but provide market exclusivity for approved formulations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Competition From Alternative Healthy Snack Categories Such

As Nuts And Seeds

Competition From Alternative Healthy Snack Categories Such

As Nuts And Seeds

| -0.8% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, with strongest impact in North America &

Europe

|

Impact Timeline

:

Medium term (2-4 years)

|

High Cost Of Organic And Natural Fruit Snacks Compared To

Traditional Snacks

High Cost Of Organic And Natural Fruit Snacks Compared To

Traditional Snacks

| -0.6% | North America & Europe, emerging pressure in Asia-Pacific | Long term (≥ 4 years) | |||

Consumer Concerns Over Added Sugar Content In Some Fruit

Snacks

Consumer Concerns Over Added Sugar Content In Some Fruit

Snacks

| -0.5% | Global, with regulatory pressure in developed markets | Short term (≤ 2 years) | |||

Consumer Skepticism About Processed Fruit Snack

Nutritional Value

Consumer Skepticism About Processed Fruit Snack

Nutritional Value

| -0.4% | North America & Europe, expanding to educated urban Asia-Pacific | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Competition From Alternative Healthy Snack Categories Such As Nuts And Seeds

Alternative snacking categories are capturing health-conscious consumers through superior nutritional profiles and perceived naturalness, creating competitive pressure on processed fruit snacks positioning. Nuts and seeds offer protein content and healthy fats that fruit snacks cannot match, appealing to consumers prioritizing satiety and nutritional density. UN COMTRADE data shows expanding global trade in tree nuts and seeds, indicating supply chain development that supports competitive pricing and availability. Raw and minimally processed positioning of alternative snacks contrasts with fruit snacks' manufactured perception, despite functional ingredient enhancements. Premium pricing tolerance for nuts and seeds demonstrates consumer willingness to pay for perceived health benefits, suggesting market share vulnerability for fruit snacks lacking clear nutritional differentiation. Cross-category competition intensifies in convenience retail channels where shelf space allocation reflects consumer preference shifts.

High Cost of Organic and Natural Fruit Snacks Compared To Traditional Snacks

Cost premiums for organic and natural formulations create market access barriers, particularly in price-sensitive demographics and developing markets where discretionary spending limits premium product adoption. USDA organic certification requirements increase production costs through specialized sourcing, processing segregation, and compliance documentation, while natural ingredient sourcing commands premium pricing compared to synthetic alternatives. Producer Price Index increases in snack food manufacturing compound cost pressures, with organic ingredients experiencing higher inflation rates than conventional alternatives. Manufacturing scale limitations for organic production prevent cost optimization achieved in conventional processing, maintaining structural cost disadvantages. Consumer price sensitivity varies by region and demographic, with premium positioning successful in affluent markets yet limiting penetration in price-conscious segments.

