Hair Serum Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

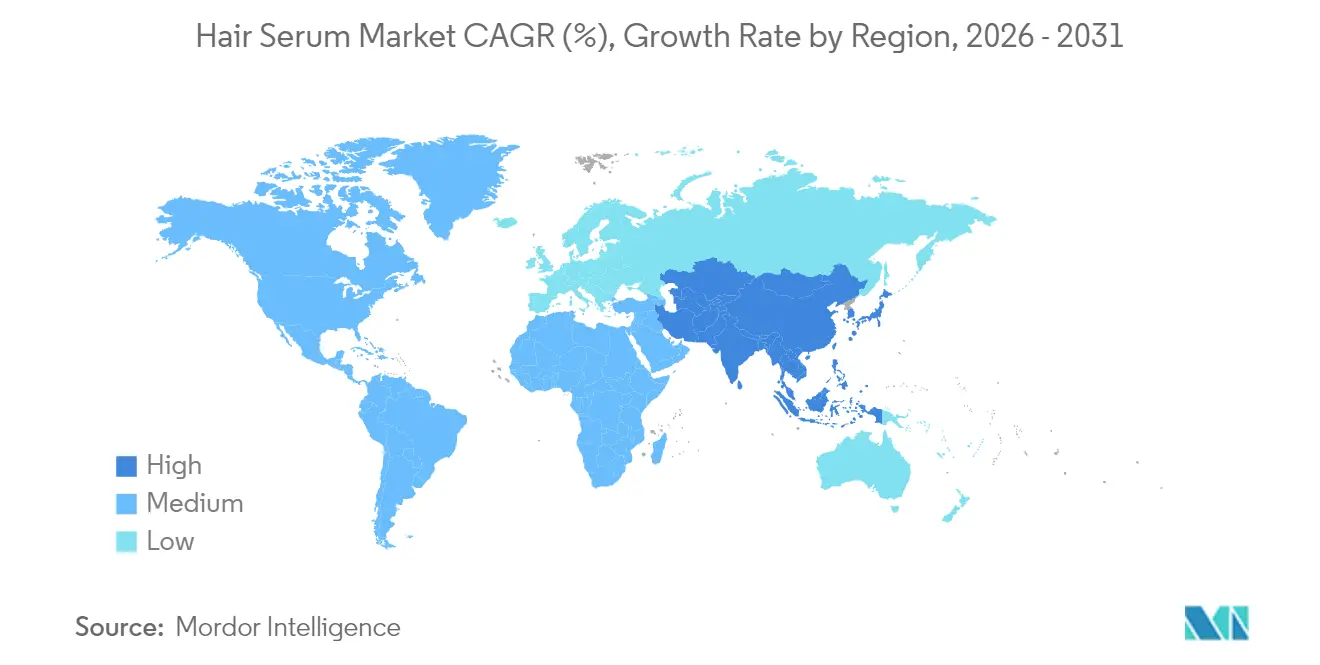

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

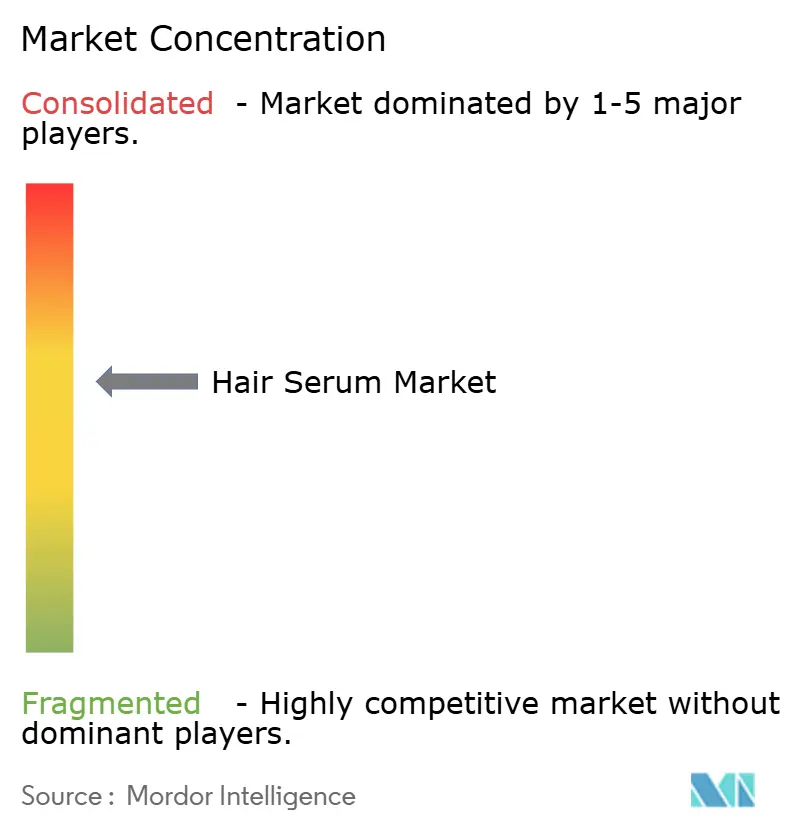

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hair Serum Market Analysis by Mordor Intelligence

The hair serum market size was valued at USD 1.36 billion in 2025 and estimated to grow from USD 1.43 billion in 2026 to reach USD 1.85 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). This growth highlights the market's shift from being primarily a styling product to a platform focused on scalp health. Factors such as increased urban pollution, exposure to hard water, and UV stress are influencing ingredient innovation, with research focusing on components like ectoin, moringa extract, and chelators to address mineral buildup. The rise of online social-commerce platforms is shortening the discovery-to-purchase process, enabling rapid scaling for independent brands. Additionally, professional salons are transforming into diagnostic centers, offering personalized serum recommendations based on trichoscopy and water-hardness analysis. Regulatory changes in the European Union and the United States are driving silicone-free reformulations and requiring brands to validate hair-growth claims through randomized trials. Efforts to combat counterfeit products on platforms like Amazon and Alibaba are enhancing brand protection, though challenges persist in emerging markets.

Key Report Takeaways

- By product type, treatment serums captured 65.94% of hair serum market share in 2025, while styling serums are trailing as treatment formats post a 6.41% CAGR through 2031.

- By ingredient type, conventional formulations held 73.31% of the hair serum market size in 2025, whereas organic variants are expanding at a 6.01% CAGR to 2031.