Segment Analysis

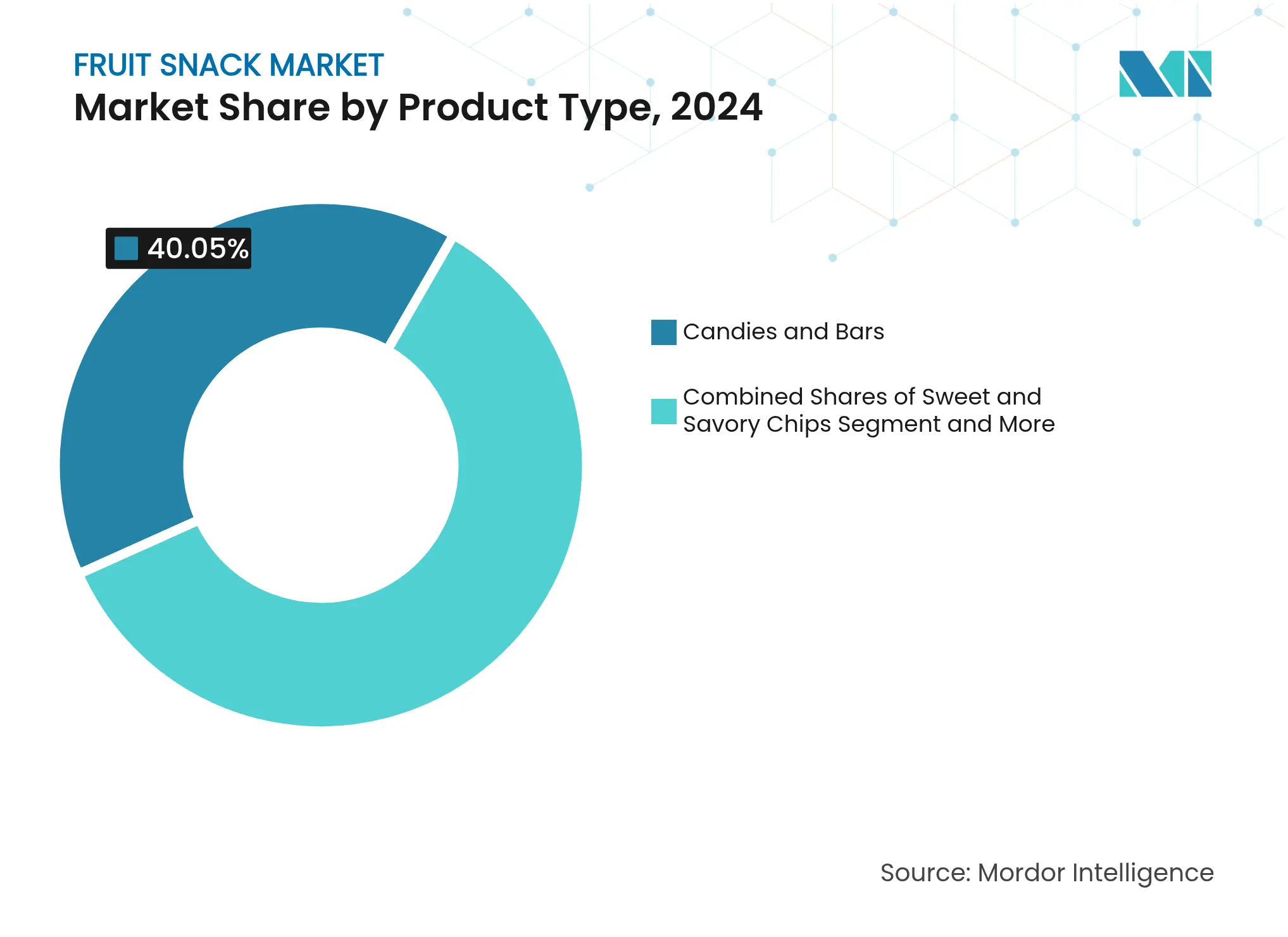

By Product Type: Candies Drive Volume While Chips Capture Innovation

Sweet and savory chips represent the fastest-growing product segment at 9.53% CAGR through 2030, despite candies and bars commanding 40.05% market share in 2024, reflecting consumer migration toward innovative textures and flavor profiles that differentiate from traditional confectionery. Chips format enables incorporation of vegetable-fruit blends and superfruit combinations that appeal to health-conscious consumers seeking nutritional density beyond conventional fruit snacks. Dairy-based products occupy specialized positioning for protein-enhanced formulations, while other fruit snacks including gummies, jellies, purees, and squeezable pouches address specific age demographics and consumption occasions. General Mills' expansion of Mott's fruit snacks into convenience store channels demonstrates format optimization for impulse purchasing, with 5-oz bags priced at USD 1.99 targeting on-the-go consumption.

Manufacturing complexity varies significantly across product types, with chips requiring specialized dehydration equipment and controlled moisture content, while candies and bars benefit from established confectionery production infrastructure. Regulatory compliance factors through FDA nutrition labeling requirements influence product formulation strategies, particularly for functional ingredient integration in premium segments. Squeezable pouches target younger demographics with convenience positioning yet face packaging cost pressures from specialized barrier films required for shelf stability. The integration of automation and quality control systems in manufacturing facilities has become essential to maintain consistent product quality and meet increasing production demands. Companies must also invest in research and development to optimize processing parameters and ensure product stability throughout the intended shelf life.

Note: Segment shares of all individual segments available upon report purchase

By Category: Organic Acceleration Despite Conventional Dominance

Conventional fruit snacks maintain 85.67% market share in 2024, yet organic variants accelerate at 10.55% CAGR through 2030, indicating premium positioning success despite production cost pressures from specialized sourcing and processing requirements. Organic certification through USDA standards creates competitive differentiation that justifies price premiums of 15-25% above conventional alternatives, particularly in developed markets where health consciousness correlates with purchasing power. Supply chain complexity increases significantly for organic production, requiring segregated processing facilities and documentation systems that prevent cross-contamination with conventional ingredients.

Consumer education becomes critical for organic segment expansion, as perceived health benefits must overcome cost resistance in price-sensitive demographics. Organic Trade Association standards provide industry framework for certification consistency, yet regulatory compliance costs create barriers for smaller manufacturers lacking scale economies. The category growth differential suggests market maturation opportunities for conventional products through functional ingredient integration, while organic positioning captures premium-willing consumers prioritizing natural formulations over cost considerations.

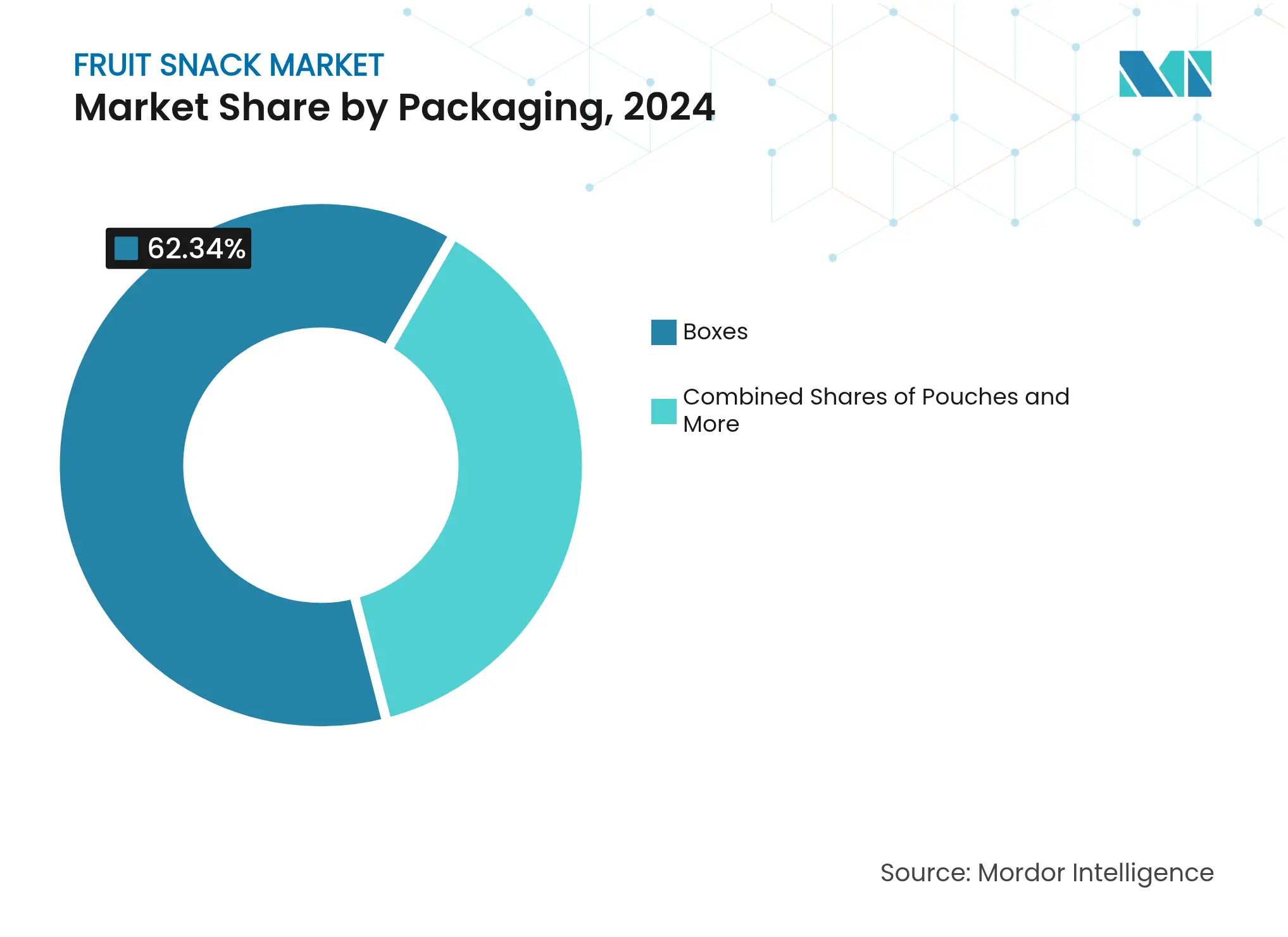

By Packaging: Pouches Gain Ground on Traditional Boxes

Innovation in packaging formats drives competitive differentiation, with pouches emerging as the fastest-growing segment at 8.74% CAGR through 2030, despite boxes maintaining 62.34% market share in 2024, reflecting consumer preference shifts toward portability and portion control. Pouch technology advances in barrier films and resealable closures address mobility requirements while maintaining product freshness, enabling on-the-go consumption that aligns with urbanization trends. Other packaging formats including sticks, sachets, and canisters serve specialized applications for different age demographics and consumption occasions.