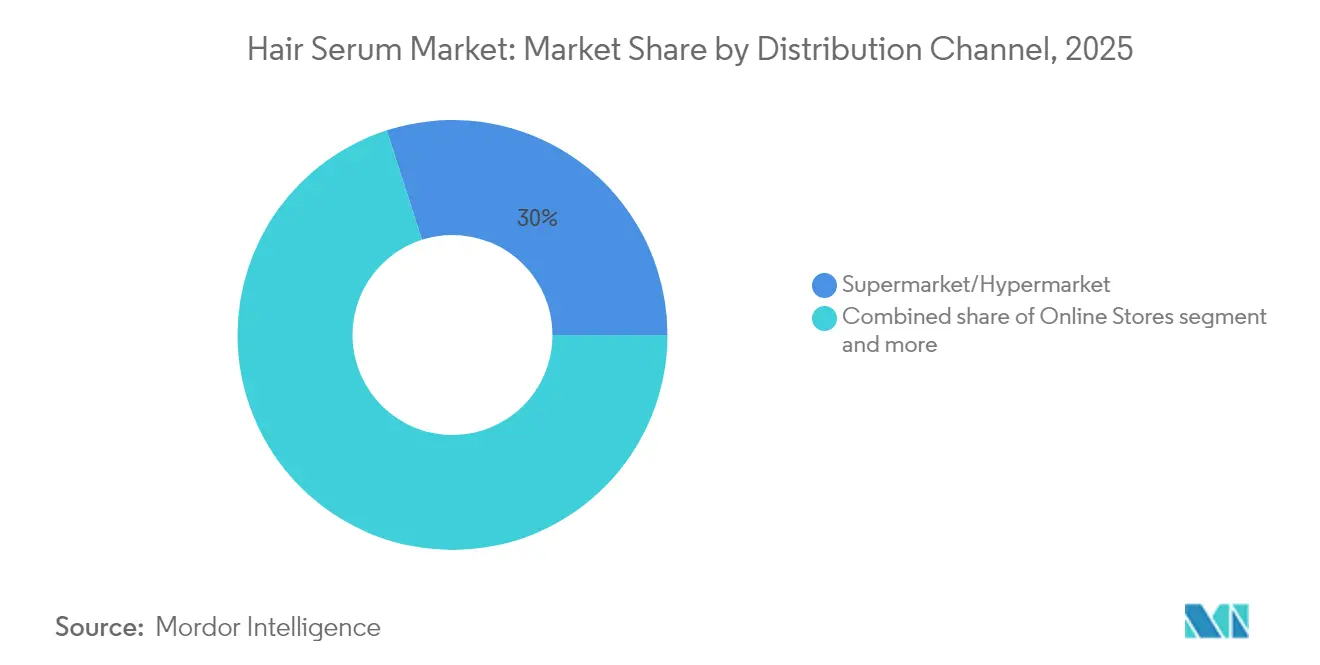

- By distribution channel, supermarkets and hypermarkets accounted for 29.95% revenue share of the hair serum market in 2025, but online stores are advancing at a 6.08% CAGR through 2031.

- By geography, Asia-Pacific commanded 38.45% of global hair serum market share in 2025 and is forecast to grow at a 5.86% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Serum Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of hair damage from pollution, UV, hard water, and environmental stressors | +1.2% | Global, with acute impact in Asia-Pacific (Delhi, Beijing, Jakarta) and urban North America | Medium term (2-4 years) |

| Growing demand for scalp-focused serums targeting microbiome balance, dandruff, sensitivity, and follicle health | +1.5% | North America, Europe, Asia-Pacific core markets (South Korea, Japan) | Long term (≥ 4 years) |

| Expansion of professional salon and spa channel | +0.9% | North America, Europe, with spillover to premium urban centers in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Rapid product innovation and line extensions | +0.8% | Global, led by North America and Europe research and development hubs | Short term (≤ 2 years) |

| Shift toward advanced, functional ingredients | +1.0% | North America, Europe, with adoption lag in South America and Middle East and Africa | Medium term (2-4 years) |

| Growing focus on holistic self-care and at-home beauty rituals | +0.7% | Global, accelerated by post-pandemic behavior shifts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Hair Damage from Pollution, UV, Hard Water, and Environmental Stressors

Urban air quality deterioration is significantly influencing hair-care priorities, as particulate matter becomes embedded in the scalp's lipid matrix, initiating inflammatory responses that compromise the strength of follicle anchors. Major urban centers, including Delhi and Beijing, experience particulate matter (PM2.5) levels far above the thresholds recommended by the World Health Organization (WHO) [1]Source: World Health Organization, “WHO Global Air Quality Guidelines,” who.int. This has led to a noticeable rise in consumer demand for anti-pollution serums formulated with ingredients such as moringa peptides and ectoin, which are known to neutralize free radicals before they can oxidize keratin disulfide bonds. Additionally, hard water, which contains high levels of calcium and magnesium, deposits mineral scale on hair shafts, leading to reduced elasticity and increased susceptibility to breakage. Chelating serums incorporating ethylenediaminetetraacetic acid (EDTA) or phytic acid are becoming increasingly popular in areas where water is supplied from limestone aquifers, such as certain regions in the United States and Southern Europe [2]Source: U.S. Geological Survey, “Hardness of Water,” usgs.gov. Furthermore, ultraviolet (UV) radiation, particularly UVA wavelengths that penetrate deep into the hair cortex, causes degradation of melanin and structural proteins. Serums enriched with UV filters like ethylhexyl methoxycinnamate or natural alternatives such as red algae extract are being positioned as essential leave-in photoprotection solutions. The combined effects of these environmental stressors have transformed serums from optional styling products into critical barrier-defense solutions, encouraging brands such as Moroccanoil and Living Proof to reformulate their existing product lines to include advanced anti-pollution complexes.