Berlin Packaging analysis indicates Q2 2024 cost pressures in packaging materials, with specialized barrier films commanding premium pricing yet providing competitive advantages through extended shelf life and product protection. Sustainability considerations influence packaging material selection, with recyclable and biodegradable options gaining consumer preference despite cost increases. Manufacturing efficiency varies across packaging formats, with boxes benefiting from established production lines while pouches require specialized equipment investment for heat sealing and quality control.

By Distribution Channel: Digital Commerce Disrupts Traditional Retail

Supermarkets and hypermarkets command 55.82% market share in 2024, yet online retail stores accelerate at 9.03% CAGR through 2030, reflecting e-commerce penetration in food categories and changing consumer shopping behaviors. FMI research projects online grocery reaching 20.5% of total grocery sales by 2026, with shelf-stable products like fruit snacks well-positioned for digital fulfillment due to packaging durability and extended shelf life. Convenience and grocery stores maintain steady positioning for impulse purchasing, while other distribution channels including vending machines and institutional sales serve specialized applications.

Direct-to-consumer strategies through e-commerce enable brand relationship building and higher margins compared to traditional retail distribution, yet require investment in fulfillment infrastructure and digital marketing capabilities. Subscription model adoption for regular consumption products creates predictable revenue streams and customer lifetime value optimization. Mobile commerce growth enables impulse purchasing patterns that complement on-the-go consumption trends, particularly for premium and specialty products that benefit from detailed product information and consumer reviews.