Growing Demand for Scalp-Focused Serums Targeting Microbiome Balance, Dandruff, Sensitivity, and Follicle Health

The scalp microbiome, consisting of species such as Cutibacterium, Staphylococcus, and Malassezia, has become a focus for therapeutic interventions, as its imbalance is associated with conditions like seborrheic dermatitis, folliculitis, and telogen effluvium. Serums containing postbiotics, such as lactobacillus ferment, and prebiotics, like inulin, are being used to regulate microbial populations while preserving commensal flora. These formulations provide a gentler alternative to traditional treatments like zinc pyrithione or ketoconazole. Brands such as Briogeo and Virtue Labs have introduced scalp serums featuring ingredients like Centella asiatica (CICA), which reduces pro-inflammatory cytokines, and niacinamide, which enhances the epidermal barrier and minimizes transepidermal water loss. Additionally, follicle-health products now incorporate biomimetic peptides, such as Capixyl—a combination of biochanin A and acetyl tetrapeptide-3—that inhibit 5-alpha reductase and extend the anagen phase, offering a solution for androgenetic alopecia without the systemic side effects associated with finasteride. The industry is shifting from symptom management to addressing root causes, gaining support from dermatologists and driving investments in clinical trials. For example, several brands are pursuing Food and Drug Administration (FDA) over-the-counter monograph pathways for hair-growth claims, which require randomized controlled trials to demonstrate statistically significant improvements in hair density [3]Source: United States Food & Drug Administration, “Is It a Cosmetic, a Drug, or Both? (Or Is It Soap?),” fda.gov. This trend is expected to drive growth over the long term, supported by the adoption of personalized scalp diagnostics, such as trichoscopy and sebum pH testing, in premium salons across North America, Europe, and developed Asia-Pacific markets.

Expansion of Professional Salon and Spa Channel

Professional channels are shifting from being purely transactional retail points to becoming experiential consultation hubs. Stylists now use diagnostic tools, such as digital scalp cameras and moisture analyzers, to recommend serums tailored to individual factors like hair porosity, sebum levels, and water hardness. Salon-exclusive brands, including Redken, Pureology, and Olaplex, maintain their premium pricing by combining in-salon treatments with take-home serums, fostering recurring revenue and strengthening brand loyalty. The collaboration between Glamsquad and Olaplex highlights how brands are extending salon services into consumers' homes, addressing needs that physical salon locations cannot fulfill. Stylists are increasingly incentivized through commission-based structures tied to product sales, encouraging them to educate clients on serum layering techniques and ingredient compatibility. Training academies operated by Wella, L'Oréal Professional, and Schwarzkopf are integrating serum application methods into their certification programs, positioning serums as essential service offerings rather than supplementary retail products. This expansion of professional channels is expected to drive growth, with the medium-term impact primarily concentrated in North America and Europe, where salon density and per-visit spending are highest, and gradual growth anticipated in premium urban areas across Asia-Pacific and the Middle East.