Geography Analysis

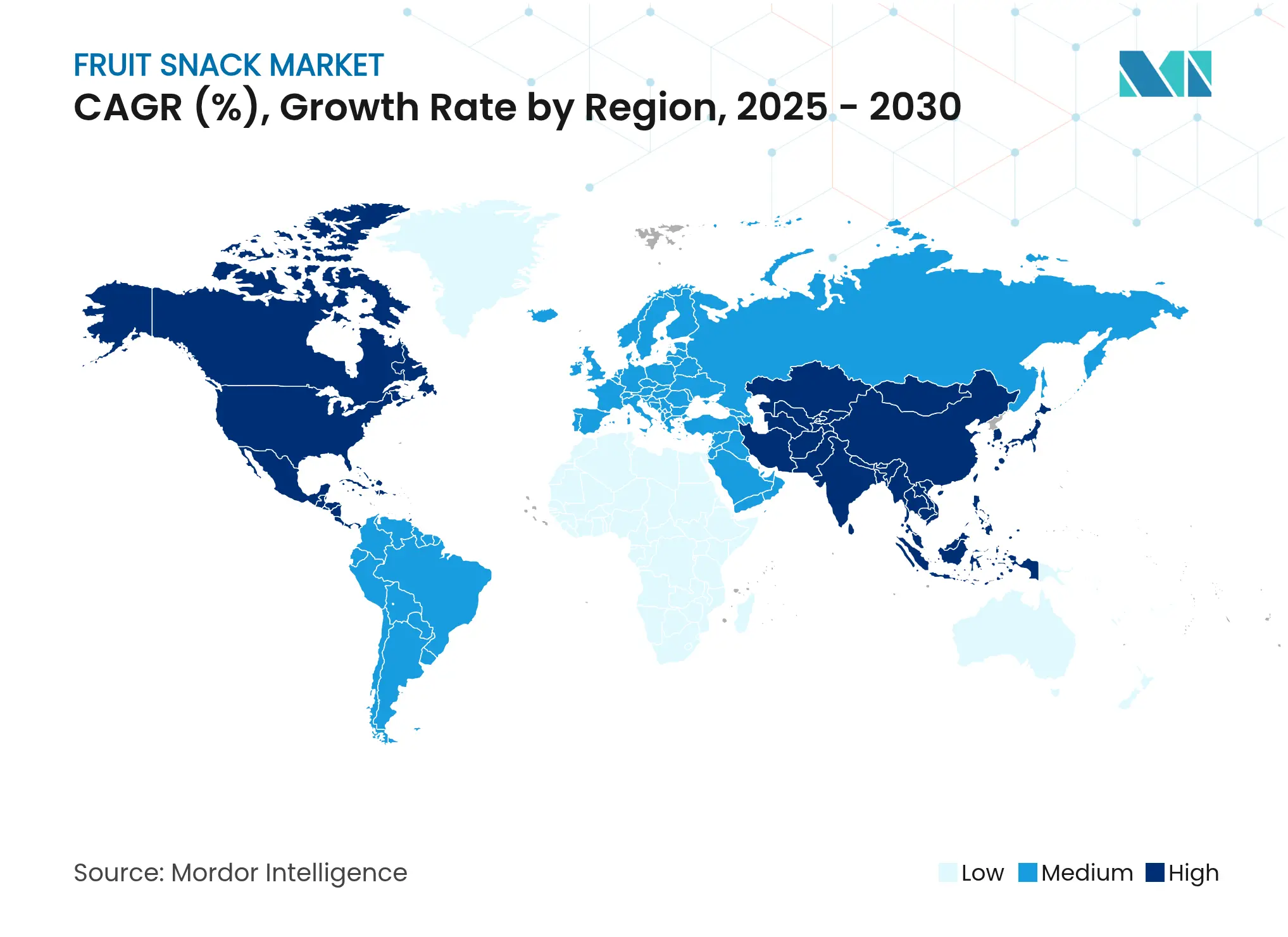

Asia-Pacific is projected to post a 9.32% CAGR through 2030, a pace set by rapid urbanization, growing middle-class purchasing power, and clearer rules on nutrient and sugar labeling that boost trust in packaged snacks. Chinese cold-chain upgrades now allow purée pouches and freeze-dried chips to travel long distances without quality loss, while cross-border e-commerce hubs introduce U.S. organic SKUs to digital shoppers. Southeast Asian processors are also receiving technical support programs that lower entry barriers for modern drying and packaging lines, widening local assortment and reinforcing the region’s demand pull.

North America kept its lead with 35.06% revenue share in 2024, thanks to deep supermarket penetration, high per-capita snack spending, and consumers who accept premium prices for added functionality. Growth is slower than in Asia-Pacific, yet value expansion continues as probiotic gummies, keto-aligned fruit-nut bars, and low-sugar chewy bites earn resets in wellness aisles. Retailers lean on loyalty-card data to refine planograms, pruning slower flavors while spotlighting organic or vitamin-fortified launches that sustain foot traffic.

Europe shows steady mid-single-digit expansion as sugar-reduction pledges and eco-design laws reshape new-product briefs. Private-label programs from major grocers accelerate penetration of recyclable pouches, while Mediterranean markets favor local fruit profiles such as peach or citrus blends. Latin America and the Middle East & Africa are at earlier stages; currency swings and tempered cold-chain reach limit immediate upside, but rising disposable incomes and modern trade construction lay groundwork for future acceleration once logistics hurdles ease.

Competitive Landscape

Market Concentration

The sector earns a medium concentration score, reflecting a fragmented field where global giants and agile challengers share shelf space. PepsiCo’s acquisition of BFY Brands widened its better-for-you roster and gave immediate access to established beverage distribution routes, while Mars spent USD 35.9 billion to secure Kellanova’s fruit-forward patents and international scale. General Mills keeps visibility high through licensed characters that pull family shoppers toward Mott’s gummies at convenience outlets.

Functional formulation is the core battleground. Brands use botanicals such as ashwagandha, plant-based fibers, and verified probiotics to move SKUs from treat status to daily wellness support. Investment flows into high-speed aeration lines, continuous moisture monitoring, and blockchain traceability that proves origin claims to regulators and retailers alike. Packaging partnerships yield multilayer pouches that hit recyclability targets without sacrificing oxygen barriers, letting marketers combine sustainability messaging with freshness guarantees.

Private-label programs add price tension yet also validate category demand, especially in Europe where vertically integrated retailers wield strong sourcing leverage. Mid-sized companies pursue joint ventures in Asia-Pacific to marry local flavor insight with Western quality cues, while direct-to-consumer start-ups exploit subscription models and social-commerce amplification to win niche followings. The resulting landscape rewards firms that can scale quickly, innovate on functionality, and navigate regional regulations without compromising speed to shelf.

Fruit Snack Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Wyman's, a frozen fruit brand, added three new products to its line of offerings. This was the company's fourth new product launch in four years. New products included Wyman's Protein Blends for smoothies, Wyman's Fruit First Waffles and Wyman's Fruit and Peanut Butter Poppers.