Shift Toward Advanced, Functional Ingredients

Formulators are shifting from traditional silicones and mineral oils to bioengineered actives that provide clear performance benefits, such as bond repair, cuticle sealing, and follicle energization. Peptides like acetyl tetrapeptide-3 and copper tripeptide-1 are designed to penetrate the hair cortex, promoting keratinocyte proliferation and collagen synthesis. Furthermore, plant stem cells derived from edelweiss and sea fennel offer antioxidant protection and support cellular regeneration. Adaptogens, including ashwagandha, rhodiola, and holy basil, are being integrated to address cortisol-induced hair thinning, focusing on the psychodermatological aspects of hair loss. Nano-encapsulation technologies are enabling hydrophobic actives, such as retinol and tocopherol, to remain stable in aqueous serums, overcoming previous formulation challenges that limited ingredient diversity. Exosome-based serums, which deliver micro ribonucleic acid (microRNA) and growth factors derived from plant or stem-cell cultures, represent an emerging area in regenerative hair care. However, regulatory uncertainty regarding their classification as either cosmetic or biologic products remains unresolved. The Ordinary's introduction of multi-peptide hair serums at accessible price points is increasing consumer access to functional ingredients, compelling legacy brands to justify premium pricing through clinical validation. This trend is expected to drive growth in the medium term as ingredient costs decrease and regulatory frameworks stabilize in North America and Europe, followed by adoption in the Asia-Pacific region and gradual market penetration in South America and the Middle East.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent cosmetic regulations on ingredient safety | -0.6% | Europe (EU Cosmetics Regulation), North America (FDA), Asia-Pacific (ASEAN Cosmetic Directive) | Medium term (2-4 years) |

| Ongoing safety concerns around certain silicones, preservatives, and synthetic actives | -0.4% | Global, with heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| High complexity and cost of formulating stable, multifunctional serums with natural actives | -0.3% | Global, with acute impact on indie brands and emerging market players | Long term (≥ 4 years) |

| Widespread presence of counterfeit and grey-market serums online | -0.5% | Global, with acute impact in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Cosmetic Regulations on Ingredient Safety

Regulatory agencies are increasing oversight of cosmetic claims and ingredient safety, requiring brands to perform comprehensive toxicological assessments and clinical trials before product launch. The European Union's ongoing updates to the Cosmetics Regulation are expanding the list of restricted substances and mandating safety evaluations for nanomaterials, which are increasingly utilized in serums to enhance penetration. In the United States, the Food and Drug Administration has issued warning letters to brands making unsupported hair-growth claims, demanding randomized controlled trials that adhere to pharmaceutical-grade standards—a requirement that smaller brands often find challenging without venture capital support. The Association of Southeast Asian Nations' harmonized Cosmetic Directive seeks to simplify ingredient approvals across member states; however, varying implementation timelines create compliance challenges for multinational product launches. Environmental concerns regarding certain silicones, such as cyclopentasiloxane and cyclohexasiloxane, classified by the European Union as substances of very high concern due to their environmental persistence, are driving reformulations toward plant-based alternatives like hemisqualane and caprylic/capric triglyceride. These alternatives, however, often underperform in sensory attributes and require more expensive stabilization. Additionally, preservative systems are under scrutiny, with phenoxyethanol and parabens being replaced by multifunctional ingredients such as caprylyl glycol and ethylhexylglycerin. While these alternatives provide antimicrobial efficacy, they also narrow the formulation window.

Ongoing Safety Concerns Around Certain Silicones, Preservatives, and Synthetic Actives

Consumer advocacy groups and environmental organizations continue to question the safety of commonly used serum ingredients, creating reputational challenges for brands and prompting reformulations, even in the absence of regulatory restrictions. Silicones, such as dimethicone and cyclopentasiloxane, are criticized for their environmental persistence and potential to bioaccumulate in aquatic ecosystems, despite their effectiveness in providing slip, shine, and heat protection. The Environmental Working Group's Skin Deep database assigns hazard scores to cosmetic ingredients based on toxicity studies. High scores, even when derived from precautionary principles rather than conclusive evidence, can lead to consumer boycotts and retailer delistings. Preservatives like methylisothiazolinone and formaldehyde-releasing agents have been associated with contact dermatitis in sensitive individuals. As a result, brands are increasingly adopting preservative-free formulations or natural antimicrobial alternatives, such as radish root ferment and honeysuckle extract. However, these alternatives often reduce shelf life and necessitate cold-chain logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Treatment Serums Anchor Growth

Hair treatment serums accounted for 65.94% of market revenue in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 6.41% through 2031. This growth is expected to outpace that of styling serums, as consumer preferences increasingly shift toward addressing hair health concerns such as bond repair, keratin reconstruction, and scalp fortification, rather than focusing solely on achieving a cosmetic finish. These treatment formulations are designed to tackle structural damage at the molecular level by leveraging advanced ingredients such as biomimetic peptides, plant stem cells, and postbiotics. These components work to repair disulfide bonds that are often fractured due to chemical processing, heat styling, and environmental oxidation. A notable example is Olaplex's bis-aminopropyl diglycol dimaleate technology, which has set a benchmark in the market by effectively reconnecting broken keratin chains. Competitors are striving to replicate or innovate beyond this standard by utilizing alternative crosslinking agents, including maleic acid derivatives and polyquaternium complexes, to deliver comparable or enhanced results.

Scalp-treatment serums are also gaining traction, particularly those targeting issues such as follicle miniaturization and seborrheic dermatitis. These products are increasingly incorporating 5-alpha reductase inhibitors, such as saw palmetto and pumpkin seed extract, as well as anti-inflammatory botanicals like Centella Asiatica (CICA) and licorice root. These ingredients are formulated to regulate the hair growth cycle, reduce shedding, and address underlying scalp conditions. This growing demand reflects a broader consumer trend of reframing hair care as a form of preventive dermatology. Treatment serums are now being positioned as daily-use interventions that support long-term hair and scalp health, rather than being viewed as occasional remedies for specific issues.

By Ingredient Type: Organic Gains Momentum

Conventional formulations accounted for 73.31% of the market share in 2025, primarily due to their affordability, reliable sensory performance, and stable formulation characteristics. These attributes make them a preferred choice for a wide range of consumers. However, organic variants are steadily closing the gap, growing at a compound annual growth rate (CAGR) of 6.01%. This growth is fueled by the rising influence of clean-beauty mandates and increasing consumer demand for ingredient transparency. Organic serums, certified by recognized organizations such as the United States Department of Agriculture (USDA) Organic, COSMOS (Cosmetic Organic and Natural Standard), or Ecocert, avoid synthetic preservatives, silicones, and petrochemical-derived emollients. Instead, they incorporate natural ingredients such as cold-pressed oils (e.g., argan, marula, rosehip), plant extracts (e.g., aloe, chamomile, green tea), and natural emulsifiers (e.g., lecithin, xanthan gum). These formulations resonate with environmentally conscious consumers who value sustainability, biodegradability, and minimal environmental impact. This trend is particularly evident in North America and Europe, where clean-beauty retail standards—such as Sephora's Clean at Sephora and Credo Beauty's Dirty List—prohibit the use of numerous ingredients considered harmful or ethically questionable.

Despite their growing popularity, organic serums face several formulation challenges. These include a shorter shelf life due to the absence of synthetic preservatives, a higher susceptibility to oxidation and rancidity, and variability in active ingredient concentrations caused by inconsistencies in agricultural sourcing. To address these challenges, brands are adopting innovative solutions such as airless packaging, nitrogen flushing, and the incorporation of natural antioxidant systems (e.g., tocopherol, rosemary extract). These measures help extend product stability while ensuring compliance with organic certification standards. By leveraging these advancements, brands aim to meet consumer expectations for high-quality organic products without compromising on performance or sustainability.