- August 2024: Hidden Fruits, recognized for its British raspberries coated in white and milk Belgian chocolate, adapted to the cocoa market shortages by introducing a new limited-edition product. The offering featured British blackberries, frozen and coated in a blend of white and ruby Belgian chocolate. This combination was designed to provide a balance of flavors.

- September 2023: Golden West Food Group entered a licensing partnership with The Hershey Co. to create a new line of chocolate-covered fruit products. The partnership aimed to capitalize on the mindful snacking trend, combining frozen fruits and Hershey brand candy coatings. Hershey's Frozen Fruit offerings launched in 8-oz varieties such as Reese's Frozen Fruit Banana Slices, Hershey's Cookies 'N' Creme Frozen Fruit Strawberries, Hershey's White Creme & Milk Chocolate Frozen Fruit Blueberries and Hershey's White Creme & Milk Chocolate Frozen Fruit Raspberries.

Table of Contents for Fruit Snack Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Consumer Demand For Healthier Snack Options

- 4.2.2Growth In Vegan, Gluten-Free, And Allergen-Free Fruit Snack Options

- 4.2.3Growing Trend Of On-The-Go And Convenient Snacking

- 4.2.4Innovation In Flavors, Product Formats, And Packaging

- 4.2.5Rising Awareness About Functional Benefits Like Added Vitamins, Fiber, Probiotics

- 4.2.6Expansion Of E-Commerce And Online Retail Sales Channels

- 4.3Market Restraints

- 4.3.1Competition From Alternative Healthy Snack Categories Such As Nuts And Seeds

- 4.3.2High Cost Of Organic And Natural Fruit Snacks Compared To Traditional Snacks

- 4.3.3Consumer Concerns Over Added Sugar Content In Some Fruit Snacks

- 4.3.4Consumer Skepticism About Processed Fruit Snack Nutritional Value

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Sweet and Savory Chips

- 5.1.2Candies and Bars

- 5.1.3Dairy-Based

- 5.1.4Other Fruit Snacks

- 5.2By Category

- 5.2.1Conventional

- 5.2.2Organic

- 5.3By Packaging

- 5.3.1Boxes

- 5.3.2Pouches

- 5.3.3Others

- 5.4By Distribution Channel

- 5.4.1Supermarkets/Hypermarkets

- 5.4.2Convenience Stores

- 5.4.3Online Retail Stores

- 5.4.4Other Distribution Channels

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.1.4Rest of North America

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3Italy

- 5.5.2.4France

- 5.5.2.5Spain

- 5.5.2.6Netherlands

- 5.5.2.7Poland

- 5.5.2.8Belgium

- 5.5.2.9Sweden

- 5.5.2.10Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4Australia

- 5.5.3.5Indonesia

- 5.5.3.6South Korea

- 5.5.3.7Thailand

- 5.5.3.8Singapore

- 5.5.3.9Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Colombia

- 5.5.4.4Chile

- 5.5.4.5Peru

- 5.5.4.6Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1South Africa

- 5.5.5.2Saudi Arabia

- 5.5.5.3United Arab Emirates

- 5.5.5.4Nigeria

- 5.5.5.5Egypt

- 5.5.5.6Morocco

- 5.5.5.7Turkey

- 5.5.5.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1RIND Snacks

- 6.4.2PIM Brands, Inc.

- 6.4.3General Mills Inc.

- 6.4.4Nestlé S.A.

- 6.4.5Beyond Better Foods, LLC

- 6.4.6Danone S.A.

- 6.4.7Dole Food Company, Inc.

- 6.4.8SunOpta Inc.

- 6.4.9Welch Foods Inc.

- 6.4.10Mott’s LLP

- 6.4.11Sunkist Growers, Inc.

- 6.4.12Bare Foods Co.

- 6.4.13Crisp Green, Inc.

- 6.4.14Brothers International Food Corporation

- 6.4.15Sensible Foods Inc.

- 6.4.16Mount Franklin Foods

- 6.4.17Nutty Goodness LLC

- 6.4.18That’s It Nutrition, LLC

- 6.4.19Tropicana Products, Inc.

- 6.4.20WhiteWave Services (Danone)

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Fruit Snack Market Report Scope

Fruit snacks are a type of snack made of different kinds of fruits or flavors. Fruit snacks are consumed and preferred by all age groups due to their unique taste and health benefits. The fruit snack market is segmented by product type into sweet and savory chips, candies and bars, dairy-based, and other fruit snacks, by distribution channel into supermarkets/hypermarkets, convenience stores, specialist retailers, online retailing, and other distribution channels, and by geography into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million)