By Distribution Channel: Online Surges Ahead

In 2025, supermarkets and hypermarkets accounted for 29.95% of market revenue, highlighting the widespread presence of the grocery channel and the influence of impulse purchases. However, online stores are growing at a CAGR of 6.08%, driven by the integration of social commerce, influencer-led product discovery, and subscription models that transform one-time buyers into repeat customers. E-commerce platforms such as Amazon, Sephora.com, and Ulta.com utilize algorithmic recommendations, user-generated reviews, and virtual try-on tools to minimize purchase barriers. These platforms also allow consumers to review ingredient lists and clinical claims before making a purchase decision.

Social commerce platforms, including TikTok Shop, Instagram Shopping, and YouTube Shopping, streamline the process from product discovery to checkout. Influencers play a key role by demonstrating product applications, such as serum usage, in real time and embedding purchase links directly within video content. Subscription services like Ipsy, Birchbox, and FabFitFun introduce consumers to premium serums through discounted trial sizes, encouraging full-price purchases after users experience the products' effectiveness. Additionally, direct-to-consumer brands such as Divi, Briogeo, and Virtue Labs bypass traditional retail channels by leveraging their own websites and social media platforms. This approach helps them build brand communities and collect first-party data for personalized marketing strategies.

Geography Analysis

Asia-Pacific led the global market in 2025, holding a 38.45% share, and is expected to grow at a steady rate of 5.86% through 2031. This growth is driven by South Korea's advancements in scalp health, including trichoscopy clinics, pH-balancing serums, and CICA (Centella Asiatica)-infused treatments. Brands like Amorepacific's mise-en-scène and LG Household & Health Care have introduced innovative products such as cushion applicators and fermented botanicals to improve active ingredient absorption. Japan's minimalist approach, featuring lightweight serums with tsubaki (camellia) oil, rice water, and yuzu extract, appeals to consumers prioritizing ingredient purity and multifunctionality. Meanwhile, China's cross-border e-commerce platforms, such as Tmall and Douyin, enable international brands to bypass traditional import barriers, while local players like Proya and Chando gain traction by tailoring products to regional water hardness and humidity. In India, urban consumers are adopting Western-style treatment serums, while rural and semi-urban segments prefer Ayurvedic brands like Forest Essentials and Kama Ayurveda, which incorporate traditional ingredients such as bhringraj, amla, and brahmi oils.

North America and Europe represent significant market shares, with North America focusing on clinical efficacy and clean-beauty certifications. United States. consumers prefer serums backed by clinical trial data and dermatologist endorsements, favoring brands like Olaplex, Living Proof, and Virtue Labs, which publish peer-reviewed studies or white papers validating their claims. The professional salon channel remains robust, with stylists recommending serums based on individual hair porosity, chemical damage, and styling habits. In Europe, sustainability and regulatory compliance are key drivers. Consumers prioritize eco-certifications such as COSMOS (COSMetic Organic Standard), Ecocert, and Natrue, along with biodegradable packaging. This has increased demand for refillable serum bottles and waterless formulations that reduce carbon footprints. The EU's Cosmetics Regulation modernization is pushing brands to reformulate with plant-based alternatives, meeting stringent safety and environmental standards. Specialty retailers like Sephora and Douglas dominate distribution in both regions, offering curated assortments and in-store consultations that justify premium pricing. However, North America's growth is tempered by market saturation and competition, while Europe's trajectory is shaped by regulatory challenges and a shift toward circular economy models emphasizing product longevity and recyclability.South America, the Middle East, and Africa present emerging opportunities. Brazil leads South American demand with its vibrant beauty culture and preference for keratin-based treatments. In the Middle East, the UAE and Saudi Arabia drive growth through luxury retail channels and expatriate populations seeking international brands. In Africa, Nigeria and South Africa anchor the market, with local brands incorporating indigenous botanicals such as shea butter, baobab oil, and marula oil, which resonate with consumers seeking culturally relevant formulations. Despite challenges like inconsistent cold-chain logistics, limited e-commerce penetration, and currency volatility, these regions offer untapped potential as urbanization accelerates and beauty retail modernizes. Brands entering these markets must balance global brand equity with localized formulations tailored to regional hair types, climate conditions, and ingredient preferences. Collaborating with local distributors who have market knowledge and regulatory expertise is often critical for success in these regions.

Competitive Landscape

The hair serum market is moderately concentrated, with competition driven by multinational corporations such as L'Oréal, Unilever, Procter & Gamble, Henkel, and Kao. These companies rely on their broad product portfolios, research and development capabilities, and partnerships with salons to maintain their market positions. However, they face growing challenges from direct-to-consumer brands and independent companies that leverage digital platforms and influencer networks to bypass traditional retail channels.

Leading companies adopt multi-brand strategies to cater to different price points, distribution channels, and consumer needs. For instance, L'Oréal operates Kérastase in premium salons, Redken in professional channels, and Elvive in mass retail, each offering unique serum lines targeting specific concerns like bond repair, scalp health, or styling. Patent protections around bond-building technologies, such as Olaplex's bis-aminopropyl diglycol dimaleate and Unilever's maleic acid derivatives, provide a temporary competitive edge. However, the expiration of key patents and the availability of alternative crosslinking agents are reducing exclusivity in the market.

Opportunities for growth include personalized diagnostics, such as artificial intelligence (AI)-powered scalp analysis and at-home microbiome testing. Hybrid product formats are also gaining popularity, combining the benefits of serums with styling convenience. Examples include heat-activated bond-repair serums and overnight scalp treatments that double as leave-in conditioners. Additionally, technological advancements like augmented reality (AR) for virtual consultations, blockchain for product authentication, and nano-encapsulation to stabilize active ingredients are reshaping the market. Meanwhile, biotech innovations, such as lab-grown peptides and fermentation-derived postbiotics, are addressing sustainability concerns while offering enhanced performance compared to traditional plant-based extracts.

Hair Serum Industry Leaders

L'Oréal S.A

Unilever PLC

The Procter & Gamble Company

Henkel AG & Co KGaA

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Mallia Aesthetics introduced the 8T3 Essentials Hair Serum, incorporating MAL-838, a hormone-free sCD83 protein derivative designed to stimulate hair growth. This scientifically developed product targets androgenetic alopecia through localized immunomodulatory action, marking a notable development in the competitive global hair serum market.

- October 2025: Obagi Medical, a Walden Cast portfolio company, introduced Nu-Cilr BioStim Scalp Serum, a clinically formulated biotech treatment targeting scalp health and hair growth. The launch strengthens Obagi's presence in the premium therapeutic hair care segment, addressing professional dermatology and medical aesthetics channels globally.

- February 2024: Kérastase unveiled its Première collection, introducing advanced haircare solutions addressing damage and aging. The range features targeted treatments and serums designed to restore hair vitality and enhance resilience. This premium offering strengthens Kérastase's position in the professional and luxury hair serum market globally.

Global Hair Serum Market Report Scope

Hair serum is a hair care product that adds a protective layer to the scalp and helps in the nourishment of hair, generally used post hair coloring and bleaching. The global hair serum market is segmented by product type, distribution channel, and geography. By product type, the market is segmented into hair styling serum and hair treatment serum. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores, online stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Hair Treatment Serum |

| Hair Styling Serum |

| Conventional |

| Organic |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Chile | |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hair Treatment Serum | |

| Hair Styling Serum | ||

| By Ingredient Type | Conventional | |

| Organic | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the hair serum market in 2026?

The hair serum market size is USD 1.43 billion in 2026 and is projected to reach USD 1.85 billion by 2031.

Which product category is growing fastest?

Treatment serums are advancing at a 6.41% CAGR and already account for two-thirds of global revenue.

Which region leads demand?

Asia-Pacific holds 38.45% share and is forecast to grow at a 5.86% CAGR, led by K-beauty influence and China’s premiumization.

What is driving online channel growth?

Social-commerce platforms, influencer tutorials, and subscription models are helping online sales expand at 6.08% CAGR.

Page last updated on: